Dole (DOLE)

We wouldn’t buy Dole. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Dole Will Underperform

Known for its delicious pineapples and Hawaiian roots, Dole (NYSE:DOLE) is a global agricultural company specializing in fresh fruits and vegetables.

- Easily substituted products (and therefore stiff competition) result in an inferior gross margin of 8.1% that must be offset through higher volumes

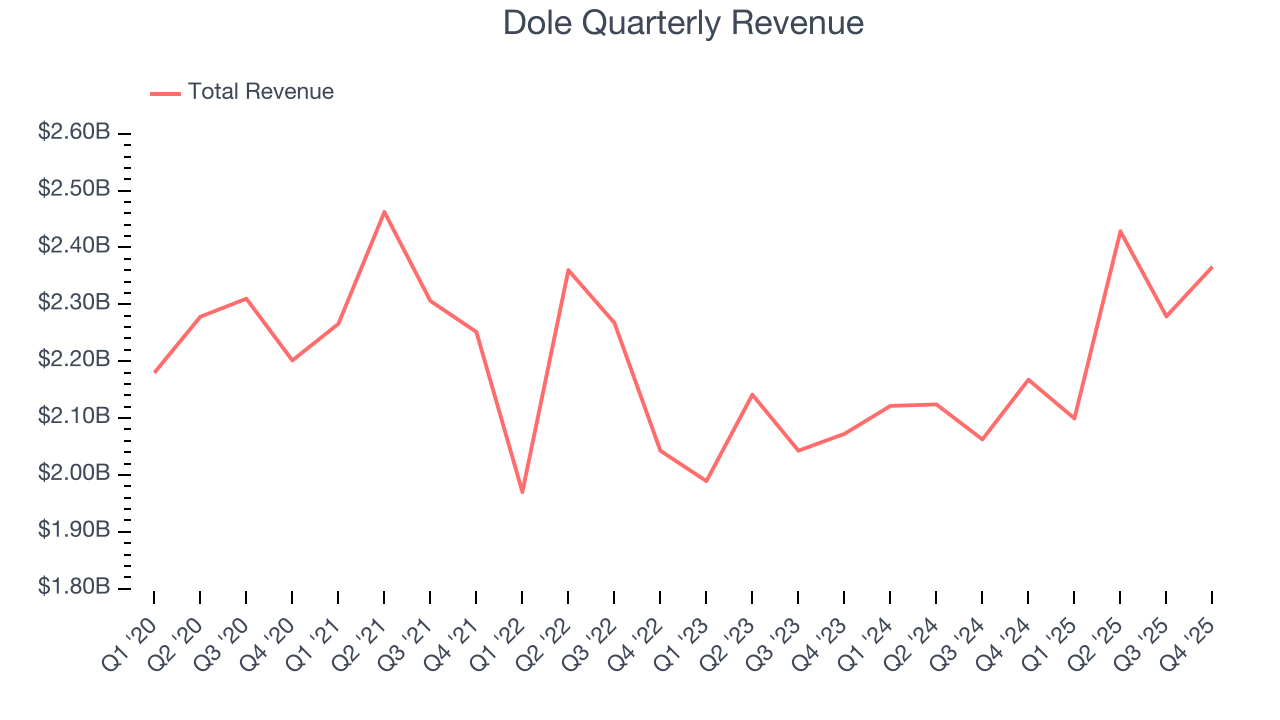

- Sales trends were unexciting over the last three years as its 2% annual growth was below the typical consumer staples company

- Subpar operating margin constrains its ability to invest in process improvements or effectively respond to new competitive threats

Dole’s quality is inadequate. There are more rewarding stocks elsewhere.

Why There Are Better Opportunities Than Dole

Dole is trading at $14.36 per share, or 10.6x forward P/E. Yes, this valuation multiple is lower than that of other consumer staples peers, but we’ll remind you that you often get what you pay for.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Dole (DOLE) Research Report: Q4 CY2025 Update

Fresh produce company Dole (NYSE:DOLE) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 9.2% year on year to $2.37 billion. Its non-GAAP profit of $0.14 per share was in line with analysts’ consensus estimates.

