FirstCash (FCFS)

We aren’t fans of FirstCash. It’s recently struggled to grow its revenue, a worrying sign for investors seeking high-quality stocks.― StockStory Analyst Team

1. News

2. Summary

Why FirstCash Is Not Exciting

Offering a financial lifeline to the unbanked and credit-constrained since 1988, FirstCash (NASDAQ:FCFS) operates pawn stores across the U.S. and Latin America while also providing retail point-of-sale payment solutions for credit-constrained consumers.

- Products and services are facing significant credit quality challenges during this cycle as tangible book value per share has declined by 159% annually over the last five years

- On the plus side, its additional sales over the last five years increased its profitability as the 19.2% annual growth in its earnings per share outpaced its revenue

FirstCash doesn’t satisfy our quality benchmarks. There are better opportunities in the market.

Why There Are Better Opportunities Than FirstCash

FirstCash’s stock price of $171.80 implies a valuation ratio of 17.6x forward P/E. Not only does FirstCash trade at a premium to companies in the financials space, but this multiple is also high for its fundamentals.

We prefer to invest in similarly-priced but higher-quality companies with superior earnings growth.

3. FirstCash (FCFS) Research Report: Q4 CY2025 Update

Pawn store operator FirstCash Holdings (NASDAQ:FCFS) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 19.8% year on year to $1.06 billion. Its non-GAAP profit of $2.64 per share was 4.2% above analysts’ consensus estimates.

FirstCash (FCFS) Q4 CY2025 Highlights:

- Revenue: $1.06 billion vs analyst estimates of $1.02 billion (19.8% year-on-year growth, 3.5% beat)

- Pre-tax Profit: $142.8 million (13.5% margin)

- Adjusted EPS: $2.64 vs analyst estimates of $2.53 (4.2% beat)

- Market Capitalization: $7.59 billion

Company Overview

Offering a financial lifeline to the unbanked and credit-constrained since 1988, FirstCash (NASDAQ:FCFS) operates pawn stores across the U.S. and Latin America while also providing retail point-of-sale payment solutions for credit-constrained consumers.

FirstCash's pawn operations function as neighborhood-based retail locations where customers can both buy and sell pre-owned consumer products ranging from jewelry and electronics to tools and musical instruments. These stores also provide non-recourse pawn loans secured by personal property, requiring no credit checks and carrying no legal obligation for repayment. If a customer chooses not to repay their loan, FirstCash simply retains and sells the collateral rather than pursuing collections or reporting to credit agencies.

The company maintains a significant footprint with pawn stores in 29 U.S. states, 32 Mexican states, and locations in Guatemala, El Salvador, and Colombia. Its U.S. stores are strategically concentrated in the Southeast, Midwest, Southwest, and Mountain West regions where regulations and demographics favor profitable operations.

Through its American First Finance (AFF) subsidiary, FirstCash offers three main retail payment solutions: lease-to-own arrangements, retail installment sales agreements, and bank-originated installment loans. These products are available through approximately 13,600 merchant partner locations and e-commerce platforms across 26 vertical channels. For example, a customer unable to qualify for traditional financing might use AFF's lease-to-own option to purchase furniture, making affordable payments over 6-24 months with the option to own the item at the end of the term.

FirstCash experiences seasonal patterns in its business, with pawn loan balances typically growing in the third and fourth quarters, followed by increased repayments in the first quarter when U.S. customers receive tax refunds. Retail sales peak during the fourth quarter holiday shopping season.

4. Personal Loan

Personal loan providers offer unsecured credit for various consumer needs. The sector benefits from digital application processes, increasing consumer comfort with online financial services, and opportunities in underserved credit segments. Headwinds include credit risk management in unsecured lending, regulatory oversight of lending practices, and intense competition affecting margins from both traditional and fintech lenders.

FirstCash's pawn store competitors include EZCORP (NASDAQ:EZPW) and privately-held Cash America, while its retail POS payment solutions business competes with Affirm (NASDAQ:AFRM), Katapult (NASDAQ:KPLT), Progressive Leasing (NYSE:PRG), and Rent-A-Center (NASDAQ:RCII).

