MercadoLibre (MELI)

MercadoLibre is a special business. Its fast revenue growth, profitability, and exceptional prospects make it a spectacular asset.― StockStory Analyst Team

1. News

2. Summary

Why We Like MercadoLibre

Originally started as an online auction platform, MercadoLibre (NASDAQ:MELI) is a one-stop e-commerce marketplace and fintech platform in Latin America.

- Annual revenue growth of 40% over the last three years was superb and indicates its market share is rising

- Market share will likely rise over the next 12 months as its expected revenue growth of 33.6% is robust

- Impressive free cash flow profitability enables the company to fund new investments or reward investors with share buybacks/dividends, and its improved cash conversion implies it’s becoming a less capital-intensive business

MercadoLibre sets the bar. The valuation looks reasonable relative to its quality, and we think now is a favorable time to buy the stock.

Why Is Now The Time To Buy MercadoLibre?

MercadoLibre’s stock price of $1,732 implies a valuation ratio of 16x forward EV/EBITDA. This price is justified - even cheap depending on how much you believe in the bull case - for the business fundamentals.

By definition, where you buy a stock impacts returns. Compared to entry price, business quality matters much more for long-term market outperformance. Buying in at a great price helps, nevertheless.

3. MercadoLibre (MELI) Research Report: Q4 CY2025 Update

Latin American e-commerce and fintech company MercadoLibre (NASDAQ:MELI) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 44.6% year on year to $8.76 billion. Its GAAP profit of $11.03 per share was 3.6% below analysts’ consensus estimates.

MercadoLibre (MELI) Q4 CY2025 Highlights:

- Revenue: $8.76 billion vs analyst estimates of $8.49 billion (44.6% year-on-year growth, 3.2% beat)

- EPS (GAAP): $11.03 vs analyst expectations of $11.44 (3.6% miss)

- Adjusted EBITDA: $1.13 billion vs analyst estimates of $1.10 billion (12.9% margin, 2.1% beat)

- Operating Margin: 10.1%, down from 13.5% in the same quarter last year

- Free Cash Flow Margin: 33.9%, down from 35.1% in the previous quarter

- Unique Active Buyers: 83 million, up 16 million year on year

- Market Capitalization: $94.52 billion

Company Overview

Originally started as an online auction platform, MercadoLibre (NASDAQ:MELI) is a one-stop e-commerce marketplace and fintech platform in Latin America.

The company connects buyers and sellers in the majority of countries across the continent. On its e-commerce platform, buyers can browse and purchase products ranging from furniture to groceries while sellers can list products and access tools to manage their online stores. It also offers payment and shipping solutions, as well as financial services such as loans through its subsidiary, MercadoPago.

MercadoLibre’s competitive advantage is its logistics network, which delivers 80%+ of orders within 48 hours. Shipping is particularly difficult in Latin America because of the region’s mountainous geography, so no other competitor is close to MercadoLibre’s capabilities.

MercadoLibre’s e-commerce business generates revenue primarily through commissions on third-party transactions. For example, when a seller makes a sale, MercadoLibre charges a fee ranging from mid-single-digits percentages to mid-teens percentages, depending on the category and sales volumes. Recently, it has started selling its own products to fill key inventory gaps. Advertising and sponsored listings are also additional sources of revenue.

In its fintech business, MercadoLibre leverages the seller data generated in its e-commerce business to provide loans to merchants. It also has a digital wallet offering that allows users to park their money and earn higher yields than in a traditional bank account—a high value proposition given the notorious inflation rates in Latin America.

4. Online Marketplace

Marketplaces have existed for centuries. Where once it was a main street in a small town or a mall in the suburbs, sellers benefitted from proximity to one another because they could draw customers by offering convenience and selection. Today, a myriad of online marketplaces fulfill that same role, aggregating large customer bases, which attracts commission-paying sellers, generating flywheel scale effects that feed back into further customer acquisition.

Competitors operating similar platforms include Amazon.com (NASDAQ:AMZN), Alibaba (NYSE:BABA), and eBay (NASDAQ:EBAY).

