Integra LifeSciences (IART)

Integra LifeSciences is up against the odds. Its sales have underperformed and its low returns on capital show it has few growth opportunities.― StockStory Analyst Team

1. News

2. Summary

Why We Think Integra LifeSciences Will Underperform

Founded in 1989 as a pioneer in regenerative medicine technology, Integra LifeSciences (NASDAQ:IART) develops and manufactures medical technologies for neurosurgery, wound care, and surgical reconstruction, including regenerative tissue products and surgical instruments.

- Performance over the past five years shows its incremental sales were much less profitable, as its earnings per share fell by 1.9% annually

- Modest revenue base of $1.64 billion gives it less fixed cost leverage and fewer distribution channels than larger companies

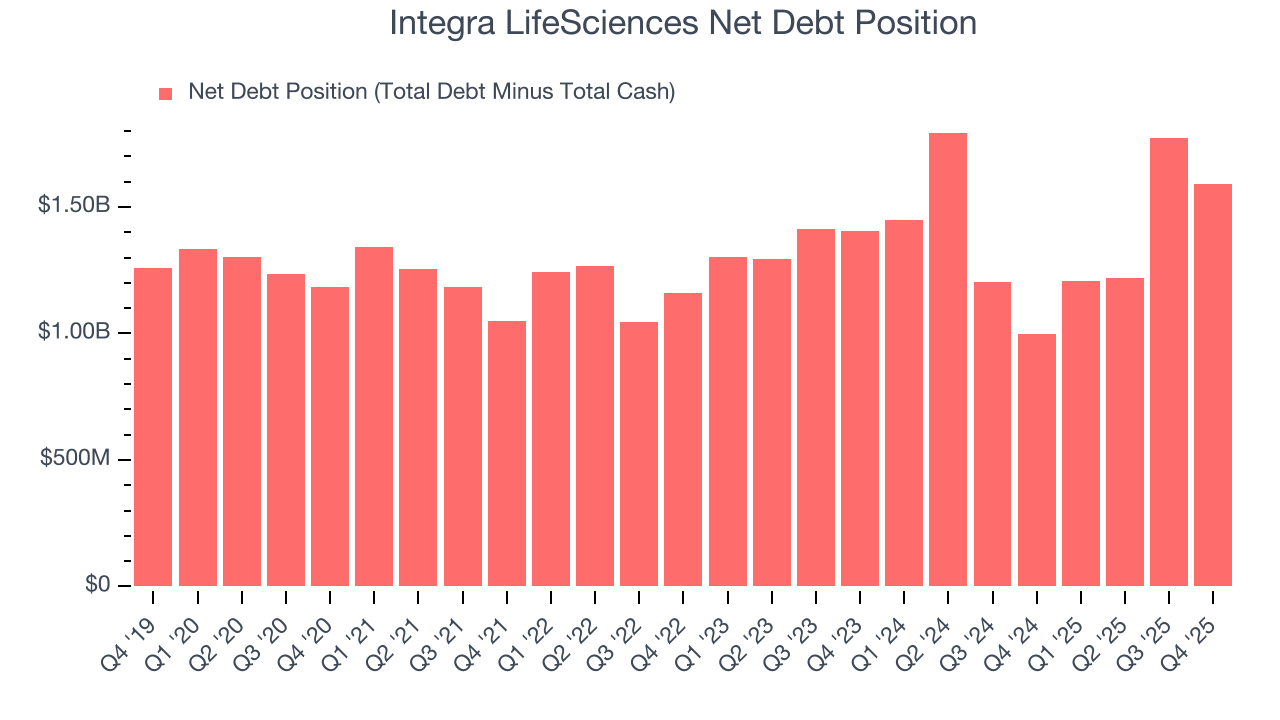

- 6× net-debt-to-EBITDA ratio makes lenders less willing to extend additional capital, potentially necessitating dilutive equity offerings

Integra LifeSciences’s quality doesn’t meet our hurdle. Better stocks can be found in the market.

Why There Are Better Opportunities Than Integra LifeSciences

Integra LifeSciences is trading at $9.28 per share, or 3.9x forward P/E. This is a cheap valuation multiple, but for good reason. You get what you pay for.

