Etsy (ETSY)

We’re wary of Etsy. Its revenue growth has been weak and its profitability has caved, showing it’s struggling to adapt.― StockStory Analyst Team

1. News

2. Summary

Why We Think Etsy Will Underperform

Founded by a struggling amateur furniture maker Robert Kalin and his two friends, Etsy (NASDAQ:ETSY) is one of the world’s largest online marketplaces, focusing on handmade or vintage items.

- Market opportunities are plateauing as it failed to grow its active buyers over the last two years

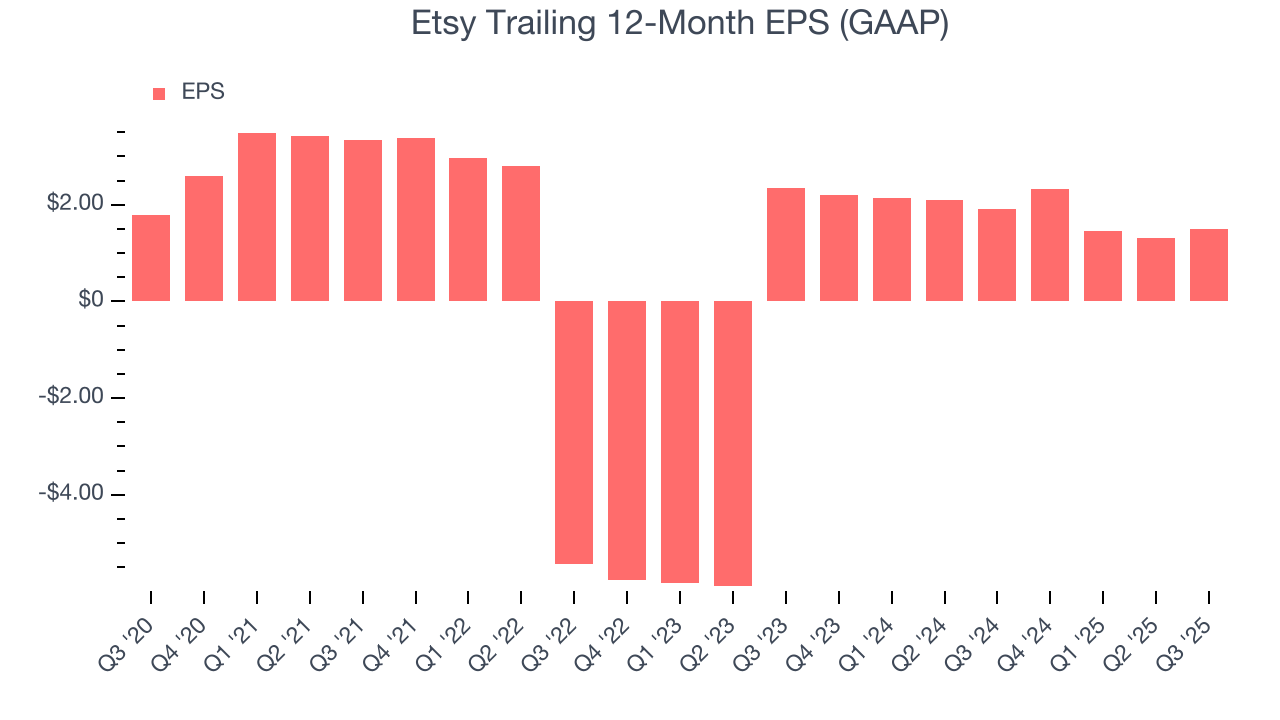

- Performance over the past three years shows its incremental sales were much less profitable, as its earnings per share fell by 1.1% annually

- A silver lining is that its successful business model is illustrated by its impressive EBITDA margin

Etsy is in the penalty box. We see more favorable opportunities in the market.

Why There Are Better Opportunities Than Etsy

Etsy’s stock price of $61.24 implies a valuation ratio of 12.8x forward EV/EBITDA. This multiple is high given its weaker fundamentals.

We’d rather pay up for companies with elite fundamentals than get a decent price on a poor one. High-quality businesses often have more durable earnings power, helping us sleep well at night.

