Keurig Dr Pepper (KDP)

Keurig Dr Pepper is interesting. Although its sales growth has been weak, its profitability gives it the flexibility to ride out cycles.― StockStory Analyst Team

1. News

2. Summary

Why Keurig Dr Pepper Is Interesting

Born out of a 2018 merger between Keurig Green Mountain and Dr Pepper Snapple, Keurig Dr Pepper (NASDAQ:KDP) is a consumer staples powerhouse boasting a portfolio of beverages including sodas, coffees, and juices.

- Exciting sales outlook for the upcoming 12 months calls for 57.5% growth, an acceleration from its three-year trend

- Products command premium prices and result in a top-tier gross margin of 54.9%

- One risk is its below-average returns on capital indicate management struggled to find compelling investment opportunities

Keurig Dr Pepper shows some signs of a high-quality business. If you’re a believer, the valuation seems reasonable.

Why Is Now The Time To Buy Keurig Dr Pepper?

Keurig Dr Pepper is trading at $27.47 per share, or 11.8x forward P/E. Keurig Dr Pepper’s current multiple might be below that of most consumer staples peers, but we think this valuation is warranted after considering its business quality.

If you think the market is undervaluing the company, now could be a good time to build a position.

3. Keurig Dr Pepper (KDP) Research Report: Q4 CY2025 Update

Beverage company Keurig Dr Pepper (NASDAQ:KDP) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 10.5% year on year to $4.50 billion. Its non-GAAP profit of $0.60 per share was 1.9% above analysts’ consensus estimates.

Keurig Dr Pepper (KDP) Q4 CY2025 Highlights:

- Revenue: $4.50 billion vs analyst estimates of $4.36 billion (10.5% year-on-year growth, 3.1% beat)

- Adjusted EPS: $0.60 vs analyst estimates of $0.59 (1.9% beat)

- Operating Margin: 19.6%, up from 1.5% in the same quarter last year

- Free Cash Flow Margin: 12.2%, down from 16.9% in the same quarter last year

- Sales Volumes rose 4.8% year on year (2.7% in the same quarter last year)

- Market Capitalization: $40.45 billion

Company Overview

Born out of a 2018 merger between Keurig Green Mountain and Dr Pepper Snapple, Keurig Dr Pepper (NASDAQ:KDP) is a consumer staples powerhouse boasting a portfolio of beverages including sodas, coffees, and juices.

The company’s evolution is a complicated web of mergers and acquisitions. We won’t go through all the details, but prior to that 2018 combination, Keurig Green Mountain was born out of Keurig’s revolutionary single-serve technology and Green Mountain’s high-quality beans and roasting. Dr Pepper was a storied soda company that combined with Snapple when their two parent companies (Cadbury Schweppes and Triarc, respectively) merged in 2008.

Today, Keurig Dr Pepper’s portfolio boasts soda brands Dr Pepper, Canada Dry, 7Up, and A&W. Coffee brands include Keurig, Green Mountain, Van Houtte, and Krispy Kreme Coffee. Snapple, Mott’s, and Hawaiian Punch are the featured juice brands. The core customer is therefore quite broad–everyone from adults who need that morning brew to kids with a sweet tooth and everyone in between.

The company's products are widely available in grocery stores, supermarkets, convenience stores, restaurants, vending machines, and movie theaters globally. Keurig Dr Pepper’s scale leads to strong distribution and prominent shelf placement for its products.

4. Beverages, Alcohol, and Tobacco

These companies' performance is influenced by brand strength, marketing strategies, and shifts in consumer preferences. Changing consumption patterns are particularly relevant and can be seen in the rise of cannabis, craft beer, and vaping or the steady decline of soda and cigarettes. Companies that spend on innovation to meet consumers where they are with regards to trends can reap huge demand benefits while those who ignore trends can see stagnant volumes. Finally, with the advent of the social media, the cost of starting a brand from scratch is much lower, meaning that new entrants can chip away at the market shares of established players.

Competitors that offer beverages and snacks include Coca-Cola (NYSE:KO), PepsiCo (NASDAQ:PEP), and Monster Beverage (NASDAQ:MNST).

