Columbus McKinnon (CMCO)

Columbus McKinnon faces an uphill battle. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Columbus McKinnon Will Underperform

With 19 different brands across the globe, Columbus McKinnon (NASDAQ:CMCO) offers material handling equipment for the construction, manufacturing, and transportation industries.

- Sales over the last two years were less profitable as its earnings per share fell by 10.5% annually while its revenue was flat

- Sales were flat over the last two years, indicating it’s failed to expand this cycle

- Low returns on capital reflect management’s struggle to allocate funds effectively, and its decreasing returns suggest its historical profit centers are aging

Columbus McKinnon’s quality isn’t up to par. There are better opportunities in the market.

Why There Are Better Opportunities Than Columbus McKinnon

Columbus McKinnon is trading at $14.67 per share, or 9.1x forward P/E. This certainly seems like a cheap stock, but we think there are valid reasons why it trades this way.

Our advice is to pay up for elite businesses whose advantages are tailwinds to earnings growth. Don’t get sucked into lower-quality businesses just because they seem like bargains. These mediocre businesses often never achieve a higher multiple as hoped, a phenomenon known as a “value trap”.

3. Columbus McKinnon (CMCO) Research Report: Q4 CY2025 Update

Material handling equipment manufacturer Columbus McKinnon (NASDAQ:CMCO) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 10.5% year on year to $258.7 million. Its non-GAAP profit of $0.62 per share was 6.6% above analysts’ consensus estimates.

Columbus McKinnon (CMCO) Q4 CY2025 Highlights:

- Revenue: $258.7 million vs analyst estimates of $245.7 million (10.5% year-on-year growth, 5.3% beat)

- Adjusted EPS: $0.62 vs analyst estimates of $0.58 (6.6% beat)

- Adjusted EBITDA: $39.8 million vs analyst estimates of $36.1 million (15.4% margin, 10.3% beat)

