CSW (CSW)

CSW is in a league of its own. Its fusion of growth, outstanding profitability, and encouraging prospects makes it a beloved asset.― StockStory Analyst Team

1. News

2. Summary

Why We Like CSW

With over two centuries of combined operations manufacturing and supplying, CSW (NASDAQ:CSW) offers special chemicals, coatings, sealants, and lubricants for various industries.

- Impressive 20.6% annual revenue growth over the last five years indicates it’s winning market share this cycle

- Additional sales over the last five years increased its profitability as the 23.4% annual growth in its earnings per share outpaced its revenue

- Demand for the next 12 months is expected to accelerate above its two-year trend as Wall Street forecasts robust revenue growth of 31.3%

CSW is a market leader. The valuation seems reasonable relative to its quality, and we believe now is a good time to buy.

Why Is Now The Time To Buy CSW?

At $330.31 per share, CSW trades at 28.6x forward P/E. Valuation is above that of many industrials companies, but we think the price is justified given its business fundamentals.

Entry price may seem important in the moment, but our work shows that time and again, long-term market outperformance is determined by business quality rather than getting an absolute bargain on a stock.

3. CSW (CSW) Research Report: Q3 CY2025 Update

Industrial products company CSW (NASDAQ:CSW) fell short of the markets revenue expectations in Q3 CY2025, but sales rose 21.5% year on year to $277 million. Its non-GAAP profit of $2.49 per share was 9.8% below analysts’ consensus estimates.

CSW (CSW) Q3 CY2025 Highlights:

- Revenue: $277 million vs analyst estimates of $279.5 million (21.5% year-on-year growth, 0.9% miss)

- Adjusted EPS: $2.49 vs analyst expectations of $2.76 (9.8% miss)

- Adjusted EBITDA: $72.94 million vs analyst estimates of $71.75 million (26.3% margin, 1.7% beat)

- Operating Margin: 20.6%, down from 22.6% in the same quarter last year

- Free Cash Flow Margin: 21.2%, down from 26.9% in the same quarter last year

- Market Capitalization: $4.32 billion

Company Overview

With over two centuries of combined operations manufacturing and supplying, CSW (NASDAQ:CSW) offers special chemicals, coatings, sealants, and lubricants for various industries.

CSW was formed in 2015 through the merger of three distinct companies: Whitmore Manufacturing, Strathmore Products, and Jet-Lube.

Since its inception, the company has targeted the acquisition of various companies, primarily targeting small- to medium-sized companies that can add new product offerings to its portfolio. For example, the acquisition of Greco Aluminum Railings in 2020 marked its entry into the architectural railing systems market. Its railings are used today in residential and commercial projects to create barriers along elevated areas to prevent accidents.

More broadly, CSW offers special chemicals, coatings, sealants, lubricants, and other products to protect machines and systems. These offerings prevent wear and tear, reduce friction, seal leaks, and provide a protective barrier against damage and rust. For example, its sealants and lubricants are used in the plumbing industry to prevent leaks and keep pipes working well. Additionally, the coatings provide a protective shield against environmental factors like corrosion and abrasion, preserving the structural integrity of components over time.

The company engages in long-term contracts with distributors that often range from three to five years. It also offers volume discounts that include lower per-unit costs to incentivize companies to make larger purchases.

4. HVAC and Water Systems

Many HVAC and water systems companies sell essential, non-discretionary infrastructure for buildings. Since the useful lives of these water heaters and vents are fairly standard, these companies have a portion of predictable replacement revenue. In the last decade, trends in energy efficiency and clean water are driving innovation that is leading to incremental demand. On the other hand, new installations for these companies are at the whim of residential and commercial construction volumes, which tend to be cyclical and can be impacted heavily by economic factors such as interest rates.

Competitors offering similar products include 3M (NYSE:MMM), Sherwin-Williams (NYSE:SHW), and PPG (NYSE:PPG).

