The Honest Company (HNST)

The Honest Company faces an uphill battle. Not only has its sales growth been weak but also its negative returns on capital show it destroyed value.― StockStory Analyst Team

1. News

2. Summary

Why We Think The Honest Company Will Underperform

Co-founded by actress Jessica Alba, The Honest Company (NASDAQ:HNST) sells diapers and wipes, skin care products, and household cleaning products.

- Projected sales decline of 17.1% for the next 12 months points to a tough demand environment ahead

- Push for growth has led to negative returns on capital, signaling value destruction

- Revenue base of $371.3 million puts it at a disadvantage compared to larger competitors exhibiting economies of scale

The Honest Company’s quality is inadequate. Our attention is focused on better businesses.

Why There Are Better Opportunities Than The Honest Company

The Honest Company is trading at $2.76 per share, or 29.5x forward P/E. Not only does The Honest Company trade at a premium to companies in the consumer staples space, but this multiple is also high for its top-line growth.

There are stocks out there featuring similar valuation multiples with better fundamentals. We prefer to invest in those.

3. The Honest Company (HNST) Research Report: Q4 CY2025 Update

Personal care company The Honest Company (NASDAQ:HNST) met Wall Street’s revenue expectations in Q4 CY2025, but sales fell by 11.8% year on year to $88.04 million. Its GAAP loss of $0.21 per share was significantly below analysts’ consensus estimates.

The Honest Company (HNST) Q4 CY2025 Highlights:

- Revenue: $88.04 million vs analyst estimates of $88.19 million (11.8% year-on-year decline, in line)

- EPS (GAAP): -$0.21 vs analyst estimates of $0.02 (significant miss)

- Adjusted EBITDA: $3.75 million vs analyst estimates of $3.91 million (4.3% margin, relatively in line)

- EBITDA guidance for the upcoming financial year 2026 is $21.5 million at the midpoint, above analyst estimates of $20.87 million

- Operating Margin: -27.5%, down from -1% in the same quarter last year

- Free Cash Flow was $18.06 million, up from -$17.17 million in the same quarter last year

- Market Capitalization: $252.6 million

Company Overview

Co-founded by actress Jessica Alba, The Honest Company (NASDAQ:HNST) sells diapers and wipes, skin care products, and household cleaning products.

Initially conceived as a response to the lack of eco-friendly products for children, the company's first products included diapers without chemicals and biodegradable wipes, among other products. Since then, The Honest Company's growth has largely been through organic (rather than through acquisition) expansion of its existing product portfolio.

Today, The Honest Company sells not only baby products but also moisturizers and creams, cosmetics, and home cleaning supplies, for example. The unifying theme continues to be safe and sustainable products free of harmful chemicals. As such, the core customer consists of parents and individuals who care about what goes on and in their bodies as well as how their consumption habits impact the environment. These Honest Company loyalists tend to be middle to higher-income and educated.

The Honest Company's products can be found in a variety of retail channels, including major brick-and-mortar stores such as Target (NYSE:TGT), Walmart (NYSE:WMT), and Whole Foods (owned by Amazon, NASDAQ:AMZN). Their presence in these well-established retailers has contributed to their widespread accessibility.

4. Personal Care

While personal care products products may seem more discretionary than food, consumers tend to maintain or even boost their spending on the category during tough times. This phenomenon is known as "the lipstick effect" by economists, which states that consumers still want some semblance of affordable luxuries like beauty and wellness when the economy is sputtering. Consumer tastes are constantly changing, and personal care companies are currently responding to the public’s increased desire for ethically produced goods by featuring natural ingredients in their products.

Competitors in the personal care products market that are increasingly their focus on natural and eco-friendly products include Procter & Gamble (NYSE:PG), Kimberly-Clark (NYSE:KMB), and private companies such as Seventh Generation and Babyganics .

