Navient (NAVI)

We wouldn’t buy Navient. Its sales and profitability have plummeted, suggesting it struggled to scale down its costs as demand faded.― StockStory Analyst Team

1. News

2. Summary

Why We Think Navient Will Underperform

Spun off from Sallie Mae in 2014 to handle the company's loan servicing and collection operations, Navient (NASDAQ:NAVI) provides education loan servicing and business processing solutions that help manage federal student loans, private education loans, and government services.

- Sales tumbled by 18.7% annually over the last five years, showing market trends are working against its favor during this cycle

- Earnings per share have contracted by 17.1% annually over the last five years, a headwind for returns as stock prices often echo long-term EPS performance

Navient is in the doghouse. You should search for better opportunities.

Why There Are Better Opportunities Than Navient

Navient is trading at $12.08 per share, or 11.2x forward P/E. This multiple is lower than most financials companies, but for good reason.

We’d rather pay up for companies with elite fundamentals than get a bargain on weak ones. Cheap stocks can be value traps, and as their performance deteriorates, they will stay cheap or get even cheaper.

3. Navient (NAVI) Research Report: Q4 CY2025 Update

Student loan servicer Navient (NASDAQ:NAVI) missed Wall Street’s revenue expectations in Q4 CY2025, with sales falling 16% year on year to $137 million. Its GAAP loss of $0.06 per share was significantly below analysts’ consensus estimates.

Navient (NAVI) Q4 CY2025 Highlights:

- Net Interest Income: $118 million vs analyst estimates of $133.3 million

- Revenue: $137 million vs analyst estimates of $155.8 million (16% year-on-year decline, 12.1% miss)

- Pre-tax Profit: -$7 million (-5.1% margin)

- EPS (GAAP): -$0.06 vs analyst estimates of $0.32 (significant miss)

- Market Capitalization: $1.17 billion

Company Overview

Spun off from Sallie Mae in 2014 to handle the company's loan servicing and collection operations, Navient (NASDAQ:NAVI) provides education loan servicing and business processing solutions that help manage federal student loans, private education loans, and government services.

Navient operates through three main business segments. Its Federal Education Loans segment owns and services a portfolio of federally guaranteed loans under the Federal Family Education Loan Program (FFELP), generating revenue primarily through interest income on these loans. The Consumer Lending segment focuses on private education loans, including both refinancing existing student debt and originating new in-school loans through its Earnest and NaviRefi brands. These digital platforms help students find scholarships, compare financial aid offers, and secure lower interest rates on their education debt.

The company's third segment, Business Processing, leverages Navient's expertise in loan servicing to provide outsourced solutions to approximately 500 government and healthcare clients. These services include contact center operations, workflow processing, and revenue cycle management. Government clients range from federal agencies to state governments and tolling authorities, while healthcare clients include hospitals, medical centers, and physician groups.

Navient's technology infrastructure handles millions of complex transactions daily, using data-driven approaches to simplify customer experiences. For example, a recent college graduate struggling with federal loan payments might interact with Navient's systems to explore income-driven repayment options, while a hospital might use Navient's services to optimize patient billing processes and improve collection rates.

The company operates under significant regulatory oversight, including supervision by the Consumer Financial Protection Bureau (CFPB), the Department of Education, and various state agencies. This regulatory environment requires Navient to maintain comprehensive compliance systems covering everything from fair lending practices to consumer privacy protections.

4. Student Loan

Student loan providers finance higher education expenses. Growth opportunities exist in private loan offerings, refinancing existing debt, and international education funding. Challenges include political uncertainty around potential loan forgiveness programs, default risk correlation with employment markets, and increasing scrutiny of educational outcomes relative to debt burdens.

Navient's competitors include Nelnet (NYSE:NNI) in the student loan servicing space, Maximus (NYSE:MMS) in government services, and R1 RCM (NASDAQ:RCM) in healthcare revenue cycle management. The company also competes with SoFi (NASDAQ:SOFI) and Discover Financial Services (NYSE:DFS) in private student lending.

