First Hawaiian Bank (FHB)

We wouldn’t buy First Hawaiian Bank. Its revenue growth has been weak and its profitability has caved, showing it’s struggling to adapt.― StockStory Analyst Team

1. News

2. Summary

Why We Think First Hawaiian Bank Will Underperform

Dating back to 1858 as Hawaii's oldest bank with deep roots in the Pacific island communities, First Hawaiian (NASDAQ:FHB) operates a full-service community bank providing deposit accounts, commercial and consumer loans, credit cards, and wealth management services across Hawaii, Guam, and Saipan.

- Net interest income trends were unexciting over the last five years as its 4.4% annual growth was below the typical banking firm

- 3% annual revenue growth over the last two years was slower than its banking peers

- Capital trends were unexciting over the last five years as its 1.5% annual tangible book value per share growth was below the typical banking firm

First Hawaiian Bank doesn’t fulfill our quality requirements. We’re looking for better stocks elsewhere.

Why There Are Better Opportunities Than First Hawaiian Bank

At $23.95 per share, First Hawaiian Bank trades at 1x forward P/B. This multiple is lower than most banking companies, but for good reason.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. First Hawaiian Bank (FHB) Research Report: Q4 CY2025 Update

Hawaiian banking company First Hawaiian (NASDAQ:FHB) met Wall Streets revenue expectations in Q4 CY2025, with sales up 5.4% year on year to $225.9 million. Its GAAP profit of $0.56 per share was 2% above analysts’ consensus estimates.

First Hawaiian Bank (FHB) Q4 CY2025 Highlights:

- Net Interest Income: $170.3 million vs analyst estimates of $171 million (7.3% year-on-year growth, in line)

- Net Interest Margin: 3.2% vs analyst estimates of 3.2% (3.5 basis point beat)

- Revenue: $225.9 million vs analyst estimates of $225 million (5.4% year-on-year growth, in line)

- Efficiency Ratio: 55.1% vs analyst estimates of 56.8% (166 basis point beat)

- EPS (GAAP): $0.56 vs analyst estimates of $0.55 (2% beat)

- Tangible Book Value per Share: $14.46 vs analyst estimates of $14.30 (13.6% year-on-year growth, 1.1% beat)

- Market Capitalization: $3.41 billion

Company Overview

Dating back to 1858 as Hawaii's oldest bank with deep roots in the Pacific island communities, First Hawaiian (NASDAQ:FHB) operates a full-service community bank providing deposit accounts, commercial and consumer loans, credit cards, and wealth management services across Hawaii, Guam, and Saipan.

First Hawaiian operates through three business segments: Retail Banking, Commercial Banking, and Treasury. The Retail Banking segment serves individuals and small businesses with products ranging from checking and savings accounts to residential mortgages, home equity lines, and auto loans. These services are delivered through a network of 50 banking locations throughout Hawaii, Guam, and Saipan.

The Commercial Banking segment caters to middle-market and large companies with corporate banking products, commercial real estate loans, and auto dealer financing. While primarily focused on Hawaii-based businesses, the bank also maintains lending activities on the U.S. mainland, particularly auto dealer flooring in California and participation in the Shared National Credits Program.

A typical commercial client might be a Hawaii-based real estate developer securing financing for an apartment complex project with a loan-to-value ratio under 75%, while a retail customer might use the bank's mobile app to manage their checking account, apply for a mortgage, or set up a trust for wealth transfer.

The bank generates revenue primarily through interest income on loans and investments, as well as fees from services like wealth management, credit cards, and merchant processing. First Hawaiian emphasizes relationship banking, aiming to serve customers across multiple financial needs rather than focusing on one-off transactions. The bank's deposit base, drawn from both individual and corporate customers, serves as its primary funding source for lending activities.

