Halozyme Therapeutics (HALO)

Halozyme Therapeutics is a sound business. Its fast sales growth, profitability, and superb prospects give it an attractive return algorithm.― StockStory Analyst Team

1. News

2. Summary

Why Halozyme Therapeutics Is Interesting

Known for transforming hours-long intravenous infusions into minutes-long subcutaneous injections, Halozyme Therapeutics (NASDAQ:HALO) develops and licenses its proprietary ENHANZE technology that enables subcutaneous delivery of injectable drugs that would otherwise require intravenous administration.

- Annual revenue growth of 44.2% over the past five years was outstanding, reflecting market share gains this cycle

- Projected revenue growth of 36.9% for the next 12 months is above its two-year trend, pointing to accelerating demand

- A drawback is its smaller revenue base of $1.24 billion means it hasn’t achieved the economies of scale that some industry juggernauts enjoy (but also enables it to grow faster if it executes properly)

Halozyme Therapeutics is solid, but not perfect. If you like the stock, the valuation looks reasonable.

Why Is Now The Time To Buy Halozyme Therapeutics?

Halozyme Therapeutics’s stock price of $79 implies a valuation ratio of 9.9x forward P/E. This valuation is quite compelling when considering the revenue growth you get.

Now could be a good time to invest if you believe in the story.

3. Halozyme Therapeutics (HALO) Research Report: Q4 CY2025 Update

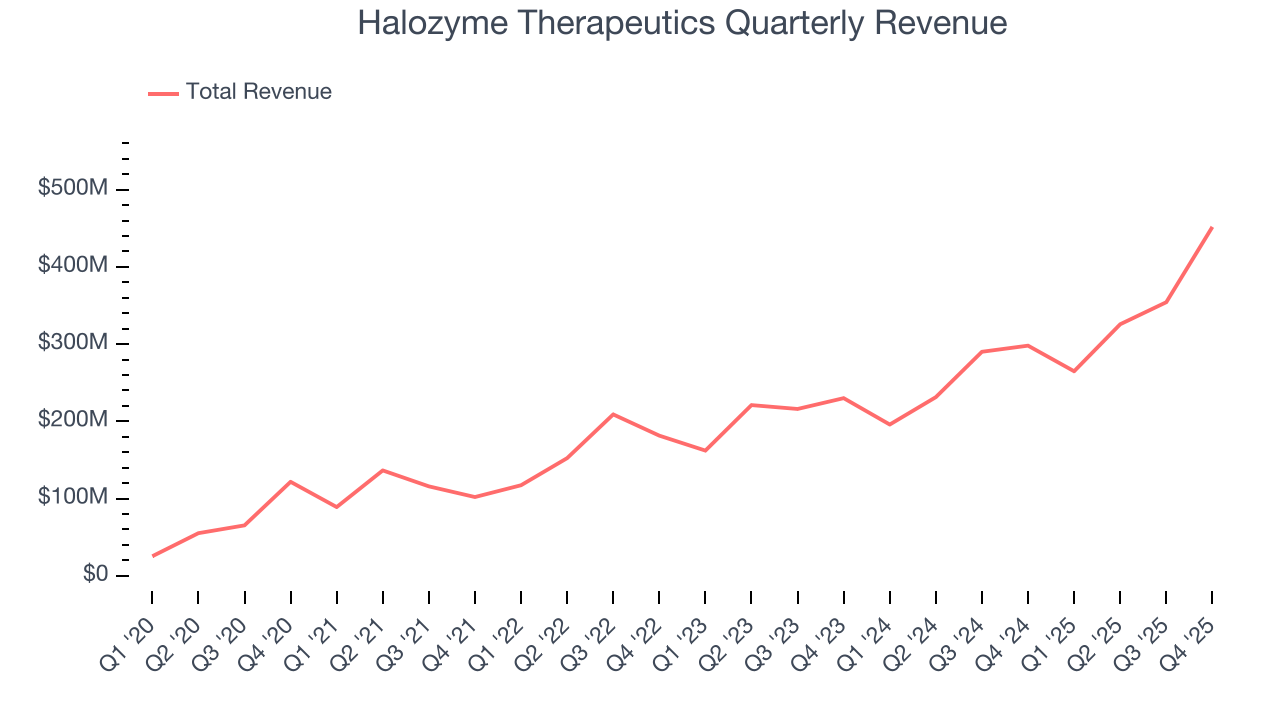

Biopharmaceutical drug delivery company Halozyme Therapeutics (NASDAQ:HALO) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 51.6% year on year to $451.8 million. The company expects the full year’s revenue to be around $1.76 billion, close to analysts’ estimates. Its non-GAAP loss of $0.24 per share was significantly below analysts’ consensus estimates.

