Globalstar (GSAT)

We see solid potential in Globalstar. It not only produces heaps of cash but also has improved its profitability, showing its quality is rising.― StockStory Analyst Team

1. News

2. Summary

Why We Like Globalstar

Known for powering the emergency SOS feature in newer Apple iPhones, Globalstar (NASDAQ:GSAT) operates a network of low-earth orbit satellites that provide voice and data communications services in remote areas where traditional cellular networks don't reach.

- Impressive 16.3% annual revenue growth over the last five years indicates it’s winning market share this cycle

- Earnings growth has trumped its peers over the last four years as its EPS has compounded at 62.7% annually

- Powerful free cash flow generation enables it to reinvest its profits or return capital to investors consistently, and its recently improved profitability means it has even more resources to invest or distribute

We have an affinity for Globalstar. The price seems reasonable relative to its quality, so this might be an opportune time to invest in some shares.

Why Is Now The Time To Buy Globalstar?

Globalstar is trading at $58.45 per share, or 50x forward EV-to-EBITDA. Sure, the valuation multiple seems high and could make for some share price rockiness. But given its fundamentals, we think the multiple is justified.

By definition, where you buy a stock impacts returns. But according to our work on the topic, business quality is a much bigger determinant of market outperformance over the long term compared to entry price.

3. Globalstar (GSAT) Research Report: Q4 CY2025 Update

Satellite communications provider Globalstar (NASDAQ:GSAT) announced better-than-expected revenue in Q4 CY2025, with sales up 17.6% year on year to $71.96 million. On the other hand, the company’s full-year revenue guidance of $292.5 million at the midpoint came in 3.9% below analysts’ estimates. Its GAAP loss of $0.11 per share was significantly below analysts’ consensus estimates.

Globalstar (GSAT) Q4 CY2025 Highlights:

- Revenue: $71.96 million vs analyst estimates of $70.64 million (17.6% year-on-year growth, 1.9% beat)

- EPS (GAAP): -$0.11 vs analyst estimates of -$0.04 (significant miss)

- Adjusted EBITDA: $32.37 million vs analyst estimates of $35.71 million (45% margin, 9.4% miss)

- Operating Margin: -0.5%, up from -6.9% in the same quarter last year

- Free Cash Flow Margin: 53.2%, down from 286% in the same quarter last year

- Market Capitalization: $7.34 billion

Company Overview

Known for powering the emergency SOS feature in newer Apple iPhones, Globalstar (NASDAQ:GSAT) operates a network of low-earth orbit satellites that provide voice and data communications services in remote areas where traditional cellular networks don't reach.

Globalstar's satellite network consists of both first and second-generation low-earth orbit satellites positioned to provide coverage between 70° north and 70° south latitude, essentially covering most of the Earth's populated areas. The company maintains ground stations called gateways that communicate with these satellites, creating a seamless network that can authenticate users and establish voice or data connections.

The company offers several key services through its satellite infrastructure. Its Duplex service enables two-way voice and data communications via specialized satellite phones. The SPOT family of products provides personal tracking and emergency notification devices popular with outdoor enthusiasts, having initiated thousands of rescues since launching in 2007. Commercial IoT devices like SmartOne and ST100 allow businesses to track and monitor remote assets such as shipping containers, rail cars, and oil equipment.

In 2022, Globalstar entered a significant partnership with Apple to provide satellite connectivity for emergency SOS features in newer iPhone models. This wholesale capacity service represents an important revenue stream alongside its traditional subscriber-based business. The company is also developing its terrestrial spectrum assets, with licenses in 11 countries covering a population of approximately 814 million people.

Customers span diverse industries including recreation, government, public safety, oil and gas, maritime, utilities, and transportation. A typical user might be an oil rig worker making a call from a remote location, a hiker sending an SOS signal after an injury, or a logistics company tracking shipping containers across oceans. The company generates revenue through activation fees, usage charges, and equipment sales.