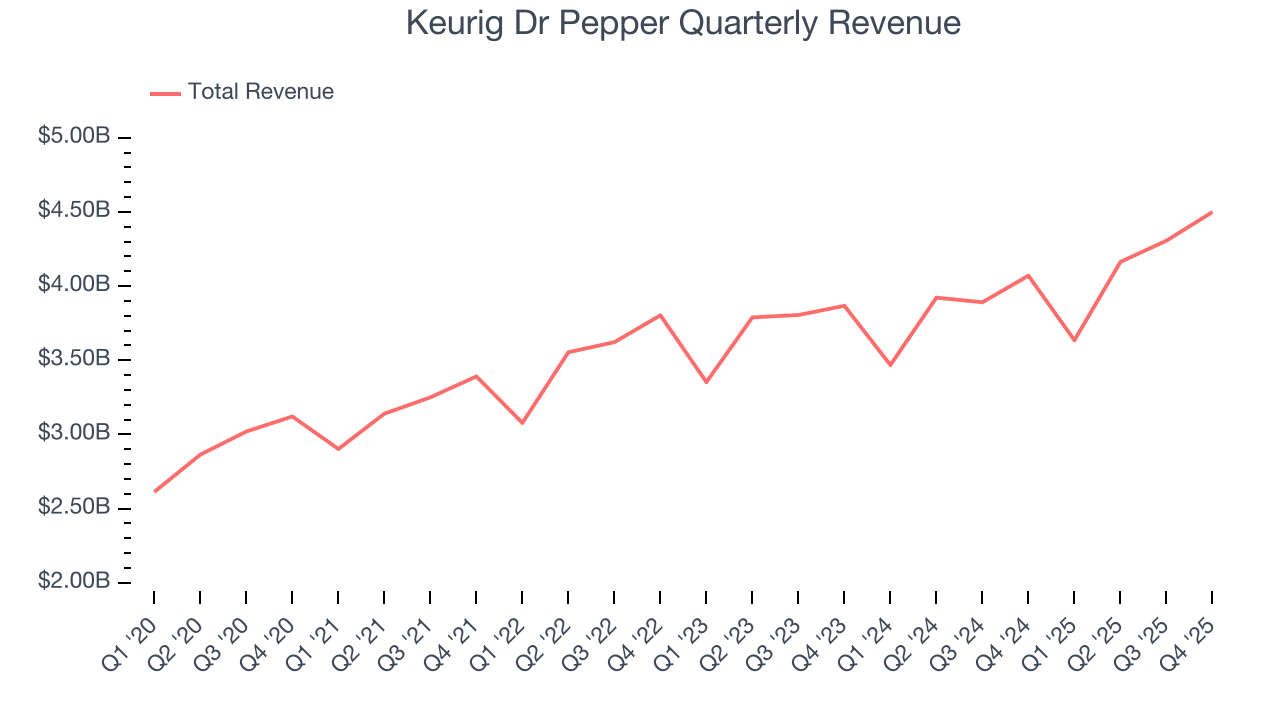

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $16.6 billion in revenue over the past 12 months, Keurig Dr Pepper is larger than most consumer staples companies and benefits from economies of scale, enabling it to gain more leverage on its fixed costs than smaller competitors. Its size also gives it negotiating leverage with distributors, allowing its products to reach more shelves. However, its scale is a double-edged sword because there are only a finite number of major retail partners, placing a ceiling on its growth. To accelerate sales, Keurig Dr Pepper likely needs to optimize its pricing or lean into new products and international expansion.

As you can see below, Keurig Dr Pepper’s 5.7% annualized revenue growth over the last three years was mediocre, but to its credit, consumers bought more of its products.

This quarter, Keurig Dr Pepper reported year-on-year revenue growth of 10.5%, and its $4.50 billion of revenue exceeded Wall Street’s estimates by 3.1%.

Looking ahead, sell-side analysts expect revenue to grow 4.6% over the next 12 months, similar to its three-year rate. This projection is underwhelming and implies its products will face some demand challenges.