Halozyme Therapeutics (HALO) Q4 CY2025 Highlights:

- Revenue: $451.8 million vs analyst estimates of $449.2 million (51.6% year-on-year growth, 0.6% beat)

- Adjusted EBITDA: $21.9 million vs analyst estimates of $303.2 million (4.8% margin, 92.8% miss but included acquired IPR&D expense of $284.9 million related to the Surf Bio acquisition in the fourth quarter of 2025)

- Adjusted EPS: -$0.24 vs analyst estimates of $2.20 (significant miss but included acquired IPR&D expense of $284.9 million related to the Surf Bio acquisition in the fourth quarter of 2025)

- Adjusted EPS guidance for the upcoming financial year 2026 is $8 at the midpoint, missing analyst estimates by 2.2%

- EBITDA guidance for the upcoming financial year 2026 is $1.17 billion at the midpoint, below analyst estimates of $1.22 billion

- Operating Margin: -20.6%, down from 58.9% in the same quarter last year

- Market Capitalization: $9.34 billion

Company Overview

Known for transforming hours-long intravenous infusions into minutes-long subcutaneous injections, Halozyme Therapeutics (NASDAQ:HALO) develops and licenses its proprietary ENHANZE technology that enables subcutaneous delivery of injectable drugs that would otherwise require intravenous administration.

Halozyme's ENHANZE technology is built around rHuPH20, a recombinant human enzyme that temporarily breaks down hyaluronan, a structural component found in tissues beneath the skin. This temporary degradation creates a pathway for large volume or viscous drug formulations to be administered subcutaneously instead of through time-consuming intravenous infusions.

The company operates primarily through partnerships with major pharmaceutical companies, who pay Halozyme licensing fees, milestone payments, and royalties to incorporate ENHANZE into their products. Notable partners include Roche, Takeda, Janssen, Bristol Myers Squibb, and argenx, who use the technology to develop subcutaneous versions of established intravenous drugs. For example, Roche's breast cancer treatment Herceptin can be administered in 2-5 minutes subcutaneously rather than 30-90 minutes intravenously when formulated with ENHANZE.

Beyond its flagship ENHANZE platform, Halozyme also develops and commercializes auto-injector technologies for pharmaceutical companies. The company markets two proprietary products: Hylenex, a formulation of rHuPH20 used to increase the absorption and dispersion of other injected drugs, and XYOSTED, an auto-injector testosterone replacement therapy product for men with conditions associated with testosterone deficiency.

Halozyme's business model leverages its specialized technology across multiple therapeutic areas through partnerships while maintaining a relatively focused internal commercial operation. This approach allows pharmaceutical companies to extend patent life, improve patient convenience, and potentially enable home administration of therapies that previously required clinical settings for intravenous delivery.

4. Therapeutics

Over the next few years, therapeutic companies, which develop a wide variety of treatments for diseases and disorders, face strong tailwinds from advancements in precision medicine (including the use of AI to improve hit rates) and growing demand for treatments targeting rare diseases. However, headwinds such as rising scrutiny over drug pricing, regulatory unknowns, and competition from larger, more resourced pharmaceutical companies could weigh on growth.

Halozyme's competitors in the drug delivery technology space include Antares Pharma (acquired by Halozyme), West Pharmaceutical Services (NYSE: WST), Becton Dickinson (NYSE: BDX), and several private companies developing alternative delivery systems for injectable medications.

5. Revenue Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With just $1.40 billion in revenue over the past 12 months, Halozyme Therapeutics is a small company in an industry where scale matters. This makes it difficult to build trust with customers because healthcare is heavily regulated, complex, and resource-intensive. On the bright side, Halozyme Therapeutics’s smaller revenue base allows it to grow faster if it can execute well.

