Grid Dynamics (GDYN)

We’re firm believers in Grid Dynamics. Its exceptional revenue growth indicates it’s winning market share.― StockStory Analyst Team

1. News

2. Summary

Why We Like Grid Dynamics

With engineering centers across the Americas, Europe, and India serving Fortune 1000 companies, Grid Dynamics (NASDAQ:GDYN) provides technology consulting, engineering, and analytics services to help large enterprises modernize their technology systems and business processes.

- Annual revenue growth of 29.9% over the past five years was outstanding, reflecting market share gains this cycle

- Earnings growth has trumped its peers over the last five years as its EPS has compounded at 21.7% annually

- Forecasted revenue growth of 8.3% for the next 12 months indicates its momentum over the last two years is sustainable

We’re optimistic about Grid Dynamics. The valuation looks reasonable relative to its quality, so this could be a good time to invest in some shares.

Why Is Now The Time To Buy Grid Dynamics?

Grid Dynamics’s stock price of $6.43 implies a valuation ratio of 14.5x forward P/E. Valuation is lower than most companies in the business services space, and we believe Grid Dynamics is attractively-priced for its quality.

Our analysis and backtests consistently tell us that buying high-quality companies and holding them for many years leads to market outperformance. Entry price matters less, but if you can get a good one, all the better.

3. Grid Dynamics (GDYN) Research Report: Q4 CY2025 Update

Digital transformation consultancy Grid Dynamics (NASDAQ:GDYN) met Wall Street’s revenue expectations in Q4 CY2025, with sales up 5.9% year on year to $106.2 million. On the other hand, next quarter’s revenue guidance of $103.5 million was less impressive, coming in 2.9% below analysts’ estimates. Its non-GAAP profit of $0.10 per share was in line with analysts’ consensus estimates.

Grid Dynamics (GDYN) Q4 CY2025 Highlights:

- Revenue: $106.2 million vs analyst estimates of $105.9 million (5.9% year-on-year growth, in line)

- Adjusted EPS: $0.10 vs analyst estimates of $0.09 (in line)

- Adjusted EBITDA: $13.74 million vs analyst estimates of $13.24 million (12.9% margin, 3.8% beat)

- Revenue Guidance for Q1 CY2026 is $103.5 million at the midpoint, below analyst estimates of $106.6 million

- EBITDA guidance for Q1 CY2026 is $12.5 million at the midpoint, below analyst estimates of $13.68 million

- Operating Margin: 0.5%, in line with the same quarter last year

- Market Capitalization: $610.6 million

Company Overview

With engineering centers across the Americas, Europe, and India serving Fortune 1000 companies, Grid Dynamics (NASDAQ:GDYN) provides technology consulting, engineering, and analytics services to help large enterprises modernize their technology systems and business processes.

Grid Dynamics operates at the intersection of business transformation and advanced technology, helping companies implement solutions in four key areas: cloud engineering, AI/machine learning, digital engagement, and supply chain optimization. The company builds custom platforms and applications that enable businesses to leverage cloud computing, data analytics, and artificial intelligence to gain competitive advantages.

For example, Grid Dynamics might help a retailer develop an omnichannel commerce platform that integrates online and in-store shopping experiences, or assist a financial services firm in implementing real-time fraud detection systems using machine learning algorithms. These solutions allow clients to improve customer experiences, optimize operations, and make data-driven decisions.

The company employs a "land and expand" business model, often starting with smaller projects that demonstrate value before expanding into broader transformation initiatives. Grid Dynamics typically deploys technology leaders at client sites who identify new opportunities while delivering current projects. This approach has helped the company deepen relationships with existing clients while attracting new ones.

Grid Dynamics serves clients across several industry verticals, including technology, media and telecom, retail, consumer packaged goods, manufacturing, and financial services. The company's delivery model combines on-site, off-site, and offshore staffing, with engineering teams located in multiple countries to provide flexibility and cost efficiency.

Through acquisitions of companies like Tacit Knowledge, Mutual Mobile, and NextSphere Technologies, Grid Dynamics has expanded its geographic presence and service capabilities. The company maintains ISO 27001:2013 certification for information security management, which is particularly important for its financial services clients who operate in highly regulated environments.

