DocuSign (DOCU)

We aren’t fans of DocuSign. It’s recently struggled to grow its revenue, a worrying sign for investors seeking high-quality stocks.― StockStory Analyst Team

1. News

2. Summary

Why We Think DocuSign Will Underperform

Creating the digital equivalent of "sign on the dotted line" for over a billion users worldwide, DocuSign (NASDAQ:DOCU) provides an agreement management platform that enables businesses to electronically prepare, sign, and manage documents and contracts.

- Anticipated sales growth of 6.7% for the next year implies demand will be shaky

- Underwhelming ARR growth of 8.4% over the last year suggests the company faced challenges in acquiring and retaining long-term customers

- A positive is that its software platform has product-market fit given the rapid recovery of its customer acquisition costs

DocuSign is in the doghouse. Our attention is focused on better businesses.

Why There Are Better Opportunities Than DocuSign

At $45.09 per share, DocuSign trades at 2.8x forward price-to-sales. DocuSign’s valuation may seem like a bargain, but we think there are valid reasons why it’s so cheap.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. DocuSign (DOCU) Research Report: Q3 CY2025 Update

Electronic signature company DocuSign (NASDAQ:DOCU) reported Q3 CY2025 results topping the market’s revenue expectations, with sales up 8.4% year on year to $818.4 million. The company expects next quarter’s revenue to be around $827 million, close to analysts’ estimates. Its non-GAAP profit of $1.01 per share was 10.4% above analysts’ consensus estimates.

DocuSign (DOCU) Q3 CY2025 Highlights:

- Revenue: $818.4 million vs analyst estimates of $807 million (8.4% year-on-year growth, 1.4% beat)

- Adjusted EPS: $1.01 vs analyst estimates of $0.91 (10.4% beat)

- Adjusted Operating Income: $257.1 million vs analyst estimates of $231.3 million (31.4% margin, 11.1% beat)

- Revenue Guidance for Q4 CY2025 is $827 million at the midpoint, roughly in line with what analysts were expecting

- Operating Margin: 10.4%, up from 7.8% in the same quarter last year

- Free Cash Flow Margin: 32.1%, up from 27.2% in the previous quarter

- Billings: $829.5 million at quarter end, up 10.3% year on year

- Market Capitalization: $14.2 billion

Company Overview

Creating the digital equivalent of "sign on the dotted line" for over a billion users worldwide, DocuSign (NASDAQ:DOCU) provides an agreement management platform that enables businesses to electronically prepare, sign, and manage documents and contracts.

The company's flagship product, eSignature, forms the foundation of its business, allowing organizations to securely execute agreements from virtually any device, anywhere in the world. Beyond simply capturing signatures, DocuSign offers a comprehensive suite of products that span the entire agreement lifecycle. These include contract lifecycle management (CLM) software for automating pre- and post-signature workflows, document generation tools, identity verification services, and industry-specific solutions for sectors like real estate and healthcare.

DocuSign's platform integrates with over 900 business applications including Salesforce, Microsoft, Google, and SAP, allowing companies to embed agreement processes into their existing workflows. This extensive integration ecosystem helps organizations streamline operations across departments from sales and marketing to legal, HR, and procurement.

The company employs a subscription-based business model with various pricing tiers based on functionality and usage volume. DocuSign measures usage through "Envelopes" – digital containers that hold documents sent for signature. Revenue grows as customers increase their envelope volume, upgrade plans, or adopt additional products. A Fortune 500 company might use DocuSign for everything from closing sales deals and processing vendor contracts to managing employment offers and executing internal compliance documents.

4. Document Management

The catch phrase "digital transformation" originally referred to the digitization of documents within enterprises. The growth of digital documents has spurred an explosion of collaboration within and between businesses, which in turn is driving the demand for e-signature and content management platforms.

DocuSign's primary global competitor is Adobe Acrobat Sign (formerly Adobe Sign), part of Adobe Inc. (NASDAQ:ADBE). Other competitors include HelloSign (owned by Dropbox), PandaDoc, SignNow, and various enterprise software providers that have incorporated electronic signature capabilities into their platforms.