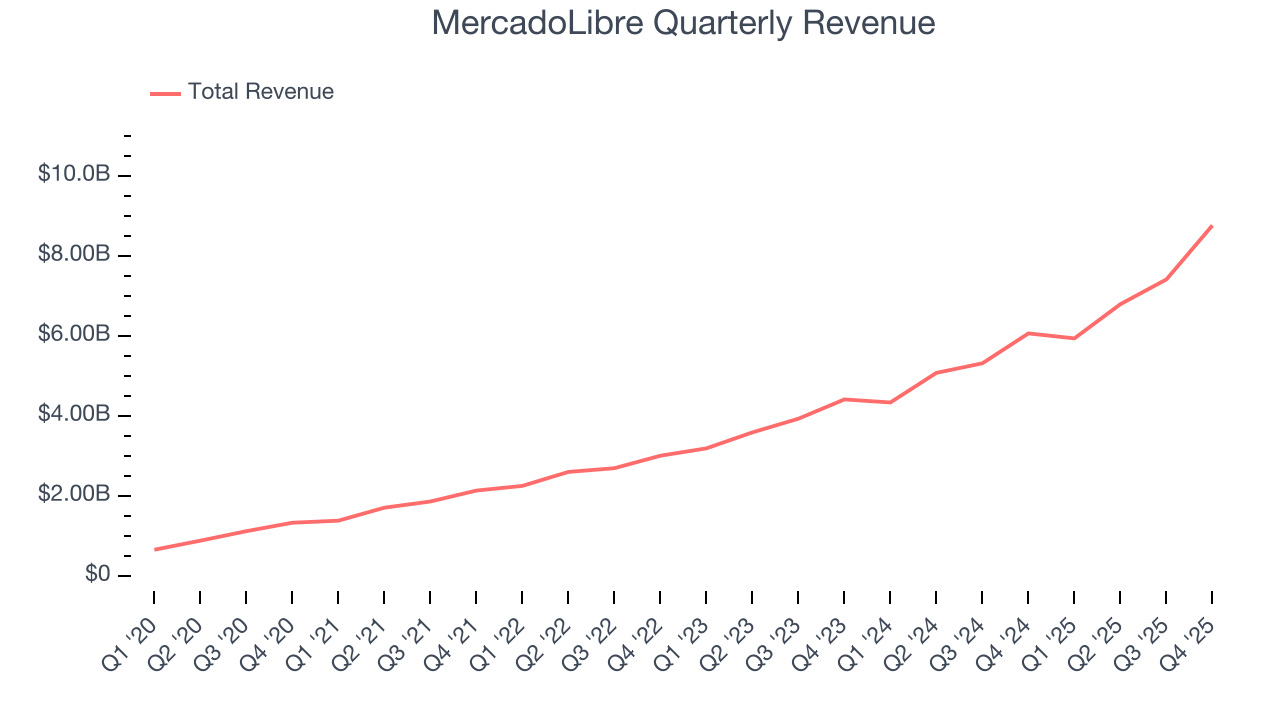

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, MercadoLibre’s 40% annualized revenue growth over the last three years was incredible. Its growth surpassed the average consumer internet company and shows its offerings resonate with customers, a great starting point for our analysis.

This quarter, MercadoLibre reported magnificent year-on-year revenue growth of 44.6%, and its $8.76 billion of revenue beat Wall Street’s estimates by 3.2%.

Looking ahead, sell-side analysts expect revenue to grow 29% over the next 12 months, a deceleration versus the last three years. Still, this projection is eye-popping given its scale and suggests the market is baking in success for its products and services.

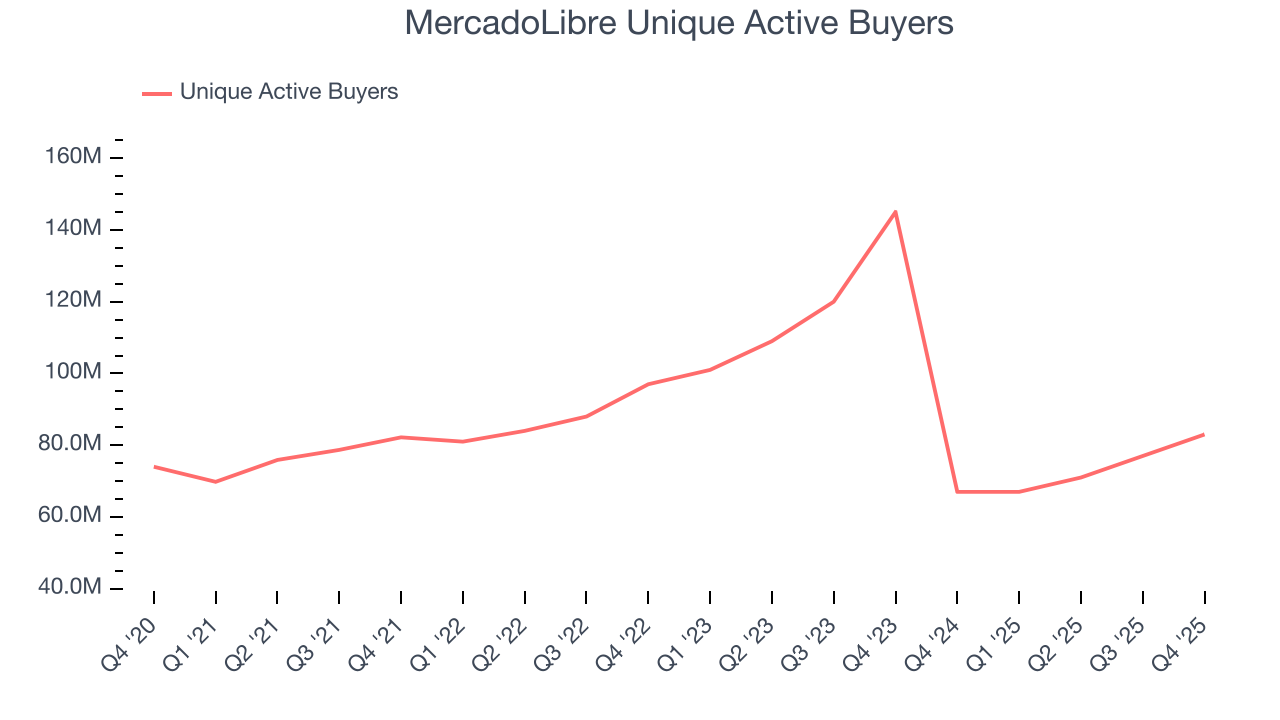

6. Unique Active Buyers

User Growth

As an online marketplace, MercadoLibre generates revenue growth by increasing both the number of users on its platform and the average order size in dollars.

