Freshpet (FRPT)

Freshpet doesn’t excite us. Its low returns on capital raise concerns about its ability to deliver profits, a must for quality companies.― StockStory Analyst Team

1. News

2. Summary

Why We Think Freshpet Will Underperform

Standing out from typical processed pet foods, Freshpet (NASDAQ:FRPT) is a pet food company whose product portfolio includes natural meals and treats for dogs and cats.

- ROIC of 0.1% reflects management’s challenges in identifying attractive investment opportunities

- Subscale operations are evident in its revenue base of $1.10 billion, meaning it has fewer distribution channels than its larger rivals

- The good news is that its performance over the past three years shows its incremental sales were extremely profitable, as its annual earnings per share growth of 79.4% outpaced its revenue gains

Freshpet doesn’t fulfill our quality requirements. We’re redirecting our focus to better businesses.

Why There Are Better Opportunities Than Freshpet

At $75.39 per share, Freshpet trades at 56.5x forward P/E. The current multiple is quite expensive, especially for the fundamentals of the business.

We prefer to invest in similarly-priced but higher-quality companies with superior earnings growth.

3. Freshpet (FRPT) Research Report: Q4 CY2025 Update

Pet food company Freshpet (NASDAQ:FRPT) met Wall Street’s revenue expectations in Q4 CY2025, with sales up 8.6% year on year to $285.2 million. Its GAAP profit of $0.64 per share was 64.7% above analysts’ consensus estimates.

Freshpet (FRPT) Q4 CY2025 Highlights:

- Revenue: $285.2 million vs analyst estimates of $285.8 million (8.6% year-on-year growth, in line)

- EPS (GAAP): $0.64 vs analyst estimates of $0.39 (64.7% beat)

- Adjusted EBITDA: $61.15 million vs analyst estimates of $57.89 million (21.4% margin, 5.6% beat)

- EBITDA guidance for the upcoming financial year 2026 is $210 million at the midpoint, below analyst estimates of $226.3 million

- Operating Margin: 15.6%, up from 7.4% in the same quarter last year

- Free Cash Flow was $2.06 million, up from -$7.90 million in the same quarter last year

- Organic Revenue rose 8.6% year on year (miss)

- Sales Volumes rose 9.7% year on year (20.7% in the same quarter last year)

- Market Capitalization: $3.64 billion

Company Overview

Standing out from typical processed pet foods, Freshpet (NASDAQ:FRPT) is a pet food company whose product portfolio includes natural meals and treats for dogs and cats.

The company was founded in 2006 with the vision of better food for pets, who were becoming more and more important parts of a family. Since its founding, Freshpet has expanded its portfolio organically rather than through the mergers and acquisitions that are common in the packaged foods industry.

At the core of Freshpet's offering is a commitment to fresh, all-natural pet food. The food is typically sold refrigerated, emphasizing its freshness and real ingredients. Notable brands under the Freshpet umbrella include Freshpet Select, Vital, and Nature's Fresh. These brands offer various recipes, including grain-free options, high-protein meals, and foods tailored for specific life stages or health needs.

Freshpet's core customer is the health-conscious pet owner who views their pet as a family member and wants to provide the best nutrition possible. This target audience is willing to pay a premium for high-quality, natural ingredients, and values transparency in sourcing and production. Freshpet products can be found in the refrigerated sections of grocery stores, pet stores, and mass market retailers. While fresh food is a differentiator, it makes Freshpet’s products a bit more challenging to ship than traditional, shelf-stable pet food.

4. Perishable Food

The perishable food industry is diverse, encompassing large-scale producers and distributors to specialty and artisanal brands. These companies sell produce, dairy products, meats, and baked goods and have become integral to serving modern American consumers who prioritize freshness, quality, and nutritional value. Investing in perishable food stocks presents both opportunities and challenges. While the perishable nature of products can introduce risks related to supply chain management and shelf life, it also creates a constant demand driven by the necessity for fresh food. Companies that can efficiently manage inventory, distribution, and quality control are well-positioned to thrive in this competitive market. Navigating the perishable food industry requires adherence to strict food safety standards, regulations, and labeling requirements.