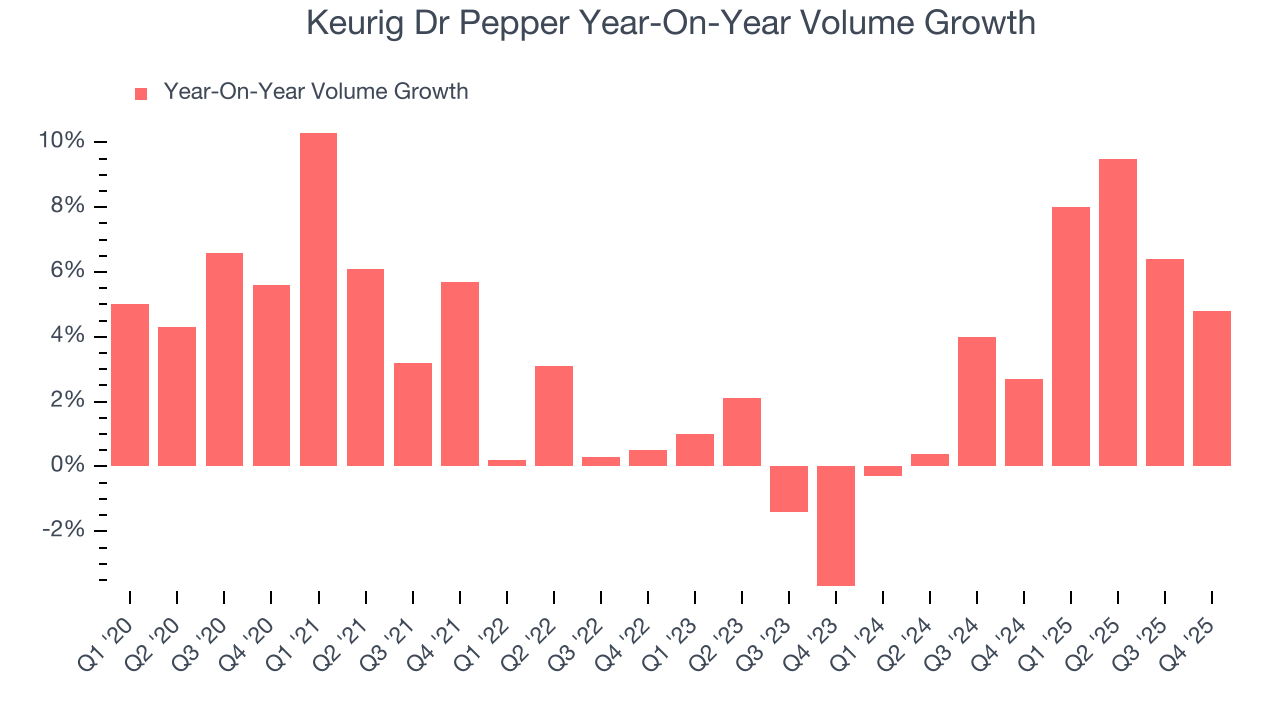

6. Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

Keurig Dr Pepper’s average quarterly volume growth was a robust 4.4% over the last two years. This is good because meaningful volume growth is hard to come by in the stable consumer staples sector.

In Keurig Dr Pepper’s Q4 2025, sales volumes jumped 4.8% year on year. This result was in line with its historical levels.

