The Marzetti Company (MZTI)

We’re skeptical of The Marzetti Company. Its weak revenue growth and gross margin show it not only lacks demand but also decent unit economics.― StockStory Analyst Team

1. News

2. Summary

Why The Marzetti Company Is Not Exciting

Known for its frozen garlic bread and Parkerhouse rolls, The Marzetti Company (NASDAQ:MZTI) sells bread, dressing, and dips to the retail and food service channels.

- Estimated sales growth of 1.1% for the next 12 months implies demand will slow from its three-year trend

- 3.2% annual revenue growth over the last three years was slower than its consumer staples peers

- On the plus side, its robust free cash flow profile gives it the flexibility to invest in growth initiatives or return capital to shareholders, and its growing cash flow gives it even more resources to deploy

The Marzetti Company’s quality isn’t great. There are more profitable opportunities elsewhere.

Why There Are Better Opportunities Than The Marzetti Company

The Marzetti Company’s stock price of $161.59 implies a valuation ratio of 23.9x forward P/E. Not only does The Marzetti Company trade at a premium to companies in the consumer staples space, but this multiple is also high for its top-line growth.

There are stocks out there similarly priced with better business quality. We prefer owning these.

3. The Marzetti Company (MZTI) Research Report: Q4 CY2025 Update

Specialty food company The Marzetti Company (NASDAQ:MZTI) met Wall Streets revenue expectations in Q4 CY2025, with sales up 1.7% year on year to $518 million. Its GAAP profit of $2.15 per share was 3.4% below analysts’ consensus estimates.

The Marzetti Company (MZTI) Q4 CY2025 Highlights:

- Revenue: $518 million vs analyst estimates of $519.6 million (1.7% year-on-year growth, in line)

- EPS (GAAP): $2.15 vs analyst expectations of $2.23 (3.4% miss)

- Operating Margin: 14.5%, in line with the same quarter last year

- Sales Volumes fell 3.1% year on year (6% in the same quarter last year)

- Market Capitalization: $4.78 billion

Company Overview

Known for its frozen garlic bread and Parkerhouse rolls, The Marzetti Company (NASDAQ:MZTI) sells bread, dressing, and dips to the retail and food service channels.

The company was founded in 1961 as a glass and automotive products company. However, it quickly shifted focus towards specialty foods. Since its inception, Lancaster Colony (now The Marzetti Company) has grown both organically and through a series of acquisitions, with its purchase of salad dressings giant Marzetti in 1969 as one of the most significant.

In addition to Marzetti dressings, the company goes to market with the Sister Schubert brand of rolls and the New York Brand Bakery brand of garlic breads, croutons, and toasts. The company sells to the retail channel, where its dressings and dips products can be found in grocery produce departments and where other products can be found in the shelf-stable sections. It also sells private-label products to restaurants.

At retail, the core customer is likely someone who does the grocery shopping for his or her household. This customer values convenience, as he or she has little time between work, kids, and other commitments to make food from scratch. Those who buy the company’s dressings are likely also health conscious and use the products to add some pizzazz to their salads.

4. Shelf-Stable Food

As America industrialized and moved away from an agricultural economy, people faced more demands on their time. Packaged foods emerged as a solution offering convenience to the evolving American family, whether it be canned goods or snacks. Today, Americans seek brands that are high in quality, reliable, and reasonably priced. Furthermore, there's a growing emphasis on health-conscious and sustainable food options. Packaged food stocks are considered resilient investments. People always need to eat, so these companies can enjoy consistent demand as long as they stay on top of changing consumer preferences. The industry spans from multinational corporations to smaller specialized firms and is subject to food safety and labeling regulations.

Competitors in specialty foods include Treehouse Foods (NYSE:THS), Flowers Foods (NYSE:FLO), and Clorox (NYSE;CLX), which owns the Hidden Valley dressing brand.

