DexCom (DXCM)

We’re firm believers in DexCom. Its superior revenue growth and returns on capital show it can achieve fast and profitable expansion.― StockStory Analyst Team

1. News

2. Summary

Why We Like DexCom

Founded in 1999 and receiving its first FDA approval in 2006, DexCom (NASDAQ:DXCM) develops and sells continuous glucose monitoring systems that allow people with diabetes to track their blood sugar levels without repeated finger pricks.

- Incremental sales significantly boosted profitability as its annual earnings per share growth of 22.1% over the last five years outstripped its revenue performance

- Industry-leading 23.7% return on capital demonstrates management’s skill in finding high-return investments, and its rising returns show it’s making even more lucrative bets

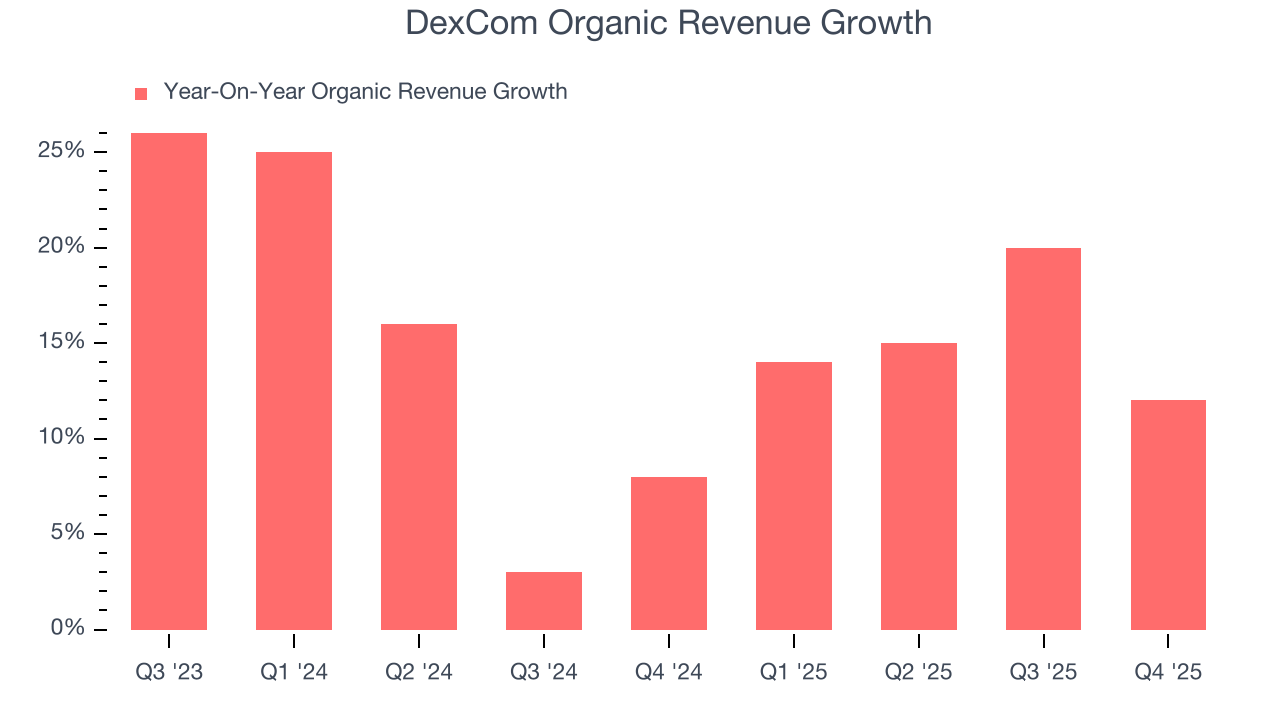

- Core business is healthy and doesn’t need acquisitions to boost sales as its organic revenue growth averaged 14.1% over the past two years

DexCom is a market leader. The valuation seems fair relative to its quality, so this might be an opportune time to buy some shares.

Why Is Now The Time To Buy DexCom?

DexCom is trading at $61.86 per share, or 25x forward P/E. Valuation is above that of many healthcare companies, but we think the price is justified given its business fundamentals.

By definition, where you buy a stock impacts returns. Still, our extensive analysis shows that investors should worry much more about business quality than entry price if the ultimate goal is long-term returns.

3. DexCom (DXCM) Research Report: Q4 CY2025 Update

Medical device company DexCom (NASDAQ:DXCM) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 13.1% year on year to $1.26 billion. The company expects the full year’s revenue to be around $5.21 billion, close to analysts’ estimates. Its non-GAAP profit of $0.68 per share was 4.5% above analysts’ consensus estimates.

