Illumina (ILMN)

We’re cautious of Illumina. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Illumina Will Underperform

Pioneering the ability to read the human genome at unprecedented speed and affordability, Illumina (NASDAQ:ILMN) develops and sells advanced DNA sequencing and microarray technologies that allow researchers and clinicians to analyze genetic variations and functions.

- Underwhelming 0.3% return on capital reflects management’s difficulties in finding profitable growth opportunities

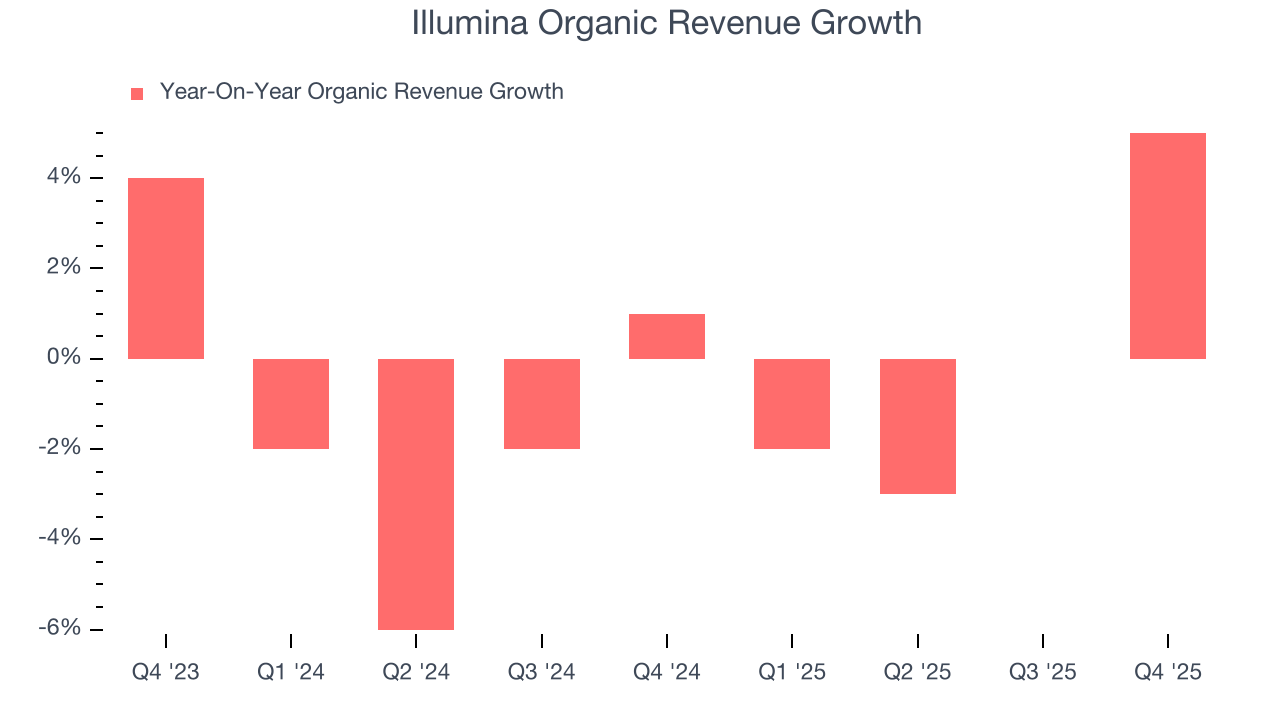

- Organic revenue growth fell short of our benchmarks over the past two years and implies it may need to improve its products, pricing, or go-to-market strategy

- One positive is that its excellent adjusted operating margin highlights the strength of its business model

Illumina is skating on thin ice. There are more profitable opportunities elsewhere.

Why There Are Better Opportunities Than Illumina

Illumina is trading at $125.65 per share, or 24.6x forward P/E. Not only does Illumina trade at a premium to companies in the healthcare space, but this multiple is also high for its top-line growth.

There are stocks out there similarly priced with better business quality. We prefer owning these.

