Northwest Pipe (NWPX)

We see potential in Northwest Pipe. Its rising free cash flow margin gives it more chips to play with.― StockStory Analyst Team

1. News

2. Summary

Why Northwest Pipe Is Interesting

Playing a large role in the Integrated Pipeline (IPL) project in Texas to deliver ~350 million gallons of water per day, Northwest Pipe (NASDAQ:NWPX) is a manufacturer of pipeline systems for water infrastructure.

- Annual revenue growth of 13% over the last five years was superb and indicates its market share increased during this cycle

- Earnings per share grew by 11.1% annually over the last five years and topped the peer group average

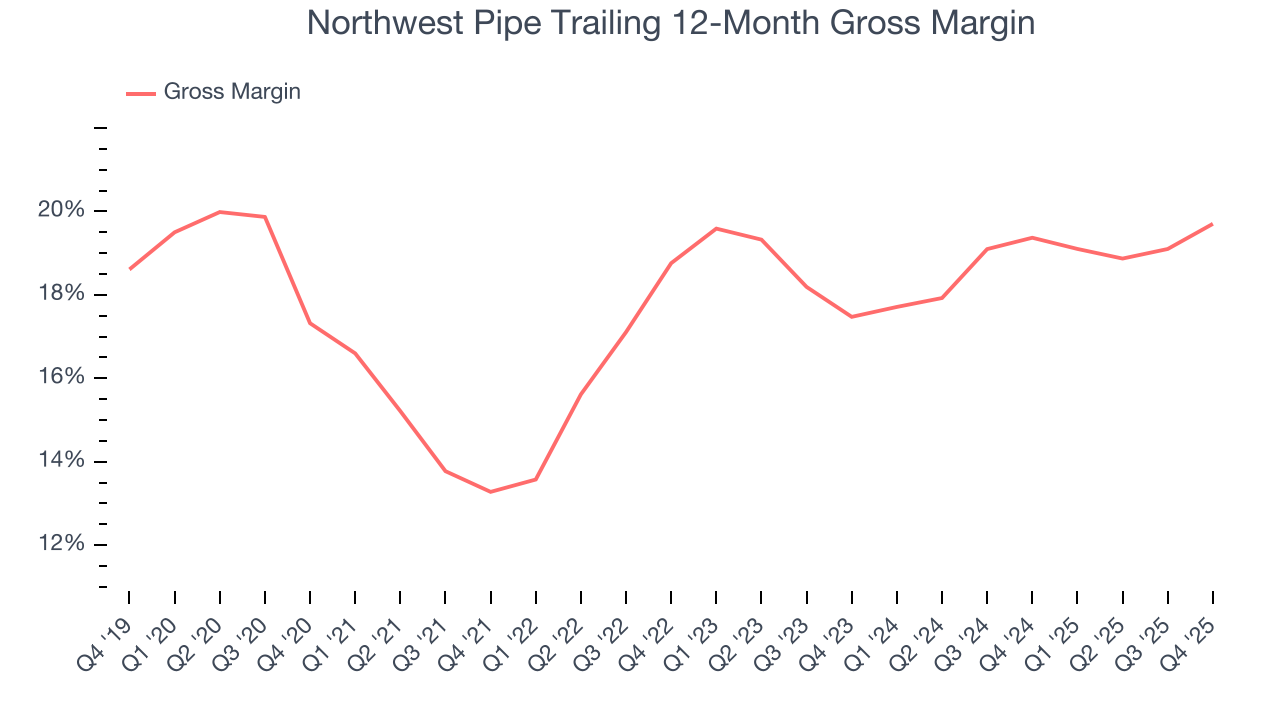

- A downside is its gross margin of 18% reflects its high production costs

Northwest Pipe shows some promise. If you’re a believer, the valuation looks reasonable.

Why Is Now The Time To Buy Northwest Pipe?

At $72.25 per share, Northwest Pipe trades at 17.2x forward P/E. Many industrials companies may feature a higher valuation multiple, but that doesn’t make Northwest Pipe a great deal. We think the current multiple fairly reflects the revenue characteristics.

It could be a good time to invest if you see something the market doesn’t.