Competitors in the better-for-you pet food space include Blue Buffalo (owned by General Mills, NYSE:GIS) and Hill's Pet Nutrition (owned by Colgate-Palmolive, NYSE:CL). Private competitors include The Farmer's Dog and Ollie.

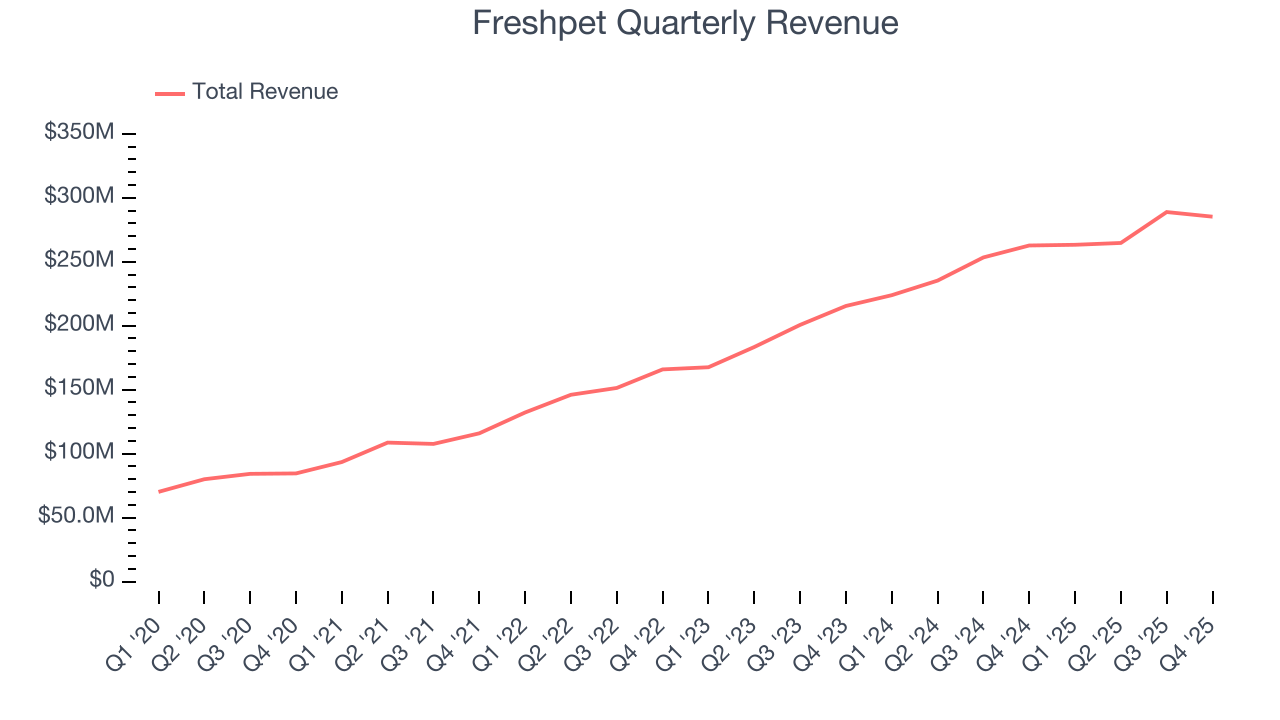

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $1.10 billion in revenue over the past 12 months, Freshpet is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers. On the bright side, it can grow faster because it has a longer list of untapped store chains to sell into.

As you can see below, Freshpet grew its sales at an excellent 22.8% compounded annual growth rate over the last three years as consumers bought more of its products.

This quarter, Freshpet grew its revenue by 8.6% year on year, and its $285.2 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 9.1% over the next 12 months, a deceleration versus the last three years. Still, this projection is noteworthy and indicates the market is baking in success for its products.

