European Wax Center (EWCZ)

European Wax Center faces an uphill battle. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think European Wax Center Will Underperform

Founded by two siblings, European Wax Center (NASDAQ:EWCZ) is a beauty and waxing salon chain specializing in professional wax services and skincare products.

- Annual revenue growth of 14.8% over the last five years was below our standards for the consumer discretionary sector

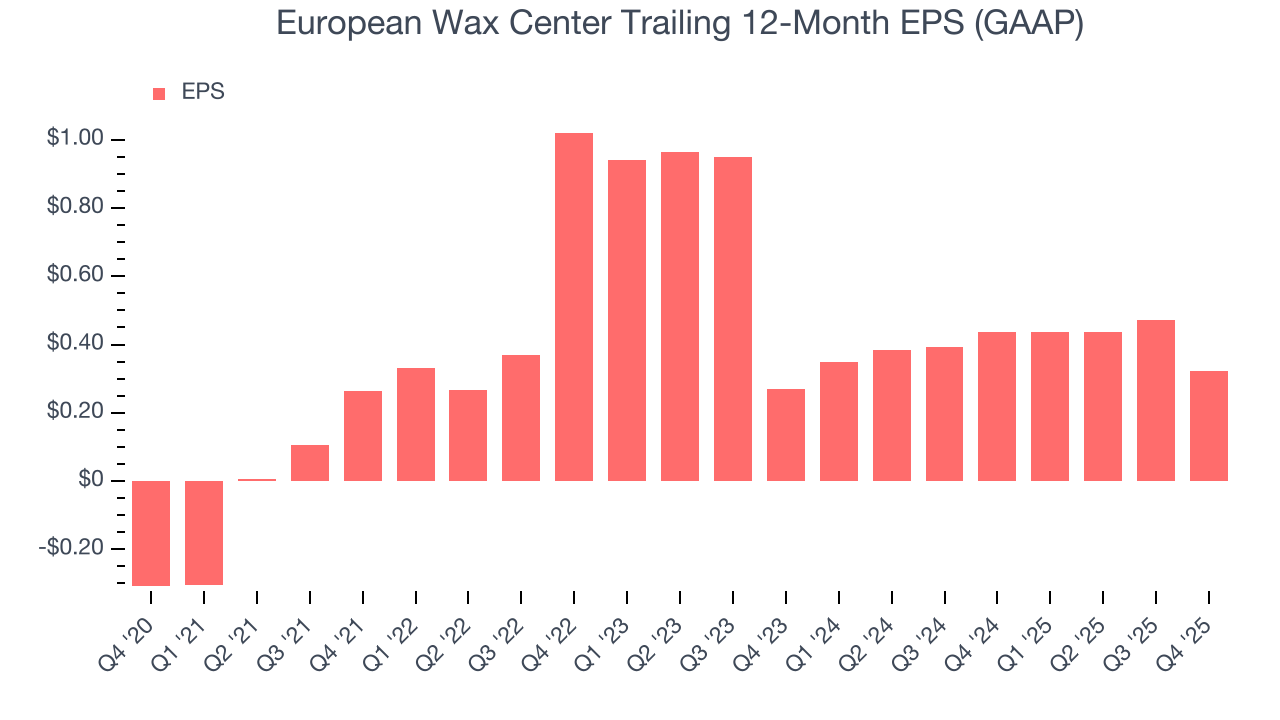

- Earnings growth underperformed the sector average over the last four years as its EPS grew by just 11.8% annually

- Underwhelming 12.1% return on capital reflects management’s difficulties in finding profitable growth opportunities, and its decreasing returns suggest its historical profit centers are aging

European Wax Center’s quality is inadequate. More profitable opportunities exist elsewhere.