Globalstar is expanding its satellite constellation, having contracted with MDA to build up to 26 new satellites with launches beginning in 2025 via SpaceX. The company is also developing two-way commercial IoT products to expand its capabilities beyond tracking to include command and control functions.

4. Satellite Telecommunication Services

Satellite telecommunication is generally buoyed by rising global demand for connectivity in costly-to-connect and remote areas. IoT (Internet of Things) expansion and government-backed space and defense initiatives also help. As advancements in low Earth orbit (LEO) technology happen, companies in the space will have more favorable competitive positions, which could lead to further partnerships with mobile network operators to extend coverage. On the other hand, headwinds include high capital expenditures for satellite deployment as well as regulatory hurdles related to spectrum allocation. Competition from larger players like SpaceX’s Starlink and Amazon’s Kuiper could also intensify over time, especially if tech advancements lead to better unit economics and financial prospects.

Globalstar's primary competitors in the satellite communications market include Iridium Communications (NASDAQ:IRDM), Viasat (NASDAQ:VSAT), and ORBCOMM. The company also faces emerging competition in the direct-to-cellular satellite service space from SpaceX's Starlink and other new market entrants.

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

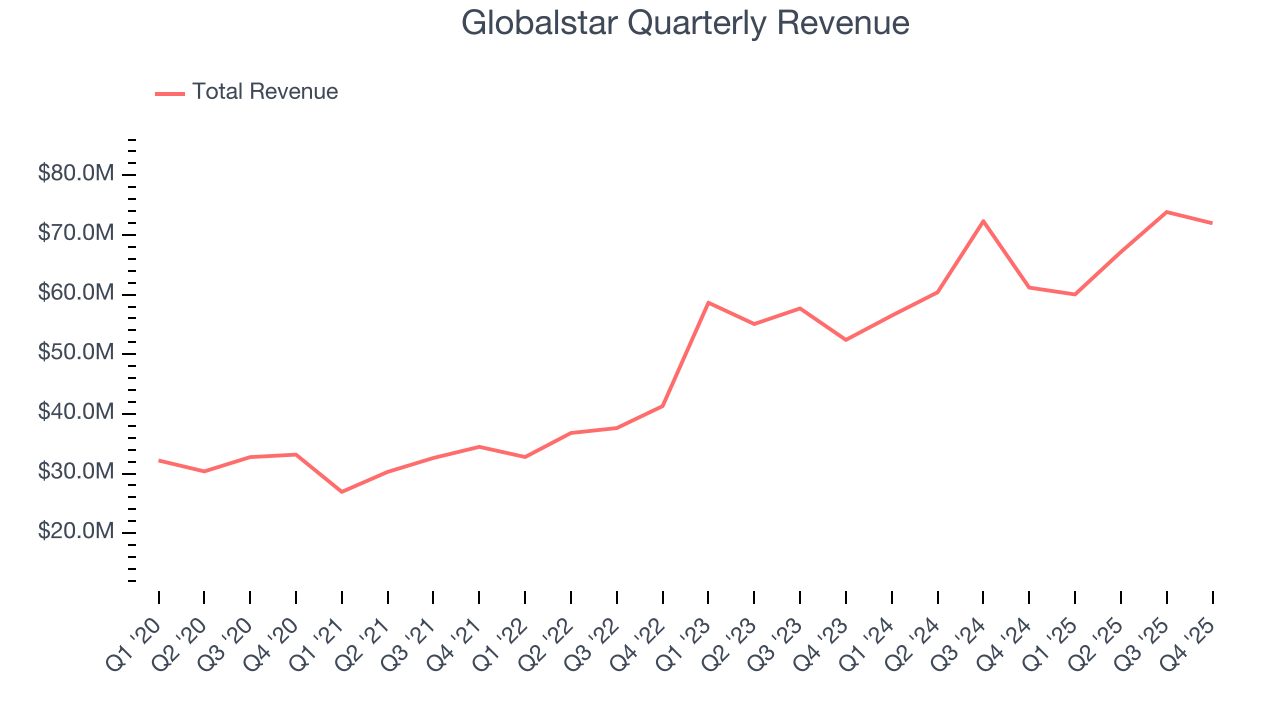

With $273 million in revenue over the past 12 months, Globalstar is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