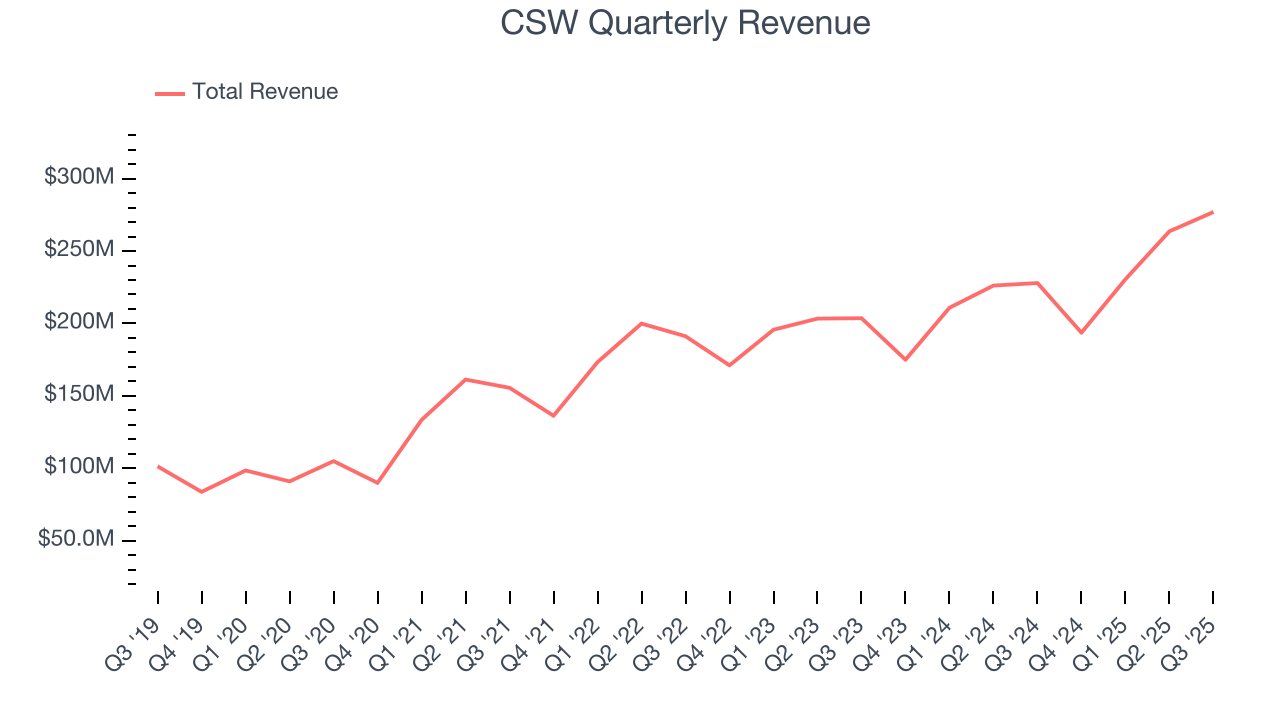

5. Revenue Growth

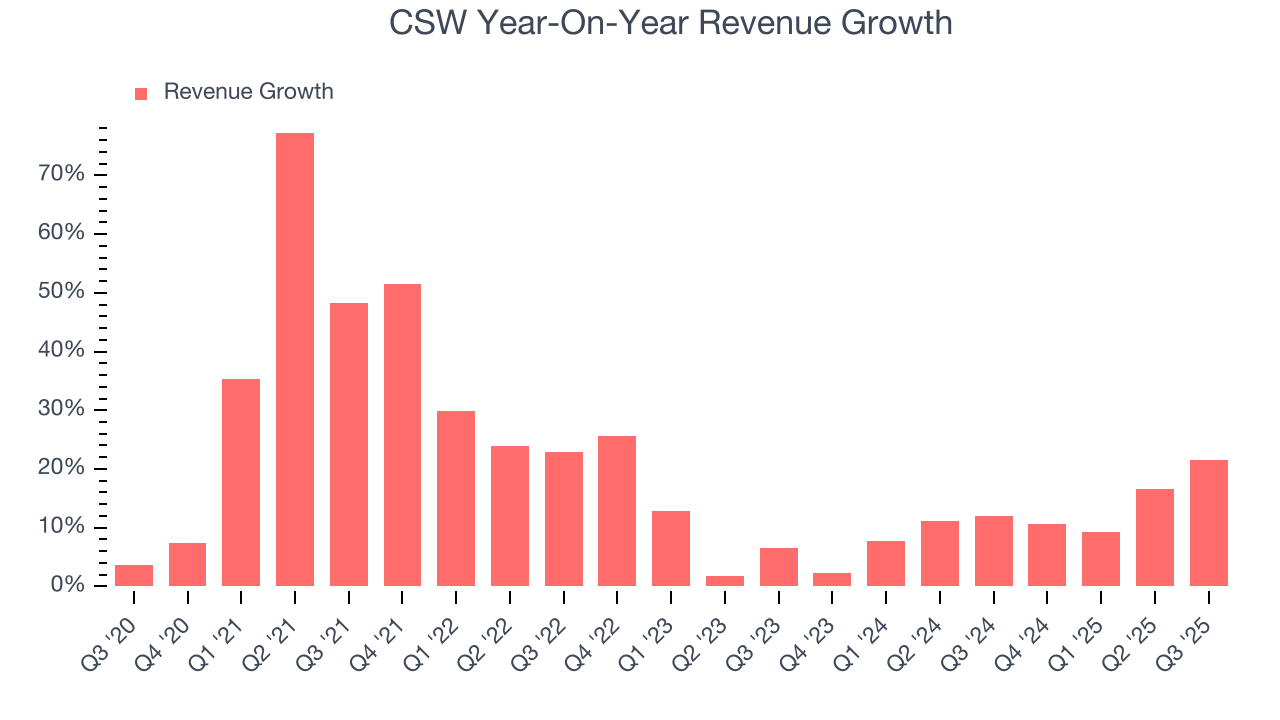

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Thankfully, CSW’s 20.6% annualized revenue growth over the last five years was incredible. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. CSW’s annualized revenue growth of 11.7% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, CSW generated an excellent 21.5% year-on-year revenue growth rate, but its $277 million of revenue fell short of Wall Street’s high expectations.

Looking ahead, sell-side analysts expect revenue to grow 28.2% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and implies its newer products and services will catalyze better top-line performance.

6. Gross Margin & Pricing Power

For industrials businesses, cost of sales is usually comprised of the direct labor, raw materials, and supplies needed to offer a product or service. These costs can be impacted by inflation and supply chain dynamics in the short term and a company’s purchasing power and scale over the long term.

