Dime Community Bancshares (DCOM)

We aren’t fans of Dime Community Bancshares. Its poor returns on capital indicate it barely generated any profits, a must for high-quality companies.― StockStory Analyst Team

1. News

2. Summary

Why We Think Dime Community Bancshares Will Underperform

With roots dating back to 1910 and a name that evokes the historic "dime savings banks" of America's past, Dime Community Bancshares (NASDAQ:DCOM) is a New York-based bank holding company that provides commercial banking and financial services to businesses and consumers throughout Greater Long Island.

- Performance over the past five years shows its incremental sales were less profitable, as its 1.9% annual earnings per share growth trailed its revenue gains

- Weak unit economics are reflected in its net interest margin of 2.7%, one of the worst among bank companies

- The good news is that its operating profits are forecasted to increase over the next year as it scales and becomes more productive

Dime Community Bancshares is skating on thin ice. We’d search for superior opportunities elsewhere.

Why There Are Better Opportunities Than Dime Community Bancshares

At $31.89 per share, Dime Community Bancshares trades at 1x forward P/B. This multiple is cheaper than most banking peers, but we think this is justified.

Our advice is to pay up for elite businesses whose advantages are tailwinds to earnings growth. Don’t get sucked into lower-quality businesses just because they seem like bargains. These mediocre businesses often never achieve a higher multiple as hoped, a phenomenon known as a “value trap”.

3. Dime Community Bancshares (DCOM) Research Report: Q4 CY2025 Update

Regional bank Dime Community Bancshares (NASDAQ:DCOM) reported revenue ahead of Wall Streets expectations in Q4 CY2025, with sales up 24.4% year on year to $123.8 million. Its non-GAAP profit of $0.79 per share was 10.6% above analysts’ consensus estimates.

Dime Community Bancshares (DCOM) Q4 CY2025 Highlights:

- Net Interest Income: $112.3 million vs analyst estimates of $106.8 million (23.3% year-on-year growth, 5.2% beat)

- Net Interest Margin: 3.1% vs analyst estimates of 3.1% (in line)

- Revenue: $123.8 million vs analyst estimates of $117.8 million (24.4% year-on-year growth, 5.1% beat)

