Sea (SE)

Sea is one of our favorite stocks. Its fusion of growth, outstanding profitability, and encouraging prospects makes it a beloved asset.― StockStory Analyst Team

1. News

2. Summary

Why We Like Sea

Founded in 2009 and a publicly traded company since 2017, Sea (NYSE:SE) started as a gaming platform and has since expanded to offer a variety of services such as e-commerce, digital payments, and financial services across Southeast Asia.

- Notable projected revenue growth of 26.6% for the next 12 months hints at market share gains

- Paying Users have grown by 24.9% annually, allowing for more profitable cross-selling opportunities if it can build complementary products and features

- Performance over the past three years shows its incremental sales were extremely profitable, as its annual earnings per share growth of 60.9% outpaced its revenue gains

We see a bright future for Sea. The valuation looks fair in light of its quality, and we think now is a prudent time to invest in the stock.

Why Is Now The Time To Buy Sea?

Sea is trading at $85.69 per share, or 12.7x forward EV/EBITDA. This price is justified - even cheap depending on how much you believe in the bull case - for the business fundamentals.

Our work shows, time and again, that buying high-quality companies and holding them routinely leads to market outperformance. If you can get an attractive entry price, that’s icing on the cake.

3. Sea (SE) Research Report: Q4 CY2025 Update

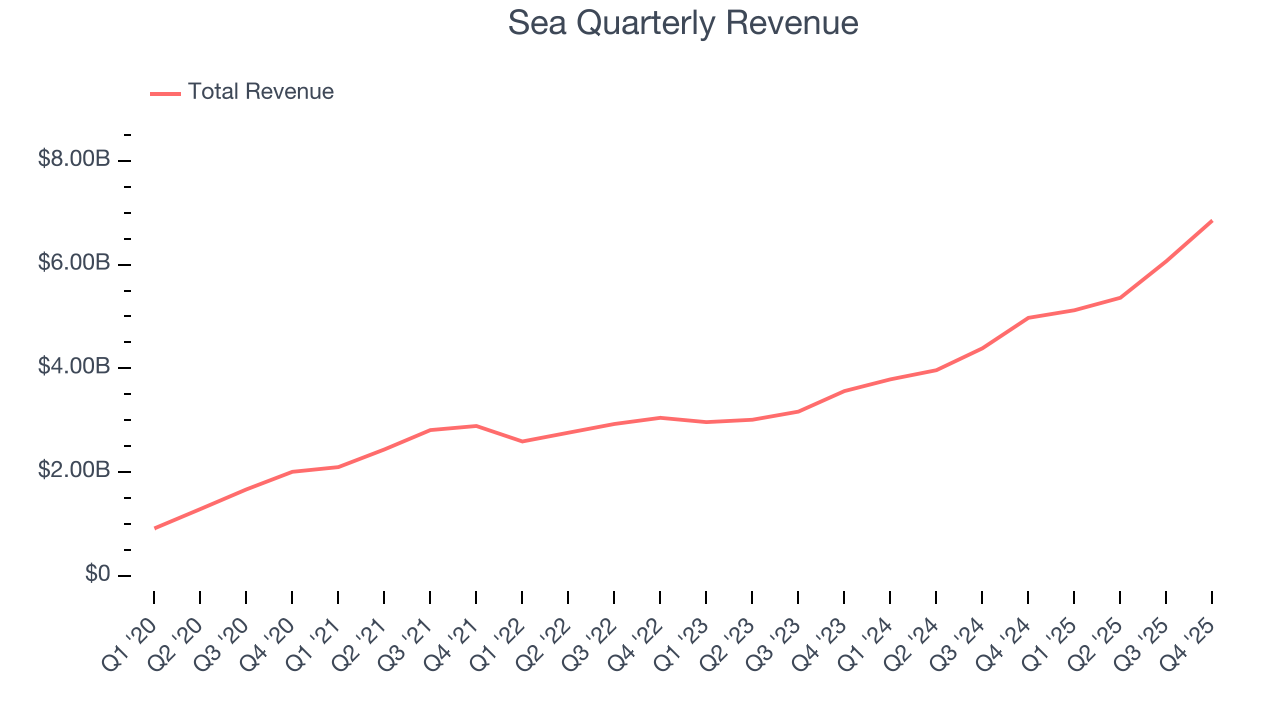

E-commerce and gaming company Sea (NYSE:SE) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 37.7% year on year to $6.85 billion. Its GAAP profit of $0.63 per share was 2.3% above analysts’ consensus estimates.