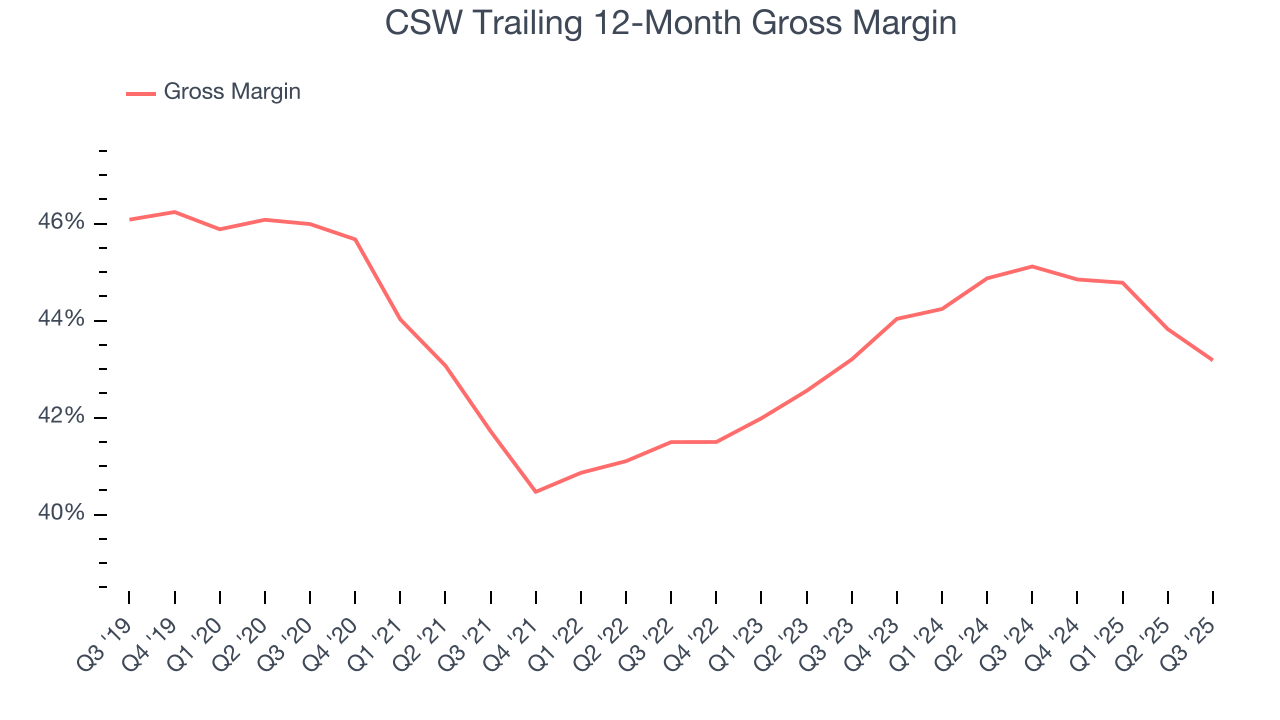

CSW has best-in-class unit economics for an industrials company, enabling it to invest in areas such as research and development. Its margin also signals it sells differentiated products, not commodities. As you can see below, it averaged an elite 43.1% gross margin over the last five years. That means CSW only paid its suppliers $56.91 for every $100 in revenue.

This quarter, CSW’s gross profit margin was 43%, down 2.6 percentage points year on year. CSW’s full-year margin has also been trending down over the past 12 months, decreasing by 1.9 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs (such as raw materials and manufacturing expenses).