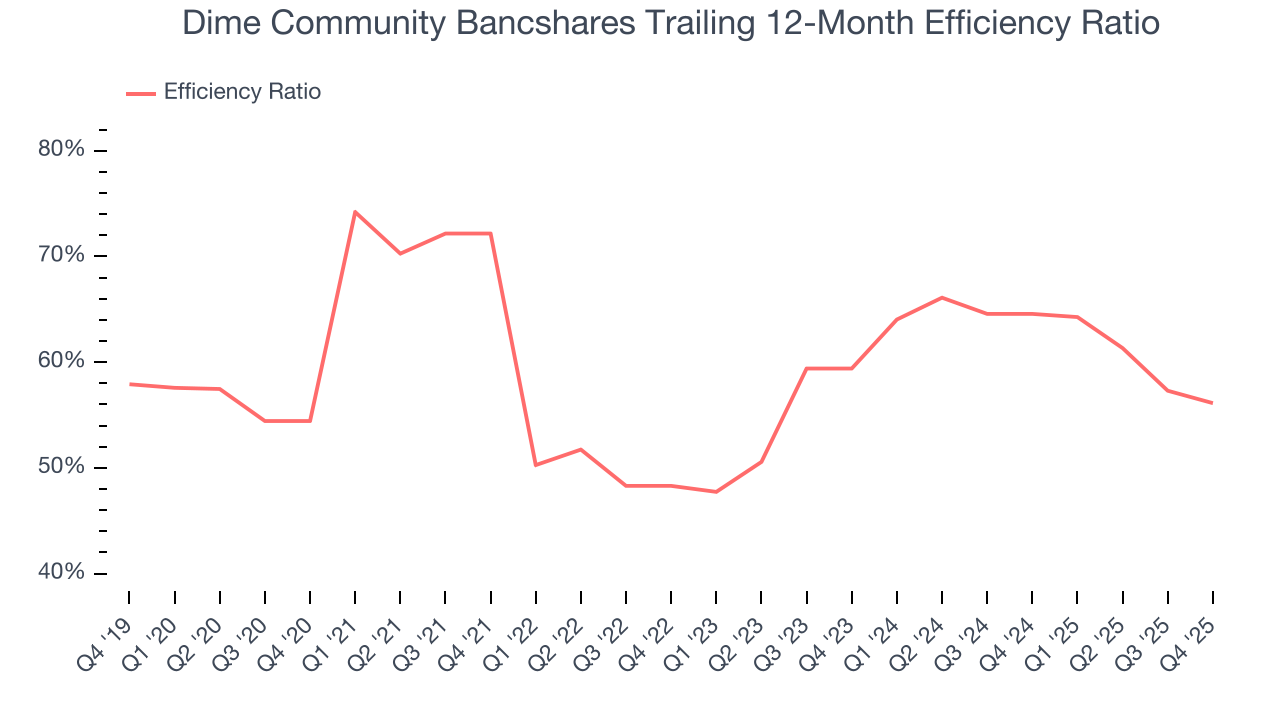

- Efficiency Ratio: 52.6% vs analyst estimates of 53.4% (80 basis point beat)

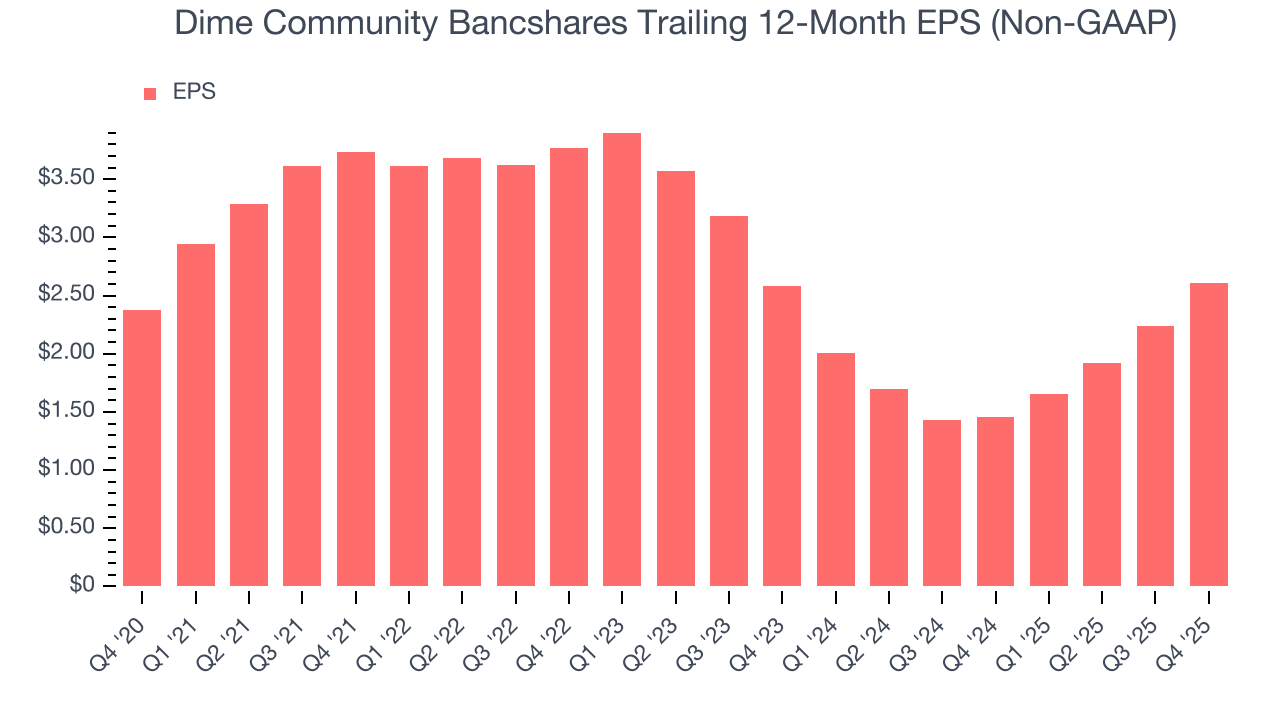

- Adjusted EPS: $0.79 vs analyst estimates of $0.71 (10.6% beat)