Sea (SE) Q4 CY2025 Highlights:

- Revenue: $6.85 billion vs analyst estimates of $6.43 billion (37.7% year-on-year growth, 6.6% beat)

- EPS (GAAP): $0.63 vs analyst estimates of $0.62 (2.3% beat)

- Adjusted EBITDA: $787.1 million vs analyst estimates of $824.2 million (11.5% margin, 4.5% miss)

- Operating Margin: 8.2%, up from 6.1% in the same quarter last year

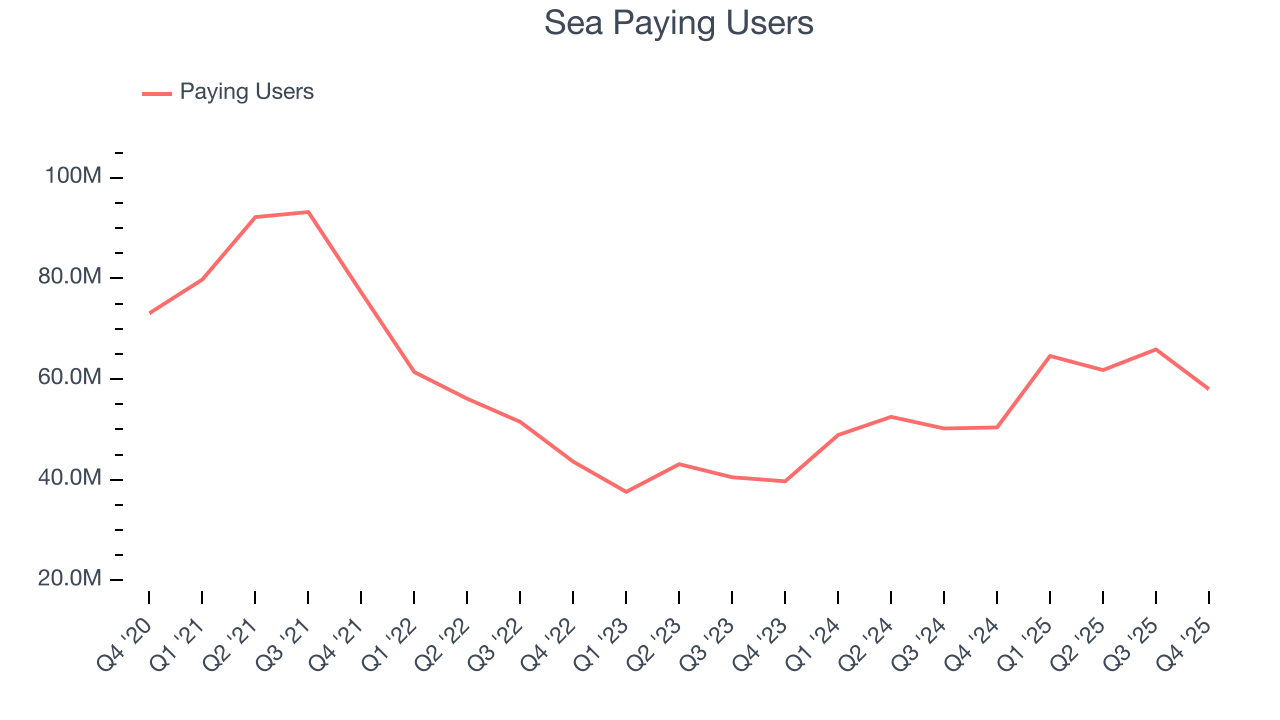

- Paying Users: 58 million, up 7.6 million year on year

- Market Capitalization: $62.29 billion

Company Overview

Founded in 2009 and a publicly traded company since 2017, Sea (NYSE:SE) started as a gaming platform and has since expanded to offer a variety of services such as e-commerce, digital payments, and financial services across Southeast Asia.

Garena, the initial product offering, is not just a single game but an ecosystem that allows users to play and socialize with other gamers from around the world. Whether players prefer action-packed shooters or strategy games, Garena seemingly has something for everyone, with additional features such as real-time chat to enhance engagement.

After gaming, Sea expanded into e-commerce with its Shopee platform, which is one of the largest digital marketplaces in Southeast Asia. Shopee allows users to buy and sell a wide variety of products, from electronics to groceries. Sea’s approach to e-commerce is a hybrid one–it acts as a marketplace but also holds inventory for some product categories. The company also offers financial services such as money transfers, bill payments, and pre-paid mobile phone top-ups through its SeaMoney platform.