4. IT Services & Consulting

IT Services & Consulting companies stand to benefit from increasing enterprise demand for digital transformation, AI-driven automation, and cybersecurity resilience. Many enterprises can't attack these topics alone and need IT services and consulting on everything from technical advice to implementation. Challenges in meeting these needs will include finding talent in specialized and evolving IT fields. While AI and automation can enhance productivity, they also threaten to commoditize certain consulting functions. Another ongoing challenge will be pricing pressures from offshore IT service providers, which have lower labor costs and increasingly equal access to advanced technology like AI.

Grid Dynamics competes with emerging digital services companies like Globant, Endava, EPAM Systems, and Thoughtworks; large global consulting firms such as Accenture and Capgemini; and India-based IT services providers including Cognizant, Infosys, and Wipro.

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

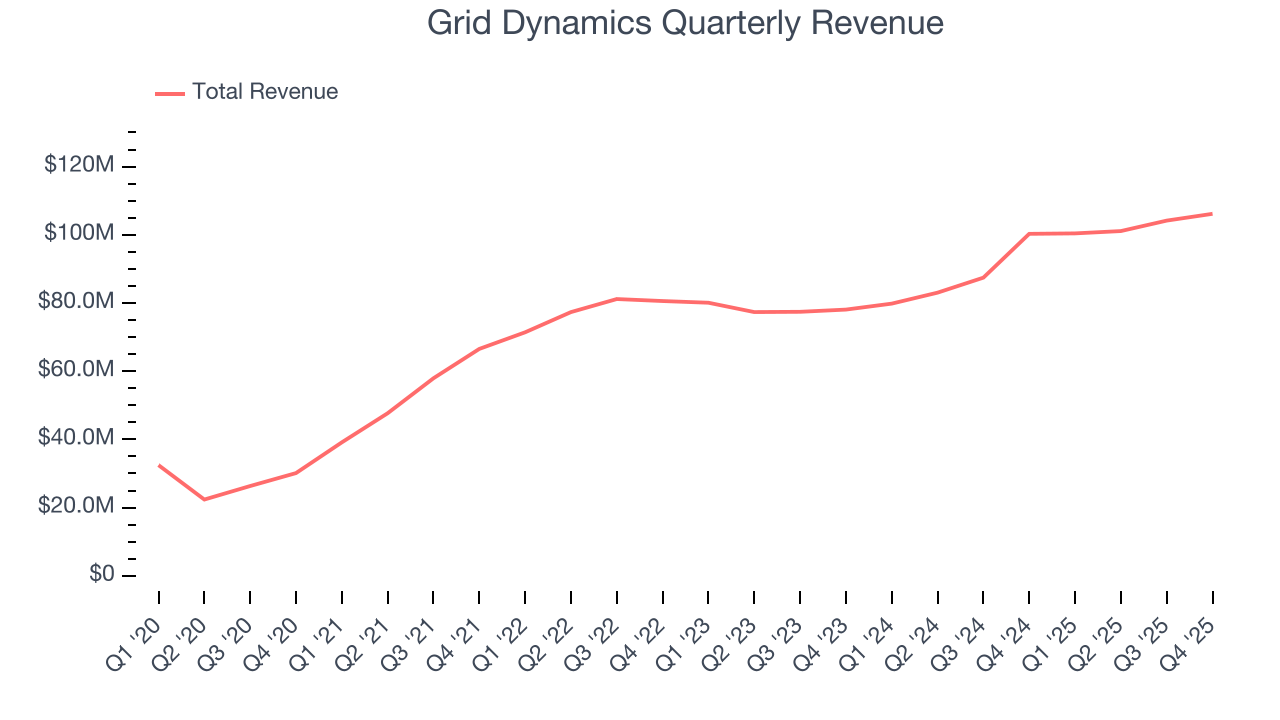

With $411.8 million in revenue over the past 12 months, Grid Dynamics is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