3. Northwest Pipe (NWPX) Research Report: Q4 CY2025 Update

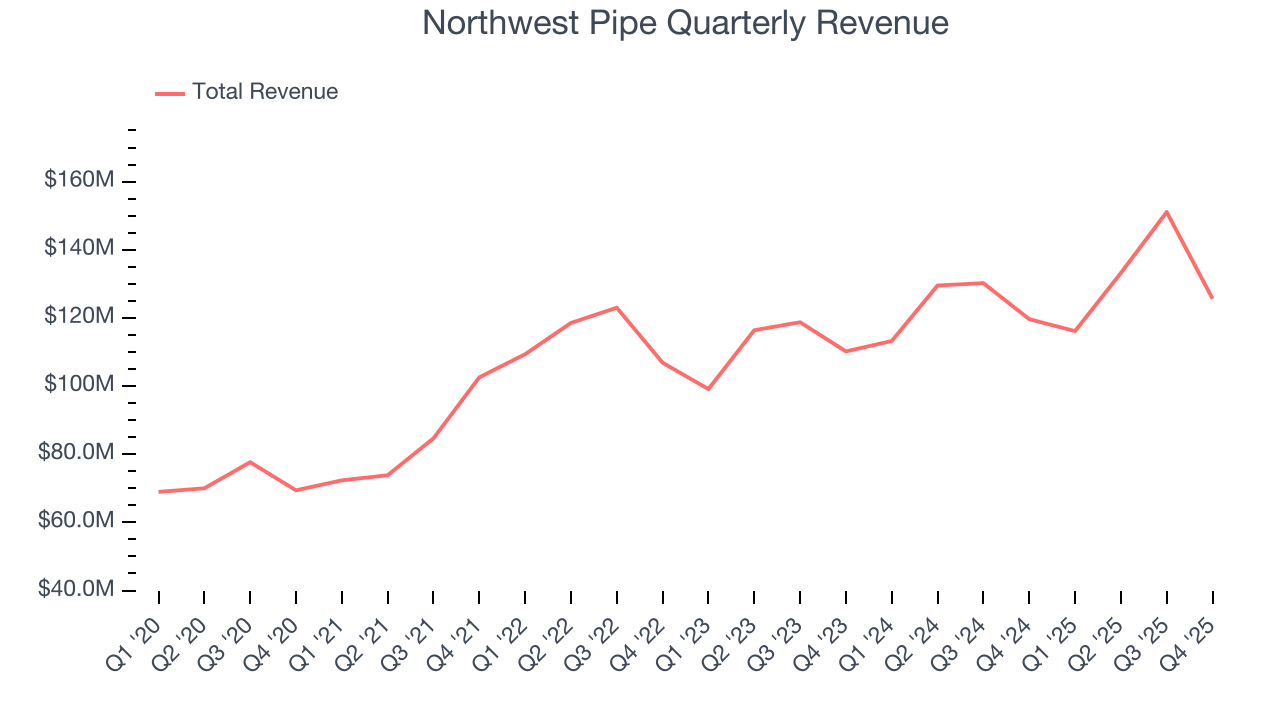

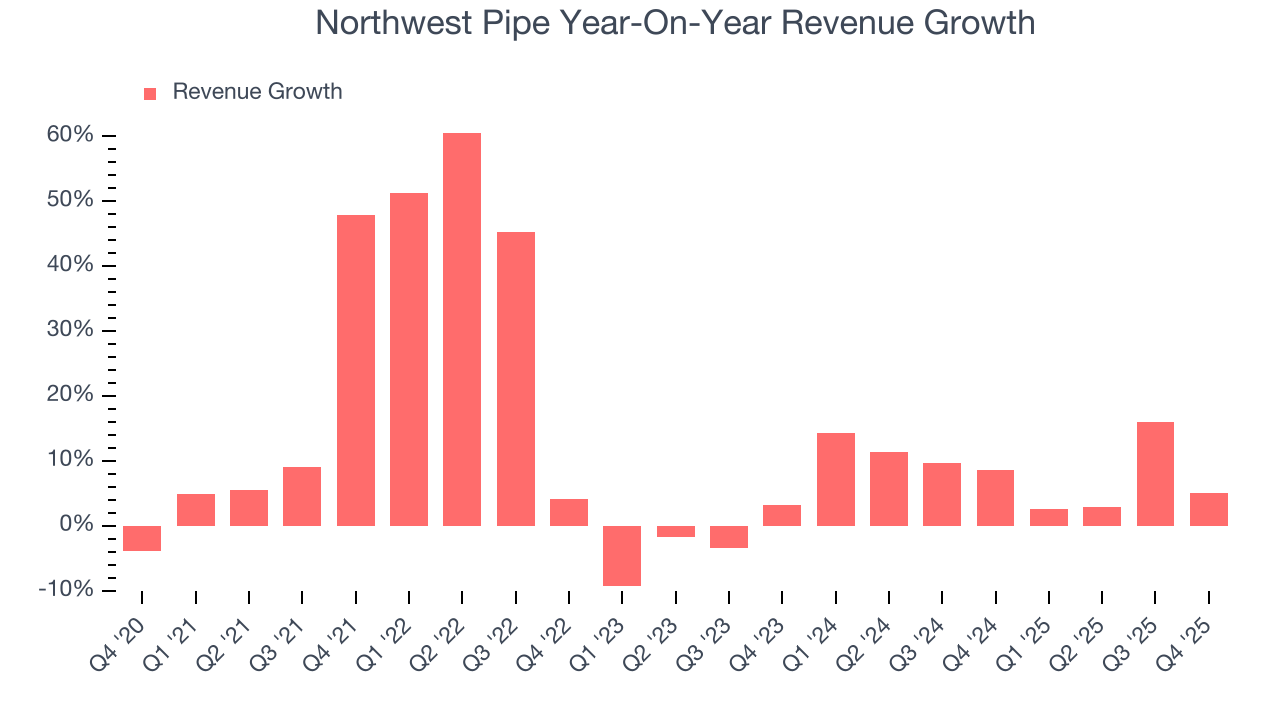

Water management company Northwest Pipe (NASDAQ:NWPX) announced better-than-expected revenue in Q4 CY2025, with sales up 5% year on year to $125.6 million. Its non-GAAP profit of $0.93 per share was 50% above analysts’ consensus estimates.

Northwest Pipe (NWPX) Q4 CY2025 Highlights:

- Revenue: $125.6 million vs analyst estimates of $122 million (5% year-on-year growth, 3% beat)

- Adjusted EPS: $0.93 vs analyst estimates of $0.62 (50% beat)