In e-commerce, Sea generates revenue by taking a cut of the sale price when it acts as a marketplace and makes money on the actual sale price when it holds inventory. Gaming revenue primarily makes money through in-game purchases, where players can buy virtual goods such as skins, weapons, and other enhancements to improve the gaming experience.

4. Online Marketplace

Marketplaces have existed for centuries. Where once it was a main street in a small town or a mall in the suburbs, sellers benefitted from proximity to one another because they could draw customers by offering convenience and selection. Today, a myriad of online marketplaces fulfill that same role, aggregating large customer bases, which attracts commission-paying sellers, generating flywheel scale effects that feed back into further customer acquisition.

Competitors offering e-commerce platforms include Amazon.com (NASDAQ:AMZN) and Alibaba (NYSE:BABA), and competitors offering digital gaming include Sony (TSE:6758) and Nintendo (TSE:7974).

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, Sea’s 27.4% annualized revenue growth over the last three years was exceptional. Its growth surpassed the average consumer internet company and shows its offerings resonate with customers, a great starting point for our analysis.

This quarter, Sea reported wonderful year-on-year revenue growth of 37.7%, and its $6.85 billion of revenue exceeded Wall Street’s estimates by 6.6%.

Looking ahead, sell-side analysts expect revenue to grow 20.5% over the next 12 months, a deceleration versus the last three years. We still think its growth trajectory is attractive given its scale and suggests the market sees success for its products and services.

6. Paying Users

User Growth

As an online marketplace, Sea generates revenue growth by increasing both the number of users on its platform and the average order size in dollars.

Over the last two years, Sea’s paying users, a key performance metric for the company, increased by 24.9% annually to 58 million in the latest quarter. This growth rate is among the fastest of any consumer internet business and indicates its offerings have significant traction.

In Q4, Sea added 7.6 million paying users, leading to 15.1% year-on-year growth. The quarterly print was lower than its two-year result, suggesting its new initiatives aren’t accelerating user growth just yet.

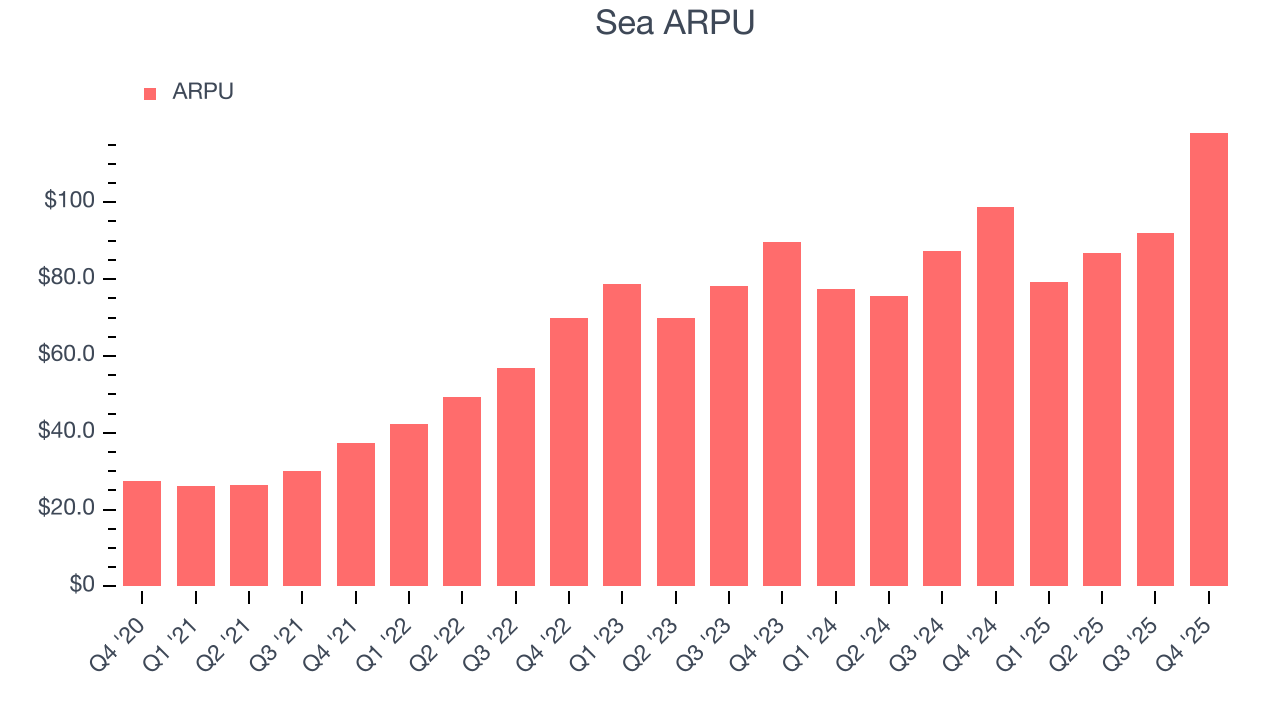

Revenue Per User

Average revenue per user (ARPU) is a critical metric to track because it measures how much the company earns in transaction fees from each user. ARPU also gives us unique insights into a user’s average order size and Sea’s take rate, or "cut", on each order.