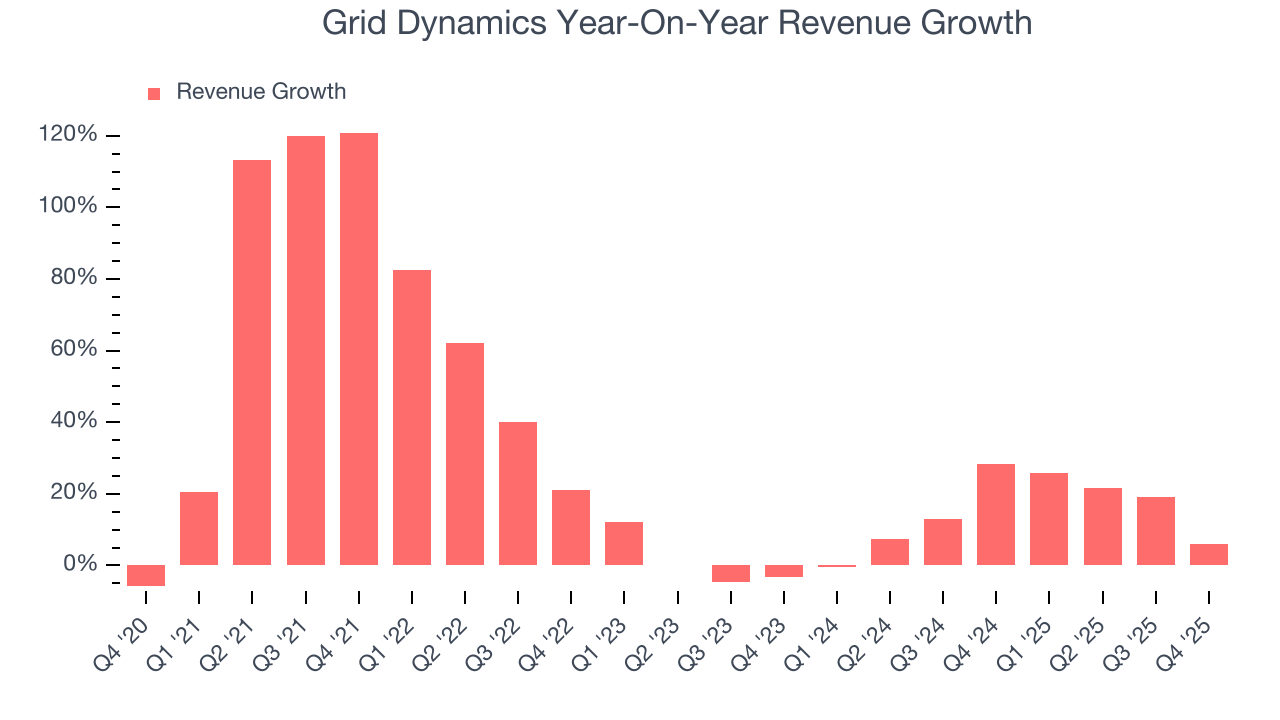

As you can see below, Grid Dynamics’s 29.9% annualized revenue growth over the last five years was incredible. This is an encouraging starting point for our analysis because it shows Grid Dynamics’s demand was higher than many business services companies.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. Grid Dynamics’s annualized revenue growth of 14.7% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Grid Dynamics grew its revenue by 5.9% year on year, and its $106.2 million of revenue was in line with Wall Street’s estimates. Company management is currently guiding for a 3.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 10.1% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is healthy and implies the market sees success for its products and services.