Our advice is to pay up for elite businesses whose advantages are tailwinds to earnings growth. Don’t get sucked into lower-quality businesses just because they seem like bargains. These mediocre businesses often never achieve a higher multiple as hoped, a phenomenon known as a “value trap”.

3. Integra LifeSciences (IART) Research Report: Q4 CY2025 Update

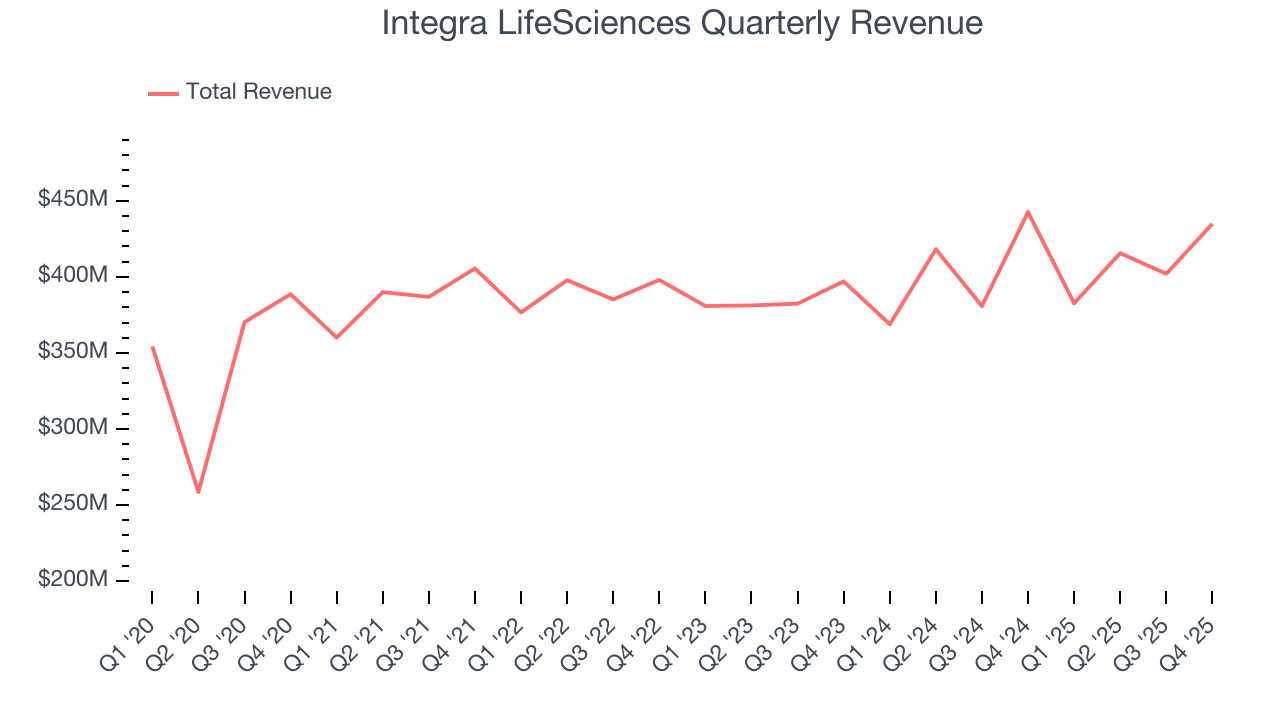

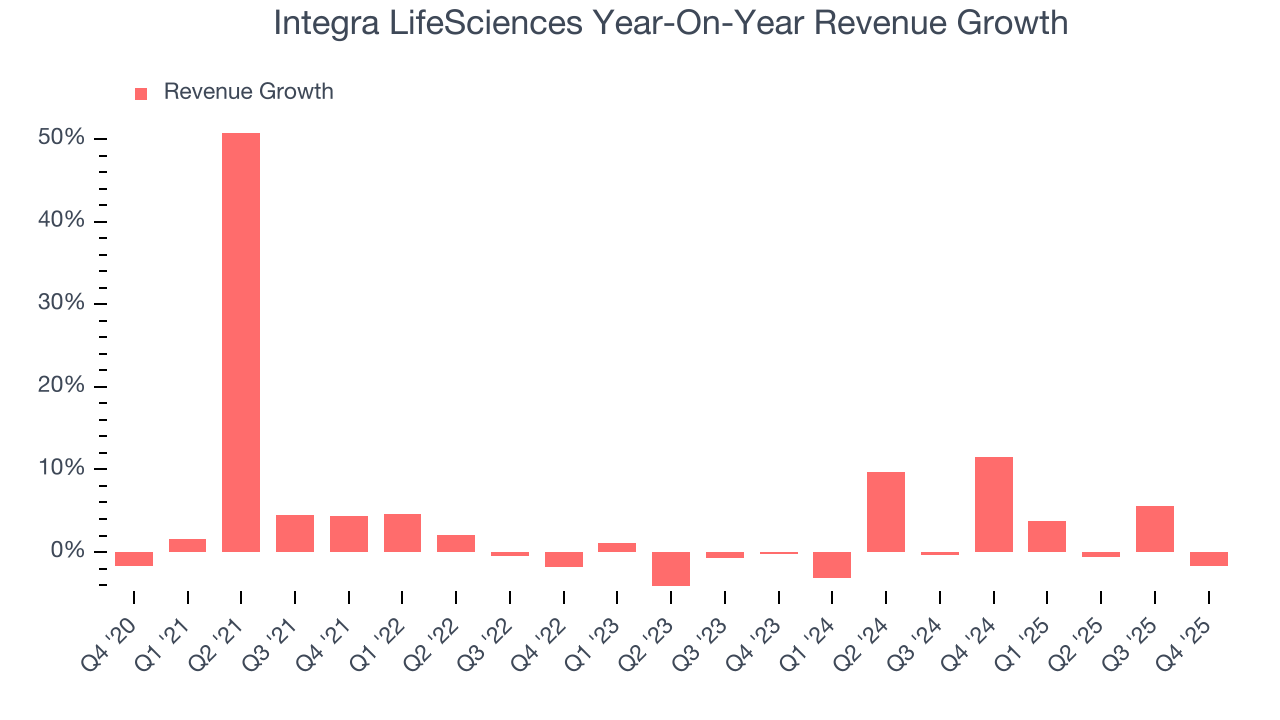

Medical device company Integra LifeSciences (NASDAQ:IART) beat Wall Street’s revenue expectations in Q4 CY2025, but sales fell by 1.7% year on year to $434.9 million. On the other hand, next quarter’s revenue guidance of $382.5 million was less impressive, coming in 2.8% below analysts’ estimates. Its non-GAAP profit of $0.83 per share was 3.7% above analysts’ consensus estimates.

Integra LifeSciences (IART) Q4 CY2025 Highlights:

- Revenue: $434.9 million vs analyst estimates of $430.5 million (1.7% year-on-year decline, 1% beat)

- Adjusted EPS: $0.83 vs analyst estimates of $0.80 (3.7% beat)

- Adjusted EBITDA: $104.2 million vs analyst estimates of $101 million (24% margin, 3.2% beat)

- Revenue Guidance for Q1 CY2026 is $382.5 million at the midpoint, below analyst estimates of $393.4 million

- Adjusted EPS guidance for the upcoming financial year 2026 is $2.35 at the midpoint, in line with analyst estimates