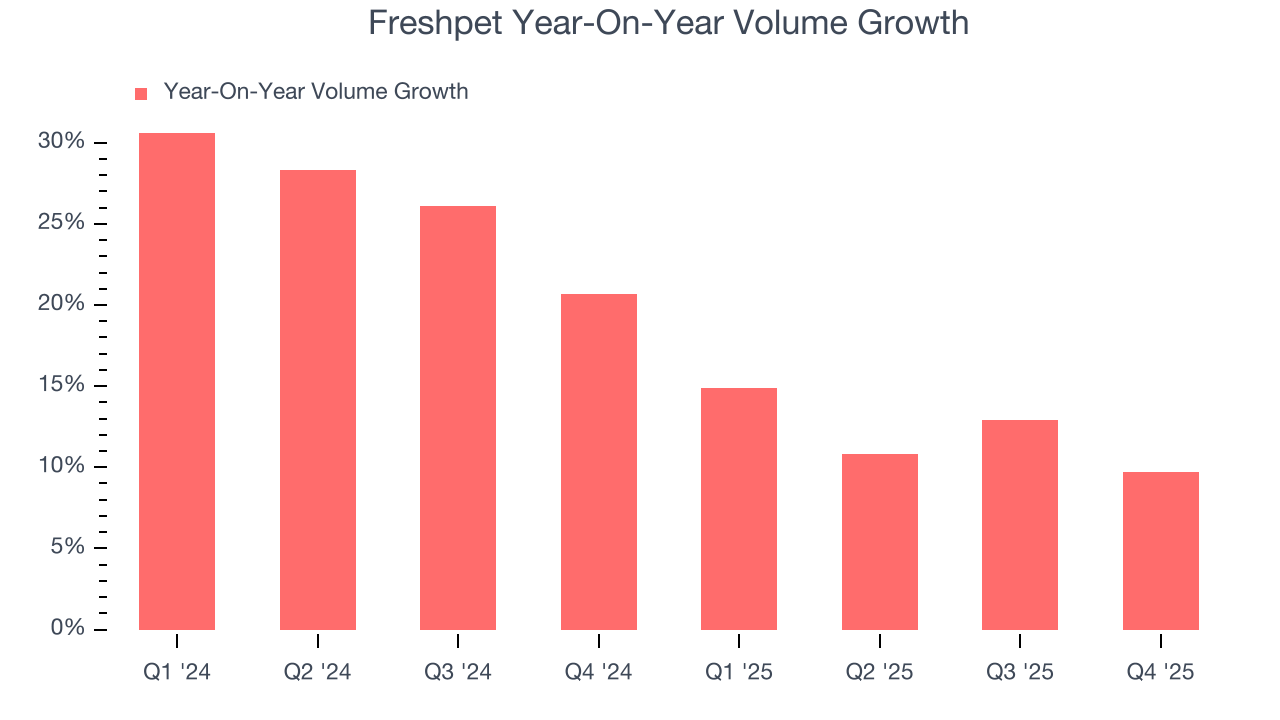

6. Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

Freshpet’s average quarterly volume growth of 19.3% over the last two years has beaten the competition by a long shot. This is great because companies with significant volume growth are needles in a haystack in the stable consumer staples sector.

In Freshpet’s Q4 2025, sales volumes jumped 9.7% year on year. This result shows the business is staying on track, but the deceleration suggests growth is getting harder to come by.