MercadoLibre struggled with new customer acquisition over the last two years as its unique active buyers have declined by 15% annually to 83 million in the latest quarter. This performance isn't ideal because internet usage is secular, meaning there are typically unaddressed market opportunities. If MercadoLibre wants to accelerate growth, it likely needs to enhance the appeal of its current offerings or innovate with new products.

Luckily, MercadoLibre added 16 million unique active buyers in Q4, leading to 23.9% year-on-year growth. The quarterly print was higher than its two-year result, suggesting its new initiatives are accelerating user growth.

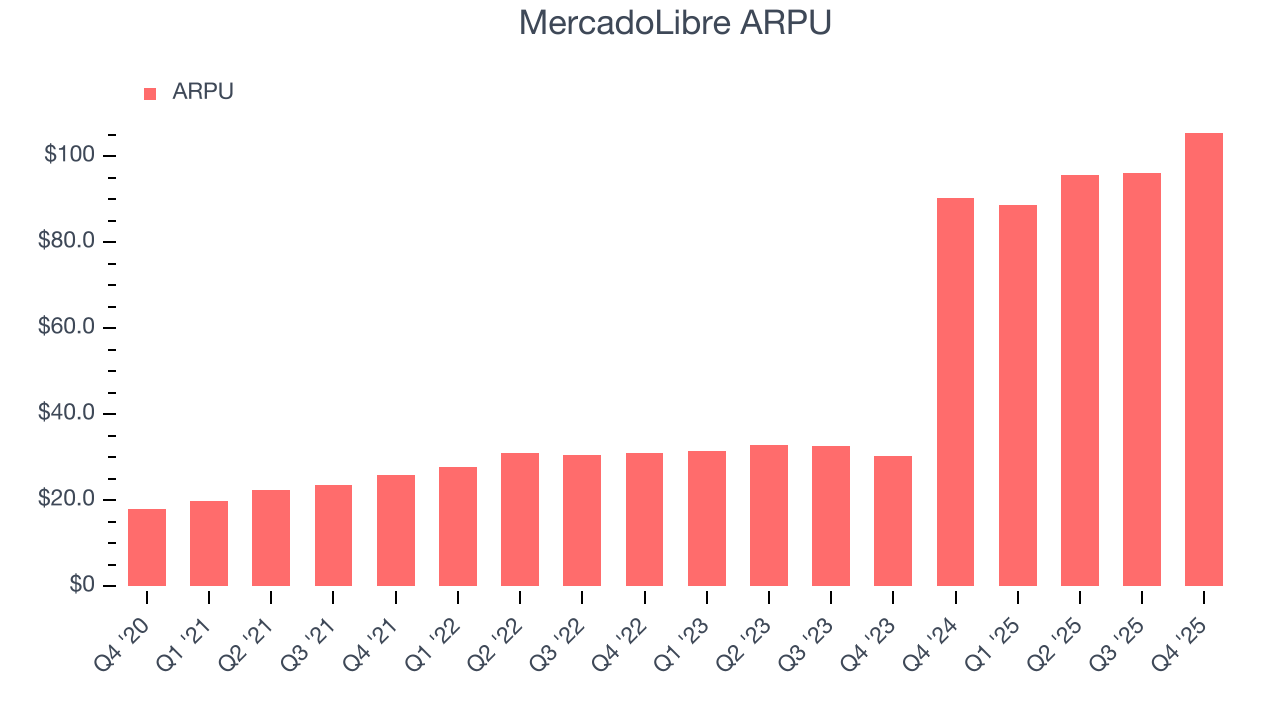

Revenue Per User

Average revenue per user (ARPU) is a critical metric to track because it measures how much the company earns in transaction fees from each user. ARPU also gives us unique insights into a user’s average order size and MercadoLibre’s take rate, or "cut", on each order.

MercadoLibre’s ARPU growth has been exceptional over the last two years, averaging 107%. Although its unique active buyers shrank during this time, the company’s ability to successfully increase monetization demonstrates its platform’s value for existing users.

This quarter, MercadoLibre’s ARPU clocked in at $105.53. It grew by 16.7% year on year, slower than its user growth.

