Moderna (MRNA)

Moderna is in for a bumpy ride. Its recent pullback in sales and profitability suggests it’s struggling to scale down costs as demand evaporates.― StockStory Analyst Team

1. News

2. Summary

Why We Think Moderna Will Underperform

Rising to global prominence during the COVID-19 pandemic with one of the first effective vaccines, Moderna (NASDAQ:MRNA) develops messenger RNA (mRNA) medicines that direct the body's cells to produce proteins with therapeutic or preventive benefits for various diseases.

- Products and services are facing significant end-market challenges during this cycle as sales have declined by 46.7% annually over the last two years

- Earnings per share fell by 30.2% annually over the last five years while its revenue grew, showing its incremental sales were much less profitable

- Revenue base of $1.94 billion puts it at a disadvantage compared to larger competitors exhibiting economies of scale

Moderna falls short of our quality standards. Better businesses are for sale in the market.

Why There Are Better Opportunities Than Moderna

Moderna is trading at $51.55 per share, or 10.2x forward price-to-sales. The market typically values companies like Moderna based on their anticipated profits for the next 12 months, but it expects the business to lose money. We also think the upside isn’t great compared to the potential downside here - there are more exciting stocks to buy.

It’s better to invest in high-quality businesses with strong long-term earnings potential rather than to buy lower-quality companies with open questions and big downside risks.

3. Moderna (MRNA) Research Report: Q4 CY2025 Update

Biotechnology company Moderna (NASDAQ:MRNA) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, but sales fell by 29.8% year on year to $678 million. Its GAAP loss of $2.11 per share was 18.9% above analysts’ consensus estimates.

Moderna (MRNA) Q4 CY2025 Highlights:

- Revenue: $678 million vs analyst estimates of $660.2 million (29.8% year-on-year decline, 2.7% beat)

- EPS (GAAP): -$2.11 vs analyst estimates of -$2.60 (18.9% beat)

- Adjusted EBITDA: -$677 million (-99.9% margin, 42.9% year-on-year growth)

- Operating Margin: -126%, up from -129% in the same quarter last year

- Free Cash Flow Margin: 131%, up from 31.4% in the same quarter last year

- Market Capitalization: $15.67 billion

Company Overview

Rising to global prominence during the COVID-19 pandemic with one of the first effective vaccines, Moderna (NASDAQ:MRNA) develops messenger RNA (mRNA) medicines that direct the body's cells to produce proteins with therapeutic or preventive benefits for various diseases.

Moderna's technology platform revolves around synthetic mRNA, which serves as instructions for cells to produce proteins. When delivered into the body, these mRNA sequences instruct cells to create specific proteins that can prevent or treat disease. This approach differs from traditional vaccines and therapeutics that often introduce weakened pathogens or manufactured proteins into the body.

The company's product portfolio extends beyond its COVID-19 vaccine (Spikevax). Moderna is advancing a respiratory vaccine franchise that includes candidates for respiratory syncytial virus (RSV), influenza, and human metapneumovirus. It's also developing vaccines against latent viruses like cytomegalovirus (CMV), Epstein-Barr virus (EBV), and HIV.

In oncology, Moderna is working on individualized neoantigen therapies (INTs) that are custom-designed for each cancer patient based on the unique mutations in their tumor cells. These personalized cancer vaccines aim to help the immune system recognize and attack cancer cells. The company has partnered with Merck to develop these therapies, with promising results in melanoma trials.

Moderna also has programs targeting rare genetic diseases such as propionic acidemia, methylmalonic acidemia, and phenylketonuria. These conditions often result from missing or defective enzymes, and Moderna's approach uses mRNA to instruct cells to produce the needed proteins.

The company's business model involves both independent development of medicines and strategic collaborations with pharmaceutical companies, research institutions, and government agencies. Its manufacturing capabilities include highly specialized facilities designed to produce mRNA-based medicines at scale, a capability that proved crucial during the COVID-19 pandemic.

As the market for COVID-19 vaccines has shifted from pandemic to endemic, Moderna has adapted by offering different product presentations, including single-dose options and pre-filled syringes, while simultaneously advancing its broader pipeline of mRNA medicines.

4. Therapeutics

Over the next few years, therapeutic companies, which develop a wide variety of treatments for diseases and disorders, face strong tailwinds from advancements in precision medicine (including the use of AI to improve hit rates) and growing demand for treatments targeting rare diseases. However, headwinds such as rising scrutiny over drug pricing, regulatory unknowns, and competition from larger, more resourced pharmaceutical companies could weigh on growth.