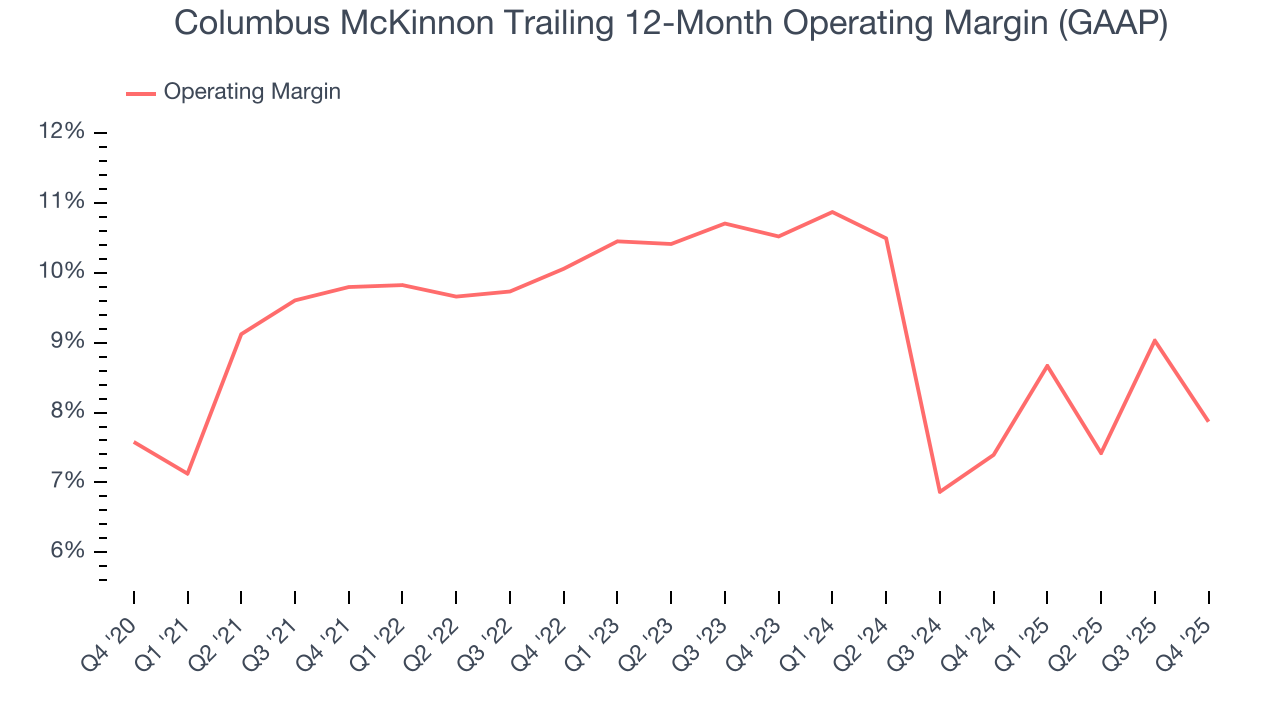

- Operating Margin: 6.3%, down from 10.9% in the same quarter last year

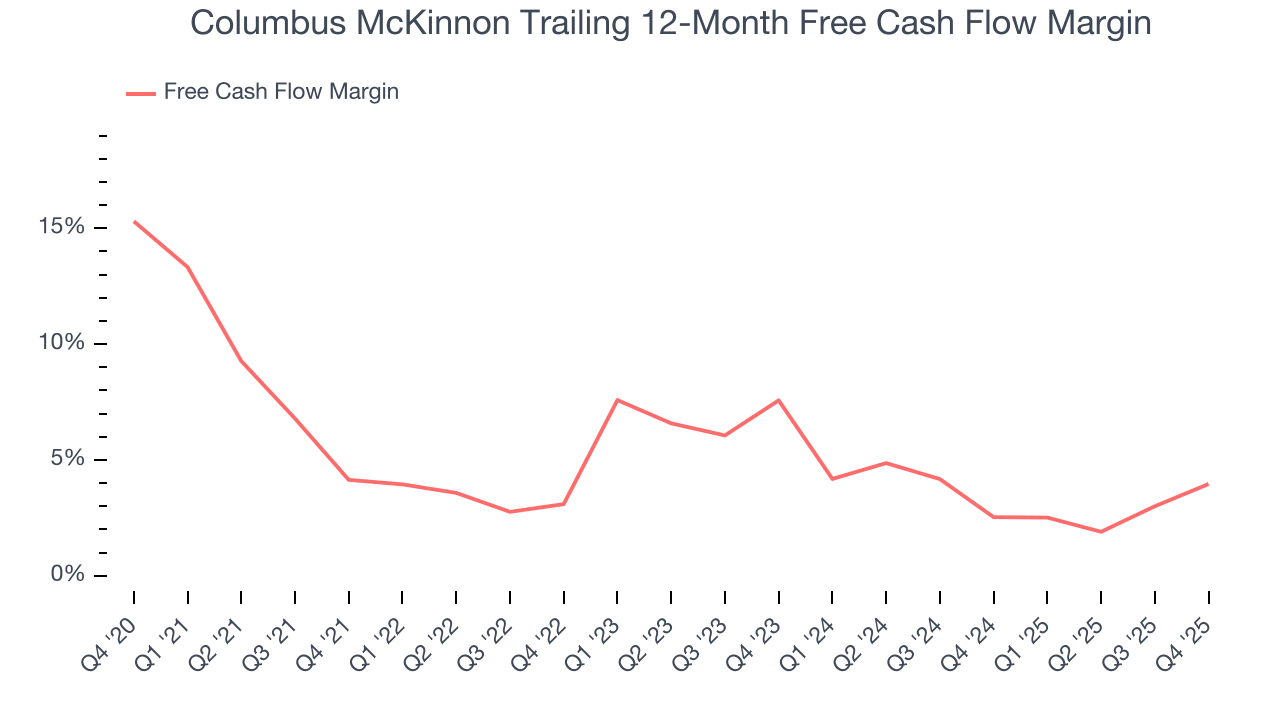

- Free Cash Flow Margin: 6.4%, up from 2.6% in the same quarter last year

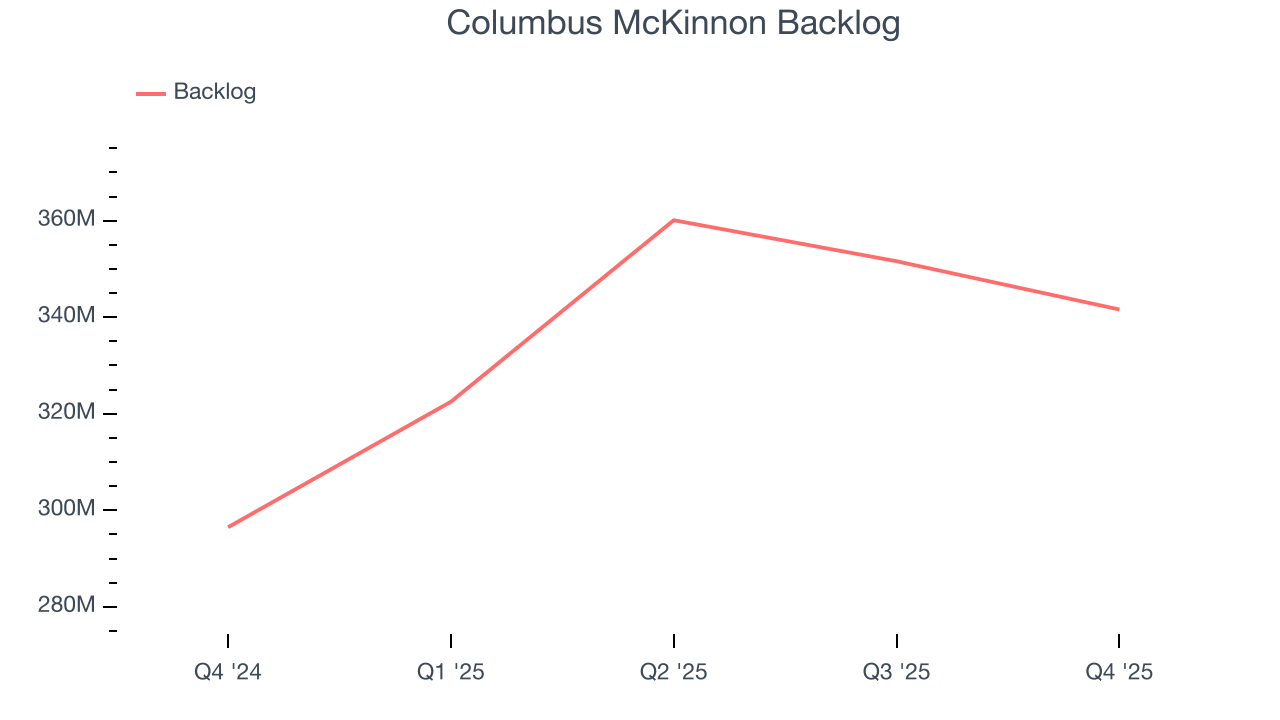

- Backlog: $341.6 million at quarter end, up 15.2% year on year

- Market Capitalization: $646.5 million

Company Overview

With 19 different brands across the globe, Columbus McKinnon (NASDAQ:CMCO) offers material handling equipment for the construction, manufacturing, and transportation industries.

Columbus McKinnon began as two separate entities focused on chain manufacturing and hoist production. The company's roots trace back to the Moore Manufacturing Company, which initially catered to the railroad industry before shifting focus to hoists and cranes. In 1929, the merger with the Columbus Chain Company formed Columbus McKinnon, expanding their product line in material handling. Over the decades, Columbus McKinnon has grown through strategic acquisitions, enhancing its presence in the hoist and chain market sectors.

Columbus McKinnon’s product range includes hoists of various types—electric, air-powered, lever, and hand-operated—along with crane components, precision conveyor systems, rigging tools, and digital power and motion control systems. These offerings cater to lifting, positioning, and securing needs in sectors such as manufacturing, transportation, energy, construction, and more. Additional specialized products include explosion-protected hoists, winches, aluminum workstations, and below-the-hook lifters. The company’s STAHL subsidiary extends its reach in crane construction and engineering procurement services, serving industries like wind power, warehousing, oil and gas, and transportation.

Columbus McKinnon Corporation's revenue primarily comes from the sale of its material handling products. The company markets its products through a global distribution network. This includes industrial and rigging shop distributors, independent crane builders, and national or regional distributors specializing in maintenance, repair, operating, and production (MROP) supplies. The company also collaborates with material handling specialists and integrators to design and assemble handling systems.

The company enhances its revenue streams with an after-sales service network, which includes chain repair service stations and hoist service and repair stations. This network supports the large installed base of Columbus McKinnon equipment by providing maintenance and repair services, ensuring operational efficiency and longevity of the products. Additionally, Columbus McKinnon offers specialized services to government agencies, such as the U.S. and Canadian Navies and Coast Guards, further diversifying its end markets.

Columbus McKinnon's growth strategy is centered on enhancing its intelligent motion product portfolio through strategic acquisitions and the development of new products that address customer challenges. Recently the company successfully integrated acquisitions such as Dorner and Garvey, which have broadened its capabilities in precision conveying and automation, providing entry into sectors like industrial automation, food processing and e-commerce.