As you can see below, Globalstar’s sales grew at an incredible 16.3% compounded annual growth rate over the last five years. This is a great starting point for our analysis because it shows Globalstar’s demand was higher than many business services companies.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. Globalstar’s annualized revenue growth of 10.4% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

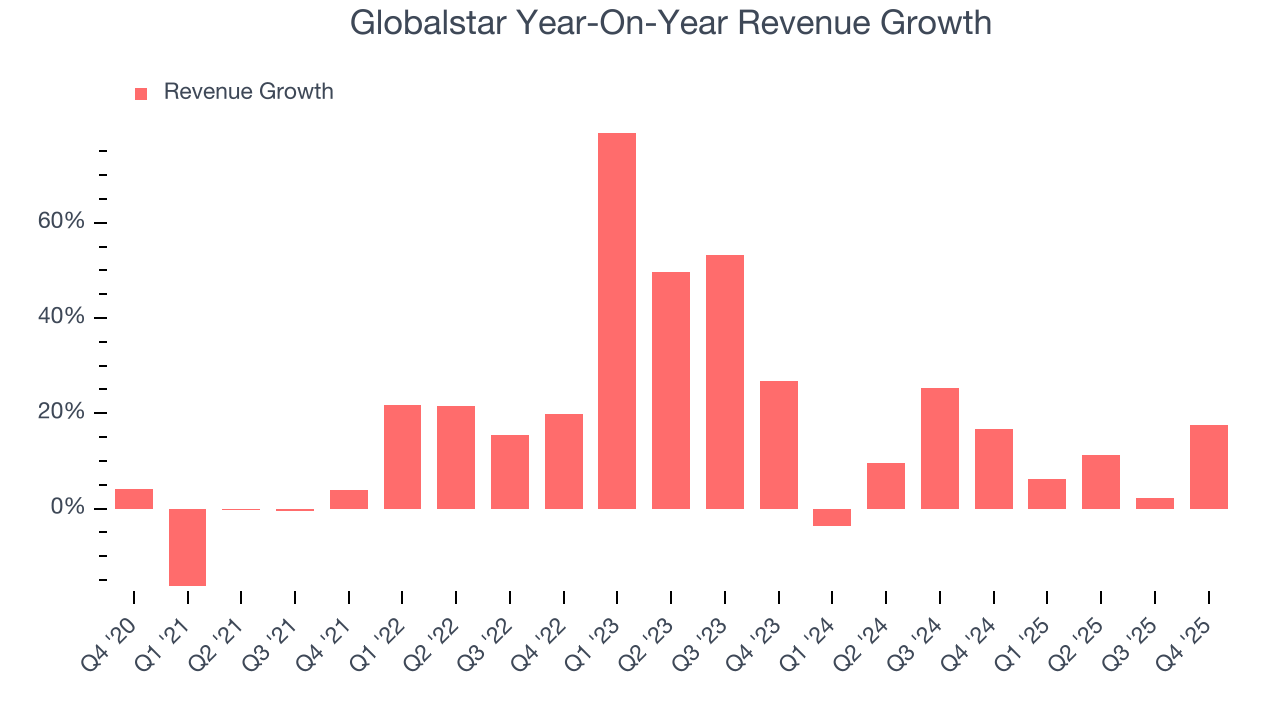

This quarter, Globalstar reported year-on-year revenue growth of 17.6%, and its $71.96 million of revenue exceeded Wall Street’s estimates by 1.9%.