3. Illumina (ILMN) Research Report: Q4 CY2025 Update

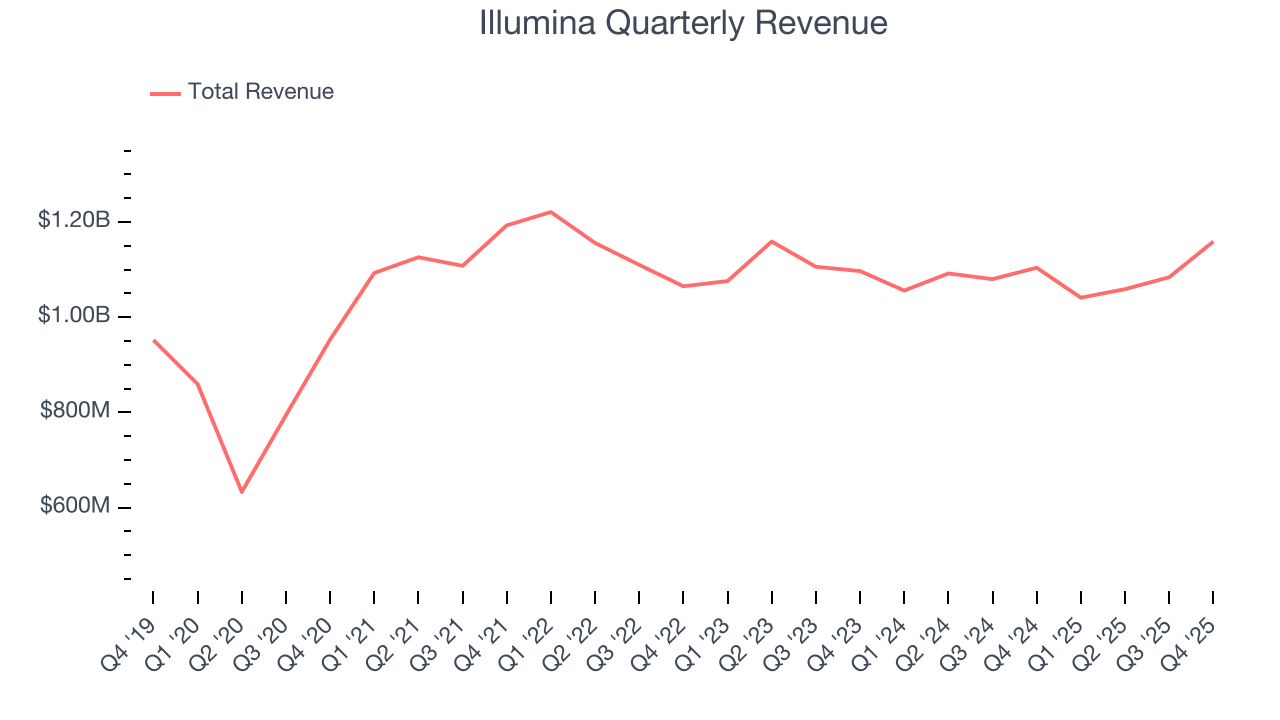

Genomics company Illumina (NASDAQ:ILMN) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 5% year on year to $1.16 billion. The company’s full-year revenue guidance of $4.55 billion at the midpoint came in 3.1% above analysts’ estimates. Its non-GAAP profit of $1.35 per share was 8.3% above analysts’ consensus estimates.

Illumina (ILMN) Q4 CY2025 Highlights:

- Revenue: $1.16 billion vs analyst estimates of $1.12 billion (5% year-on-year growth, 3.2% beat)

- Adjusted EPS: $1.35 vs analyst estimates of $1.25 (8.3% beat)

- Adjusted Operating Income: $275 million vs analyst estimates of $253 million (23.7% margin, 8.7% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $5.13 at the midpoint, beating analyst estimates by 1.1%