Dole (DOLE) Q4 CY2025 Highlights:

- Revenue: $2.37 billion vs analyst estimates of $2.31 billion (9.2% year-on-year growth, 2.3% beat)

- Adjusted EPS: $0.14 vs analyst estimates of $0.15 (in line)

- Adjusted EBITDA: $72.67 million vs analyst estimates of $68.7 million (3.1% margin, 5.8% beat)

- EBITDA guidance for the upcoming financial year 2026 is $400 million at the midpoint, below analyst estimates of $408.3 million

- Operating Margin: 1.2%, in line with the same quarter last year

- Free Cash Flow Margin: 2.9%, down from 6% in the same quarter last year

- Market Capitalization: $1.52 billion

Company Overview

Known for its delicious pineapples and Hawaiian roots, Dole (NYSE:DOLE) is a global agricultural company specializing in fresh fruits and vegetables.

The company was founded in 1901 as the Hawaiian Pineapple Company by James Dole, the “Pineapple King”. Dole’s enterprise was acquired by Castle & Cooke in 1961, who diversified it into other areas of the food industry, and it was once again bought in 1985 by entrepreneur and businessman David Murdock, whose involvement marked a turning point in the company's history.

Murdock recognized Dole’s potential for global growth and aggressively expanded its operations, transforming it into a multi-national corporation. Today, Dole is one of the world's largest producers and distributors of fresh fruits and vegetables, and its portfolio includes not only pineapples but also bananas, strawberries, salads, and more.

To maintain its complex operations, Dole leverages its well-established network of farms, packing facilities, and distribution centers spanning multiple continents, including North America, Latin America, Europe, Asia, and Africa. This extensive supply chain allows Dole to source fresh produce from different regions, ensuring a year-round supply of fruits and vegetables. Few competitors can match Dole's global presence and logistical capabilities.

The company partners with grocery stores, supermarkets, and convenience stores to sell its products. It also supplies restaurants, hotels, and catering companies with fresh produce.

4. Perishable Food

The perishable food industry is diverse, encompassing large-scale producers and distributors to specialty and artisanal brands. These companies sell produce, dairy products, meats, and baked goods and have become integral to serving modern American consumers who prioritize freshness, quality, and nutritional value. Investing in perishable food stocks presents both opportunities and challenges. While the perishable nature of products can introduce risks related to supply chain management and shelf life, it also creates a constant demand driven by the necessity for fresh food. Companies that can efficiently manage inventory, distribution, and quality control are well-positioned to thrive in this competitive market. Navigating the perishable food industry requires adherence to strict food safety standards, regulations, and labeling requirements.

Competitors in the fresh produce category include Calavo Growers (NASDAQ:CVGW), Fresh Del Monte (NYSE:FDP), and Mission Produce (NASDAQ:AVO) along with private companies Chiquita Brands International and Sunkist Growers.

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $9.17 billion in revenue over the past 12 months, Dole is one of the larger consumer staples companies and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because there are only a finite number of major retail partners, placing a ceiling on its growth. For Dole to boost its sales, it likely needs to adjust its prices, launch new offerings, or lean into foreign markets.

As you can see below, Dole’s 2% annualized revenue growth over the last three years was sluggish. This shows it failed to generate demand in any major way and is a rough starting point for our analysis.

This quarter, Dole reported year-on-year revenue growth of 9.2%, and its $2.37 billion of revenue exceeded Wall Street’s estimates by 2.3%.

Looking ahead, sell-side analysts expect revenue to grow 1.3% over the next 12 months, similar to its three-year rate. This projection is underwhelming and suggests its newer products will not catalyze better top-line performance yet.

6. Gross Margin & Pricing Power

At StockStory, we prefer high gross margin businesses because they indicate pricing power or differentiated products, giving the company a chance to generate higher operating profits.

