First Advantage (FA)

First Advantage doesn’t impress us. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why First Advantage Is Not Exciting

Processing over 200 million screens annually across more than 200 countries and territories, First Advantage (NASDAQ:FA) provides employment background screening, identity verification, and compliance solutions to help companies manage hiring risks.

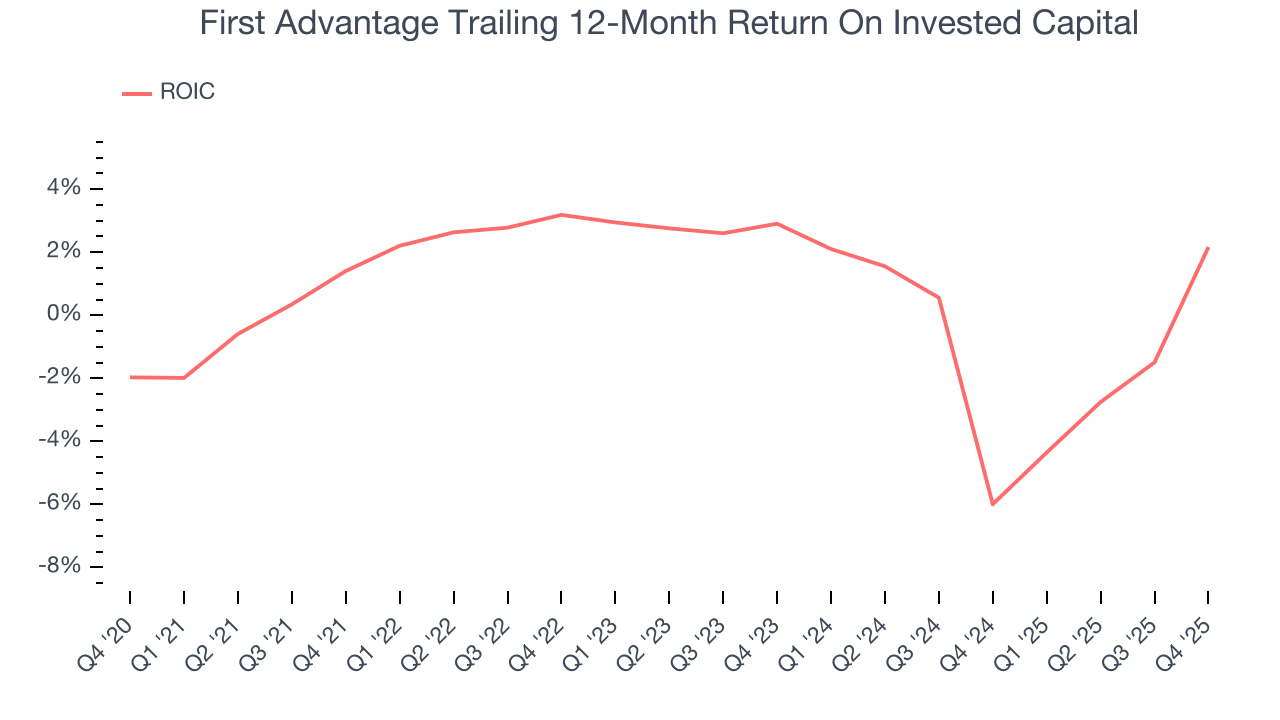

- ROIC of 0.7% reflects management’s challenges in identifying attractive investment opportunities, and its decreasing returns suggest its historical profit centers are aging

- Earnings per share were flat over the last four years and fell short of the peer group average

- On the bright side, its market share has increased this cycle as its 25.3% annual revenue growth over the last five years was exceptional

First Advantage falls short of our quality standards. We see more attractive opportunities in the market.

Why There Are Better Opportunities Than First Advantage

First Advantage’s stock price of $10.97 implies a valuation ratio of 8.9x forward P/E. This certainly seems like a cheap stock, but we think there are valid reasons why it trades this way.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. First Advantage (FA) Research Report: Q4 CY2025 Update

Background screening provider First Advantage (NASDAQ:FA) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 36.8% year on year to $420 million. The company’s full-year revenue guidance of $1.66 billion at the midpoint came in 2.4% above analysts’ estimates. Its non-GAAP profit of $0.30 per share was 13.7% above analysts’ consensus estimates.