5. Revenue Growth

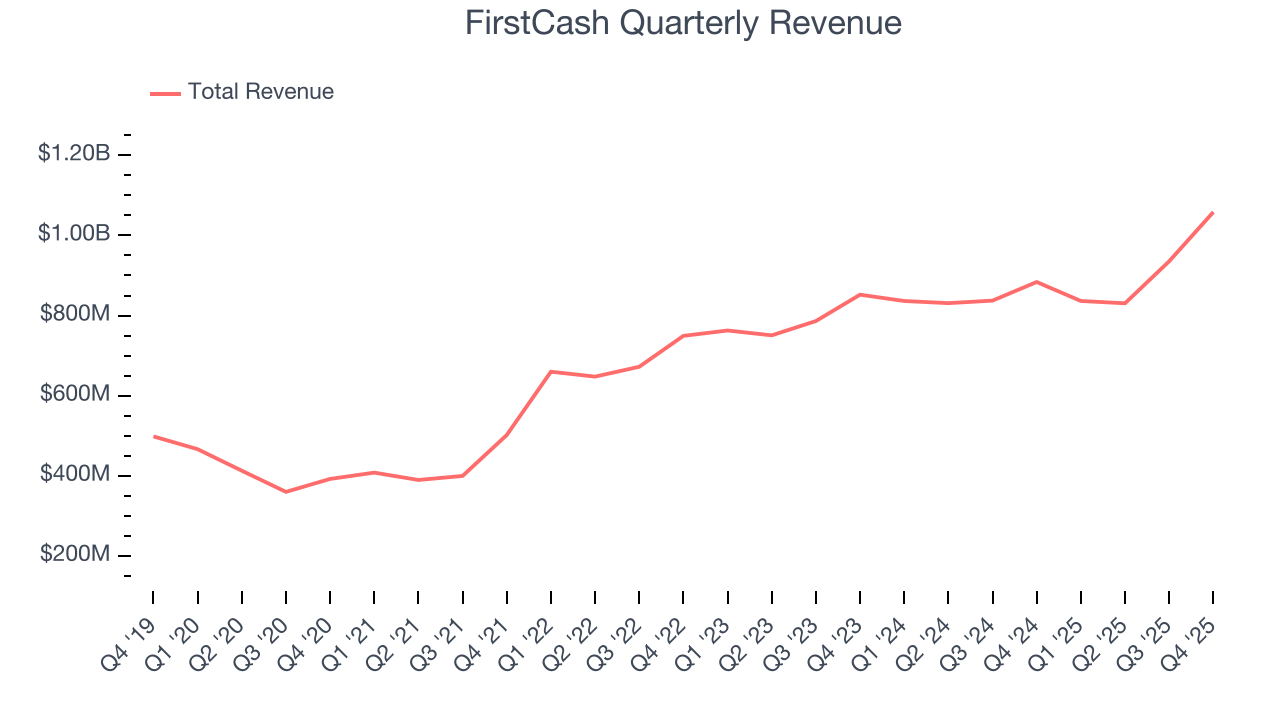

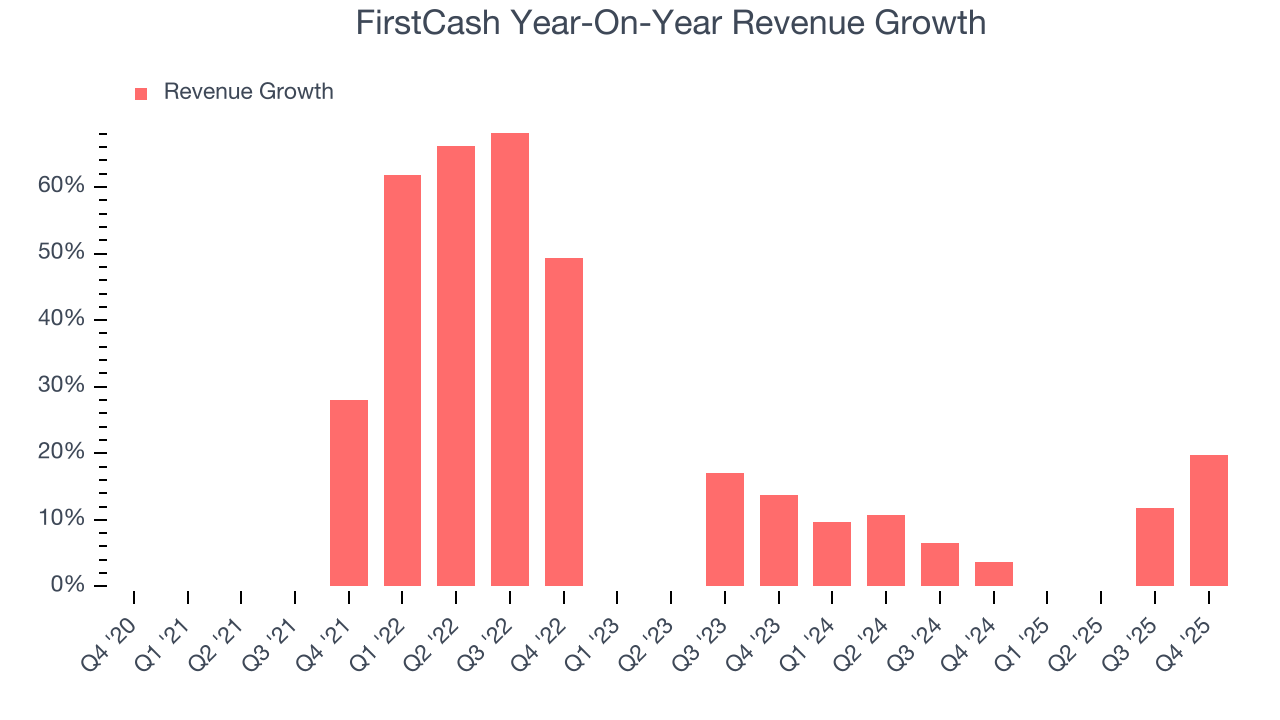

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, FirstCash’s 17.5% annualized revenue growth over the last five years was impressive. Its growth beat the average financials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. FirstCash’s annualized revenue growth of 7.8% over the last two years is below its five-year trend, but we still think the results were respectable.