Encore Capital Group (ECPG)

Encore Capital Group doesn’t impress us. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why Encore Capital Group Is Not Exciting

Operating in the often misunderstood world of debt collection since 1999, Encore Capital Group (NASDAQ:ECPG) purchases portfolios of defaulted consumer debt at deep discounts and works with individuals to recover these obligations while helping them toward financial recovery.

- Muted 3.3% annual revenue growth over the last five years shows its demand lagged behind its financials peers

- Low return on equity reflects management’s struggle to allocate funds effectively

- High net-debt-to-EBITDA ratio of 6× increases the risk of forced asset sales or dilutive financing if operational performance weakens

Encore Capital Group is in the doghouse. There are superior opportunities elsewhere.

Why There Are Better Opportunities Than Encore Capital Group

At $68.34 per share, Encore Capital Group trades at 5.7x forward P/E. Encore Capital Group’s valuation may seem like a great deal, but we think there are valid reasons why it’s so cheap.

We’d rather pay up for companies with elite fundamentals than get a bargain on weak ones. Cheap stocks can be value traps, and as their performance deteriorates, they will stay cheap or get even cheaper.

3. Encore Capital Group (ECPG) Research Report: Q4 CY2025 Update

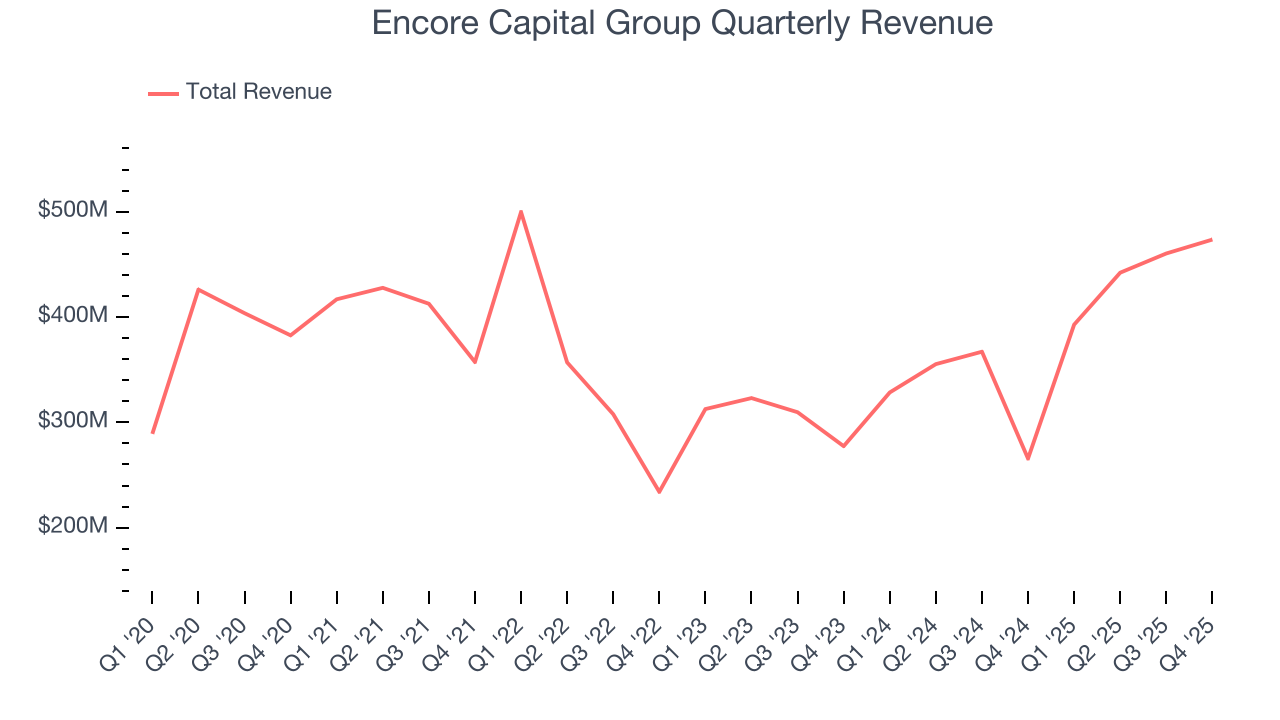

Debt recovery company Encore Capital Group (NASDAQ:ECPG) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 78.3% year on year to $473.6 million. Its GAAP profit of $3.37 per share was 51.1% above analysts’ consensus estimates.