4. General Industrial Machinery

Automation that increases efficiency and connected equipment that collects analyzable data have been trending, creating new demand for general industrial machinery companies. Those who innovate and create digitized solutions can spur sales and speed up replacement cycles, but all general industrial machinery companies are still at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

Competitors offering similar products include Terex (NYSE:TEX), Manitowoc (NYSE:MTW), and Hyster-Yale (NYSE:HY)

5. Revenue Growth

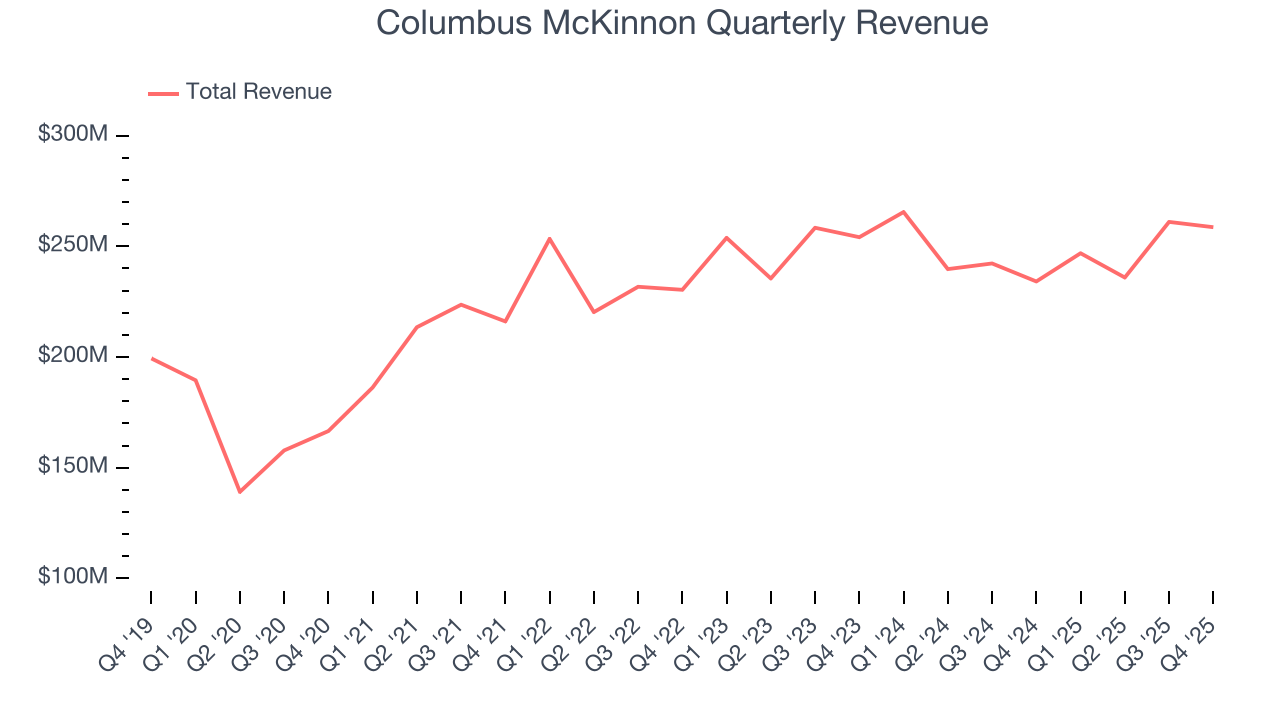

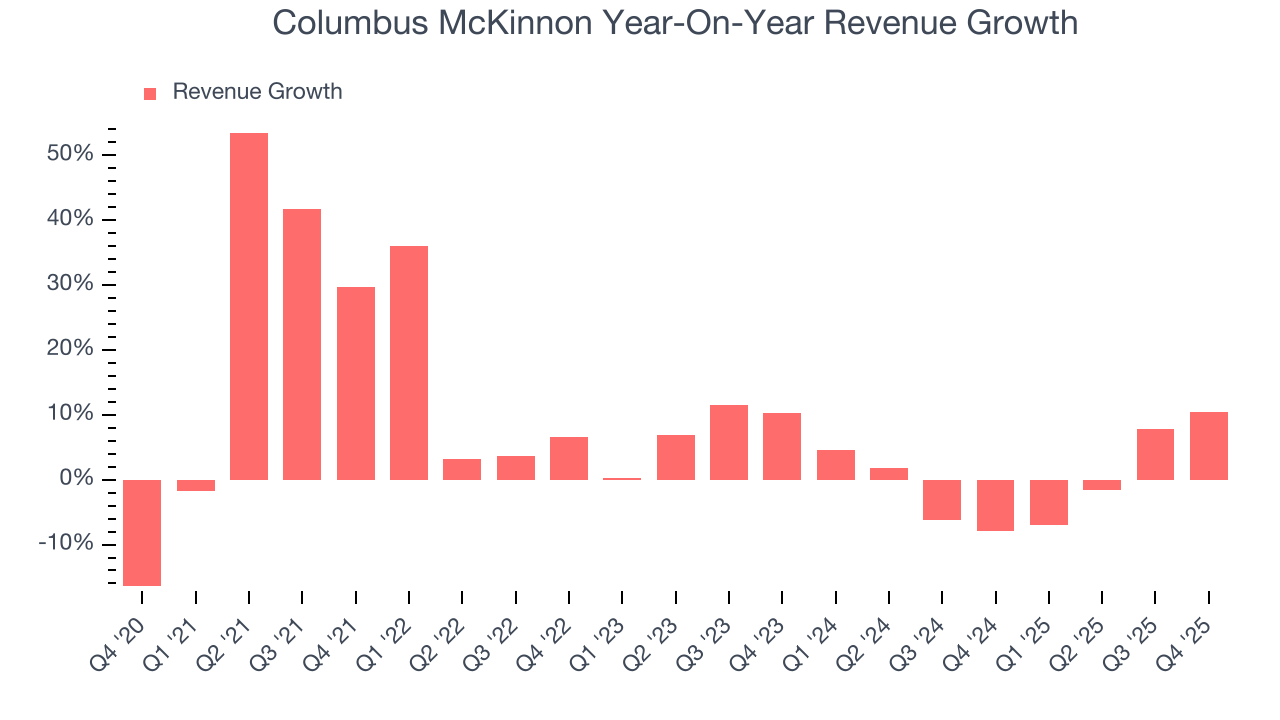

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Luckily, Columbus McKinnon’s sales grew at a decent 9% compounded annual growth rate over the last five years. Its growth was slightly above the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Columbus McKinnon’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

Columbus McKinnon also reports its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Columbus McKinnon’s backlog reached $341.6 million in the latest quarter and averaged 15.2% year-on-year growth over the last two years. Because this number is better than its revenue growth, we can see the company accumulated more orders than it could fulfill and deferred revenue to the future. This could imply elevated demand for Columbus McKinnon’s products and services but raises concerns about capacity constraints.

This quarter, Columbus McKinnon reported year-on-year revenue growth of 10.5%, and its $258.7 million of revenue exceeded Wall Street’s estimates by 5.3%.

Looking ahead, sell-side analysts expect revenue to grow 3% over the next 12 months. While this projection suggests its newer products and services will fuel better top-line performance, it is still below average for the sector.

6. Gross Margin & Pricing Power

For industrials businesses, cost of sales is usually comprised of the direct labor, raw materials, and supplies needed to offer a product or service. These costs can be impacted by inflation and supply chain dynamics in the short term and a company’s purchasing power and scale over the long term.

