PlayStudios (MYPS)

We wouldn’t recommend PlayStudios. Not only did its demand evaporate but also its negative returns on capital show it destroyed shareholder value.― StockStory Analyst Team

1. News

2. Summary

Why We Think PlayStudios Will Underperform

Founded by a team of former gaming industry executives, PlayStudios (NASDAQ:MYPS) offers free-to-play digital casino games.

- Annual revenue declines of 2.7% over the last five years indicate problems with its market positioning

- Earnings per share have contracted by 51.9% annually over the last four years, a headwind for returns as stock prices often echo long-term EPS performance

- Poor expense management has led to operating margin losses

PlayStudios fails to meet our quality criteria. You should search for better opportunities.

Why There Are Better Opportunities Than PlayStudios

PlayStudios is trading at $0.50 per share, or 0.3x forward price-to-sales. The market typically values companies like PlayStudios based on their anticipated profits for the next 12 months, but it expects the business to lose money. We also think the upside isn’t great compared to the potential downside here - there are more exciting stocks to buy.

We’d rather pay up for companies with elite fundamentals than get a bargain on poor ones. Cheap stocks can be value traps, and as their performance deteriorates, they will stay cheap or get even cheaper.

3. PlayStudios (MYPS) Research Report: Q4 CY2025 Update

Digital casino game platform PlayStudios (NASDAQ:MYPS) fell short of the market’s revenue expectations in Q4 CY2025, with sales falling 18.3% year on year to $55.4 million. Its GAAP loss of $0.11 per share was significantly below analysts’ consensus estimates.

PlayStudios (MYPS) Q4 CY2025 Highlights:

- Revenue: $55.4 million vs analyst estimates of $56.62 million (18.3% year-on-year decline, 2.2% miss)

- EPS (GAAP): -$0.11 vs analyst estimates of -$0.04 (significant miss)

- Adjusted EBITDA: $5.15 million vs analyst estimates of $6.97 million (9.3% margin, 26.1% miss)