6. Operating Margin

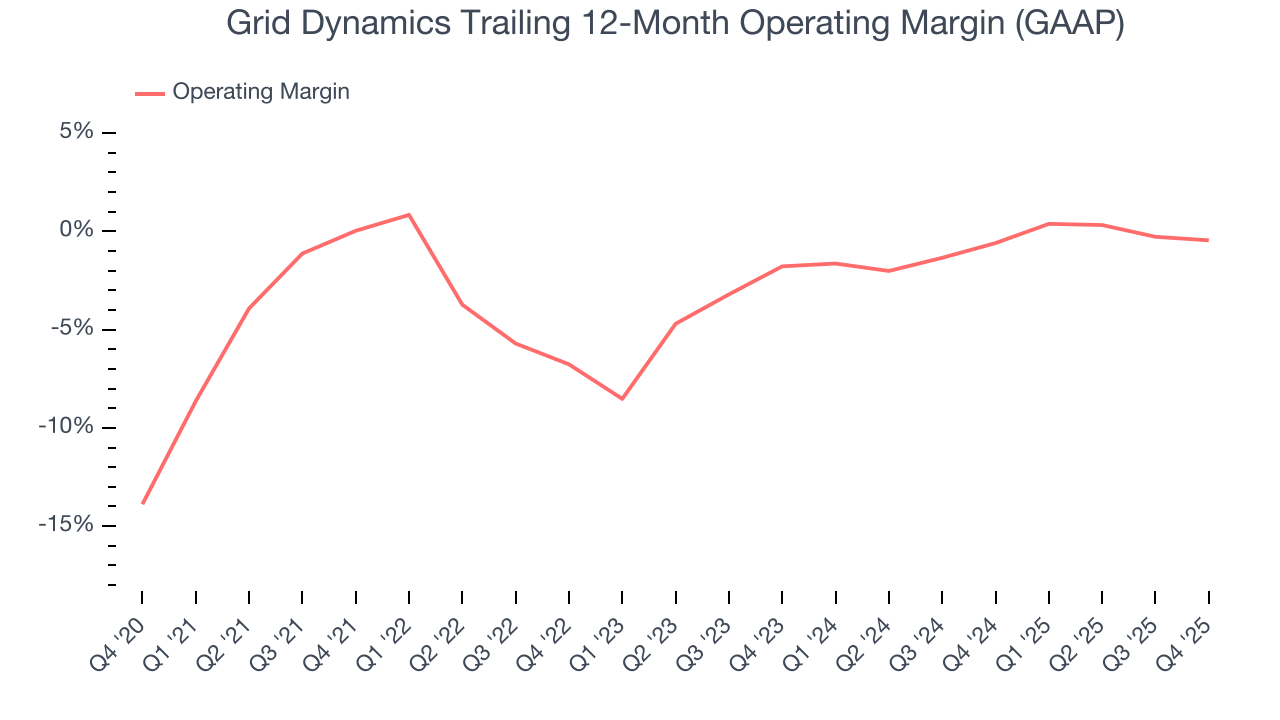

Grid Dynamics’s operating margin has more or less stayed the same over the last 12 months , averaging negative 1.9% over the last five years. Unprofitable, high-growth companies warrant extra attention, especially if their profitability doesn’t improve. In Grid Dynamics’s case, it seems it’s deferring current profits by investing heavily to win market share.

Looking at the trend in its profitability, Grid Dynamics’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Grid Dynamics’s breakeven margin was 0.5%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