Moderna's primary competitors include Pfizer/BioNTech (NYSE:PFE/NASDAQ:BNTX), which also produces an mRNA-based COVID-19 vaccine. Other competitors in the vaccine space include Novavax (NASDAQ:NVAX), Johnson & Johnson (NYSE:JNJ), and AstraZeneca (NASDAQ:AZN). In the broader mRNA therapeutics field, companies like CureVac (NASDAQ:CVAC) and Translate Bio (acquired by Sanofi) are also developing competing technologies.

5. Revenue Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With just $1.94 billion in revenue over the past 12 months, Moderna is a small company in an industry where scale matters. This makes it difficult to build trust with customers because healthcare is heavily regulated, complex, and resource-intensive.

6. Revenue Growth

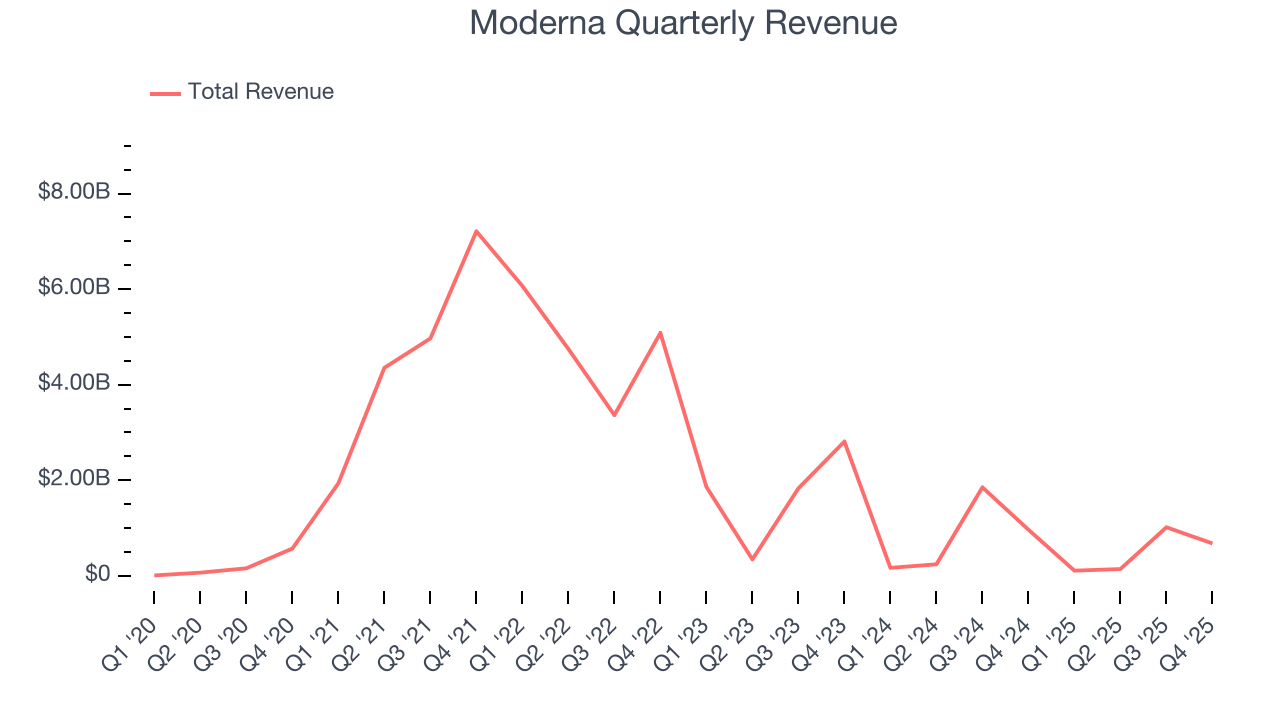

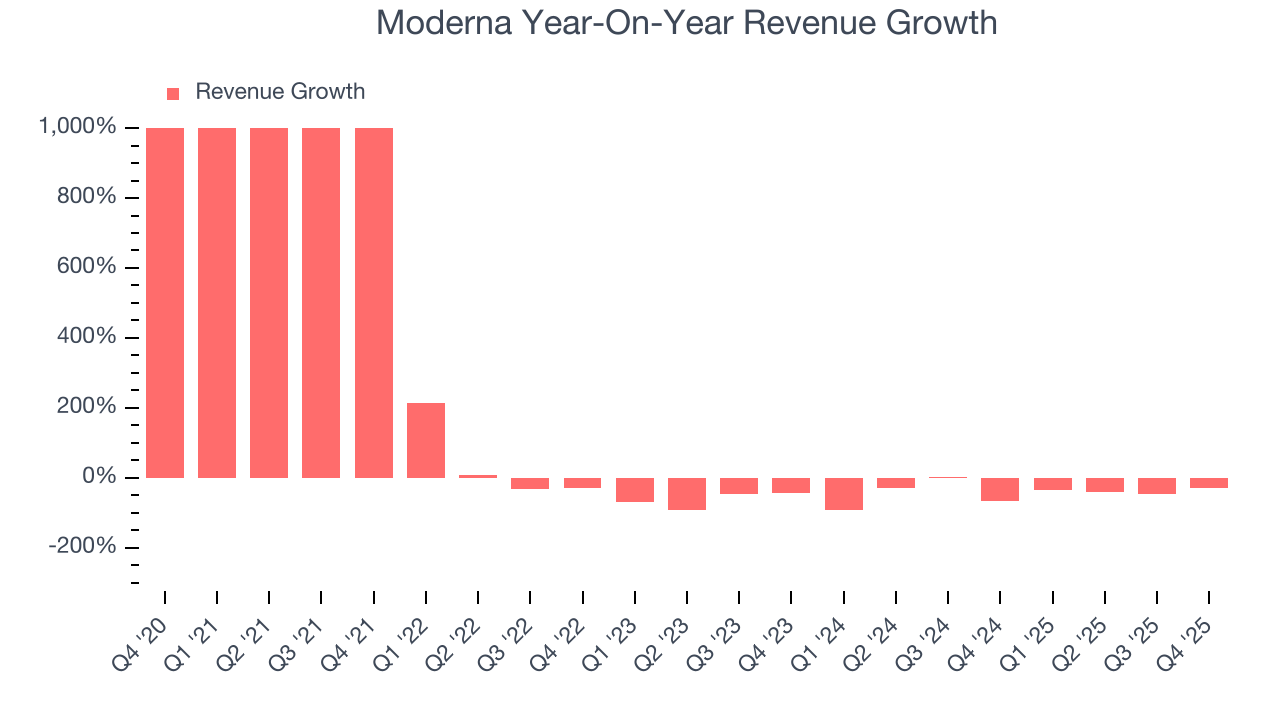

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Luckily, Moderna’s sales grew at an impressive 19.3% compounded annual growth rate over the last five years. Its growth beat the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Moderna’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 46.7% over the last two years.

This quarter, Moderna’s revenue fell by 29.8% year on year to $678 million but beat Wall Street’s estimates by 2.7%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. Although this projection indicates its newer products and services will catalyze better top-line performance, it is still below average for the sector.