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

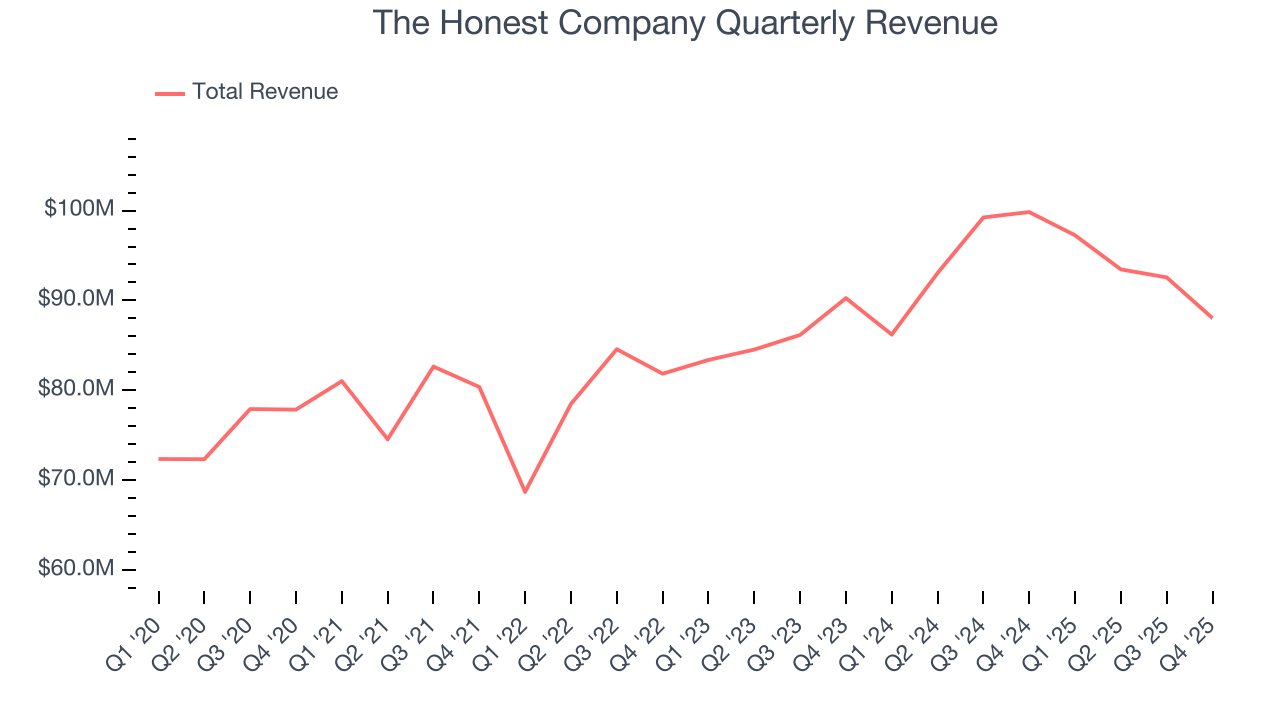

With $371.3 million in revenue over the past 12 months, The Honest Company is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

As you can see below, The Honest Company’s sales grew at a mediocre 5.8% compounded annual growth rate over the last three years. This shows it couldn’t generate demand in any major way and is a tough starting point for our analysis.

This quarter, The Honest Company reported a rather uninspiring 11.8% year-on-year revenue decline to $88.04 million of revenue, in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to decline by 7.3% over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and suggests its products will face some demand challenges.