Looking ahead, sell-side analysts expect revenue to grow 11.5% over the next 12 months, similar to its two-year rate. This projection is admirable and implies its newer products and services will spur better top-line performance.

6. Operating Margin

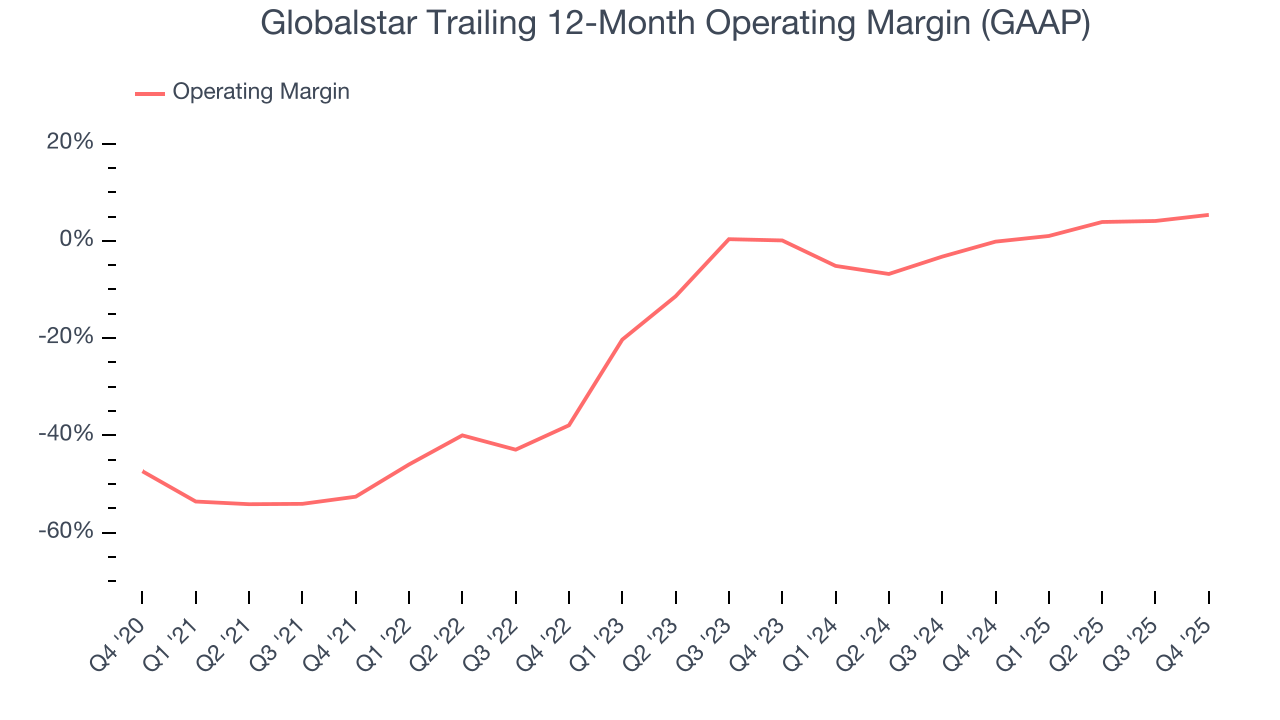

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Although Globalstar broke even this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 10.5% over the last five years. Unprofitable business services companies require extra attention because they could get caught swimming naked when the tide goes out.

On the plus side, Globalstar’s operating margin rose by 57.9 percentage points over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to reach long-term profitability.

In Q4, Globalstar generated a negative 0.5% operating margin.