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, FirstCash reported year-on-year revenue growth of 19.8%, and its $1.06 billion of revenue exceeded Wall Street’s estimates by 3.5%.

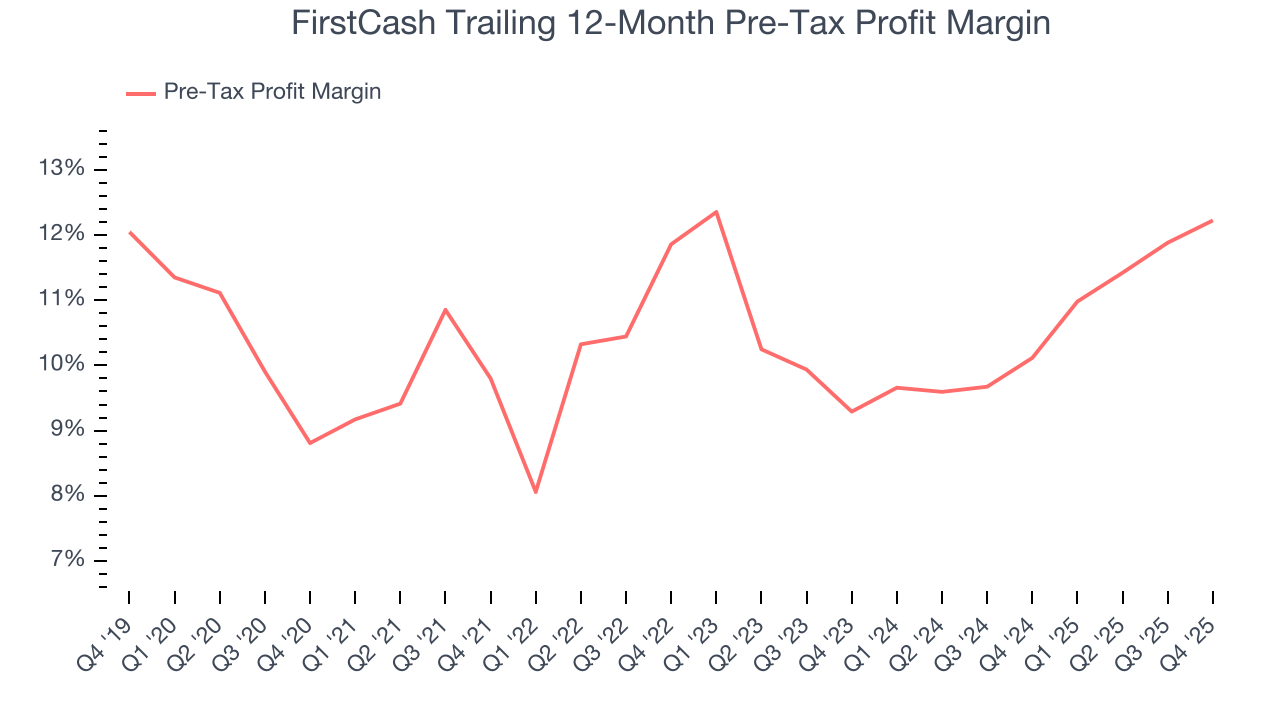

6. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For Personal Loan companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

This is because for financials businesses, interest income and expense should be factored into the definition of profit but taxes - which are largely out of a company's control - should not.