Encore Capital Group (ECPG) Q4 CY2025 Highlights:

- Revenue: $473.6 million vs analyst estimates of $422.2 million (78.3% year-on-year growth, 12.2% beat)

- Pre-tax Profit: $97.82 million (20.7% margin)

- EPS (GAAP): $3.37 vs analyst estimates of $2.23 (51.1% beat)

- Market Capitalization: $1.29 billion

Company Overview

Operating in the often misunderstood world of debt collection since 1999, Encore Capital Group (NASDAQ:ECPG) purchases portfolios of defaulted consumer debt at deep discounts and works with individuals to recover these obligations while helping them toward financial recovery.

Encore operates primarily through two main business segments: Midland Credit Management (MCM) in the United States and Cabot Credit Management (CCM) in Europe, particularly the United Kingdom. The company acquires defaulted receivables—unpaid financial obligations to banks, credit unions, retailers, and other creditors—typically at 5-20% of face value, then attempts to collect on these accounts through various channels.

When Encore acquires a portfolio, it analyzes account-level data to develop tailored collection strategies for each consumer. These strategies include direct mail campaigns, call center outreach, digital communications, and sometimes legal action. For example, when a consumer with credit card debt falls behind on payments, the original lender might eventually sell that debt to Encore, which then contacts the consumer to establish a payment plan that fits their financial situation.

The company generates revenue by collecting more than it paid for the debt portfolios. Encore's approach varies based on consumers' ability and willingness to pay—those facing genuine hardships may receive modified payment plans, while those deemed able but unwilling to pay might face legal action. In addition to its core debt purchasing business, Encore provides debt servicing operations in Europe, where it manages collections for credit originators without purchasing the debt outright.

Encore's business model is heavily regulated, with operations subject to consumer protection laws like the Fair Debt Collection Practices Act in the U.S. and Financial Conduct Authority regulations in the UK. The company has also expanded into other markets, with investments in India and Mexico, though its primary focus remains on the U.S. and European markets.

4. Specialty Finance

Specialty finance companies provide targeted lending or financial services for specific industries or needs. They benefit from expertise in particular sectors, often reduced competition in specialized niches, and tailored underwriting that can yield higher margins. Challenges include concentration risk in specific industries, difficulty achieving scale efficiencies, and potential vulnerability during sector-specific downturns affecting their specialized markets.

Encore Capital Group's main competitors include PRA Group (NASDAQ:PRAA), Ares Management (NYSE:ARES), and Arrow Global Group, along with other debt buyers and collection agencies such as Portfolio Recovery Associates and Intrum.