First Advantage (FA) Q4 CY2025 Highlights:

- Revenue: $420 million vs analyst estimates of $391.3 million (36.8% year-on-year growth, 7.3% beat)

- Adjusted EPS: $0.30 vs analyst estimates of $0.26 (13.7% beat)

- Adjusted EBITDA: $116.8 million vs analyst estimates of $110 million (27.8% margin, 6.2% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $1.20 at the midpoint, beating analyst estimates by 2.7%

- EBITDA guidance for the upcoming financial year 2026 is $472.5 million at the midpoint, in line with analyst expectations

- Operating Margin: 10.7%, up from -26.3% in the same quarter last year

- Free Cash Flow was $49.07 million, up from -$96.16 million in the same quarter last year

- Market Capitalization: $1.93 billion

Company Overview

Processing over 200 million screens annually across more than 200 countries and territories, First Advantage (NASDAQ:FA) provides employment background screening, identity verification, and compliance solutions to help companies manage hiring risks.

First Advantage's comprehensive suite of pre-onboarding services includes criminal background checks, drug testing, education and employment verification, identity checks, and specialized screenings for regulated industries. The company's technology platform integrates with over 100 human capital management and ATS systems, creating a seamless workflow for employers while providing a user-friendly experience for job applicants through its mobile-optimized Profile Advantage interface.

The company maintains proprietary databases containing over a billion records, with over 900 million criminal records in the National Criminal Records File database and approximately 135 million work history and education records in the Verified! database. This vast repository allows First Advantage to deliver faster results than competitors who rely solely on external data sources. For example, about 90% of U.S. criminal searches are completed within one day.

Beyond initial screening, First Advantage offers post-onboarding monitoring solutions that continuously check for new criminal records, sanctions, license status changes, or other issues that might affect an employee's eligibility to work. This ongoing surveillance helps employers maintain compliance with industry regulations and protect workplace safety throughout the employment lifecycle.

The company serves more than 80,000 customers across diverse industries, with particular strength in sectors with high-volume hiring needs such as retail, transportation, warehousing, and healthcare. A human resources director at a national retail chain might use First Advantage to screen thousands of seasonal workers before the holiday rush, verifying their identities, checking for criminal histories, and confirming previous employment claims.

First Advantage generates revenue through a transaction-based model, charging fees for each background check or verification service performed. The company's business is subject to various regulations including the Fair Credit Reporting Act, which governs how consumer information can be collected, used, and shared for employment purposes.

4. Professional Staffing & HR Solutions

The Professional Staffing & HR Solutions subsector within Business Services is set to benefit from evolving workforce trends, including the rise of remote work and the gig economy. With companies casting a wider net to find talent due to remote work, the expertise of staffing and recruiting companies is even more valuable. For those who invest wisely, the use of predictive AI in recruitment and screening as well as automation in HR workflows can enhance efficiency and scalability. On the other hand, digitization means that talent discovery is less of a manual process, opening the door for tech-first platforms. Additionally, regulatory scrutiny around data privacy in HR is evolving and may require companies in this sector to change their go-to-market strategies over time.

First Advantage competes with other background screening providers including HireRight (NYSE:HRT) and Accurate Background, as well as with broader human capital management companies that offer screening as part of their services, such as ADP (NASDAQ:ADP) and Equifax (NYSE:EFX).