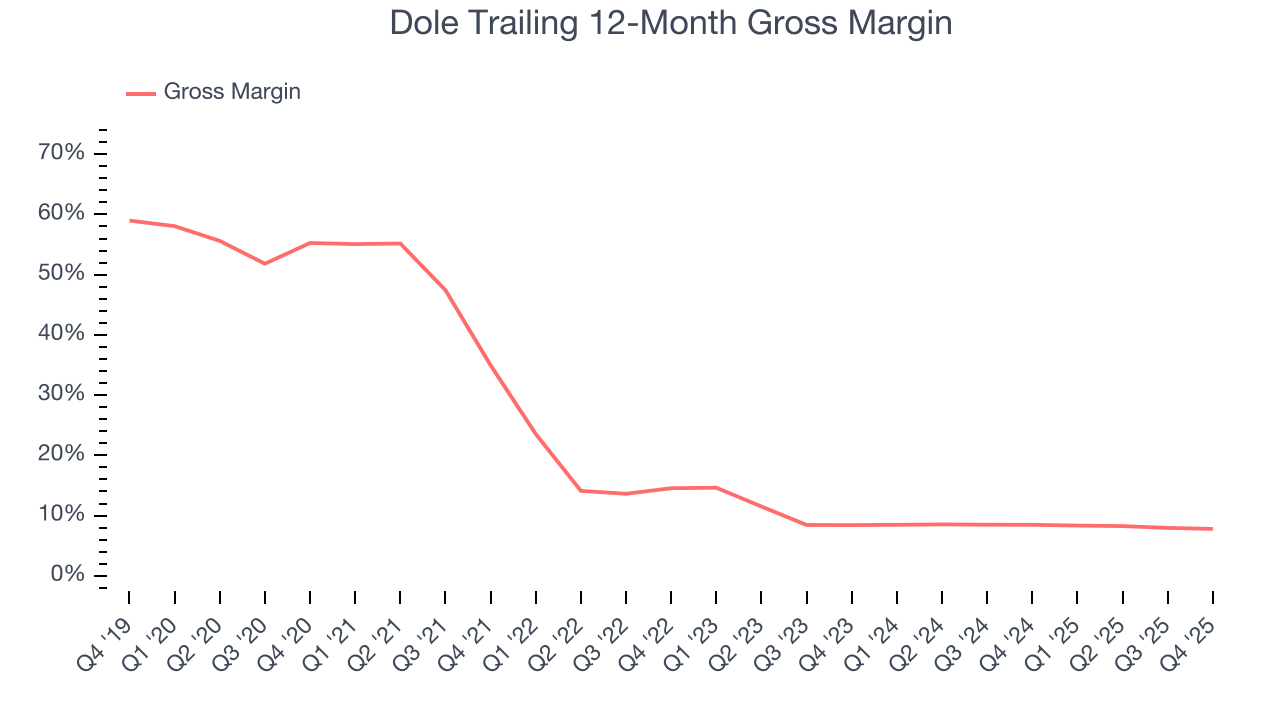

Dole has bad unit economics for a consumer staples company, signaling it operates in a competitive market and lacks pricing power because its products can be substituted. As you can see below, it averaged a 8.1% gross margin over the last two years. That means Dole paid its suppliers a lot of money ($91.89 for every $100 in revenue) to run its business.

This quarter, Dole’s gross profit margin was 6.7%, in line with the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

7. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

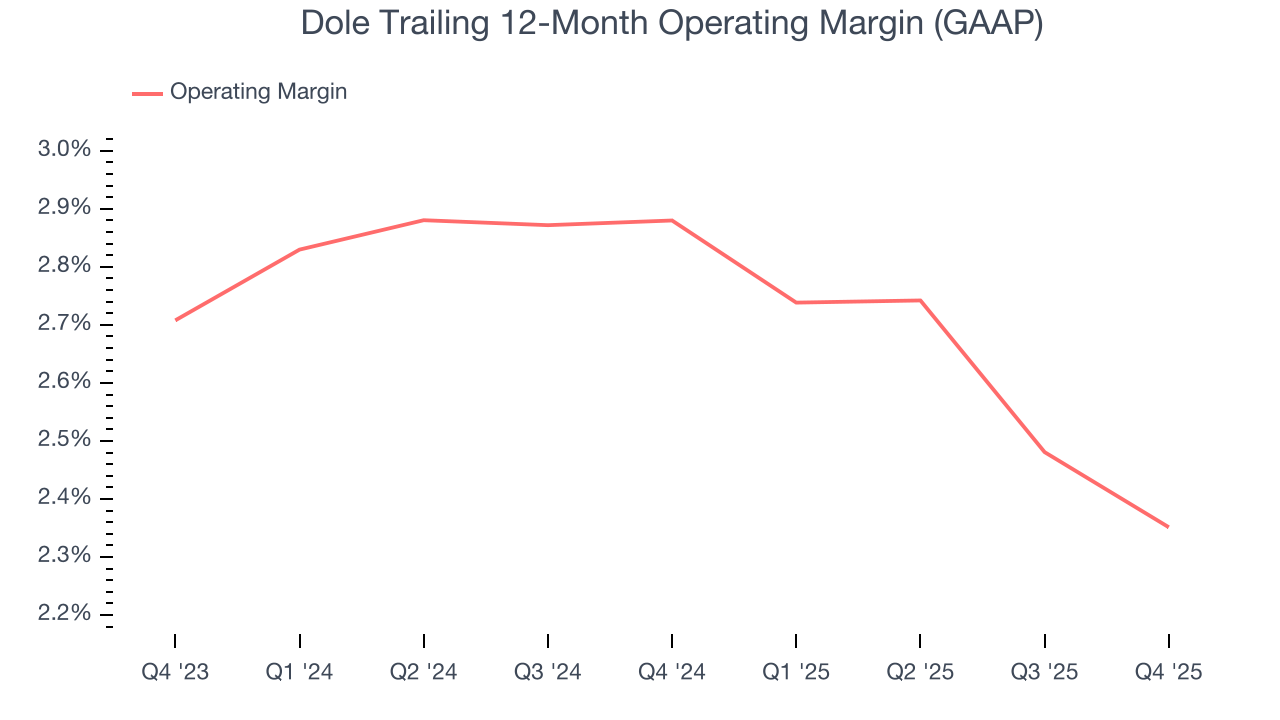

Dole’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 2.6% over the last two years. This profitability was paltry for a consumer staples business and caused by its suboptimal cost structureand low gross margin.

Analyzing the trend in its profitability, Dole’s operating margin might fluctuated slightly but has generally stayed the same over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Dole generated an operating margin profit margin of 1.2%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

