Domo (DOMO)

Domo keeps us up at night. Its underwhelming revenue growth and failure to generate meaningful free cash flow is a concerning trend.― StockStory Analyst Team

1. News

2. Summary

Why We Think Domo Will Underperform

Named for the Japanese word meaning "thank you very much," Domo (NASDAQ:DOMO) provides a cloud-based business intelligence platform that connects people with real-time data and insights across organizations.

- Customers had second thoughts about committing to its platform over the last year as its average billings growth of 2% underwhelmed

- Estimated sales for the next 12 months are flat and imply a softer demand environment

- Extended payback periods on sales investments suggest the company’s platform isn’t resonating enough to drive efficient sales conversions

Domo’s quality is lacking. We’re on the lookout for more interesting opportunities.

Why There Are Better Opportunities Than Domo

Domo’s stock price of $3.60 implies a valuation ratio of 0.5x forward price-to-sales. This is a cheap valuation multiple, but for good reason. You get what you pay for.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. Domo (DOMO) Research Report: Q4 CY2025 Update

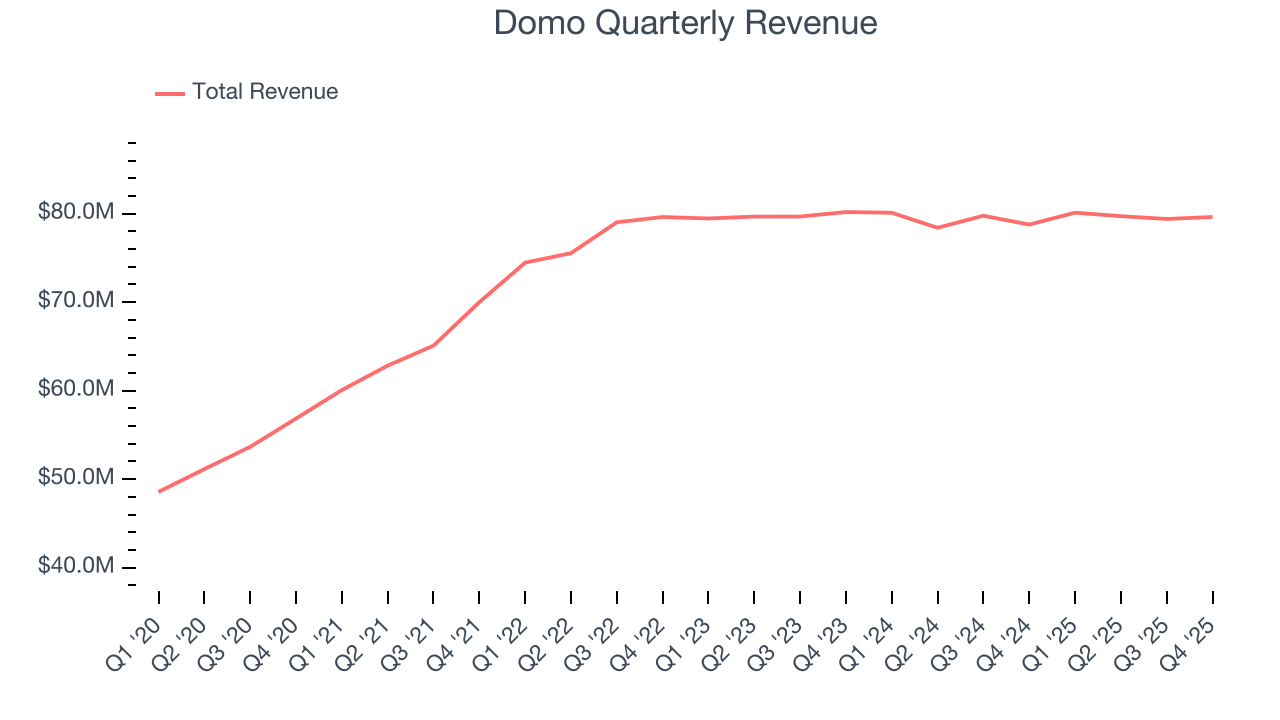

Business intelligence platform Domo (NASDAQ:DOMO) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 1.1% year on year to $79.63 million. Its non-GAAP profit of $0.03 per share was significantly above analysts’ consensus estimates.