DexCom (DXCM) Q4 CY2025 Highlights:

- Revenue: $1.26 billion vs analyst estimates of $1.25 billion (13.1% year-on-year growth, 0.8% beat)

- Adjusted EPS: $0.68 vs analyst estimates of $0.65 (4.5% beat)

- Adjusted EBITDA: $422.2 million vs analyst estimates of $425.5 million (33.5% margin, 0.8% miss)

- Operating Margin: 25.6%, up from 17% in the same quarter last year

- Organic Revenue rose 12% year on year (beat)

- Market Capitalization: $26.58 billion

Company Overview

Founded in 1999 and receiving its first FDA approval in 2006, DexCom (NASDAQ:DXCM) develops and sells continuous glucose monitoring systems that allow people with diabetes to track their blood sugar levels without repeated finger pricks.

DexCom's continuous glucose monitoring (CGM) technology consists of a small sensor inserted under the skin, a transmitter that sends data wirelessly, and a display device that shows real-time glucose readings. Unlike traditional glucose meters that provide only periodic snapshots of blood sugar levels, DexCom's systems track glucose levels continuously throughout the day and night, providing users with trend information and alerts for high or low readings.

The company's flagship products include the G6 and newer G7 systems, which are classified as integrated continuous glucose monitoring systems (iCGMs) by the FDA. These devices can communicate directly with compatible smartphones and smartwatches, allowing users to discreetly monitor their glucose levels. The data can also be shared with healthcare providers or family members through DexCom's Share remote monitoring system, enabling caregivers to receive alerts about a patient's glucose levels.

A person with Type 1 diabetes might use a DexCom CGM to monitor how their glucose levels respond to meals, exercise, and insulin doses throughout the day. The system would alert them before their glucose reaches dangerously high or low levels, allowing them to take corrective action before experiencing symptoms.

DexCom generates revenue primarily through the recurring sale of disposable sensors, which are replaced every 10 days, while transmitters are replaced approximately every three months. The company's products are covered by Medicare, Medicaid, and most commercial insurers in the United States for people with both Type 1 and Type 2 diabetes who meet certain eligibility criteria.

Beyond its core products, DexCom is expanding its offerings with Dexcom ONE, a simplified CGM system launched in several European countries, and Dexcom Stelo, designed specifically for people with Type 2 diabetes who don't use insulin. The company has also established partnerships with insulin delivery system manufacturers to integrate its CGM technology with insulin pumps and pens, supporting the development of automated insulin delivery systems.

4. Patient Monitoring

Patient monitoring companies within the healthcare equipment industry offer devices and technologies that track chronic conditions and support real-time health management, such as continuous glucose monitors (CGMs) and sleep apnea machines. These businesses benefit from recurring revenue from consumables and software subscriptions tied to device sales (razor, razor blade model). The rising prevalence of chronic diseases like diabetes and respiratory disorders due to an aging population as well as growing adoption of digitization are good for the industry. However, these companies face challenges from high R&D costs and reliance on regulatory approvals. Looking ahead, the sector is positioned for growth due to tailwinds like the rising burden of chronic diseases from an aging population, the shift toward value-based care, and increased adoption of digital health solutions. Innovations in AI and machine learning are expected to enhance device accuracy and functionality, improving patient outcomes and driving demand. However, there are headwinds such as pricing pressures as healthcare costs are a key focus, especially in the US. An evolving regulatory landscape and competition from more tech-forward new entrants could present additional challenges.

DexCom's primary competitors in the continuous glucose monitoring market include Abbott Laboratories' Diabetes Care division (NYSE:ABT) with its FreeStyle Libre system, Medtronic's Diabetes Group (NYSE:MDT), and privately-held companies like LifeScan and Ascensia Diabetes Care.

5. Economies of Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $4.66 billion in revenue over the past 12 months, DexCom has decent scale. This is important as it gives the company more leverage in a heavily regulated, competitive environment that is complex and resource-intensive.

