FuelCell Energy (FCEL)

We’d invest in FuelCell Energy. Its sales and EPS are anticipated to grow nicely over the next 12 months, a welcome sign for investors.― StockStory Analyst Team

1. News

2. Summary

Why We Like FuelCell Energy

Founded in 1969, FuelCell Energy (NASDAQ: FCEL) is a leading manufacturer and developer of carbonate fuel cell technology for stationary power generation.

- Annual revenue growth of 19.6% over the last five years was superb and indicates its market share increased during this cycle

- Earnings growth has trumped its peers over the last two years as its EPS has compounded at 31.9% annually

- Forecasted revenue growth of 11.6% for the next 12 months indicates its momentum over the last two years is sustainable

We’re fond of companies like FuelCell Energy. The valuation seems fair when considering its quality, so this could be a prudent time to buy some shares.

Why Is Now The Time To Buy FuelCell Energy?

FuelCell Energy is trading at $6.65 per share, or 1.7x forward price-to-sales. Looking at the industrials landscape today, FuelCell Energy’s qualities really stand out, and we like it at this price.

It seems like an opportune time to buy the stock if you believe in the long-term prospects of the business.

3. FuelCell Energy (FCEL) Research Report: Q4 CY2025 Update

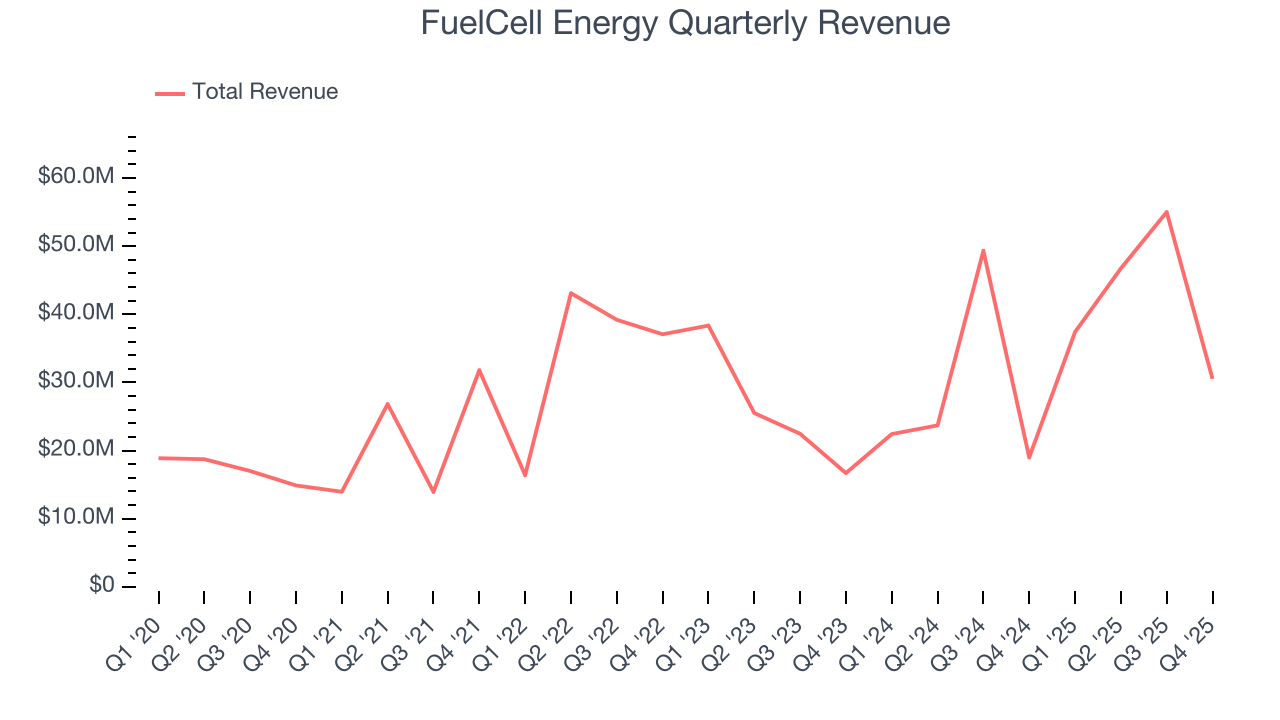

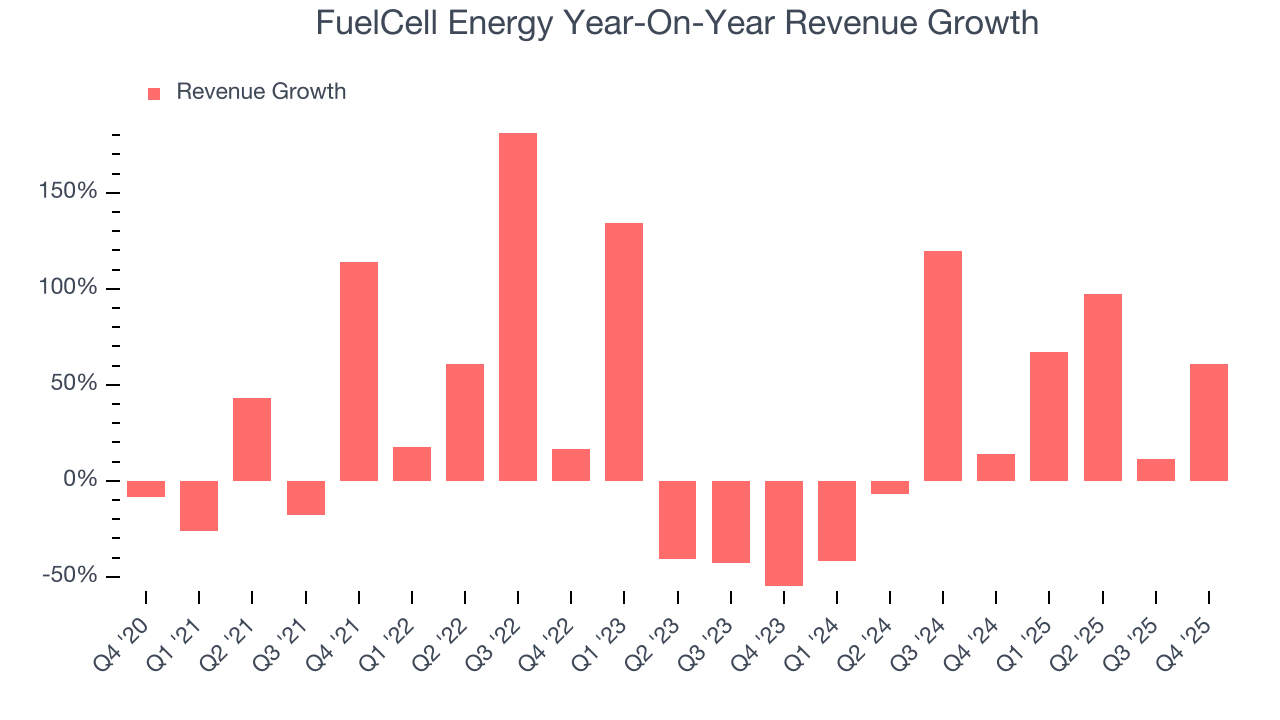

Carbonate fuel cell technology developer FuelCell Energy (NASDAQ:FCEL) missed Wall Street’s revenue expectations in Q4 CY2025, but sales rose 60.7% year on year to $30.53 million. Its non-GAAP loss of $0.52 per share was 23.1% above analysts’ consensus estimates.