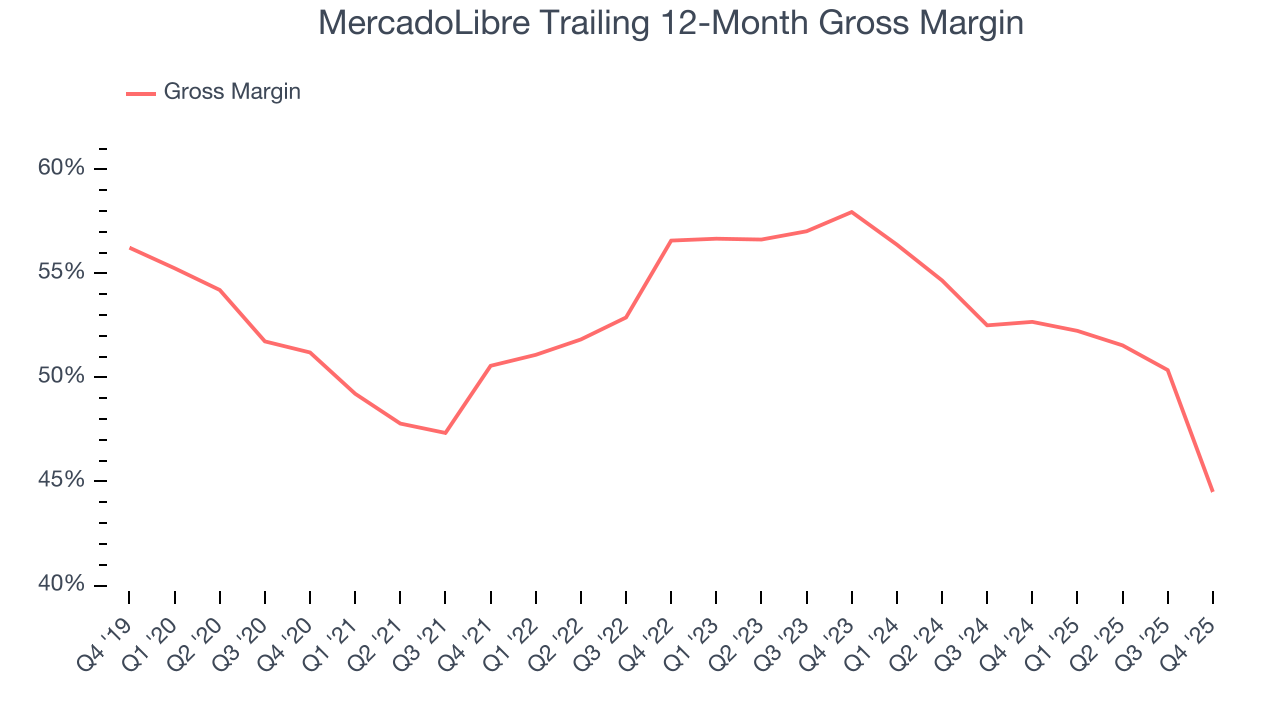

7. Gross Margin & Pricing Power

For online marketplaces like MercadoLibre, gross profit tells us how much money the company gets to keep after covering the base cost of its products and services, which typically include payment processing, hosting, and bandwidth fees in addition to the costs necessary to onboard buyers and sellers, such as identity verification.

MercadoLibre’s gross margin is below the broader consumer internet industry, giving it less room to hire engineering talent that can develop new products and services. As you can see below, it averaged a 47.9% gross margin over the last two years. Said differently, MercadoLibre had to pay a chunky $52.08 to its service providers for every $100 in revenue.

This quarter, MercadoLibre’s gross profit margin was 43.2%, down 24.7 percentage points year on year. MercadoLibre’s full-year margin has also been trending down over the past 12 months, decreasing by 8.2 percentage points. If this move continues, it could suggest a more competitive environment with pressure to lower prices and higher input costs.