6. Revenue Growth

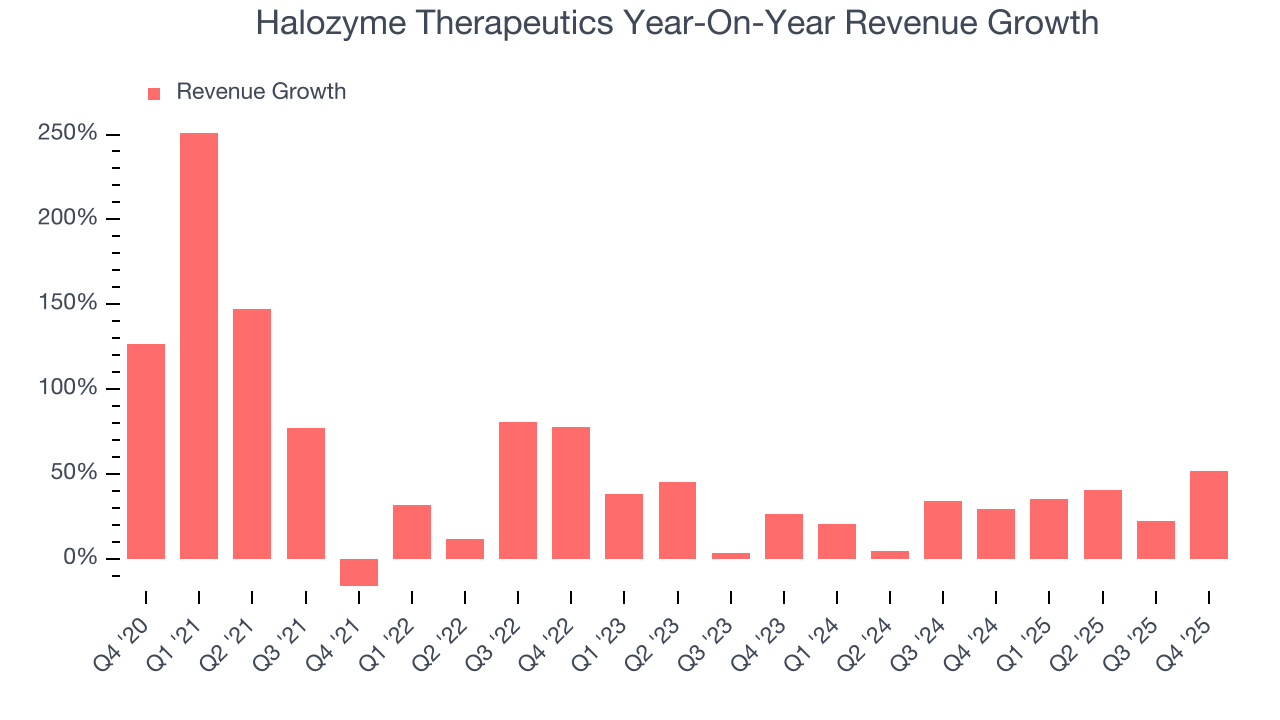

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Halozyme Therapeutics grew its sales at an incredible 39.2% compounded annual growth rate. Its growth beat the average healthcare company and shows its offerings resonate with customers, a helpful starting point for our analysis.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Halozyme Therapeutics’s annualized revenue growth of 29.8% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Halozyme Therapeutics reported magnificent year-on-year revenue growth of 51.6%, and its $451.8 million of revenue beat Wall Street’s estimates by 0.6%.

Looking ahead, sell-side analysts expect revenue to grow 26.1% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is admirable and implies the market is forecasting success for its products and services.