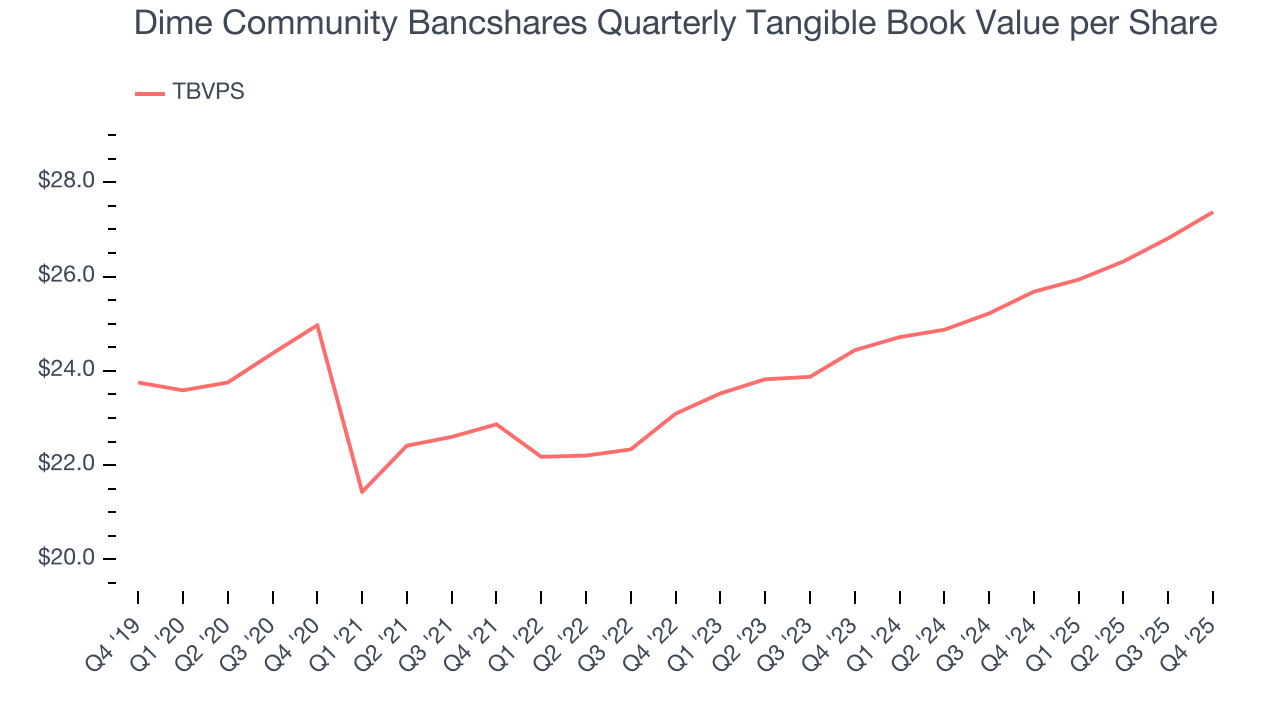

- Tangible Book Value per Share: $27.37 vs analyst estimates of $27.29 (6.6% year-on-year growth, in line)

- Market Capitalization: $1.32 billion

Company Overview

With roots dating back to 1910 and a name that evokes the historic "dime savings banks" of America's past, Dime Community Bancshares (NASDAQ:DCOM) is a New York-based bank holding company that provides commercial banking and financial services to businesses and consumers throughout Greater Long Island.

Dime Community Bank, the company's primary operating subsidiary, offers a comprehensive suite of banking products and services. Its lending portfolio is diversified across several categories, including commercial real estate loans, multifamily residential loans, one-to-four family residential loans, and commercial and industrial loans to small and medium-sized businesses.

