Sezzle (SEZL)

We’re not sold on Sezzle. Its negative returns on capital suggest it eroded shareholder value by squandering business opportunities.― StockStory Analyst Team

1. News

2. Summary

Why Sezzle Is Not Exciting

Founded in 2016 as an alternative to traditional credit cards for younger shoppers, Sezzle (NASDAQ:SEZL) provides a payment platform that allows consumers to split purchases into four interest-free installments over six weeks at participating retailers.

- Push for growth has led to negative returns on capital, signaling value destruction

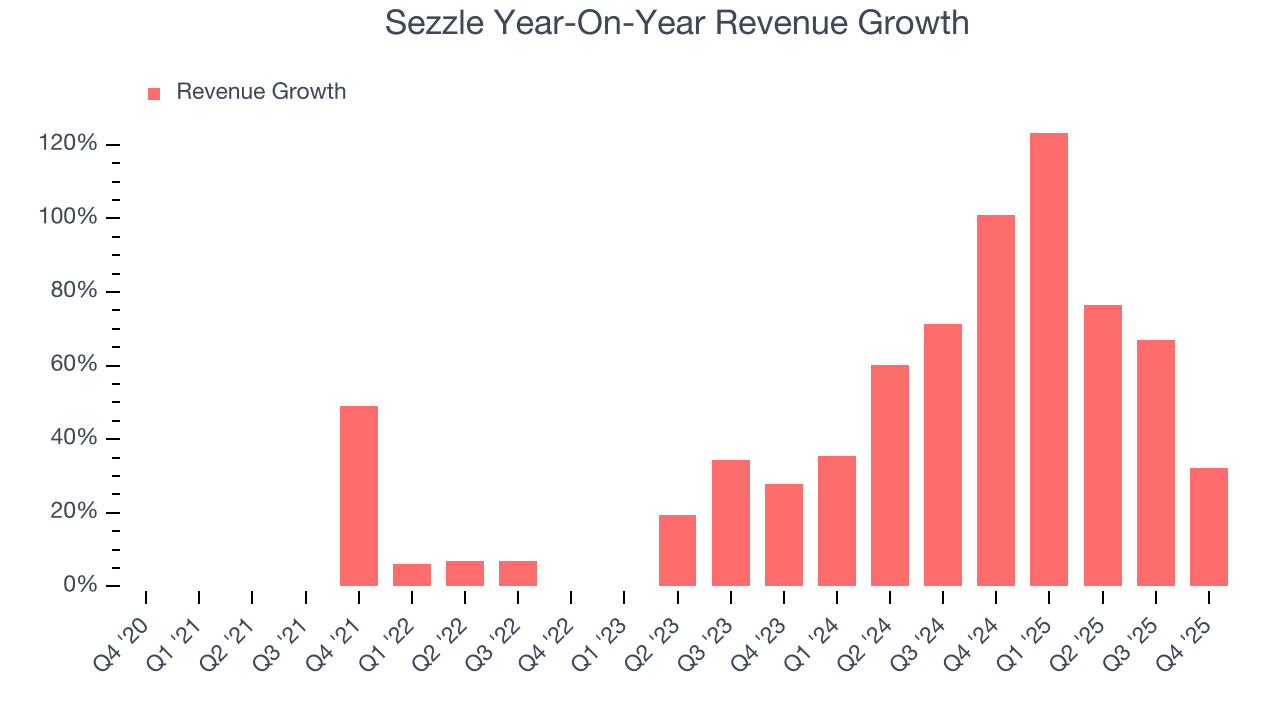

- A consolation is that its annual revenue growth of 50.3% over the past five years was outstanding, reflecting market share gains this cycle

Sezzle doesn’t meet our quality standards. We’re on the lookout for more interesting opportunities.

Why There Are Better Opportunities Than Sezzle

At $66.23 per share, Sezzle trades at 13.9x forward P/E. The current valuation may be fair, but we’re still passing on this stock due to better alternatives out there.

We’d rather invest in similarly-priced but higher-quality companies with more reliable earnings growth.

3. Sezzle (SEZL) Research Report: Q4 CY2025 Update

Buy-now-pay-later service Sezzle (NASDAQCM:SEZL) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 32.2% year on year to $129.9 million. Its GAAP profit of $1.21 per share was 25.6% above analysts’ consensus estimates.