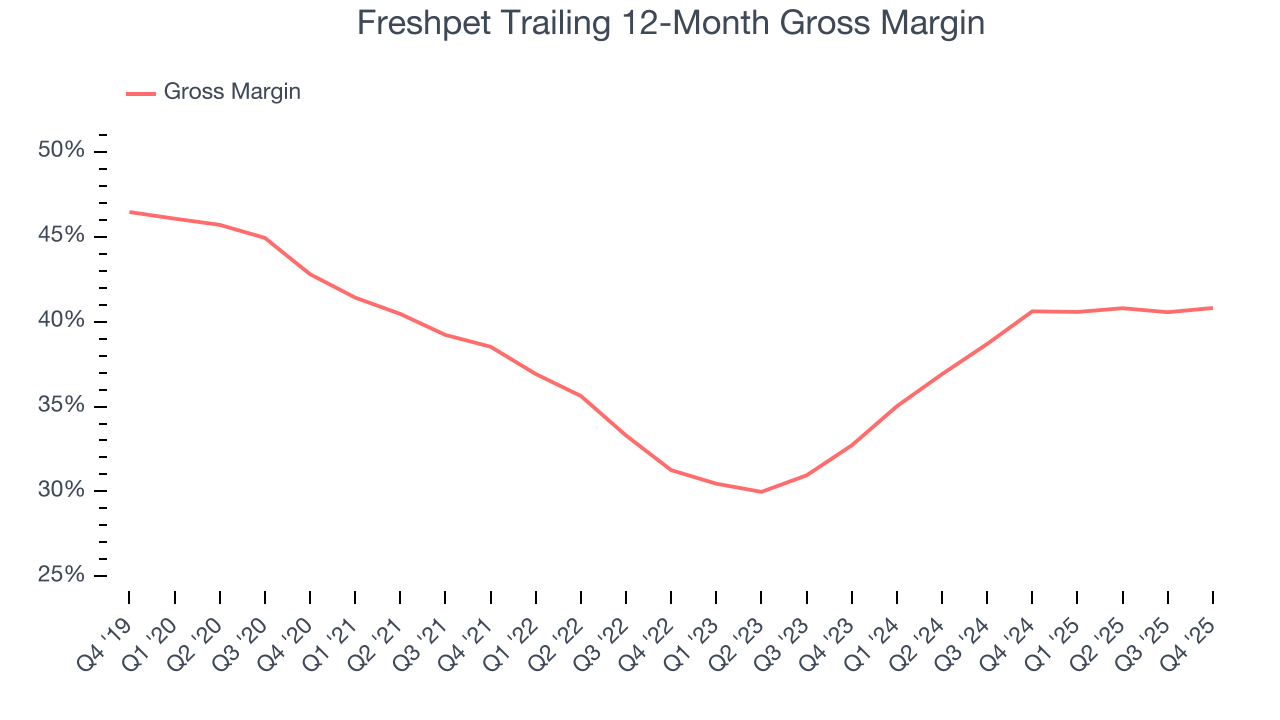

7. Gross Margin & Pricing Power

All else equal, we prefer higher gross margins because they usually indicate that a company sells more differentiated products, has a stronger brand, and commands pricing power.

Freshpet has good unit economics for a consumer staples company, giving it the opportunity to invest in areas such as marketing and talent to stay competitive. As you can see below, it averaged an impressive 40.7% gross margin over the last two years. Said differently, Freshpet paid its suppliers $59.29 for every $100 in revenue.

This quarter, Freshpet’s gross profit margin was 43.3%, in line with the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