FuelCell Energy (FCEL) Q4 CY2025 Highlights:

- Revenue: $30.53 million vs analyst estimates of $42.66 million (60.7% year-on-year growth, 28.4% miss)

- Adjusted EPS: -$0.52 vs analyst estimates of -$0.68 (23.1% beat)

- Adjusted EBITDA: -$17.03 million (-55.8% margin, 19.2% year-on-year growth)

- Adjusted EBITDA Margin: -55.8%, up from -111% in the same quarter last year

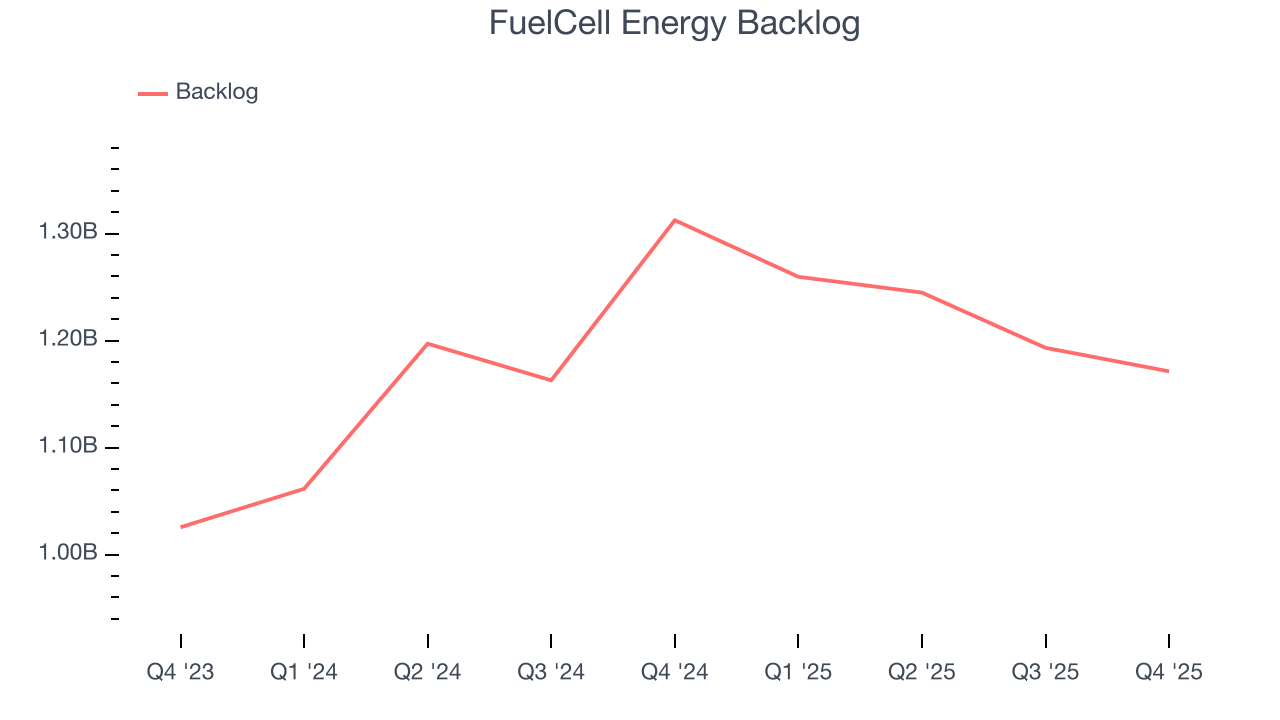

- Backlog: $1.17 billion at quarter end, down 10.8% year on year

- Market Capitalization: $349.8 million

Company Overview

Founded in 1969, FuelCell Energy (NASDAQ: FCEL) is a leading manufacturer and developer of carbonate fuel cell technology for stationary power generation.

The company focuses on designing, manufacturing, and selling fuel cell power plants for distributed power generation, offering products ranging from 250 kW to 3 MW in capacity. FuelCell Energy's primary technology is the Direct FuelCell (DFC), which generates electricity directly from a hydrocarbon fuel by reforming it inside the fuel cell to produce hydrogen.

FuelCell Energy's products are designed to meet the power requirements of various customers, including utilities, industrial facilities, data centers, and other commercial and institutional buildings. The company's fuel cells offer several advantages over traditional power generation methods, including higher fuel efficiency, lower emissions, and the ability to use multiple fuel sources such as natural gas, biogas, and coal gas.