3. Etsy (ETSY) Research Report: Q3 CY2025 Update

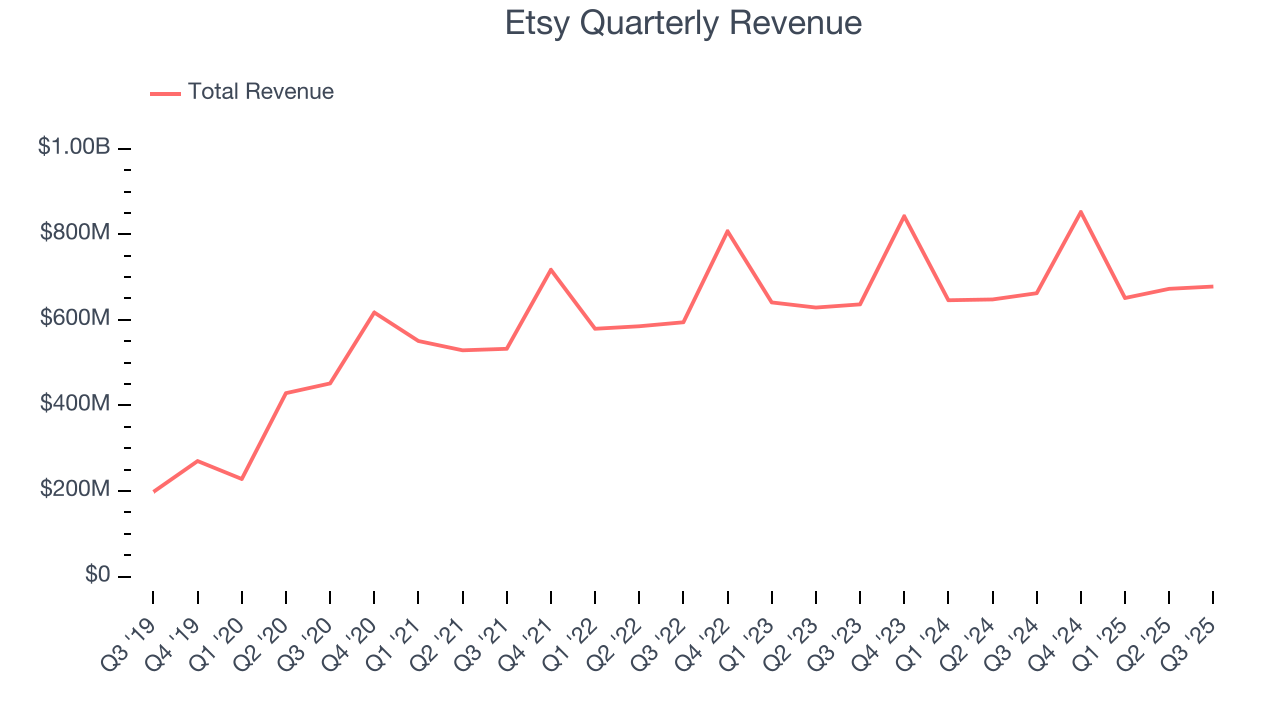

Online marketplace Etsy (NASDAQ:ETSY) announced better-than-expected revenue in Q3 CY2025, with sales up 2.4% year on year to $678 million. Its GAAP profit of $0.63 per share was 21.1% above analysts’ consensus estimates.

Etsy (ETSY) Q3 CY2025 Highlights:

- Revenue: $678 million vs analyst estimates of $656.6 million (2.4% year-on-year growth, 3.3% beat)

- EPS (GAAP): $0.63 vs analyst estimates of $0.52 (21.1% beat)

- Adjusted EBITDA: $171.9 million vs analyst estimates of $164.7 million (25.4% margin, 4.4% beat)