Sea’s ARPU growth has been impressive over the last two years, averaging 8.8%. Its ability to increase monetization while quickly growing its paying users reflects the strength of its platform, as its users continue to spend more each year.

This quarter, Sea’s ARPU clocked in at $118.14. It grew by 19.7% year on year, faster than its paying users.

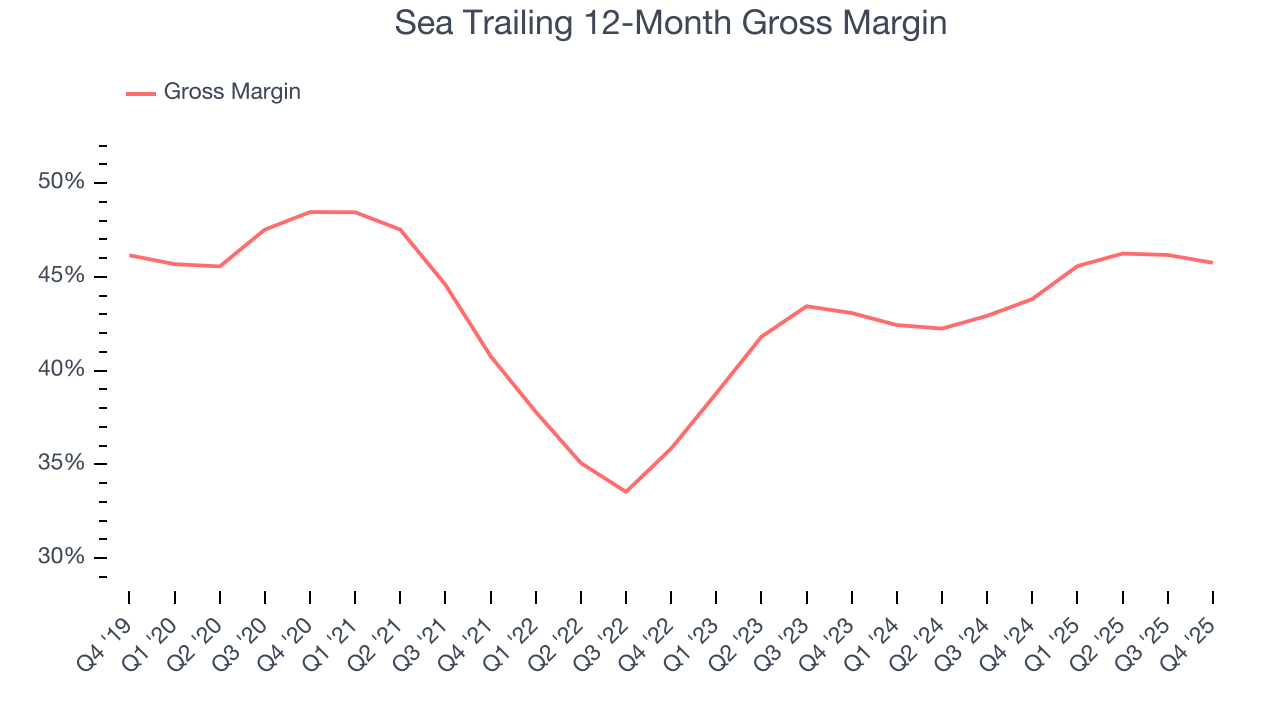

7. Gross Margin & Pricing Power

For online marketplaces like Sea, gross profit tells us how much money the company gets to keep after covering the base cost of its products and services, which typically include payment processing, hosting, and bandwidth fees in addition to the costs necessary to onboard buyers and sellers, such as identity verification.

Sea’s gross margin is below the broader consumer internet industry, giving it less room to hire engineering talent that can develop new products and services. As you can see below, it averaged a 44.9% gross margin over the last two years. That means Sea paid its providers a lot of money ($55.06 for every $100 in revenue) to run its business.

Sea’s gross profit margin came in at 43.8% this quarter , marking a 1.1 percentage point decrease from 44.8% in the same quarter last year. On a wider time horizon, however, Sea’s full-year margin has been trending up over the past 12 months, increasing by 1.9 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold (such as servers).