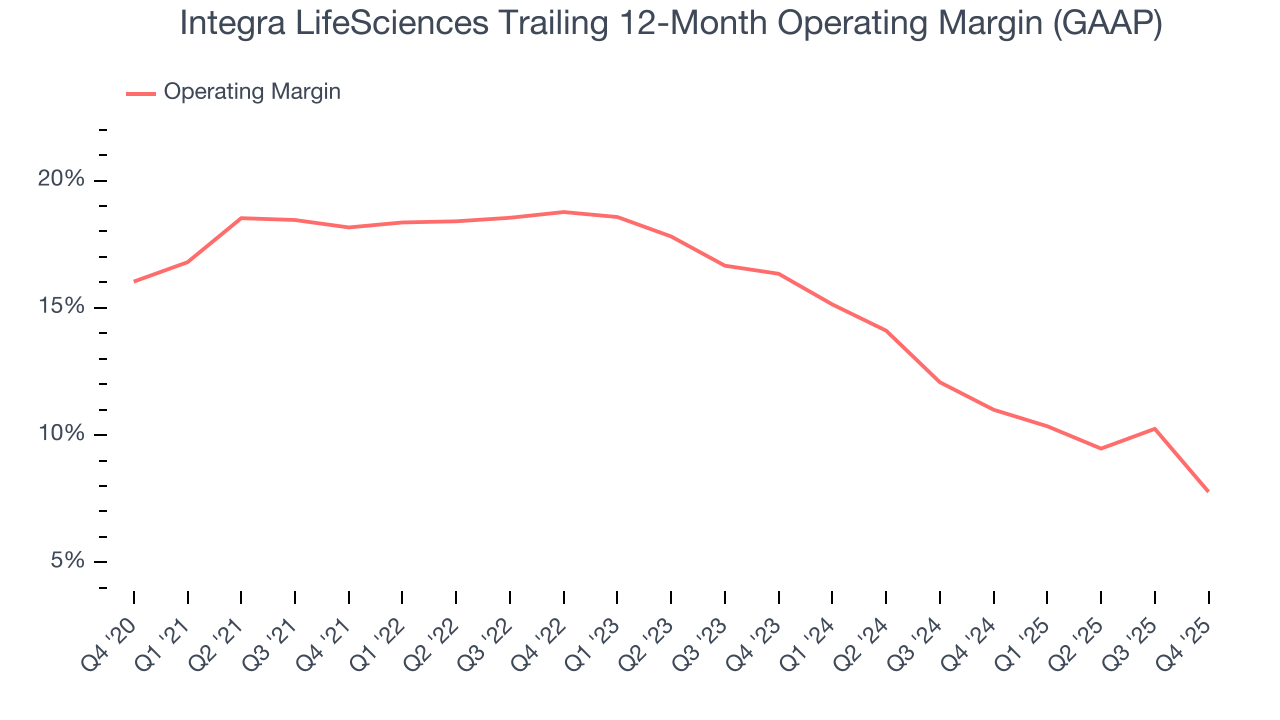

- Operating Margin: 5.3%, down from 14.5% in the same quarter last year

- Free Cash Flow was -$5.4 million, down from $21.14 million in the same quarter last year