Over the last five years, FirstCash’s pre-tax profit margin has fallen by 3.4 percentage points, going from 9.8% to 12.2%. It has also expanded by 2.9 percentage points on a two-year basis, showing its expenses have consistently grown at a slower rate than revenue. This typically signals prudent management.

In Q4, FirstCash’s pre-tax profit margin was 13.5%. This result was 1.1 percentage points better than the same quarter last year.

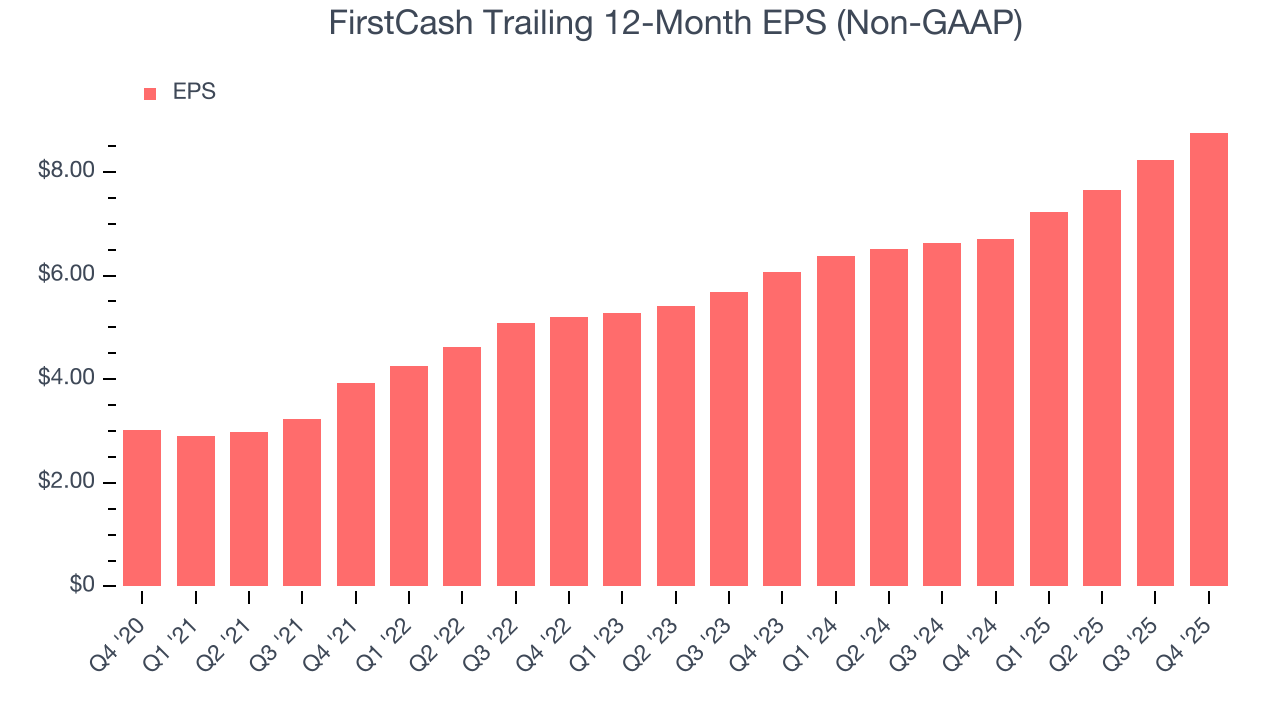

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

FirstCash’s EPS grew at a spectacular 23.8% compounded annual growth rate over the last five years, higher than its 17.5% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For FirstCash, its two-year annual EPS growth of 20.1% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q4, FirstCash reported adjusted EPS of $2.64, up from $2.12 in the same quarter last year. This print beat analysts’ estimates by 4.2%. Over the next 12 months, Wall Street expects FirstCash’s full-year EPS of $8.76 to grow 15.8%.