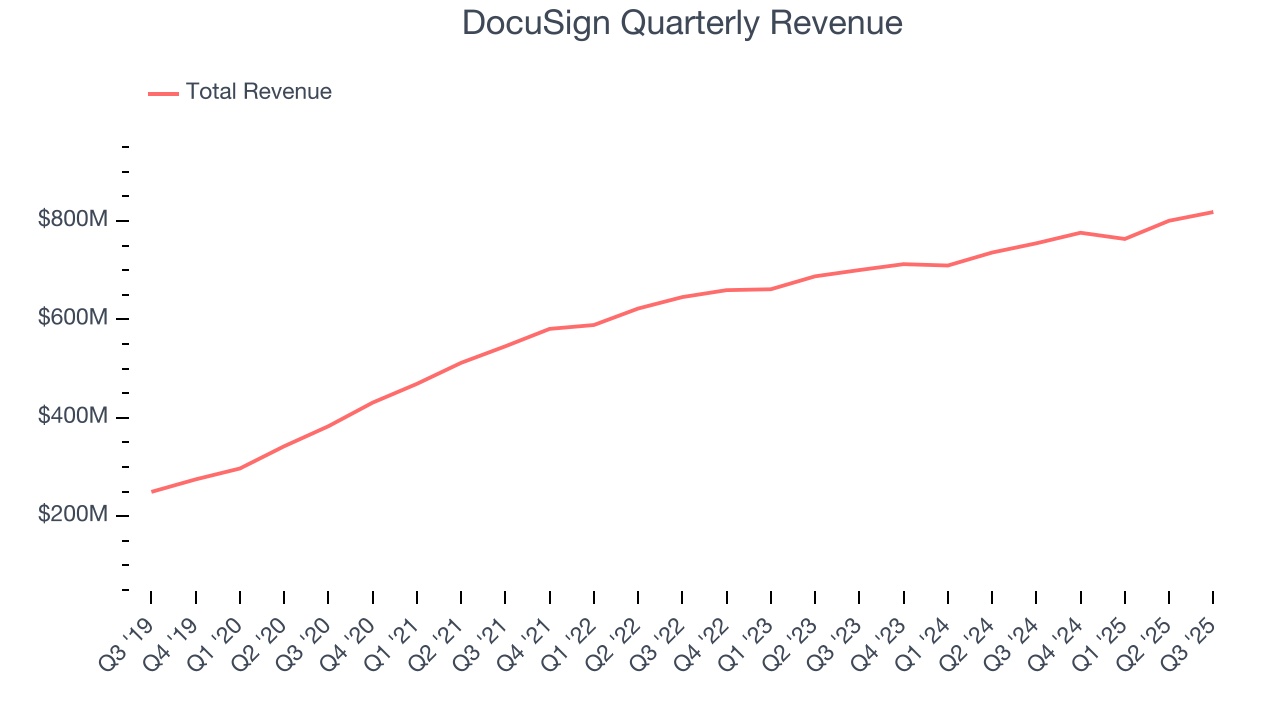

5. Revenue Growth

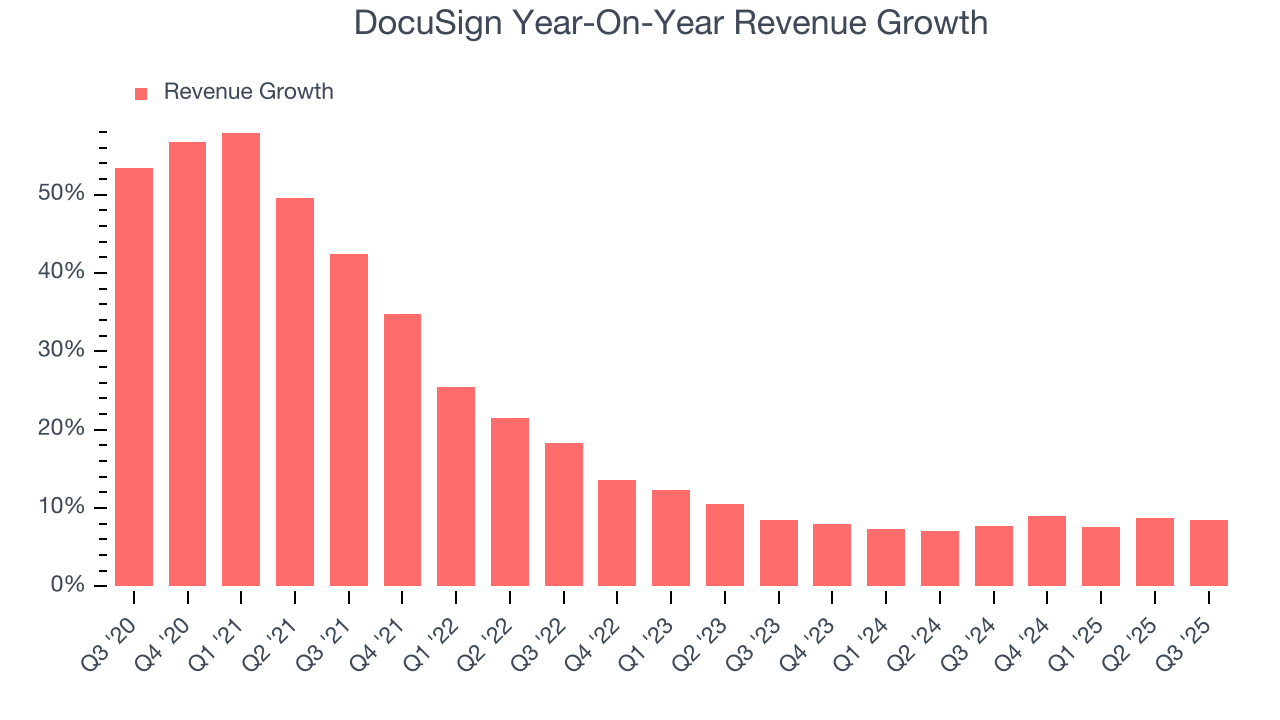

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, DocuSign’s 19.5% annualized revenue growth over the last five years was decent. Its growth was slightly above the average software company and shows its offerings resonate with customers.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. DocuSign’s recent performance shows its demand has slowed as its annualized revenue growth of 8% over the last two years was below its five-year trend.

This quarter, DocuSign reported year-on-year revenue growth of 8.4%, and its $818.4 million of revenue exceeded Wall Street’s estimates by 1.4%. Company management is currently guiding for a 6.5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 6.3% over the next 12 months, a slight deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will see some demand headwinds.