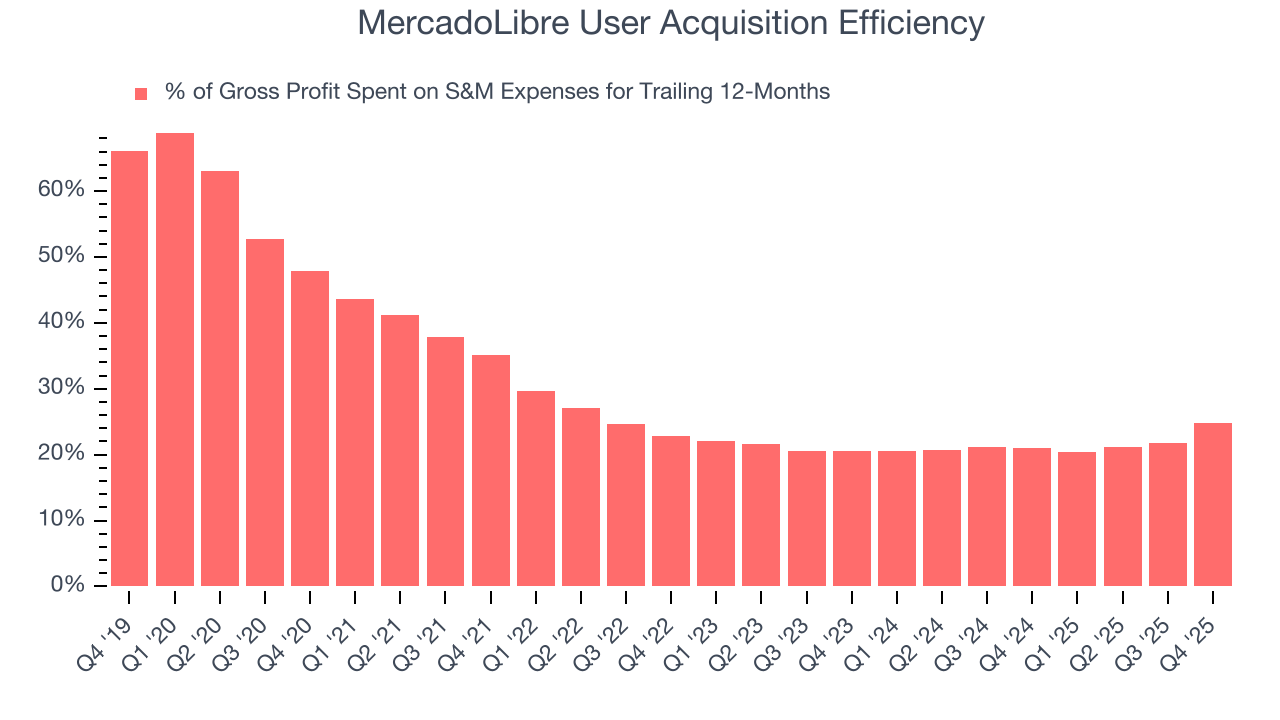

8. User Acquisition Efficiency

Consumer internet businesses like MercadoLibre grow from a combination of product virality, paid advertisement, and incentives (unlike enterprise software products, which are often sold by dedicated sales teams).

MercadoLibre is very efficient at acquiring new users, spending only 24.8% of its gross profit on sales and marketing expenses over the last year. This efficiency indicates that it has a highly differentiated product offering and strong brand reputation from scale, giving MercadoLibre the freedom to invest its resources into new growth initiatives while maintaining optionality.

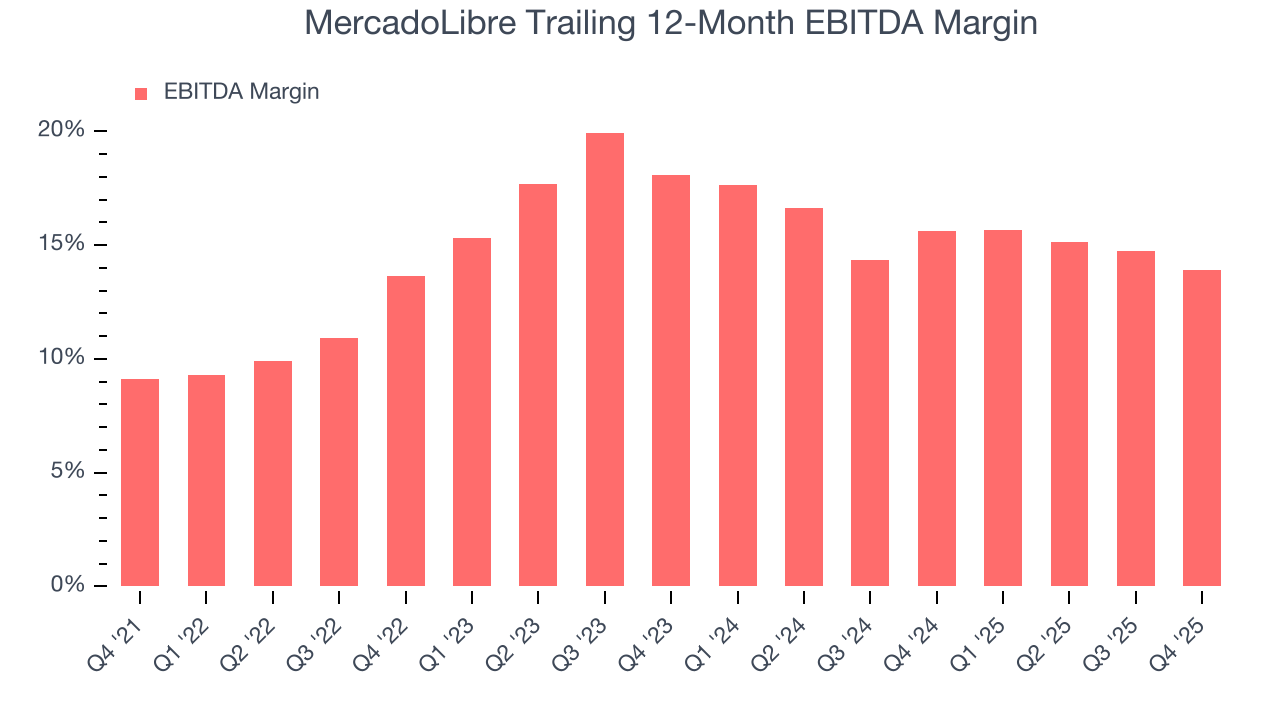

9. EBITDA

Operating income is often evaluated to assess a company’s underlying profitability. In a similar vein, EBITDA is used to analyze consumer internet companies because it excludes various one-time or non-cash expenses (depreciation), providing a clearer view of the business’s profit potential.