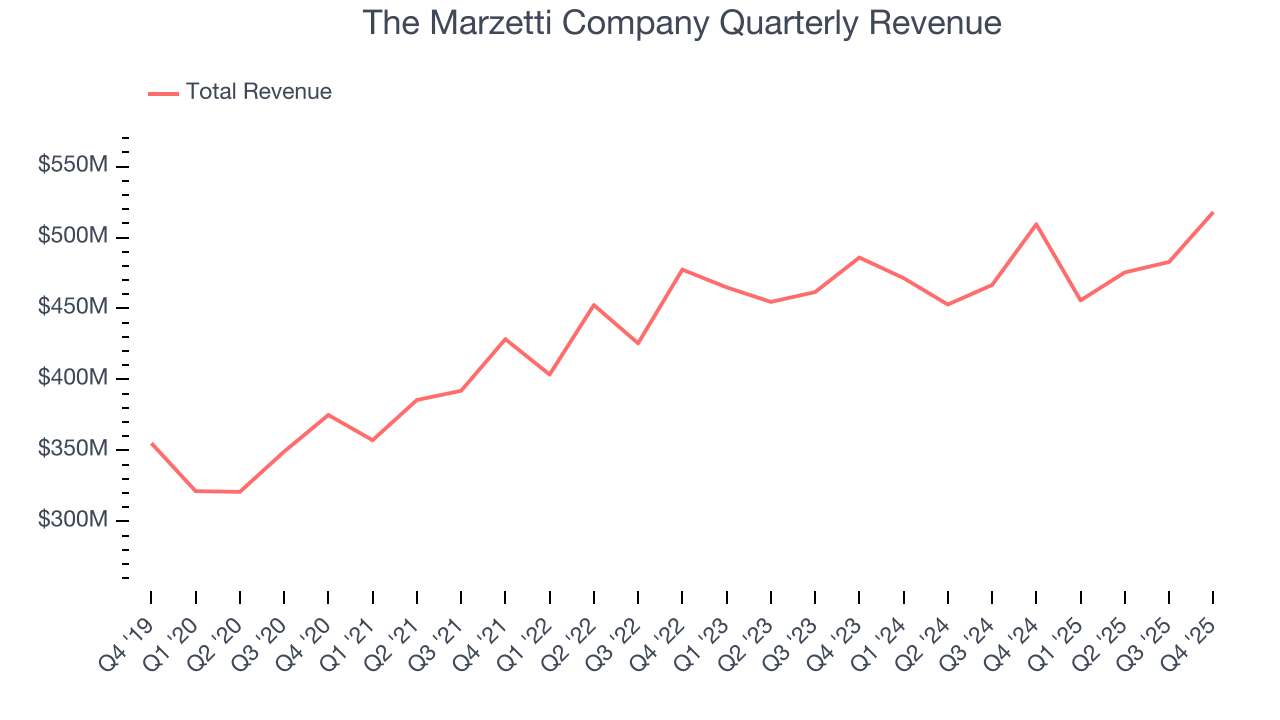

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years.

With $1.93 billion in revenue over the past 12 months, The Marzetti Company is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

As you can see below, The Marzetti Company’s sales grew at a sluggish 3.2% compounded annual growth rate over the last three years, but to its credit, consumers bought more of its products.

This quarter, The Marzetti Company grew its revenue by 1.7% year on year, and its $518 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 2.1% over the next 12 months, similar to its three-year rate. This projection is underwhelming and implies its products will see some demand headwinds.