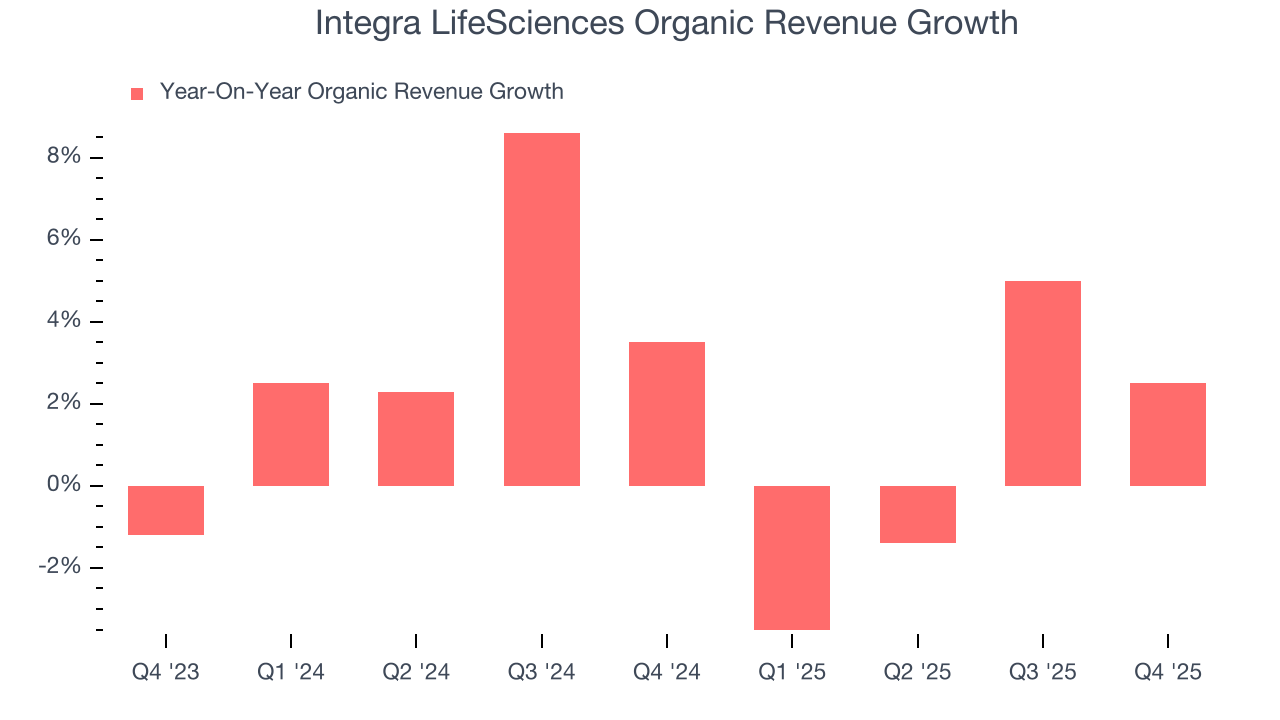

- Organic Revenue rose 2.5% year on year (beat)

- Market Capitalization: $902.8 million

Company Overview

Founded in 1989 as a pioneer in regenerative medicine technology, Integra LifeSciences (NASDAQ:IART) develops and manufactures medical technologies for neurosurgery, wound care, and surgical reconstruction, including regenerative tissue products and surgical instruments.

Integra operates through two main business segments: Codman Specialty Surgical (CSS) and Tissue Technologies (TT). The CSS segment provides neurosurgical technologies and instrumentation used in treating brain tumors, traumatic brain injuries, and other neurological conditions. Its product portfolio includes dural repair materials, ultrasonic tissue ablation devices, intracranial pressure monitoring systems, and cranial stabilization equipment. These technologies serve neurosurgeons in operating rooms and neuro-critical care units worldwide.

The Tissue Technologies segment focuses on regenerative products for complex wound surgery, surgical reconstruction, and peripheral nerve repair. Integra has developed multiple regenerative technology platforms using materials like bovine collagen, human amniotic tissue, and resorbable synthetic mesh. For example, a burn surgeon might use Integra Dermal Regeneration Template to provide a scaffold for new skin growth in severe burn patients, while a plastic surgeon could use SurgiMend for breast reconstruction following mastectomy.

The company manufactures its products in facilities across the United States, Puerto Rico, and Europe, while maintaining a global commercial presence. Integra sells its technologies through direct sales forces, distributors, and strategic partnerships to hospitals, integrated health networks, and surgery centers in more than 130 countries.

Beyond product sales, Integra invests significantly in research and development to enhance existing technologies and create new solutions. The company's innovation strategy includes both internal development and strategic acquisitions to expand its technological capabilities, such as its acquisition of Rebound Therapeutics, which added minimally invasive surgical technologies to its portfolio.

Integra generates revenue through direct product sales to healthcare providers and through private-label arrangements with other medical technology companies that incorporate Integra's regenerative and wound care technologies into their own product lines.

4. Surgical Equipment & Consumables - Specialty

The surgical equipment and consumables industry provides tools, devices, and disposable products essential for surgeries and medical procedures. These companies therefore benefit from relatively consistent demand, driven by the ongoing need for medical interventions, recurring revenue from consumables, and long-term contracts with hospitals and healthcare providers. However, the high costs of R&D and regulatory compliance, coupled with intense competition and pricing pressures from cost-conscious customers, can constrain profitability. Over the next few years, tailwinds include aging populations, which tend to need surgical interventions at higher rates. The increasing integration of AI and robotics into surgical procedures could also create opportunities for differentiation and innovation. However, the industry faces headwinds including potential supply chain vulnerabilities, evolving regulatory requirements, and more widespread efforts to make healthcare less costly.

Integra LifeSciences competes with several major medical technology companies, including Medtronic (NYSE:MDT), Stryker Corporation (NYSE:SYK), and Steris PLC (NYSE:STE) in its neurosurgical and surgical instrument markets. In the regenerative medicine and wound care segments, key competitors include Smith & Nephew (NYSE:SNN), Organogenesis (NASDAQ:ORGO), MiMedx Group (NASDAQ:MDXG), and Axogen (NASDAQ:AXGN).

5. Revenue Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With just $1.64 billion in revenue over the past 12 months, Integra LifeSciences is a small company in an industry where scale matters. This makes it difficult to build trust with customers because healthcare is heavily regulated, complex, and resource-intensive.

6. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Integra LifeSciences grew its sales at a tepid 3.6% compounded annual growth rate. This fell short of our benchmark for the healthcare sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Integra LifeSciences’s annualized revenue growth of 3% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

We can dig further into the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Integra LifeSciences’s organic revenue averaged 2.4% year-on-year growth. Because this number aligns with its two-year revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, Integra LifeSciences’s revenue fell by 1.7% year on year to $434.9 million but beat Wall Street’s estimates by 1%. Company management is currently guiding for flat sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 2.4% over the next 12 months, similar to its two-year rate. This projection is underwhelming and implies its newer products and services will not accelerate its top-line performance yet.

7. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Integra LifeSciences has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 14.3%, higher than the broader healthcare sector.

Looking at the trend in its profitability, Integra LifeSciences’s operating margin decreased by 10.4 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 8.6 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

This quarter, Integra LifeSciences generated an operating margin profit margin of 5.3%, down 9.2 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

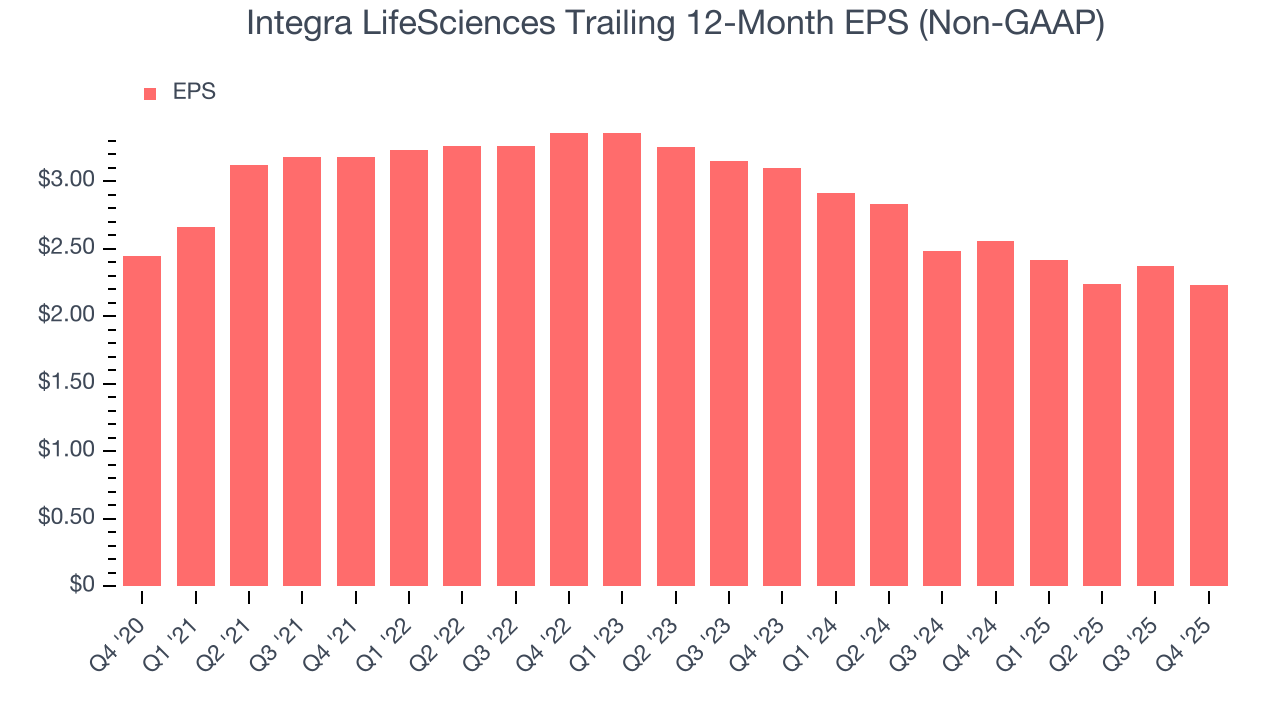

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Integra LifeSciences, its EPS declined by 1.9% annually over the last five years while its revenue grew by 3.6%. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

We can take a deeper look into Integra LifeSciences’s earnings to better understand the drivers of its performance. As we mentioned earlier, Integra LifeSciences’s operating margin declined by 10.4 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, Integra LifeSciences reported adjusted EPS of $0.83, down from $0.97 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 3.7%. Over the next 12 months, Wall Street expects Integra LifeSciences’s full-year EPS of $2.23 to grow 5.8%.