Domo (DOMO) Q4 CY2025 Highlights:

- Revenue: $79.63 million vs analyst estimates of $78.62 million (1.1% year-on-year growth, 1.3% beat)

- Adjusted EPS: $0.03 vs analyst estimates of -$0.03 (significant beat)

- Adjusted Operating Income: $8.13 million vs analyst estimates of $3.86 million (10.2% margin, significant beat)

- Operating Margin: -13.3%, up from -15.6% in the same quarter last year

- Free Cash Flow was -$5.34 million, down from $2.07 million in the previous quarter

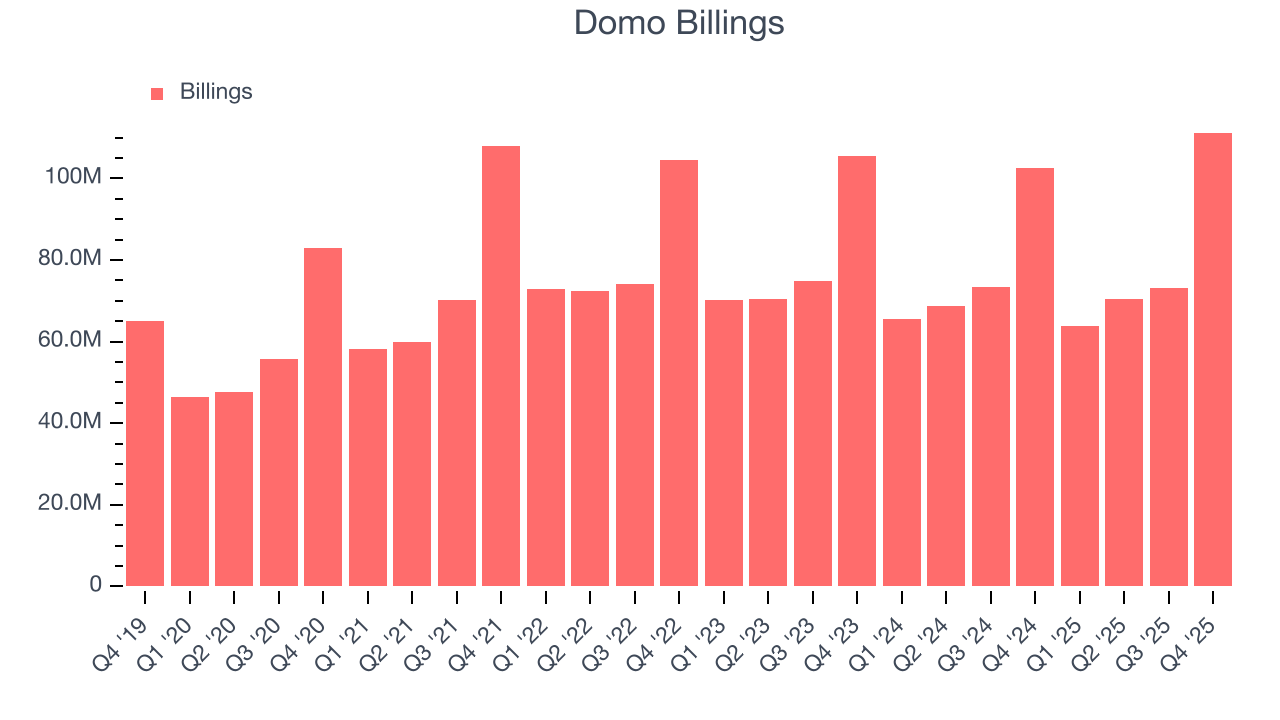

- Billings: $111.2 million at quarter end, up 8.4% year on year

- Market Capitalization: $178.5 million

Company Overview

Named for the Japanese word meaning "thank you very much," Domo (NASDAQ:DOMO) provides a cloud-based business intelligence platform that connects people with real-time data and insights across organizations.