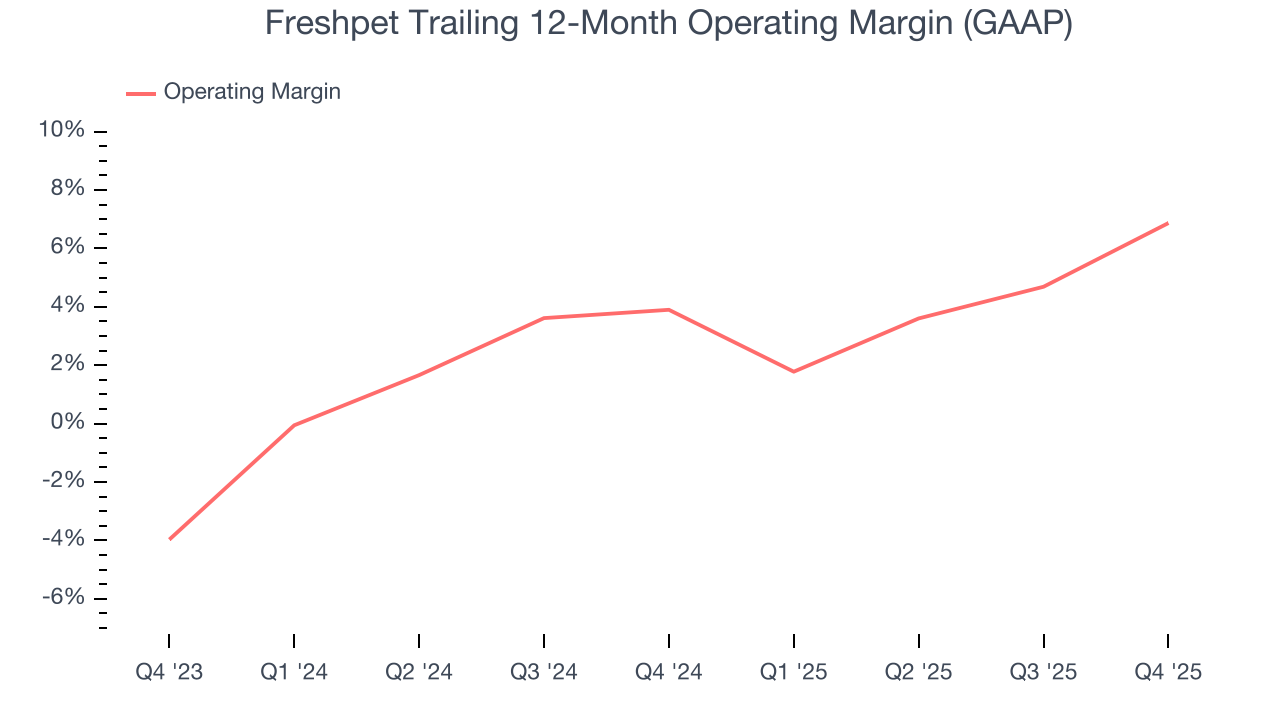

8. Operating Margin

Freshpet was profitable over the last two years but held back by its large cost base. Its average operating margin of 5.5% was weak for a consumer staples business. This result is surprising given its high gross margin as a starting point.

On the plus side, Freshpet’s operating margin rose by 3 percentage points over the last year, as its sales growth gave it operating leverage.

This quarter, Freshpet generated an operating margin profit margin of 15.6%, up 8.2 percentage points year on year. The increase was solid, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, and administrative overhead.