MercadoLibre’s EBITDA margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 14.6% over the last two years. This profitability was top-notch for a consumer internet business, showing it’s an well-run company with an efficient cost structure. This was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Looking at the trend in its profitability, MercadoLibre’s EBITDA margin might fluctuated slightly but has generally stayed the same over the last few years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, MercadoLibre generated an EBITDA margin profit margin of 12.9%, down 3.2 percentage points year on year. Since MercadoLibre’s gross margin decreased more than its EBITDA margin, we can assume its recent inefficiencies were driven more by weaker leverage on its cost of sales rather than increased marketing, R&D, and administrative overhead expenses.

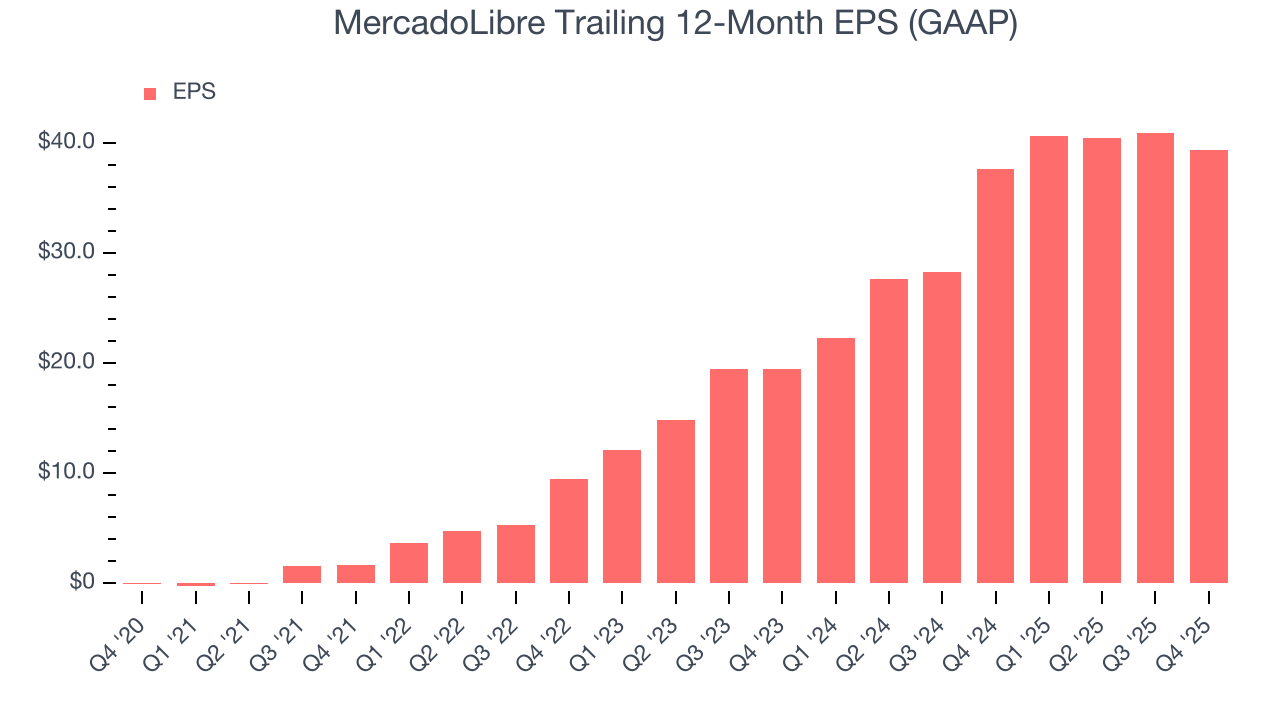

10. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

MercadoLibre’s EPS grew at an astounding 60.5% compounded annual growth rate over the last three years, higher than its 40% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its EBITDA margin didn’t improve.