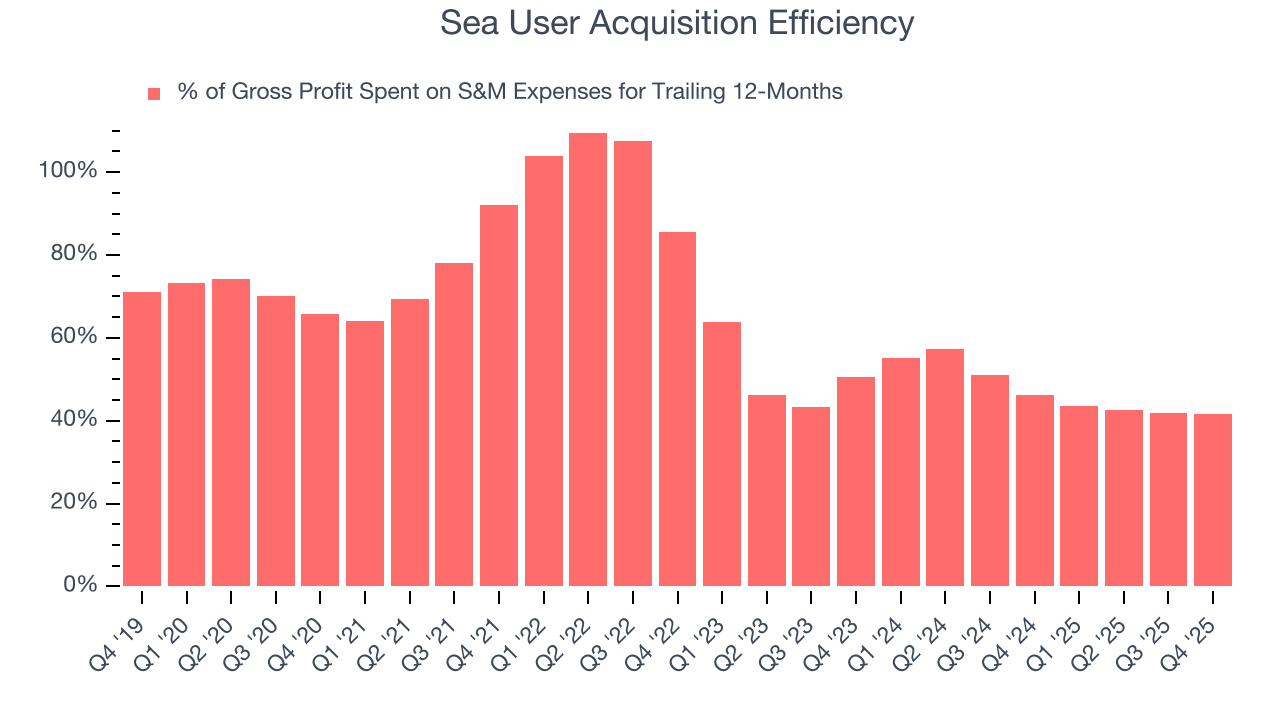

8. User Acquisition Efficiency

Consumer internet businesses like Sea grow from a combination of product virality, paid advertisement, and incentives (unlike enterprise software products, which are often sold by dedicated sales teams).

Sea does a decent job acquiring new users, spending 41.7% of its gross profit on sales and marketing expenses over the last year. This decent efficiency indicates relatively solid competitive positioning, giving Sea the freedom to invest its resources into new growth initiatives.