7. Operating Margin

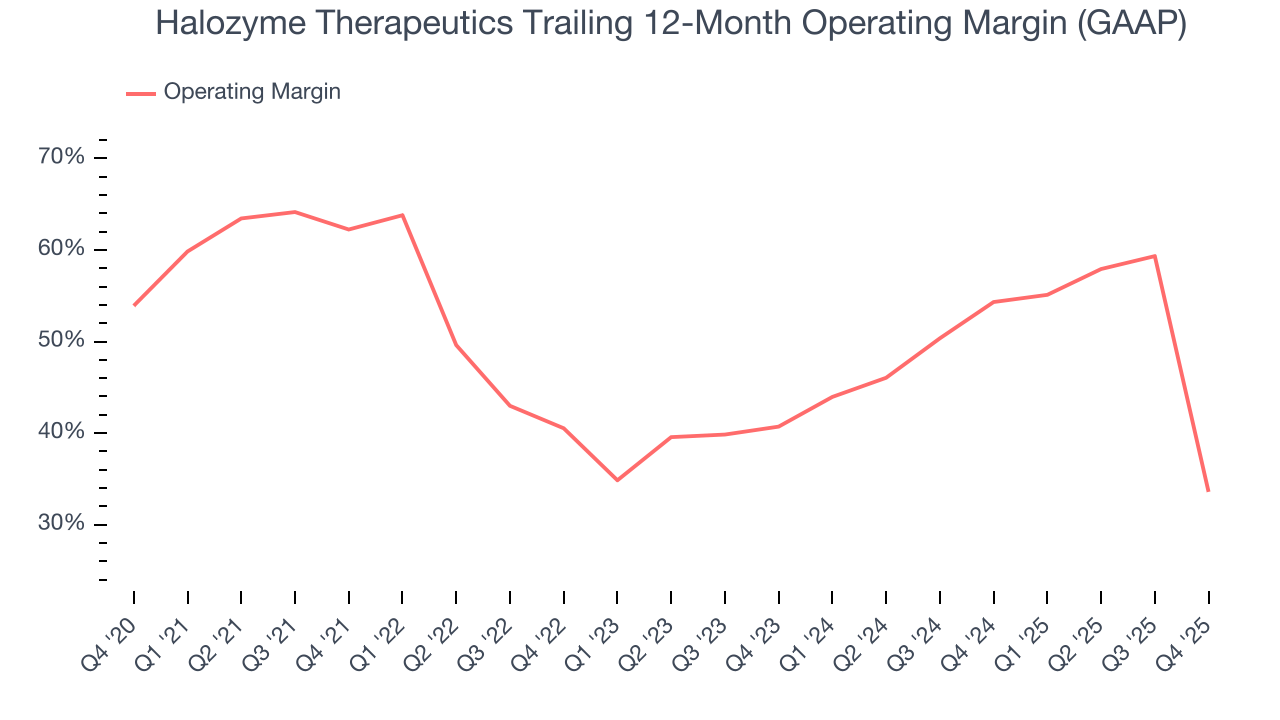

Halozyme Therapeutics has been a well-oiled machine over the last five years. It demonstrated elite profitability for a healthcare business, boasting an average operating margin of 43.8%.

Looking at the trend in its profitability, Halozyme Therapeutics’s operating margin decreased by 28.7 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 7.1 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

This quarter, Halozyme Therapeutics generated an operating margin profit margin of negative 20.6%, down 79.5 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