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

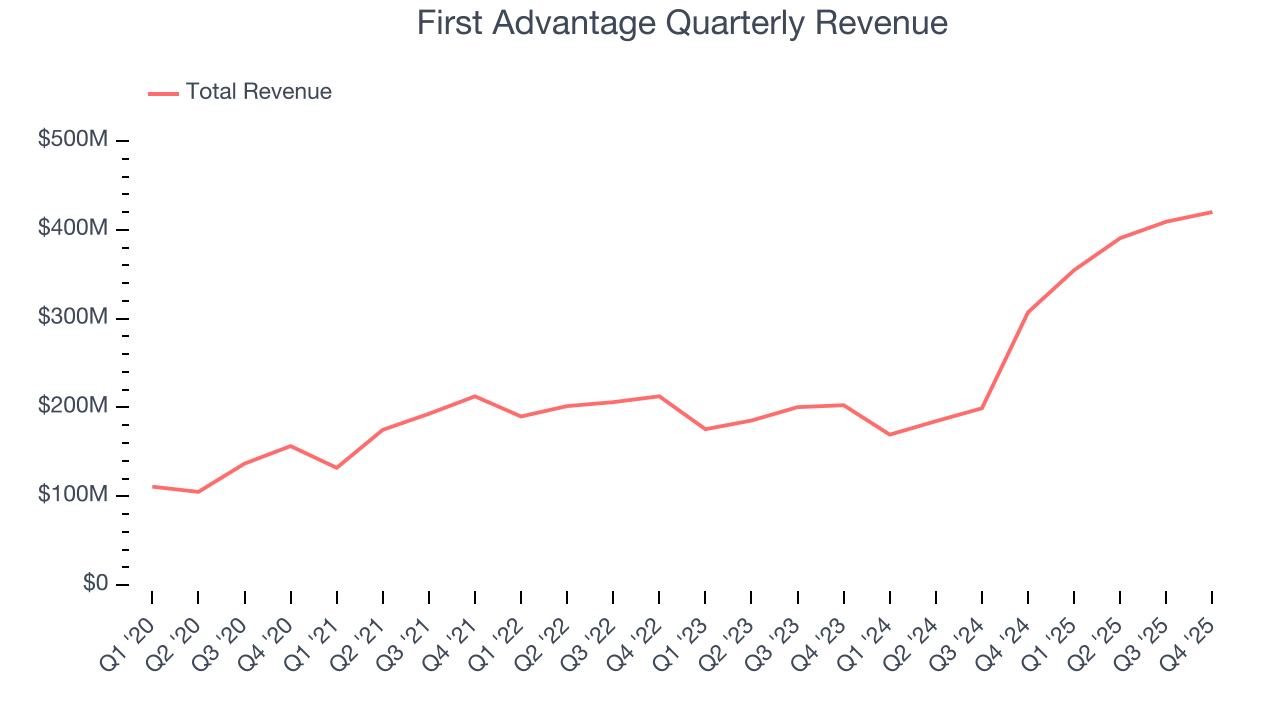

With $1.57 billion in revenue over the past 12 months, First Advantage is a mid-sized business services company, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale. On the bright side, it can still flex high growth rates because it’s working from a smaller revenue base.