- Operating Margin: -17.7%, up from -33.1% in the same quarter last year

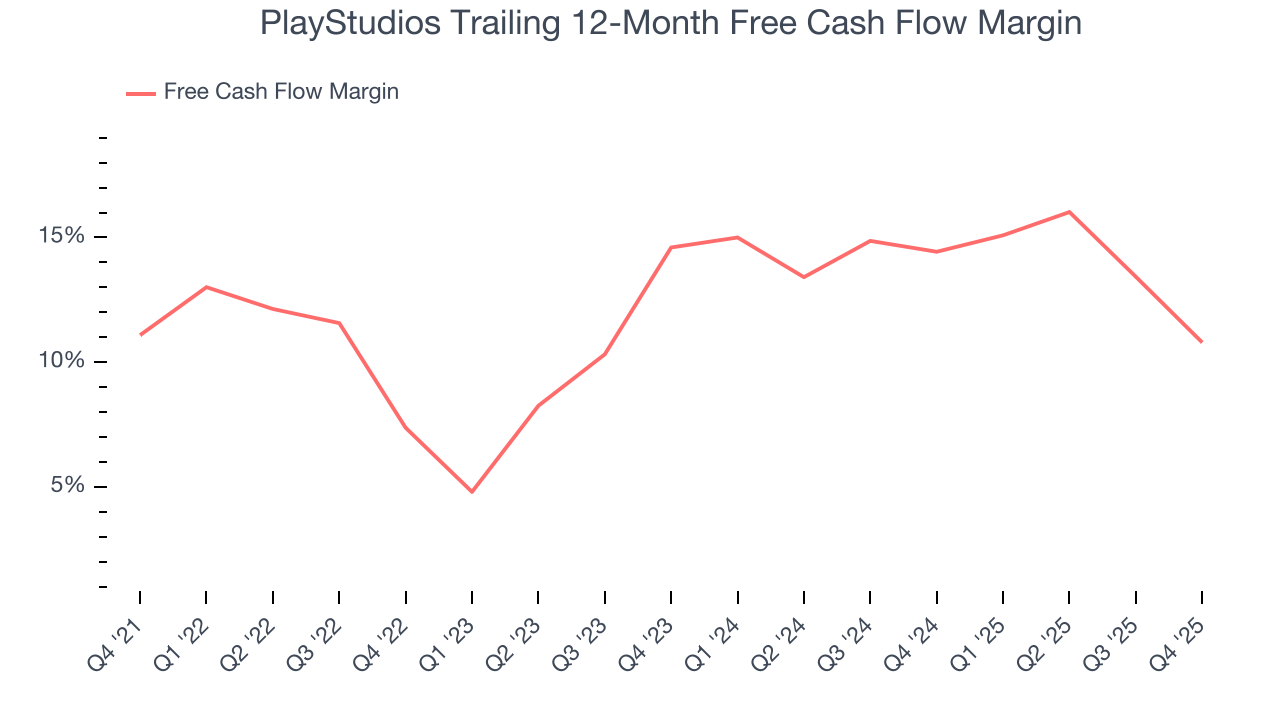

- Free Cash Flow Margin: 6.5%, down from 16.9% in the same quarter last year

- Daily Active Users: 2.04 million, down 688,000 year on year

- Market Capitalization: $64.12 million

Company Overview

Founded by a team of former gaming industry executives, PlayStudios (NASDAQ:MYPS) offers free-to-play digital casino games.

PlayStudios offers free-to-play casino games (slot machines, blackjack, and poker) that can be accessed through its mobile app myVEGAS. These are free-to-play games, which means that no real money is wagered, won, or lost.

However, players can earn rewards points that can be redeemed for prizes such as hotel stays, dining experiences, and tickets to events such as shows and concerts. Some argue there might be a potential for legal risk because the prizes that can be redeemed have real cash values. Additionally, some of the hotel stays and experiences won are at real casinos, which could feed a cycle of addictive gambling behaviors.

The company generates revenue primarily from the sale of in-game virtual currency, which players can purchase to enhance their playing experience (additional features, themes, game modes). PlayStudios also generates revenue through advertising and by partnering with real-world businesses to offer rewards to PlayStudios’s players. Businesses such as hotels, restaurants, and entertainment venues may pay PlayStudios for the right to be featured in games or to offer rewards.

4. Consumer Discretionary - Gaming Solutions

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare.

Gaming solutions companies provide the technology infrastructure behind gambling—slot machines, table game systems, lottery terminals, sports-betting platforms, and back-end software for casinos and online operators. Tailwinds include the ongoing legalization of sports betting across U.S. states and international markets, growing adoption of digital and mobile wagering, and casino operators' demand for data-driven player engagement tools. However, headwinds include stringent and evolving regulatory requirements across jurisdictions, high upfront R&D costs to develop next-generation platforms, and customer concentration risk given the limited number of large casino operators. Increasing competition from in-house technology development by major operators also pressures demand.

Competitors offering casual digital games that may feature casino-like activities include Skillz (NYSE:SKLZ), SciPlay (NASDAQ:SCPL), and Huuuge (WSE:HUG).