6. Revenue Growth

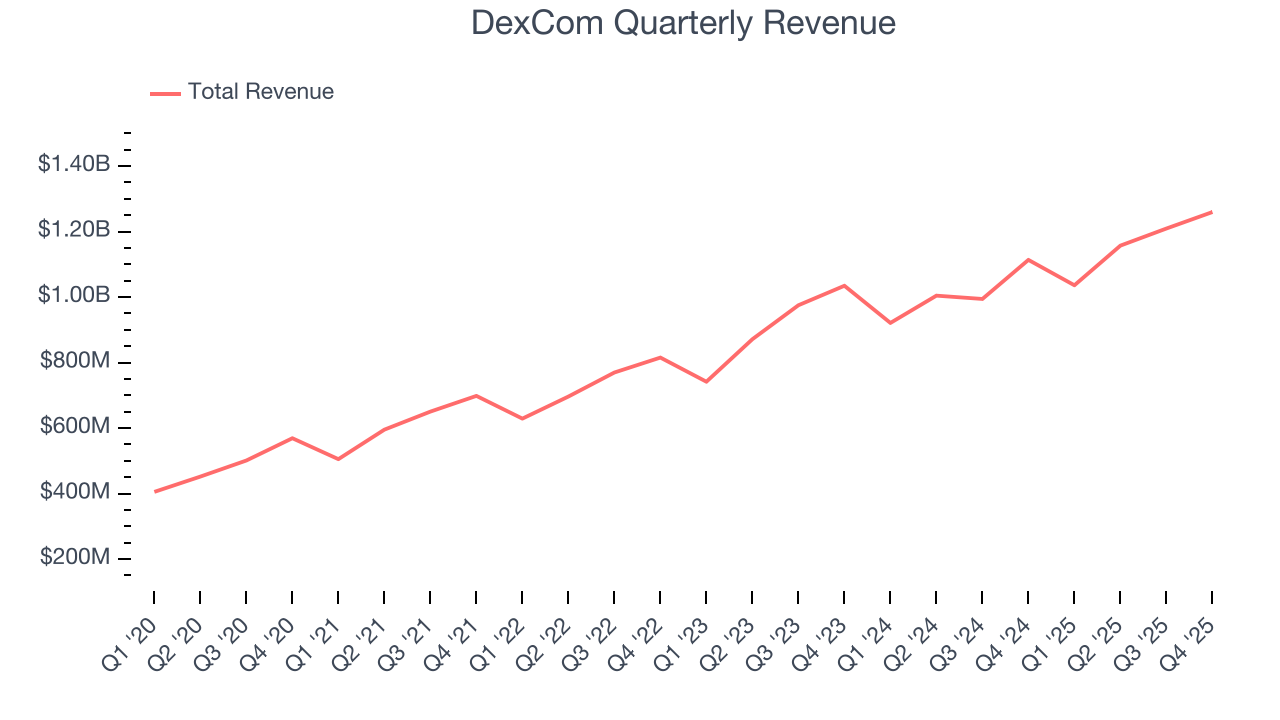

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, DexCom grew its sales at an impressive 19.3% compounded annual growth rate. Its growth surpassed the average healthcare company and shows its offerings resonate with customers, a great starting point for our analysis.