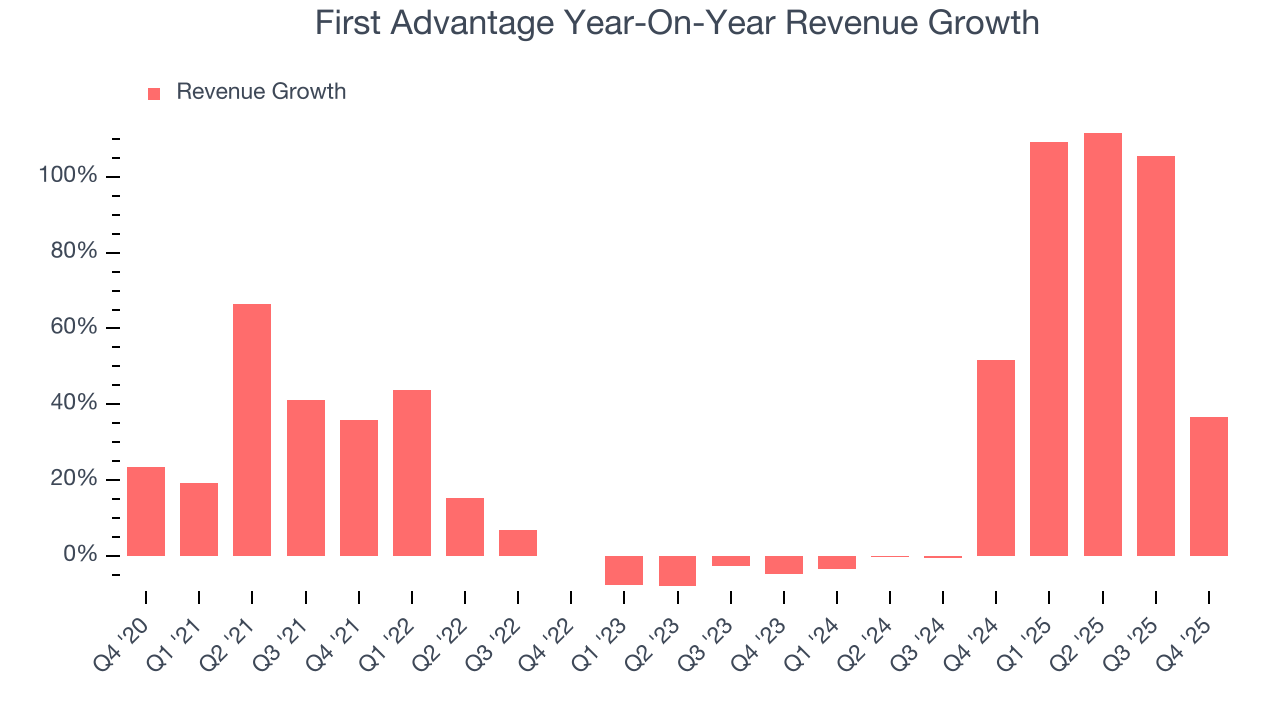

As you can see below, First Advantage grew its sales at an incredible 25.3% compounded annual growth rate over the last five years. This shows it had high demand, a useful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. First Advantage’s annualized revenue growth of 43.6% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, First Advantage reported wonderful year-on-year revenue growth of 36.8%, and its $420 million of revenue exceeded Wall Street’s estimates by 7.3%.

Looking ahead, sell-side analysts expect revenue to grow 5.7% over the next 12 months, a deceleration versus the last two years. Still, this projection is above the sector average and indicates the market is baking in some success for its newer products and services.