Domo's platform addresses the fragmentation problem in business intelligence by unifying seven core functions into a single solution: data connection, storage, preparation, analysis, visualization, collaboration, and AI-powered insights. The platform can connect to over 1,000 data sources through pre-built connectors, allowing organizations to integrate information from disparate systems without extensive technical knowledge.

What makes Domo particularly valuable is its accessibility across all organizational levels. From C-suite executives to frontline employees, users can access relevant data through intuitive dashboards on both desktop and mobile devices. For example, a retail manager can use Domo on their smartphone to instantly view store performance metrics while walking the sales floor, filtering data to identify specific product line issues and sharing insights with their team in real-time.

Domo's platform includes "Magic ETL," a low-code tool that allows users to transform and blend data without specialized programming skills. The system also features built-in AI capabilities, enabling predictive analytics, anomaly detection, and natural language processing. Customers can deploy these capabilities through a simple drag-and-drop interface or leverage more advanced options like custom Python and R scripting for specialized needs.

The company monetizes its platform through subscription-based pricing, with fees determined by feature packages or usage levels. Typically entering organizations through a specific department or use case, Domo expands its footprint as more users recognize its value and capabilities, following a "land, expand, and retain" business model. Domo also offers embedded analytics through "Domo Everywhere," allowing organizations to securely share data visualizations with external partners and customers.

4. Data Analytics

Organizations generate a lot of data that is stored in silos, often in incompatible formats, making it slow and costly to extract actionable insights, which in turn drives demand for modern cloud-based data analysis platforms that can efficiently analyze the siloed data.

Domo competes with large enterprise software providers like Microsoft, Oracle, SAP, Salesforce, and IBM. In the specialized business analytics space, it faces competition from Tableau (owned by Salesforce), Qlik, Looker (owned by Google), MicroStrategy, ThoughtSpot, Sisense, and Tibco Software.