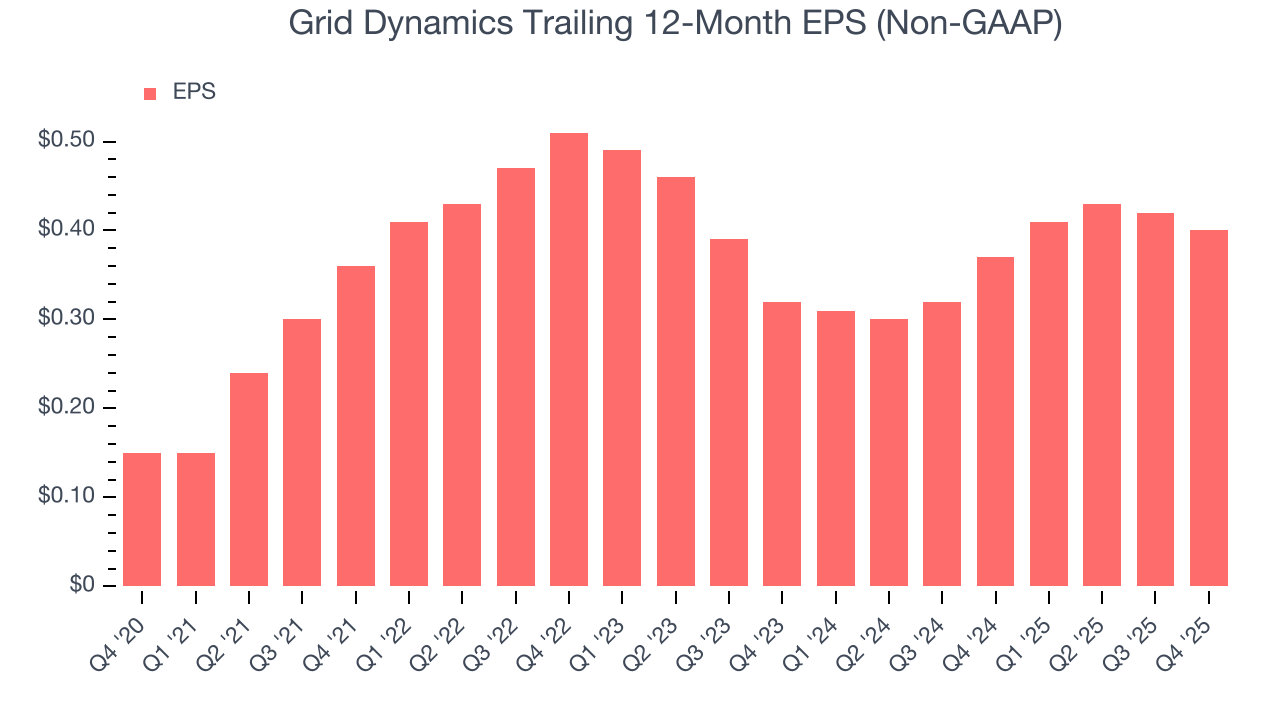

Grid Dynamics’s EPS grew at an astounding 21.7% compounded annual growth rate over the last five years. Despite its operating margin improvement during that time, this performance was lower than its 29.9% annualized revenue growth, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Grid Dynamics, its two-year annual EPS growth of 11.8% was lower than its five-year trend. This wasn’t great, but at least the company was successful in other measures of financial health.

In Q4, Grid Dynamics reported adjusted EPS of $0.10, down from $0.12 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 9.4%. Over the next 12 months, Wall Street expects Grid Dynamics’s full-year EPS of $0.40 to grow 17.5%.

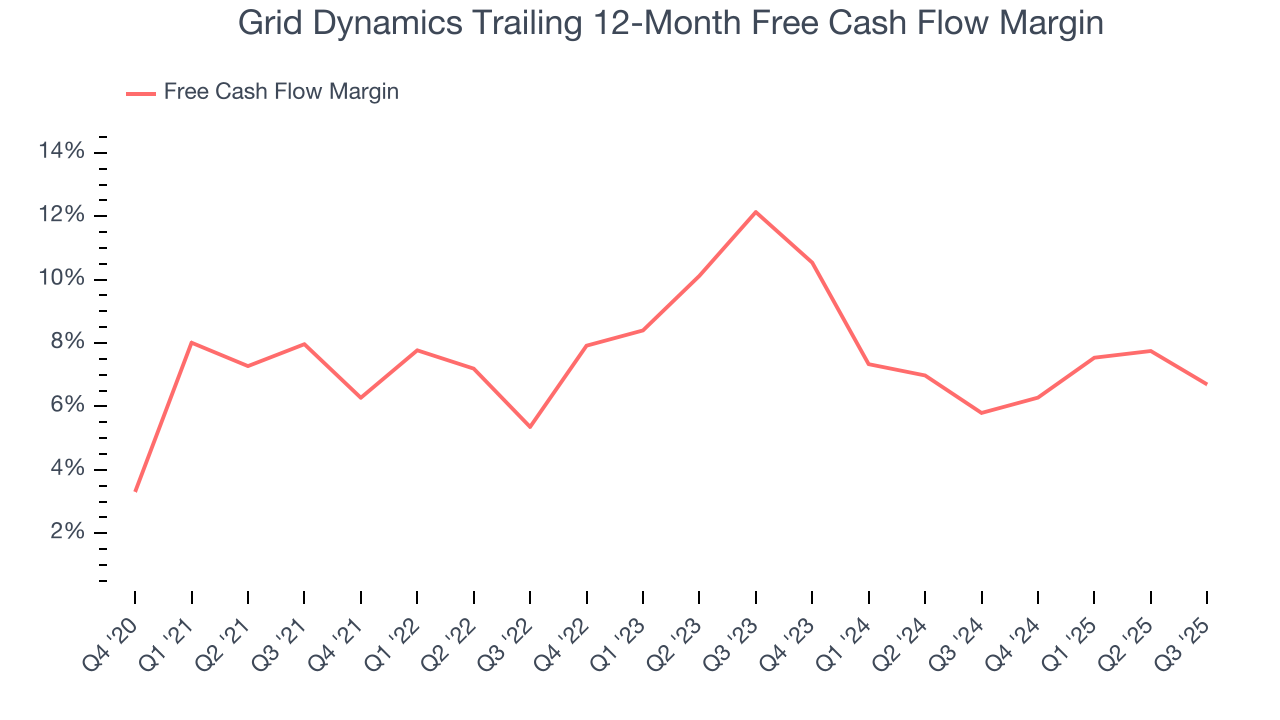

8. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Grid Dynamics has shown impressive cash profitability, giving it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 7.5% over the last five years, better than the broader business services sector. Grid Dynamics has shown impressive cash profitability relative to peers over the last five years, giving the company fewer opportunities to return capital to shareholders. The divergence from its underwhelming operating margin stems from the add-back of non-cash charges like depreciation and stock-based compensation. GAAP operating profit expenses these line items, but free cash flow does not.