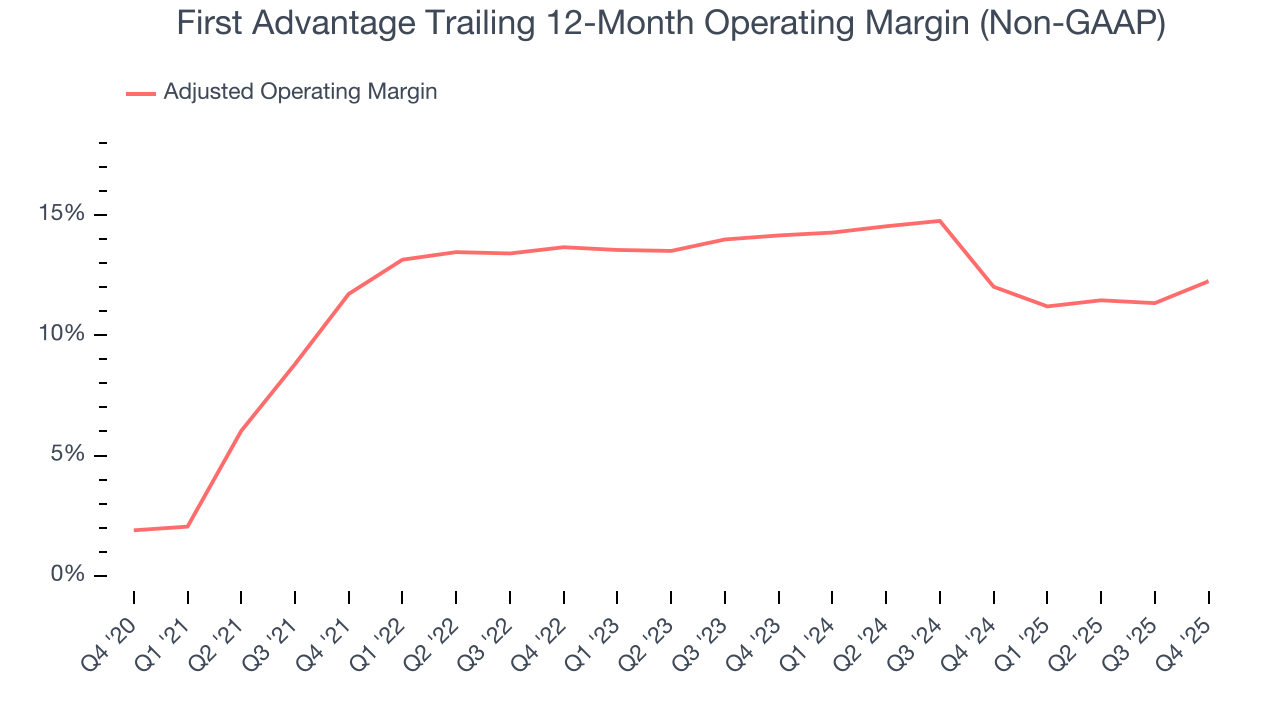

6. Adjusted Operating Margin

Adjusted operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D. It also removes various one-time costs to paint a better picture of normalized profits.

First Advantage’s adjusted operating margin has generally stayed the same over the last 12 months, averaging 12.7% over the last five years. This profitability was solid for a business services business and shows it’s an efficient company that manages its expenses well.

Looking at the trend in its profitability, First Advantage’s adjusted operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, First Advantage generated an adjusted operating margin profit margin of 12.9%, up 4.1 percentage points year on year. This increase was a welcome development and shows it was more efficient.