FuelCell Energy operates a manufacturing facility in Torrington, Connecticut, with a production capacity of 50 MW per year. The company has plans to expand this capacity to 150 MW within its current facility and potentially up to 400 MW with additional land access. FuelCell Energy also maintains a testing and conditioning facility in Danbury, Connecticut, capable of processing 50 MW of fuel cell power plants annually.

FuelCell Energy's financial performance has historically been heavily dependent on government funding. The company is working to transition towards more commercial sales as its products move closer to widespread market adoption.

4. Renewable Energy

Renewable energy companies are buoyed by the secular trend of green energy that is upending traditional power generation. Those who innovate and evolve with this dynamic market can win share while those who continue to rely on legacy technologies can see diminishing demand, which includes headwinds from increasing regulation against “dirty” energy. Additionally, these companies are at the whim of economic cycles, as interest rates can impact the willingness to invest in renewable energy projects.

Competitors of FuelCell Energy include Bloom Energy Corporation (NYSE: BE), Plug Power (NASDAQ:PLUG), and Ballard Power Systems (NASDAQ: BLDP).

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, FuelCell Energy grew its sales at an incredible 19.6% compounded annual growth rate. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. FuelCell Energy’s annualized revenue growth of 28.3% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

We can better understand the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. FuelCell Energy’s backlog reached $1.17 billion in the latest quarter and averaged 8.5% year-on-year growth over the last two years. Because this number is lower than its revenue growth, we can see the company fulfilled orders at a faster rate than it added new orders to the backlog. This implies FuelCell Energy was operating efficiently but raises questions about the health of its sales pipeline.

This quarter, FuelCell Energy achieved a magnificent 60.7% year-on-year revenue growth rate, but its $30.53 million of revenue fell short of Wall Street’s lofty estimates.

Looking ahead, sell-side analysts expect revenue to grow 21.4% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is commendable and suggests the market is baking in success for its products and services.

6. Gross Margin & Pricing Power

For industrials businesses, cost of sales is usually comprised of the direct labor, raw materials, and supplies needed to offer a product or service. These costs can be impacted by inflation and supply chain dynamics in the short term and a company’s purchasing power and scale over the long term.