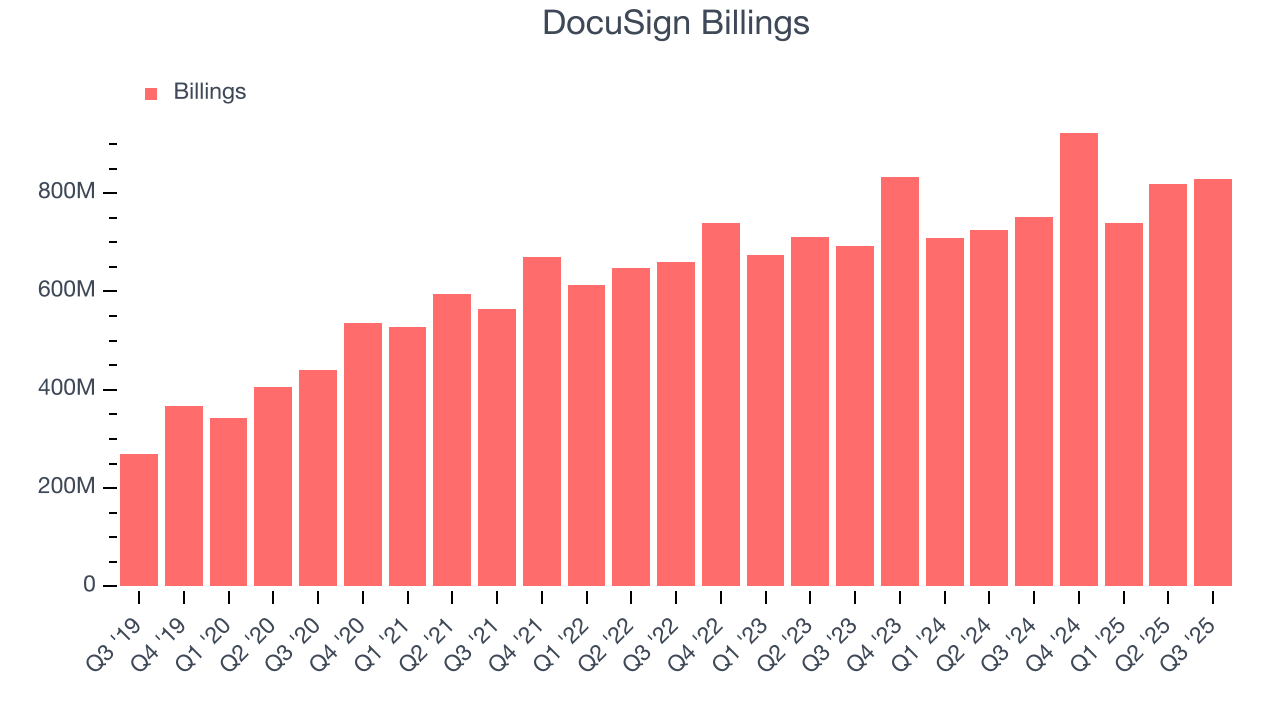

6. Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

DocuSign’s billings came in at $829.5 million in Q3, and over the last four quarters, its growth was underwhelming as it averaged 9.6% year-on-year increases. This performance mirrored its total sales and suggests that increasing competition is causing challenges in acquiring/retaining customers.

7. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