- Q4 EBITDA margin guidance of 24%, well below expectations of 27%

- Operating Margin: 12.2%, in line with the same quarter last year

- Free Cash Flow Margin: 27.1%, up from 13.4% in the previous quarter

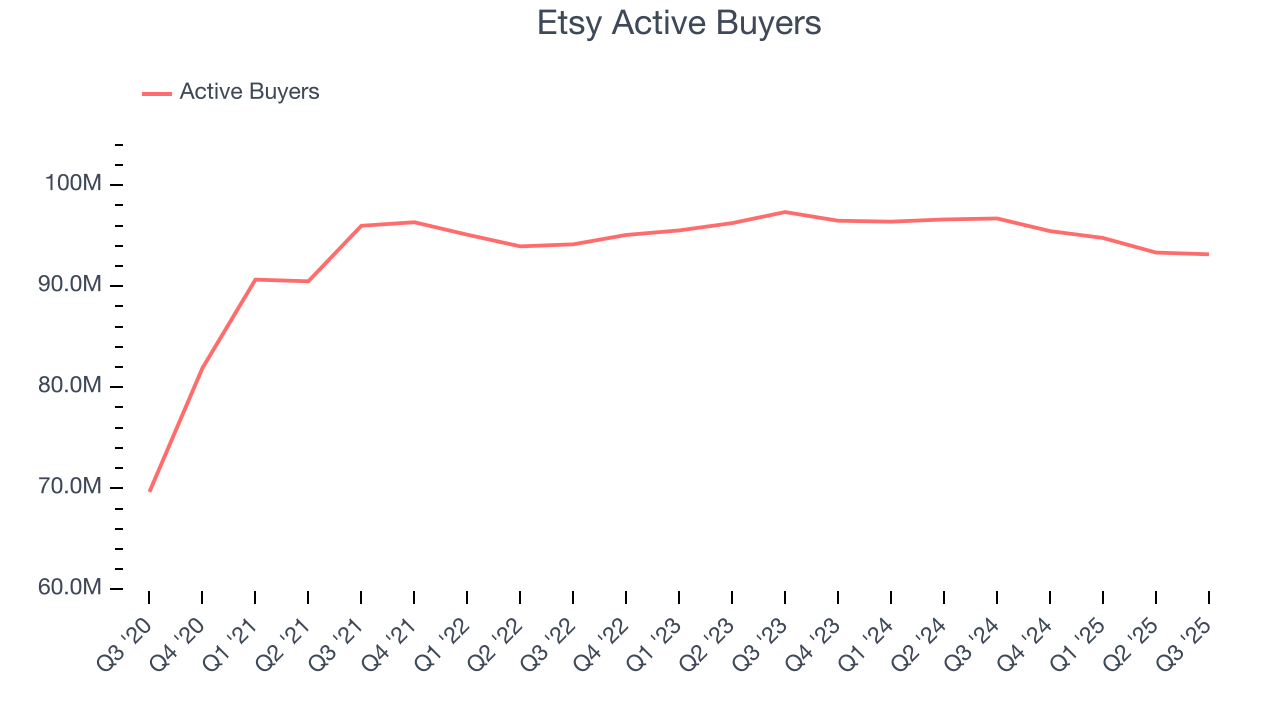

- Active Buyers: 93.16 million, down 3.55 million year on year

- Market Capitalization: $7.41 billion

Company Overview

Founded by a struggling amateur furniture maker Robert Kalin and his two friends, Etsy (NASDAQ:ETSY) is one of the world’s largest online marketplaces, focusing on handmade or vintage items.

Etsy operates a two-sided online marketplace that connects tens of millions of buyers and sellers around the world with a focus on unique and creative goods that are crafted and curated by individuals or small businesses. Most of its products are in six main categories: home furnishings, jewelry, craft supplies, apparel, paper & party supplies, and beauty & personal care. The company is asset lite: it owns no warehouses, takes no inventory risk, and does not operate a supply chain network.

Etsy offers a differentiated value proposition for its sellers and its buyers. For buyers, it has created a very successful niche to find custom and curated items, from special purpose gifts to everyday items that have added meaning. For sellers, Etsy provides a large global audience for their merchandise, while also offering a range of tools and analytics to manage their online businesses.

4. Online Marketplace

Marketplaces have existed for centuries. Where once it was a main street in a small town or a mall in the suburbs, sellers benefitted from proximity to one another because they could draw customers by offering convenience and selection. Today, a myriad of online marketplaces fulfill that same role, aggregating large customer bases, which attracts commission-paying sellers, generating flywheel scale effects that feed back into further customer acquisition.

Etsy (NASDAQ:ETSY) competes with a range of ecommerce companies such as Amazon (NASDAQ:AMZN), Walmart (NYSE:WMT), Shopify (NASDAQ:SHOP), and eBay (NASDAQ:EBAY), and increasingly with social commerce companies like Pinterest (NYSE:PINS), and Meta Platforms (NASDAQ:META).

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last three years, Etsy grew its sales at a sluggish 4.9% compounded annual growth rate. This was below our standard for the consumer internet sector and is a rough starting point for our analysis.

This quarter, Etsy reported modest year-on-year revenue growth of 2.4% but beat Wall Street’s estimates by 3.3%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last three years. This projection doesn't excite us and indicates its products and services will face some demand challenges.

6. Active Buyers

Buyer Growth

As an online marketplace, Etsy generates revenue growth by increasing both the number of users on its platform and the average order size in dollars.

Etsy struggled with new customer acquisition over the last two years as its active buyers were flat at 93.16 million. This performance isn't ideal because internet usage is secular, meaning there are typically unaddressed market opportunities. If Etsy wants to accelerate growth, it likely needs to enhance the appeal of its current offerings or innovate with new products.