7. Operating Margin

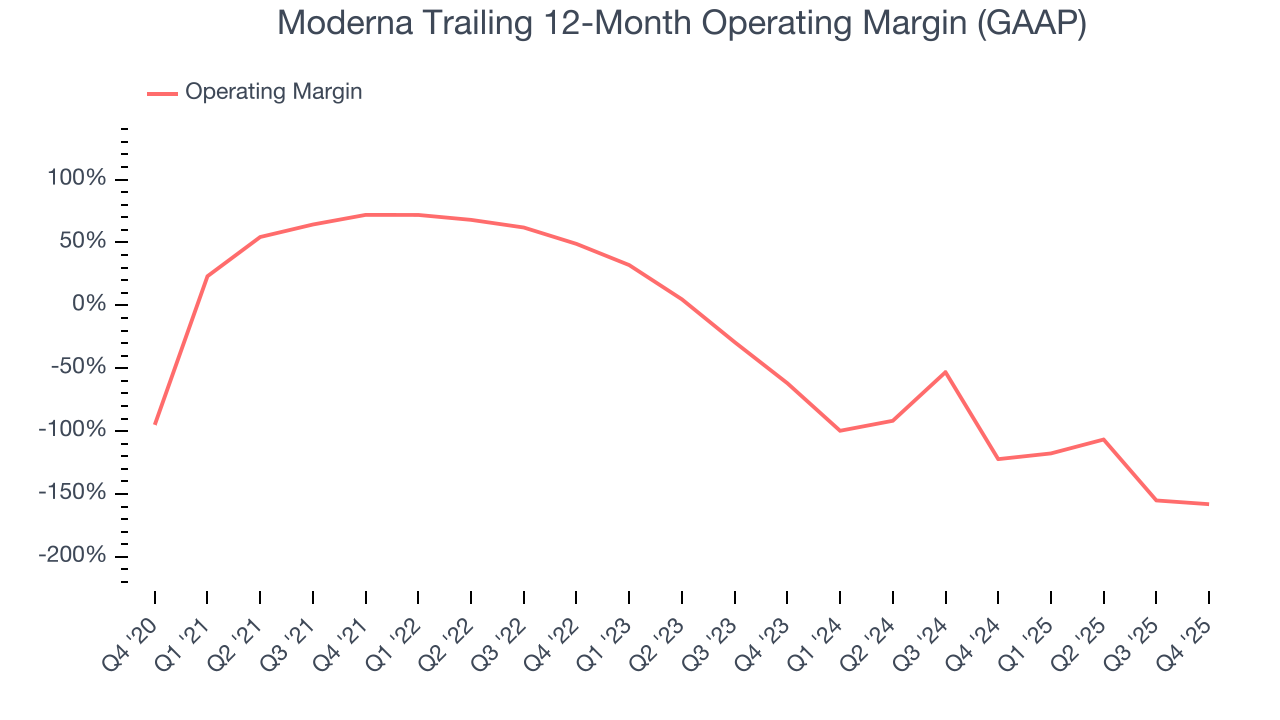

Moderna has been an efficient company over the last five years. It was one of the more profitable businesses in the healthcare sector, boasting an average operating margin of 23%.

Analyzing the trend in its profitability, Moderna’s operating margin decreased significantly over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 96.2 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

This quarter, Moderna generated an operating margin profit margin of negative 126%, up 2.6 percentage points year on year. This increase was a welcome development, especially since its revenue fell, showing it was more efficient because it scaled down its expenses.

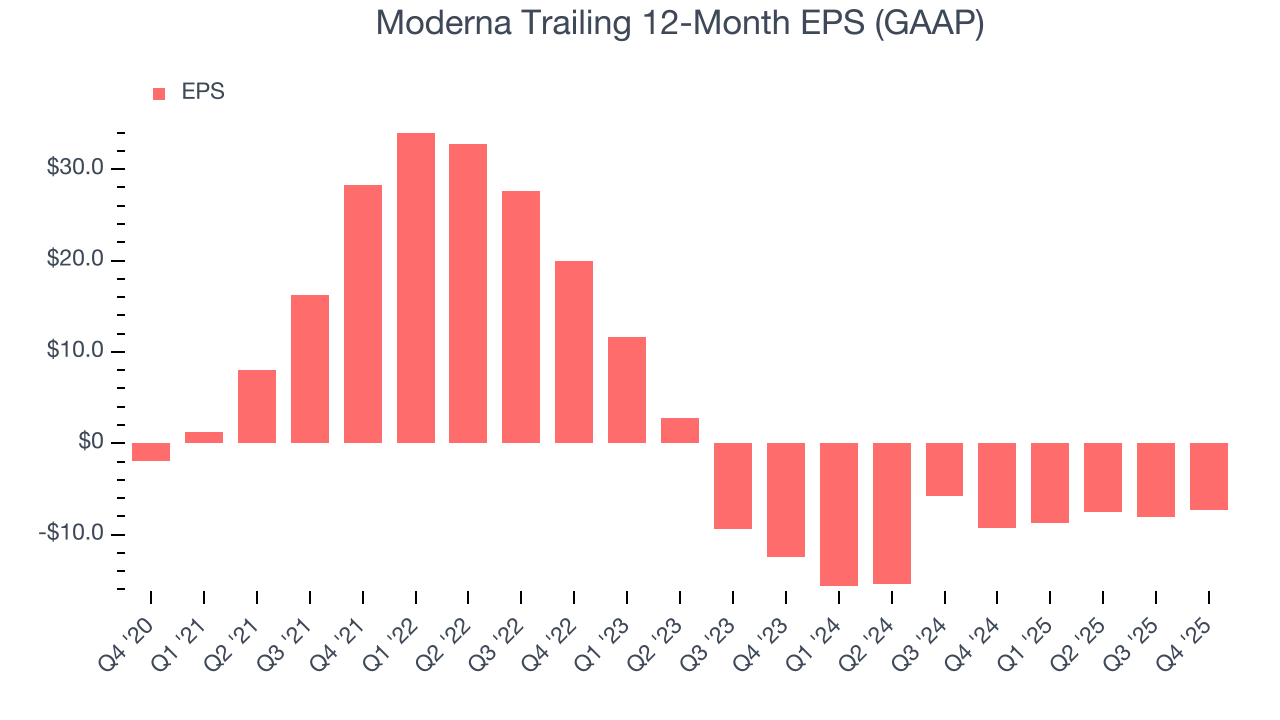

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Moderna’s earnings losses deepened over the last five years as its EPS dropped 30.2% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Moderna’s low margin of safety could leave its stock price susceptible to large downswings.