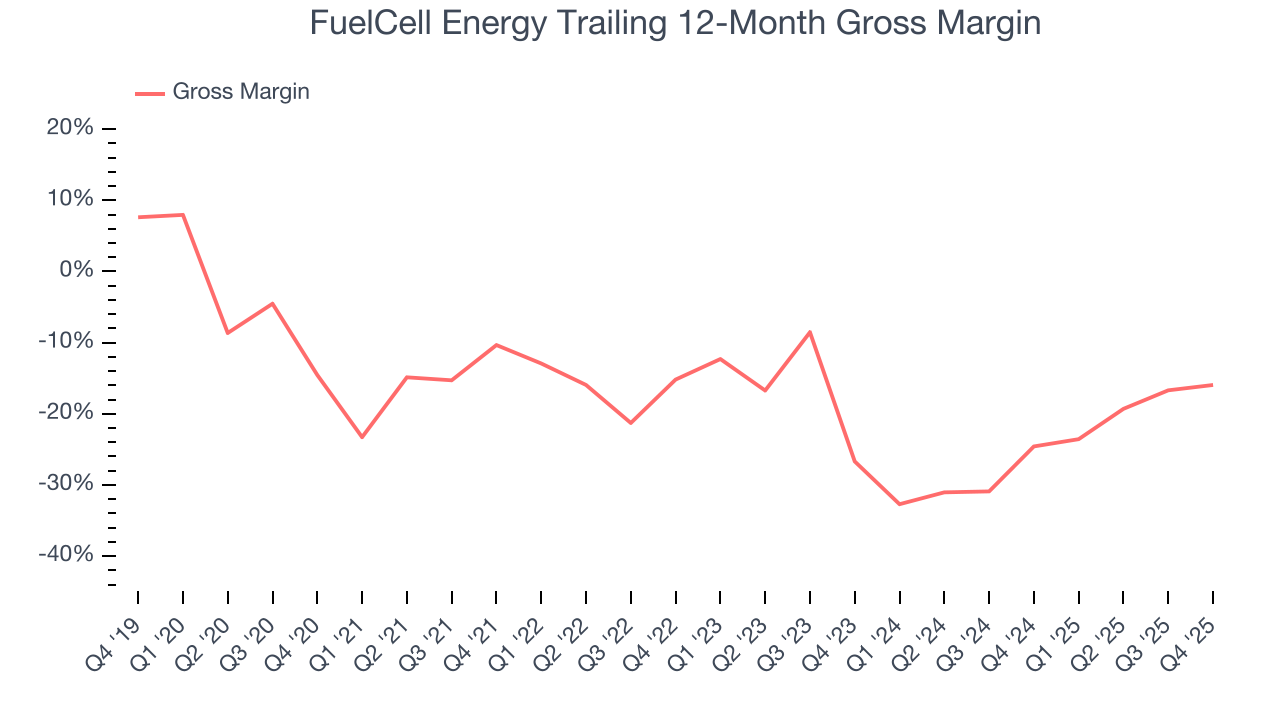

FuelCell Energy has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a negative 18.4% gross margin over the last five years. That means FuelCell Energy lost $18.42 for every $100 in revenue.

This quarter, FuelCell Energy’s gross profit margin was negative 19.2%. The company’s full-year margin was also negative, suggesting it needs to change its business model quickly.