7. Operating Margin

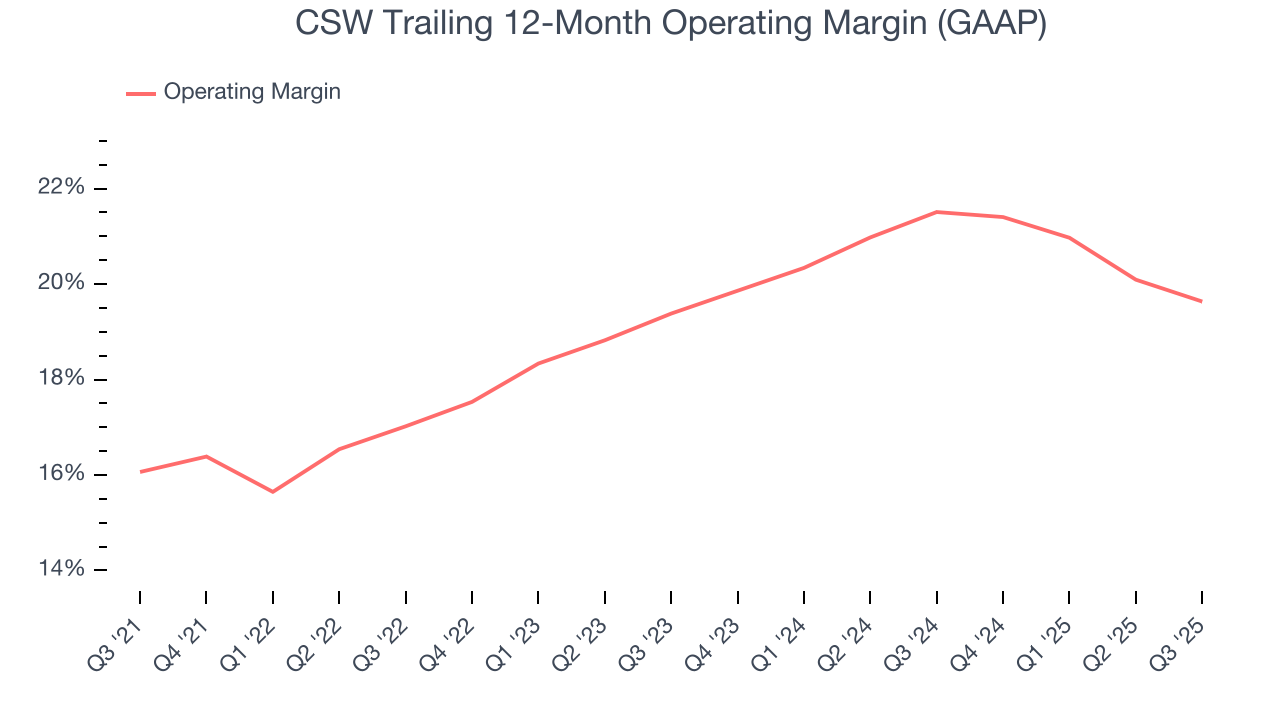

CSW has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 19%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, CSW’s operating margin rose by 3.6 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q3, CSW generated an operating margin profit margin of 20.6%, down 2 percentage points year on year. Since CSW’s gross margin decreased more than its operating margin, we can assume its recent inefficiencies were driven more by weaker leverage on its cost of sales rather than increased marketing, R&D, and administrative overhead expenses.