8. Return on Equity

Return on equity (ROE) reveals the profit generated per dollar of shareholder equity, which represents a key source of bank funding. Banks maintaining elevated ROE levels tend to accelerate wealth creation for shareholders via earnings retention, buybacks, and distributions.

Over the last five years, FirstCash has averaged an ROE of 12.3%, respectable for a company operating in a sector where the average shakes out around 10% and those putting up 25%+ are greatly admired.

9. Balance Sheet Assessment

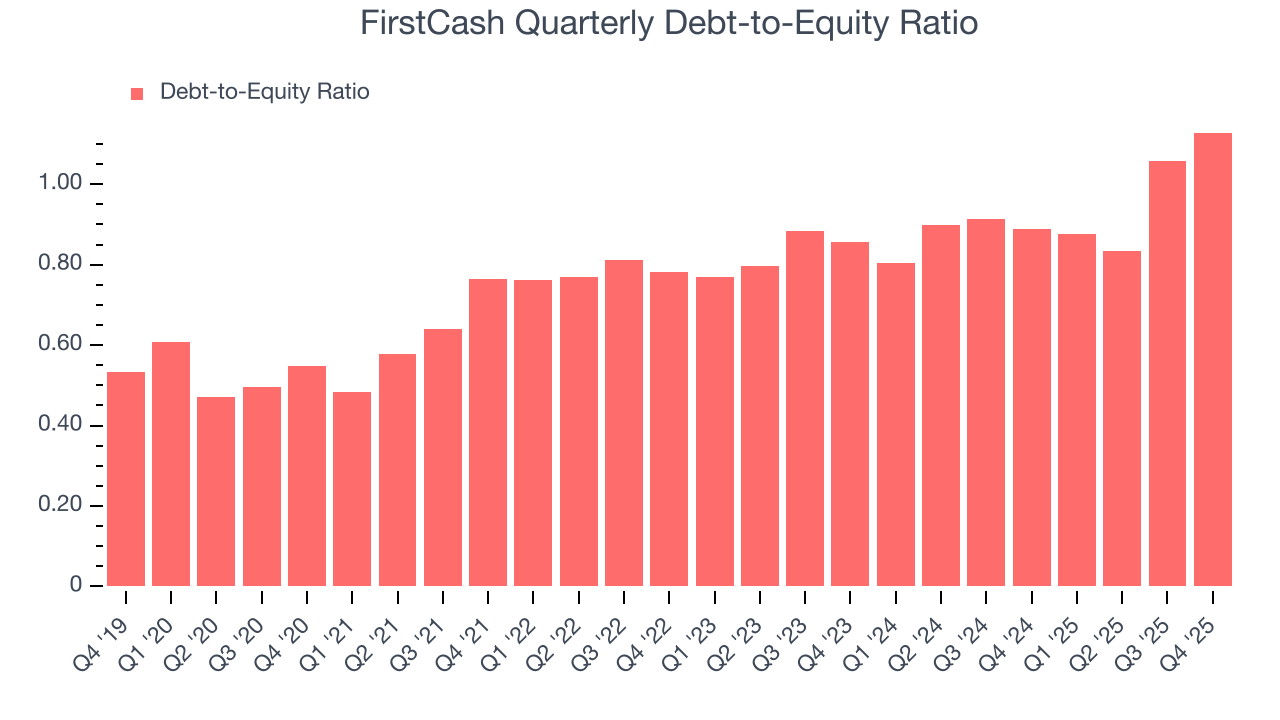

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

FirstCash currently has $2.57 billion of debt and $2.28 billion of shareholder's equity on its balance sheet, and over the past four quarters, has averaged a debt-to-equity ratio of 1×. We think this is safe and raises no red flags. In general, we’re comfortable with any ratio below 3.5× for a financials business.

10. Key Takeaways from FirstCash’s Q4 Results

It was encouraging to see FirstCash beat analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The stock remained flat at $171.80 immediately after reporting.

11. Is Now The Time To Buy FirstCash?

Updated: February 5, 2026 at 6:10 AM EST

Before investing in or passing on FirstCash, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

For starters, its revenue growth was impressive over the last five years. On top of that, its spectacular EPS growth over the last five years shows its profits are trickling down to shareholders, and its expanding pre-tax profit margin shows the business has become more efficient.

FirstCash’s P/E ratio based on the next 12 months is 16.9x. While this valuation is fair, the upside isn’t great compared to the potential downside. We're pretty confident there are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $189.60 on the company (compared to the current share price of $171.80).