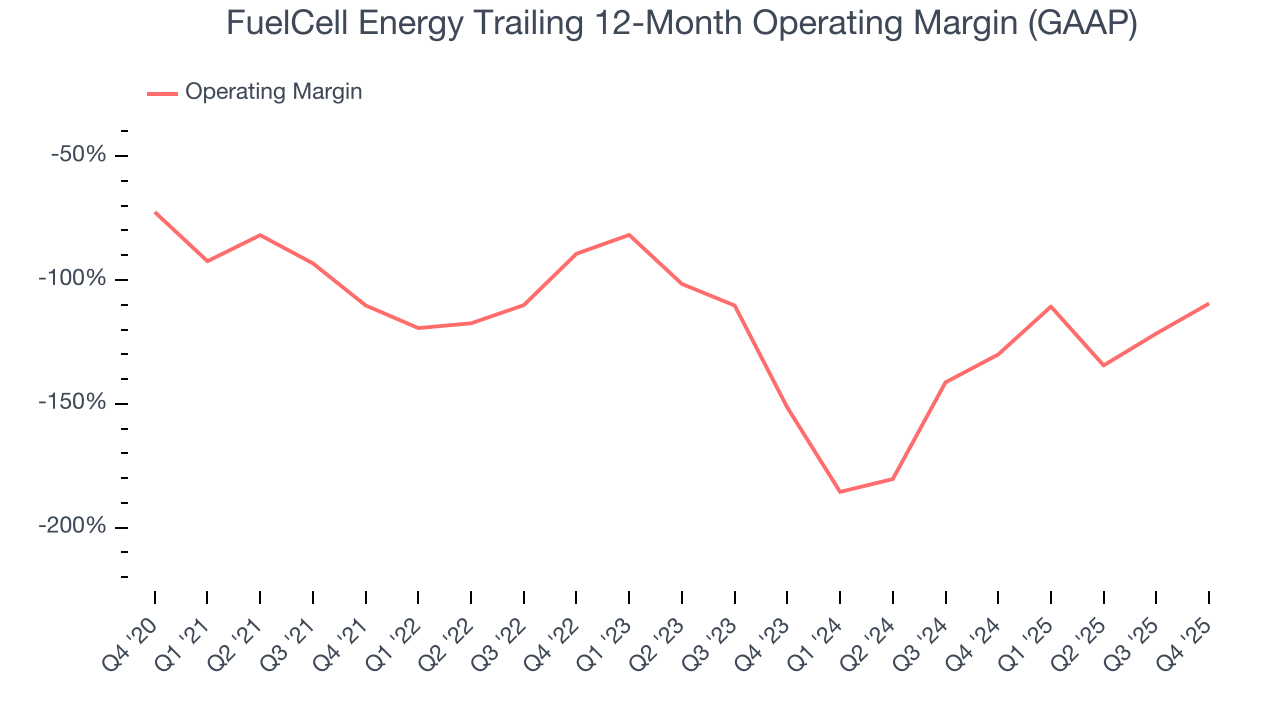

7. Operating Margin

FuelCell Energy’s operating margin has risen over the last 12 months, but it still averaged negative 116% over the last five years. This is due to its large expense base and inefficient cost structure. It might have a shot at long-term profitability if it can scale quickly and gain operating leverage.

Analyzing the trend in its profitability, FuelCell Energy’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, FuelCell Energy generated a negative 86.1% operating margin.

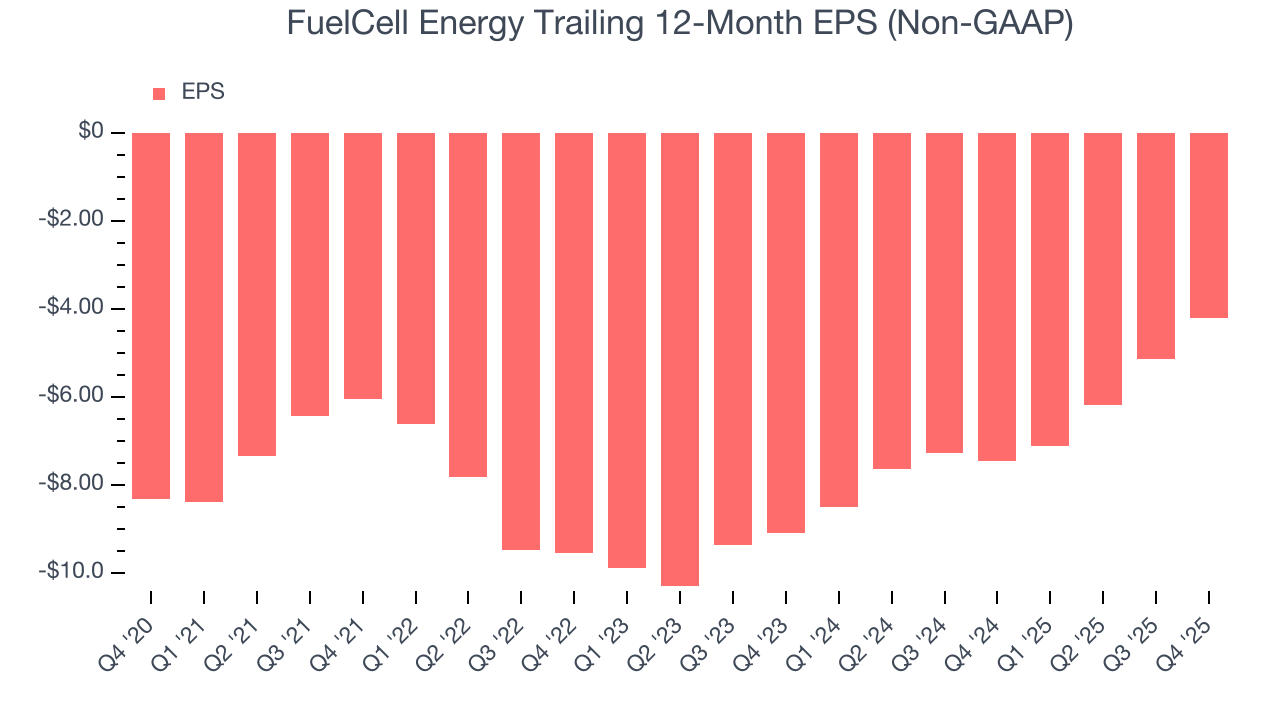

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Although FuelCell Energy’s full-year earnings are still negative, it reduced its losses and improved its EPS by 12.7% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability. We hope to see an inflection point soon.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For FuelCell Energy, its two-year annual EPS growth of 31.9% was higher than its five-year trend. We love it when earnings improve, but a caveat is that its EPS is still in the red.