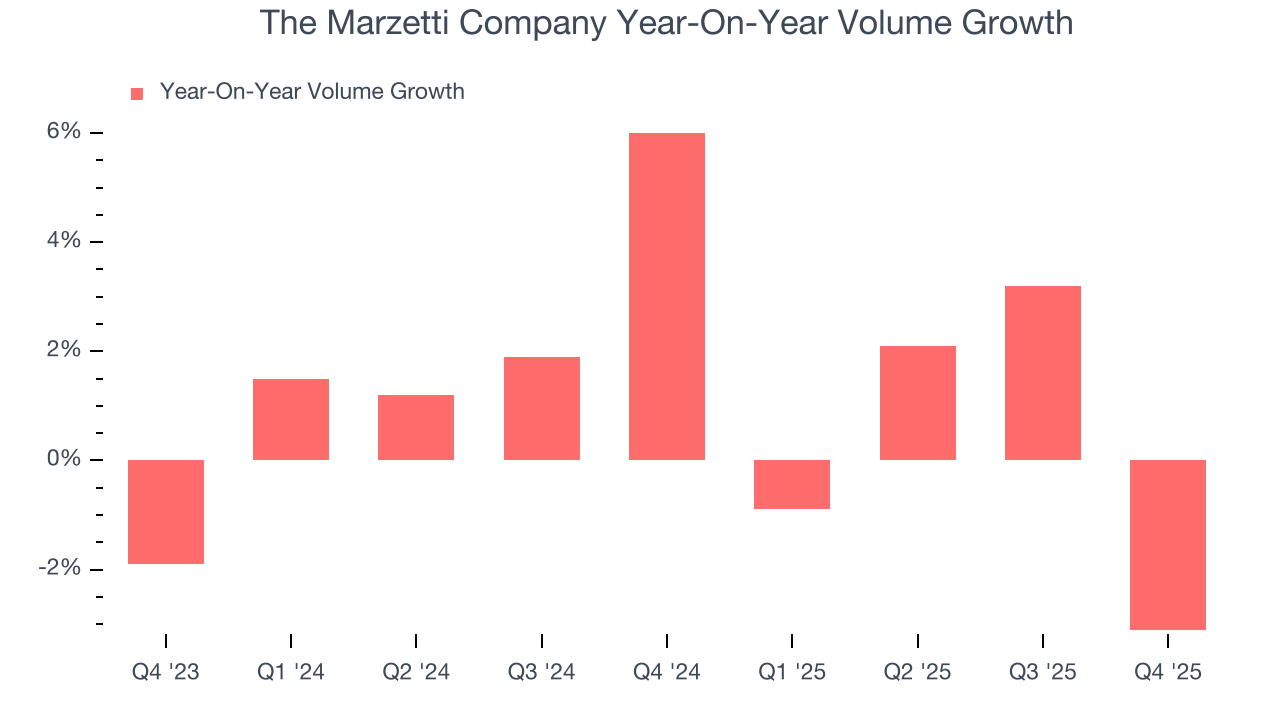

6. Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

The Marzetti Company’s average quarterly volume growth was a healthy 1.5% over the last two years. This is pleasing because it shows consumers are purchasing more of its products.

In The Marzetti Company’s Q4 2026, sales volumes dropped 3.1% year on year. This result was a reversal from its historical levels.