Sezzle (SEZL) Q4 CY2025 Highlights:

- Revenue: $129.9 million vs analyst estimates of $126.4 million (32.2% year-on-year growth, 2.7% beat)

- Pre-tax Profit: $51.58 million (39.7% margin)

- EPS (GAAP): $1.21 vs analyst estimates of $0.96 (25.6% beat)

- Market Capitalization: $2.21 billion

Company Overview

Founded in 2016 as an alternative to traditional credit cards for younger shoppers, Sezzle (NASDAQ:SEZL) provides a payment platform that allows consumers to split purchases into four interest-free installments over six weeks at participating retailers.

Sezzle's buy-now-pay-later (BNPL) solution integrates with merchants' checkout systems, both online and in physical stores. When shoppers select Sezzle at checkout, they pay 25% upfront and the remaining balance in three equal bi-weekly payments, with no interest charges if payments are made on time. This payment structure appeals particularly to millennial and Gen Z consumers who may be wary of traditional credit products but still want purchasing flexibility.

For merchants, Sezzle serves as more than just a payment processor—it's a tool for increasing sales. Retailers typically see higher conversion rates and larger average order values when offering Sezzle as a payment option, as it removes the barrier of upfront cost for consumers. The company assumes the credit risk, paying merchants in full at the time of purchase while collecting the installments from consumers.

Sezzle's revenue comes primarily from merchant fees, typically a percentage of the transaction value plus a fixed fee per transaction. The company also generates income from late payment fees when consumers miss scheduled payments, though its business model emphasizes responsible lending through soft credit checks and spending limits tailored to each user's payment history.

The company differentiates itself in the competitive BNPL market through its user-friendly mobile app, which allows consumers to track payments, discover partner retailers, and access exclusive deals. Sezzle also maintains B Corporation certification, reflecting its commitment to social responsibility and ethical business practices in the financial technology sector.

4. Personal Loan

Personal loan providers offer unsecured credit for various consumer needs. The sector benefits from digital application processes, increasing consumer comfort with online financial services, and opportunities in underserved credit segments. Headwinds include credit risk management in unsecured lending, regulatory oversight of lending practices, and intense competition affecting margins from both traditional and fintech lenders.

Sezzle competes in the increasingly crowded buy-now-pay-later space against larger players like Affirm (NASDAQ:AFRM), Block's Afterpay (NYSE:SQ), Klarna, and PayPal's Pay in 4 (NASDAQ:PYPL), as well as traditional credit card companies expanding into installment payment options.