In Q4, FuelCell Energy reported adjusted EPS of negative $0.52, up from negative $1.44 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects FuelCell Energy to improve its earnings losses. Analysts forecast its full-year EPS of negative $4.22 will advance to negative $2.38.

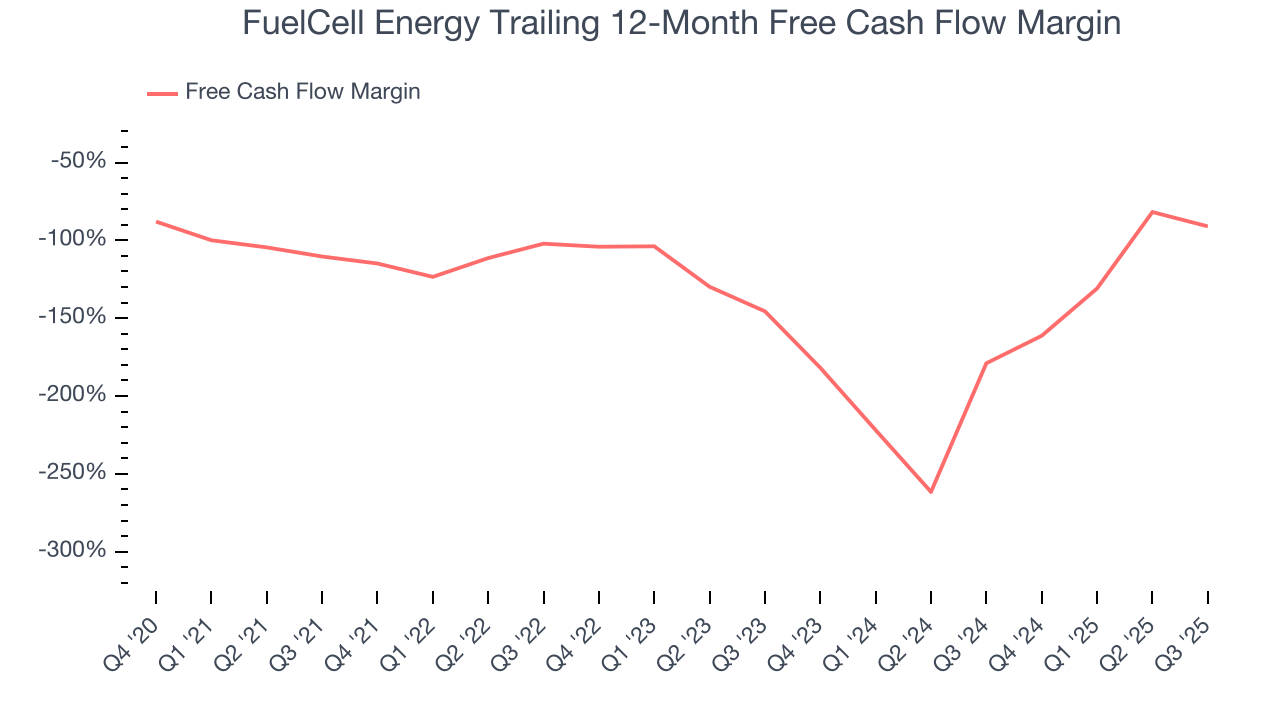

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

FuelCell Energy’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 122%, meaning it lit $121.55 of cash on fire for every $100 in revenue.

Taking a step back, an encouraging sign is that FuelCell Energy’s margin expanded by 19.1 percentage points during that time. In light of its glaring cash burn, however, this improvement is a bucket of hot water in a cold ocean.