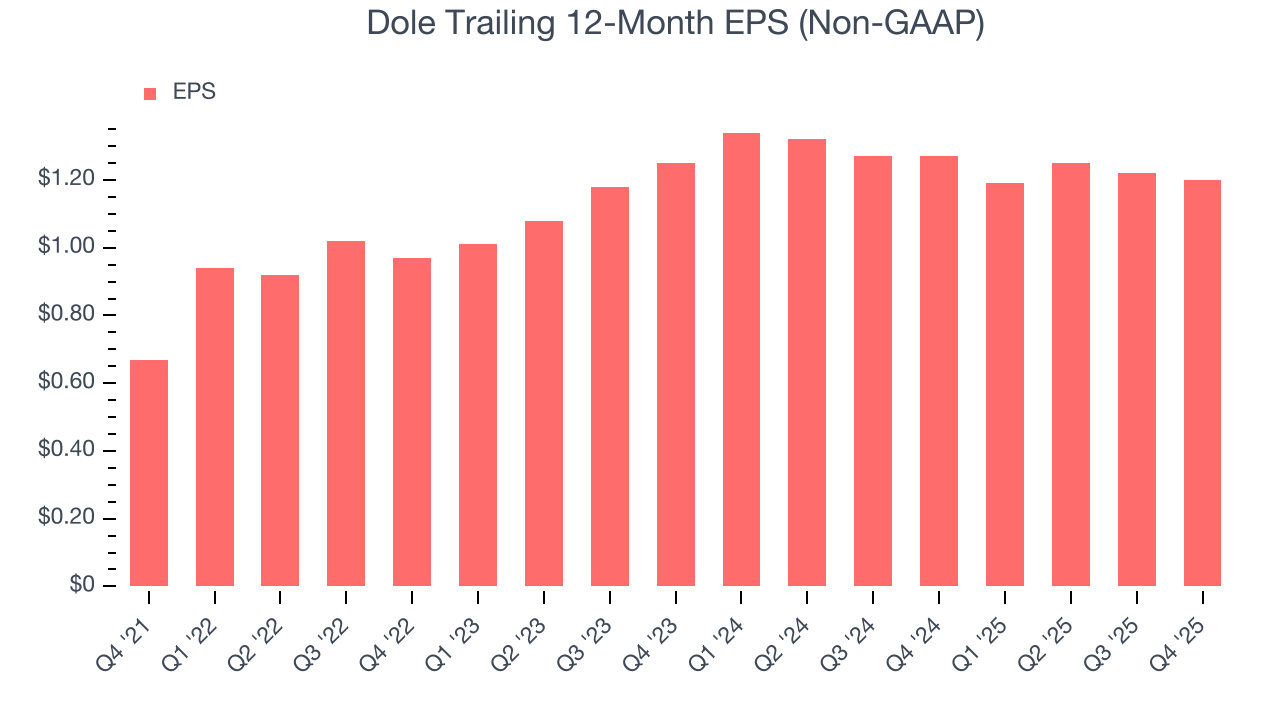

Dole’s EPS grew at a decent 7.4% compounded annual growth rate over the last three years, higher than its 2% annualized revenue growth. However, we take this with a grain of salt because its operating margin didn’t improve and it didn’t repurchase its shares, meaning the delta came from reduced interest expenses or taxes.

In Q4, Dole reported adjusted EPS of $0.14, down from $0.16 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects Dole’s full-year EPS of $1.20 to grow 23.3%.

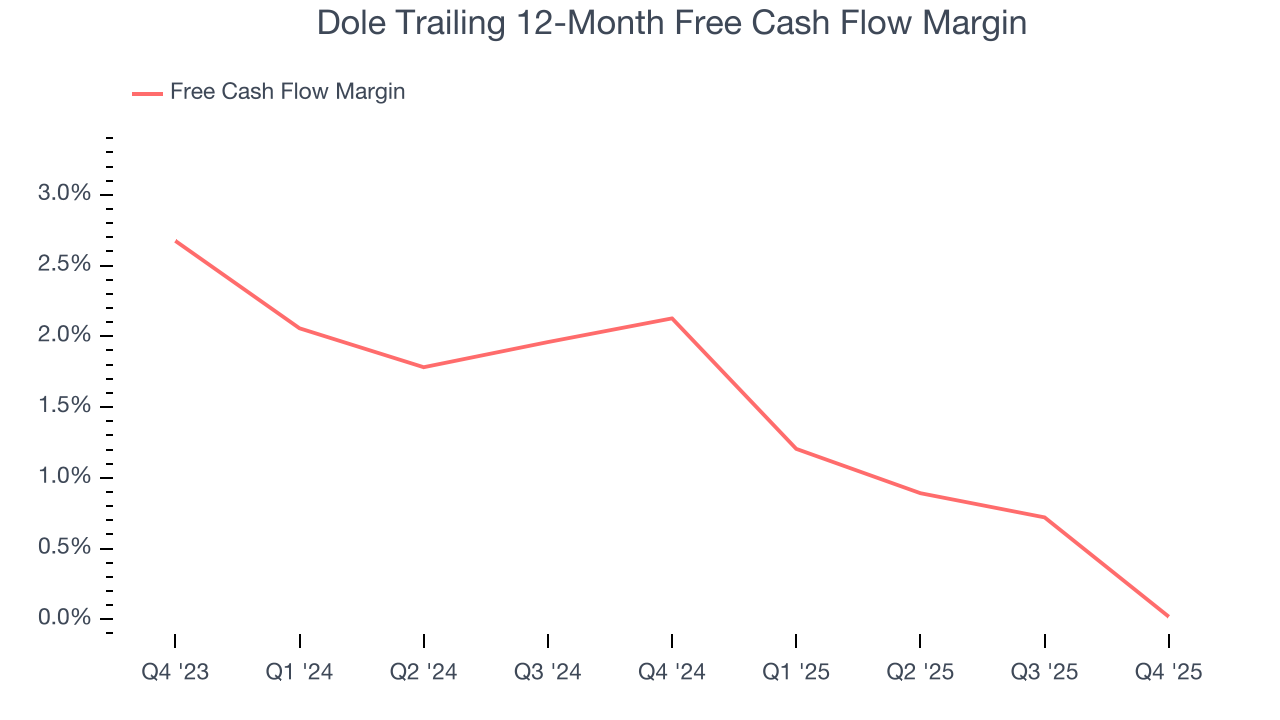

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Dole has shown weak cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 1%, subpar for a consumer staples business.