5. Revenue Growth

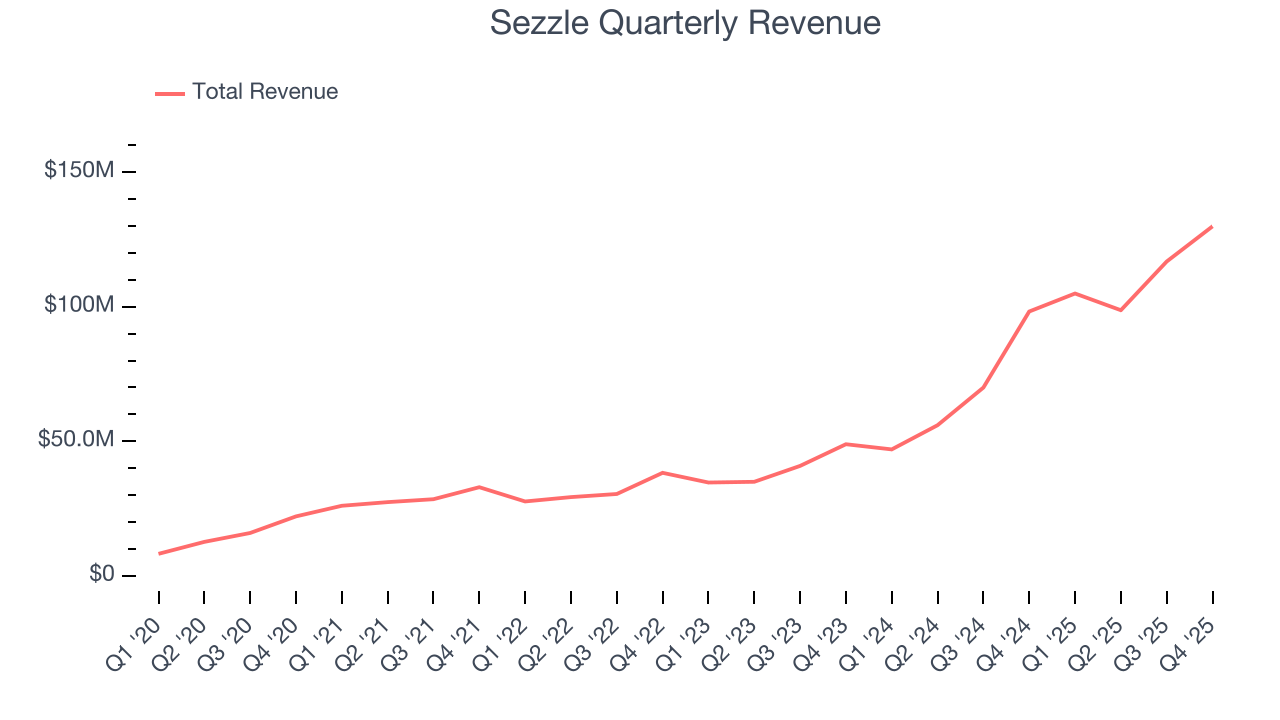

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Luckily, Sezzle’s revenue grew at an incredible 50.3% compounded annual growth rate over the last five years. Its growth beat the average financials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Sezzle’s annualized revenue growth of 68.1% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Sezzle reported wonderful year-on-year revenue growth of 32.2%, and its $129.9 million of revenue exceeded Wall Street’s estimates by 2.7%.

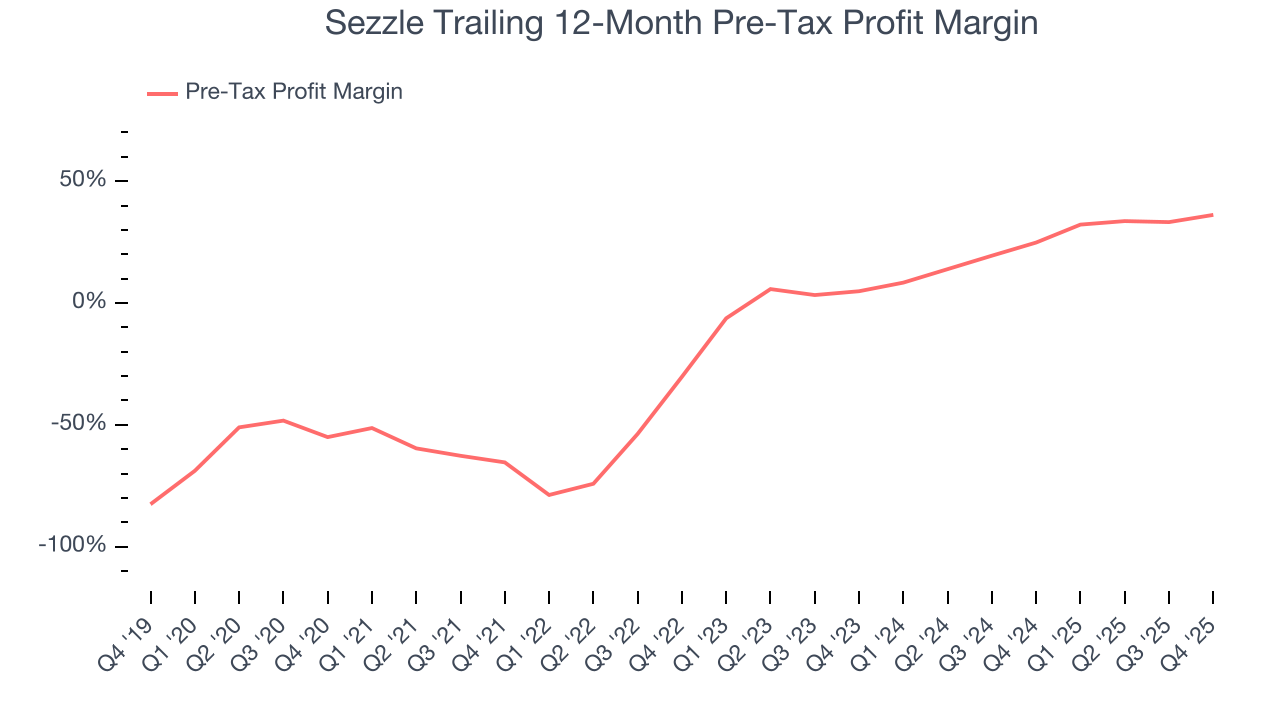

6. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For Personal Loan companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

Interest income and expenses play a big role in financial institutions' profitability, so they should be factored into the definition of profit. Taxes, however, should not as they are largely out of a company's control. This is pre-tax profit by definition.