In Q3, Etsy’s active buyers decreased by 3.55 million, a 3.7% drop since last year. The quarterly print was lower than its two-year result, suggesting its new initiatives aren’t moving the needle for buyers yet.

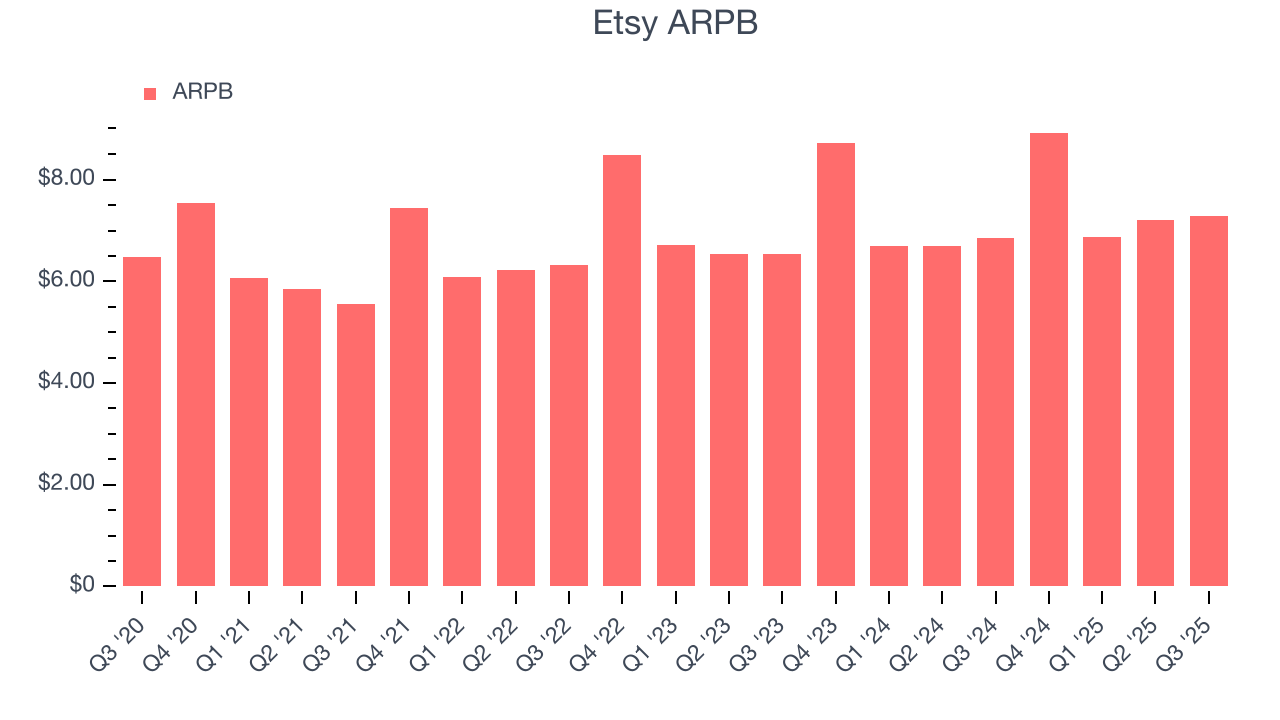

Revenue Per Buyer

Average revenue per buyer (ARPB) is a critical metric to track because it measures how much the company earns in transaction fees from each buyer. ARPB also gives us unique insights into a user’s average order size and Etsy’s take rate, or "cut", on each order.

Etsy’s ARPB growth has been mediocre over the last two years, averaging 3.6%. This raises questions about its platform’s health when paired with its flat active buyers. If Etsy wants to grow its buyers, it must either develop new features or lower its monetization of existing ones.

This quarter, Etsy’s ARPB clocked in at $7.28. It grew by 6.3% year on year, faster than its active buyers.