4. Regional Banks

Regional banks, financial institutions operating within specific geographic areas, serve as intermediaries between local depositors and borrowers. They benefit from rising interest rates that improve net interest margins (the difference between loan yields and deposit costs), digital transformation reducing operational expenses, and local economic growth driving loan demand. However, these banks face headwinds from fintech competition, deposit outflows to higher-yielding alternatives, credit deterioration (increasing loan defaults) during economic slowdowns, and regulatory compliance costs. Recent concerns about regional bank stability following high-profile failures and significant commercial real estate exposure present additional challenges.

First Hawaiian's competitors include other regional banks operating in its markets such as Bank of Hawaii (NYSE:BOH), Central Pacific Financial (NYSE:CPF), and larger national banks with presence in Hawaii like Bank of America (NYSE:BAC) and Wells Fargo (NYSE:WFC).

5. Sales Growth

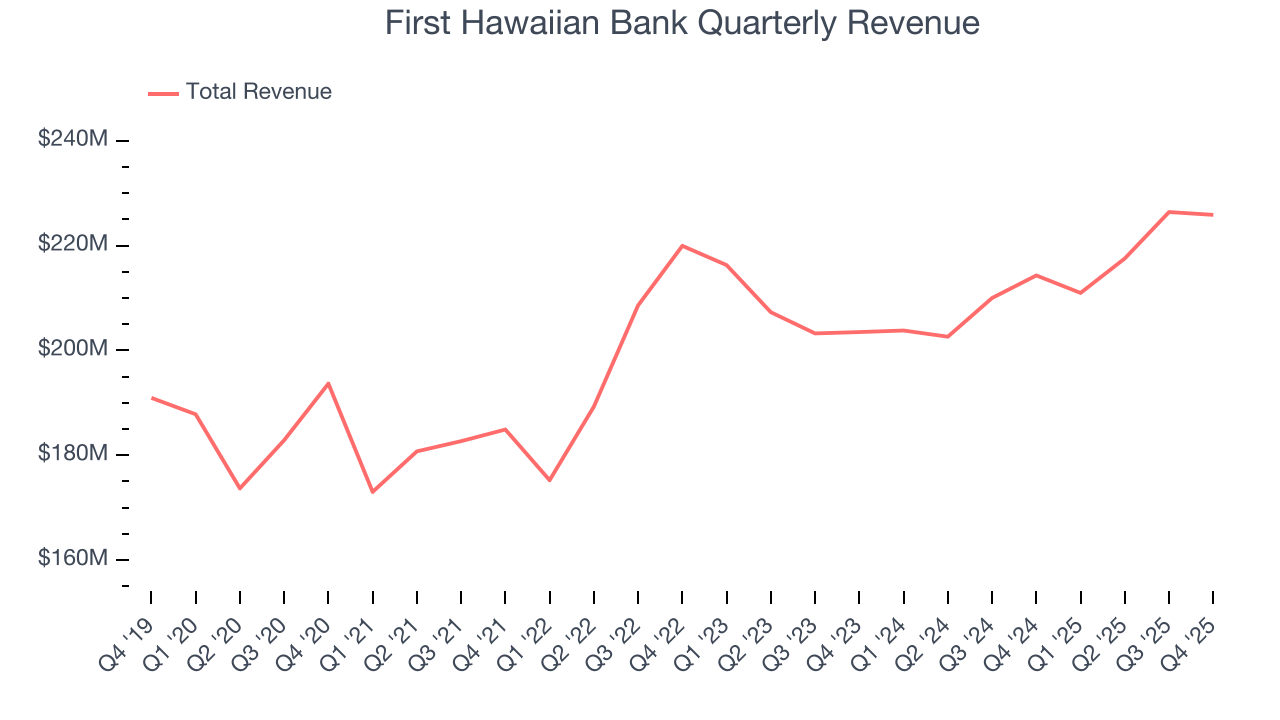

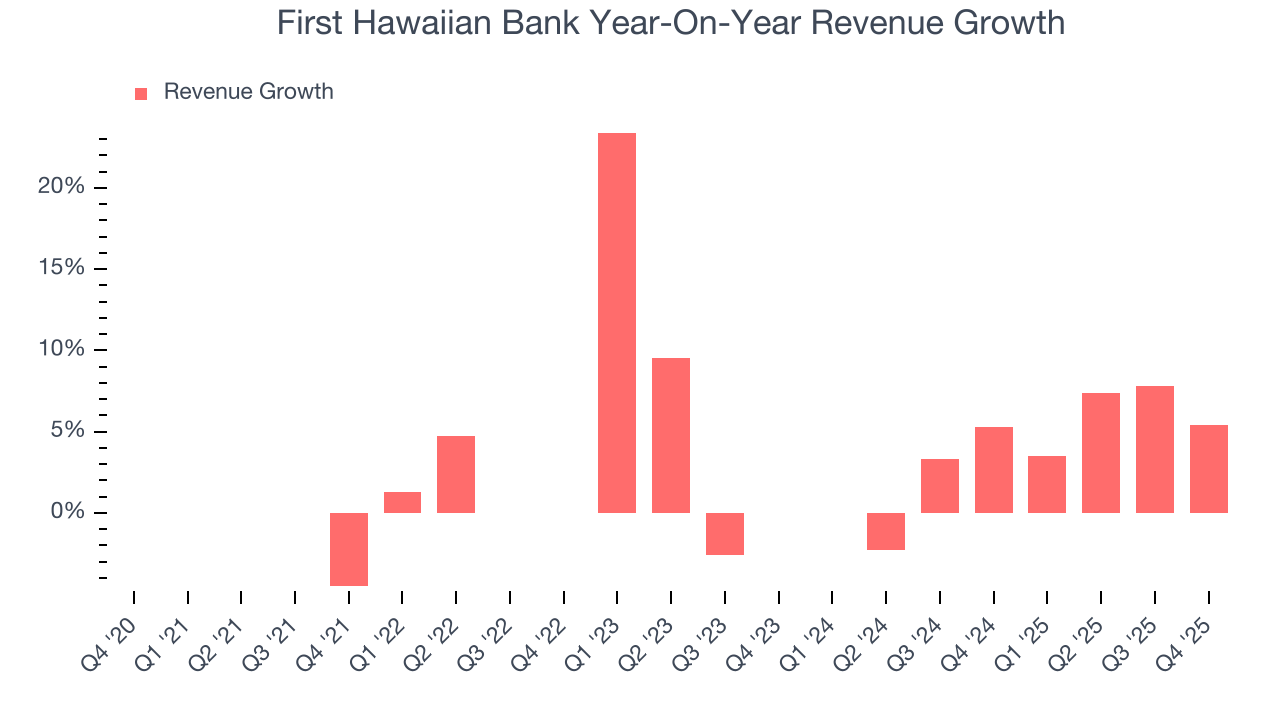

Two primary revenue streams drive bank earnings. While net interest income, which is earned by charging higher rates on loans than paid on deposits, forms the foundation, fee-based services across banking, credit, wealth management, and trading operations provide additional income. Regrettably, First Hawaiian Bank’s revenue grew at a sluggish 3.6% compounded annual growth rate over the last five years. This fell short of our benchmark for the banking sector and is a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. First Hawaiian Bank’s annualized revenue growth of 3% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, First Hawaiian Bank grew its revenue by 5.4% year on year, and its $225.9 million of revenue was in line with Wall Street’s estimates.