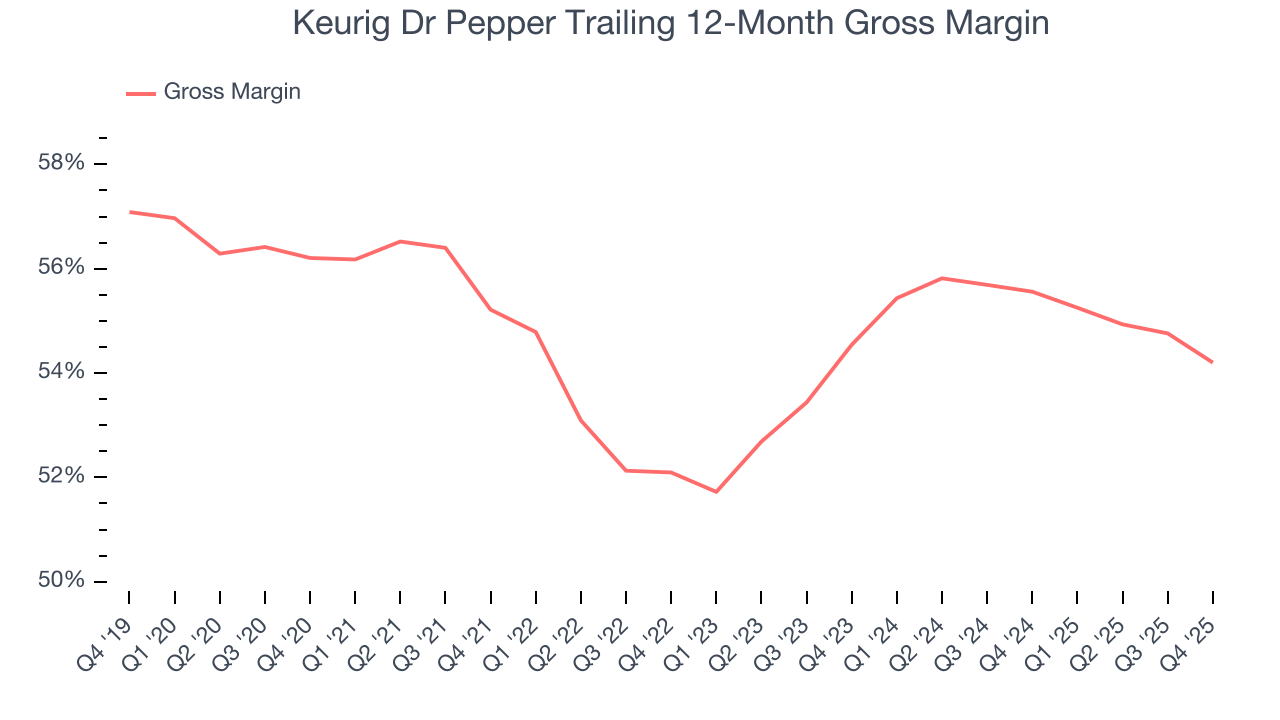

7. Gross Margin & Pricing Power

Keurig Dr Pepper has best-in-class unit economics for a consumer staples company, enabling it to invest in areas such as marketing and talent to grow its brand. As you can see below, it averaged an elite 54.9% gross margin over the last two years. That means Keurig Dr Pepper only paid its suppliers $45.15 for every $100 in revenue.

This quarter, Keurig Dr Pepper’s gross profit margin was 53.8%, down 2.2 percentage points year on year. Keurig Dr Pepper’s full-year margin has also been trending down over the past 12 months, decreasing by 1.4 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs (such as raw materials and manufacturing expenses).