- Operating Margin: 17.4%, up from 15.9% in the same quarter last year

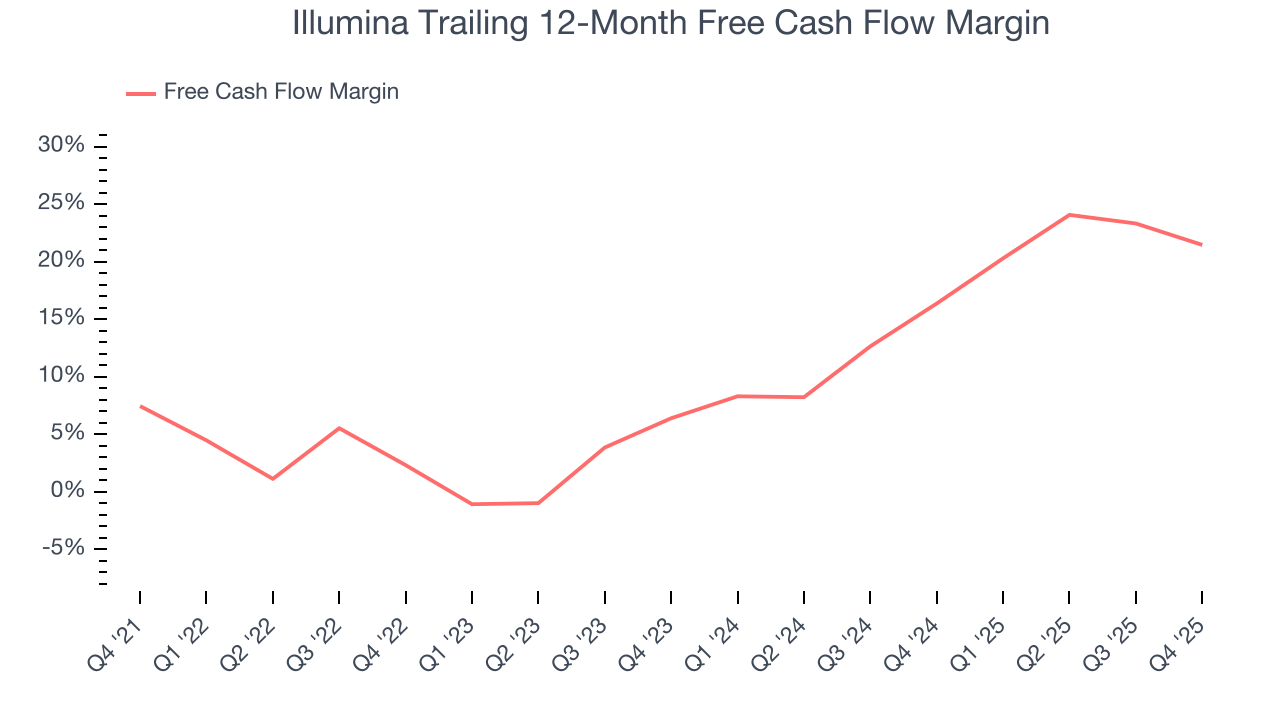

- Free Cash Flow Margin: 23%, down from 30.3% in the same quarter last year

- Organic Revenue rose 5% year on year (beat)

- Market Capitalization: $20.5 billion

Company Overview

Pioneering the ability to read the human genome at unprecedented speed and affordability, Illumina (NASDAQ:ILMN) develops and sells advanced DNA sequencing and microarray technologies that allow researchers and clinicians to analyze genetic variations and functions.

Illumina's technology platforms enable genetic analysis at all levels of complexity, from targeted gene panels to complete whole-genome sequencing. The company's flagship product line includes sequencing instruments like the NovaSeq X Plus, which can sequence a human genome for as little as $200, and the more compact MiSeq systems designed for smaller laboratories. These systems use Illumina's proprietary sequencing by synthesis (SBS) chemistry to accurately read DNA sequences.

Beyond hardware, Illumina provides a comprehensive ecosystem of consumables, software, and services. The consumables include reagents, flow cells, and library preparation kits that are essential for running experiments on their instruments. The company's bioinformatics solutions, such as the BaseSpace Informatics Suite and DRAGEN Bio-IT Platform, help customers manage, analyze, and interpret the massive amounts of data generated by sequencing.

Illumina serves diverse markets including academic research institutions, pharmaceutical companies, biotechnology firms, and clinical laboratories. In research settings, scientists use Illumina's technology to study everything from basic gene function to complex disease mechanisms. Clinically, the technology enables applications like non-invasive prenatal testing (NIPT), which can detect fetal chromosomal abnormalities from a maternal blood sample, and cancer genomics, where tumor DNA is analyzed to guide treatment decisions.

For example, an oncologist might use Illumina's technology to sequence a patient's tumor, identifying specific mutations that could make the cancer susceptible to targeted therapies. Similarly, a research institution might deploy Illumina sequencers to analyze thousands of human genomes as part of a population-wide study to discover genetic factors associated with common diseases.

Illumina generates revenue primarily through instrument sales and the recurring purchase of consumables needed for each sequencing run. The company maintains a global presence with direct sales operations in North America, Europe, Latin America, and the Asia-Pacific region, supplemented by distributors in other markets.

4. Genomics & Sequencing

Genomics and sequencing companies within the life sciences industry provide the technology for increasingly personalized medicine, drug discovery, and disease research. These firms leverage cutting-edge platforms for high-throughput sequencing and genomic analysis, enabling researchers and healthcare providers to better understand genetic underpinnings of diseases. While the industry enjoys high barriers to entry due to proprietary technology and intellectual property, the business model also faces significant R&D costs, reliance on continued innovation, and exposure to shifts in academic, biotech, and clinical research funding. Over the next few years, the subsector is well-positioned to benefit from tailwinds such as increasing adoption of precision medicine, expanded applications for sequencing technologies in areas like oncology and rare disease diagnostics, and growing use of genomic data in drug development. Advances in artificial intelligence could further enhance the speed and accuracy of genomic insights. However, potential headwinds include price sensitivity among research institutions and healthcare systems that are constantly trying to contain and lower costs. Additionally, regulations around data privacy and genomic testing are not yet set in stone, adding uncertainty to the industry.