6. Gross Margin & Pricing Power

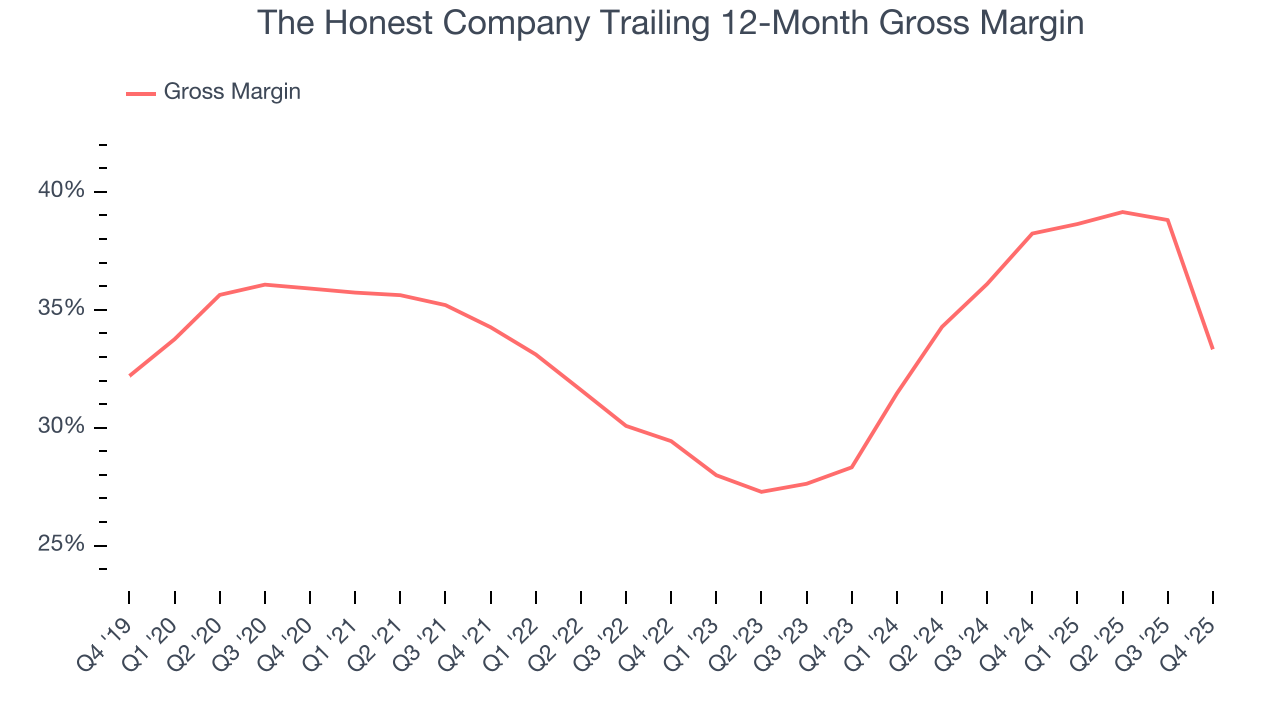

The Honest Company’s unit economics are higher than the typical consumer staples company, giving it the flexibility to invest in areas such as marketing and talent to reach more consumers. As you can see below, it averaged a decent 35.8% gross margin over the last two years. Said differently, The Honest Company paid its suppliers $64.20 for every $100 in revenue.

The Honest Company’s gross profit margin came in at 15.7% this quarter, down 23.1 percentage points year on year. The Honest Company’s full-year margin has also been trending down over the past 12 months, decreasing by 4.9 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs (such as raw materials and manufacturing expenses).

7. Operating Margin

Operating margin is a key profitability metric because it accounts for all expenses enabling a business to operate smoothly, including marketing and advertising, IT systems, wages, and other administrative costs.