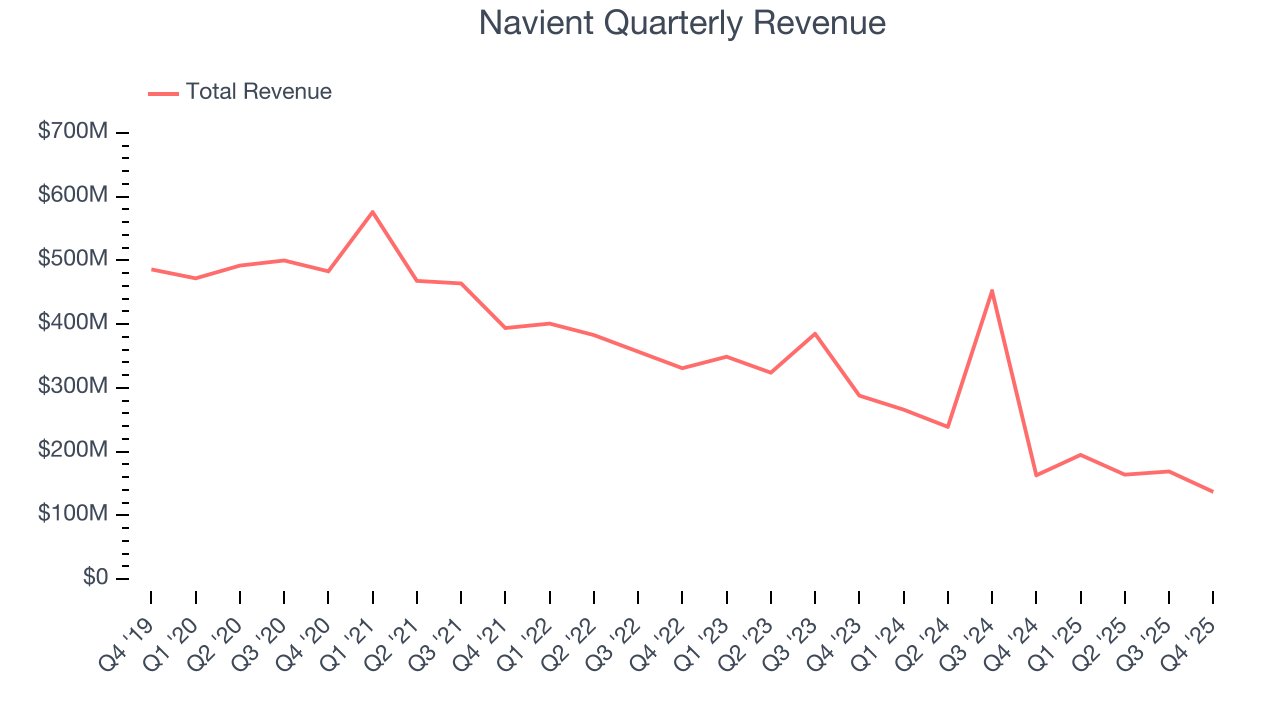

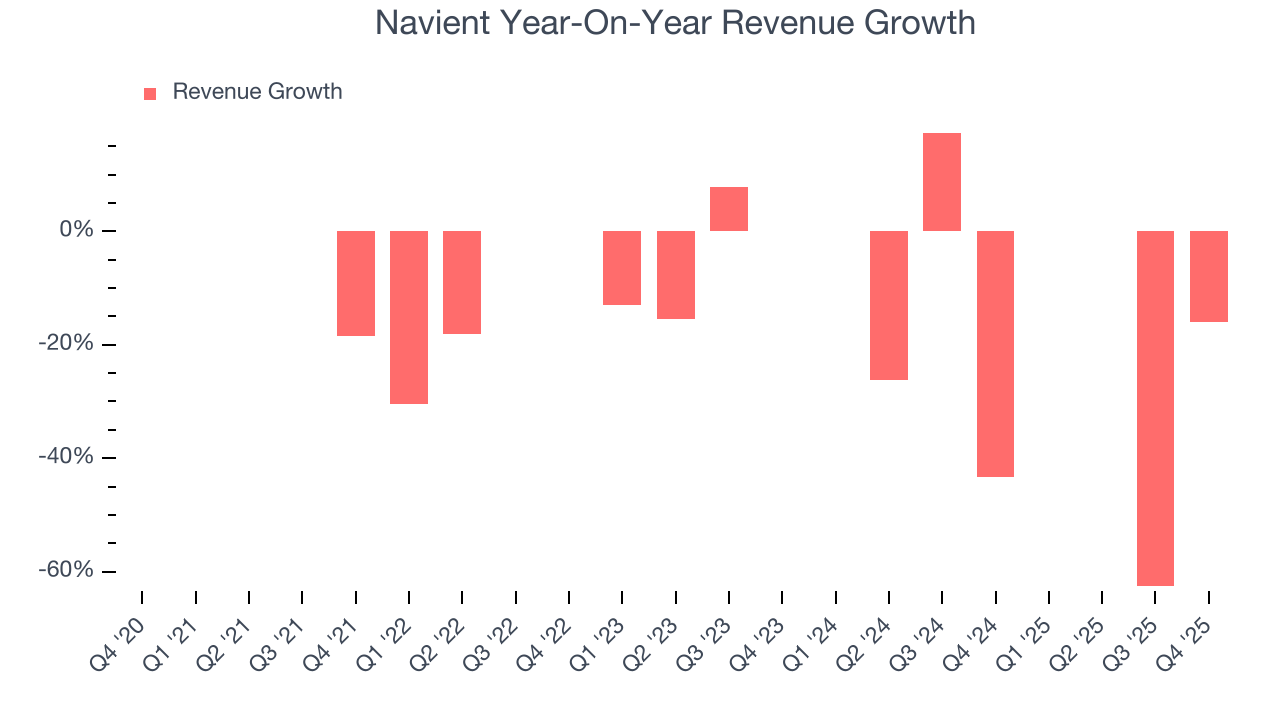

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Navient’s demand was weak over the last five years as its revenue fell at a 19.3% annual rate. This was below our standards and is a sign of poor business quality.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Navient’s recent performance shows its demand remained suppressed as its revenue has declined by 29.7% annually over the last two years.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Navient missed Wall Street’s estimates