Illumina's main competitors include Thermo Fisher Scientific (NYSE:TMO) with its Ion Torrent sequencing platform, Pacific Biosciences (NASDAQ:PACB) specializing in long-read sequencing technology, and Oxford Nanopore Technologies (LSE:ONT) known for its portable sequencing devices. The company also faces competition from emerging players like Element Biosciences and BGI Genomics (SHE:300676).

5. Economies of Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $4.34 billion in revenue over the past 12 months, Illumina has decent scale. This is important as it gives the company more leverage in a heavily regulated, competitive environment that is complex and resource-intensive.

6. Revenue Growth

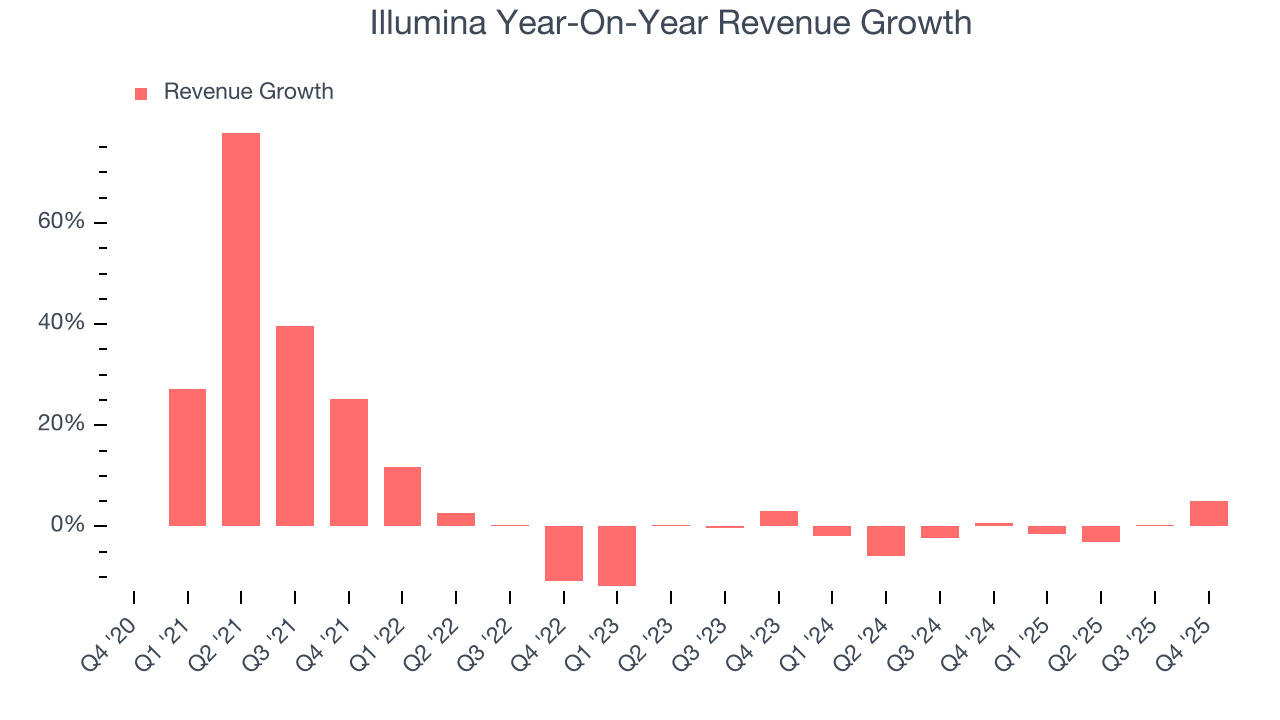

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Regrettably, Illumina’s sales grew at a mediocre 6% compounded annual growth rate over the last five years. This fell short of our benchmark for the healthcare sector and is a tough starting point for our analysis.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Illumina’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 1.1% annually.

We can dig further into the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Illumina’s organic revenue averaged 1.1% year-on-year declines. Because this number aligns with its two-year revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, Illumina reported modest year-on-year revenue growth of 5% but beat Wall Street’s estimates by 3.2%.

Looking ahead, sell-side analysts expect revenue to grow 1.7% over the next 12 months. Although this projection indicates its newer products and services will spur better top-line performance, it is still below average for the sector.