5. Revenue Growth

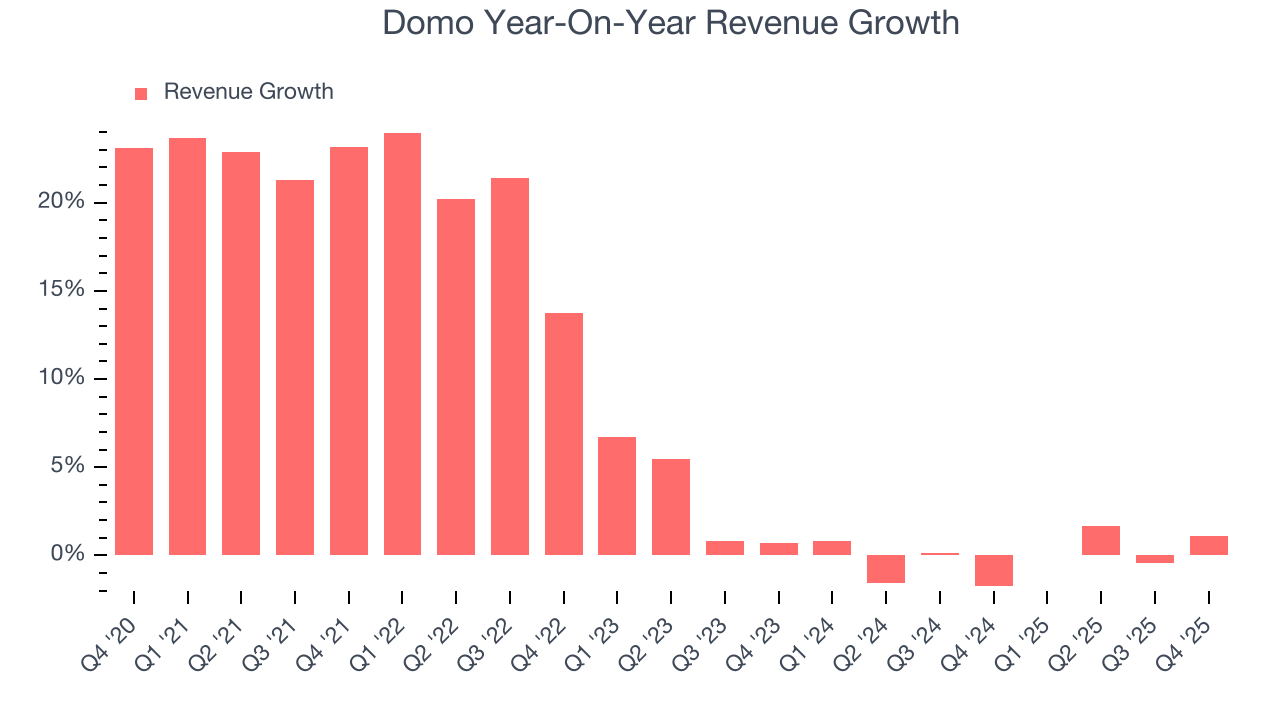

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years. Regrettably, Domo’s sales grew at a sluggish 8.7% compounded annual growth rate over the last five years. This fell short of our benchmark for the software sector and is a tough starting point for our analysis.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. Domo’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

This quarter, Domo reported modest year-on-year revenue growth of 1.1% but beat Wall Street’s estimates by 1.3%.

Looking ahead, sell-side analysts expect revenue to grow 2.3% over the next 12 months. While this projection suggests its newer products and services will fuel better top-line performance, it is still below average for the sector.

6. Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Domo’s billings came in at $111.2 million in Q4, and over the last four quarters, its growth was underwhelming as it averaged 2% year-on-year increases. This performance mirrored its total sales and suggests that increasing competition is causing challenges in acquiring/retaining customers.

7. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Domo’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its incremental sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a highly competitive environment where there is little differentiation between Domo’s products and its peers.