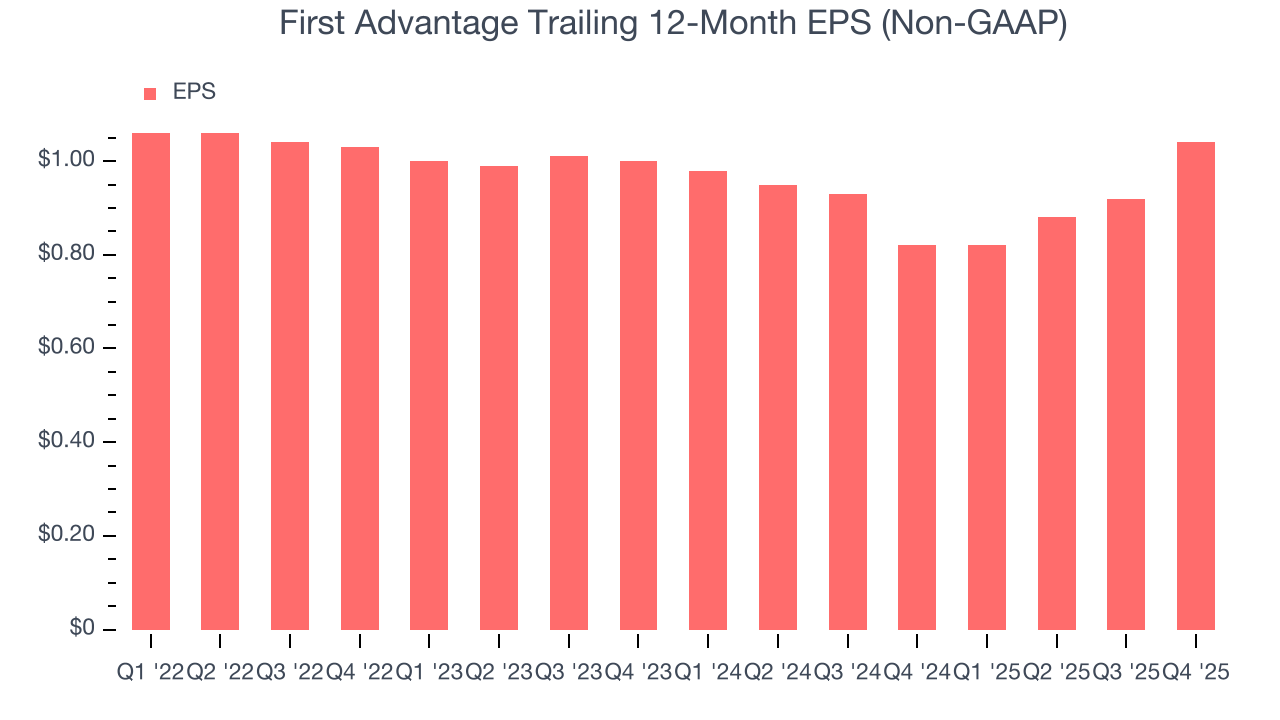

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

First Advantage’s full-year EPS was flat over the last four years, worse than the broader business services sector.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

First Advantage’s EPS grew at a weak 2% compounded annual growth rate over the last two years, lower than its 43.6% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

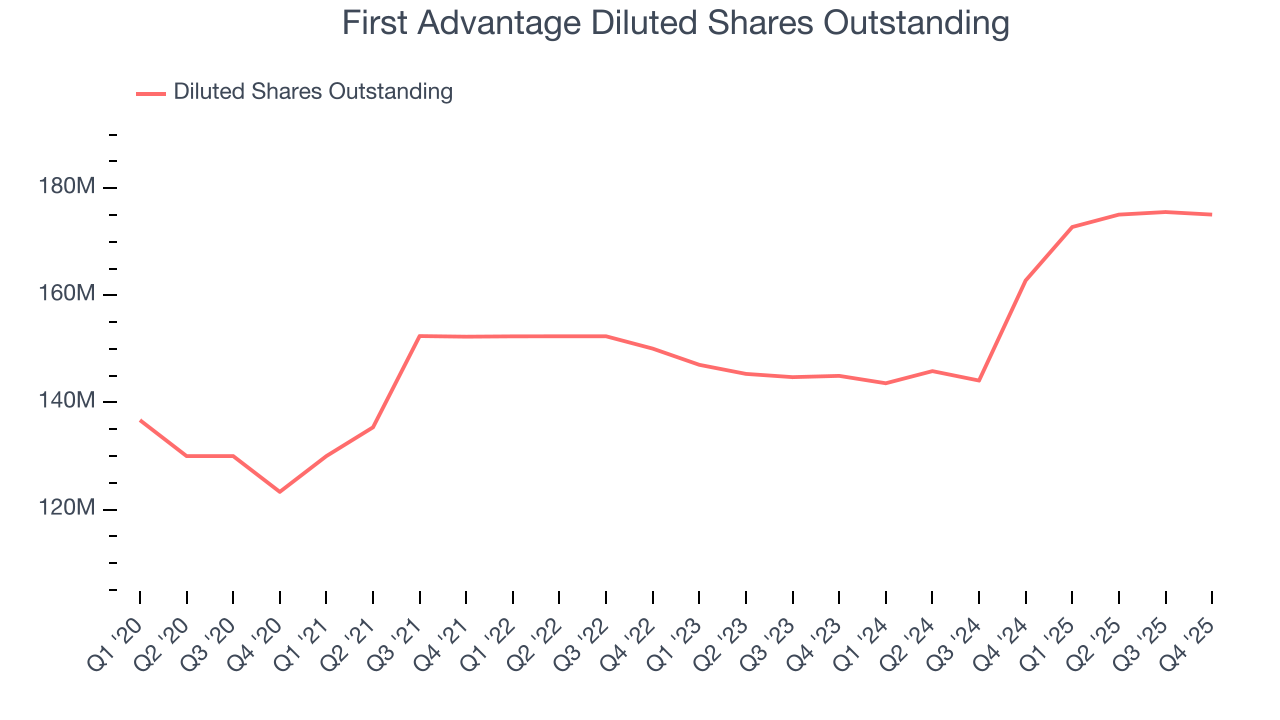

We can take a deeper look into First Advantage’s earnings to better understand the drivers of its performance. We mentioned earlier that First Advantage’s adjusted operating margin expanded this quarter, but a two-year view shows its margin has declinedwhile its share count has grown 20.8%. This means the company not only became less efficient with its operating expenses but also diluted its shareholders.