and reported a rather uninspiring 16% year-on-year revenue decline, generating $137 million of revenue.

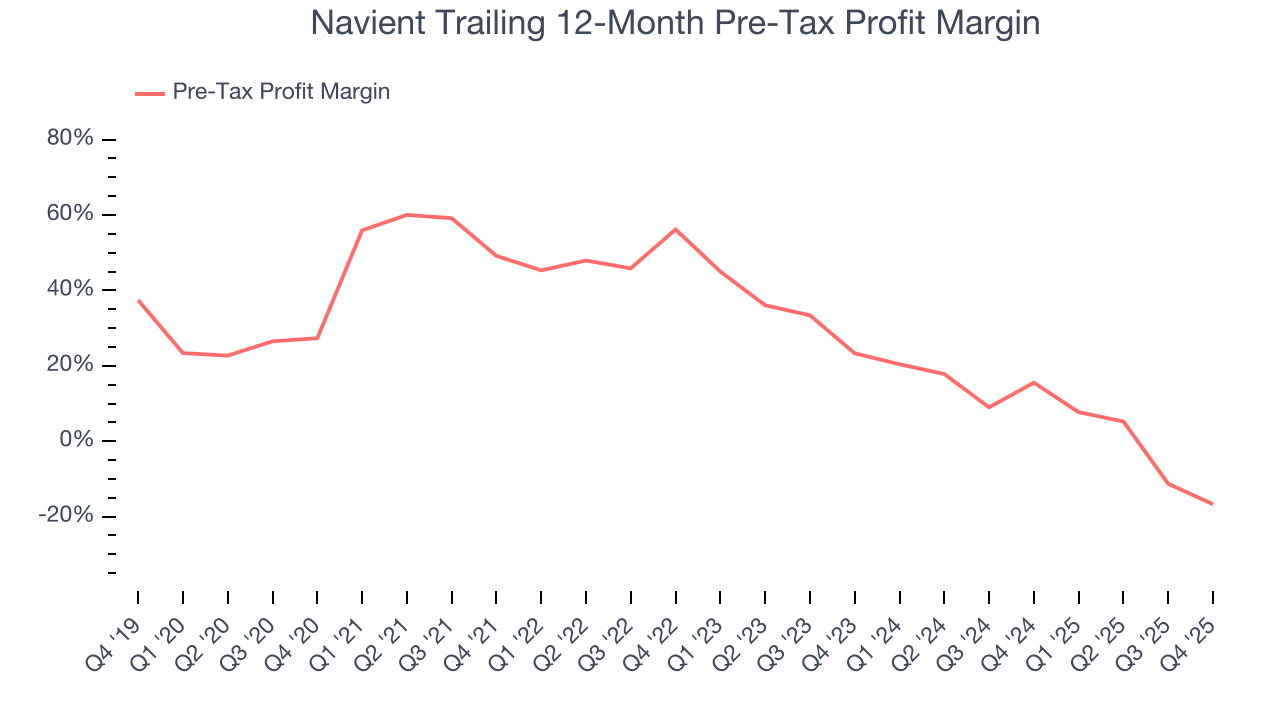

6. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For Student Loan companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

The pre-tax profit margin includes interest because it's central to how financial institutions generate revenue and manage costs. Tax considerations are excluded since they represent government policy rather than operational performance, giving investors a clearer view of business fundamentals.