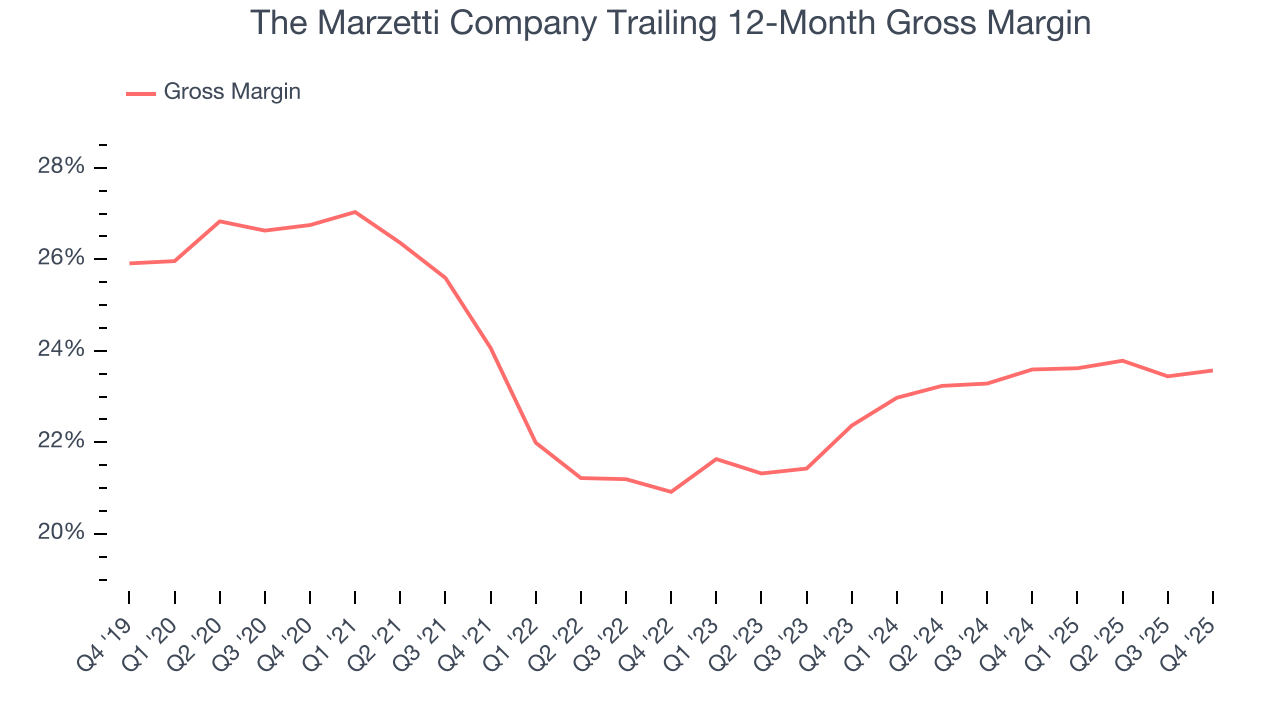

7. Gross Margin & Pricing Power

The Marzetti Company has bad unit economics for a consumer staples company, giving it less room to reinvest and develop new products. As you can see below, it averaged a 23.6% gross margin over the last two years. Said differently, for every $100 in revenue, a chunky $76.42 went towards paying for raw materials, production of goods, transportation, and distribution.

The Marzetti Company’s gross profit margin came in at 26.5% this quarter, in line with the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