In Q4, Moderna reported EPS of negative $2.11, up from negative $2.91 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Moderna to improve its earnings losses. Analysts forecast its full-year EPS of negative $7.26 will advance to negative $6.68.

9. Cash Is King

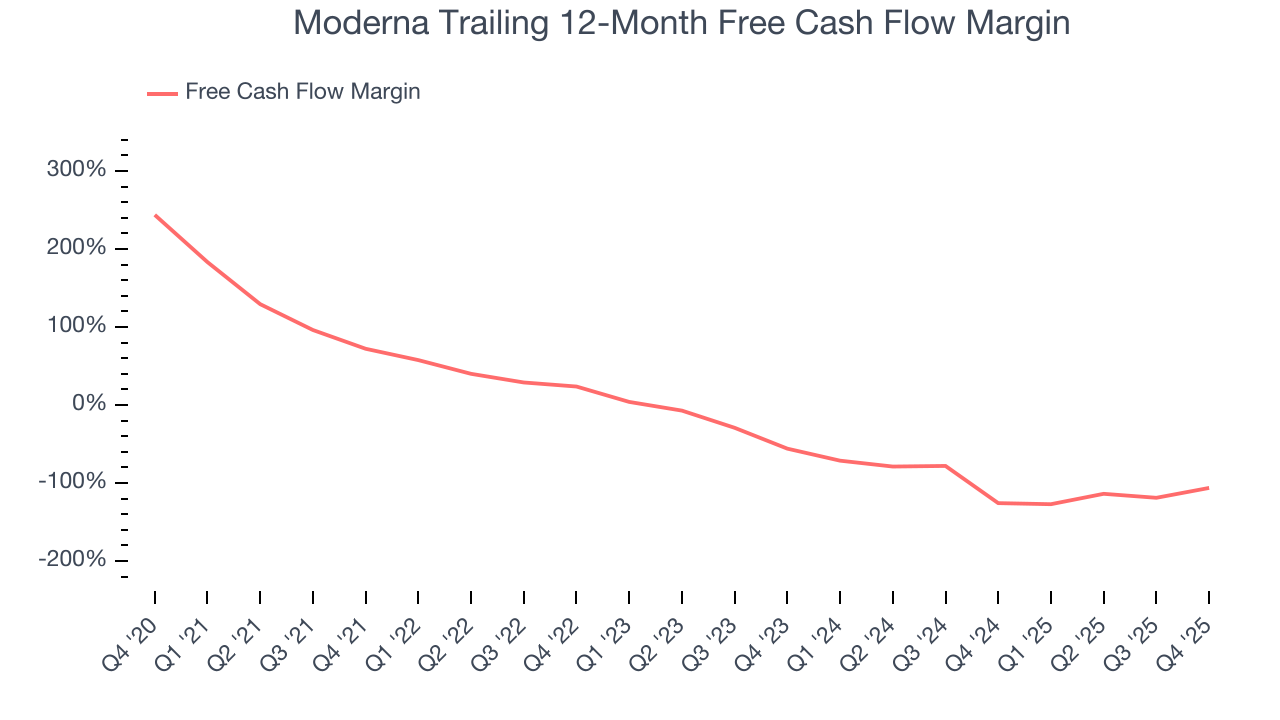

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Moderna has shown robust cash profitability, giving it an edge over its competitors and the ability to reinvest or return capital to investors. The company’s free cash flow margin averaged 16% over the last five years, quite impressive for a healthcare business.

Taking a step back, we can see that Moderna’s margin dropped meaningfully during that time. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level. If the longer-term trend returns, it could signal it is in the middle of an investment cycle.

Moderna’s free cash flow clocked in at $891 million in Q4, equivalent to a 131% margin. This result was good as its margin was 100 percentage points higher than in the same quarter last year, but we wouldn’t put too much weight on the short term because investment needs can be seasonal, causing temporary swings. Long-term trends are more important.