Why There Are Better Opportunities Than European Wax Center

European Wax Center’s stock price of $5.75 implies a valuation ratio of 10.1x forward P/E. European Wax Center’s valuation may seem like a bargain, especially when stacked up against other consumer discretionary companies. We remind you that you often get what you pay for, though.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. European Wax Center (EWCZ) Research Report: Q4 CY2025 Update

Beauty and waxing service franchise European Wax Center (NASDAQ:EWCZ) missed Wall Street’s revenue expectations in Q4 CY2025, with sales falling 9.3% year on year to $45.1 million. Its GAAP loss of $0.03 per share was significantly below analysts’ consensus estimates.

European Wax Center (EWCZ) Q4 CY2025 Highlights:

- Revenue: $45.1 million vs analyst estimates of $45.88 million (9.3% year-on-year decline, 1.7% miss)

- EPS (GAAP): -$0.03 vs analyst estimates of $0.04 (significant miss)

- Adjusted EBITDA: $12.68 million vs analyst estimates of $12.77 million (28.1% margin, 0.7% miss)

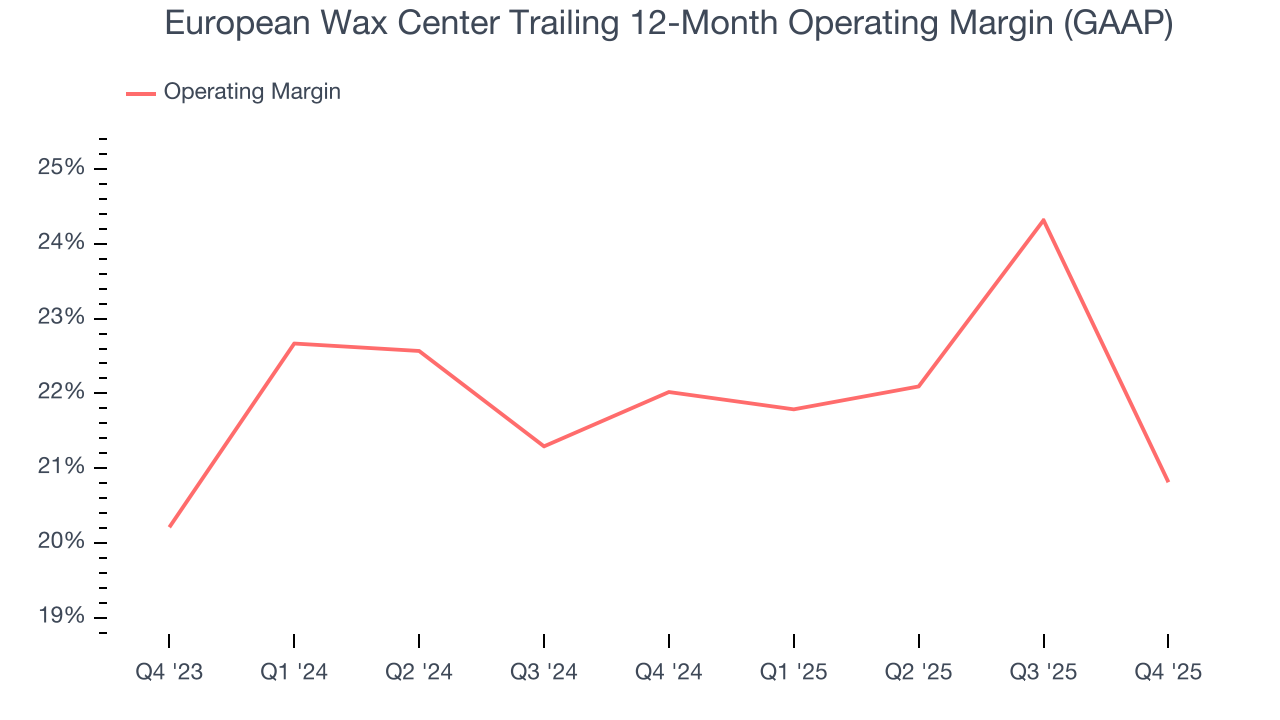

- Operating Margin: 9.9%, down from 25.8% in the same quarter last year