7. Adjusted Operating Margin

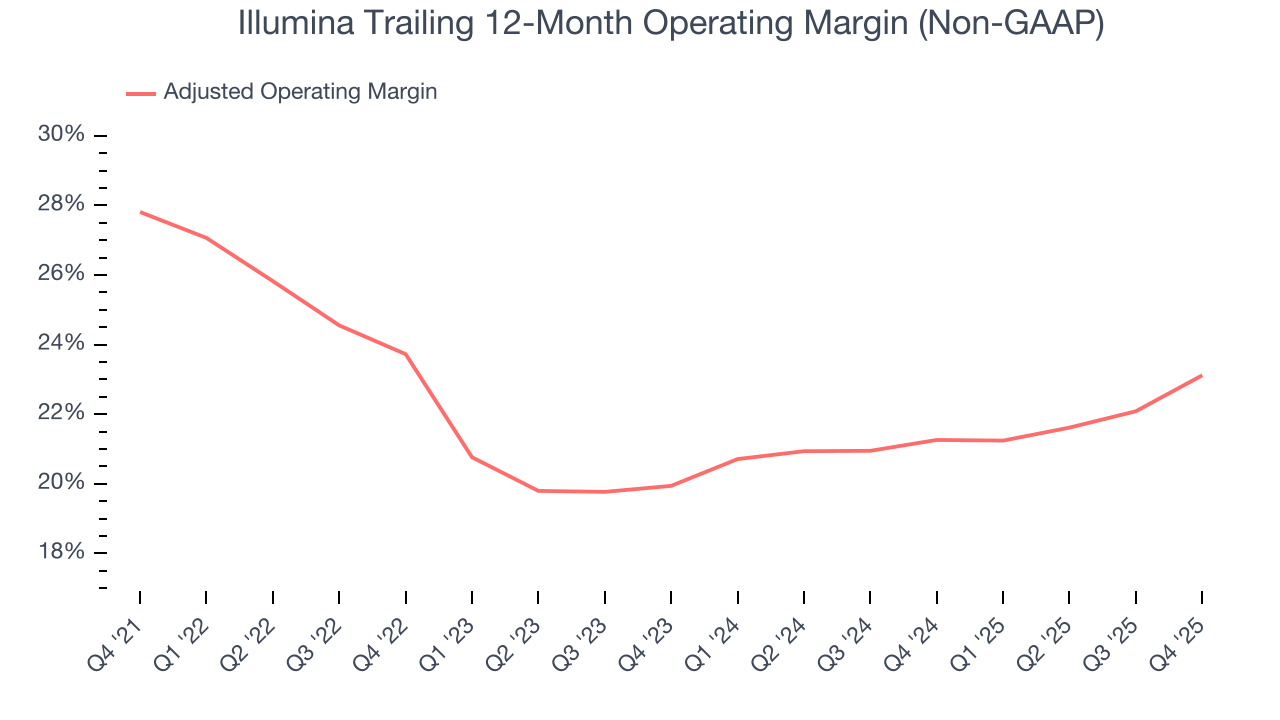

Illumina has been an efficient company over the last five years. It was one of the more profitable businesses in the healthcare sector, boasting an average adjusted operating margin of 23.2%.

Looking at the trend in its profitability, Illumina’s adjusted operating margin decreased by 4.7 percentage points over the last five years, but it rose by 3.2 percentage points on a two-year basis. Still, shareholders will want to see Illumina become more profitable in the future.

In Q4, Illumina generated an adjusted operating margin profit margin of 23.7%, up 4 percentage points year on year. This increase was a welcome development and shows it was more efficient.