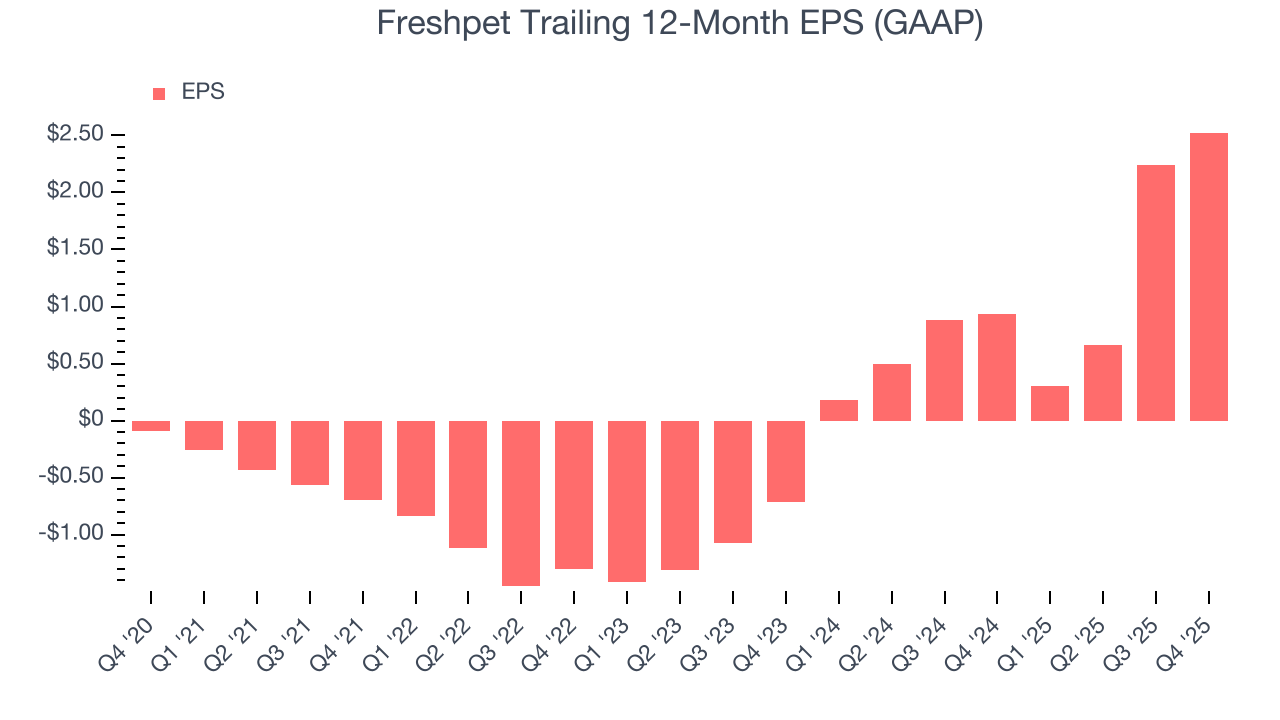

9. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Freshpet’s full-year EPS flipped from negative to positive over the last three years. This is encouraging and shows it’s at a critical moment in its life.

In Q4, Freshpet reported EPS of $0.64, up from $0.36 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Freshpet’s full-year EPS of $2.52 to shrink by 46.6%.

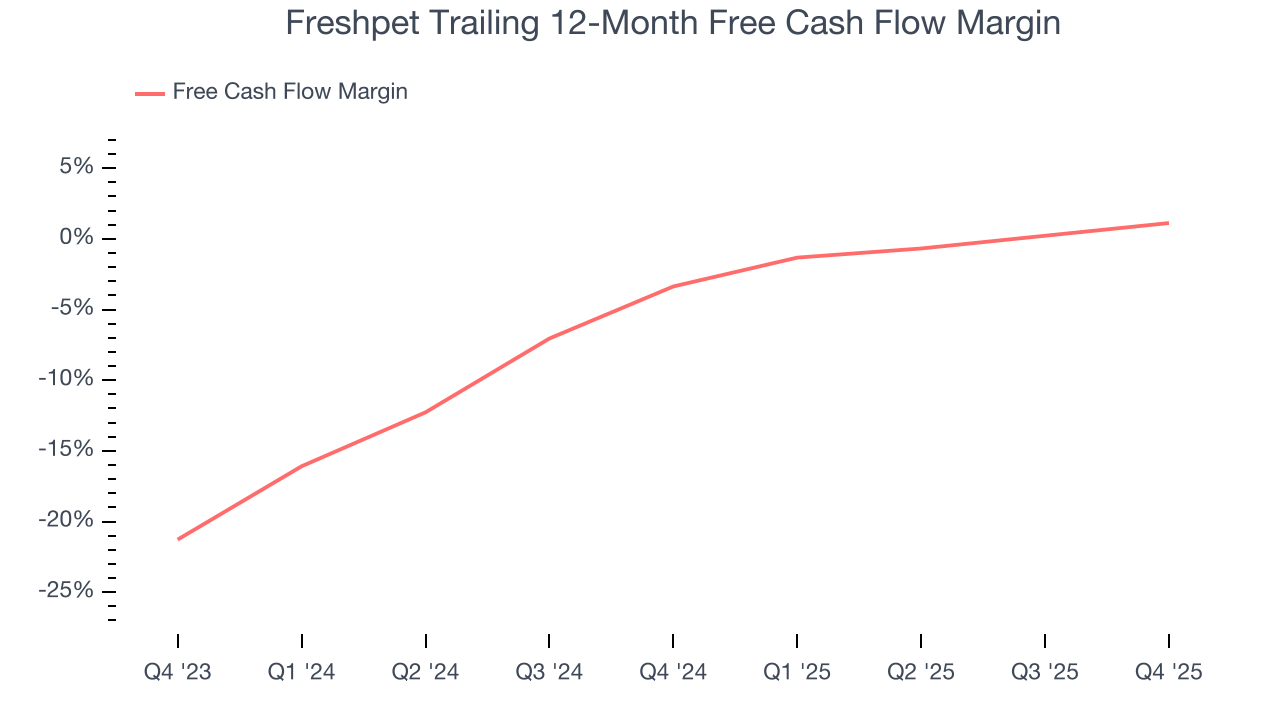

10. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Freshpet broke even from a free cash flow perspective over the last two years, giving the company limited opportunities to return capital to shareholders.