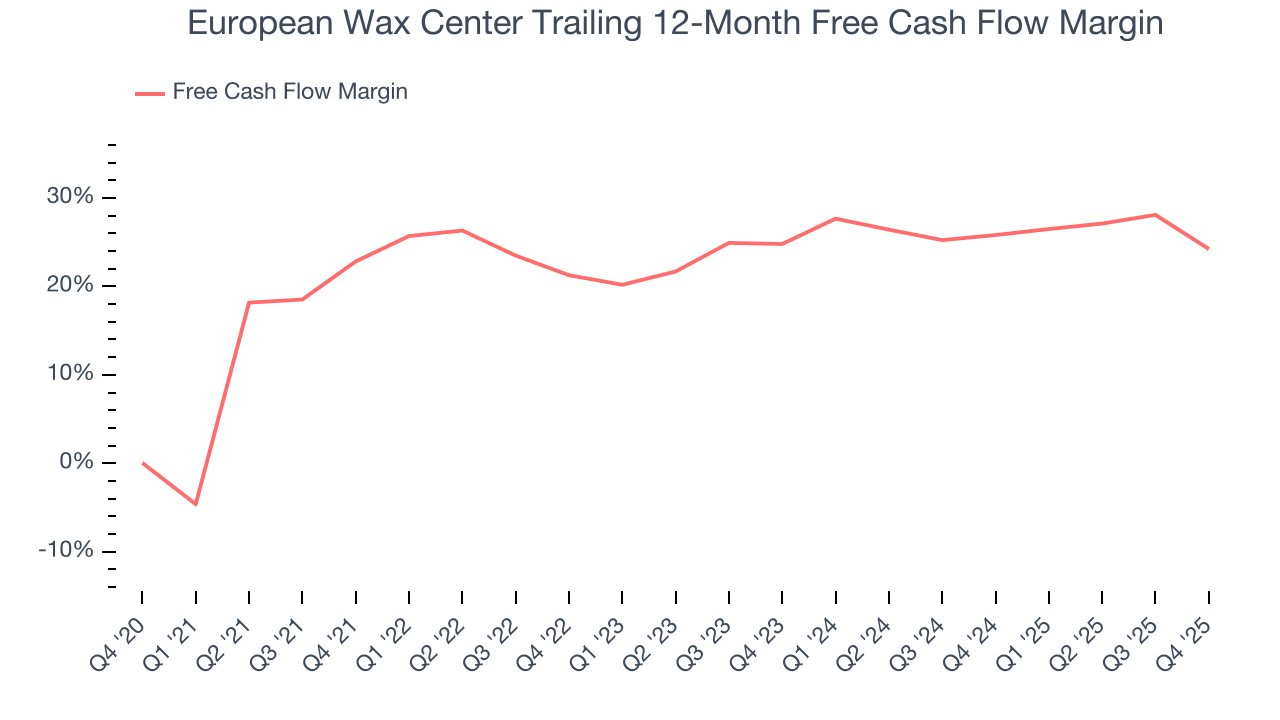

- Free Cash Flow Margin: 15.6%, down from 32.8% in the same quarter last year

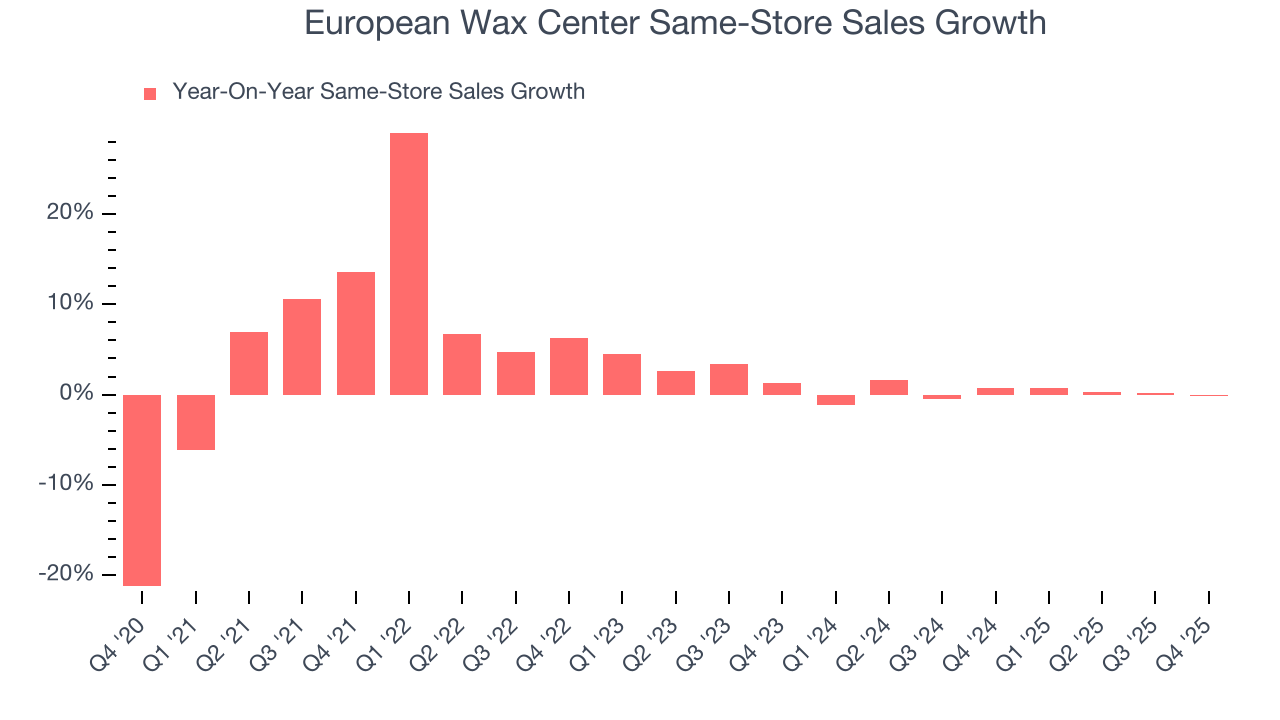

- Same-Store Sales were flat year on year, in line with the same quarter last year

- Market Capitalization: $252.7 million

Company Overview

Founded by two siblings, European Wax Center (NASDAQ:EWCZ) is a beauty and waxing salon chain specializing in professional wax services and skincare products.

European Wax Center recognized the need for a waxing experience focused on comfort and hygiene. The company aimed to provide a luxurious experience, prioritizing customer care and high-quality products. It began with a single salon and has since expanded into a prominent chain.

The company offers a wide range of waxing services for both men and women, including facial and body waxing. European Wax Center's appeal is in its proprietary Comfort Wax, made from natural beeswax. The popularity of Comfort Wax has incentivized the company to market other skincare products that complement its core services.

Revenue is generated through a combination of service fees and product sales. Its business model includes franchise and corporate-owned locations, allowing for scalability and flexibility in expansion. European Wax Center's revenue model is further bolstered by royalty fees from franchisees, which typically come with higher margins.

4. Consumer Discretionary - Leisure Facilities

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare.

Leisure facilities companies own and operate theme parks, fitness centers, bowling alleys, and other venue-based entertainment destinations, generating revenue from admissions, memberships, and on-site spending. Tailwinds include consumer preference for experiential spending, tourism recovery, and technology-enhanced guest experiences that support premium pricing. Headwinds are notable: high fixed costs, such as real estate, labor, and maintenance, make profitability highly sensitive to attendance fluctuations during economic slowdowns. Weather, pandemics, and safety incidents can disrupt operations unpredictably. Rising construction and labor costs inflate expansion budgets, while competition from at-home entertainment alternatives and other experiential options limits pricing power in many markets.