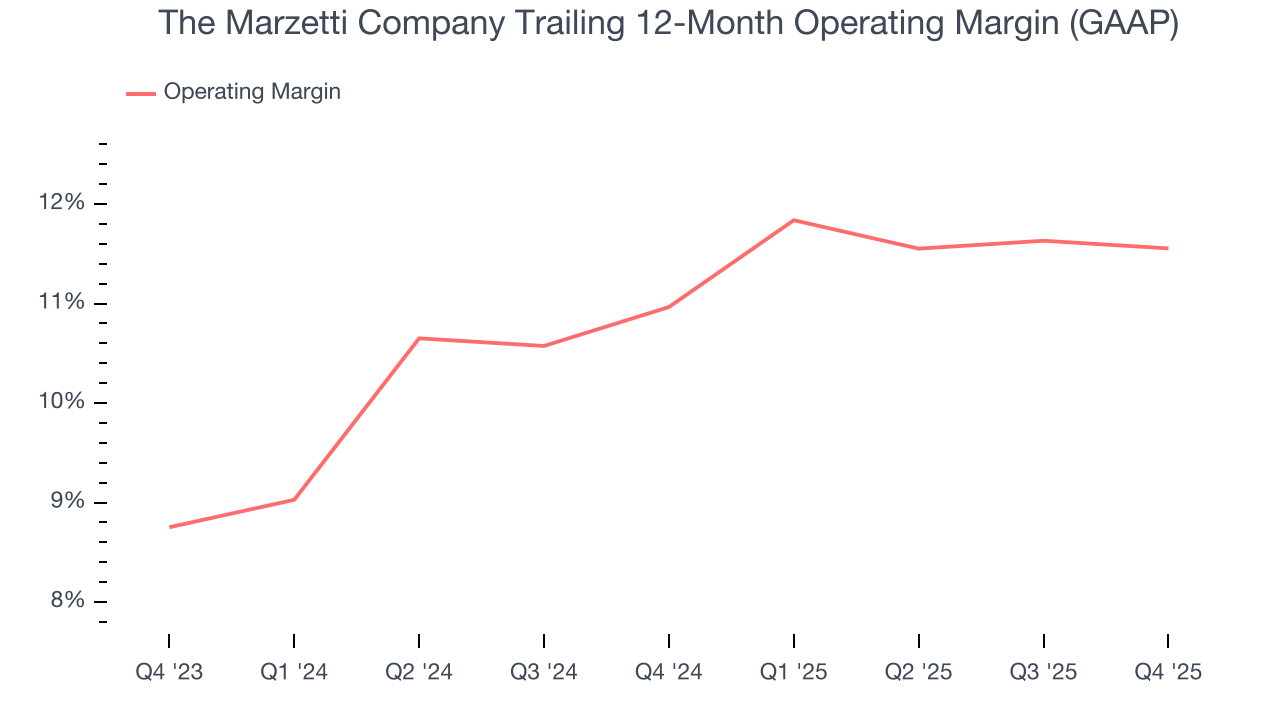

8. Operating Margin

The Marzetti Company’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 11.3% over the last two years. This profitability was solid for a consumer staples business and shows it’s an efficient company that manages its expenses well. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Looking at the trend in its profitability, The Marzetti Company’s operating margin might fluctuated slightly but has generally stayed the same over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, The Marzetti Company generated an operating margin profit margin of 14.5%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