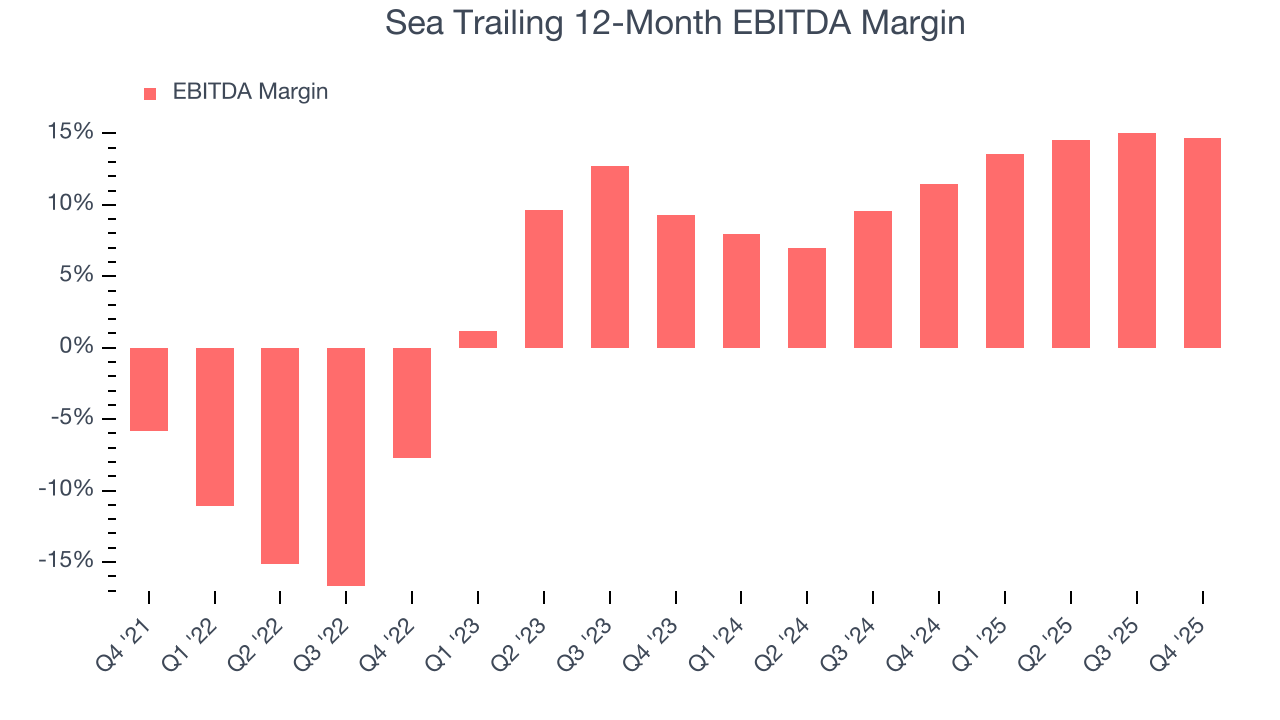

9. EBITDA

Operating income is often evaluated to assess a company’s underlying profitability. In a similar vein, EBITDA is used to analyze consumer internet companies because it excludes various one-time or non-cash expenses (depreciation), providing a clearer view of the business’s profit potential.

Sea has been an efficient company over the last two years. It was one of the more profitable businesses in the consumer internet sector, boasting an average EBITDA margin of 13.3%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Analyzing the trend in its profitability, Sea’s EBITDA margin rose by 22.4 percentage points over the last few years, as its sales growth gave it immense operating leverage.

This quarter, Sea generated an EBITDA margin profit margin of 11.5%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