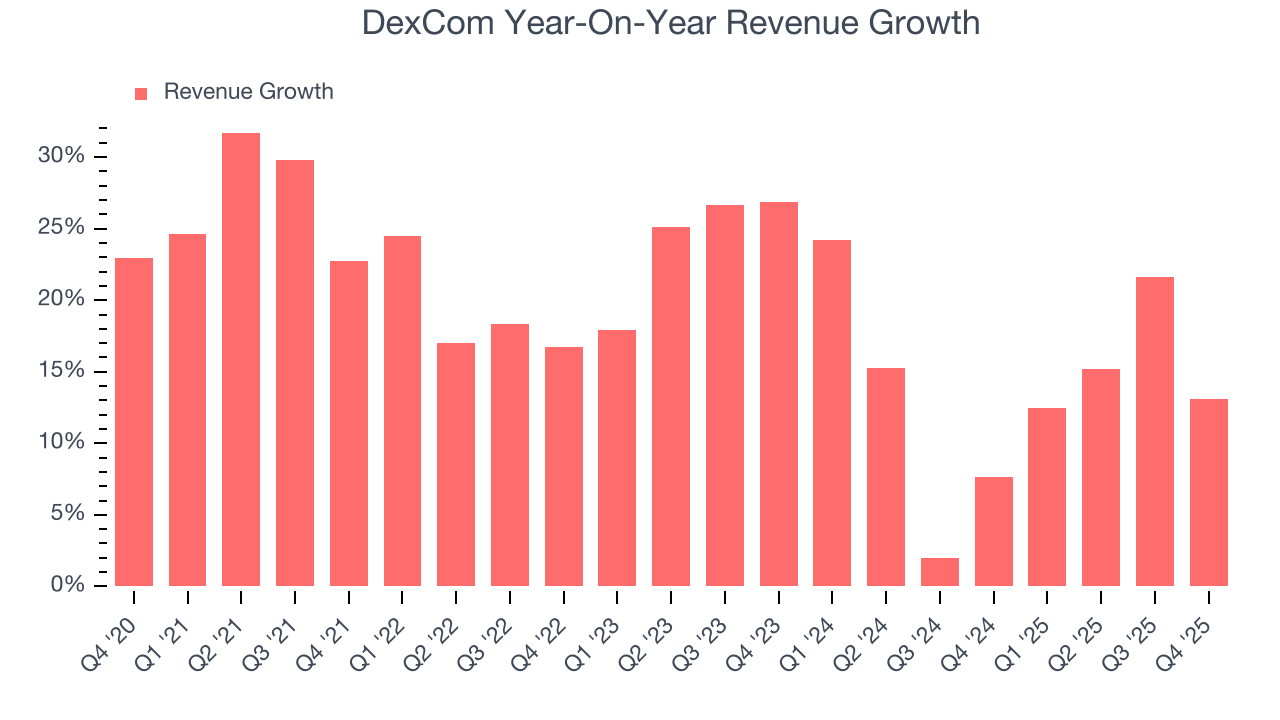

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. DexCom’s annualized revenue growth of 13.4% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

DexCom also reports organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, DexCom’s organic revenue averaged 14.1% year-on-year growth. Because this number aligns with its two-year revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, DexCom reported year-on-year revenue growth of 13.1%, and its $1.26 billion of revenue exceeded Wall Street’s estimates by 0.8%.

Looking ahead, sell-side analysts expect revenue to grow 12.3% over the next 12 months, similar to its two-year rate. Still, this projection is admirable and indicates the market is baking in success for its products and services.

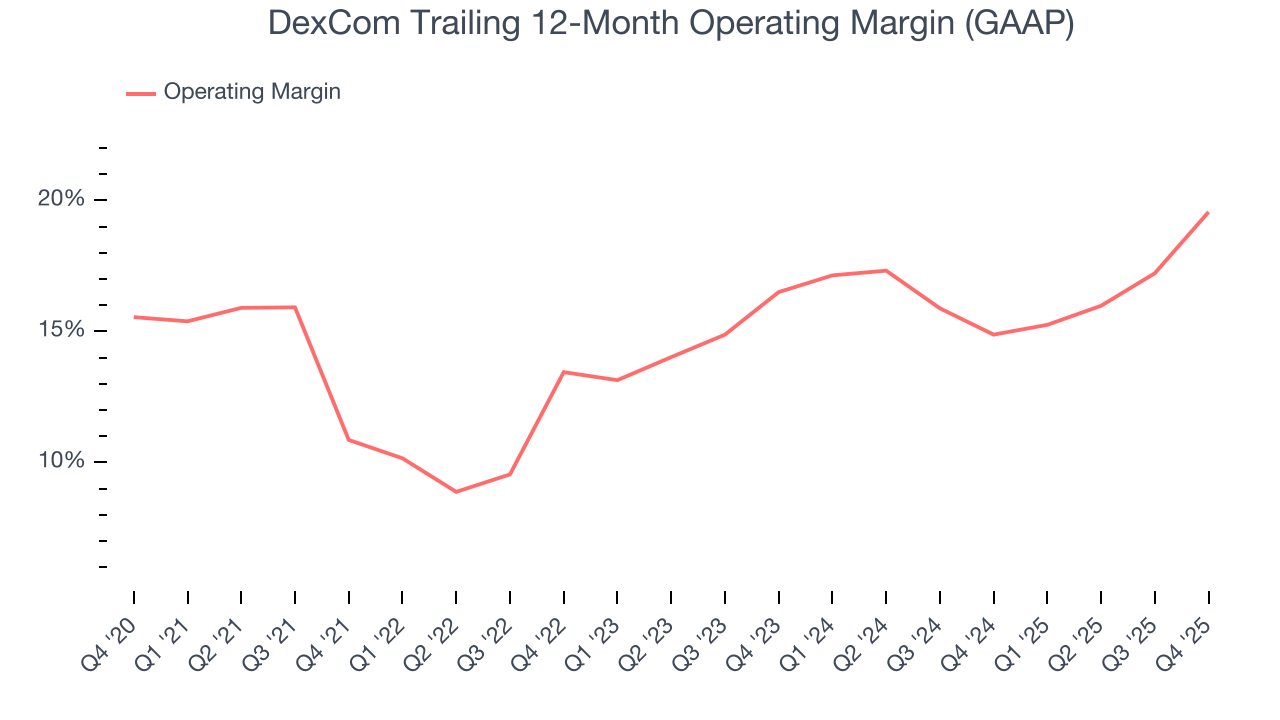

7. Operating Margin

DexCom has managed its cost base well over the last five years. It demonstrated solid profitability for a healthcare business, producing an average operating margin of 15.7%.