Over the last five years, Sezzle’s pre-tax profit margin has fallen by 91.2 percentage points, going from negative 65.4% to 36.2%. It has also expanded by 31.3 percentage points on a two-year basis, showing its expenses have consistently grown at a slower rate than revenue. This typically signals prudent management.

Sezzle’s pre-tax profit margin came in at 39.7% this quarter. This result was 11.5 percentage points better than the same quarter last year.

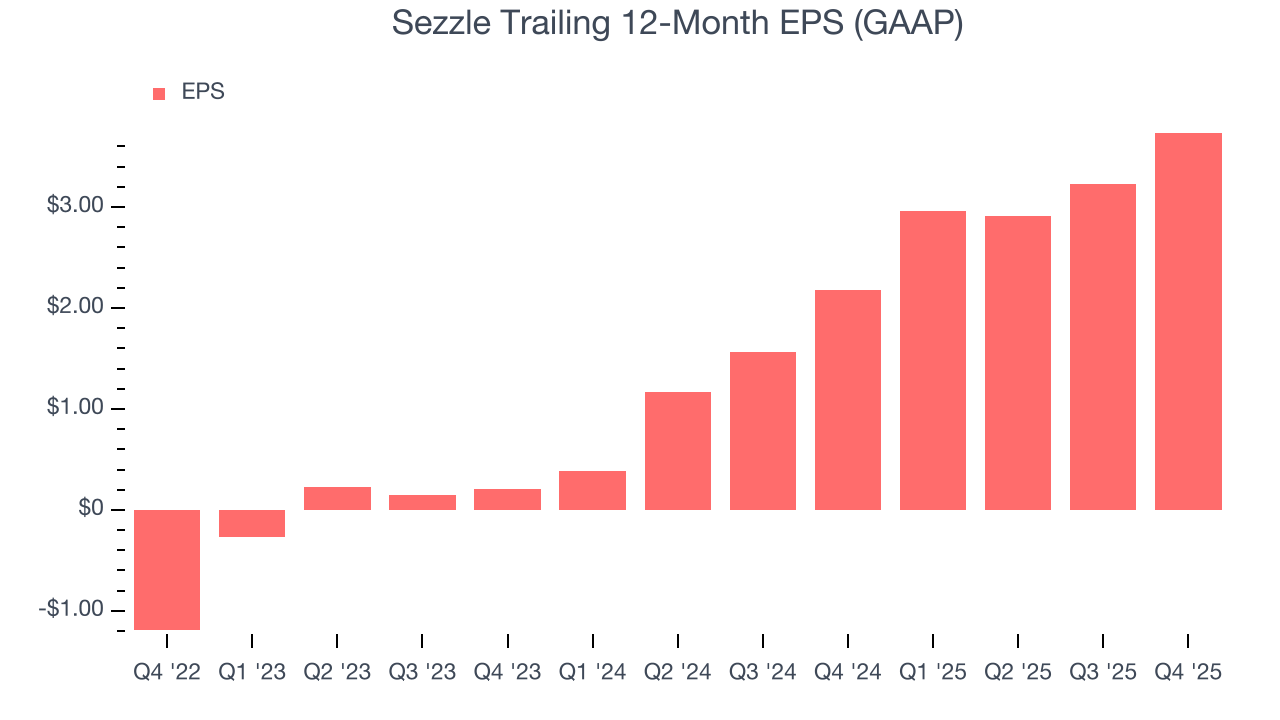

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sezzle’s full-year EPS flipped from negative to positive over the last three years. This is a good sign and shows it’s at an inflection point.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Sezzle, its two-year annual EPS growth of 323% was higher than its three-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q4, Sezzle reported EPS of $1.21, up from $0.70 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Sezzle’s full-year EPS of $3.73 to grow 24.2%.

8. Return on Equity

Return on equity, or ROE, tells us how much profit a company generates for each dollar of shareholder equity, a key funding source for banks. Over a long period, banks with high ROE tend to compound shareholder wealth faster through retained earnings, buybacks, and dividends.