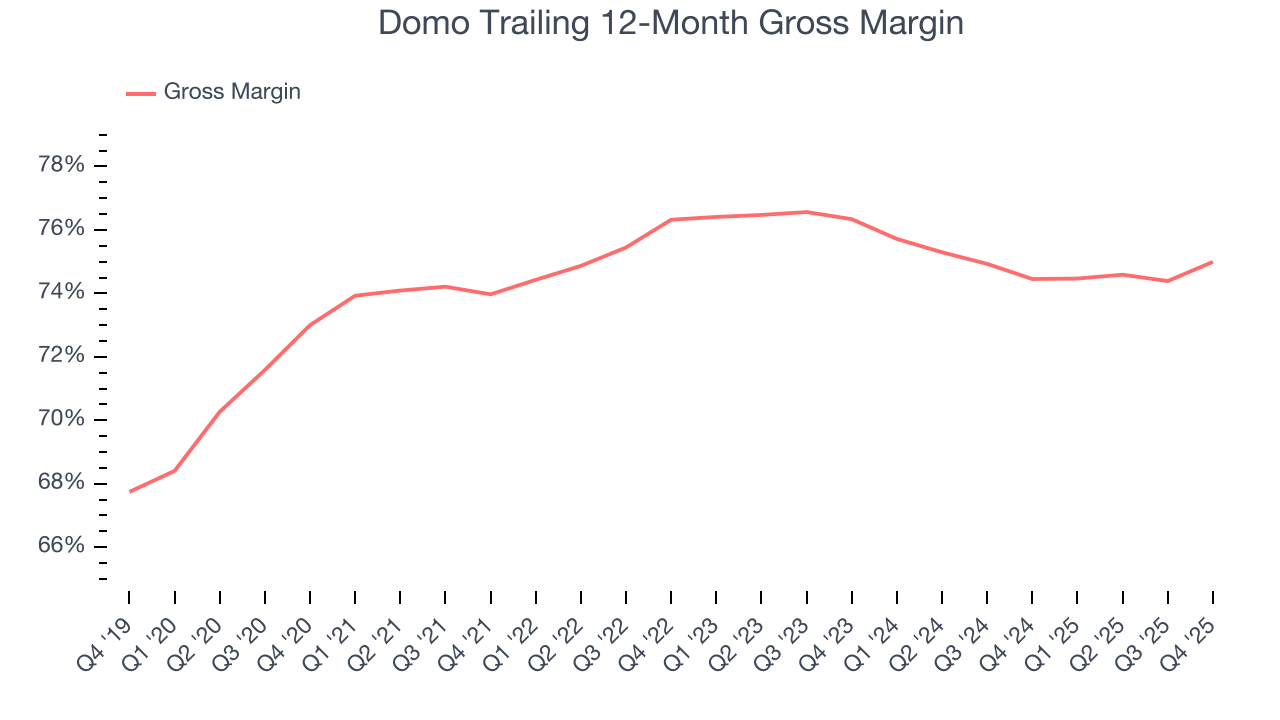

8. Gross Margin & Pricing Power

For software companies like Domo, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Domo’s gross margin is better than the broader software industry and signals it has solid unit economics and competitive products. As you can see below, it averaged a decent 75% gross margin over the last year. That means for every $100 in revenue, roughly $74.99 was left to spend on selling, marketing, and R&D.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Domo has seen gross margins decline by 1.3 percentage points over the last 2 year, which is poor compared to software peers.

This quarter, Domo’s gross profit margin was 76.8% , marking a 2.4 percentage point increase from 74.4% in the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

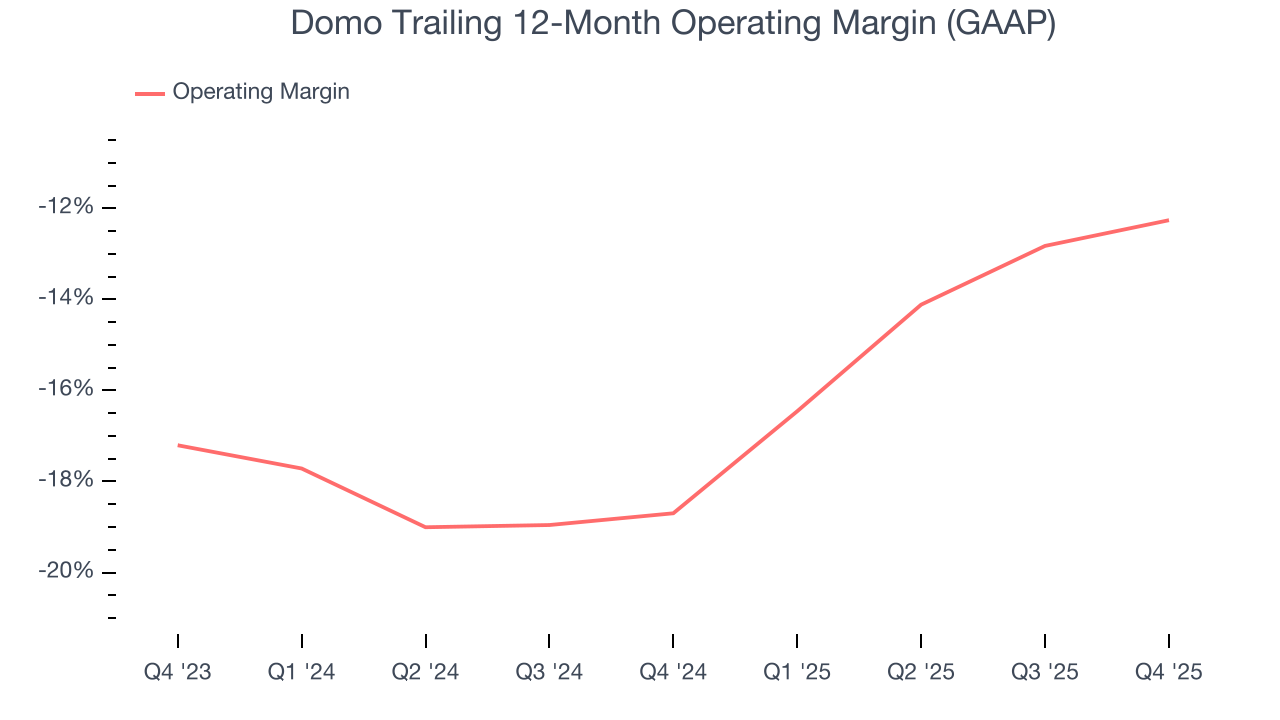

9. Operating Margin

While many software businesses point investors to their adjusted profits, which exclude stock-based compensation (SBC), we prefer GAAP operating margin because SBC is a legitimate expense used to attract and retain talent. This metric shows how much revenue remains after accounting for all core expenses – everything from the cost of goods sold to sales and R&D.