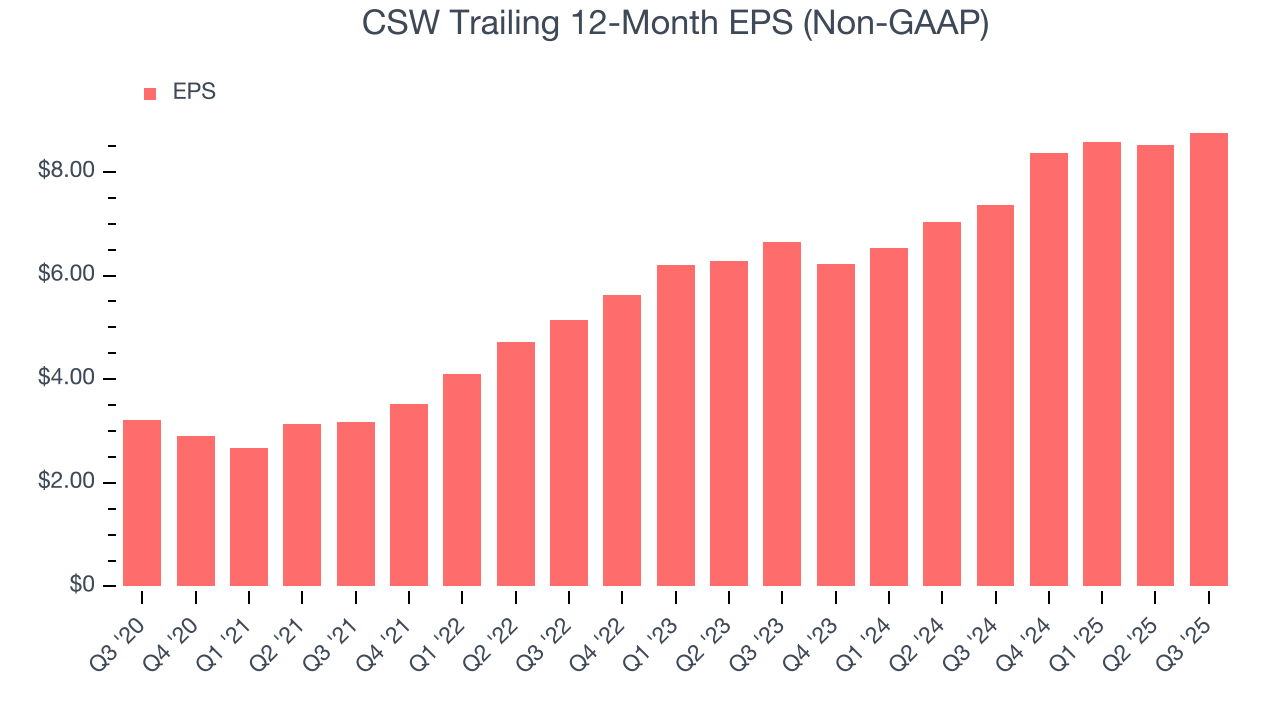

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

CSW’s astounding 22.2% annual EPS growth over the last five years aligns with its revenue performance. This tells us its incremental sales were profitable.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For CSW, its two-year annual EPS growth of 14.8% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q3, CSW reported adjusted EPS of $2.49, up from $2.26 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects CSW’s full-year EPS of $8.76 to grow 28.9%.

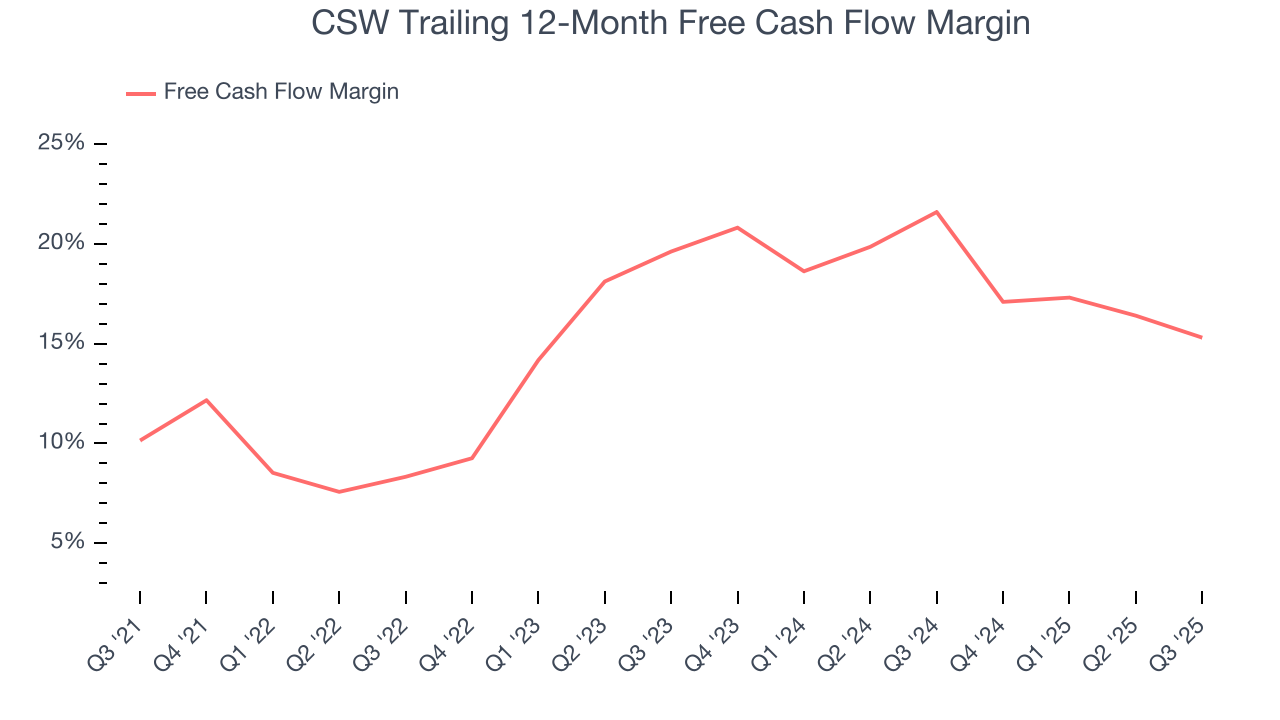

9. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

CSW has shown terrific cash profitability, putting it in an advantageous position to invest in new products, return capital to investors, and consolidate the market during industry downturns. The company’s free cash flow margin was among the best in the industrials sector, averaging 15.6% over the last five years.