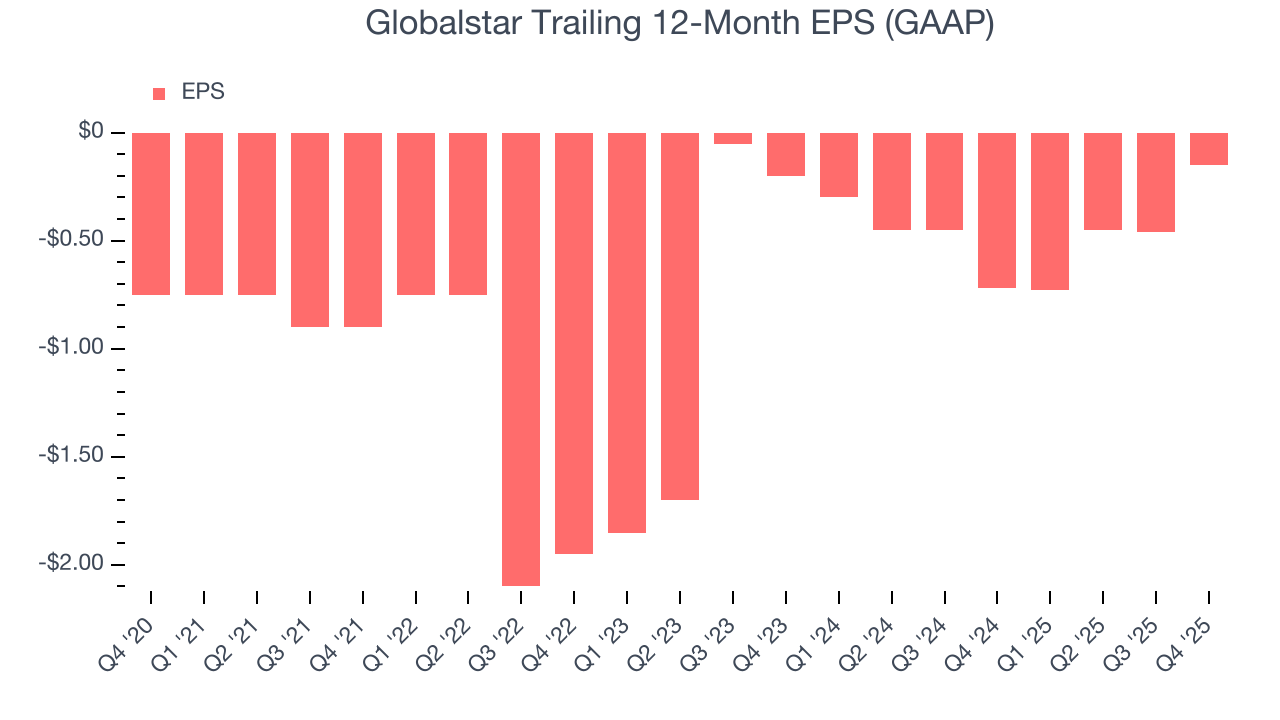

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Although Globalstar’s full-year earnings are still negative, it reduced its losses and improved its EPS by 27.5% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability. We hope to see an inflection point soon.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Globalstar, its two-year annual EPS growth of 13.6% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q4, Globalstar reported EPS of negative $0.11, up from negative $0.42 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street expects Globalstar to improve its earnings losses. Analysts forecast its full-year EPS of negative $0.15 will advance to negative $0.04.