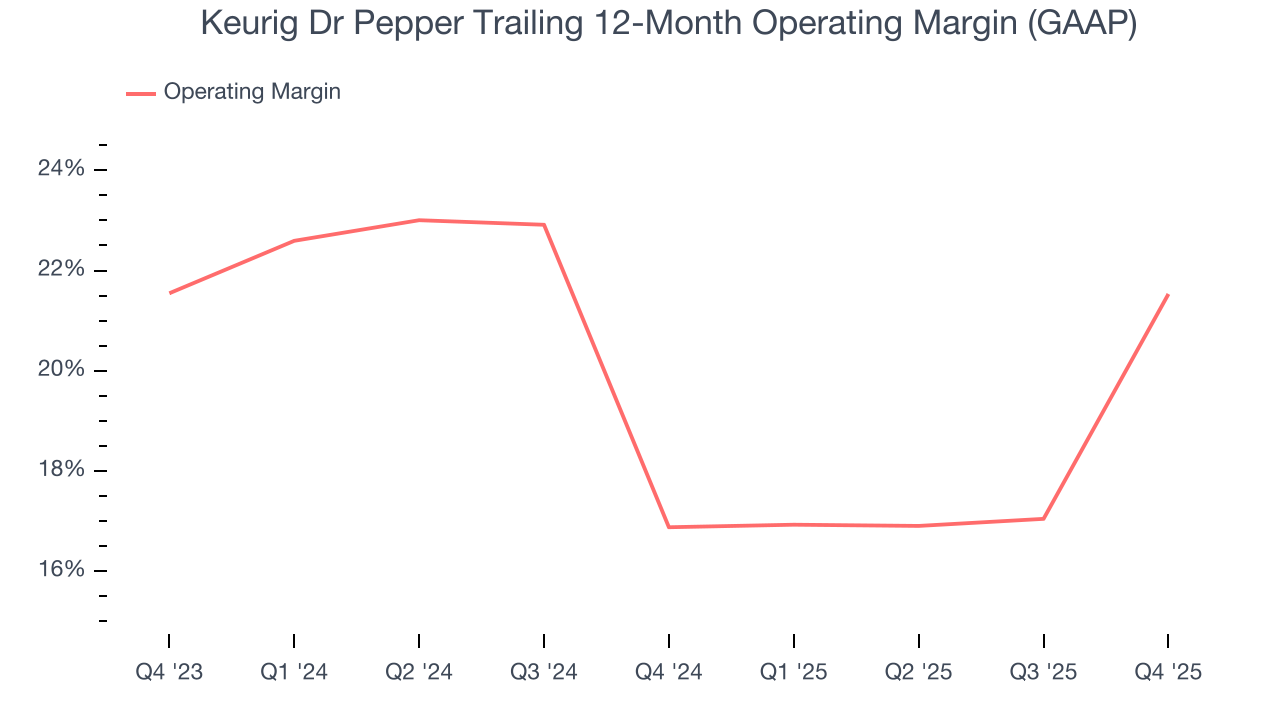

8. Operating Margin

Operating margin is a key profitability metric because it accounts for all expenses enabling a business to operate smoothly, including marketing and advertising, IT systems, wages, and other administrative costs.

Keurig Dr Pepper has been an efficient company over the last two years. It was one of the more profitable businesses in the consumer staples sector, boasting an average operating margin of 19.3%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Keurig Dr Pepper’s operating margin rose by 4.7 percentage points over the last year, as its sales growth gave it operating leverage.

In Q4, Keurig Dr Pepper generated an operating margin profit margin of 19.6%, up 18 percentage points year on year. The increase was solid, and because its gross margin actually decreased, we can assume it was more efficient because its operating expenses like marketing, and administrative overhead grew slower than its revenue.