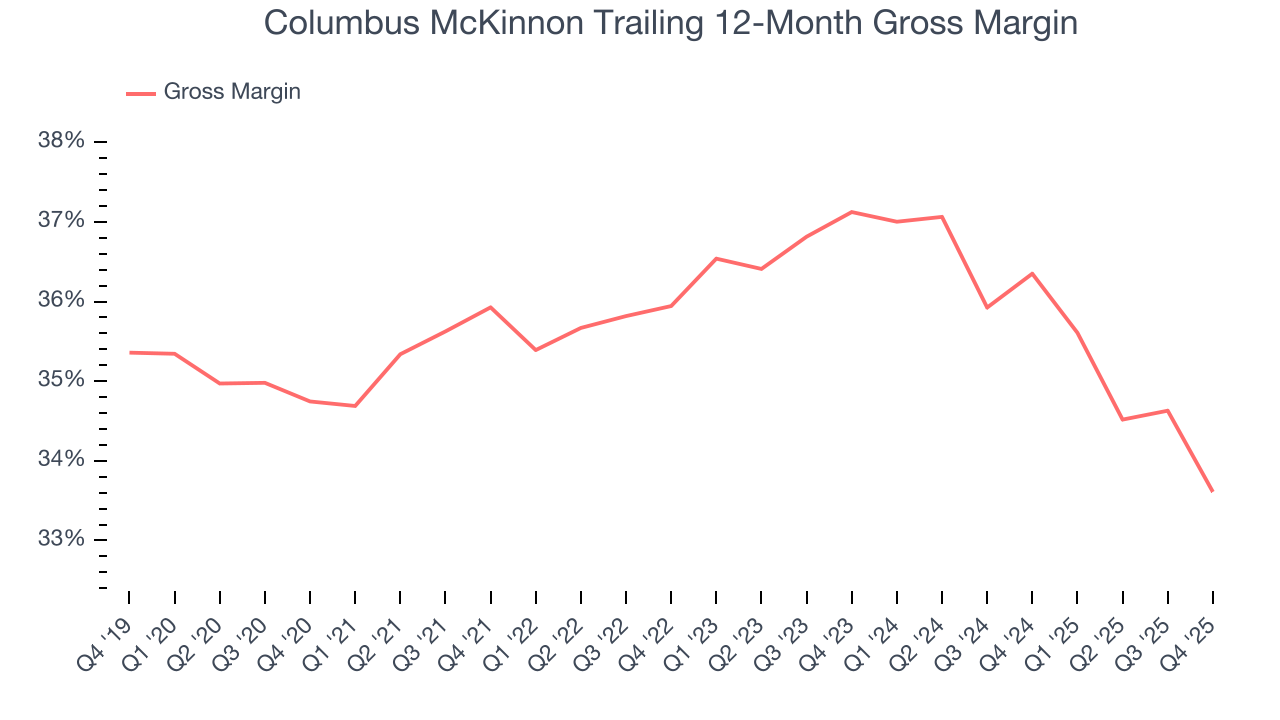

Columbus McKinnon’s gross margin is good compared to other industrials businesses and signals it sells differentiated products, not commodities. As you can see below, it averaged an impressive 35.8% gross margin over the last five years. Said differently, Columbus McKinnon paid its suppliers $64.22 for every $100 in revenue.

Columbus McKinnon produced a 34.5% gross profit margin in Q4, marking a 4.3 percentage point decrease from 38.8% in the same quarter last year. Columbus McKinnon’s full-year margin has also been trending down over the past 12 months, decreasing by 2.7 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs (such as raw materials and manufacturing expenses).

7. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Columbus McKinnon has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 9.1%, higher than the broader industrials sector.

Analyzing the trend in its profitability, Columbus McKinnon’s operating margin decreased by 1.9 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Columbus McKinnon generated an operating margin profit margin of 6.3%, down 4.7 percentage points year on year. Since Columbus McKinnon’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