In Q4, First Advantage reported adjusted EPS of $0.30, up from $0.18 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects First Advantage’s full-year EPS of $1.04 to grow 15.3%.

8. Cash Is King

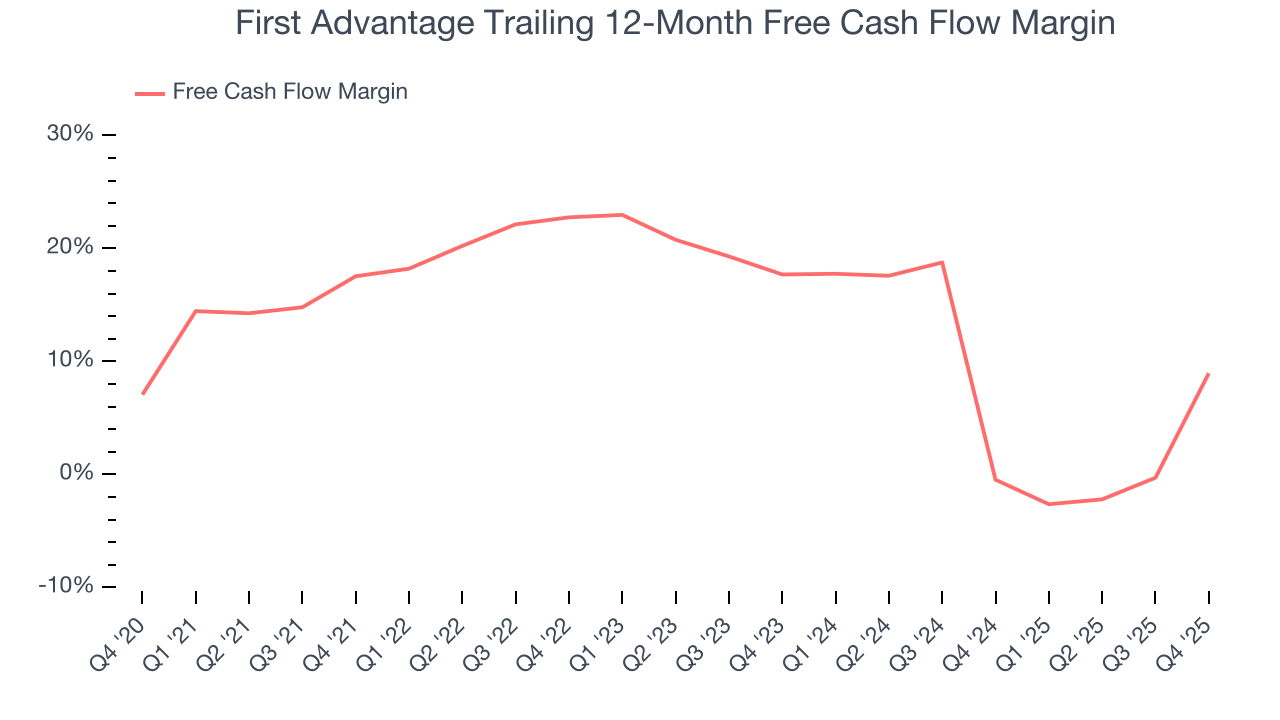

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

First Advantage has shown robust cash profitability, giving it an edge over its competitors and the ability to reinvest or return capital to investors. The company’s free cash flow margin averaged 12.3% over the last five years, quite impressive for a business services business.

Taking a step back, we can see that First Advantage’s margin dropped by 8.6 percentage points during that time. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level. If the longer-term trend returns, it could signal increasing investment needs and capital intensity.

First Advantage’s free cash flow clocked in at $49.07 million in Q4, equivalent to a 11.7% margin. Its cash flow turned positive after being negative in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends are more important.