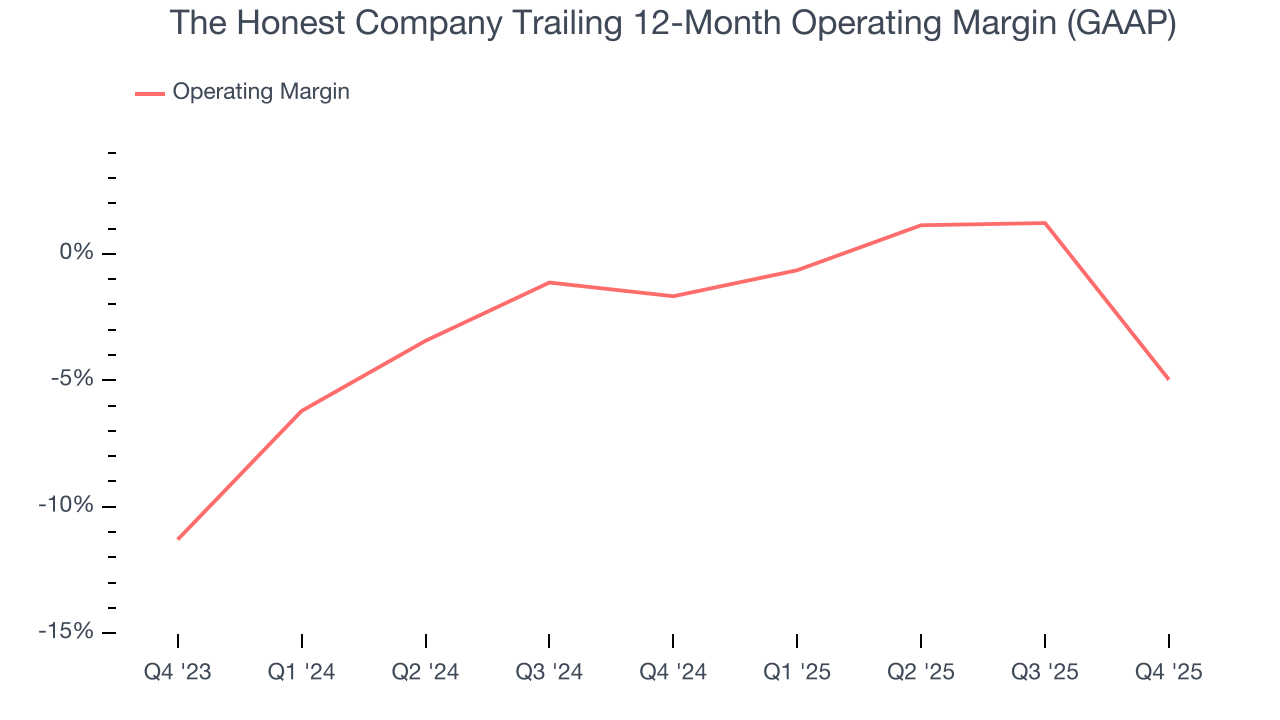

Unprofitable public companies are rare in the defensive consumer staples industry. Unfortunately, The Honest Company was one of them over the last two years as its high expenses contributed to an average operating margin of negative 3.3%.

Analyzing the trend in its profitability, The Honest Company’s operating margin decreased by 3.3 percentage points over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. The Honest Company’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q4, The Honest Company generated a negative 27.5% operating margin. The company's consistent lack of profits raise a flag.