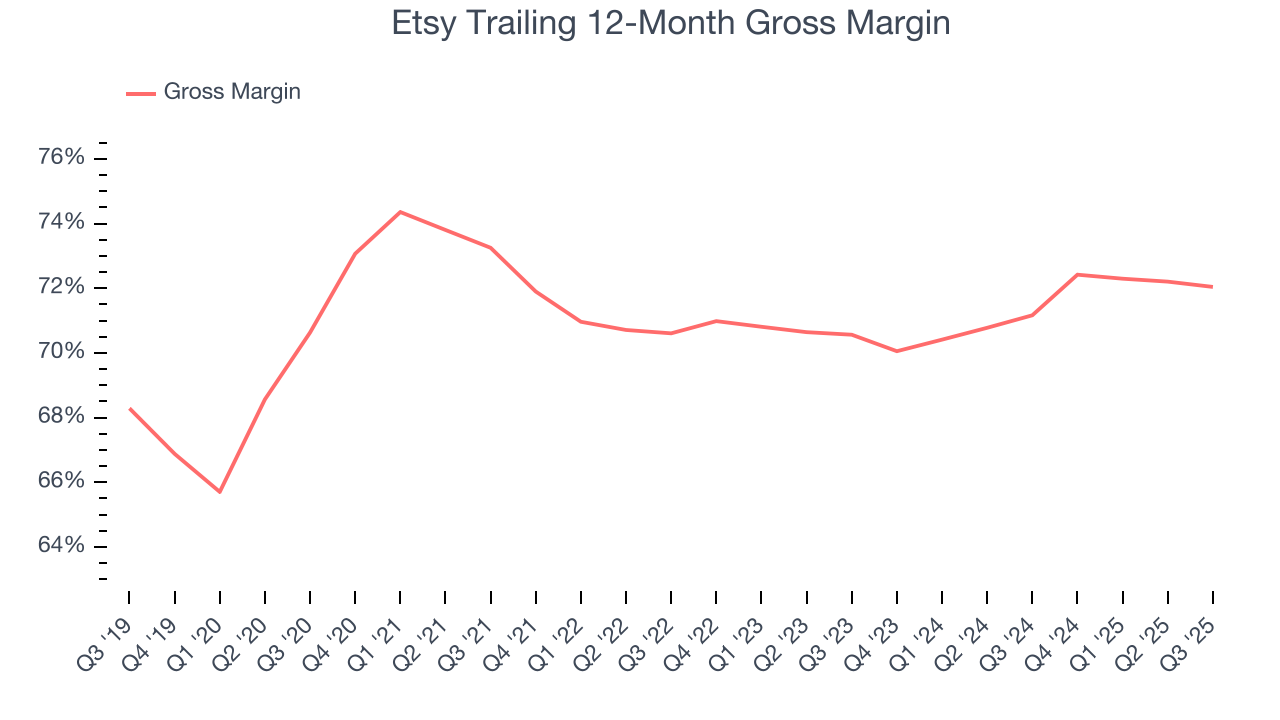

7. Gross Margin & Pricing Power

For online marketplaces like Etsy, gross profit tells us how much money the company gets to keep after covering the base cost of its products and services, which typically include payment processing, hosting, and bandwidth fees in addition to the costs necessary to onboard buyers and sellers, such as identity verification.

Etsy has robust unit economics, an output of its asset-lite business model and pricing power. Its margin is better than the broader consumer internet industry and enables the company to fund large investments in new products and marketing during periods of rapid growth to achieve higher profits in the future. As you can see below, it averaged an excellent 71.6% gross margin over the last two years. That means Etsy only paid its providers $28.39 for every $100 in revenue.

Etsy’s gross profit margin came in at 71.3% this quarter, in line with the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