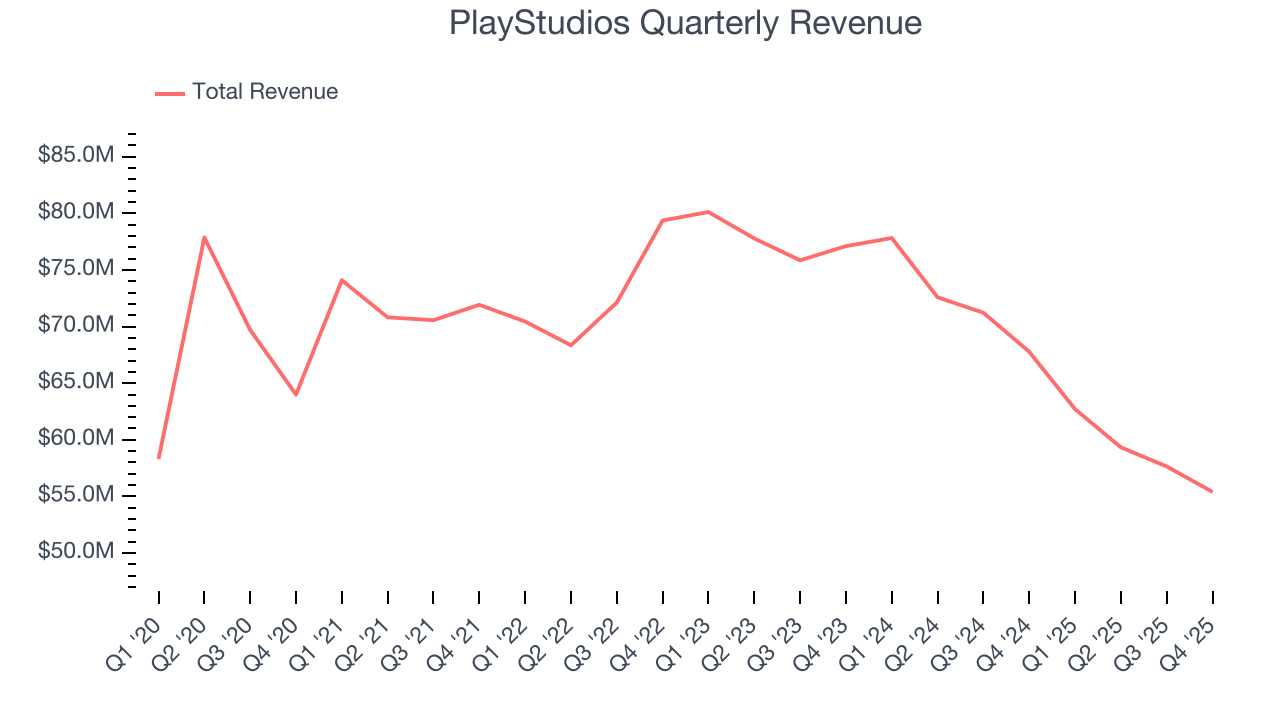

5. Revenue Growth

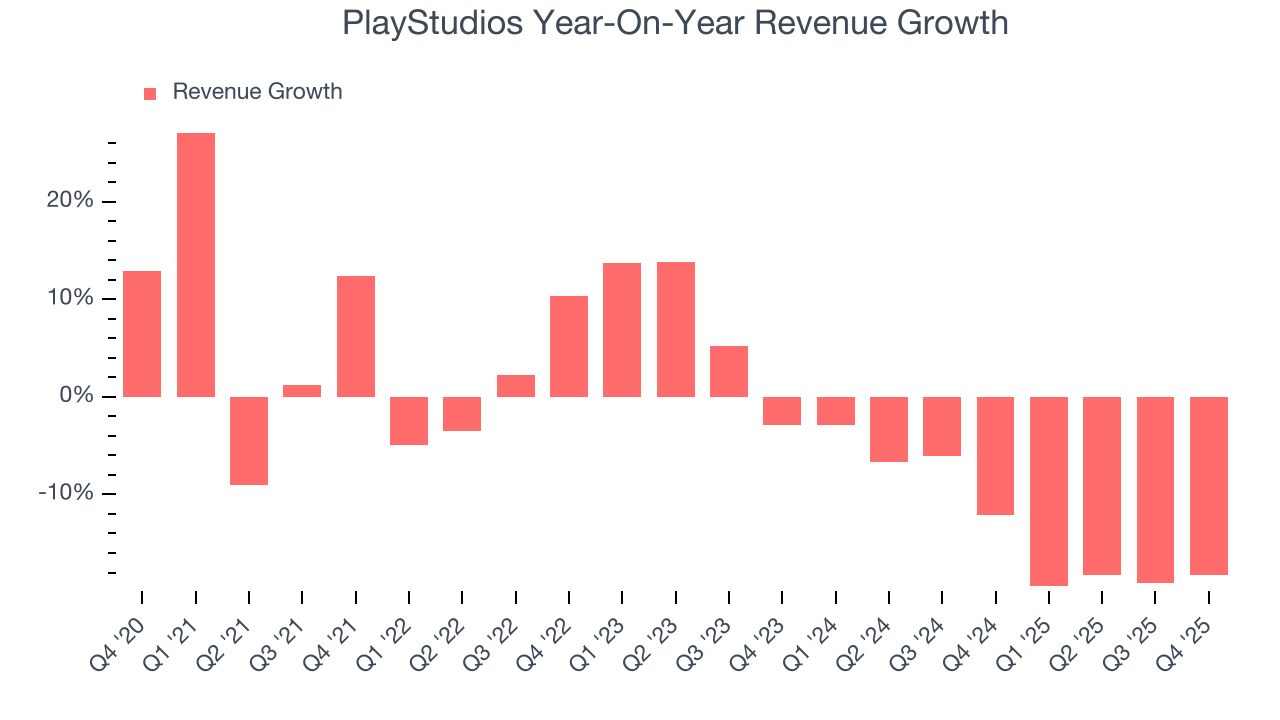

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. PlayStudios’s demand was weak over the last five years as its sales fell at a 2.7% annual rate. This was below our standards and suggests it’s a low quality business.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. PlayStudios’s recent performance shows its demand remained suppressed as its revenue has declined by 13% annually over the last two years.

This quarter, PlayStudios missed Wall Street’s estimates and reported a rather uninspiring 18.3% year-on-year revenue decline, generating $55.4 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 3.2% over the next 12 months. Although this projection indicates its newer products and services will catalyze better top-line performance, it is still below average for the sector.