As a niche business, European Wax Center has no direct public competitors. Privately owned competitors include Bluemercury, Radiant Waxing, and Waxing the City.

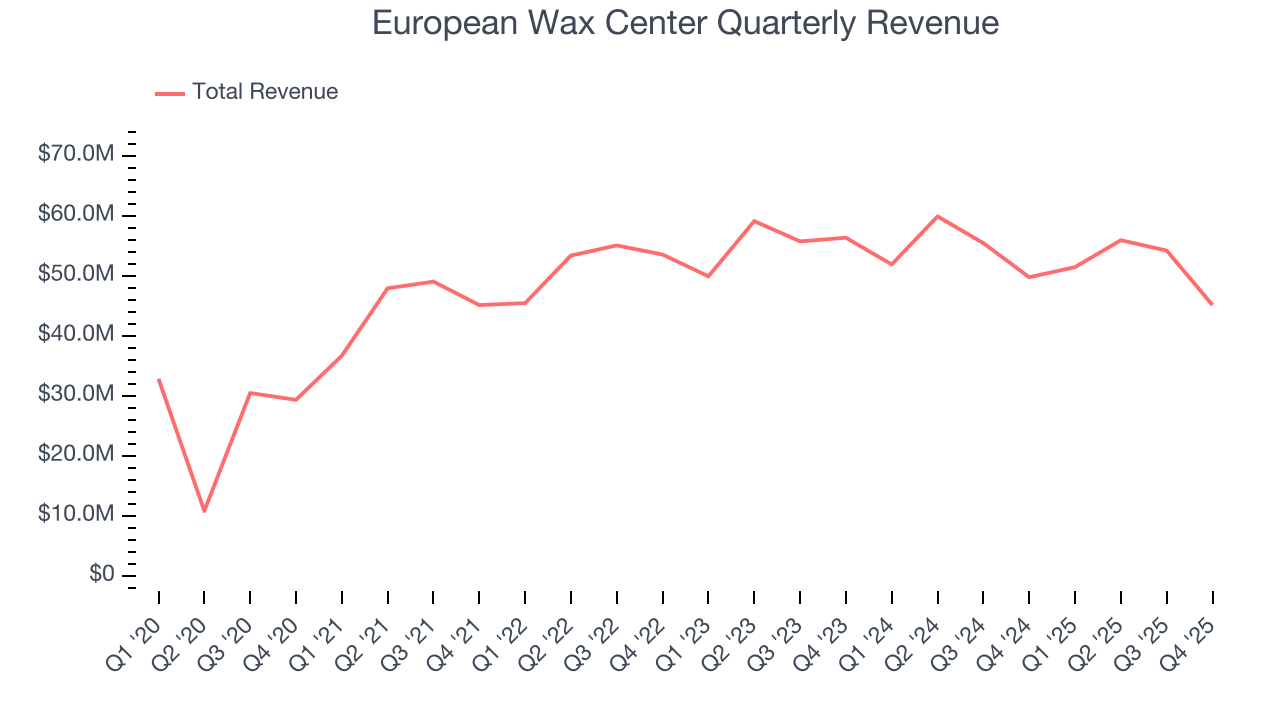

5. Revenue Growth

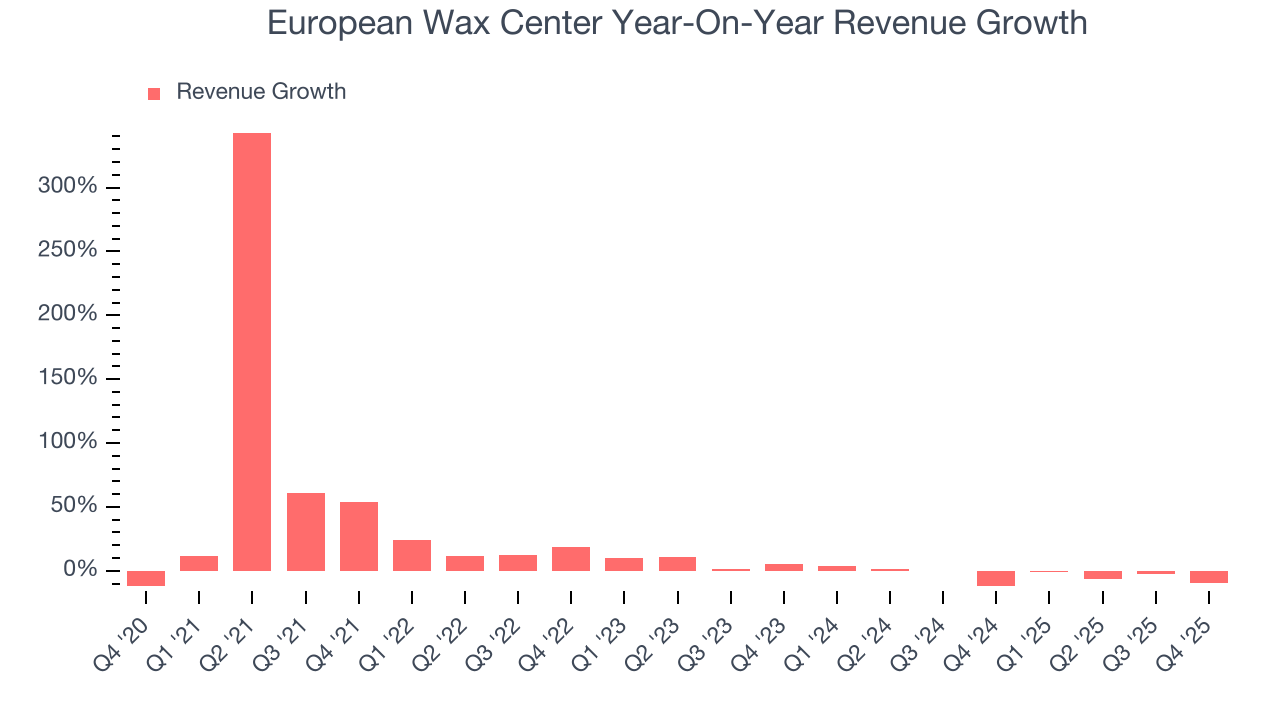

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, European Wax Center grew its sales at a 14.8% compounded annual growth rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the consumer discretionary sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. European Wax Center’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 3.3% annually. Note that COVID hurt European Wax Center’s business in 2020 and part of 2021, and it bounced back in a big way thereafter.

European Wax Center also reports same-store sales, which show how much revenue its established locations generate. Over the last two years, European Wax Center’s same-store sales were flat. Because this number is better than its revenue growth, we can see its sales from existing locations are performing better than its sales from new locations.

This quarter, European Wax Center missed Wall Street’s estimates and reported a rather uninspiring 9.3% year-on-year revenue decline, generating $45.1 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 2.7% over the next 12 months. Although this projection suggests its newer products and services will spur better top-line performance, it is still below average for the sector.

6. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

European Wax Center’s operating margin has been trending down over the last 12 months and averaged 21.4% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

This quarter, European Wax Center generated an operating margin profit margin of 9.9%, down 15.9 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

European Wax Center’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q4, European Wax Center reported EPS of negative $0.03, down from $0.12 in the same quarter last year. This print missed analysts’ estimates. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

8. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

European Wax Center has shown weak cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 25%, below what we’d expect for a consumer discretionary business.