DocuSign is extremely efficient at acquiring new customers, and its CAC payback period checked in at 14.2 months this quarter. The company’s rapid recovery of its customer acquisition costs means it can attempt to spur growth by increasing its sales and marketing investments.

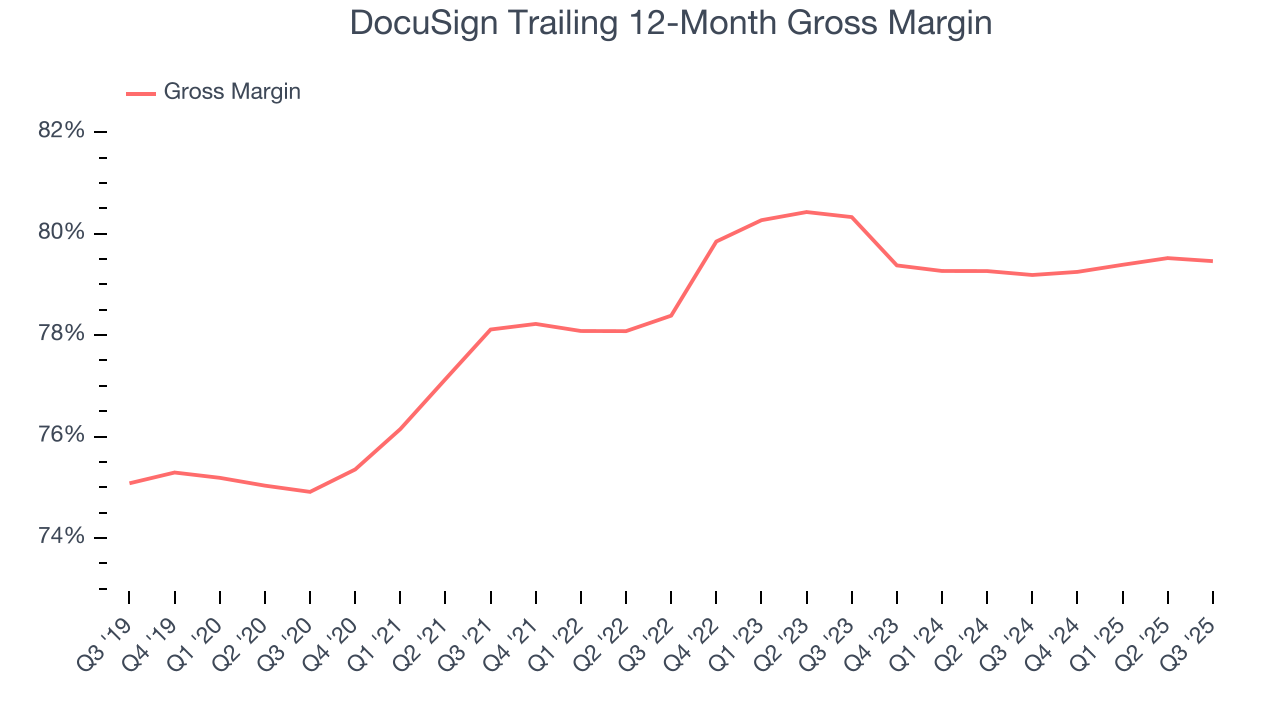

8. Gross Margin & Pricing Power

For software companies like DocuSign, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