Taking a step back, we can see that Dole’s margin dropped by 2.1 percentage points over the last year. Almost any movement in the wrong direction is undesirable because of its already low cash conversion. If the trend continues, it could signal it’s becoming a more capital-intensive business.

Dole’s free cash flow clocked in at $67.87 million in Q4, equivalent to a 2.9% margin. The company’s cash profitability regressed as it was 3.2 percentage points lower than in the same quarter last year, but it’s still above its two-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, causing short-term swings. Long-term trends trump temporary fluctuations.

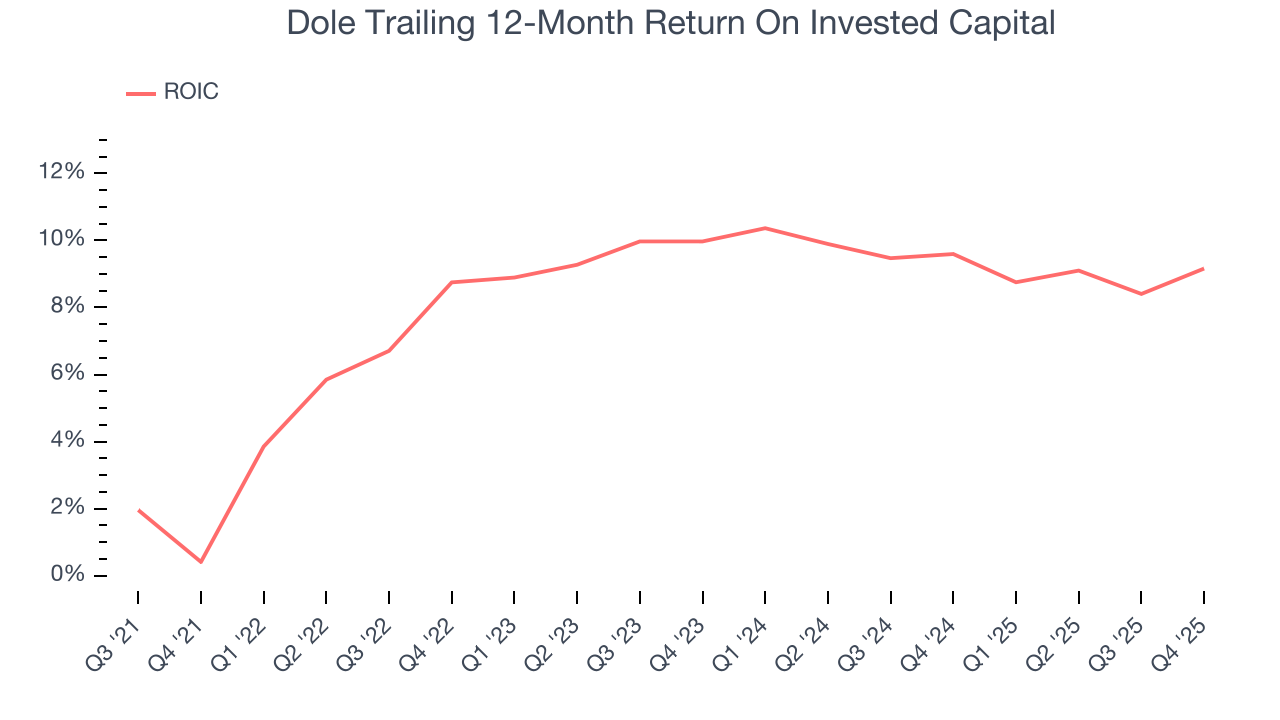

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Dole historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 7.6%, somewhat low compared to the best consumer staples companies that consistently pump out 20%+.