9. Earnings Per Share

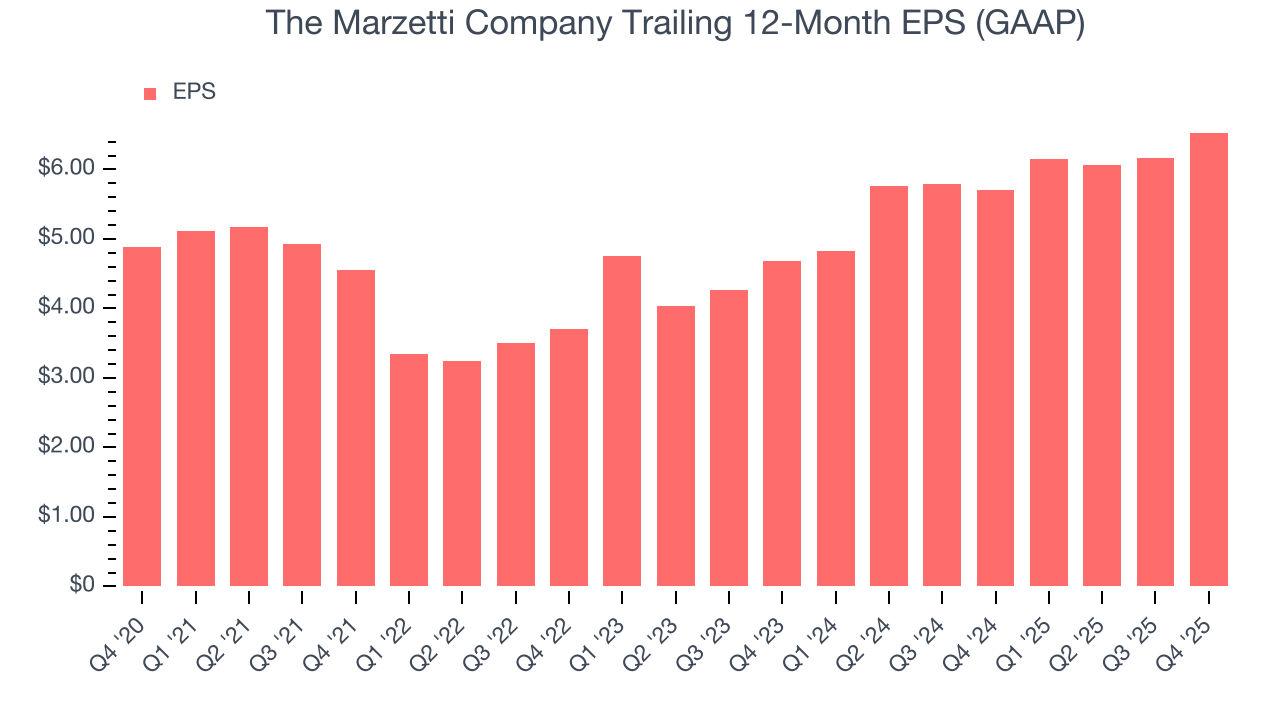

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

The Marzetti Company’s EPS grew at a spectacular 20.8% compounded annual growth rate over the last three years, higher than its 3.2% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

In Q4, The Marzetti Company reported EPS of $2.15, up from $1.78 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects The Marzetti Company’s full-year EPS of $6.53 to grow 10.8%.

10. Cash Is King

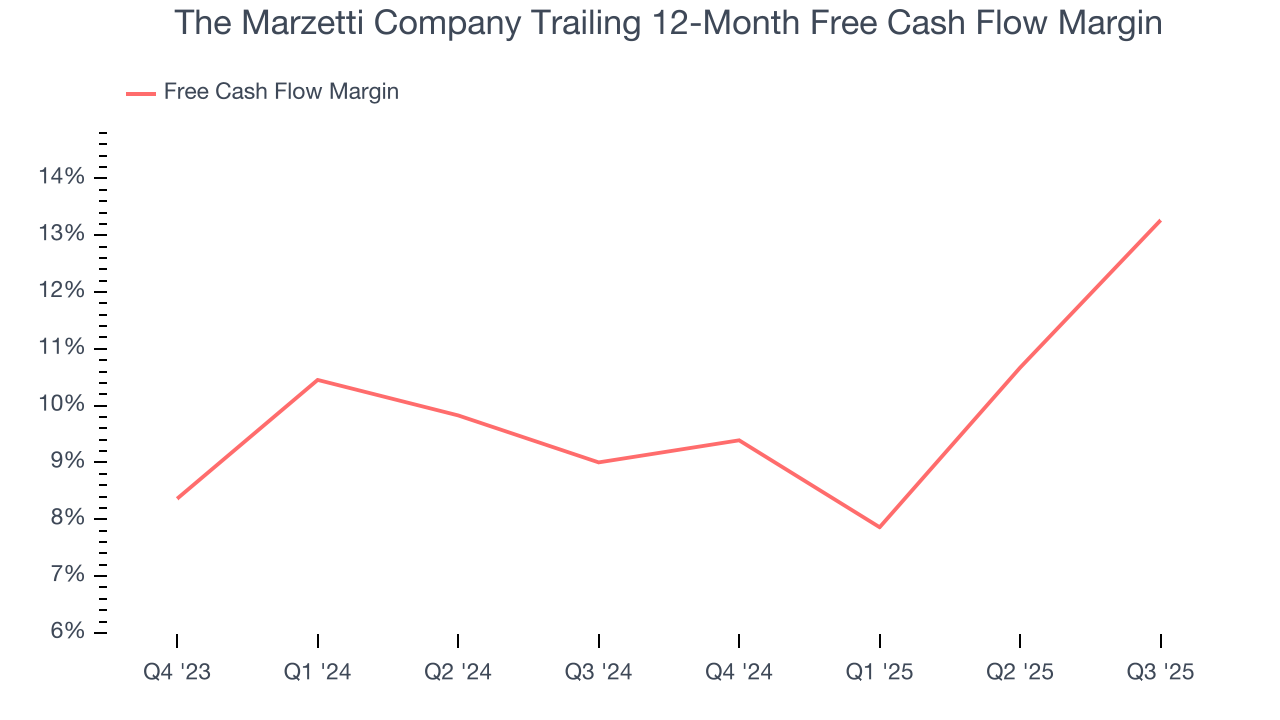

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

The Marzetti Company has shown robust cash profitability, giving it an edge over its competitors and the ability to reinvest or return capital to investors. The company’s free cash flow margin averaged 10.2% over the last two years, quite impressive for a consumer staples business.