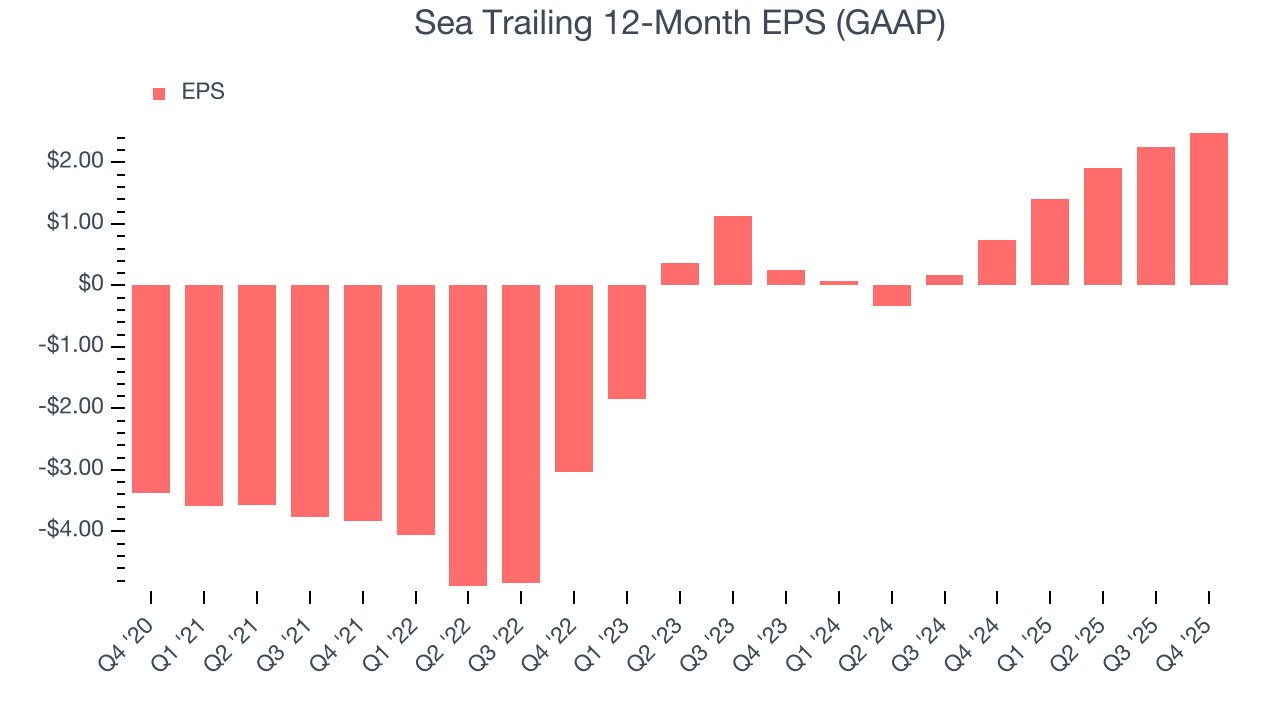

10. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sea’s full-year EPS flipped from negative to positive over the last three years. This is a good sign and shows it’s at an inflection point.

In Q4, Sea reported EPS of $0.63, up from $0.39 in the same quarter last year. This print beat analysts’ estimates by 2.3%. Over the next 12 months, Wall Street expects Sea’s full-year EPS of $2.49 to grow 47.2%.

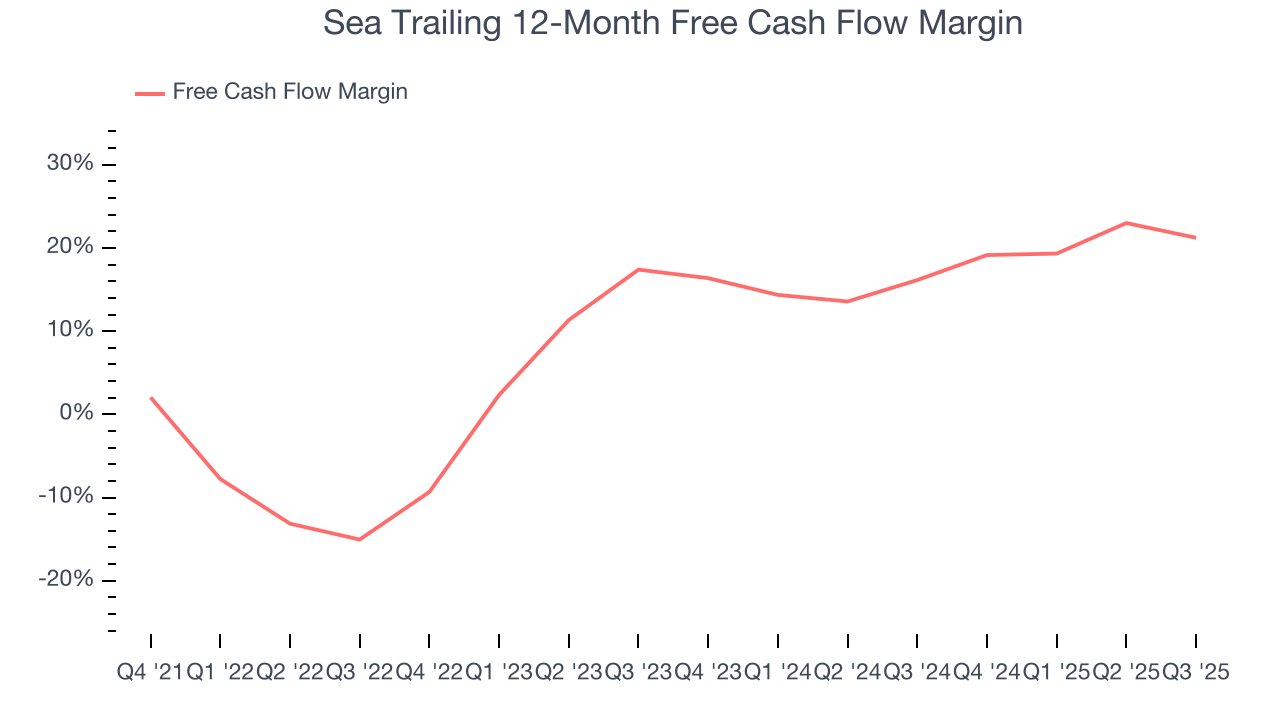

11. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Sea has shown robust cash profitability, giving it an edge over its competitors and the ability to reinvest or return capital to investors. The company’s free cash flow margin averaged 20.3% over the last two years, quite impressive for a consumer internet business.