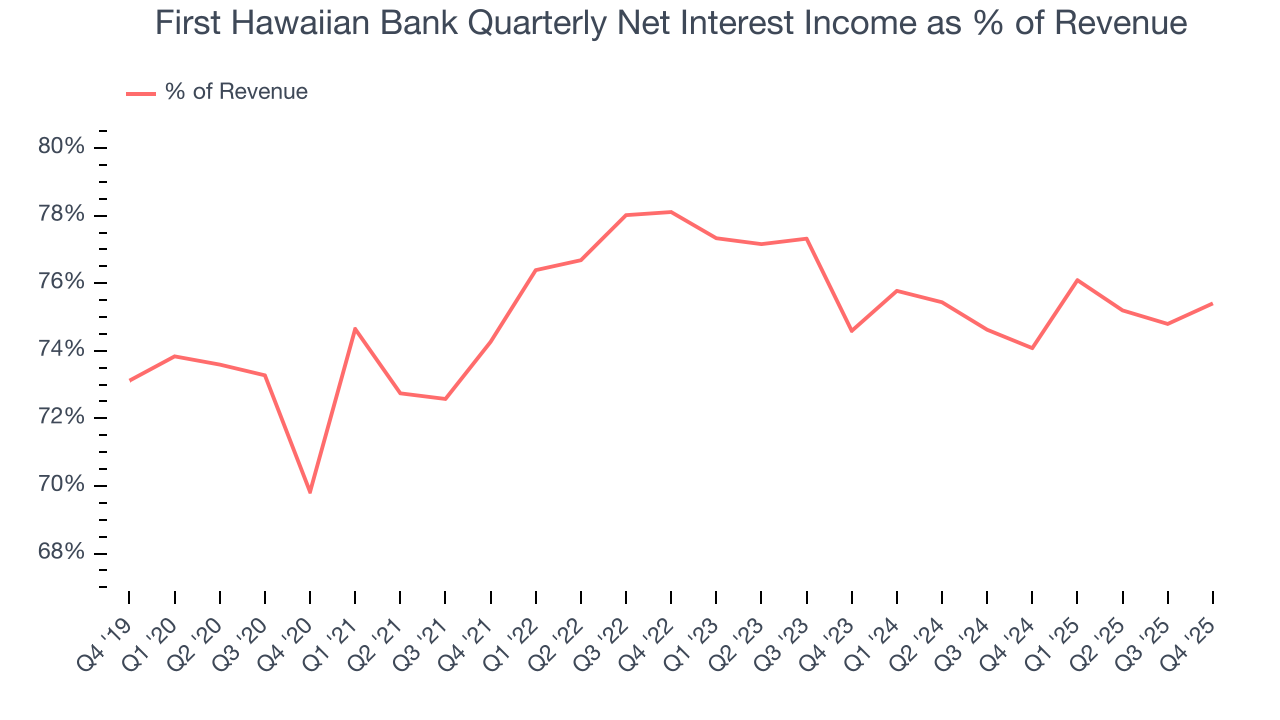

Net interest income made up 75.6% of the company’s total revenue during the last five years, meaning lending operations are First Hawaiian Bank’s largest source of revenue.

Markets consistently prioritize net interest income growth over fee-based revenue, recognizing its superior quality and recurring nature compared to the more unpredictable non-interest income streams.