Over the last five years, Sezzle has averaged an ROE of negative 5%, a bad result not only in absolute terms but also relative to the majority of firms putting up 25%+. It also shows that Sezzle has little to no competitive moat.

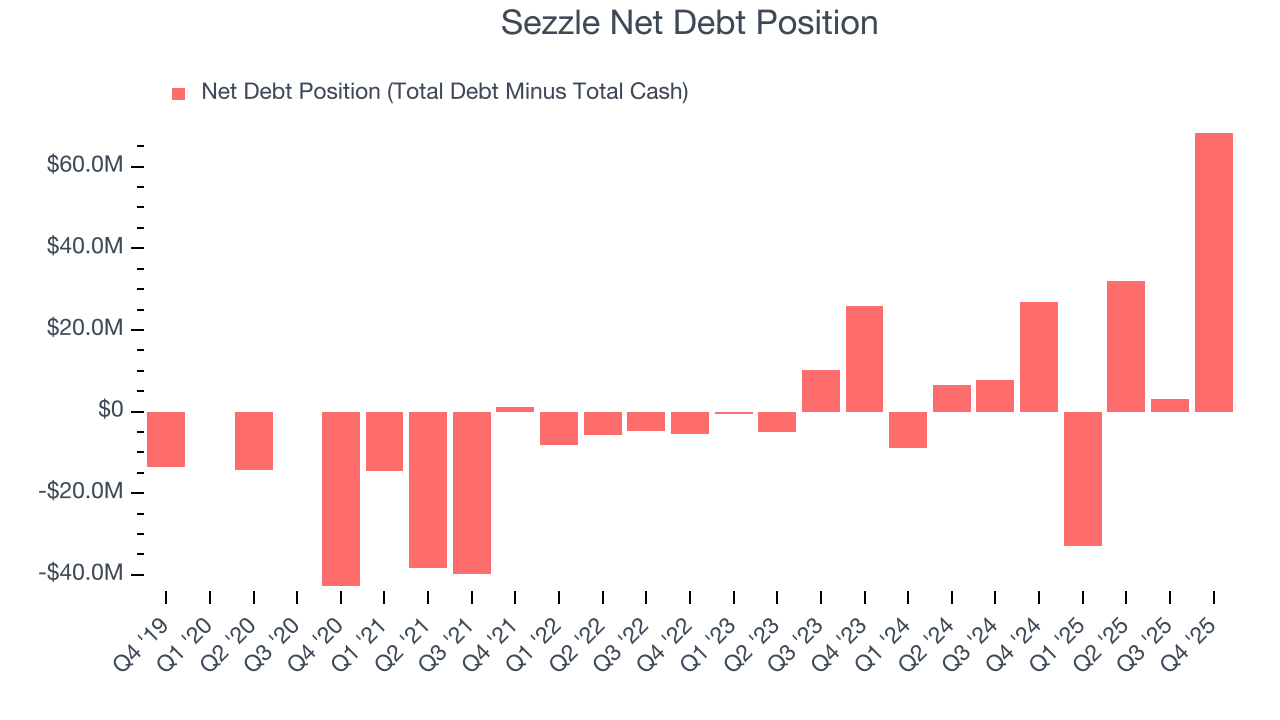

9. Balance Sheet Assessment

Sezzle reported $72.47 million of cash and $140.8 million of debt on its balance sheet in the most recent quarter.

As investors in high-quality companies, we primarily focus on whether a company’s profits can support its debt.

With $187.3 million of EBITDA over the last 12 months, we view Sezzle’s 0.4× net-debt-to-EBITDA ratio as safe. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

10. Key Takeaways from Sezzle’s Q4 Results

It was good to see Sezzle beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this quarter featured some important positives. The stock remained flat at $65.00 immediately after reporting.

11. Is Now The Time To Buy Sezzle?

Updated: March 14, 2026 at 12:38 AM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Sezzle.

First of all, the company’s revenue growth was exceptional over the last five years. And while its relatively low ROE suggests management has struggled to find compelling investment opportunities, its astounding EPS growth over the last three years shows its profits are trickling down to shareholders. On top of that, Sezzle’s expanding pre-tax profit margin shows the business has become more efficient.

Sezzle’s P/E ratio based on the next 12 months is 13.9x. This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're pretty confident there are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $97 on the company (compared to the current share price of $66.23).