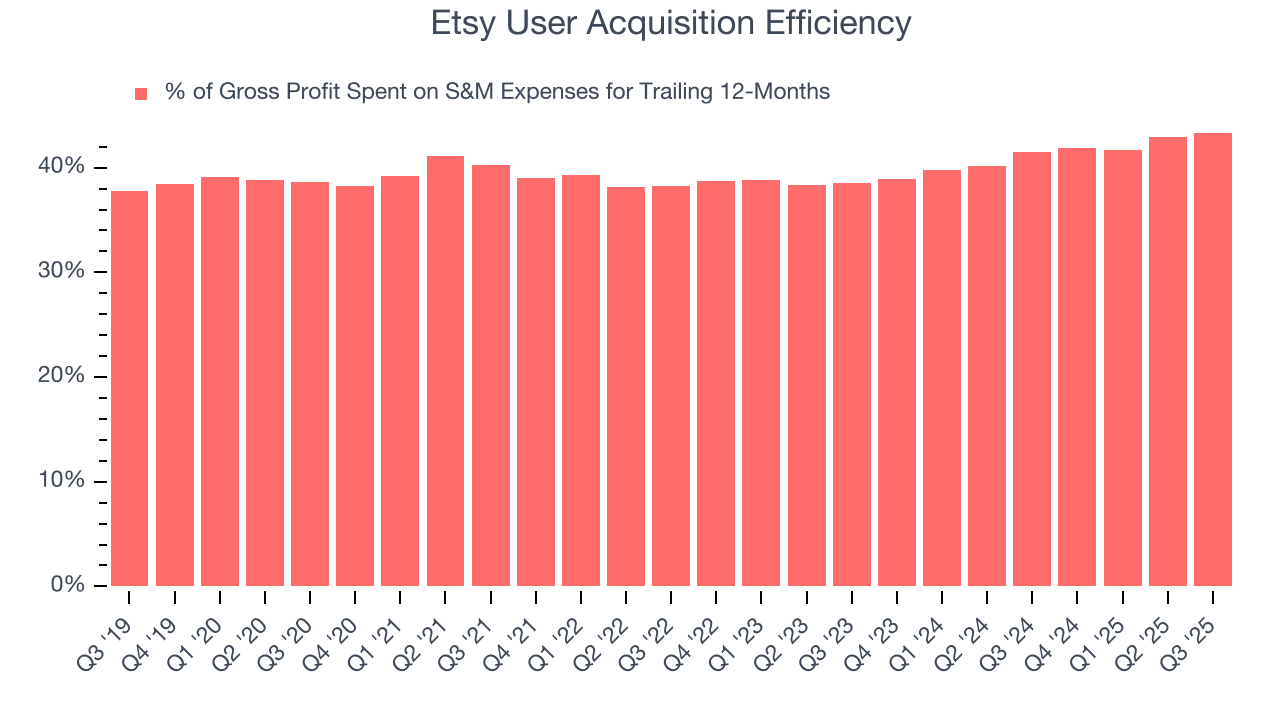

8. User Acquisition Efficiency

Unlike enterprise software that’s typically sold by dedicated sales teams, consumer internet businesses like Etsy grow from a combination of product virality, paid advertisement, and incentives.

Etsy does a decent job acquiring new users, spending 43.3% of its gross profit on sales and marketing expenses over the last year. This decent efficiency indicates relatively solid competitive positioning, giving Etsy the freedom to invest its resources into new growth initiatives.