Looking at the trend in its profitability, DexCom’s operating margin rose by 8.7 percentage points over the last five years, as its sales growth gave it operating leverage. Zooming in on its more recent performance, we can see the company’s trajectory is intact as its margin has also increased by 3.1 percentage points on a two-year basis. These data points are very encouraging and show momentum is on its side.

In Q4, DexCom generated an operating margin profit margin of 25.6%, up 8.7 percentage points year on year. This increase was a welcome development and shows it was more efficient.

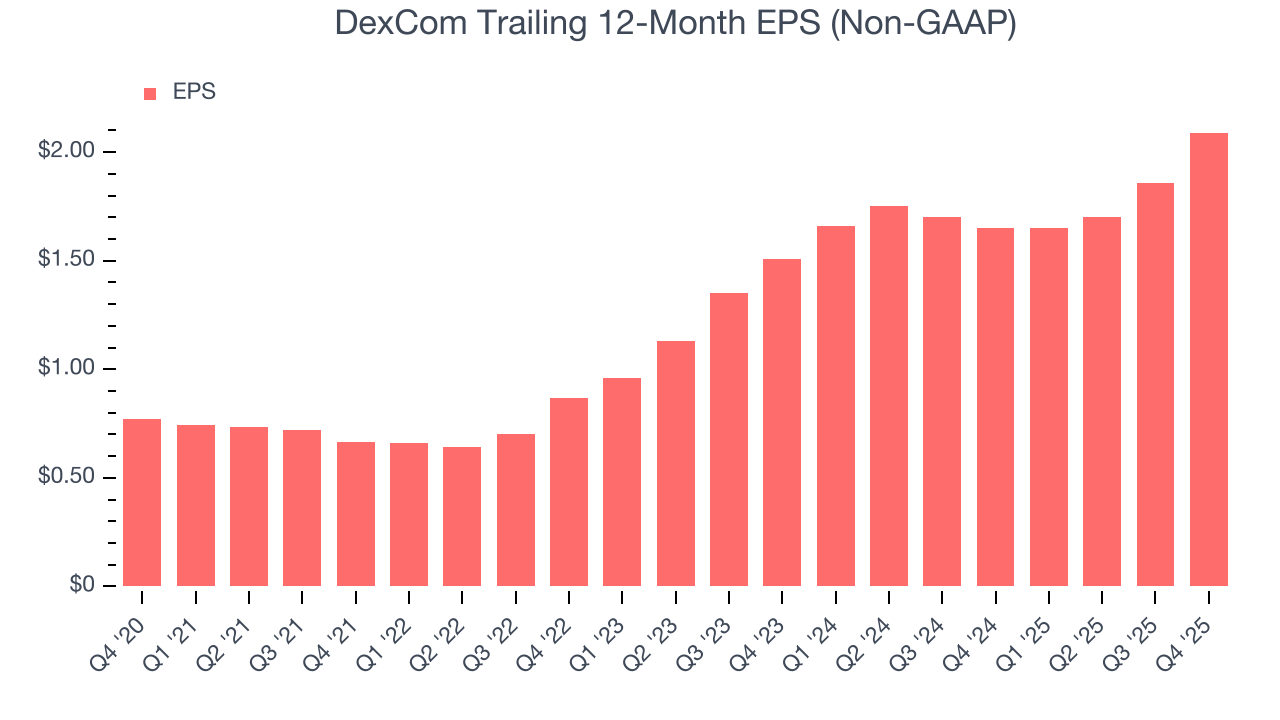

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

DexCom’s EPS grew at an astounding 22.1% compounded annual growth rate over the last five years, higher than its 19.3% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