The bank generates revenue primarily through interest income on loans and securities, as well as fees from various banking services. Customers can access deposit products such as checking and savings accounts, certificates of deposit, and money market accounts. Beyond traditional banking, Dime offers cash management services, merchant card processing, online banking, remote deposit capture, and investment services through a third-party broker-dealer.

A local business owner might use Dime for multiple banking needs—securing a commercial real estate loan to purchase a storefront, establishing business checking accounts for daily operations, and utilizing cash management services to optimize their company's finances. Meanwhile, a residential property developer might obtain construction financing for a multifamily housing project in Brooklyn.

Dime's title insurance subsidiary serves as a broker for title insurance services, adding another dimension to its real estate-focused offerings. The bank operates numerous branches throughout Long Island and across all five boroughs of New York City, providing both physical and digital banking channels for its customers. As a regulated financial institution, Dime must comply with various federal and state banking regulations, including those related to capital requirements, lending practices, and consumer protection.

4. Regional Banks

Regional banks, financial institutions operating within specific geographic areas, serve as intermediaries between local depositors and borrowers. They benefit from rising interest rates that improve net interest margins (the difference between loan yields and deposit costs), digital transformation reducing operational expenses, and local economic growth driving loan demand. However, these banks face headwinds from fintech competition, deposit outflows to higher-yielding alternatives, credit deterioration (increasing loan defaults) during economic slowdowns, and regulatory compliance costs. Recent concerns about regional bank stability following high-profile failures and significant commercial real estate exposure present additional challenges.

Dime Community Bancshares competes with other regional banks serving the New York metropolitan area, including New York Community Bancorp (NYSE:NYCB), Valley National Bancorp (NASDAQ:VLY), and M&T Bank (NYSE:MTB), as well as larger national banks with significant presence in the region.