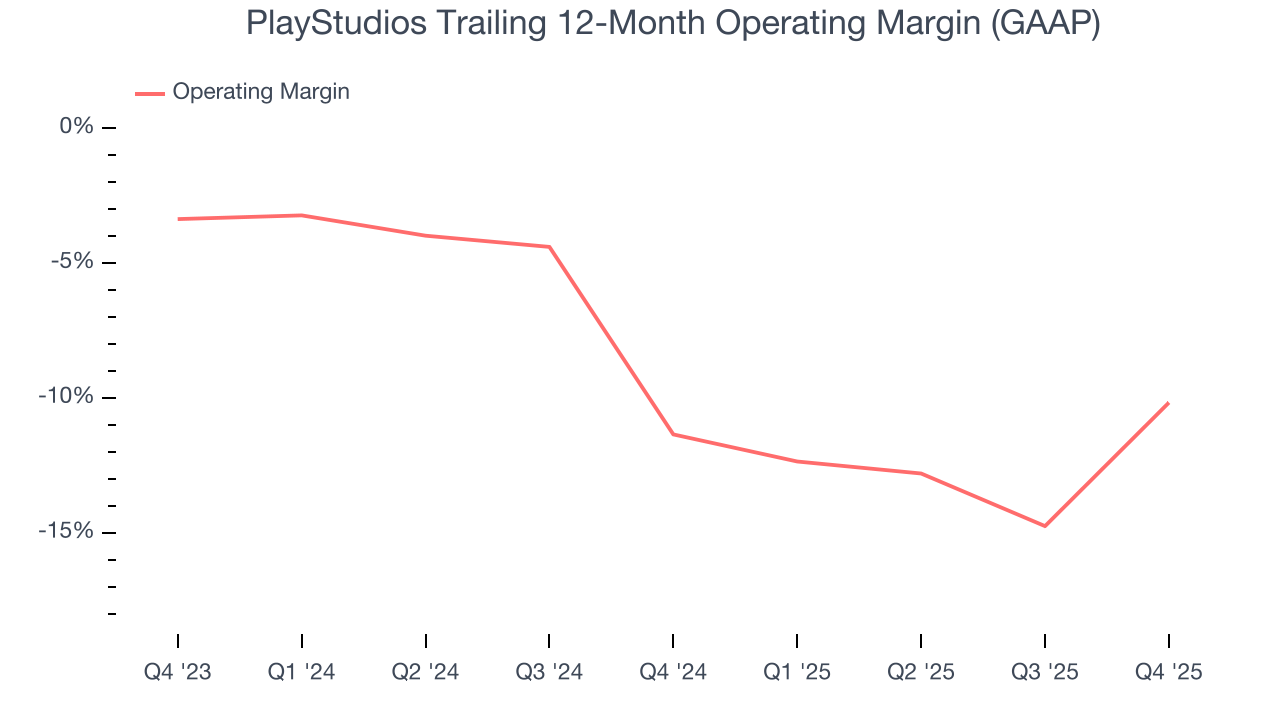

6. Operating Margin

PlayStudios’s operating margin has been trending up over the last 12 months, but it still averaged negative 10.8% over the last two years. This is due to its large expense base and inefficient cost structure.

In Q4, PlayStudios generated a negative 17.7% operating margin. The company's consistent lack of profits raise a flag.

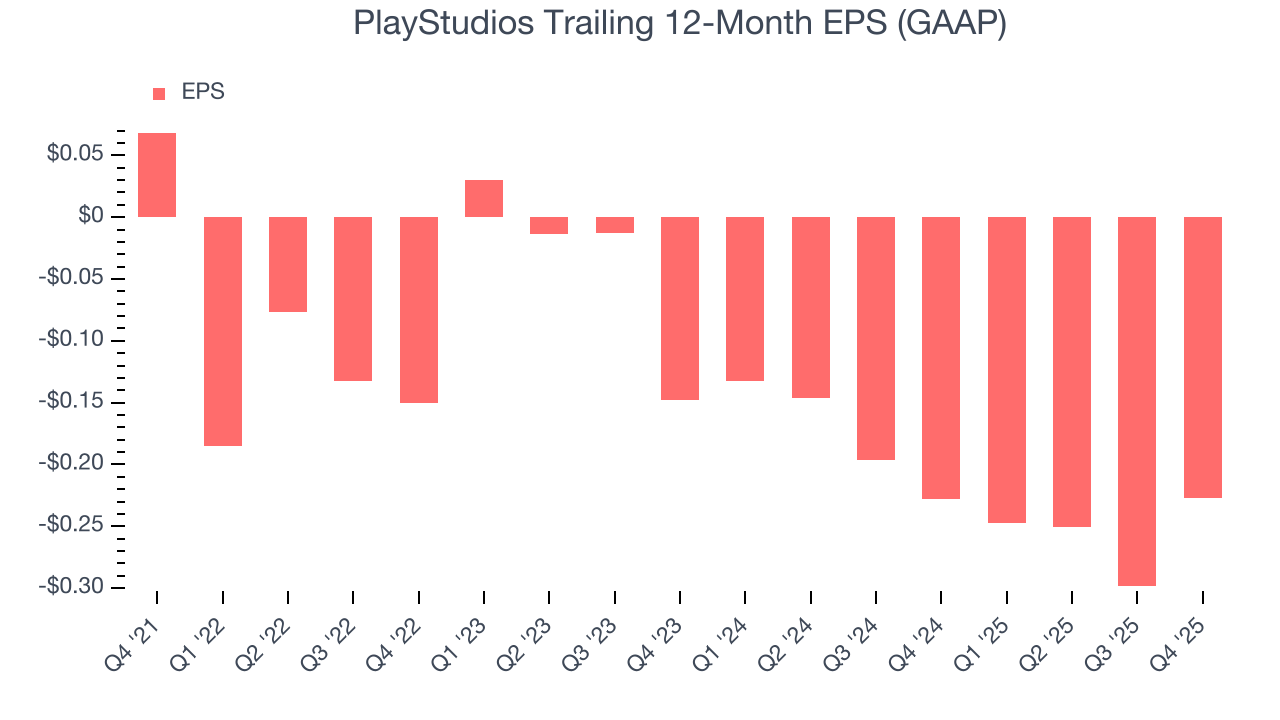

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

PlayStudios’s full-year EPS turned negative over the last four years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. Consumer Discretionary companies are particularly exposed to this, and if the tide turns unexpectedly, PlayStudios’s low margin of safety could leave its stock price susceptible to large downswings.