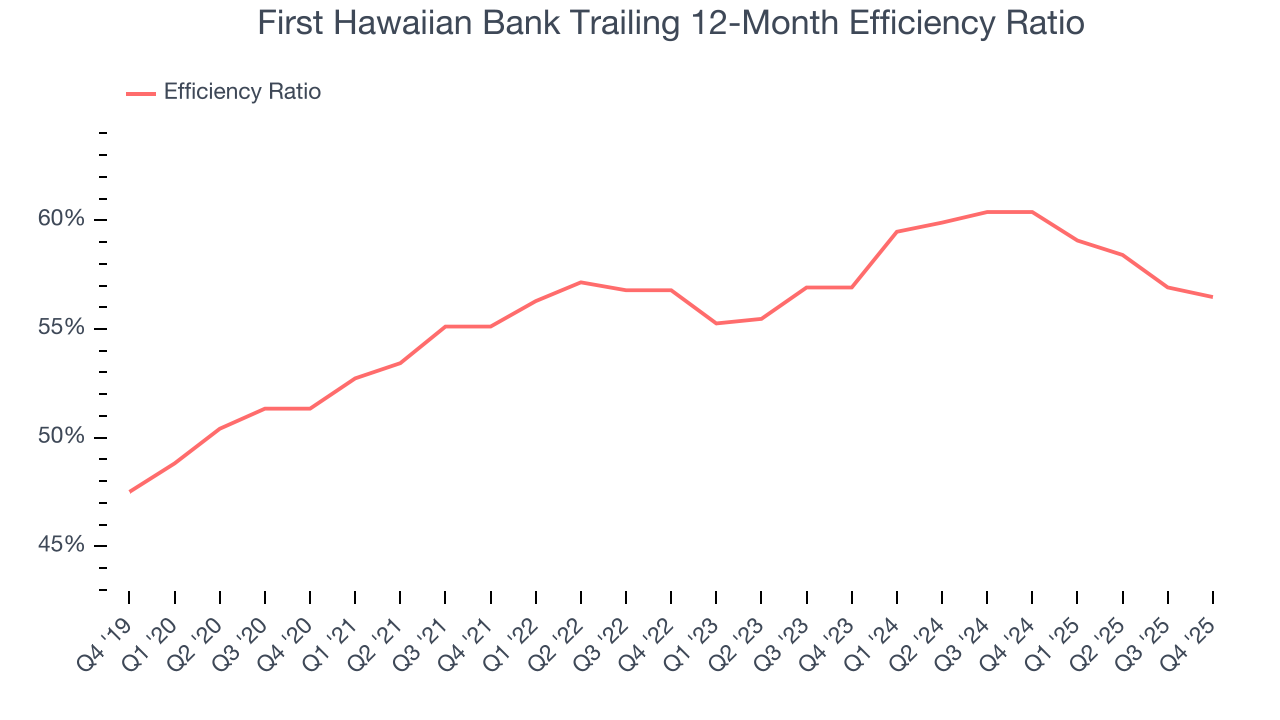

6. Efficiency Ratio

Topline growth alone doesn't tell the complete story - the profitability of that growth shapes actual earnings impact. Banks track this dynamic through efficiency ratios, which compare non-interest expenses such as personnel, rent, IT, and marketing costs to total revenue streams.

Markets emphasize efficiency ratio trends over static measurements, recognizing that revenue compositions drive different expense bases. Lower efficiency ratios signal superior performance by indicating that banks are controlling costs effectively relative to their income.

Over the last five years, First Hawaiian Bank’s efficiency ratio has increased by 5.1 percentage points, going from 55.1% to 56.5%. Said differently, the company’s expenses have increased at a faster rate than revenue, which usually raises questions unless the company is in high-growth mode and reinvesting its profits into attractive ventures.

First Hawaiian Bank’s efficiency ratio came in at 55.1% this quarter, beating analysts’ expectations by 166 basis points (100 basis points = 1 percentage point).

For the next 12 months, Wall Street expects First Hawaiian Bank to maintain its trailing one-year ratio with a projection of 57.3%.