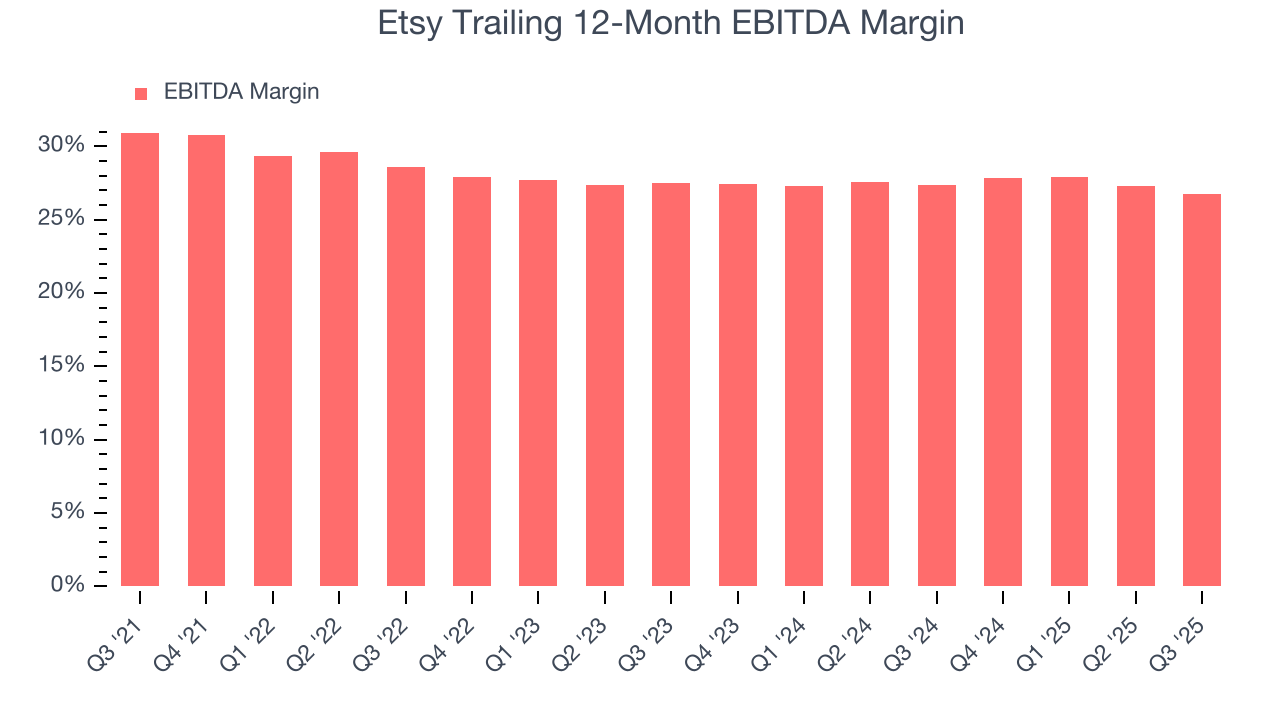

9. EBITDA

Etsy has been a well-oiled machine over the last two years. It demonstrated elite profitability for a consumer internet business, boasting an average EBITDA margin of 27.1%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Etsy’s EBITDA margin decreased by 1.9 percentage points over the last few years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Etsy generated an EBITDA margin profit margin of 25.4%, down 2.4 percentage points year on year. Since Etsy’s EBITDA margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

10. Earnings Per Share

Revenue trends explain a company’s historical growth, but the change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

In Q3, Etsy reported EPS of $0.63, up from $0.44 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Etsy’s full-year EPS of $1.50 to grow 75.3%.

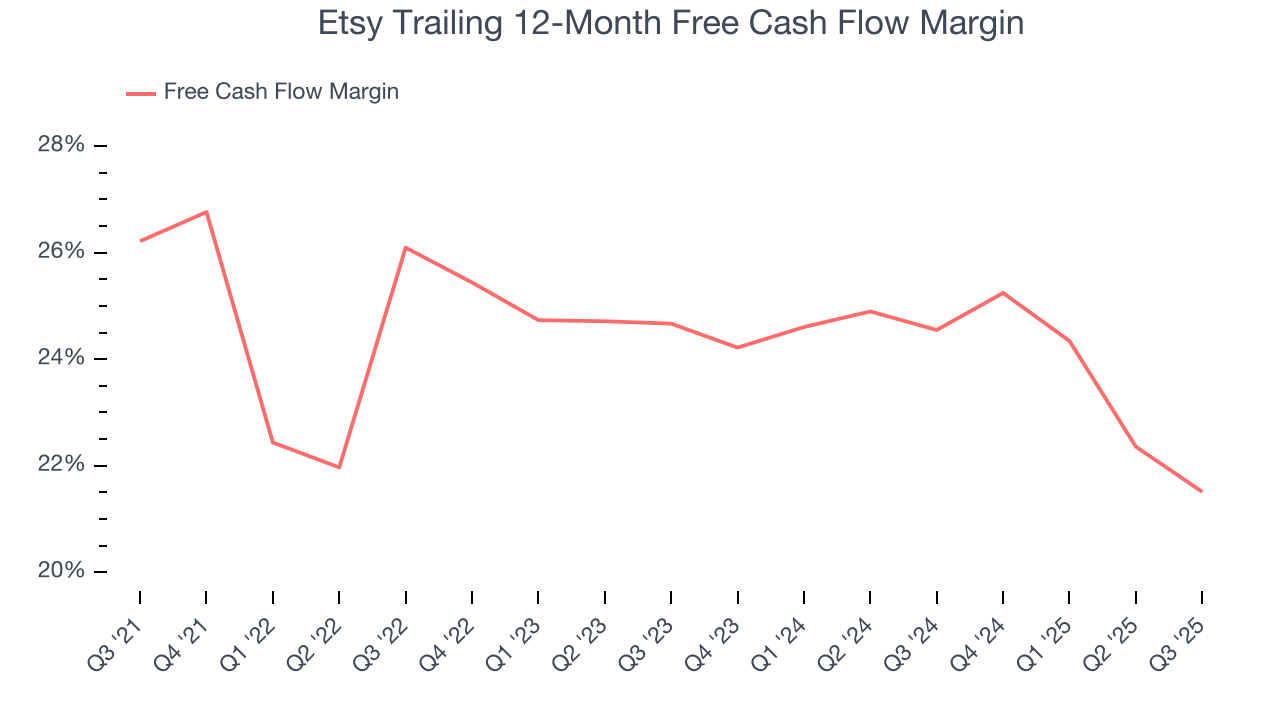

11. Cash Is King

Although EBITDA is undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Etsy has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition while maintaining an ample cushion. The company’s free cash flow margin was among the best in the consumer internet sector, averaging 23% over the last two years.

Taking a step back, we can see that Etsy’s margin dropped by 4.6 percentage points over the last few years. If its declines continue, it could signal increasing investment needs and capital intensity.