Over the last five years, Navient’s pre-tax profit margin has risen by 44 percentage points, going from 49.2% to negative 16.7%. It has also declined by 40 percentage points on a two-year basis, showing its expenses have consistently increased at a faster rate than revenue. This usually raises questions unless the company is in high-growth mode and reinvesting its profits into attractive ventures.

Navient’s pre-tax profit margin came in at negative 5.1% this quarter. This result was 21.1 percentage points worse than the same quarter last year.

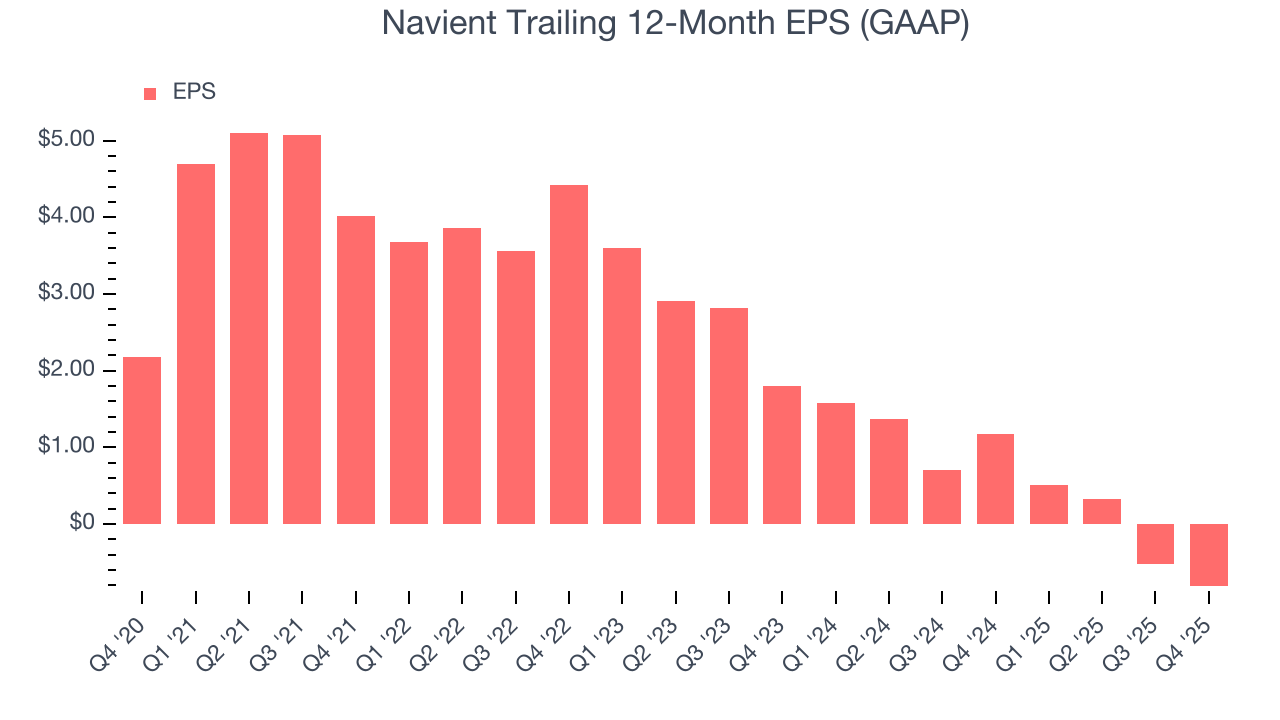

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Navient, its EPS and revenue declined by 18.9% and 19.3% annually over the last five years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Navient’s low margin of safety could leave its stock price susceptible to large downswings.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Navient, its two-year annual EPS declines of 56.6% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, Navient reported EPS of negative $0.06, down from $0.23 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast Navient’s full-year EPS of negative $0.81 will flip to positive $1.18.

8. Return on Equity

Return on equity, or ROE, quantifies bank profitability relative to shareholder equity - an essential capital source for these institutions. Over extended periods, superior ROE performance drives faster shareholder wealth compounding through reinvestment, share repurchases, and dividend growth.