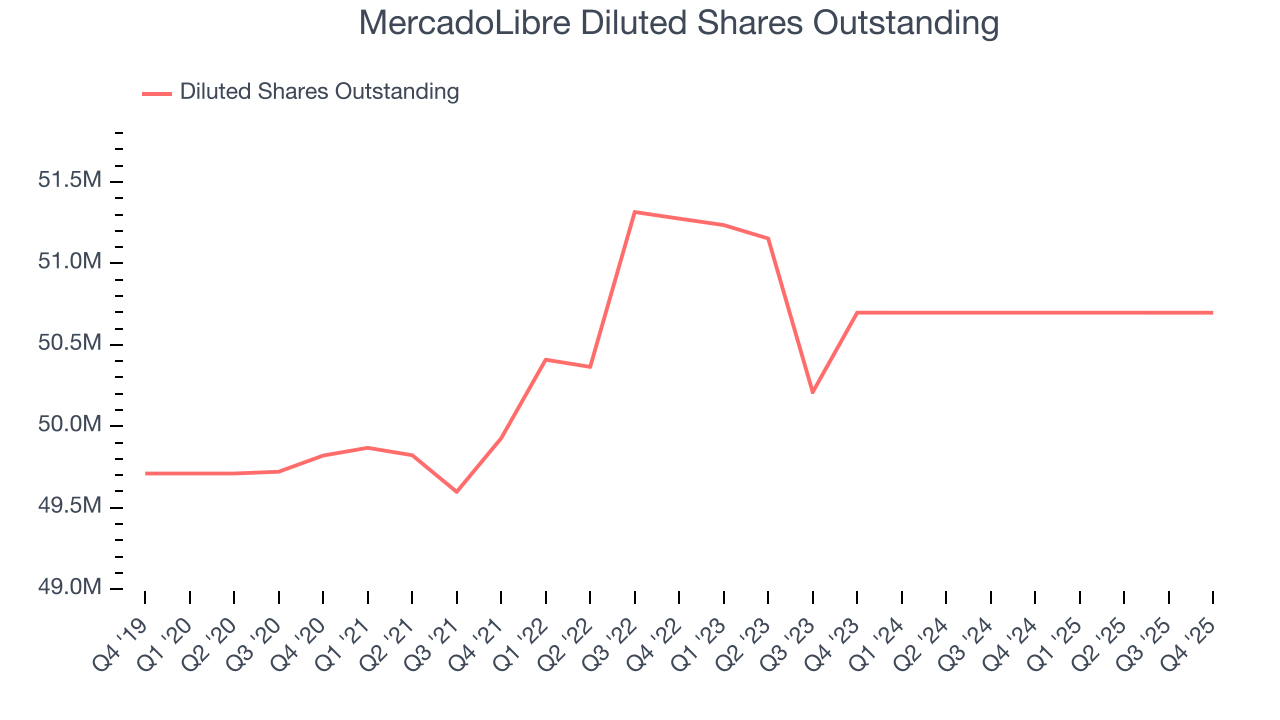

We can take a deeper look into MercadoLibre’s earnings to better understand the drivers of its performance. A three-year view shows that MercadoLibre has repurchased its stock, shrinking its share count by 1.1%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q4, MercadoLibre reported EPS of $11.03, down from $12.60 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects MercadoLibre’s full-year EPS of $39.39 to grow 46.5%.

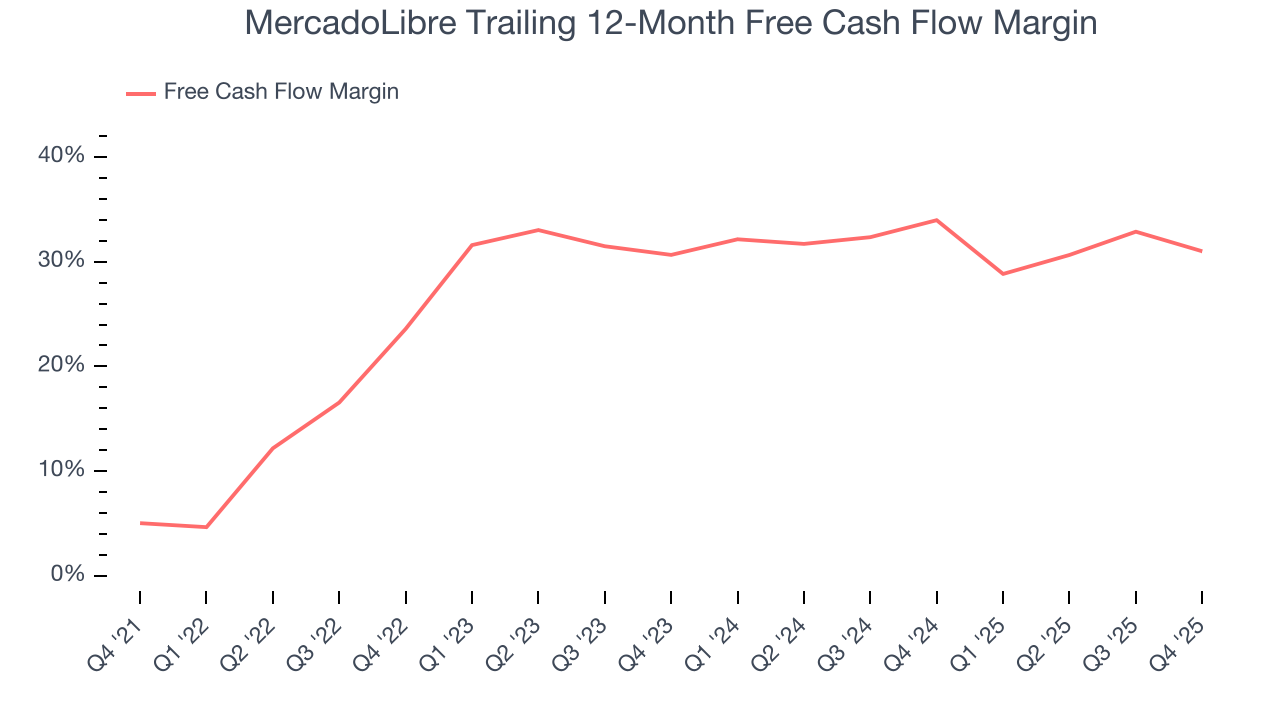

11. Cash Is King

Although EBITDA is undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

MercadoLibre has shown terrific cash profitability, driven by its cost-effective customer acquisition strategy that enables it to stay ahead of the competition through investments in new products rather than sales and marketing. The company’s free cash flow margin was among the best in the consumer internet sector, averaging an eye-popping 32.2% over the last two years.