5. Revenue Growth

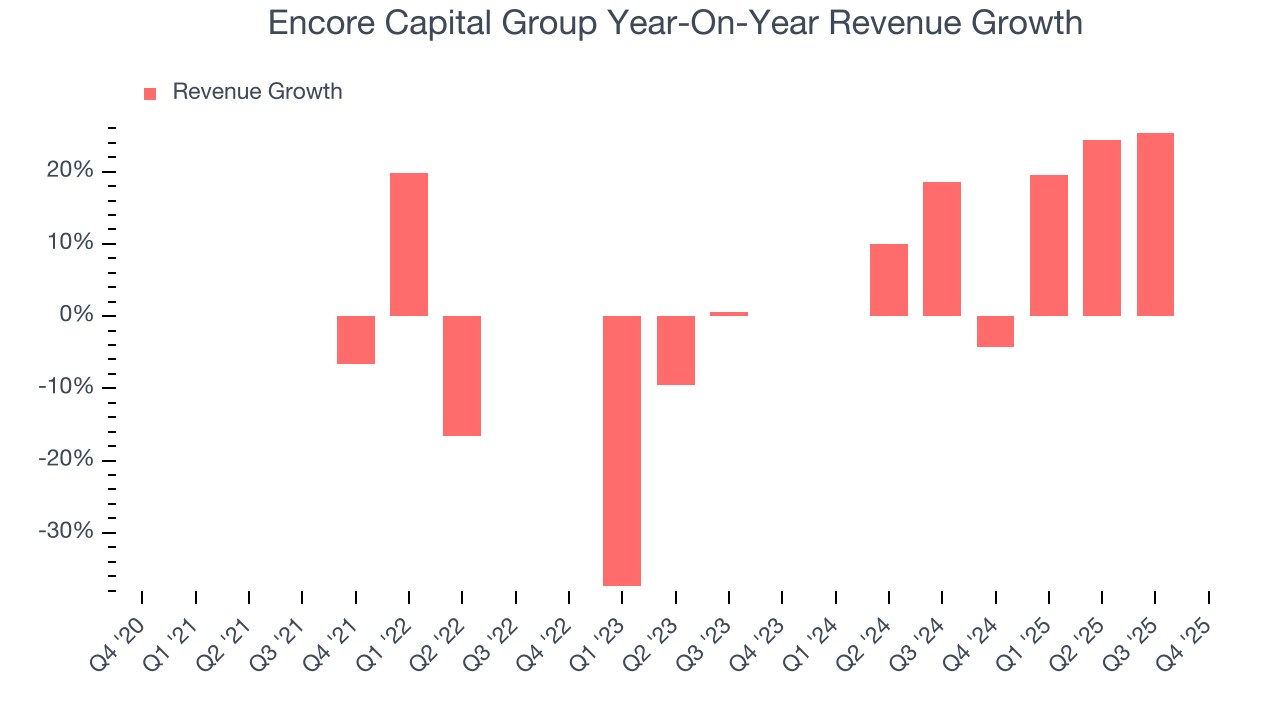

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, Encore Capital Group’s revenue grew at a sluggish 3.3% compounded annual growth rate over the last five years. This fell short of our benchmark for the financials sector and is a poor baseline for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Encore Capital Group’s annualized revenue growth of 20.3% over the last two years is above its five-year trend, suggesting its demand recently accelerated.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Encore Capital Group reported magnificent year-on-year revenue growth of 78.3%, and its $473.6 million of revenue beat Wall Street’s estimates by 12.2%.

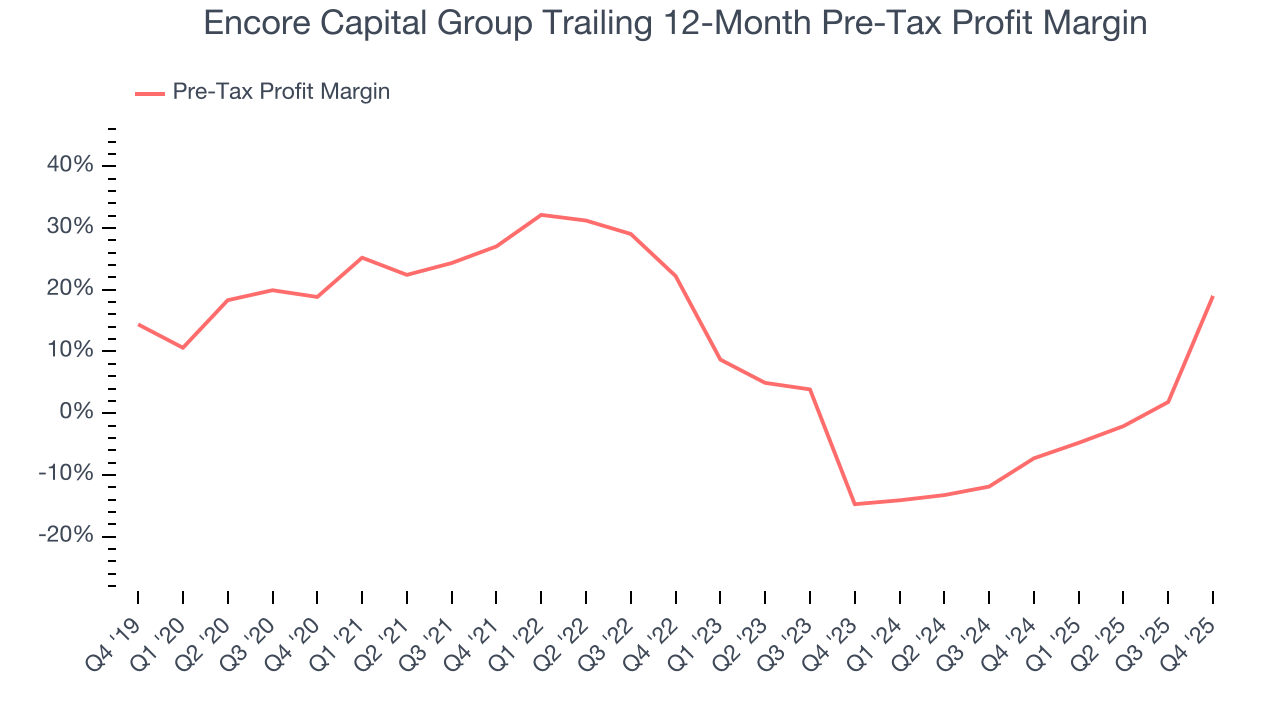

6. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For Specialty Finance companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

This is because for financials businesses, interest income and expense should be factored into the definition of profit but taxes - which are largely out of a company's control - should not.