Over the last five years, Navient has averaged an ROE of 12.5%, respectable for a company operating in a sector where the average shakes out around 10% and those putting up 25%+ are greatly admired.

9. Balance Sheet Risk

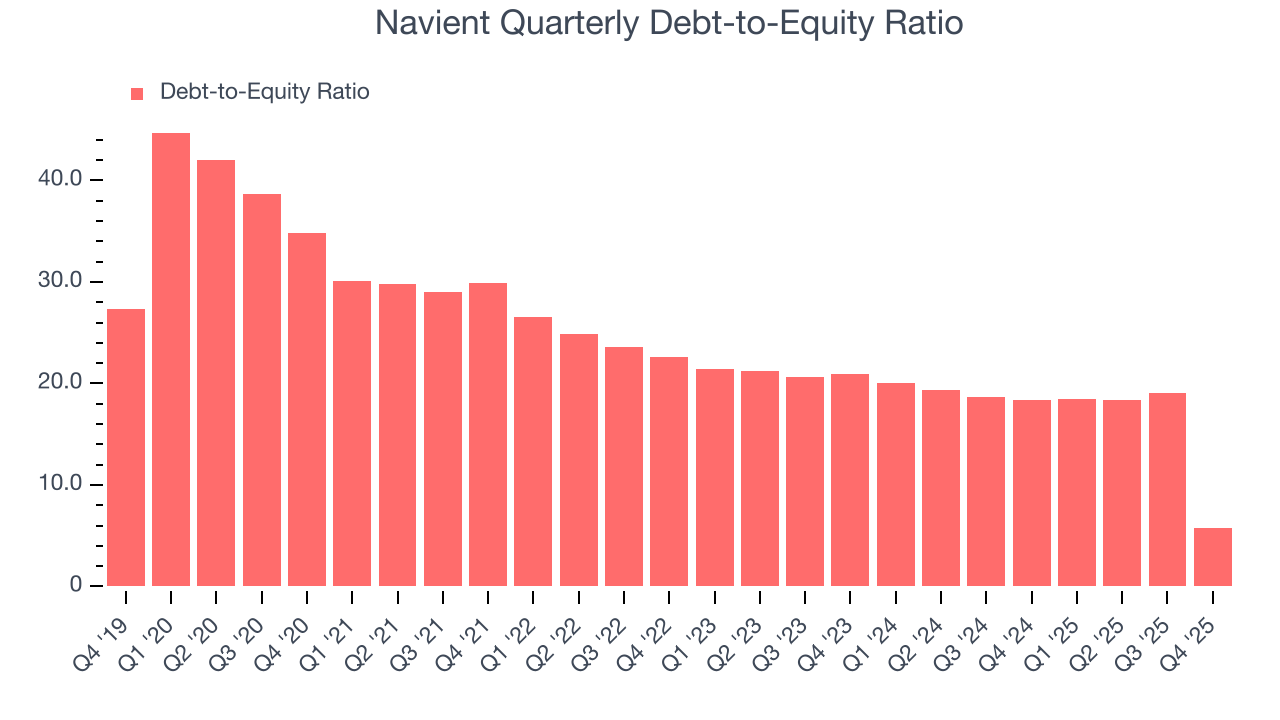

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

Navient currently has $45.71 billion of debt and $7.96 billion of shareholder's equity on its balance sheet, and over the past four quarters, has averaged a debt-to-equity ratio of 15.4×. We think this is dangerous - for a financials business, anything above 3.5× raises red flags.

10. Key Takeaways from Navient’s Q4 Results

We struggled to find many positives in these results. Its net interest income missed and its revenue fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock remained flat at $12.08 immediately following the results.

11. Is Now The Time To Buy Navient?

Updated: January 28, 2026 at 7:53 AM EST

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Navient, you should also grasp the company’s longer-term business quality and valuation.

We see the value of companies driving economic growth, but in the case of Navient, we’re out. To kick things off, its revenue has declined over the last five years. And while its above-average ROE suggests its management team has made good investment decisions, the downside is its declining pre-tax profit margin shows the business has become less efficient. On top of that, its declining EPS over the last five years makes it a less attractive asset to the public markets.

Navient’s P/E ratio based on the next 12 months is 10.2x. This multiple tells us a lot of good news is priced in - we think there are better opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $13.06 on the company (compared to the current share price of $12.08).