10. Balance Sheet Assessment

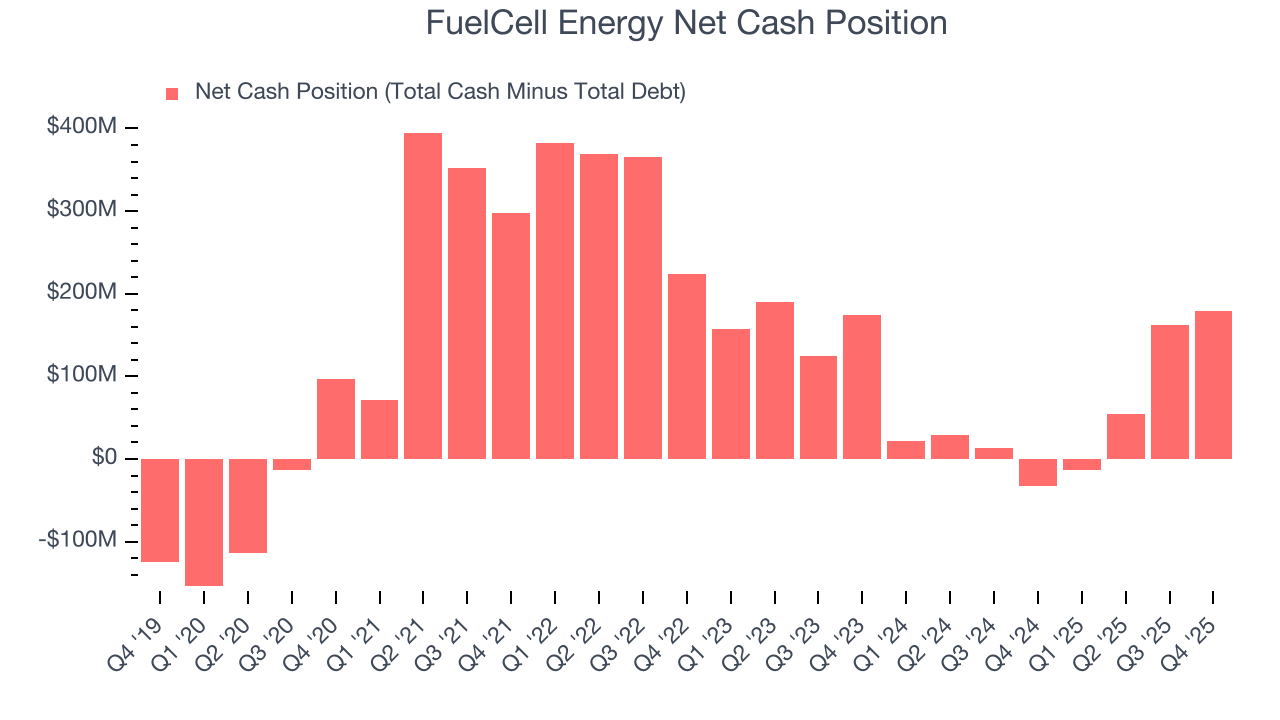

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

FuelCell Energy is a well-capitalized company with $329.5 million of cash and $150.7 million of debt on its balance sheet. This $178.8 million net cash position is 52.6% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

11. Key Takeaways from FuelCell Energy’s Q4 Results

It was good to see FuelCell Energy beat analysts’ EPS expectations this quarter. On the other hand, its revenue missed and its EBITDA fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 3.6% to $7.33 immediately following the results.

12. Is Now The Time To Buy FuelCell Energy?

Updated: March 20, 2026 at 11:28 PM EDT

Before investing in or passing on FuelCell Energy, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

There are multiple reasons why we think FuelCell Energy is an amazing business. For starters, its revenue growth was exceptional over the last five years. And while its operating margins reveal poor profitability compared to other industrials companies, its rising cash profitability gives it more optionality. On top of that, FuelCell Energy’s projected EPS for the next year implies the company’s fundamentals will improve.

FuelCell Energy’s forward price-to-sales ratio is 1.7x. Looking at the industrials landscape today, FuelCell Energy’s qualities really stand out, and we like it at this price.

Wall Street analysts have a consensus one-year price target of $8.24 on the company (compared to the current share price of $6.65), implying they see 23.9% upside in buying FuelCell Energy in the short term.