Domo’s expensive cost structure has contributed to an average operating margin of negative 12.3% over the last year. Unprofitable software companies require extra attention because they spend heaps of money to capture market share. As seen in its historically underwhelming revenue performance, this strategy hasn’t worked so far, and it’s unclear what would happen if Domo reeled back its investments. Wall Street seems to think it will face some obstacles, and we tend to agree.

Over the last two years, Domo’s expanding sales gave it operating leverage as its margin rose by 6.4 percentage points. Still, it will take much more for the company to reach long-term profitability.

In Q4, Domo generated a negative 13.3% operating margin. The company's consistent lack of profits raise a flag.

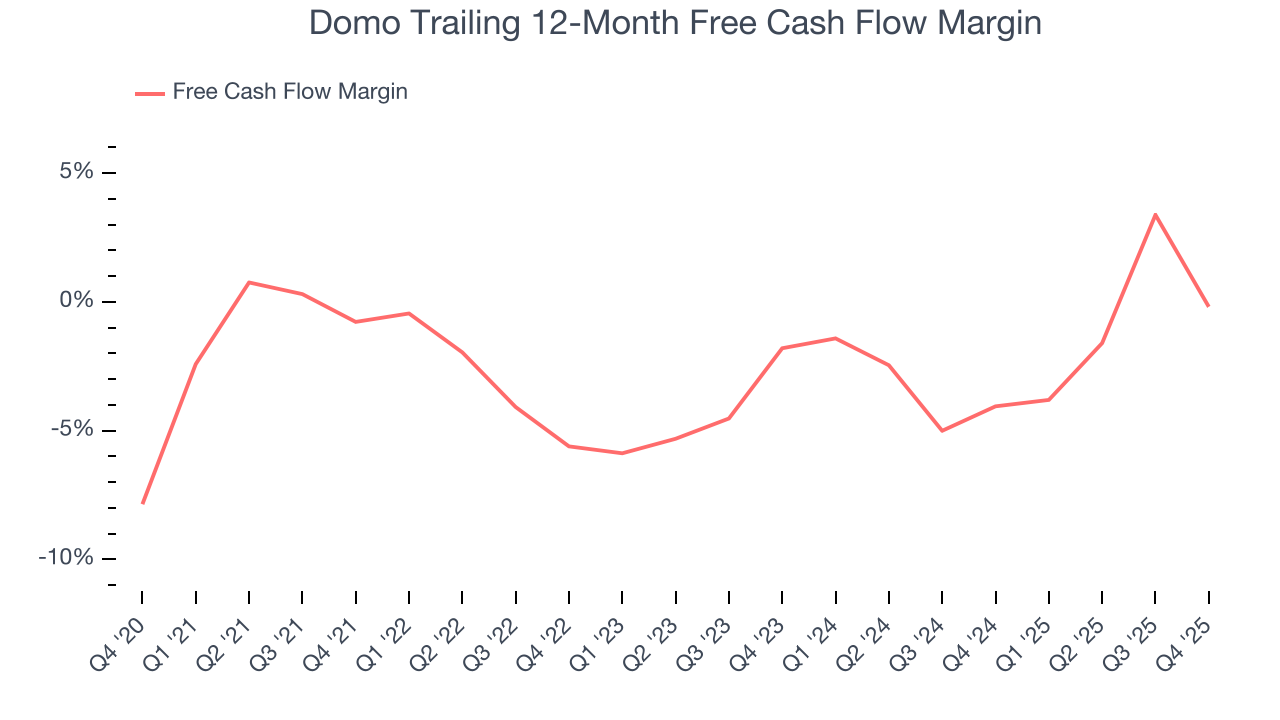

10. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Domo broke even from a free cash flow perspective over the last year, giving the company limited opportunities to return capital to shareholders.

Domo burned through $5.34 million of cash in Q4, equivalent to a negative 6.7% margin. The company’s cash flow turned negative after being positive in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

Over the next year, analysts predict Domo’s cash conversion will improve. Their consensus estimates imply its breakeven free cash flow margin for the last 12 months will increase to 2.6%, giving it more money to invest.