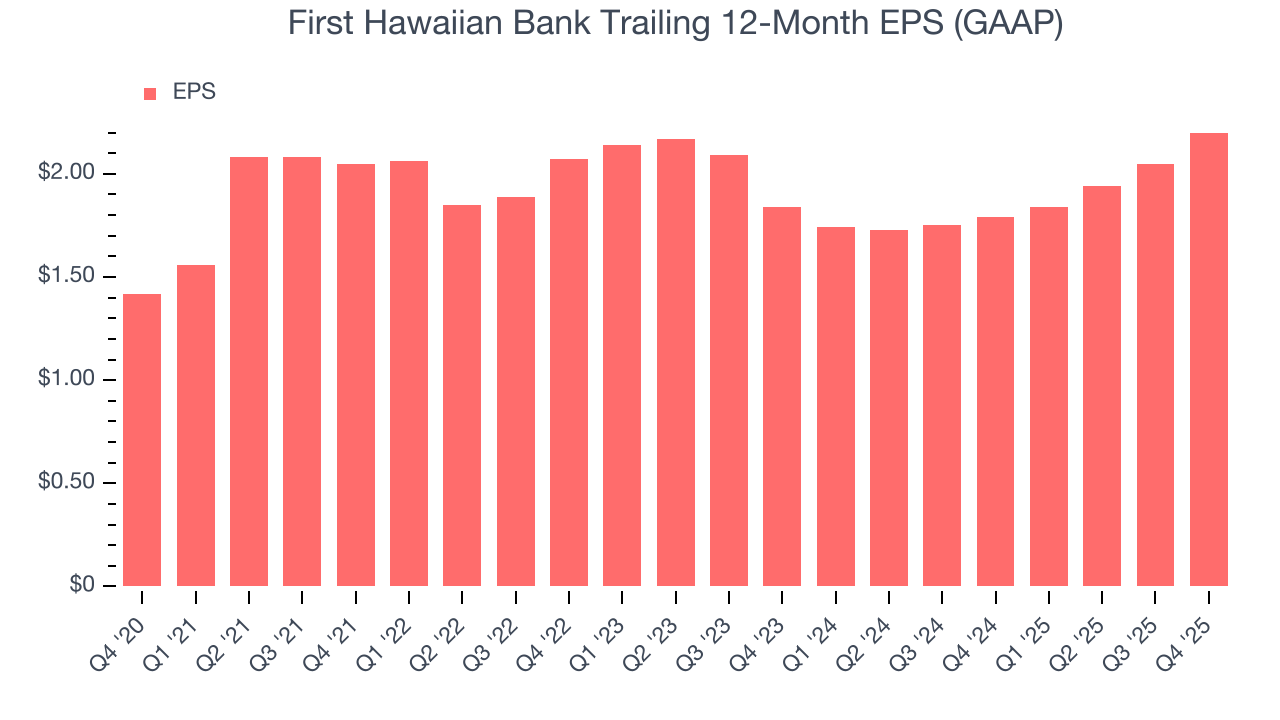

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

First Hawaiian Bank’s EPS grew at an unimpressive 9.2% compounded annual growth rate over the last five years. On the bright side, this performance was better than its 3.6% annualized revenue growth and tells us the company became more profitable on a per-share basis as it expanded.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For First Hawaiian Bank, its two-year annual EPS growth of 9.3% is similar to its five-year trend, implying stable earnings.

In Q4, First Hawaiian Bank reported EPS of $0.56, up from $0.41 in the same quarter last year. This print beat analysts’ estimates by 2%. Over the next 12 months, Wall Street expects First Hawaiian Bank’s full-year EPS of $2.20 to grow 2.2%.