5. Sales Growth

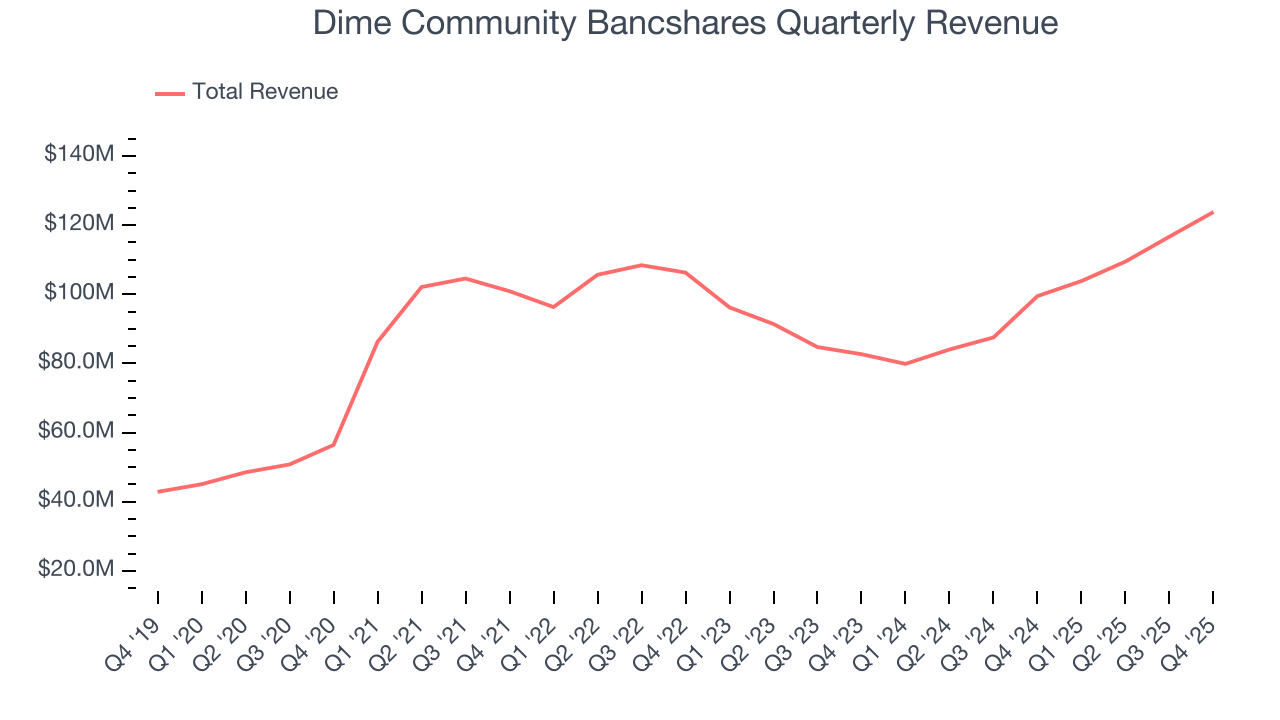

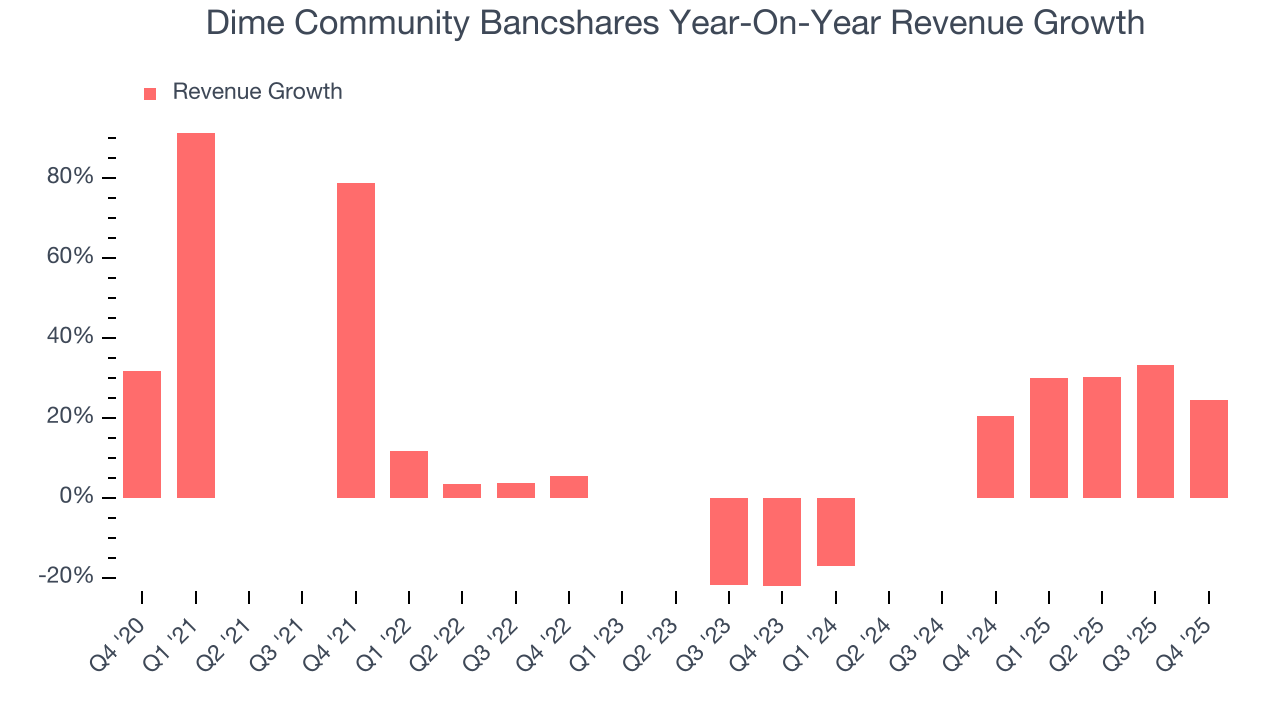

Net interest income and and fee-based revenue are the two pillars supporting bank earnings. The former captures profit from the gap between lending rates and deposit costs, while the latter encompasses charges for banking services, credit products, wealth management, and trading activities. Thankfully, Dime Community Bancshares’s 17.7% annualized revenue growth over the last five years was excellent. Its growth beat the average banking company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Dime Community Bancshares’s annualized revenue growth of 13.1% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Dime Community Bancshares reported robust year-on-year revenue growth of 24.4%, and its $123.8 million of revenue topped Wall Street estimates by 5.1%.