Taking a step back, we can see that CSW’s margin expanded by 5.2 percentage points during that time. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

CSW’s free cash flow clocked in at $58.75 million in Q3, equivalent to a 21.2% margin. The company’s cash profitability regressed as it was 5.7 percentage points lower than in the same quarter last year, but it’s still above its five-year average. We wouldn’t read too much into this quarter’s decline because capital expenditures can be seasonal and companies often stockpile inventory in anticipation of higher demand, causing short-term swings. Long-term trends trump temporary fluctuations.

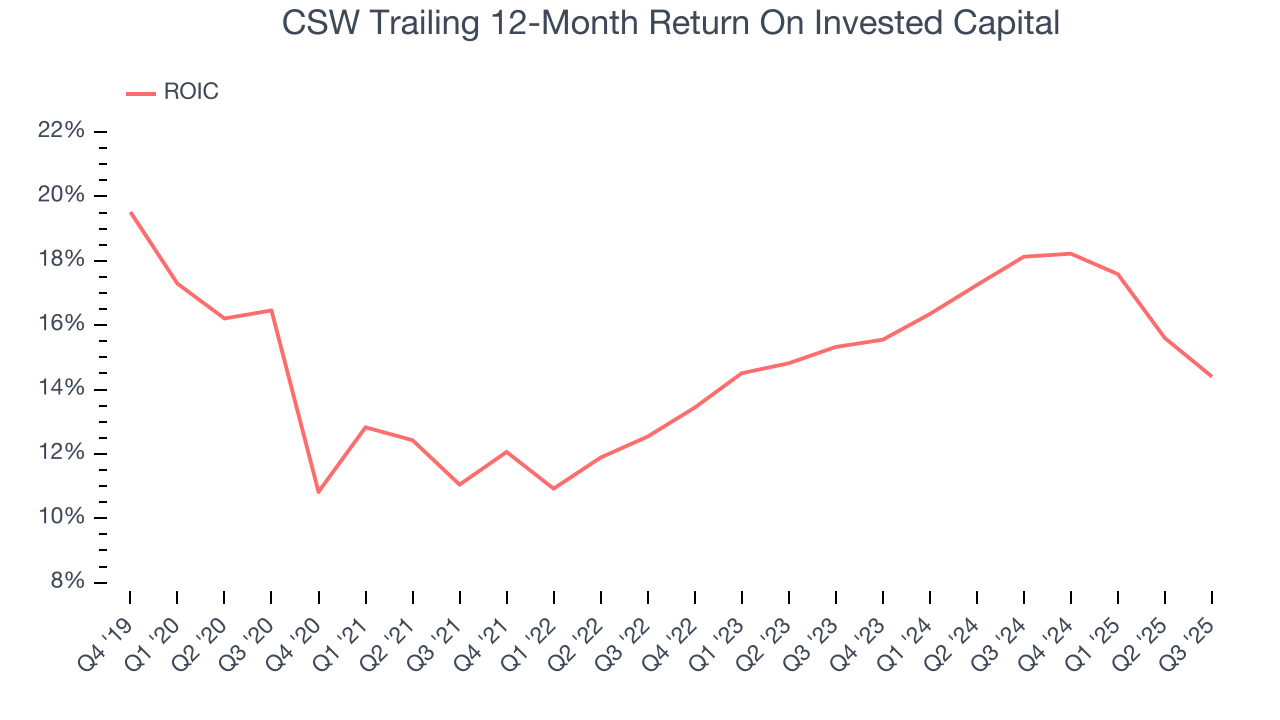

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

CSW’s five-year average ROIC was 14.3%, beating other industrials companies by a wide margin. This illustrates its management team’s ability to invest in attractive growth opportunities and produce tangible results for shareholders.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, CSW’s ROIC averaged 4.5 percentage point increases each year. This is a great sign when paired with its already strong returns. It could suggest its competitive advantage or profitable growth opportunities are expanding.