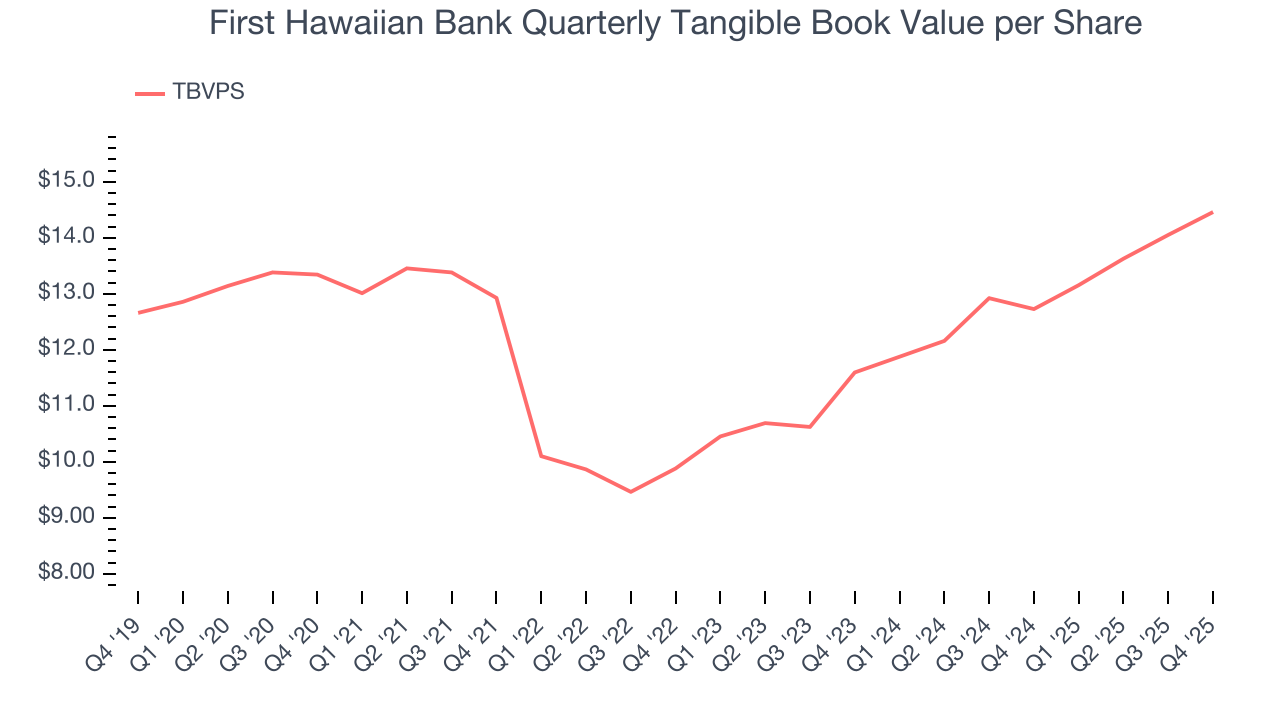

8. Tangible Book Value Per Share (TBVPS)

The balance sheet drives banking profitability since earnings flow from the spread between borrowing and lending rates. As such, valuations for these companies concentrate on capital strength and sustainable equity accumulation potential.

This explains why tangible book value per share (TBVPS) stands as the premier banking metric. TBVPS strips away questionable intangible assets, revealing concrete per-share net worth that investors can trust. On the other hand, EPS is often distorted by mergers and flexible loan loss accounting. TBVPS provides clearer performance insights.

First Hawaiian Bank’s TBVPS grew at a sluggish 1.6% annual clip over the last five years. However, TBVPS growth has accelerated recently, growing by 11.7% annually over the last two years from $11.60 to $14.46 per share.

Over the next 12 months, Consensus estimates call for First Hawaiian Bank’s TBVPS to grow by 8.5% to $15.69, paltry growth rate.

9. Balance Sheet Assessment

Leverage is core to a financial firm’s business model (loans funded by deposits). To ensure economic stability and avoid a repeat of the 2008 GFC, regulators require certain levels of capital and liquidity, focusing on the Tier 1 capital ratio.

Tier 1 capital is the highest-quality capital that a firm holds, consisting primarily of common stock and retained earnings, but also physical gold. It serves as the primary cushion against losses and is the first line of defense in times of financial distress.

This capital is divided by risk-weighted assets to derive the Tier 1 capital ratio. Risk-weighted means that cash and US treasury securities are assigned little risk while unsecured consumer loans and equity investments get much higher risk weights, for example.

New regulation after the 2008 financial crisis requires that all firms must maintain a Tier 1 capital ratio greater than 4.5%. On top of this, there are additional buffers based on scale, risk profile, and other regulatory classifications, so that at the end of the day, firms generally must maintain a 7-10% ratio at minimum.

Over the last two years, First Hawaiian Bank has averaged a Tier 1 capital ratio of 12.9%, which is considered safe and well capitalized in the event that macro or market conditions suddenly deteriorate.