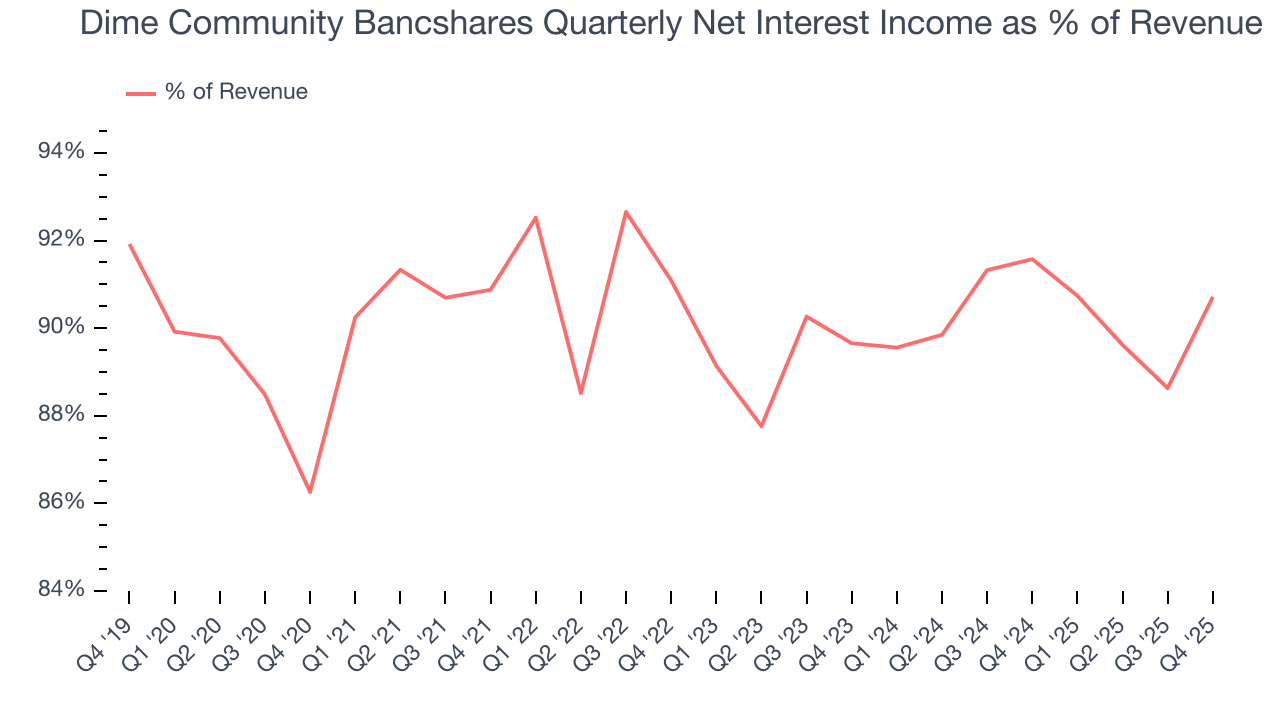

Net interest income made up 90.3% of the company’s total revenue during the last five years, meaning Dime Community Bancshares lives and dies by its lending activities because non-interest income barely moves the needle.

Net interest income commands greater market attention due to its reliability and consistency, whereas non-interest income is often seen as lower-quality revenue that lacks the same dependable characteristics.

6. Efficiency Ratio

Topline growth alone doesn't tell the complete story - the profitability of that growth shapes actual earnings impact. Banks track this dynamic through efficiency ratios, which compare non-interest expenses such as personnel, rent, IT, and marketing costs to total revenue streams.