Taking a step back, we can see that Sea’s margin expanded by 38.1 percentage points over the last few years. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

12. Balance Sheet Assessment

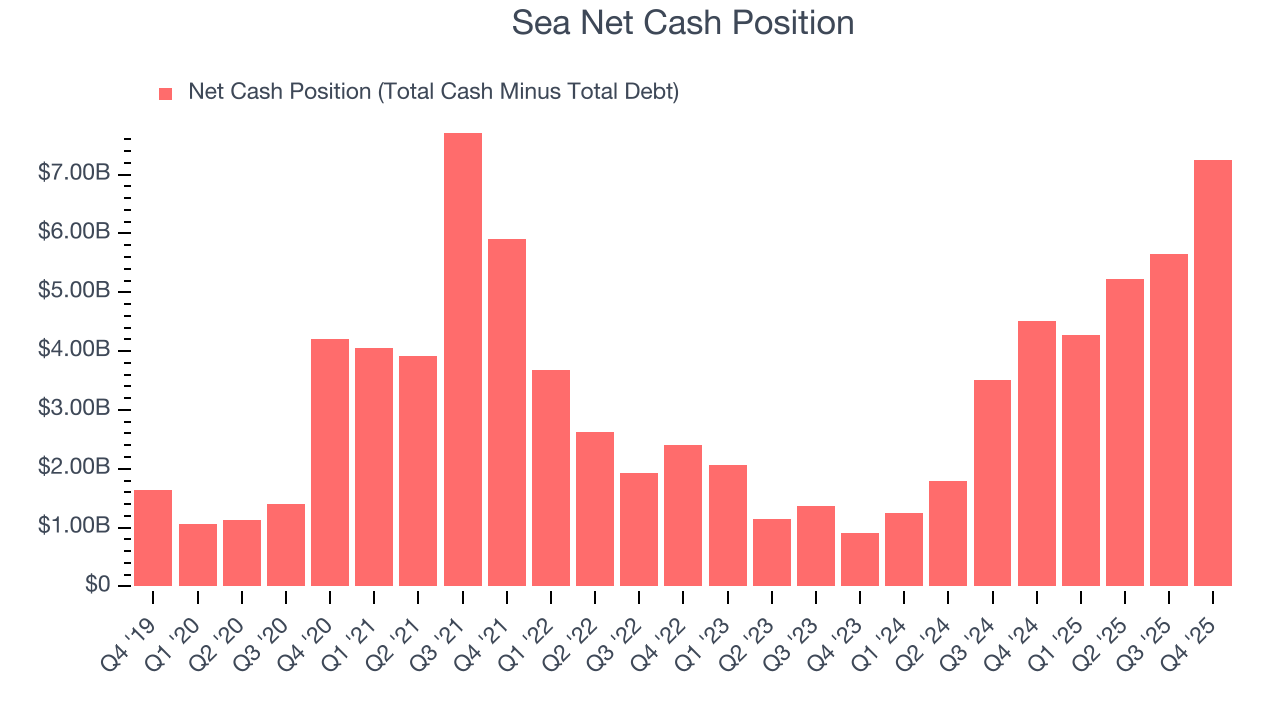

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

Sea is a profitable, well-capitalized company with $10.57 billion of cash and $3.33 billion of debt on its balance sheet. This $7.24 billion net cash position is 13.9% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

13. Key Takeaways from Sea’s Q4 Results

We enjoyed seeing Sea beat analysts’ revenue expectations this quarter. We were also glad it expanded its number of users. On the other hand, its EBITDA missed. Overall, this was a softer quarter. The stock traded down 12.1% to $92.44 immediately after reporting.

14. Is Now The Time To Buy Sea?

Updated: March 14, 2026 at 10:32 PM EDT

When considering an investment in Sea, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Sea is truly a cream-of-the-crop consumer internet company. First, the company’s revenue growth was exceptional over the last three years, and analysts believe it can continue growing at these levels. And while its gross margins make it more difficult to reach positive operating profits compared to other consumer internet businesses, its rising cash profitability gives it more optionality. Additionally, Sea’s expanding EBITDA margin shows the business has become more efficient.

Sea’s EV/EBITDA ratio based on the next 12 months is 12.7x. Looking at the consumer internet space today, Sea’s qualities as one of the best businesses really stand out, and we like it at this price.

Wall Street analysts have a consensus one-year price target of $142.25 on the company (compared to the current share price of $85.69), implying they see 66% upside in buying Sea in the short term.