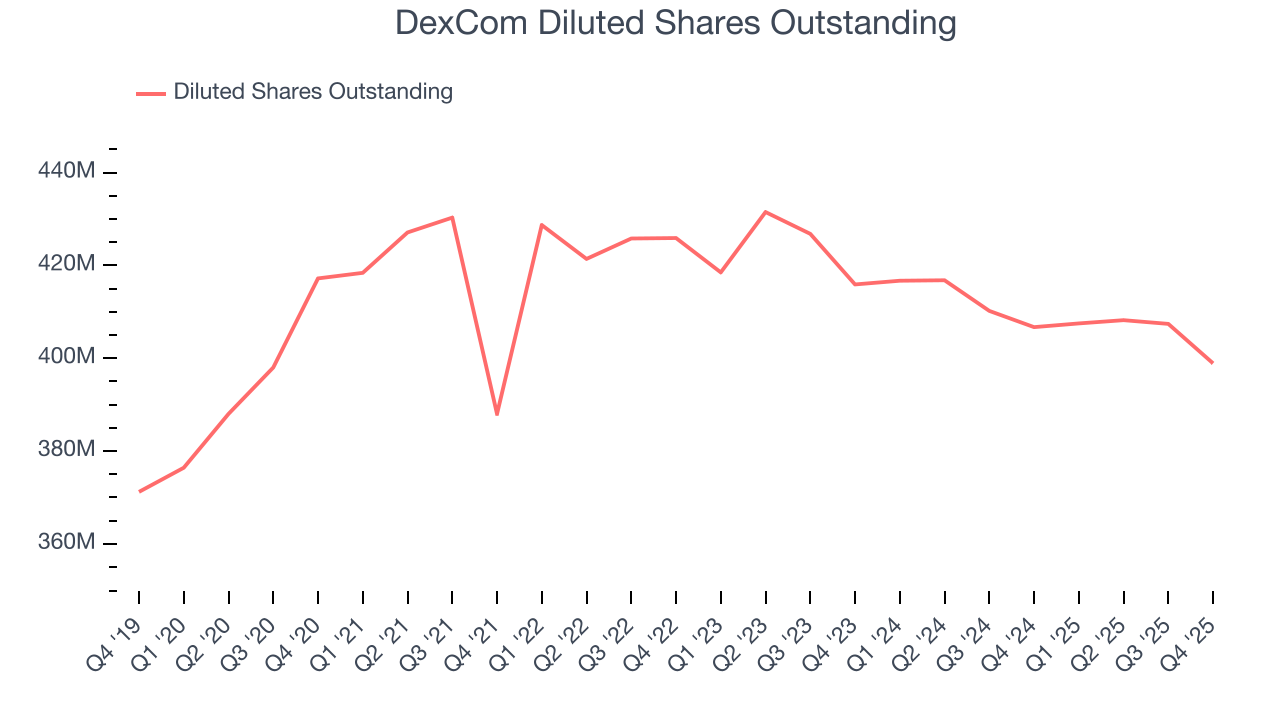

We can take a deeper look into DexCom’s earnings to better understand the drivers of its performance. As we mentioned earlier, DexCom’s operating margin expanded by 8.7 percentage points over the last five years. On top of that, its share count shrank by 4.4%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

In Q4, DexCom reported adjusted EPS of $0.68, up from $0.45 in the same quarter last year. This print beat analysts’ estimates by 4.5%. Over the next 12 months, Wall Street expects DexCom’s full-year EPS of $2.09 to grow 18.4%.