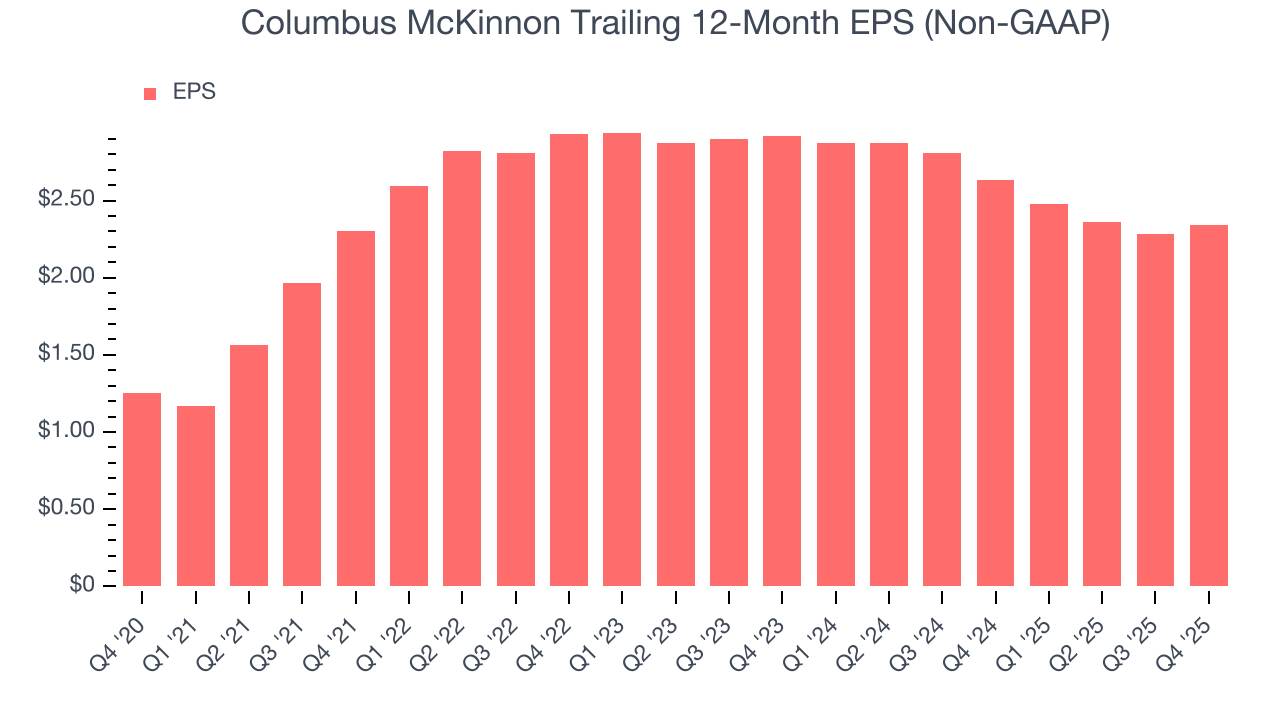

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Columbus McKinnon’s EPS grew at a remarkable 13.4% compounded annual growth rate over the last five years, higher than its 9% annualized revenue growth. However, we take this with a grain of salt because its operating margin didn’t improve and it didn’t repurchase its shares, meaning the delta came from reduced interest expenses or taxes.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Columbus McKinnon’s two-year annual EPS declines of 10.5% were bad and lower than its flat revenue.

We can take a deeper look into Columbus McKinnon’s earnings to better understand the drivers of its performance. Columbus McKinnon’s operating margin has declined over the last two years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, Columbus McKinnon reported adjusted EPS of $0.62, up from $0.56 in the same quarter last year. This print beat analysts’ estimates by 6.6%. Over the next 12 months, Wall Street expects Columbus McKinnon’s full-year EPS of $2.34 to grow 18.1%.

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Columbus McKinnon has shown weak cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 4.3%, subpar for an industrials business.

Columbus McKinnon’s free cash flow clocked in at $16.52 million in Q4, equivalent to a 6.4% margin. This result was good as its margin was 3.8 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends are more important.

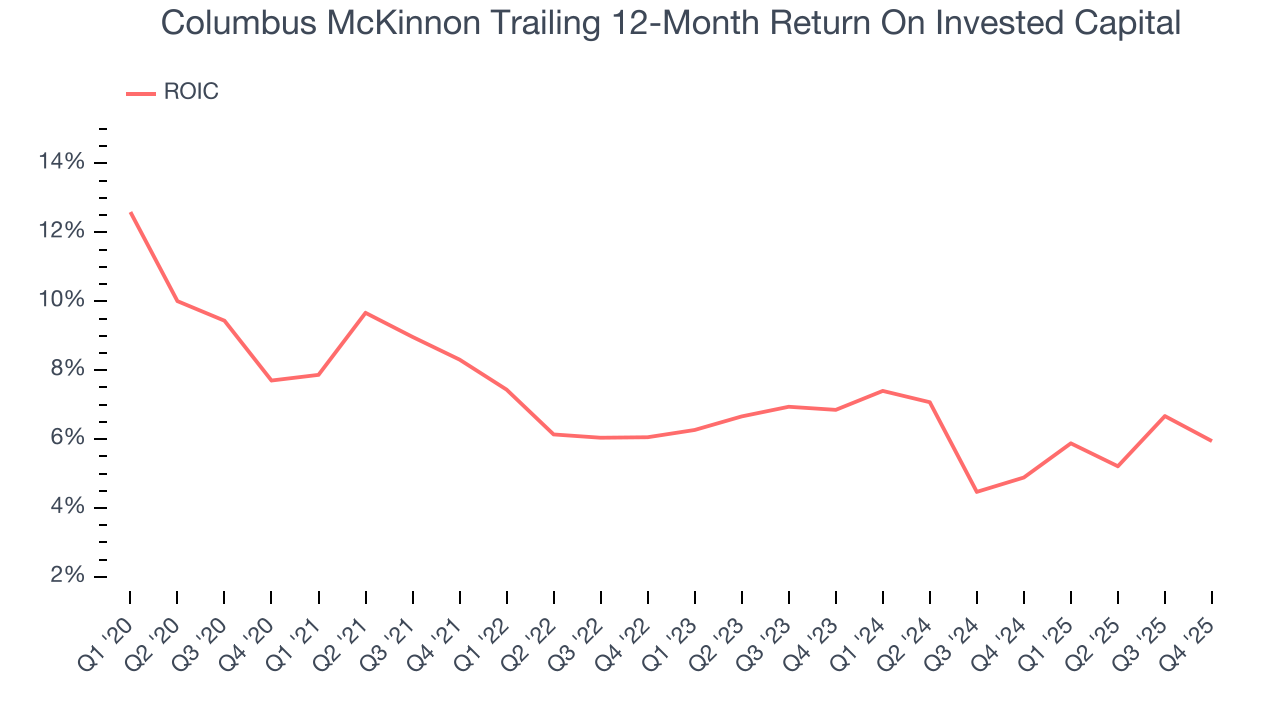

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Columbus McKinnon historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 6.4%, somewhat low compared to the best industrials companies that consistently pump out 20%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. On average, Columbus McKinnon’s ROIC decreased by 1.8 percentage points annually each year over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