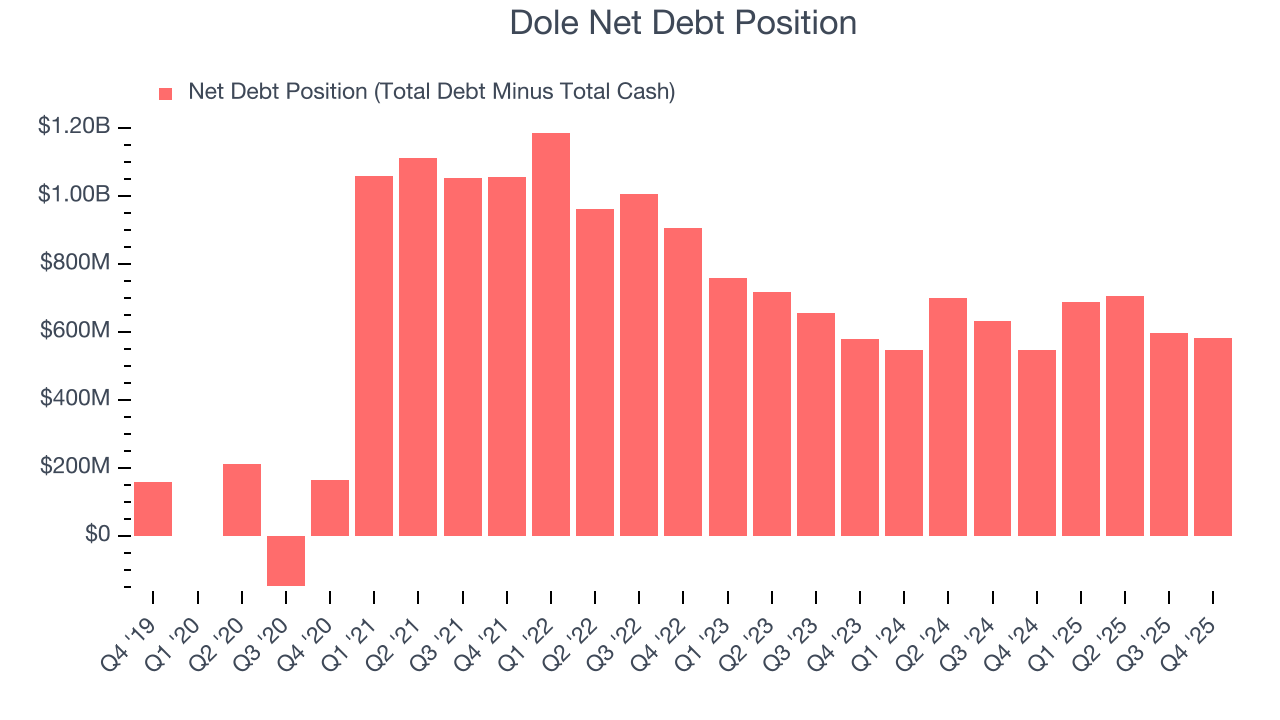

11. Balance Sheet Assessment

Dole reported $274.3 million of cash and $857.5 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $354.3 million of EBITDA over the last 12 months, we view Dole’s 1.6× net-debt-to-EBITDA ratio as safe. We also see its $30.32 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Dole’s Q4 Results

We enjoyed seeing Dole beat analysts’ EBITDA expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its gross margin missed and its EPS was in line with Wall Street’s estimates. Overall, this was a weaker quarter. The stock remained flat at $15.91 immediately after reporting.

13. Is Now The Time To Buy Dole?

Updated: March 15, 2026 at 10:57 PM EDT

When considering an investment in Dole, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

We see the value of companies helping consumers, but in the case of Dole, we’re out. To kick things off, its revenue growth was uninspiring over the last three years, and analysts don’t see anything changing over the next 12 months. While its favorable brand awareness gives it meaningful influence over consumers’ dining decisions, the downside is its gross margins make it more challenging to reach positive operating profits compared to other consumer staples businesses. On top of that, its operating margins are low compared to other consumer staples companies.

Dole’s P/E ratio based on the next 12 months is 10.6x. While this valuation is reasonable, we don’t see a big opportunity at the moment. There are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $17.50 on the company (compared to the current share price of $14.36).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.