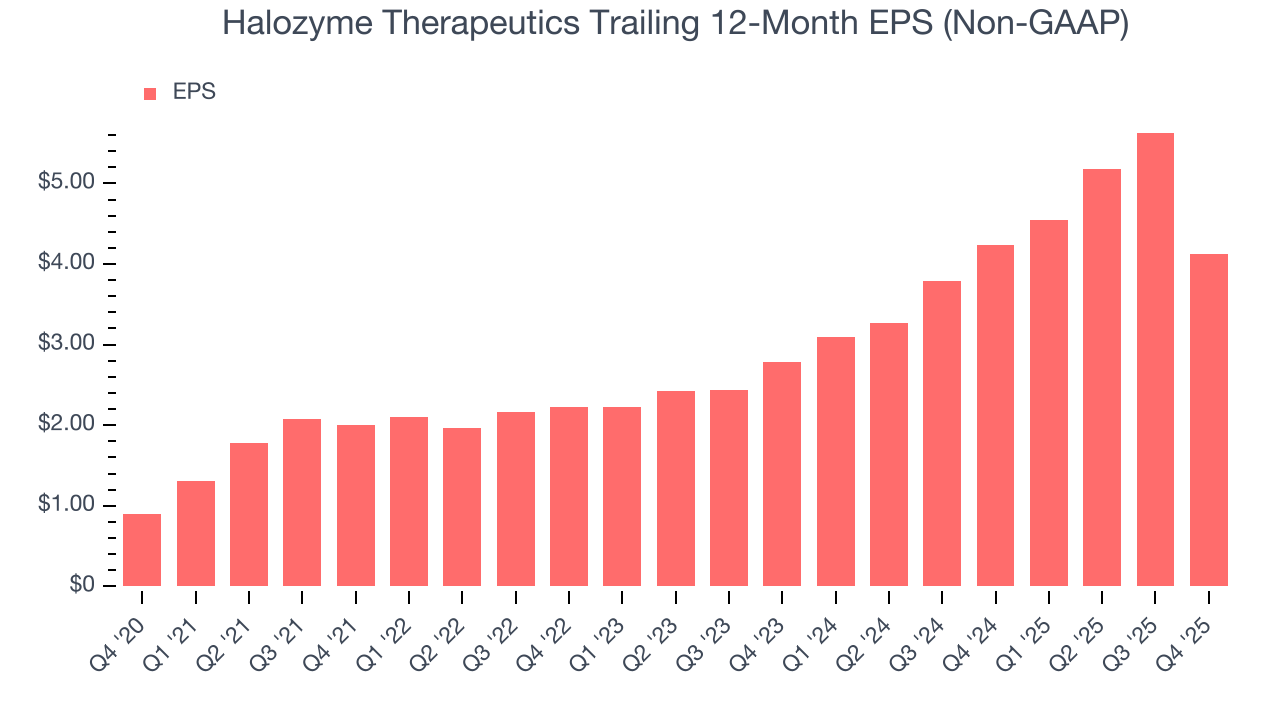

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Halozyme Therapeutics’s EPS grew at an astounding 35.6% compounded annual growth rate over the last five years. However, this performance was lower than its 39.2% annualized revenue growth, telling us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

We can take a deeper look into Halozyme Therapeutics’s earnings to better understand the drivers of its performance. As we mentioned earlier, Halozyme Therapeutics’s operating margin declined by 28.7 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, Halozyme Therapeutics reported adjusted EPS of negative $0.24, down from $1.26 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects Halozyme Therapeutics’s full-year EPS of $4.13 to grow 97.8%.

9. Cash Is King

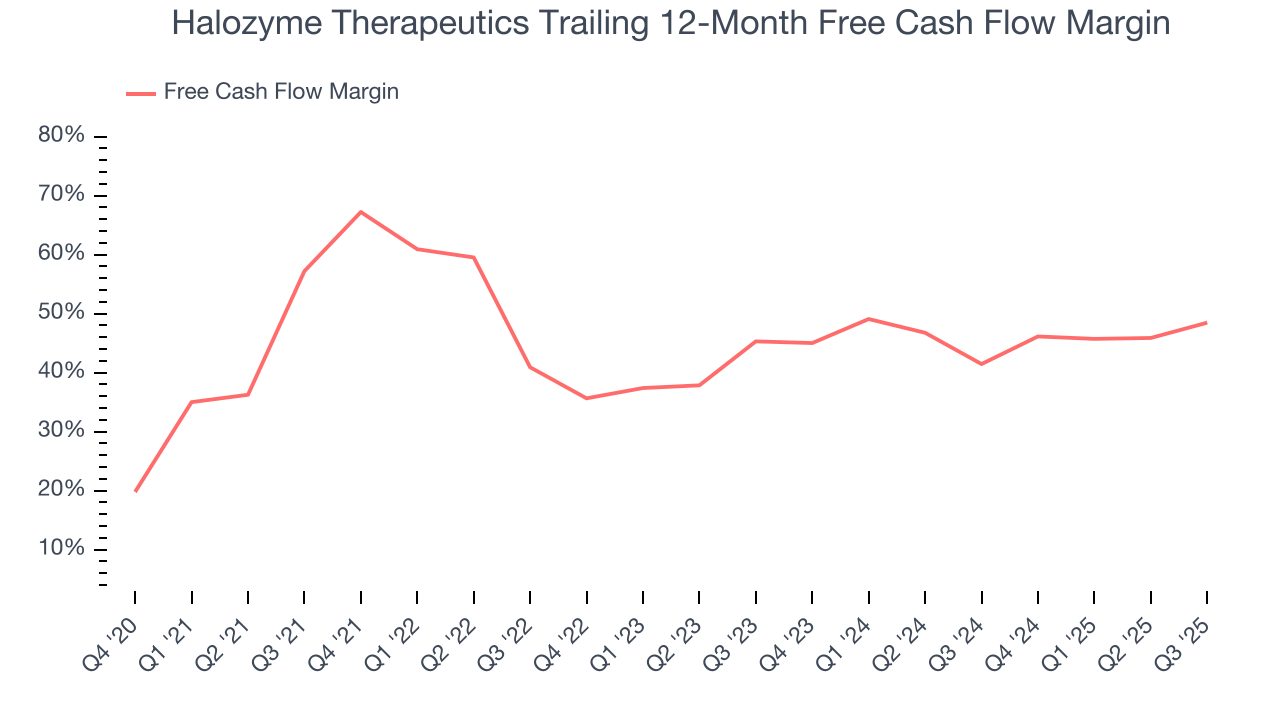

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Halozyme Therapeutics has shown terrific cash profitability, enabling it to reinvest, return capital to investors, and stay ahead of the competition while maintaining an ample cushion. The company’s free cash flow margin was among the best in the healthcare sector, averaging an eye-popping 46.3% over the last five years.