9. Cash Is King

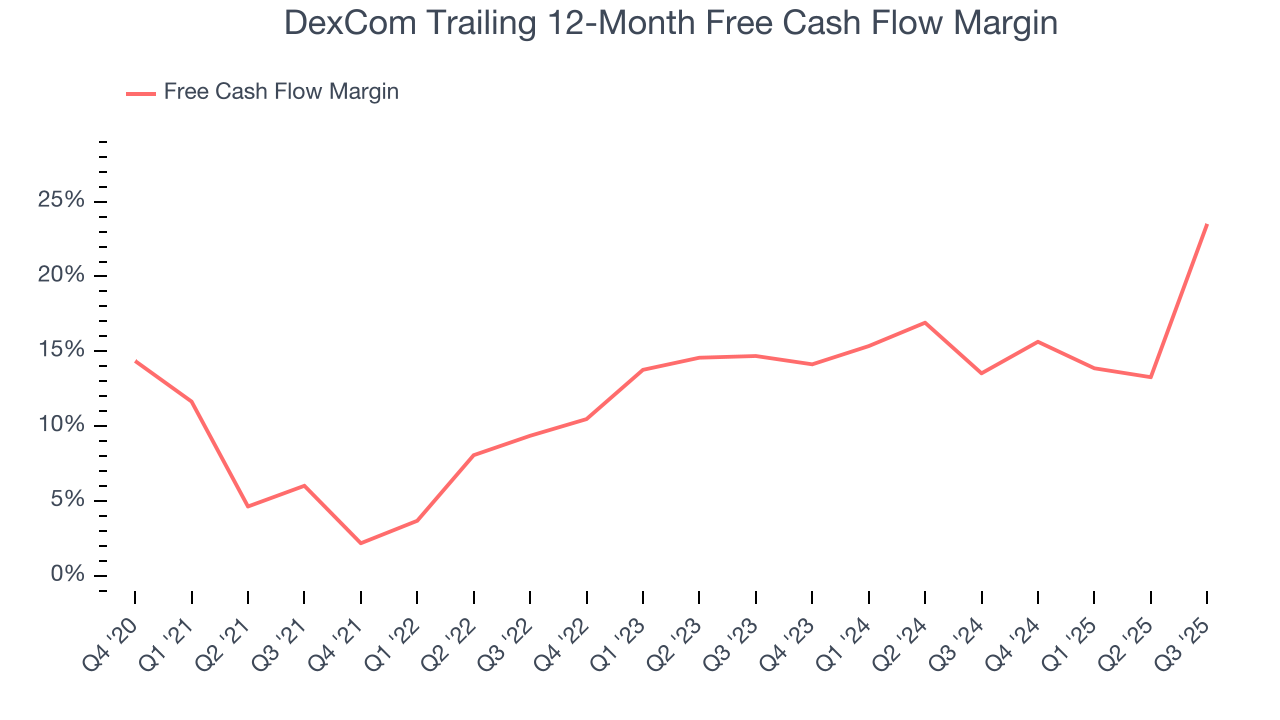

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

DexCom has shown impressive cash profitability, giving it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 14.5% over the last five years, better than the broader healthcare sector.

Taking a step back, we can see that DexCom’s margin expanded by 24.4 percentage points during that time. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

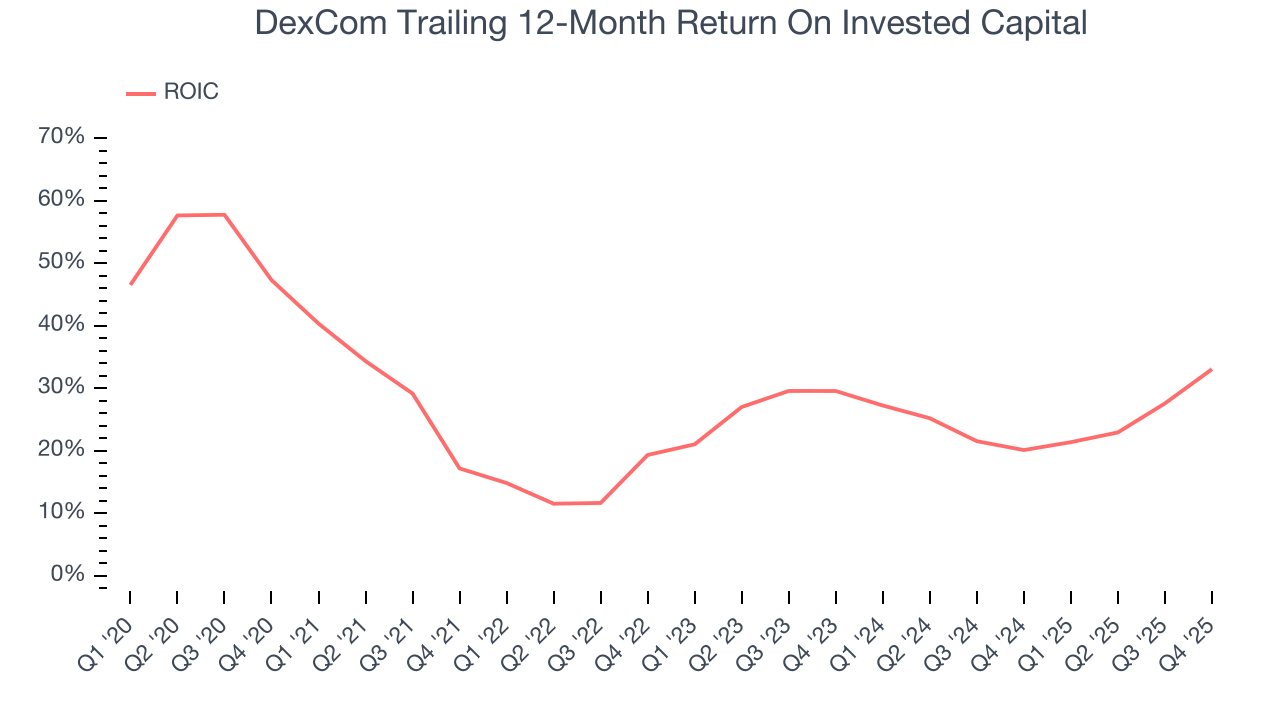

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

DexCom’s five-year average ROIC was 23.8%, placing it among the best healthcare companies. This illustrates its management team’s ability to invest in highly profitable ventures and produce tangible results for shareholders.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, DexCom’s ROIC has increased. This is a great sign when paired with its already strong returns. It could suggest its competitive advantage or profitable growth opportunities are expanding.