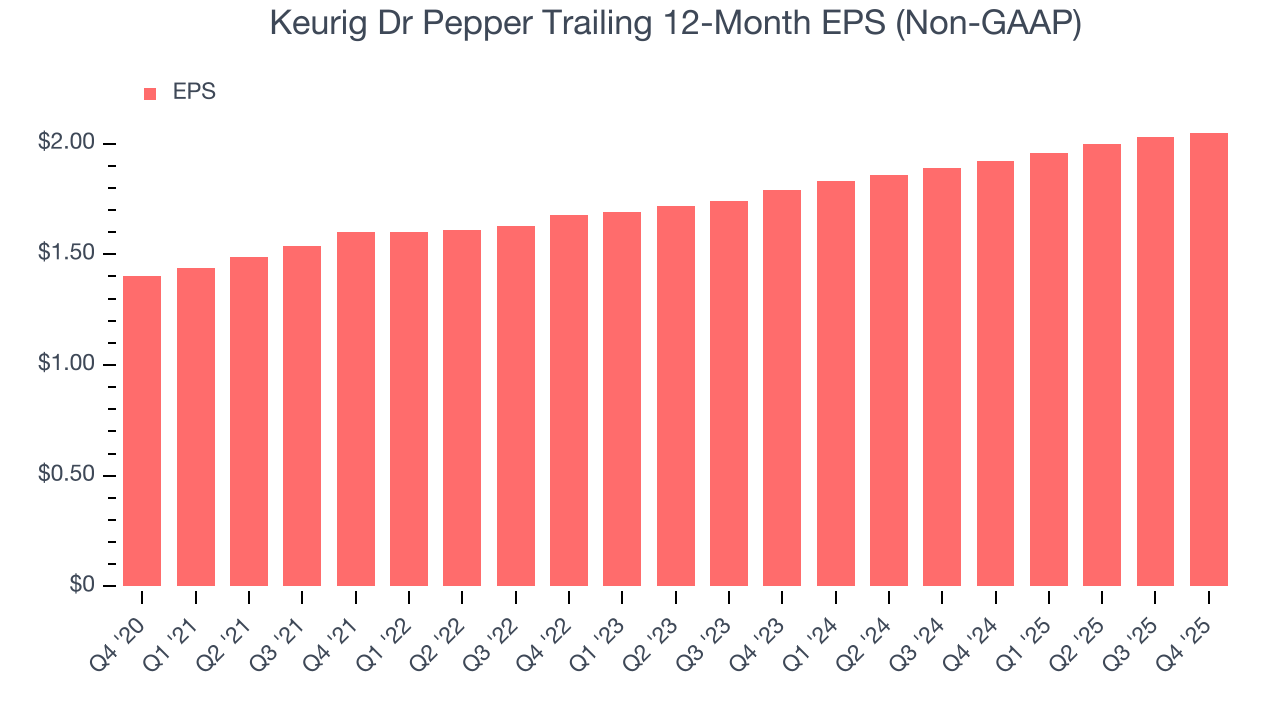

9. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Keurig Dr Pepper’s decent 6.9% annual EPS growth over the last three years aligns with its revenue performance. This tells us its incremental sales were profitable.

In Q4, Keurig Dr Pepper reported adjusted EPS of $0.60, up from $0.58 in the same quarter last year. This print beat analysts’ estimates by 1.9%. Over the next 12 months, Wall Street expects Keurig Dr Pepper’s full-year EPS of $2.05 to grow 5.2%.

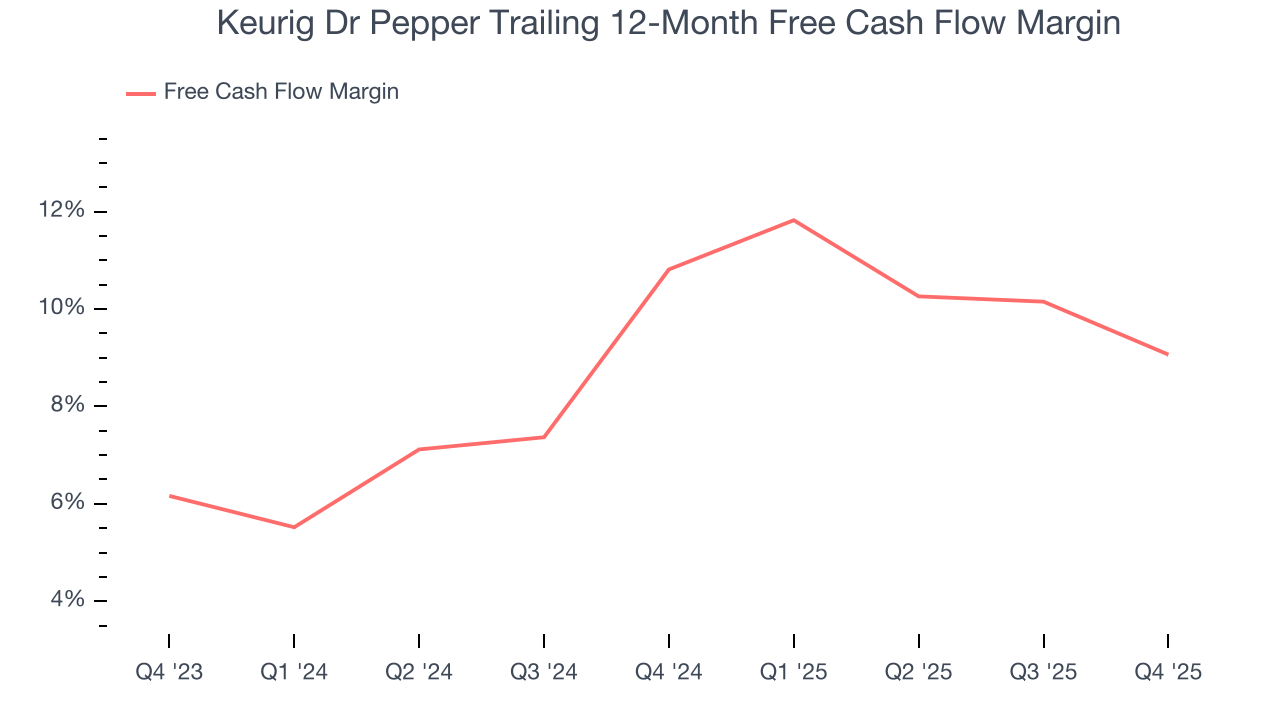

10. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Keurig Dr Pepper has shown robust cash profitability, driven by its attractive business model that enables it to reinvest or return capital to investors. The company’s free cash flow margin averaged 9.9% over the last two years, quite impressive for a consumer staples business.