10. Balance Sheet Assessment

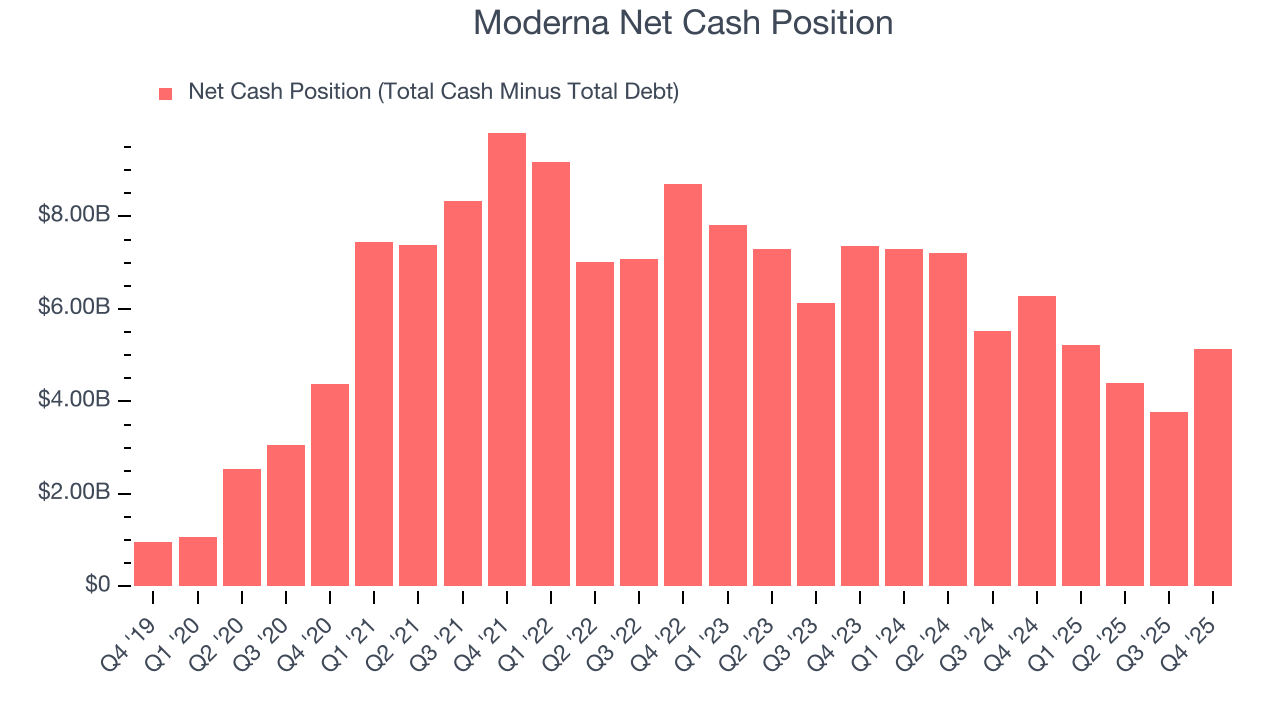

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

Moderna is a well-capitalized company with $5.80 billion of cash and $673 million of debt on its balance sheet. This $5.13 billion net cash position is 32.7% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

11. Key Takeaways from Moderna’s Q4 Results

It was good to see Moderna beat analysts’ EPS expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. Zooming out, we think this was a good print with some key areas of upside. Investors were likely hoping for more, and shares traded down 1.5% to $39.52 immediately after reporting.

12. Is Now The Time To Buy Moderna?

Updated: March 20, 2026 at 11:58 PM EDT

Before making an investment decision, investors should account for Moderna’s business fundamentals and valuation in addition to what happened in the latest quarter.

Moderna falls short of our quality standards. Although its revenue growth was impressive over the last five years, it’s expected to deteriorate over the next 12 months and its declining EPS over the last five years makes it a less attractive asset to the public markets. And while the company’s strong operating margins show it’s a well-run business, the downside is its declining adjusted operating margin shows the business has become less efficient.

Moderna’s forward price-to-sales ratio is 10.2x. The market typically values companies like Moderna based on their anticipated profits for the next 12 months, but it expects the business to lose money. We also think the upside isn’t great compared to the potential downside here - there are more exciting stocks to buy.

Wall Street analysts have a consensus one-year price target of $43.75 on the company (compared to the current share price of $51.55), implying they don’t see much short-term potential in Moderna.