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

First Advantage historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 0.7%, lower than the typical cost of capital (how much it costs to raise money) for business services companies.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. On average, First Advantage’s ROIC decreased by 4.2 percentage points annually each year over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

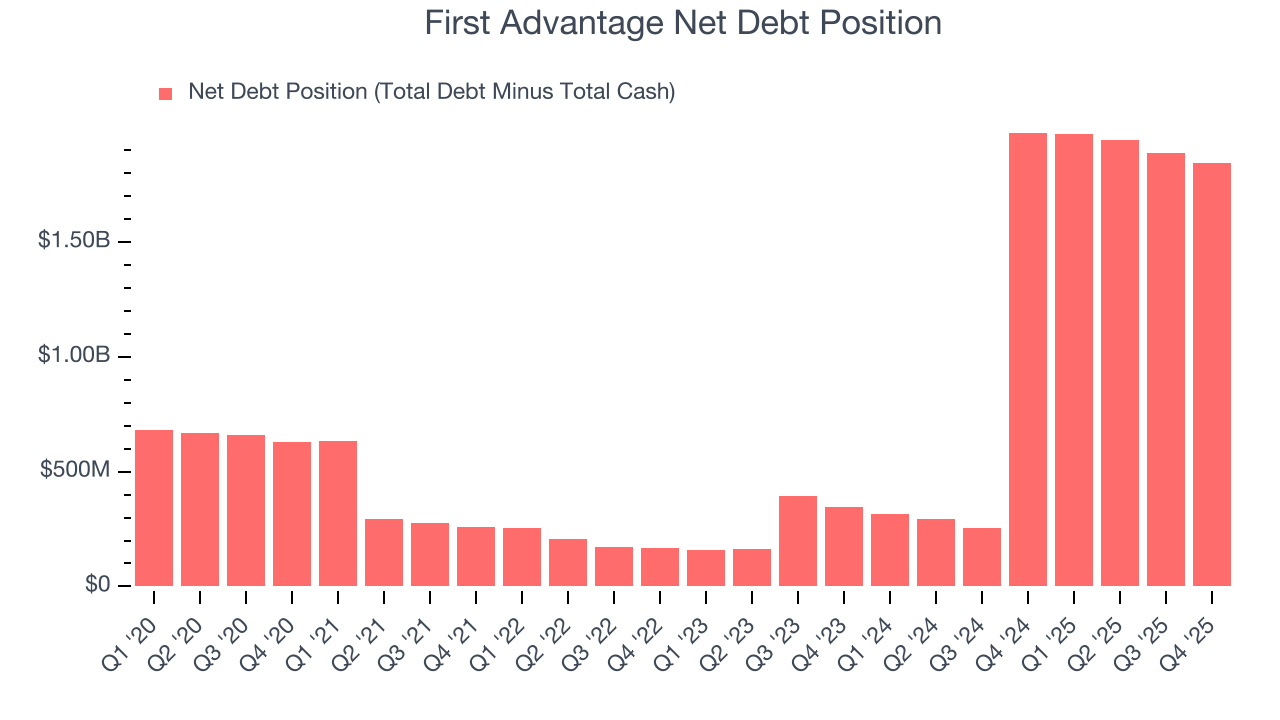

10. Balance Sheet Assessment

First Advantage reported $240.1 million of cash and $2.08 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $441.4 million of EBITDA over the last 12 months, we view First Advantage’s 4.2× net-debt-to-EBITDA ratio as safe. We also see its $168.7 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from First Advantage’s Q4 Results

We were impressed by how significantly First Advantage blew past analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock remained flat at $11.06 immediately following the results.

12. Is Now The Time To Buy First Advantage?

Updated: March 20, 2026 at 12:53 AM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own First Advantage, you should also grasp the company’s longer-term business quality and valuation.

First Advantage has a few positive attributes, but it doesn’t top our wishlist. First off, its revenue growth was exceptional over the last five years. And while First Advantage’s relatively low ROIC suggests management has struggled to find compelling investment opportunities, its projected EPS for the next year implies the company’s fundamentals will improve.

First Advantage’s P/E ratio based on the next 12 months is 8.9x. This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're pretty confident there are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $15 on the company (compared to the current share price of $10.97).