Taking a step back, we can see that Halozyme Therapeutics’s margin dropped by 18 percentage points during that time. Continued declines could signal it is in the middle of an investment cycle.

10. Balance Sheet Assessment

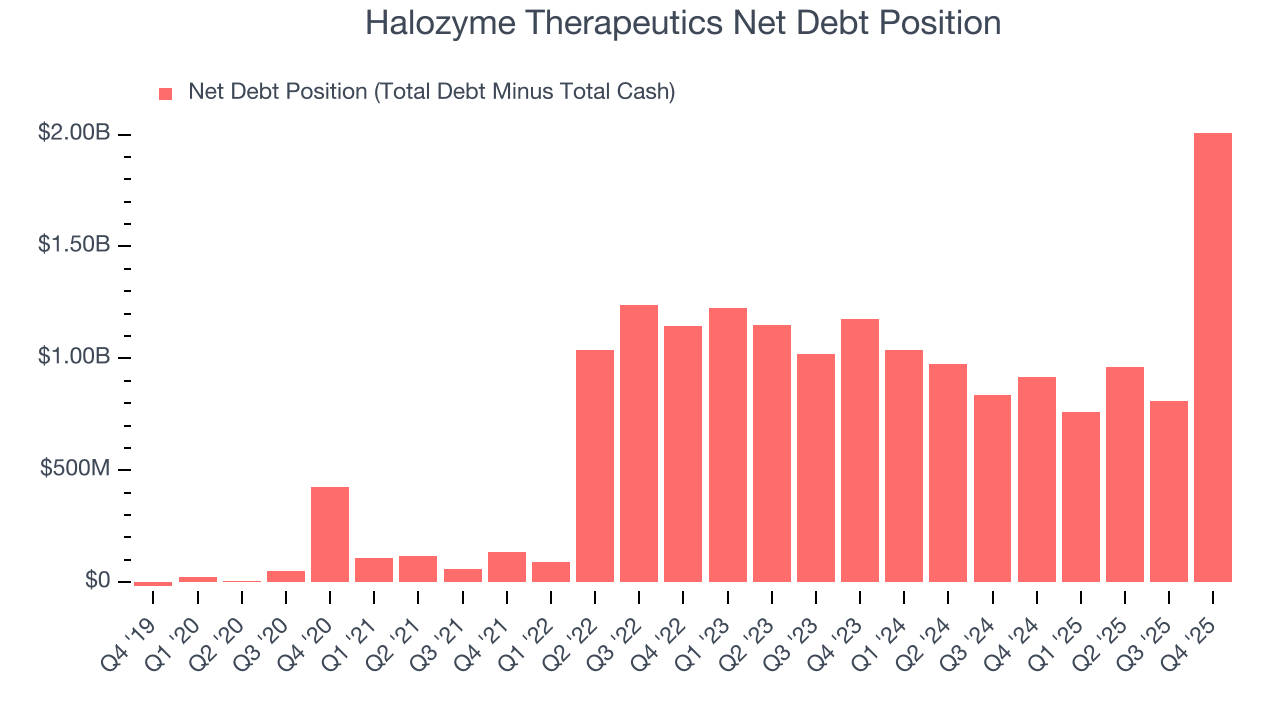

Halozyme Therapeutics reported $133.8 million of cash and $2.14 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $645.2 million of EBITDA over the last 12 months, we view Halozyme Therapeutics’s 3.1× net-debt-to-EBITDA ratio as safe. We also see its $5.40 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Halozyme Therapeutics’s Q4 Results

It was good to see Halozyme Therapeutics narrowly top analysts’ revenue expectations this quarter. On the other hand, its EPS missed and its full-year EPS guidance fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 2.7% to $78.44 immediately after reporting.

12. Is Now The Time To Buy Halozyme Therapeutics?

Updated: February 17, 2026 at 4:20 PM EST

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Halozyme Therapeutics.

There are a lot of things to like about Halozyme Therapeutics. First off, its revenue growth was exceptional over the last five years. And while Halozyme Therapeutics’s declining operating margin shows the business has become less efficient, its powerful free cash flow generation enables it to stay ahead of the competition through consistent reinvestment of profits.

Halozyme Therapeutics’s P/E ratio based on the next 12 months is 9.8x. When scanning the healthcare space, Halozyme Therapeutics trades at a fair valuation. If you trust the business and its direction, this is an ideal time to buy.

Wall Street analysts have a consensus one-year price target of $78 on the company (compared to the current share price of $78.44).