Investors place greater emphasis on efficiency ratio movements than absolute values, understanding that expense structures reflect revenue mix variations. Lower ratios represent better operational performance since they show banks generating more revenue per dollar of expense.

Over the last five years, Dime Community Bancshares’s efficiency ratio has increased by 1.7 percentage points, going from 72.2% to 56.1%. Said differently, the company’s expenses have increased at a faster rate than revenue, which usually raises questions unless the company is in high-growth mode and reinvesting its profits into attractive ventures.

In Q4, Dime Community Bancshares’s efficiency ratio was 52.6%, beating analysts’ expectations by 80 basis points (100 basis points = 1 percentage point).

For the next 12 months, Wall Street expects Dime Community Bancshares to rein in some of its expenses as it anticipates an efficiency ratio of 50.9%.

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Dime Community Bancshares’s EPS grew at a weak 1.9% compounded annual growth rate over the last five years, lower than its 17.7% annualized revenue growth. However, its efficiency ratio actually improved during this time, telling us that non-fundamental factors such as taxes affected its ultimate earnings.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Dime Community Bancshares, EPS didn’t budge over the last two years, a regression from its five-year trend. We hope it can revert to earnings growth in the coming years.

In Q4, Dime Community Bancshares reported adjusted EPS of $0.79, up from $0.42 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Dime Community Bancshares’s full-year EPS of $2.61 to grow 32.1%.

8. Tangible Book Value Per Share (TBVPS)

Banks profit by intermediating between depositors and borrowers, making them fundamentally balance sheet-driven enterprises. Market participants emphasize balance sheet quality and sustained book value growth when evaluating these institutions.

This is why we consider tangible book value per share (TBVPS) the most important metric to track for banks. TBVPS represents the real, liquid net worth per share of a bank, excluding intangible assets that have debatable value upon liquidation. EPS can become murky due to acquisition impacts or accounting flexibility around loan provisions, and TBVPS resists financial engineering manipulation.

Dime Community Bancshares’s TBVPS grew at a sluggish 1.9% annual clip over the last five years. However, TBVPS growth has accelerated recently, growing by 5.8% annually over the last two years from $24.44 to $27.37 per share.

Over the next 12 months, Consensus estimates call for Dime Community Bancshares’s TBVPS to grow by 8.9% to $29.82, paltry growth rate.

9. Balance Sheet Assessment

Leverage is core to a financial firm’s business model (loans funded by deposits). To ensure economic stability and avoid a repeat of the 2008 GFC, regulators require certain levels of capital and liquidity, focusing on the Tier 1 capital ratio.

Tier 1 capital is the highest-quality capital that a firm holds, consisting primarily of common stock and retained earnings, but also physical gold. It serves as the primary cushion against losses and is the first line of defense in times of financial distress.

This capital is divided by risk-weighted assets to derive the Tier 1 capital ratio. Risk-weighted means that cash and US treasury securities are assigned little risk while unsecured consumer loans and equity investments get much higher risk weights, for example.

New regulation after the 2008 financial crisis requires that all firms must maintain a Tier 1 capital ratio greater than 4.5%. On top of this, there are additional buffers based on scale, risk profile, and other regulatory classifications, so that at the end of the day, firms generally must maintain a 7-10% ratio at minimum.

Over the last two years, Dime Community Bancshares has averaged a Tier 1 capital ratio of 10.9%, which is considered safe and well capitalized in the event that macro or market conditions suddenly deteriorate.