8. Earnings Per Share

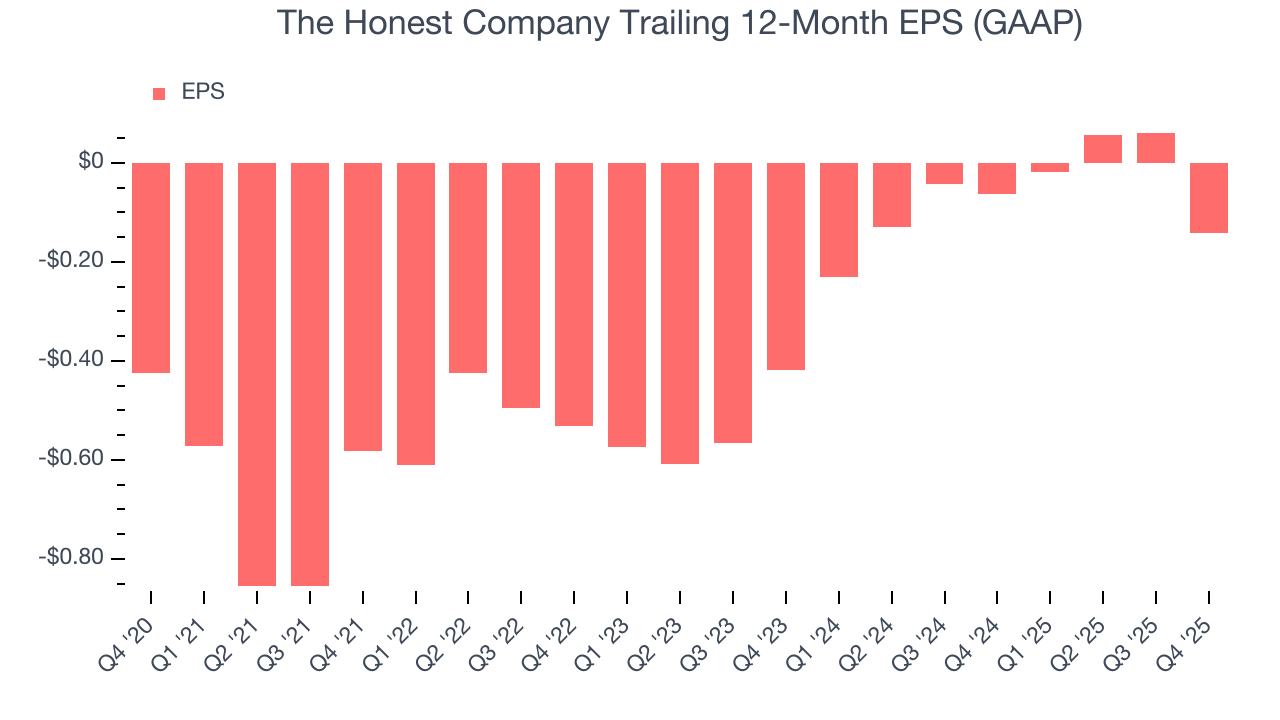

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Although The Honest Company’s full-year earnings are still negative, it reduced its losses and improved its EPS by 35.8% annually over the last three years. The next few quarters will be critical for assessing its long-term profitability.

In Q4, The Honest Company reported EPS of negative $0.21, down from negative $0.01 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast The Honest Company’s full-year EPS of negative $0.14 will flip to positive $0.18.

9. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

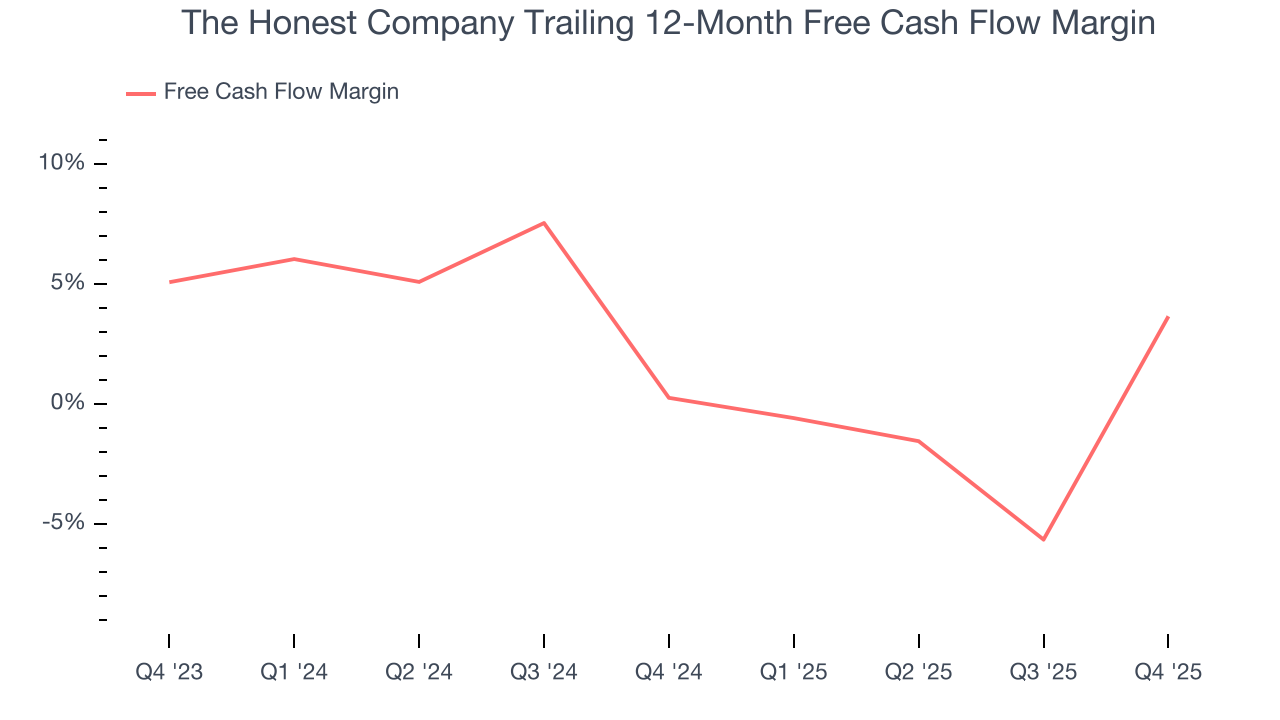

The Honest Company has shown weak cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 2%, subpar for a consumer staples business.