Taking a step back, we can see that Grid Dynamics’s margin dropped by 1.8 percentage points during that time. We’re willing to live with its performance for now but hope its cash conversion can rise soon. If its declines continue, it could signal increasing investment needs and capital intensity.

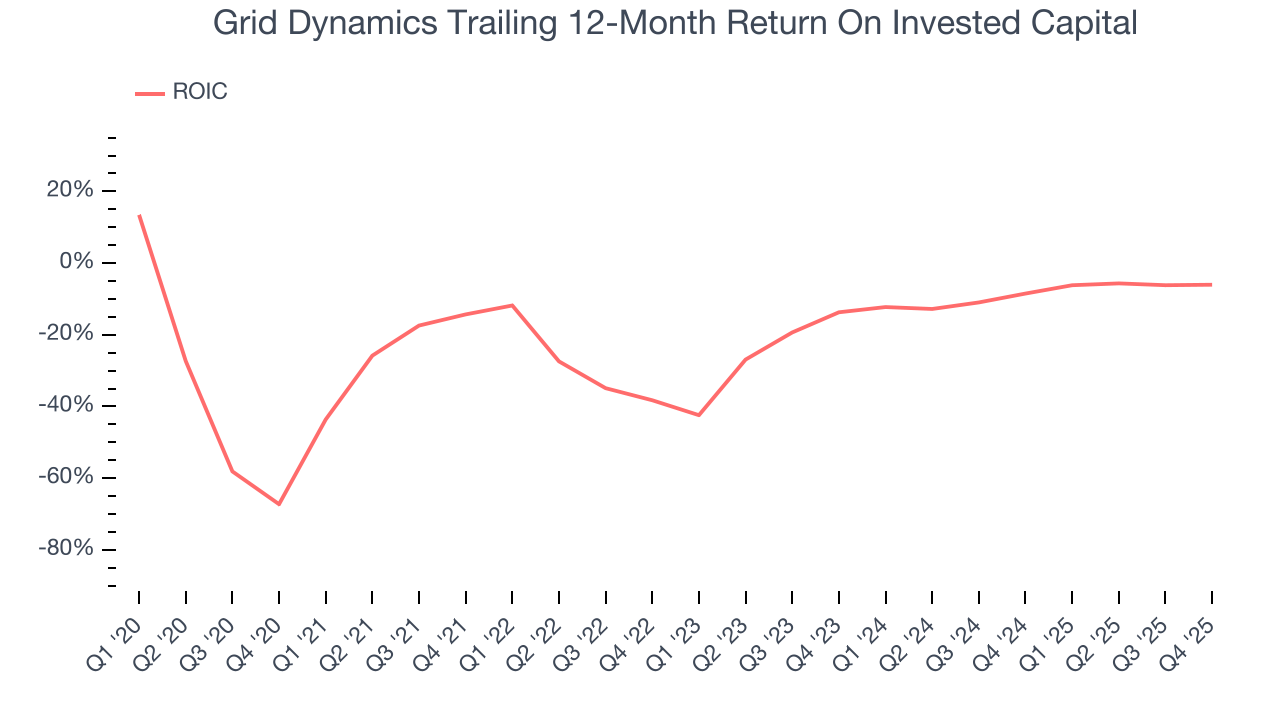

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Although Grid Dynamics has shown solid business quality lately, it struggled to grow profitably in the past. Its five-year average ROIC was negative 16.2%, meaning management lost money while trying to expand the business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Grid Dynamics’s ROIC has increased significantly over the last few years. its rising ROIC is a good sign and could suggest its competitive advantage or profitable growth opportunities are expanding.