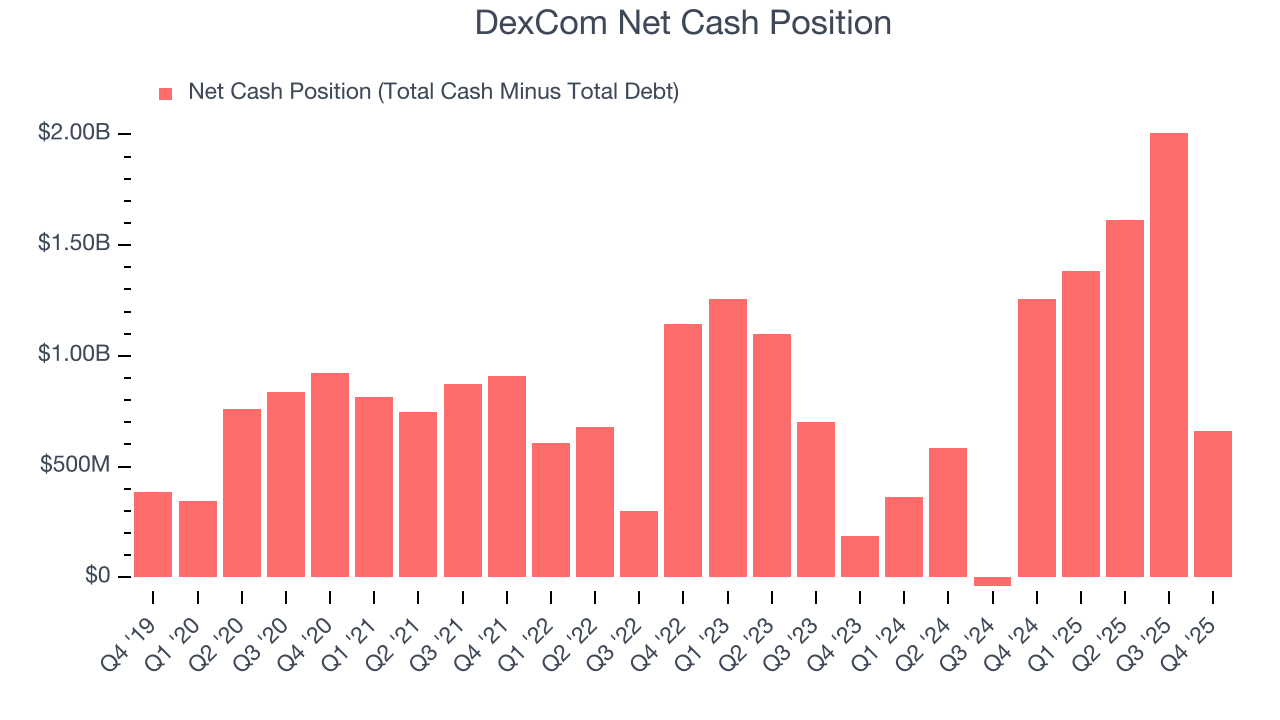

11. Balance Sheet Assessment

Companies with more cash than debt have lower bankruptcy risk.

DexCom is a profitable, well-capitalized company with $2.00 billion of cash and $1.34 billion of debt on its balance sheet. This $662.8 million net cash position is 2.5% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from DexCom’s Q4 Results

It was good to see DexCom beat analysts’ EPS expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. On the other hand, its full-year revenue guidance was in line. Zooming out, we think this was a mixed quarter. The stock remained flat at $65.12 immediately following the results.

13. Is Now The Time To Buy DexCom?

Updated: March 30, 2026 at 11:49 PM EDT

When considering an investment in DexCom, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

DexCom is a rock-solid business worth owning. First of all, the company’s revenue growth was impressive over the last five years. On top of that, its rising cash profitability gives it more optionality, and its astounding EPS growth over the last five years shows its profits are trickling down to shareholders.

DexCom’s P/E ratio based on the next 12 months is 25x. Looking across the spectrum of healthcare companies today, DexCom’s fundamentals shine bright. We like the stock at this price.

Wall Street analysts have a consensus one-year price target of $87.13 on the company (compared to the current share price of $61.86), implying they see 40.8% upside in buying DexCom in the short term.