Taking a step back, an encouraging sign is that The Honest Company’s margin expanded by 3.4 percentage points over the last year. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability fell.

The Honest Company’s free cash flow clocked in at $18.06 million in Q4, equivalent to a 20.5% margin. Its cash flow turned positive after being negative in the same quarter last year, building on its favorable historical trend.

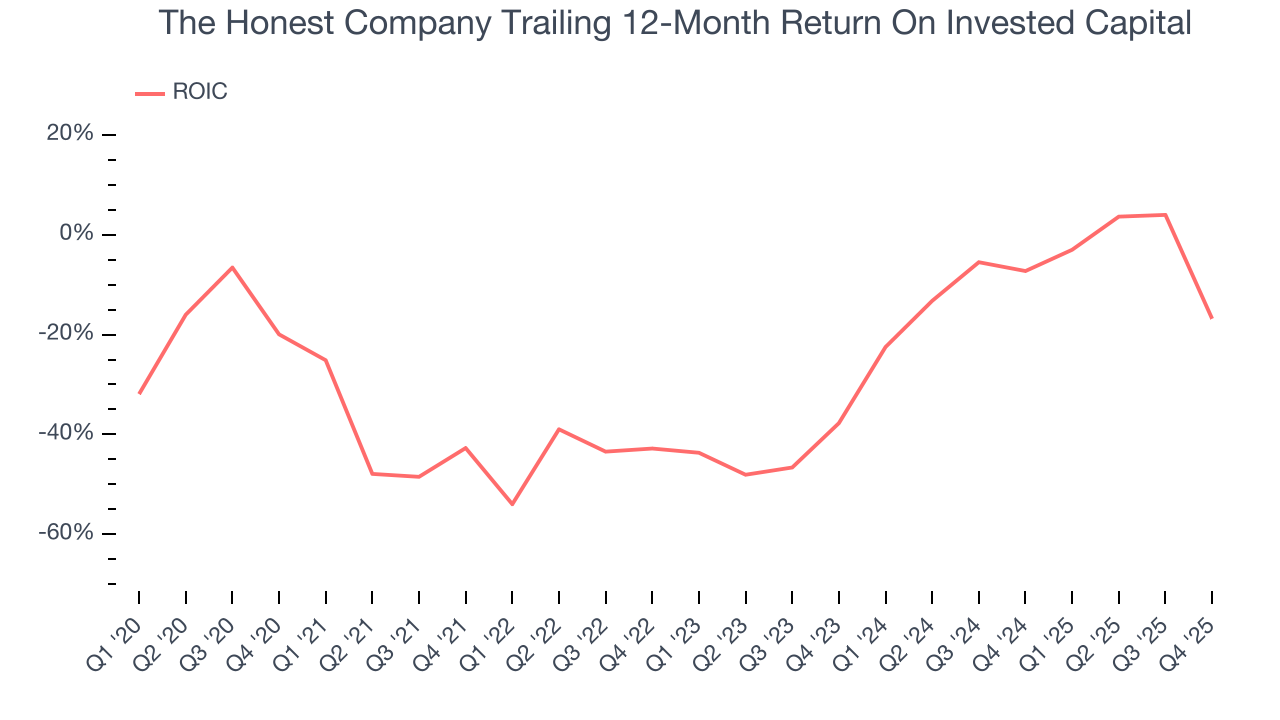

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

The Honest Company’s five-year average ROIC was negative 29.5%, meaning management lost money while trying to expand the business. Its returns were among the worst in the consumer staples sector.