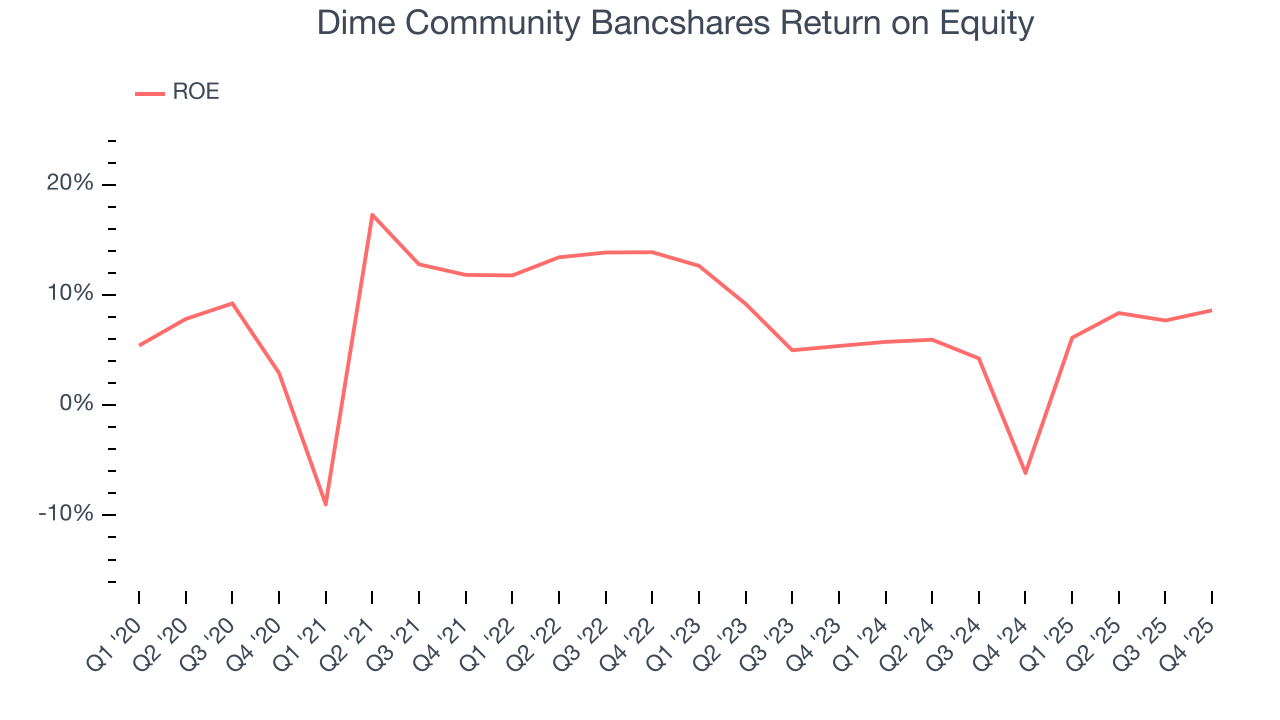

10. Return on Equity

Return on equity, or ROE, tells us how much profit a company generates for each dollar of shareholder equity, a key funding source for banks. Over a long period, banks with high ROE tend to compound shareholder wealth faster through retained earnings, buybacks, and dividends.

Over the last five years, Dime Community Bancshares has averaged an ROE of 7.9%, uninspiring for a company operating in a sector where the average shakes out around 7.5%.

11. Key Takeaways from Dime Community Bancshares’s Q4 Results

We were impressed by how significantly Dime Community Bancshares blew past analysts’ net interest income expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a solid print. The stock remained flat at $30.12 immediately following the results.

12. Is Now The Time To Buy Dime Community Bancshares?

Updated: March 16, 2026 at 12:49 AM EDT

Before making an investment decision, investors should account for Dime Community Bancshares’s business fundamentals and valuation in addition to what happened in the latest quarter.

Dime Community Bancshares’s business quality ultimately falls short of our standards. Although its revenue growth was impressive over the last five years, it’s expected to deteriorate over the next 12 months and its weak EPS growth over the last five years shows it’s failed to produce meaningful profits for shareholders. And while the company’s expanding net interest margin shows its loan book is becoming more profitable, the downside is its net interest margin limits its operating profit potential compared to other banks that can earn more, all else equal..

Dime Community Bancshares’s P/B ratio based on the next 12 months is 1x. This valuation multiple is fair, but we don’t have much faith in the company. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $39.60 on the company (compared to the current share price of $31.89).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.