In Q4, PlayStudios reported EPS of negative $0.11, up from negative $0.18 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street expects PlayStudios to perform poorly. Analysts forecast its full-year EPS of negative $0.23 will tumble to negative $0.28.

8. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

PlayStudios has shown poor cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 12.8%, below what we’d expect for a consumer discretionary business.

PlayStudios’s free cash flow clocked in at $3.61 million in Q4, equivalent to a 6.5% margin. The company’s cash profitability regressed as it was 10.4 percentage points lower than in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

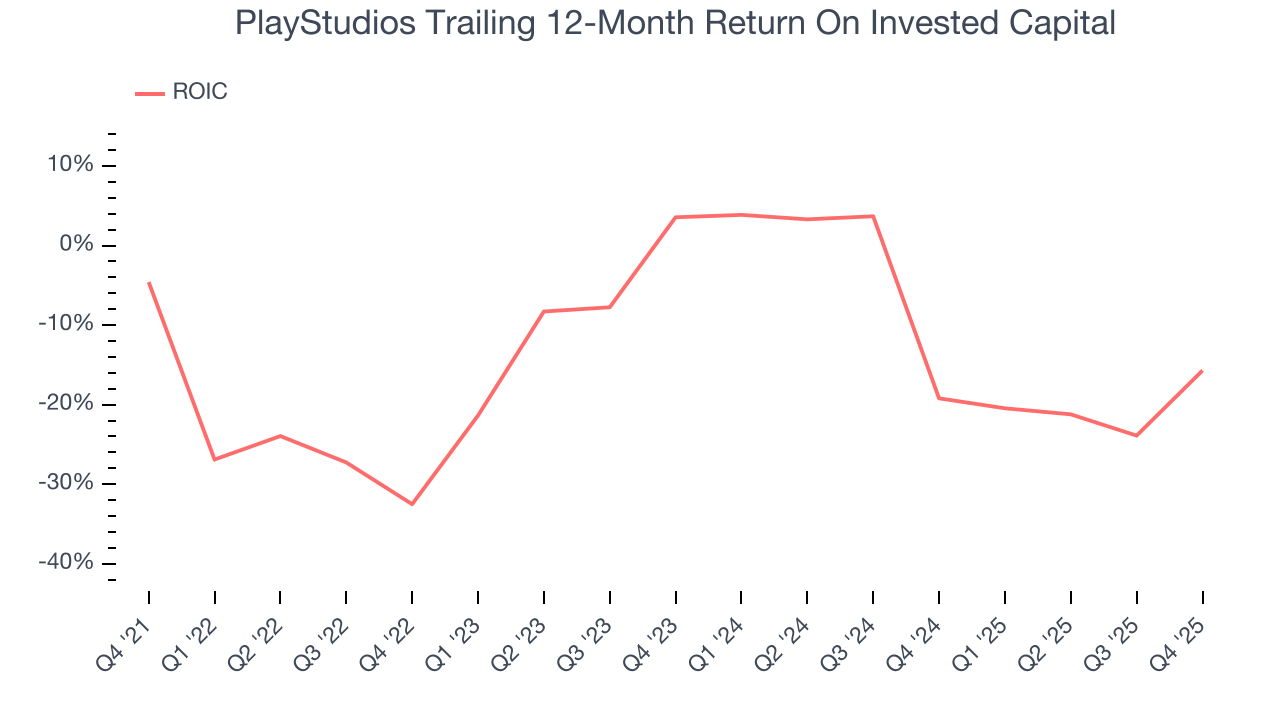

PlayStudios’s five-year average ROIC was negative 13.7%, meaning management lost money while trying to expand the business. Its returns were among the worst in the consumer discretionary sector.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Fortunately, PlayStudios’s ROIC averaged 1.1 percentage point increases each year over the last few years. This is a good sign, and we hope the company can continue improving.

10. Balance Sheet Assessment

Businesses that maintain a cash surplus face reduced bankruptcy risk.