Taking a step back, we can see that Keurig Dr Pepper’s margin dropped by 1.7 percentage points over the last year. If its declines continue, it could signal increasing investment needs and capital intensity.

Keurig Dr Pepper’s free cash flow clocked in at $550 million in Q4, equivalent to a 12.2% margin. The company’s cash profitability regressed as it was 4.7 percentage points lower than in the same quarter last year, but it’s still above its two-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, causing short-term swings. Long-term trends are more important.

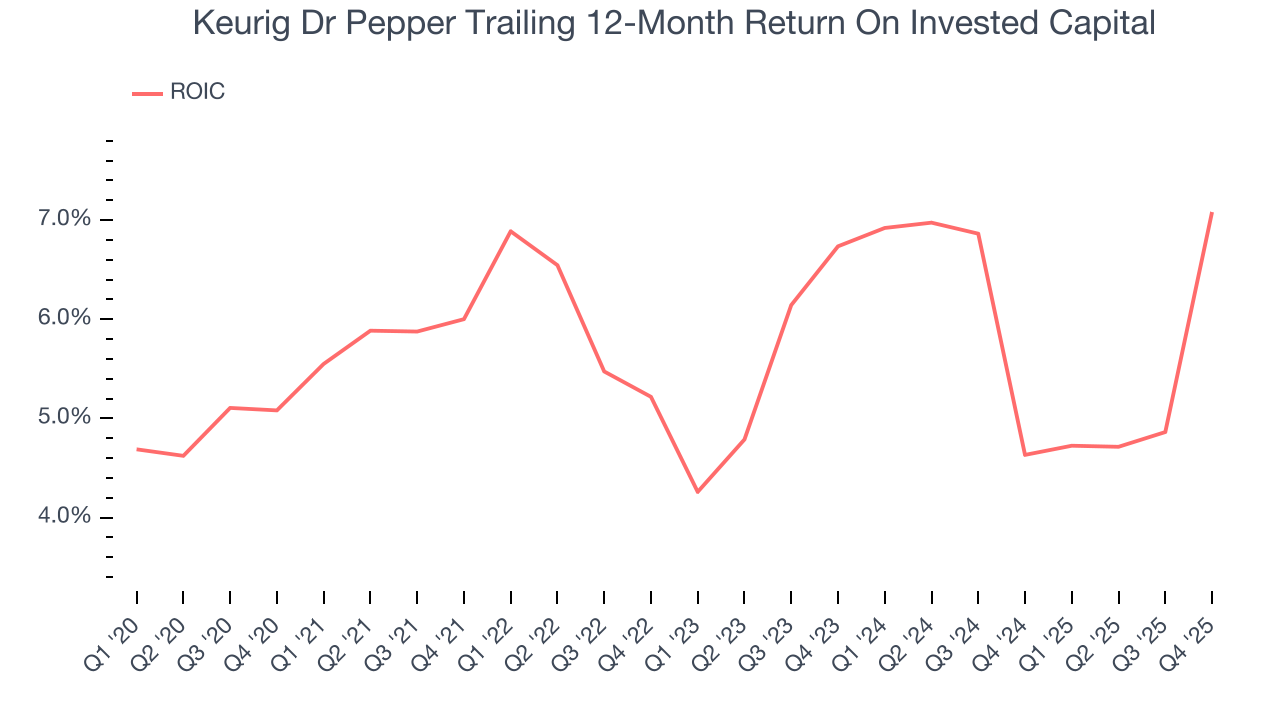

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Keurig Dr Pepper historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 5.9%, somewhat low compared to the best consumer staples companies that consistently pump out 20%+.