11. Balance Sheet Assessment

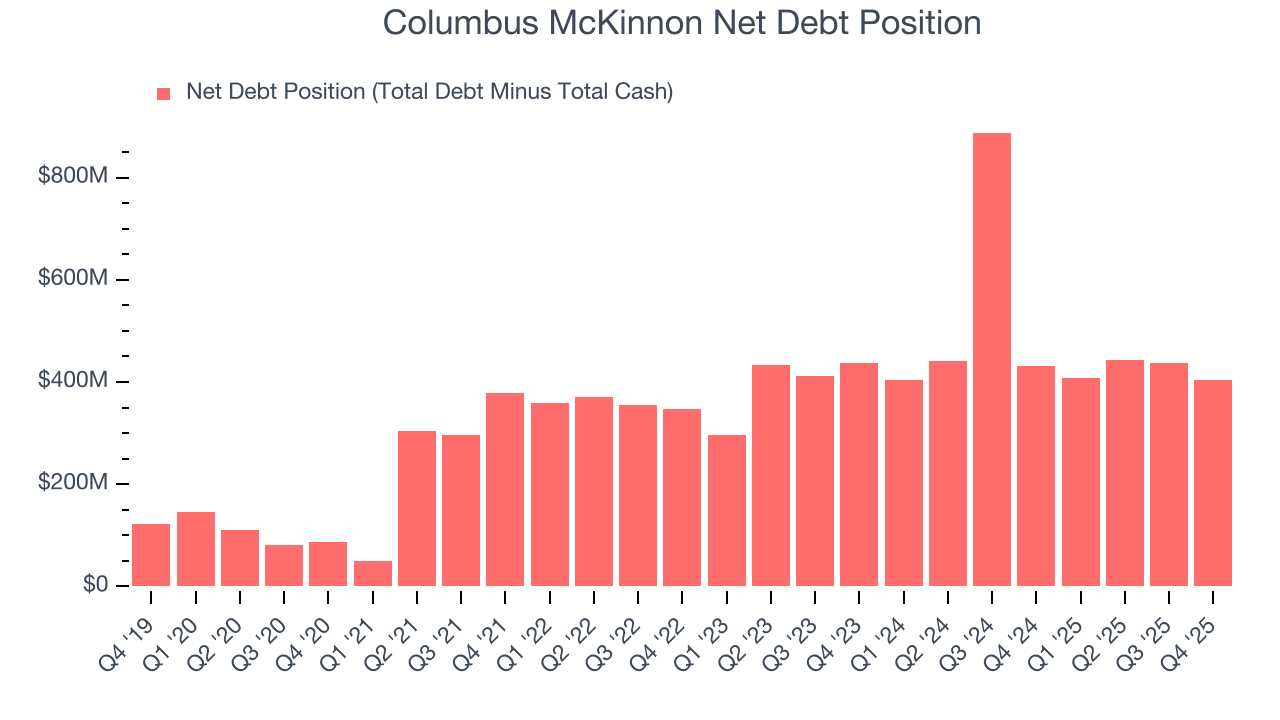

Columbus McKinnon reported $45.95 million of cash and $450.3 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $144 million of EBITDA over the last 12 months, we view Columbus McKinnon’s 2.8× net-debt-to-EBITDA ratio as safe. We also see its $15.67 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Columbus McKinnon’s Q4 Results

We were impressed by how significantly Columbus McKinnon blew past analysts’ EBITDA expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this quarter featured some important positives. The stock remained flat at $23.11 immediately after reporting.

13. Is Now The Time To Buy Columbus McKinnon?

Updated: March 14, 2026 at 11:33 PM EDT

Before investing in or passing on Columbus McKinnon, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

We cheer for all companies making their customers lives easier, but in the case of Columbus McKinnon, we’ll be cheering from the sidelines. Although its revenue growth was good over the last five years and is expected to accelerate over the next 12 months, its projected EPS for the next year is lacking. And while the company’s backlog growth has been marvelous, the downside is its declining operating margin shows the business has become less efficient.

Columbus McKinnon’s P/E ratio based on the next 12 months is 9.1x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $26.50 on the company (compared to the current share price of $14.67).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.