11. Return on Invested Capital (ROIC)

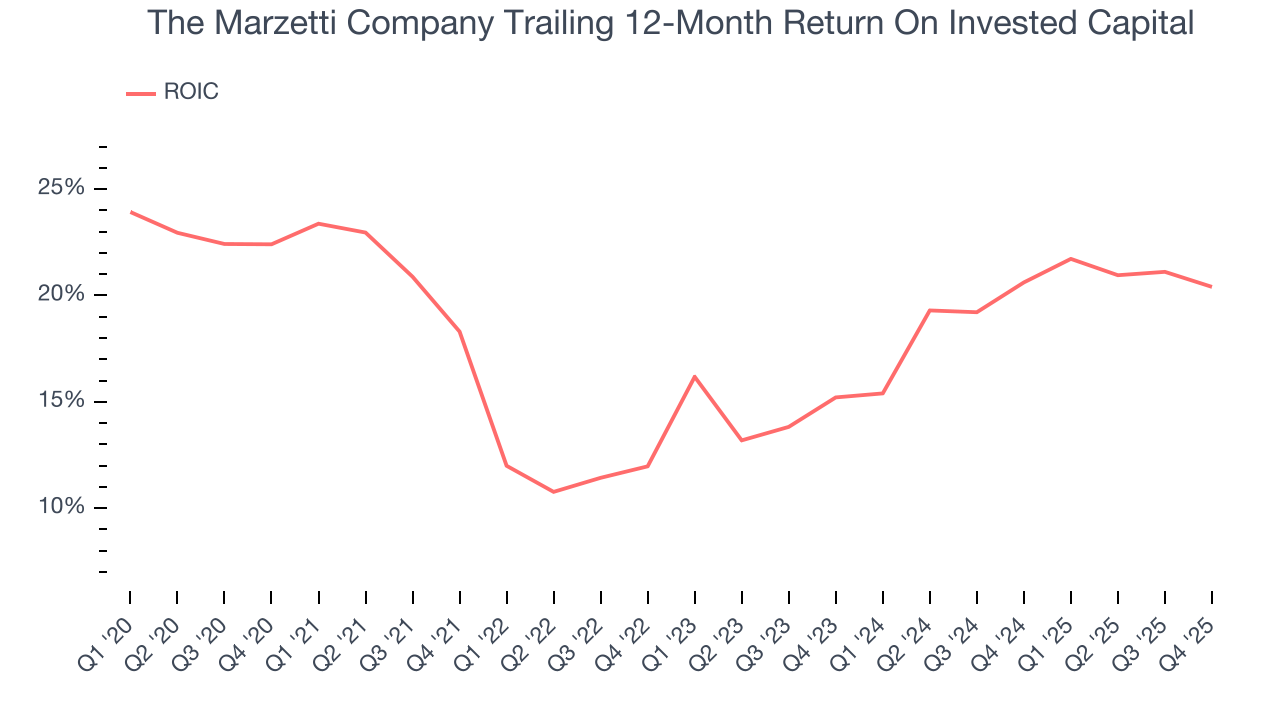

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although The Marzetti Company hasn’t been the highest-quality company lately because of its poor top-line performance, it historically found a few growth initiatives that worked. Its five-year average ROIC was 17.3%, higher than most consumer staples businesses.