8. Cash Is King

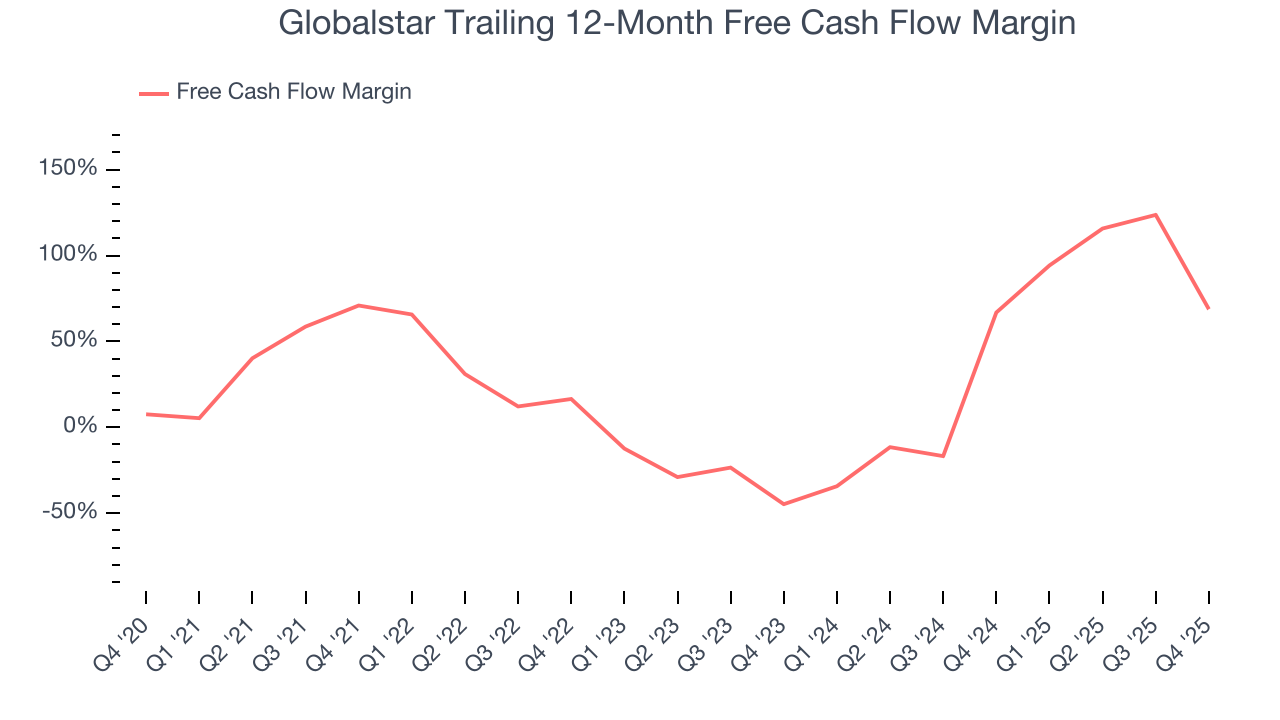

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Globalstar has shown terrific cash profitability, enabling it to reinvest, return capital to investors, and stay ahead of the competition while maintaining an ample cushion. The company’s free cash flow margin was among the best in the business services sector, averaging an eye-popping 36% over the last five years. The divergence from its underwhelming operating margin stems from the add-back of non-cash charges like depreciation and stock-based compensation. GAAP operating profit expenses these line items, but free cash flow does not.

Taking a step back, we can see that Globalstar’s margin dropped by 2.1 percentage points during that time. If its declines continue, it could signal increasing investment needs and capital intensity.

Globalstar’s free cash flow clocked in at $38.26 million in Q4, equivalent to a 53.2% margin. The company’s cash profitability regressed as it was 232.6 percentage points lower than in the same quarter last year, but it’s still above its five-year average. We wouldn’t put too much weight on this quarter’s decline because investment needs can be seasonal, causing short-term swings. Long-term trends carry greater meaning.