Etsy’s free cash flow clocked in at $183.7 million in Q3, equivalent to a 27.1% margin. The company’s cash profitability regressed as it was 3.8 percentage points lower than in the same quarter last year, but it’s still above its two-year average. We wouldn’t put too much weight on this quarter’s decline because investment needs can be seasonal, causing short-term swings. Long-term trends are more important.

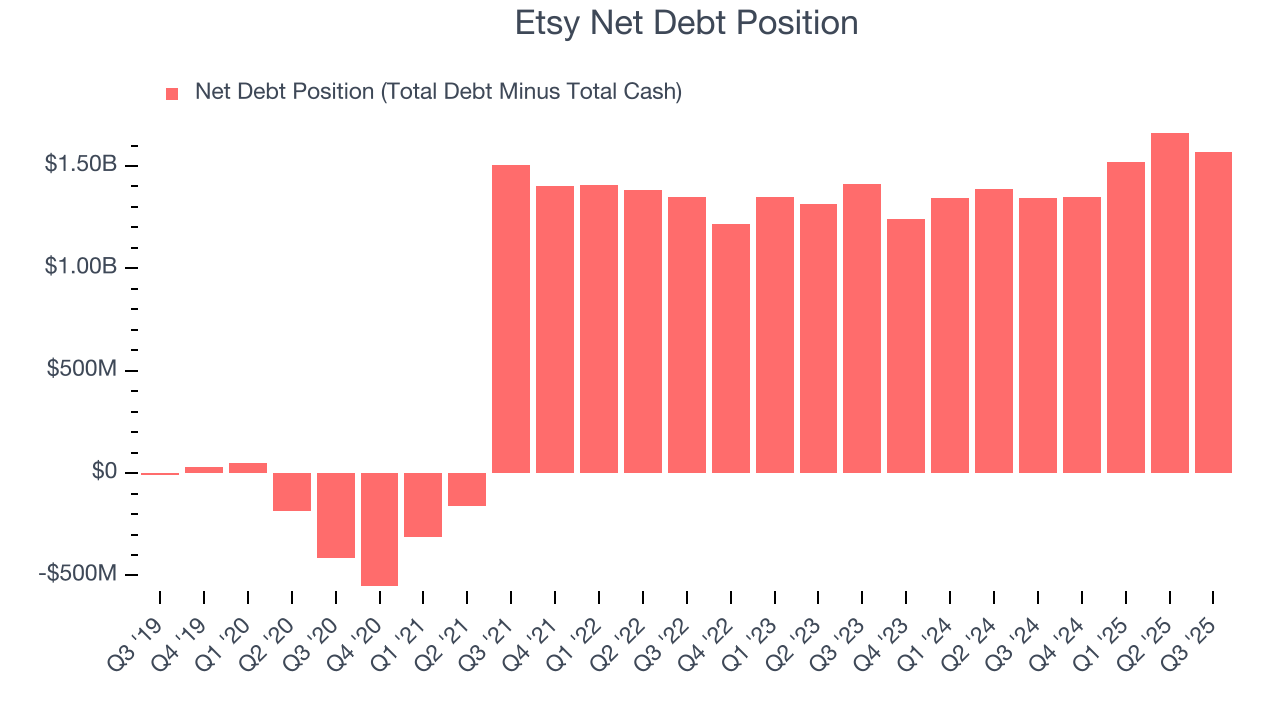

12. Balance Sheet Assessment

Etsy reported $1.51 billion of cash and $3.08 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $762.7 million of EBITDA over the last 12 months, we view Etsy’s 2.1× net-debt-to-EBITDA ratio as safe. We also see its $14.27 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from Etsy’s Q3 Results

We enjoyed seeing Etsy beat analysts’ revenue and EBITDA expectations this quarter. On the other hand, its number of buyers declined and the company guided to EBITDA margin of 24% next quarter, well below expectations of 27%. This margin outlook is weighing on shares, and the stock traded down 8% to $68.85 immediately following the results.

14. Is Now The Time To Buy Etsy?

Updated: January 21, 2026 at 9:17 PM EST

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

Etsy isn’t a terrible business, but it doesn’t pass our quality test. First off, its revenue growth was weak over the last three years, and analysts expect its demand to deteriorate over the next 12 months. And while its impressive EBITDA margins show it has a highly efficient business model, the downside is its active buyers were flat. On top of that, its declining EPS over the last three years makes it a less attractive asset to the public markets.

Etsy’s EV/EBITDA ratio based on the next 12 months is 12.8x. At this valuation, there’s a lot of good news priced in - you can find more timely opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $66.93 on the company (compared to the current share price of $61.24).