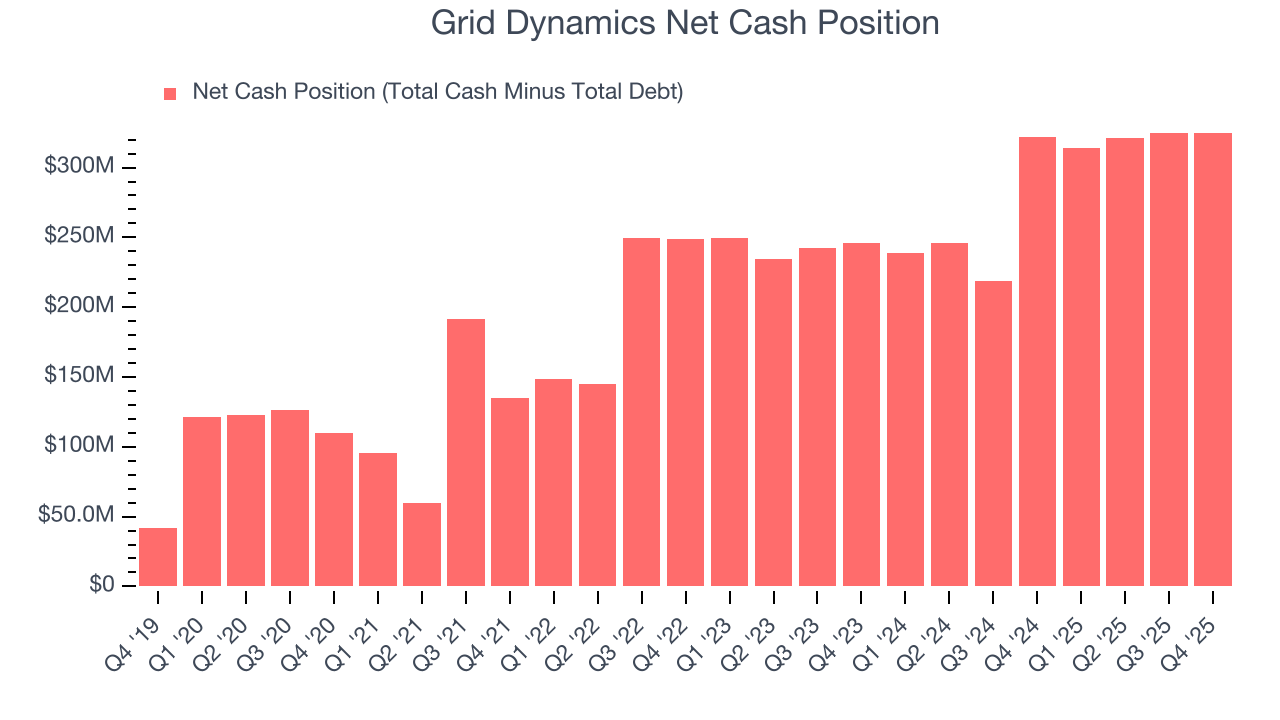

10. Balance Sheet Assessment

Businesses that maintain a cash surplus face reduced bankruptcy risk.

Grid Dynamics is a well-capitalized company with $342.1 million of cash and $17.04 million of debt on its balance sheet. This $325 million net cash position is 53.6% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

11. Key Takeaways from Grid Dynamics’s Q4 Results

It was encouraging to see Grid Dynamics meet analysts’ EPS expectations this quarter. On the other hand, its revenue guidance for next quarter missed and its full-year revenue guidance was in line with Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 2.6% to $6.96 immediately following the results.

12. Is Now The Time To Buy Grid Dynamics?

Updated: March 14, 2026 at 12:24 AM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Grid Dynamics, you should also grasp the company’s longer-term business quality and valuation.

There are several reasons why we think Grid Dynamics is a great business. First of all, the company’s revenue growth was exceptional over the last five years. And while its relatively low ROIC suggests management has struggled to find compelling investment opportunities, its astounding EPS growth over the last five years shows its profits are trickling down to shareholders. On top of that, Grid Dynamics’s rising returns show management's prior bets are starting to pay off.

Grid Dynamics’s P/E ratio based on the next 12 months is 14.5x. Analyzing the business services landscape today, Grid Dynamics’s positive attributes shine bright. We like the stock at this price.

Wall Street analysts have a consensus one-year price target of $10.60 on the company (compared to the current share price of $6.43), implying they see 64.8% upside in buying Grid Dynamics in the short term.