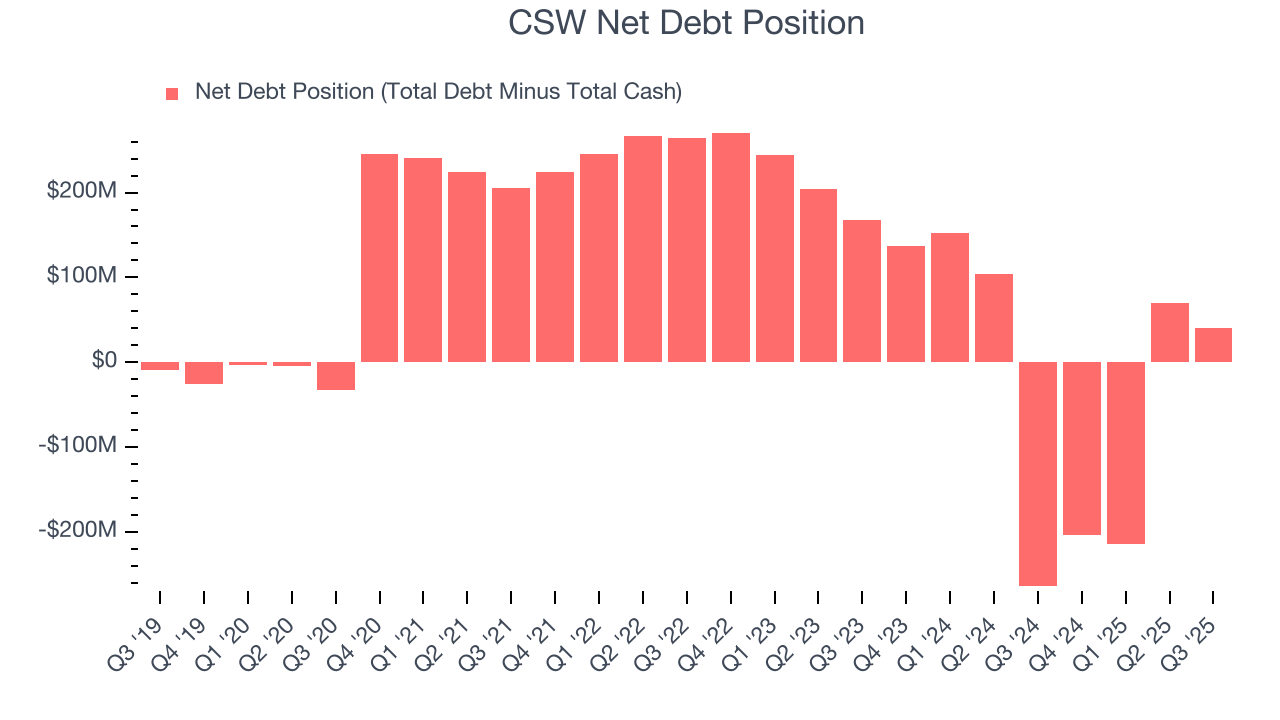

11. Balance Sheet Assessment

CSW reported $31.47 million of cash and $72.31 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $237.6 million of EBITDA over the last 12 months, we view CSW’s 0.2× net-debt-to-EBITDA ratio as safe. We also see its $1.25 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from CSW’s Q3 Results

It was encouraging to see CSW beat analysts’ EBITDA expectations this quarter. On the other hand, its EPS missed and its revenue fell slightly short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock remained flat at $259.19 immediately following the results.

13. Is Now The Time To Buy CSW?

Updated: January 22, 2026 at 10:06 PM EST

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own CSW, you should also grasp the company’s longer-term business quality and valuation.

There are numerous reasons why we think CSW is one of the best industrials companies out there. For starters, its revenue growth was exceptional over the last five years and is expected to accelerate over the next 12 months. On top of that, its powerful free cash flow generation enables it to stay ahead of the competition through consistent reinvestment of profits, and its impressive operating margins show it has a highly efficient business model.

CSW’s P/E ratio based on the next 12 months is 28.6x. Looking at the industrials space today, CSW’s qualities as one of the best businesses really stand out, and we like it at this price.

Wall Street analysts have a consensus one-year price target of $321.17 on the company (compared to the current share price of $330.31).