8. Earnings Per Share

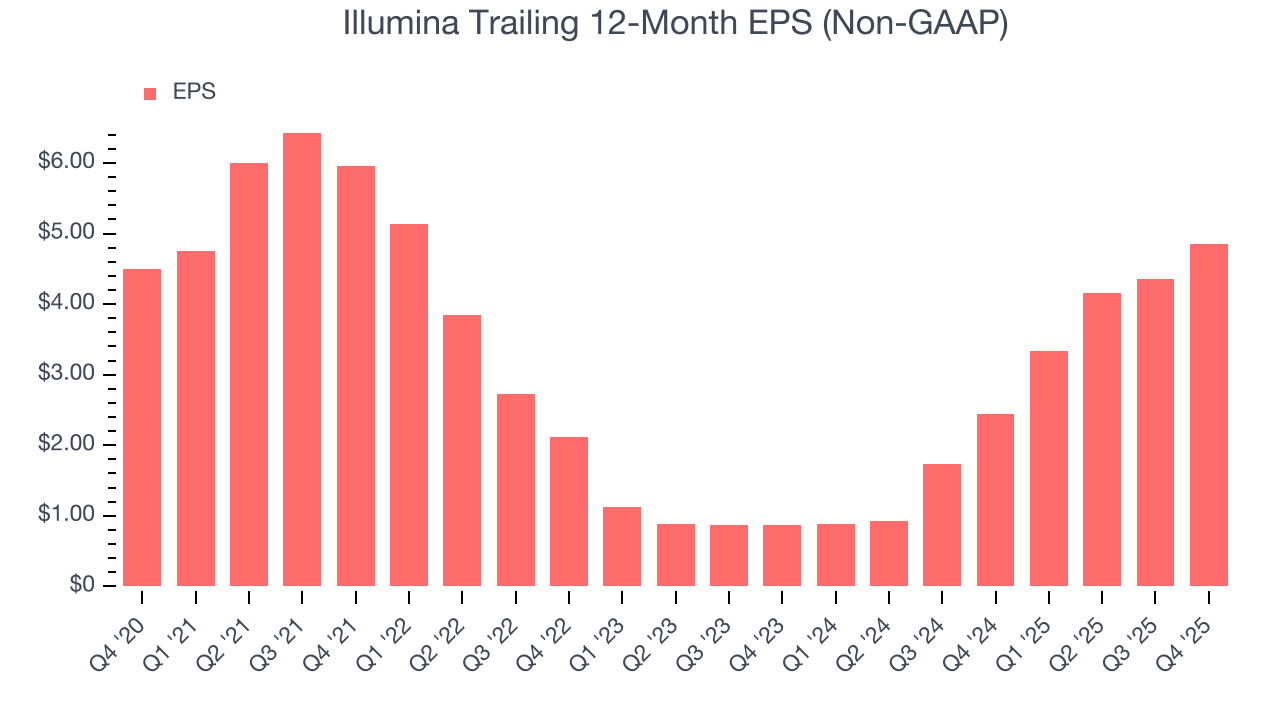

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Illumina’s EPS grew at an unimpressive 1.5% compounded annual growth rate over the last five years, lower than its 6% annualized revenue growth. However, its adjusted operating margin actually improved during this time, telling us that non-fundamental factors such as interest expenses and taxes affected its ultimate earnings.