Over the last five years, Encore Capital Group’s pre-tax profit margin couldn’t build momentum, hanging around 19%. Luckily, it seems the company has recently taken steps to address its expense base as its pre-tax profit margin expanded by 33.7 percentage points on a two-year basis.

In Q4, Encore Capital Group’s pre-tax profit margin was 20.7%. This result was 99.7 percentage points better than the same quarter last year.

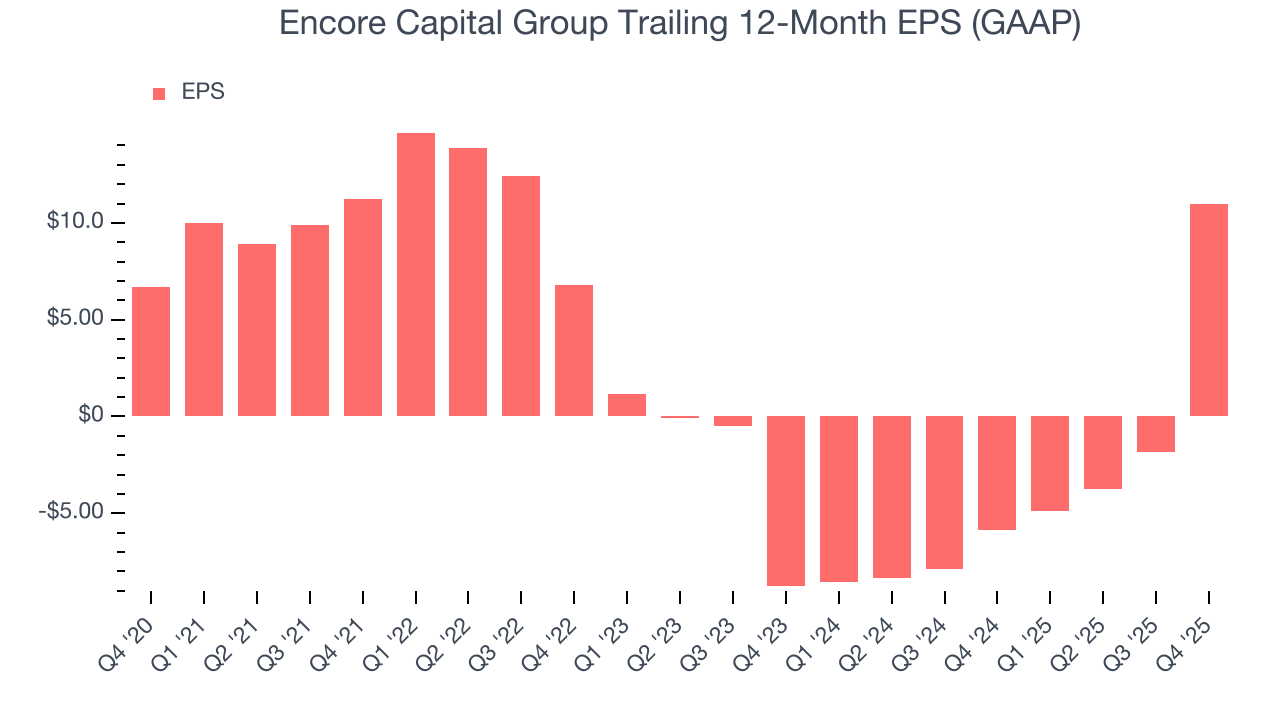

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Encore Capital Group’s EPS grew at a decent 10.4% compounded annual growth rate over the last five years, higher than its 3.3% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Encore Capital Group, its two-year annual EPS growth of 80.2% was higher than its five-year trend. This acceleration made it one of the faster-growing financials companies in recent history.

In Q4, Encore Capital Group reported EPS of $3.37, up from negative $9.42 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Encore Capital Group’s full-year EPS of $10.96 to shrink by 13%.