Taking a step back, an encouraging sign is that Freshpet’s margin expanded by 4.5 percentage points over the last year. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

Freshpet broke even from a free cash flow perspective in Q4. This result was good as its margin was 3.7 percentage points higher than in the same quarter last year, building on its favorable historical trend.

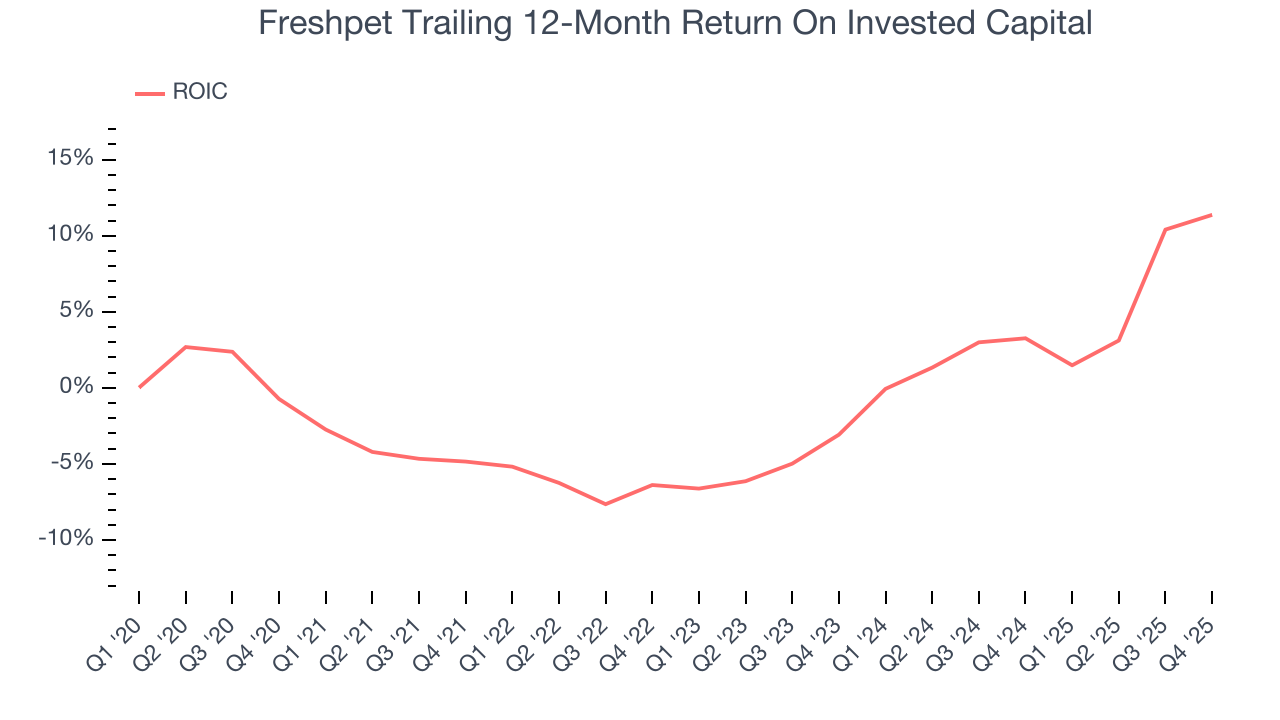

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Freshpet historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 0.1%, lower than the typical cost of capital (how much it costs to raise money) for consumer staples companies.