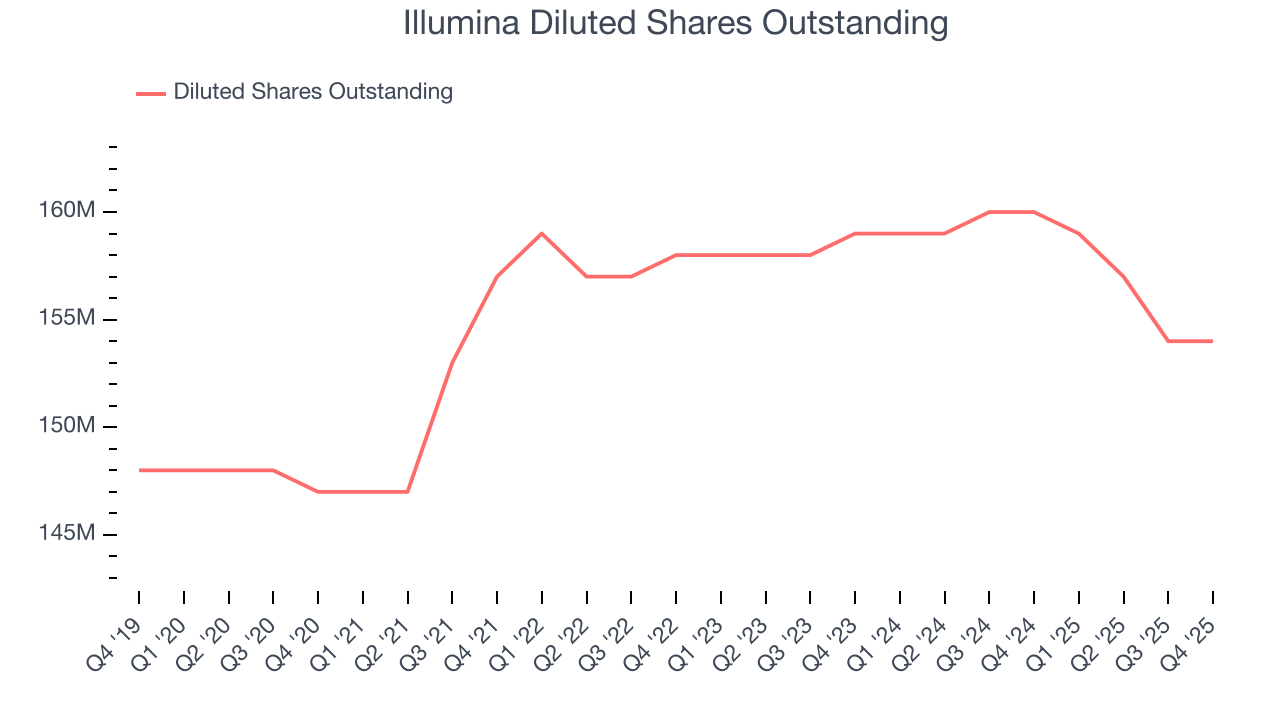

Diving into the nuances of Illumina’s earnings can give us a better understanding of its performance. As we mentioned earlier, Illumina’s adjusted operating margin expanded this quarter but declined by 4.7 percentage points over the last five years. Its share count also grew by 4.8%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

In Q4, Illumina reported adjusted EPS of $1.35, up from $0.86 in the same quarter last year. This print beat analysts’ estimates by 9.7%. Over the next 12 months, Wall Street expects Illumina’s full-year EPS of $4.85 to grow 4.5%.

9. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Illumina has shown impressive cash profitability, giving it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 10.7% over the last five years, better than the broader healthcare sector.

Taking a step back, we can see that Illumina’s margin expanded by 14 percentage points during that time. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability fell.

Illumina’s free cash flow clocked in at $267 million in Q4, equivalent to a 23% margin. The company’s cash profitability regressed as it was 7.3 percentage points lower than in the same quarter last year, but it’s still above its five-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, leading to short-term swings. Long-term trends trump temporary fluctuations.

10. Return on Invested Capital (ROIC)

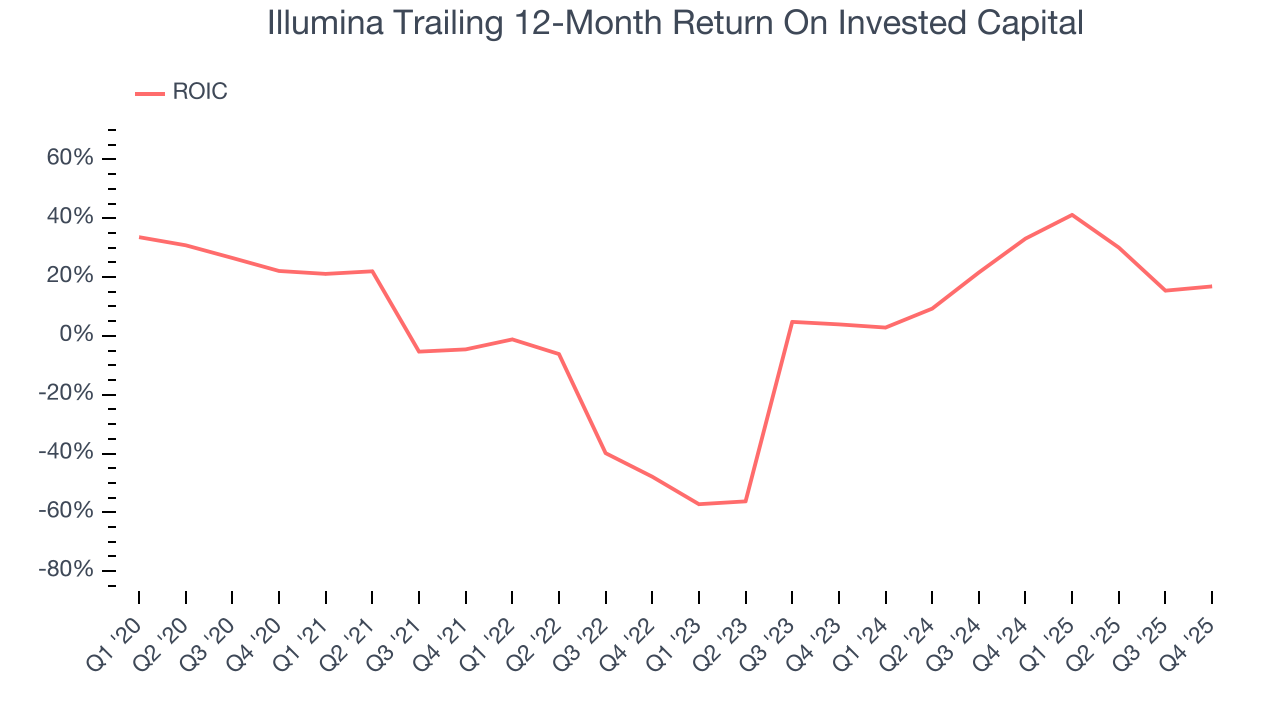

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Illumina historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 0.3%, lower than the typical cost of capital (how much it costs to raise money) for healthcare companies.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Illumina’s ROIC has increased significantly. This is a good sign, and we hope the company can continue improving.