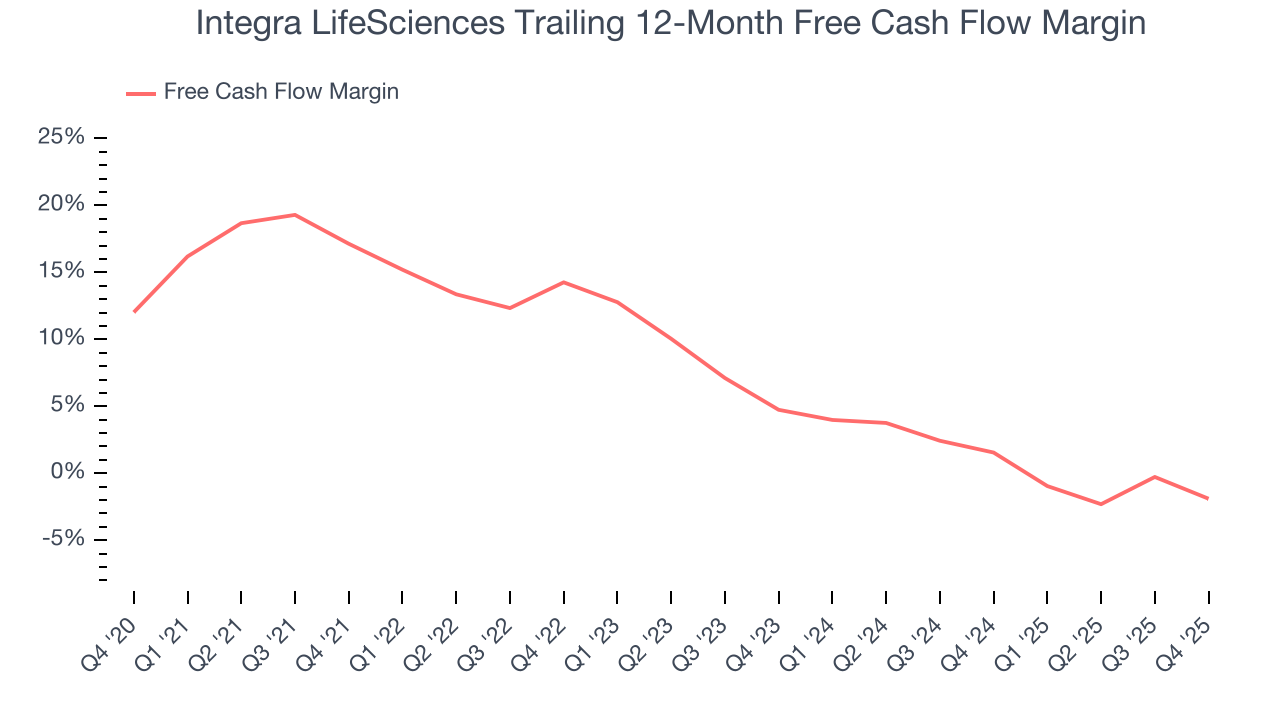

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Integra LifeSciences has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 7% over the last five years, slightly better than the broader healthcare sector.

Taking a step back, we can see that Integra LifeSciences’s margin dropped by 19 percentage points during that time. If its declines continue, it could signal increasing investment needs and capital intensity.

Integra LifeSciences burned through $5.4 million of cash in Q4, equivalent to a negative 1.2% margin. The company’s cash flow turned negative after being positive in the same quarter last year, suggesting its historical struggles have dragged on.