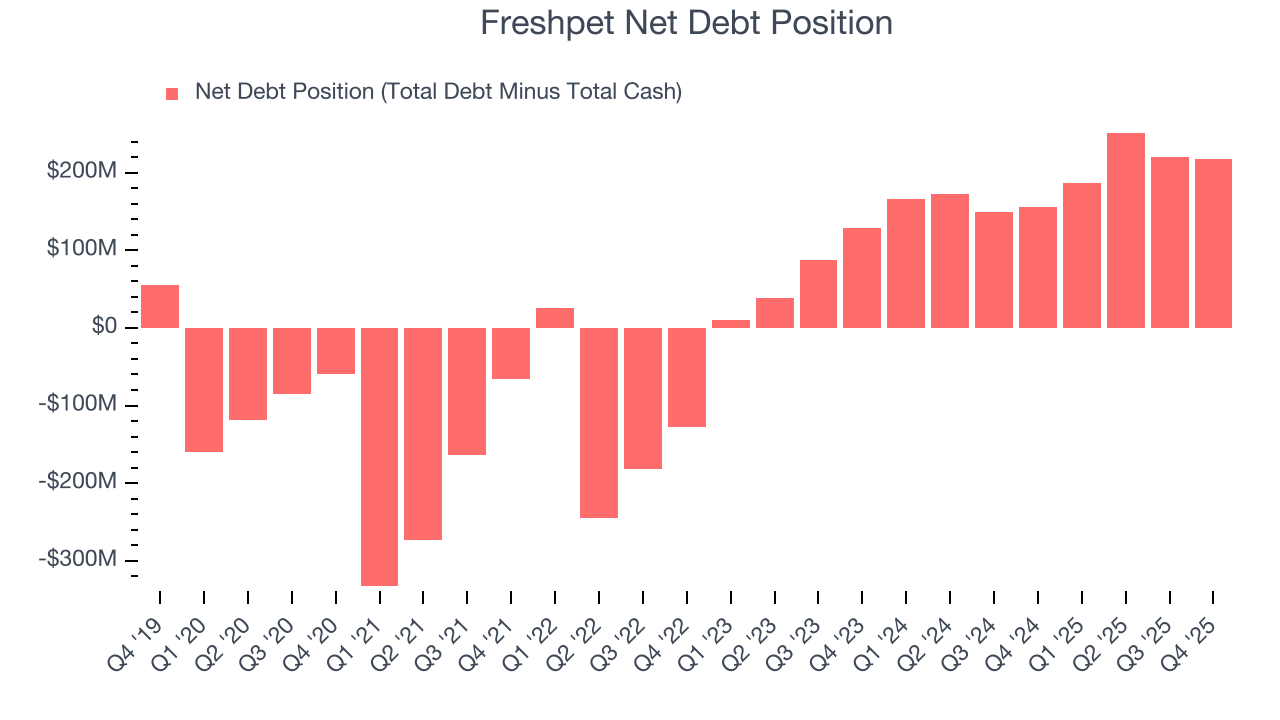

12. Balance Sheet Assessment

Freshpet reported $278 million of cash and $495 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $195.7 million of EBITDA over the last 12 months, we view Freshpet’s 1.1× net-debt-to-EBITDA ratio as safe. We also see its $2.73 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from Freshpet’s Q4 Results

It was good to see Freshpet beat analysts’ EPS expectations this quarter. We were also glad its EBITDA outperformed Wall Street’s estimates. On the other hand, its gross margin missed and its full-year EBITDA guidance fell short of Wall Street’s estimates. Zooming out, we think this was a mixed quarter. Investors were likely hoping for more, and shares traded down 2.8% to $72.46 immediately after reporting.

14. Is Now The Time To Buy Freshpet?

Updated: March 16, 2026 at 10:41 PM EDT

Before investing in or passing on Freshpet, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

Freshpet’s business quality ultimately falls short of our standards. Although its revenue growth was impressive over the last three years, it’s expected to deteriorate over the next 12 months and its projected EPS for the next year is lacking. And while the company’s volume growth has been in a league of its own, the downside is its relatively low ROIC suggests management has struggled to find compelling investment opportunities.

Freshpet’s P/E ratio based on the next 12 months is 56.5x. This valuation tells us a lot of optimism is priced in - you can find more timely opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $87.60 on the company (compared to the current share price of $75.39).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.