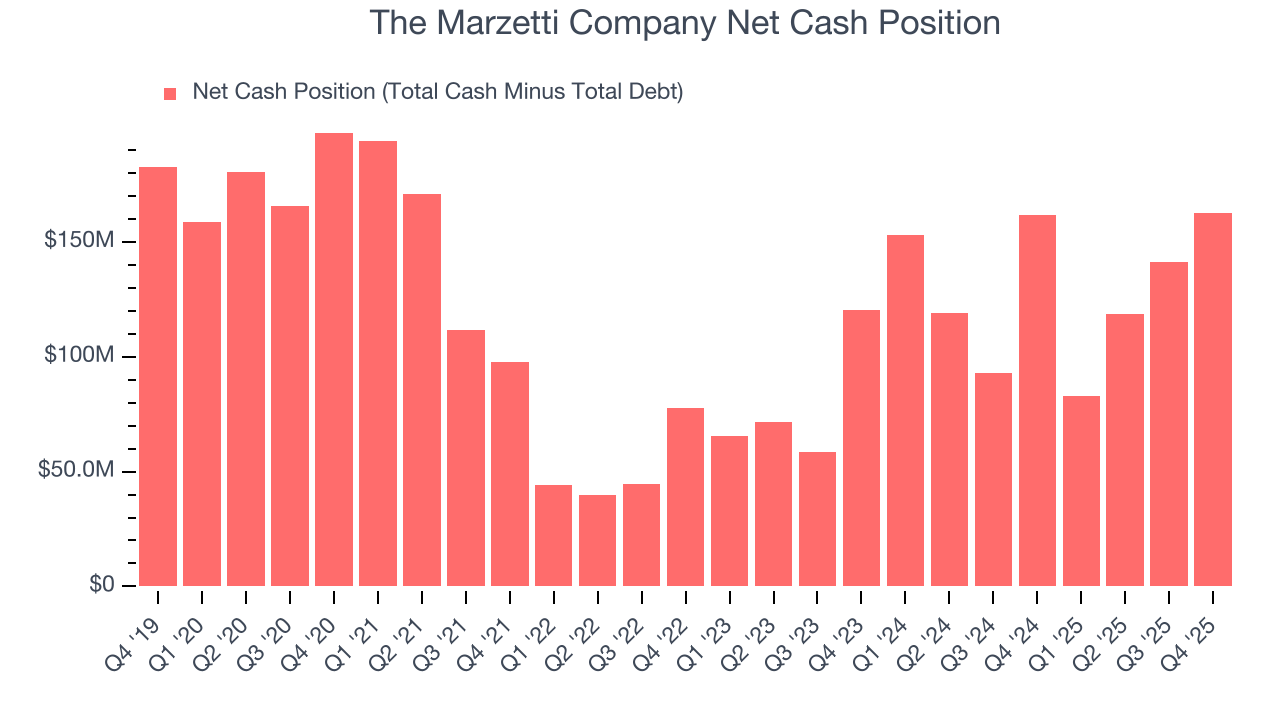

12. Balance Sheet Assessment

Companies with more cash than debt have lower bankruptcy risk.

The Marzetti Company is a profitable, well-capitalized company with $201.6 million of cash and $38.77 million of debt on its balance sheet. This $162.8 million net cash position is 3.7% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

13. Key Takeaways from The Marzetti Company’s Q4 Results

We struggled to find many positives in these results. Overall, this quarter could have been better. The stock remained flat at $174.08 immediately following the results.

14. Is Now The Time To Buy The Marzetti Company?

Updated: February 3, 2026 at 9:57 PM EST

Are you wondering whether to buy The Marzetti Company or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

The Marzetti Company isn’t a terrible business, but it doesn’t pass our bar. To begin with, its revenue growth was uninspiring over the last three years, and analysts expect its demand to deteriorate over the next 12 months. And while its strong free cash flow generation allows it to invest in growth initiatives while maintaining an ample cushion, the downside is its gross margins make it more difficult to reach positive operating profits compared to other consumer staples businesses. On top of that, its brand caters to a niche market.

The Marzetti Company’s P/E ratio based on the next 12 months is 24x. Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $197.20 on the company (compared to the current share price of $161.59).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.