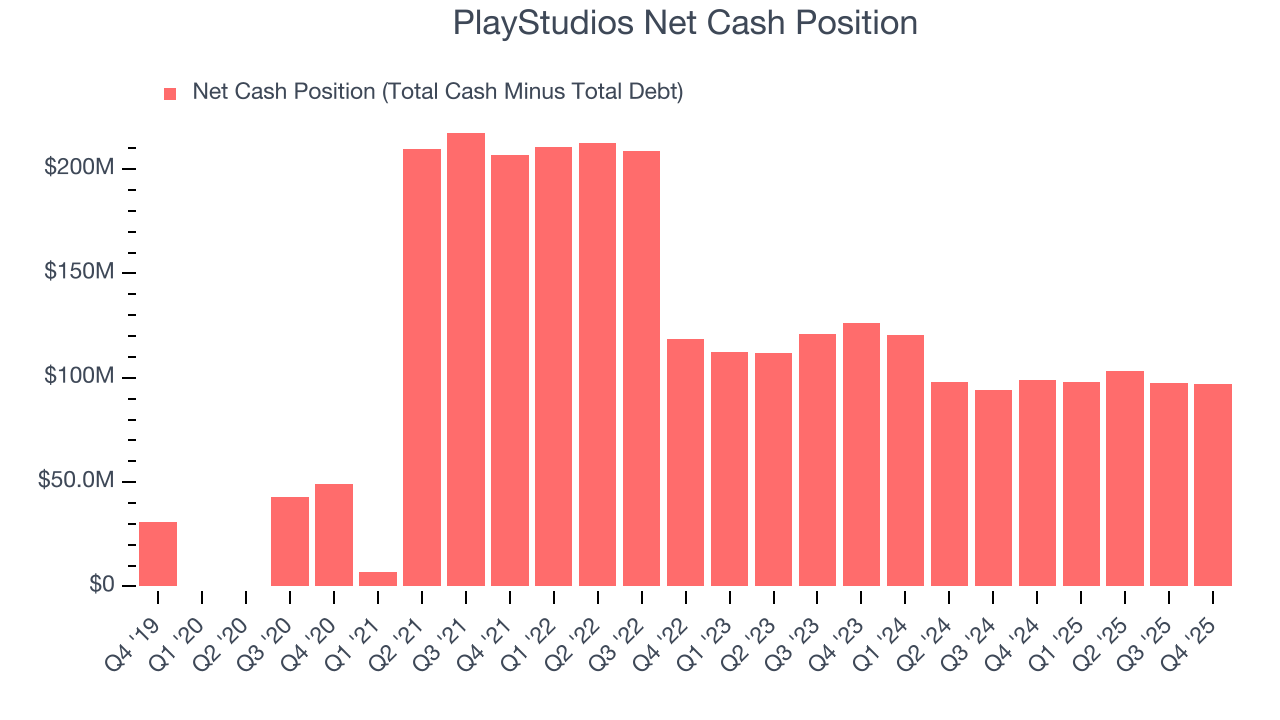

PlayStudios is a well-capitalized company with $104.9 million of cash and $7.73 million of debt on its balance sheet. This $97.21 million net cash position is 152% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

11. Key Takeaways from PlayStudios’s Q4 Results

We struggled to find many positives in these results. Its adjusted operating income missed and its EBITDA fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock remained flat at $0.52 immediately after reporting.

12. Is Now The Time To Buy PlayStudios?

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in PlayStudios.

PlayStudios falls short of our quality standards. On top of that, PlayStudios’s declining EPS over the last four years makes it a less attractive asset to the public markets, and its projected EPS for the next year is lacking.

PlayStudios’s forward price-to-sales ratio is 0.3x. The market typically values companies like PlayStudios based on their anticipated profits for the next 12 months, but it expects the business to lose money. We also think the upside isn’t great compared to the potential downside here - there are more exciting stocks to buy.

Wall Street analysts have a consensus one-year price target of $1.50 on the company (compared to the current share price of $0.52).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.