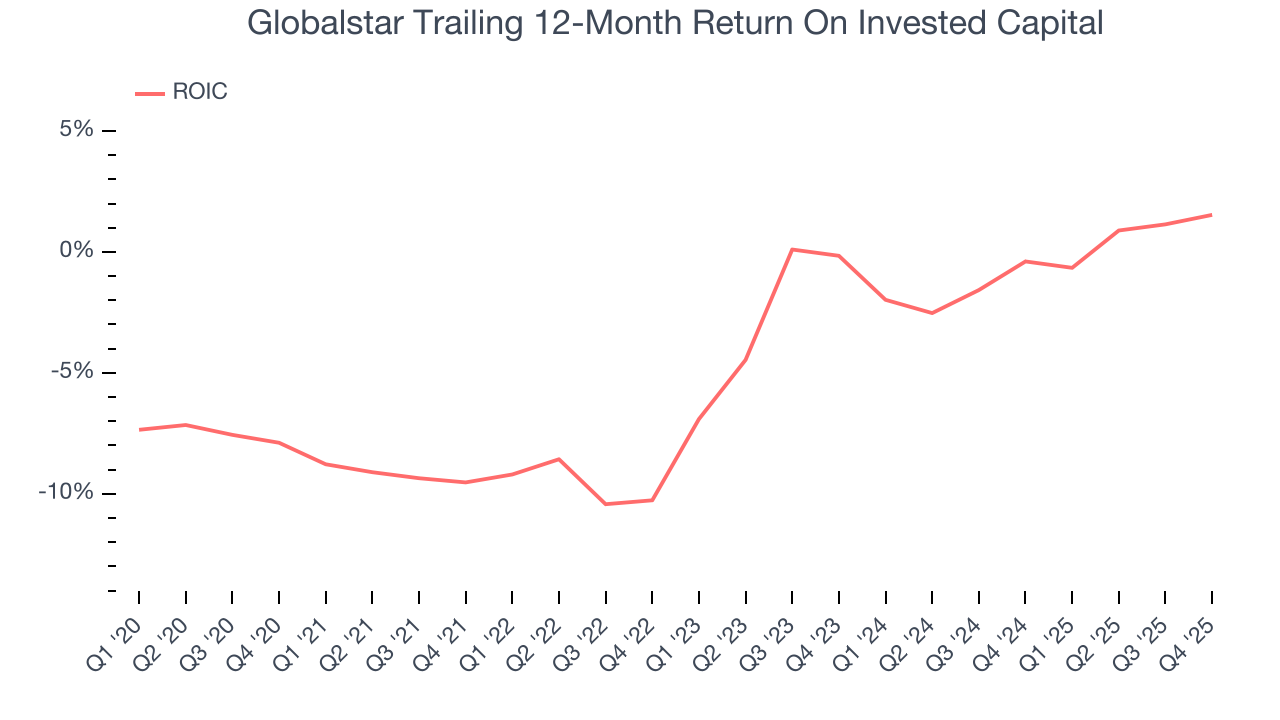

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although Globalstar has shown solid business quality lately, it struggled to grow profitably in the past. Its five-year average ROIC was negative 3.8%, meaning management lost money while trying to expand the business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Globalstar’s ROIC has increased. This is a good sign, but we recognize its lack of profitable growth during the COVID era was the primary reason for the change.

10. Balance Sheet Assessment

Globalstar reported $447.5 million of cash and $538.3 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $136.1 million of EBITDA over the last 12 months, we view Globalstar’s 0.7× net-debt-to-EBITDA ratio as safe. We also see its $40.92 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Globalstar’s Q4 Results

It was encouraging to see Globalstar beat analysts’ revenue expectations this quarter. On the other hand, its full-year revenue guidance missed and its EPS fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 1.9% to $56.41 immediately after reporting.

12. Is Now The Time To Buy Globalstar?

Updated: March 15, 2026 at 12:00 AM EDT

Before deciding whether to buy Globalstar or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

There is a lot to like about Globalstar. First of all, the company’s revenue growth was exceptional over the last five years. And while its relatively low ROIC suggests management has struggled to find compelling investment opportunities, its powerful free cash flow generation enables it to stay ahead of the competition through consistent reinvestment of profits. Additionally, Globalstar’s rising cash profitability gives it more optionality.

Globalstar’s EV-to-EBITDA ratio based on the next 12 months is 50x. You get what you pay for, and in this particular situation, Globalstar’s higher valuation multiple is justified because its fundamentals shine bright. We think it deserves a spot in your portfolio.

Wall Street analysts have a consensus one-year price target of $69.33 on the company (compared to the current share price of $58.45), implying they see 18.6% upside in buying Globalstar in the short term.