Taking a step back, we can see that MercadoLibre’s margin expanded by 7.4 percentage points over the last few years. This shows the company is heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability was flat.

MercadoLibre’s free cash flow clocked in at $2.97 billion in Q4, equivalent to a 33.9% margin. The company’s cash profitability regressed as it was 9.4 percentage points lower than in the same quarter last year, but it’s still above its two-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, causing short-term swings. Long-term trends trump temporary fluctuations.

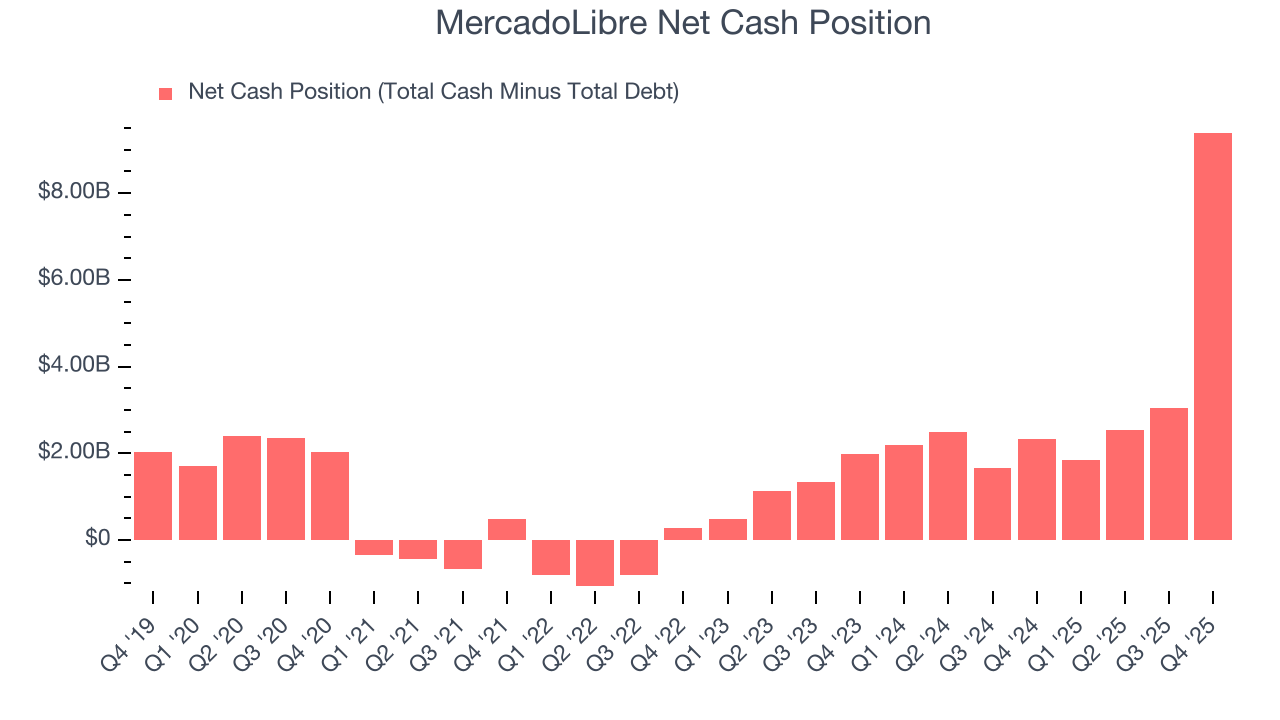

12. Balance Sheet Assessment

Companies with more cash than debt have lower bankruptcy risk.

MercadoLibre is a profitable, well-capitalized company with $16.17 billion of cash and $6.77 billion of debt on its balance sheet. This $9.40 billion net cash position is 9.6% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

13. Key Takeaways from MercadoLibre’s Q4 Results

We enjoyed seeing MercadoLibre increase its number of users this quarter. We were also happy its revenue outperformed Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 1.1% to $1,942 immediately after reporting.

14. Is Now The Time To Buy MercadoLibre?

Updated: March 16, 2026 at 10:29 PM EDT

Are you wondering whether to buy MercadoLibre or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

MercadoLibre is one of the best consumer internet companies out there. First of all, the company’s revenue growth was exceptional over the last three years. And while its daily active users have declined, its powerful free cash flow generation enables it to stay ahead of the competition through consistent reinvestment of profits. On top of that, MercadoLibre’s rising cash profitability gives it more optionality.

MercadoLibre’s EV/EBITDA ratio based on the next 12 months is 16x. Looking across the spectrum of consumer internet businesses, MercadoLibre’s fundamentals clearly illustrate it’s a special business. We like the stock at this price.

Wall Street analysts have a consensus one-year price target of $2,659 on the company (compared to the current share price of $1,732), implying they see 53.6% upside in buying MercadoLibre in the short term.