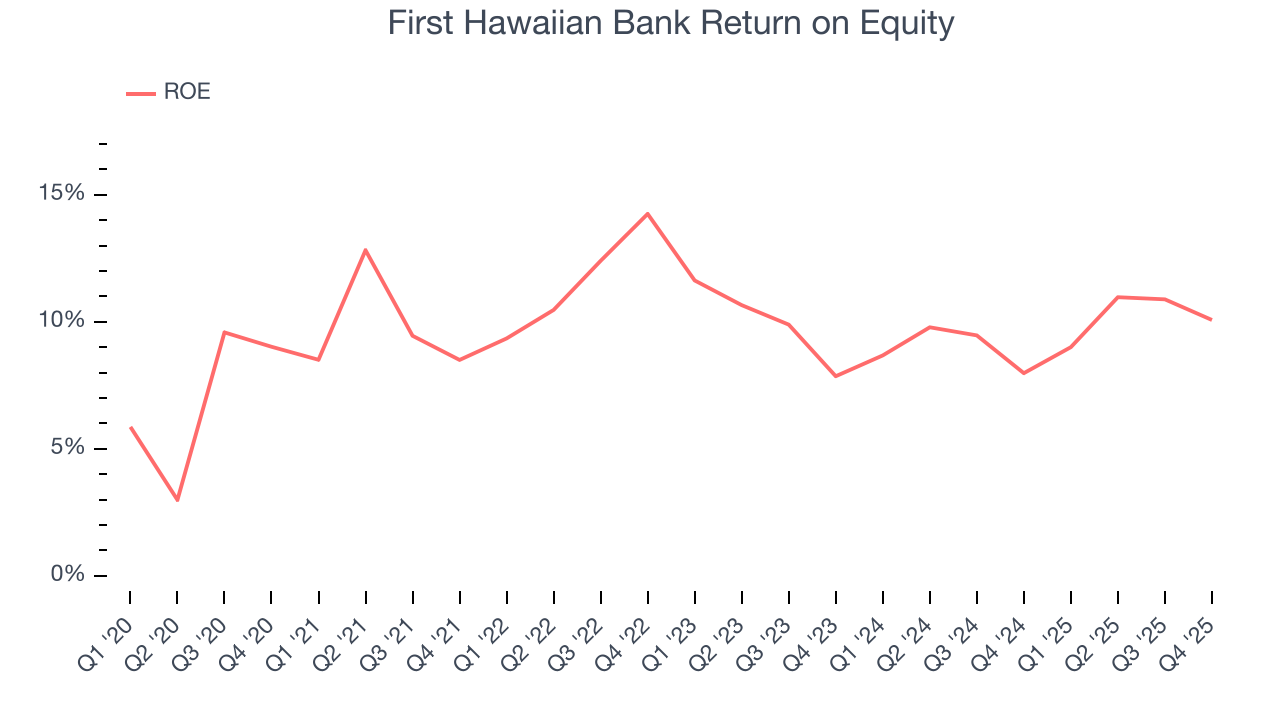

10. Return on Equity

Return on equity, or ROE, quantifies bank profitability relative to shareholder equity - an essential capital source for these institutions. Over extended periods, superior ROE performance drives faster shareholder wealth compounding through reinvestment, share repurchases, and dividend growth.

Over the last five years, First Hawaiian Bank has averaged an ROE of 10.1%, respectable for a company operating in a sector where the average shakes out around 7.5% and those putting up 15%+ are greatly admired.

11. Key Takeaways from First Hawaiian Bank’s Q4 Results

It was good to see First Hawaiian Bank narrowly top analysts’ EPS and tangible book value per share expectations this quarter. On the other hand, its net interest income was just in line with Wall Street’s estimates. Overall, this was still a decentquarter. The stock remained flat at $27.57 immediately following the results.

12. Is Now The Time To Buy First Hawaiian Bank?

Updated: March 15, 2026 at 12:54 AM EDT

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

We see the value of companies driving economic growth, but in the case of First Hawaiian Bank, we’re out. To begin with, its revenue growth was weak over the last five years, and analysts expect its demand to deteriorate over the next 12 months. While its expanding net interest margin shows its loan book is becoming more profitable, the downside is its net interest income growth was weak over the last five years. On top of that, its TBVPS growth was weak over the last five years.

First Hawaiian Bank’s P/B ratio based on the next 12 months is 1x. This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think other companies feature superior fundamentals at the moment.

Wall Street analysts have a consensus one-year price target of $27.72 on the company (compared to the current share price of $23.95).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.