DocuSign’s robust unit economics are better than the broader software industry, an output of its asset-lite business model and pricing power. They also enable the company to fund large investments in new products and sales during periods of rapid growth to achieve higher profits in the future. As you can see below, it averaged an excellent 79.5% gross margin over the last year. That means DocuSign only paid its providers $20.54 for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. DocuSign has seen gross margins decline by 0.9 percentage points over the last 2 year, which is poor compared to software peers.

In Q3, DocuSign produced a 79.2% gross profit margin, in line with the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

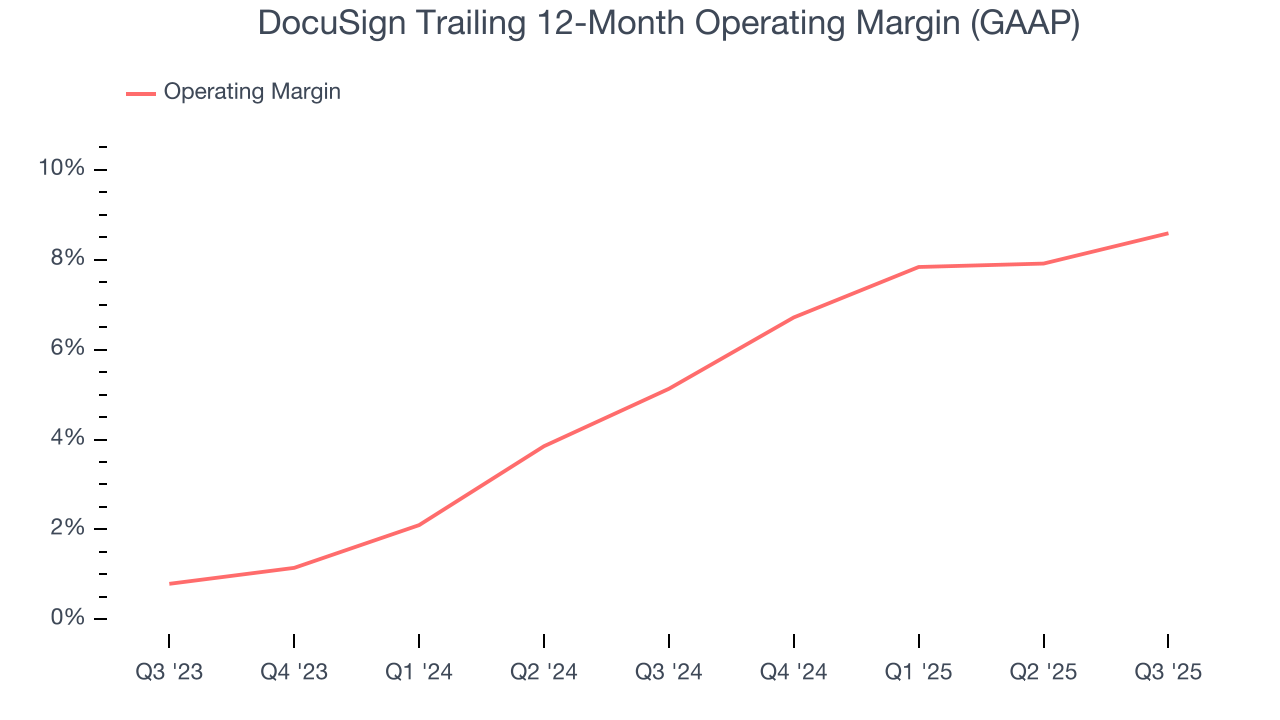

9. Operating Margin

While many software businesses point investors to their adjusted profits, which exclude stock-based compensation (SBC), we prefer GAAP operating margin because SBC is a legitimate expense used to attract and retain talent. This is one of the best measures of profitability because it shows how much money a company takes home after developing, marketing, and selling its products.