11. Balance Sheet Assessment

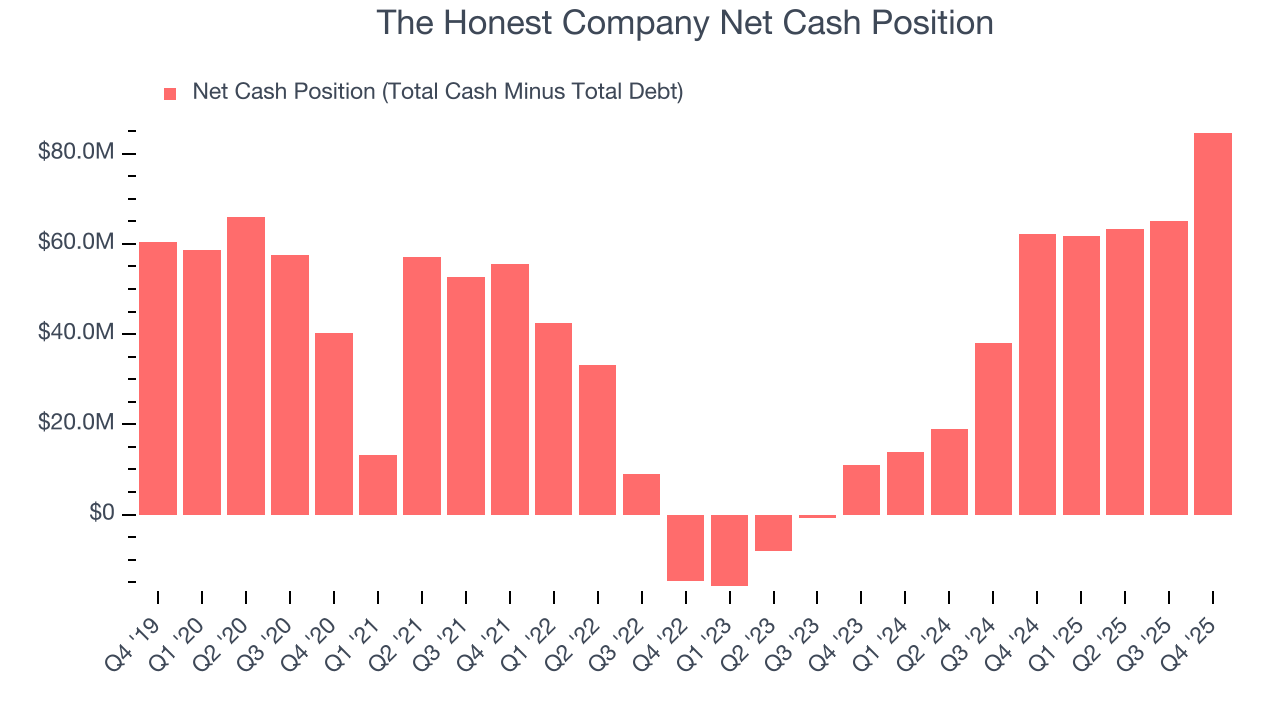

Companies with more cash than debt have lower bankruptcy risk.

The Honest Company is a well-capitalized company with $89.58 million of cash and $4.92 million of debt on its balance sheet. This $84.66 million net cash position is 33.5% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from The Honest Company’s Q4 Results

It was encouraging to see The Honest Company’s full-year EBITDA guidance beat analysts’ expectations. On the other hand, its gross margin missed and its EPS fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 5.1% to $2.20 immediately following the results.

13. Is Now The Time To Buy The Honest Company?

Updated: March 15, 2026 at 10:56 PM EDT

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

The Honest Company doesn’t pass our quality test. For starters, its revenue growth was a little slower over the last three years, and analysts expect its demand to deteriorate over the next 12 months. While its EPS growth over the last three years has been fantastic, the downside is its brand caters to a niche market. On top of that, its relatively low ROIC suggests management has struggled to find compelling investment opportunities.

The Honest Company’s P/E ratio based on the next 12 months is 29.5x. This multiple tells us a lot of good news is priced in - we think there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $3.50 on the company (compared to the current share price of $2.76).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.