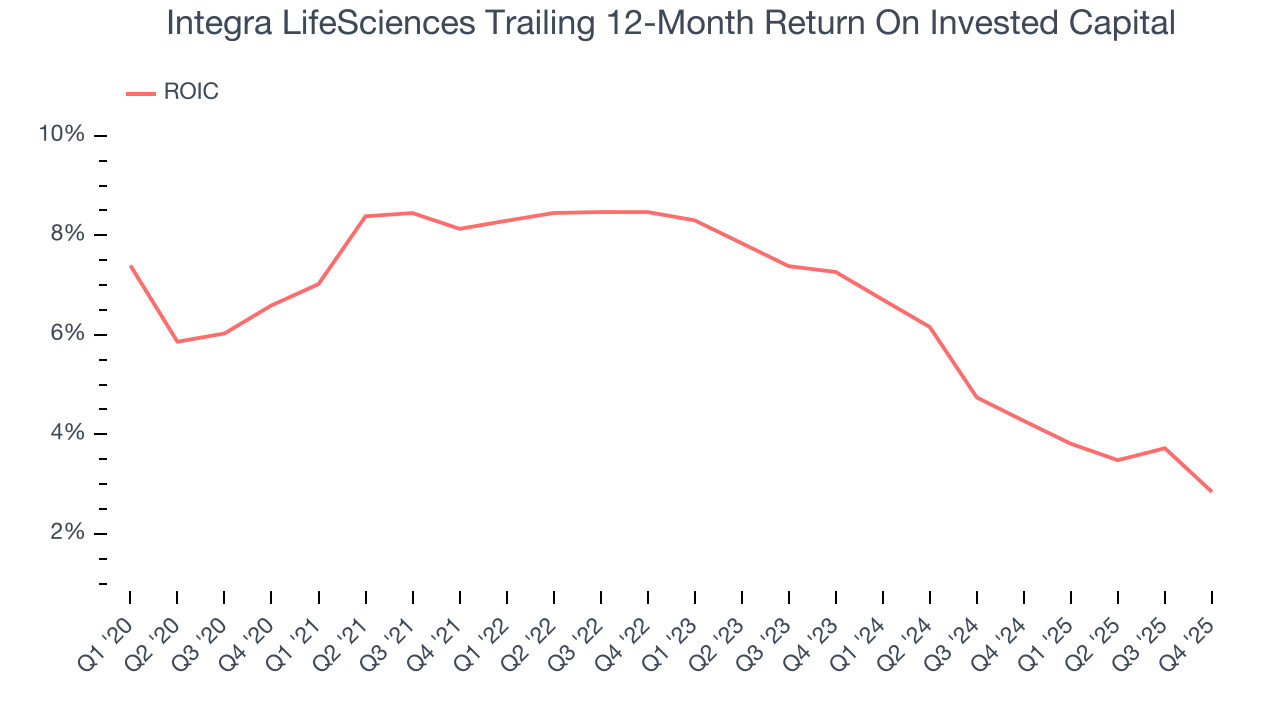

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Integra LifeSciences historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 6.2%, somewhat low compared to the best healthcare companies that consistently pump out 20%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Integra LifeSciences’s ROIC averaged 4.7 percentage point decreases each year over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

11. Balance Sheet Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly. As long-term investors, we aim to avoid companies taking excessive advantage of this instrument because it could lead to insolvency.

Integra LifeSciences’s $1.86 billion of debt exceeds the $263.7 million of cash on its balance sheet. Furthermore, its 5× net-debt-to-EBITDA ratio (based on its EBITDA of $317.5 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. Integra LifeSciences could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope Integra LifeSciences can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

12. Key Takeaways from Integra LifeSciences’s Q4 Results

We were impressed by how significantly Integra LifeSciences blew past analysts’ organic revenue expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. On the other hand, its revenue guidance for next quarter missed and its EPS guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a mixed quarter. The stock remained flat at $11.71 immediately following the results.

13. Is Now The Time To Buy Integra LifeSciences?

Updated: March 16, 2026 at 12:08 AM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Integra LifeSciences.

We cheer for all companies helping people live better, but in the case of Integra LifeSciences, we’ll be cheering from the sidelines. First off, its revenue growth was uninspiring over the last five years, and analysts expect its demand to deteriorate over the next 12 months. While its sturdy operating margins show it has disciplined cost controls, the downside is its cash profitability fell over the last five years. On top of that, its declining EPS over the last five years makes it a less attractive asset to the public markets.

Integra LifeSciences’s P/E ratio based on the next 12 months is 3.9x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $14.88 on the company (compared to the current share price of $9.28).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.