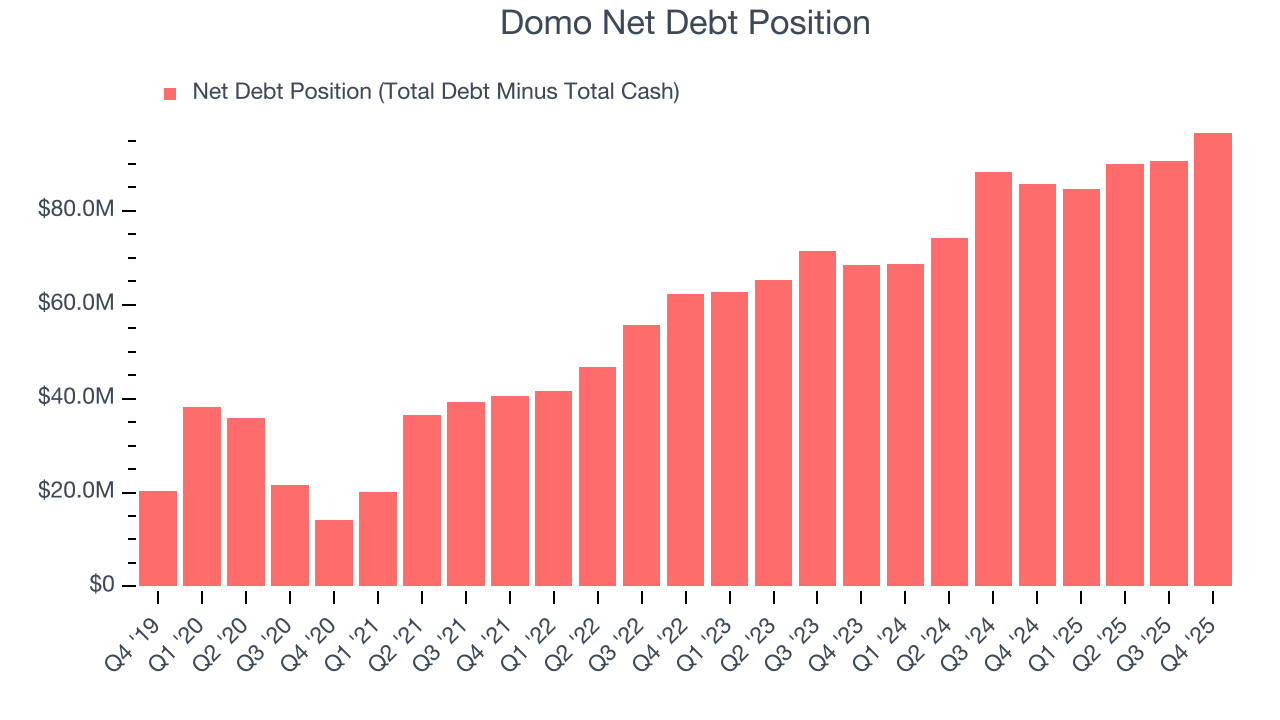

11. Balance Sheet Assessment

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Domo burned through $604,000 of cash over the last year. Although the company has $139.6 million of debt on its balance sheet, we think its $42.95 million of cash gives it enough runway (we typically look for at least two years) to prioritize growth over profitability.

12. Key Takeaways from Domo’s Q4 Results

It was encouraging to see Domo beat analysts’ billings expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 31.3% to $5.76 immediately following the results.

13. Is Now The Time To Buy Domo?

Updated: March 20, 2026 at 10:29 PM EDT

Before investing in or passing on Domo, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

Domo falls short of our quality standards. To kick things off, its revenue growth was weak over the last five years, and analysts expect its demand to deteriorate over the next 12 months. While its gross margin suggests it can generate sustainable profits, the downside is its customer acquisition is less efficient than many comparable companies. On top of that, its operating margins reveal poor profitability compared to other software companies.

Domo’s price-to-sales ratio based on the next 12 months is 0.5x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $6.70 on the company (compared to the current share price of $3.60).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.