DocuSign has been an efficient company over the last year. It was one of the more profitable businesses in the software sector, boasting an average operating margin of 8.6%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, DocuSign’s operating margin rose by 3.5 percentage points over the last two years, as its sales growth gave it operating leverage.

In Q3, DocuSign generated an operating margin profit margin of 10.4%, up 2.6 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

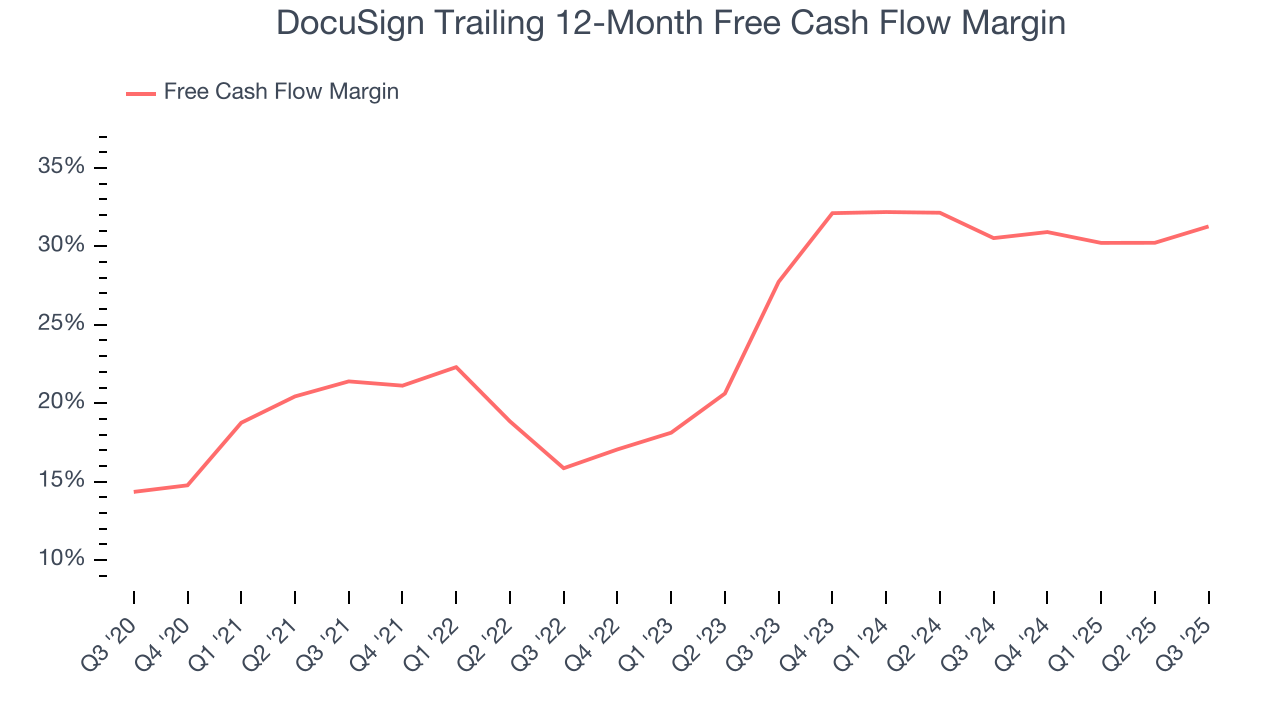

10. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

DocuSign has shown terrific cash profitability, driven by its lucrative business model and cost-effective customer acquisition strategy that enable it to stay ahead of the competition through investments in new products rather than sales and marketing. The company’s free cash flow margin was among the best in the software sector, averaging an eye-popping 31.3% over the last year.

DocuSign’s free cash flow clocked in at $262.9 million in Q3, equivalent to a 32.1% margin. This result was good as its margin was 4.2 percentage points higher than in the same quarter last year, but we wouldn’t put too much weight on the short term because investment needs can be seasonal, causing temporary swings. Long-term trends carry greater meaning.

Over the next year, analysts’ consensus estimates show they’re expecting DocuSign’s free cash flow margin of 31.3% for the last 12 months to remain the same.