European Wax Center’s free cash flow clocked in at $7.05 million in Q4, equivalent to a 15.6% margin. The company’s cash profitability regressed as it was 17.2 percentage points lower than in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

European Wax Center historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 12.1%, somewhat low compared to the best consumer discretionary companies that consistently pump out 25%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, European Wax Center’s ROIC has unfortunately decreased. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

10. Balance Sheet Assessment

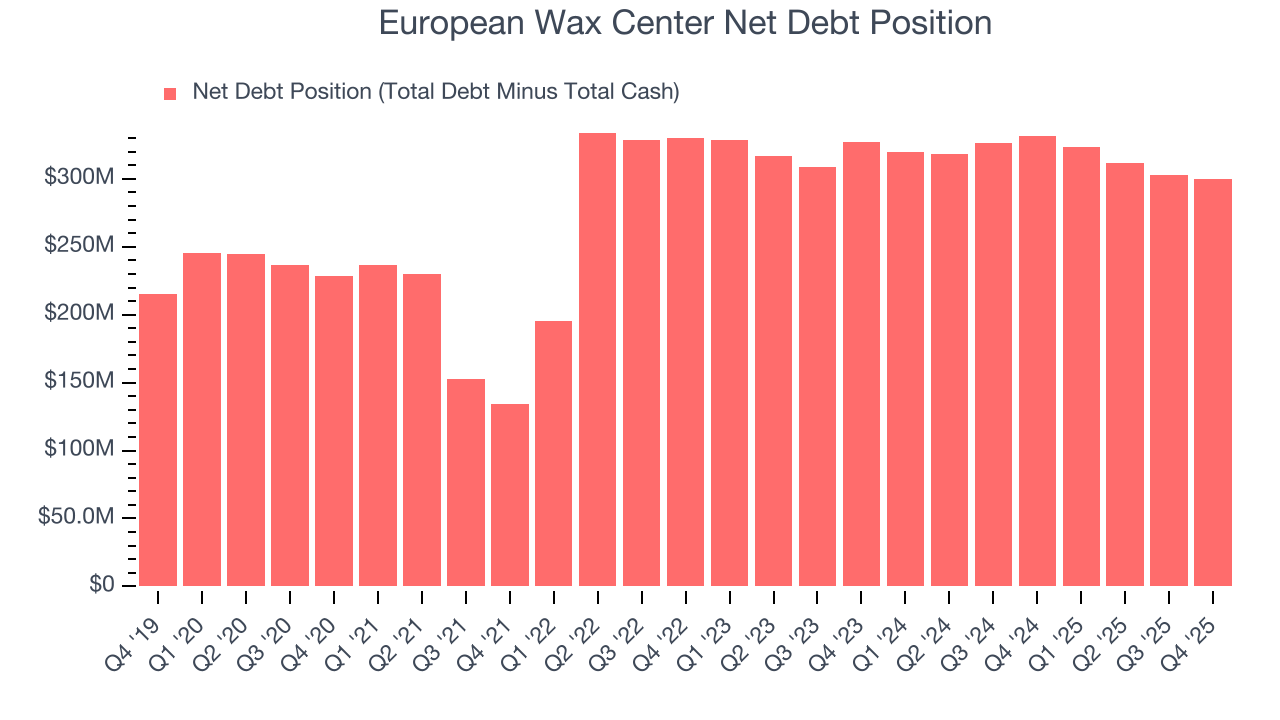

European Wax Center reported $82.48 million of cash and $382.3 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $73.22 million of EBITDA over the last 12 months, we view European Wax Center’s 4.1× net-debt-to-EBITDA ratio as safe. We also see its $13.19 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from European Wax Center’s Q4 Results

We struggled to find many positives in these results. Its EPS missed and its revenue fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock remained flat at $5.75 immediately after reporting.

12. Is Now The Time To Buy European Wax Center?

Updated: March 14, 2026 at 11:05 PM EDT

Before investing in or passing on European Wax Center, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

We cheer for all companies serving everyday consumers, but in the case of European Wax Center, we’ll be cheering from the sidelines. On top of that, European Wax Center’s Forecasted free cash flow margin suggests the company will ramp up its investments next year, and its same-store sales performance has disappointed.

European Wax Center’s P/E ratio based on the next 12 months is 10.1x. While this valuation is reasonable, we don’t see a big opportunity at the moment. There are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $7.64 on the company (compared to the current share price of $5.75).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.