8. Return on Equity

Return on equity, or ROE, quantifies bank profitability relative to shareholder equity - an essential capital source for these institutions. Over extended periods, superior ROE performance drives faster shareholder wealth compounding through reinvestment, share repurchases, and dividend growth.

Over the last five years, Encore Capital Group has averaged an ROE of 5.8%, uninspiring for a company operating in a sector where the average shakes out around 10%.

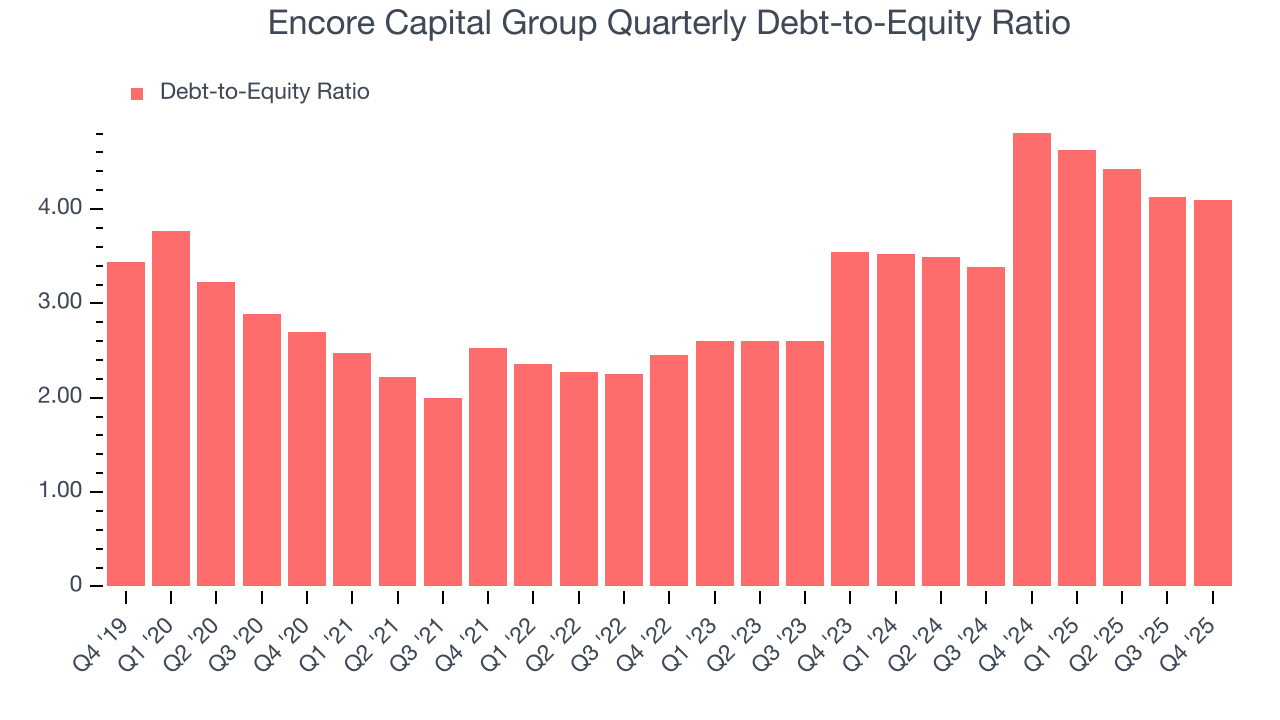

9. Balance Sheet Risk

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

Encore Capital Group currently has $4.00 billion of debt and $976.8 million of shareholder's equity on its balance sheet, and over the past four quarters, has averaged a debt-to-equity ratio of 4.3×. We think this is dangerous - for a financials business, anything above 3.5× raises red flags.

10. Key Takeaways from Encore Capital Group’s Q4 Results

It was good to see Encore Capital Group beat analysts’ EPS expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 4.5% to $61.75 immediately following the results.

11. Is Now The Time To Buy Encore Capital Group?

Updated: March 19, 2026 at 12:30 AM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Encore Capital Group, you should also grasp the company’s longer-term business quality and valuation.

Encore Capital Group is a pretty decent company if you ignore its balance sheet. Although its revenue growth was weak over the last five years,

Encore Capital Group’s P/E ratio based on the next 12 months is 5.7x. All that said, we aren’t investing at the moment because its balance sheet makes us balk. If you’re interested in buying the stock, wait until it generates sufficient cash flows or raises some money.

Wall Street analysts have a consensus one-year price target of $82.67 on the company (compared to the current share price of $68.34).