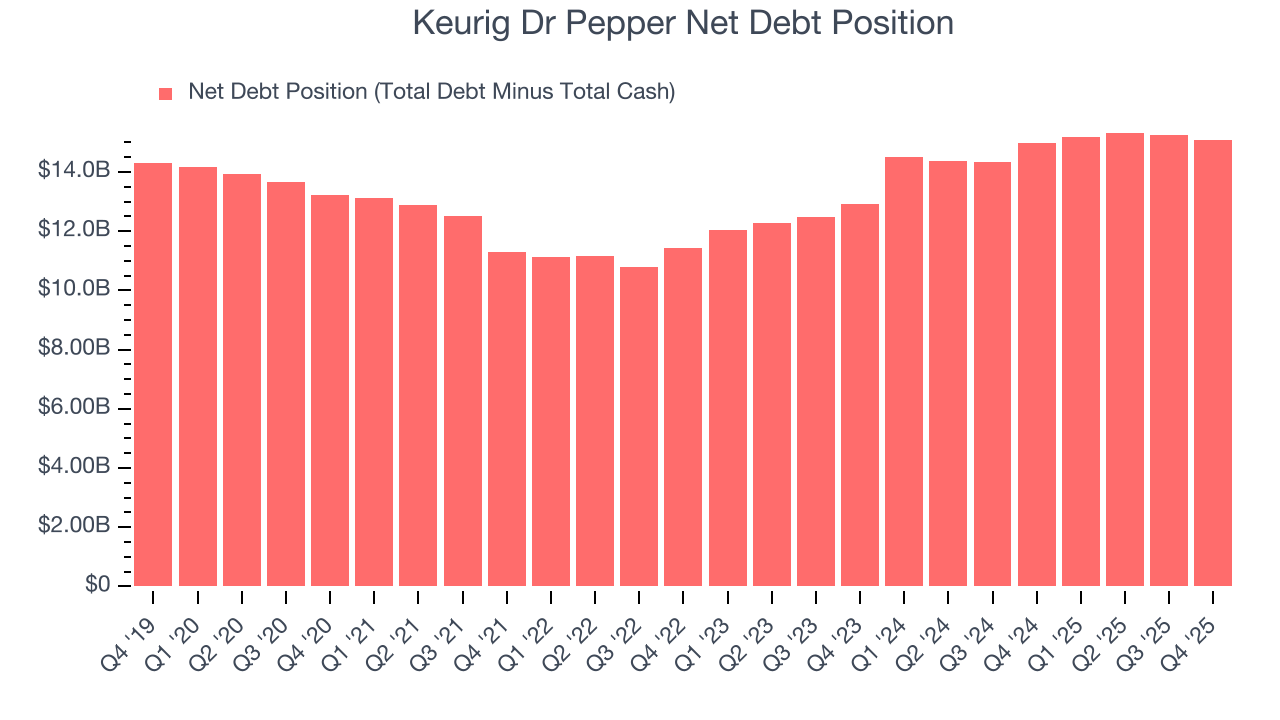

12. Balance Sheet Assessment

Keurig Dr Pepper reported $1.04 billion of cash and $16.14 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $4.84 billion of EBITDA over the last 12 months, we view Keurig Dr Pepper’s 3.1× net-debt-to-EBITDA ratio as safe. We also see its $754 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from Keurig Dr Pepper’s Q4 Results

We enjoyed seeing Keurig Dr Pepper beat analysts’ revenue and EPS expectations this quarter. Overall, this print had some key positives. The stock traded up 2% to $30.25 immediately following the results.

14. Is Now The Time To Buy Keurig Dr Pepper?

Updated: March 15, 2026 at 10:53 PM EDT

Before investing in or passing on Keurig Dr Pepper, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

There are a lot of things to like about Keurig Dr Pepper. Although its revenue growth was a little slower over the last three years, its growth over the next 12 months is expected to be higher. And while Keurig Dr Pepper’s relatively low ROIC suggests management has struggled to find compelling investment opportunities, its expanding operating margin shows the business has become more efficient. On top of that, its admirable gross margins are a wonderful starting point for the overall profitability of the business.

Keurig Dr Pepper’s P/E ratio based on the next 12 months is 11.8x. Looking at the consumer staples landscape right now, Keurig Dr Pepper trades at a pretty interesting price. If you’re a fan of the business and management team, now is a good time to scoop up some shares.

Wall Street analysts have a consensus one-year price target of $35.64 on the company (compared to the current share price of $27.47), implying they see 29.8% upside in buying Keurig Dr Pepper in the short term.