11. Balance Sheet Assessment

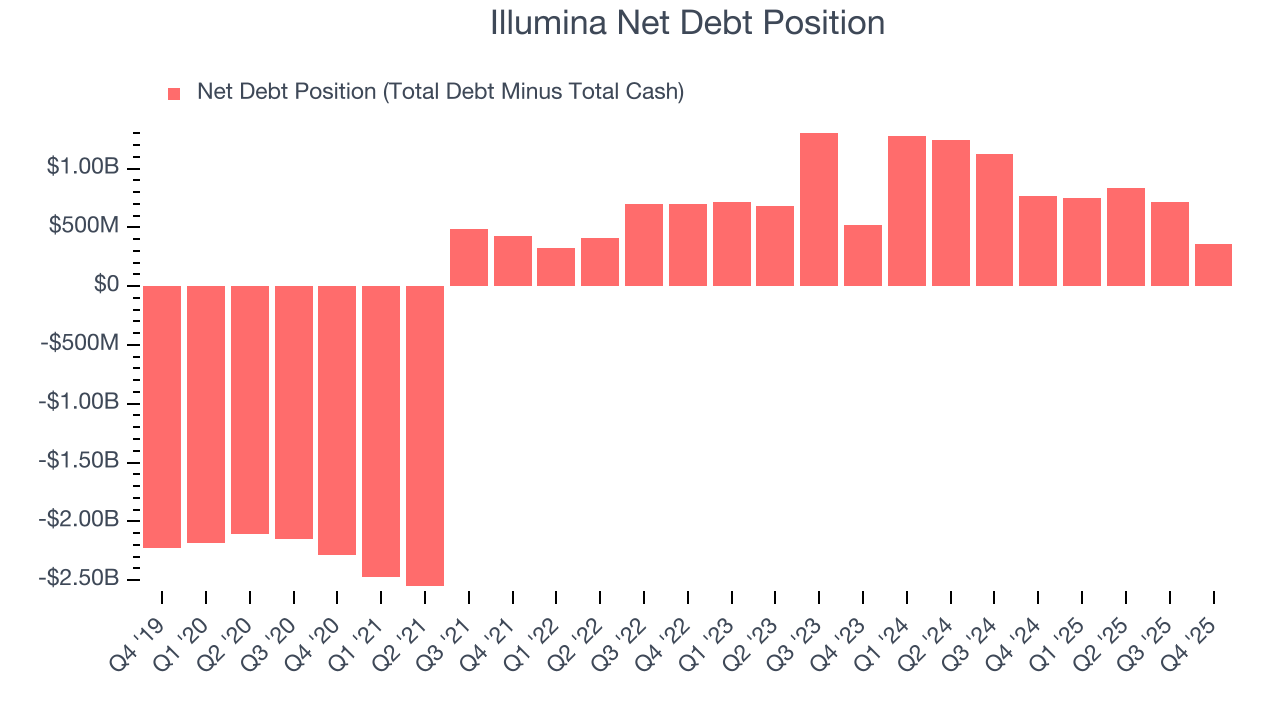

Illumina reported $1.63 billion of cash and $1.99 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $1.22 billion of EBITDA over the last 12 months, we view Illumina’s 0.3× net-debt-to-EBITDA ratio as safe. We also see its $45 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Illumina’s Q4 Results

We were impressed by Illumina’s optimistic full-year revenue guidance, which blew past analysts’ expectations. We were also glad its organic revenue outperformed Wall Street’s estimates. Zooming out, we think this was a solid print. Investors were likely hoping for more, and shares traded down 1.4% to $131.67 immediately following the results.

13. Is Now The Time To Buy Illumina?

Updated: March 26, 2026 at 12:36 AM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Illumina.

Illumina’s business quality ultimately falls short of our standards. To begin with, its revenue growth was mediocre over the last five years, and analysts expect its demand to deteriorate over the next 12 months. While its rising cash profitability gives it more optionality, the downside is its relatively low ROIC suggests management has struggled to find compelling investment opportunities. On top of that, its organic revenue declined.

Illumina’s P/E ratio based on the next 12 months is 24.6x. Beauty is in the eye of the beholder, but we don’t really see a big opportunity at the moment. We're pretty confident there are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $136.11 on the company (compared to the current share price of $125.65).