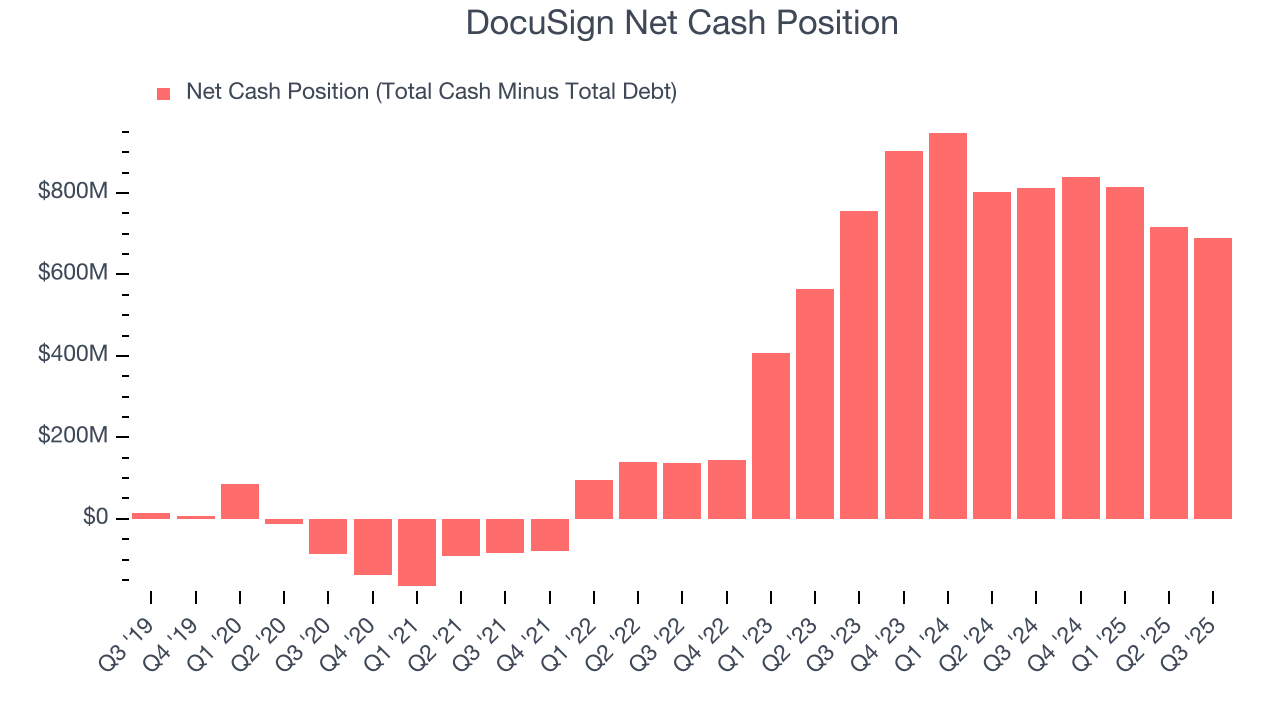

11. Balance Sheet Assessment

Companies with more cash than debt have lower bankruptcy risk.

DocuSign is a profitable, well-capitalized company with $839.9 million of cash and $150.4 million of debt on its balance sheet. This $689.5 million net cash position is 4.8% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from DocuSign’s Q3 Results

We enjoyed seeing DocuSign beat analysts’ billings expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. Overall, this print had some key positives. Investors were likely hoping for more, and shares traded down 1.4% to $70.25 immediately following the results.

13. Is Now The Time To Buy DocuSign?

Updated: February 17, 2026 at 9:01 PM EST

Before investing in or passing on DocuSign, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

DocuSign’s business quality ultimately falls short of our standards. Although its revenue growth was solid over the last five years, it’s expected to deteriorate over the next 12 months and its ARR has disappointed and shows the company is having difficulty retaining customers and their spending. And while the company’s efficient sales strategy allows it to target and onboard new users at scale, the downside is its expanding operating margin shows it’s becoming more efficient at building and selling its software.

DocuSign’s price-to-sales ratio based on the next 12 months is 2.8x. While this valuation is fair, the upside isn’t great compared to the potential downside. We're pretty confident there are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $83.78 on the company (compared to the current share price of $45.09).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.