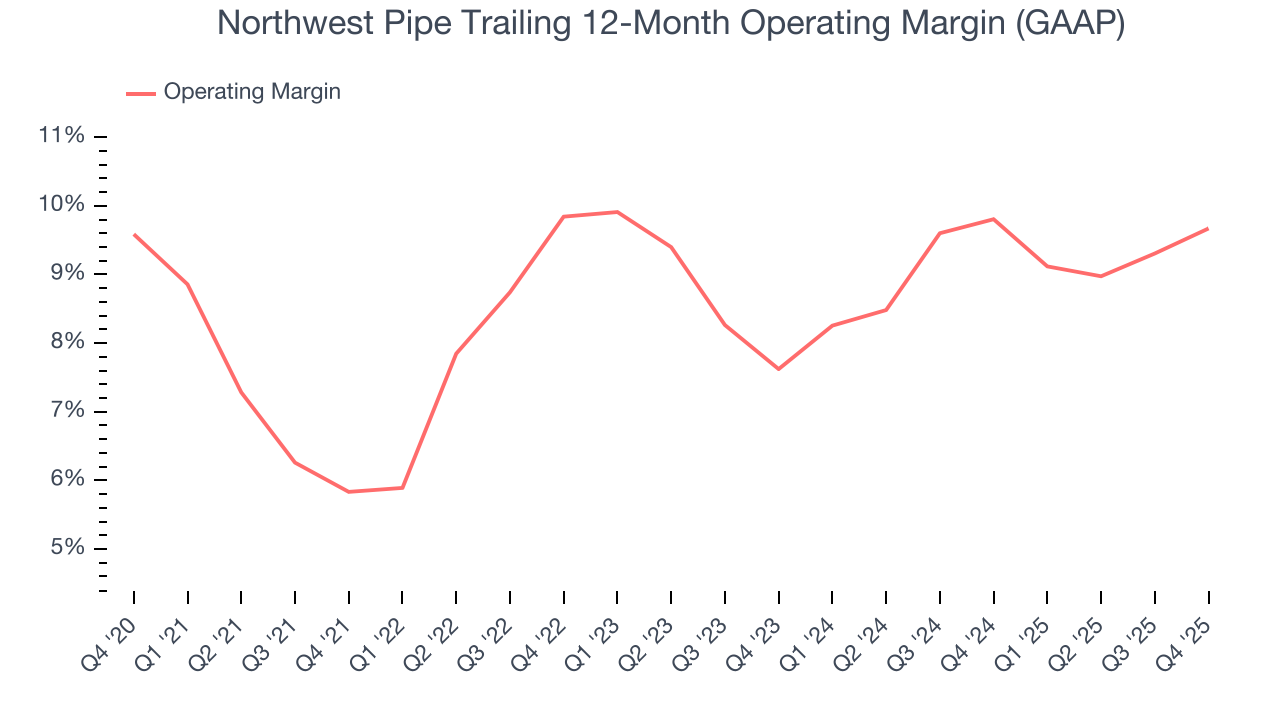

- Operating Margin: 10.4%, up from 8.8% in the same quarter last year

- Free Cash Flow Margin: 24.5%, down from 26.7% in the same quarter last year

- Market Capitalization: $702.9 million

Company Overview

Playing a large role in the Integrated Pipeline (IPL) project in Texas to deliver ~350 million gallons of water per day, Northwest Pipe (NASDAQ:NWPX) is a manufacturer of pipeline systems for water infrastructure.

Northwest Pipe was founded in 1966 as a manufacturer of pipeline systems for water infrastructure. Initially starting with just three steel pipe mills and 20 employees, the company has expanded significantly through acquisitions. One of the most notable acquisitions was the purchase of Ameron Water Transmission Group in 2018. which added bar-wrapped concrete pipe and reinforced concrete pipe to its portfolio.

Today, the company makes and sells various types of pipes and other products needed for managing water. It offers strong steel water pipes used to carry water over long distances and concrete products used in systems that treat wastewater and manage stormwater which are important for keeping water clean. For example, its bar-wrapped concrete cylinder pipe, which combines steel and concrete to handle high-pressure water transport, is used for moving large volumes of water through municipal and industrial water systems.

Northwest Pipe engages in long-term contracts typically spanning five to ten years for city water systems, industrial water systems, and infrastructure projects. These contracts often include agreements to supply parts regularly and provide maintenance and support to keep everything working well.

4. HVAC and Water Systems

Many HVAC and water systems companies sell essential, non-discretionary infrastructure for buildings. Since the useful lives of these water heaters and vents are fairly standard, these companies have a portion of predictable replacement revenue. In the last decade, trends in energy efficiency and clean water are driving innovation that is leading to incremental demand. On the other hand, new installations for these companies are at the whim of residential and commercial construction volumes, which tend to be cyclical and can be impacted heavily by economic factors such as interest rates.

Competitors offering similar products include Mueller (NYSE:MWA), Advanced Drainage Systems (NYSE:WMS), and American States Water Company (NYSE:AWR).

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Northwest Pipe grew its sales at an excellent 13% compounded annual growth rate. Its growth beat the average industrials company and shows its offerings resonate with customers, a helpful starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Northwest Pipe’s annualized revenue growth of 8.8% over the last two years is below its five-year trend, but we still think the results were respectable.

This quarter, Northwest Pipe reported year-on-year revenue growth of 5%, and its $125.6 million of revenue exceeded Wall Street’s estimates by 3%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

6. Gross Margin & Pricing Power

For industrials businesses, cost of sales is usually comprised of the direct labor, raw materials, and supplies needed to offer a product or service. These costs can be impacted by inflation and supply chain dynamics in the short term and a company’s purchasing power and scale over the long term.

Northwest Pipe has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 18% gross margin over the last five years. Said differently, Northwest Pipe had to pay a chunky $81.95 to its suppliers for every $100 in revenue.

Northwest Pipe’s gross profit margin came in at 21.3% this quarter , marking a 2.5 percentage point increase from 18.8% in the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

7. Operating Margin

Northwest Pipe has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 8.8%, higher than the broader industrials sector.

Looking at the trend in its profitability, Northwest Pipe’s operating margin rose by 3.8 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, Northwest Pipe generated an operating margin profit margin of 10.4%, up 1.6 percentage points year on year. Since its gross margin expanded more than its operating margin, we can infer that leverage on its cost of sales was the primary driver behind the recently higher efficiency.

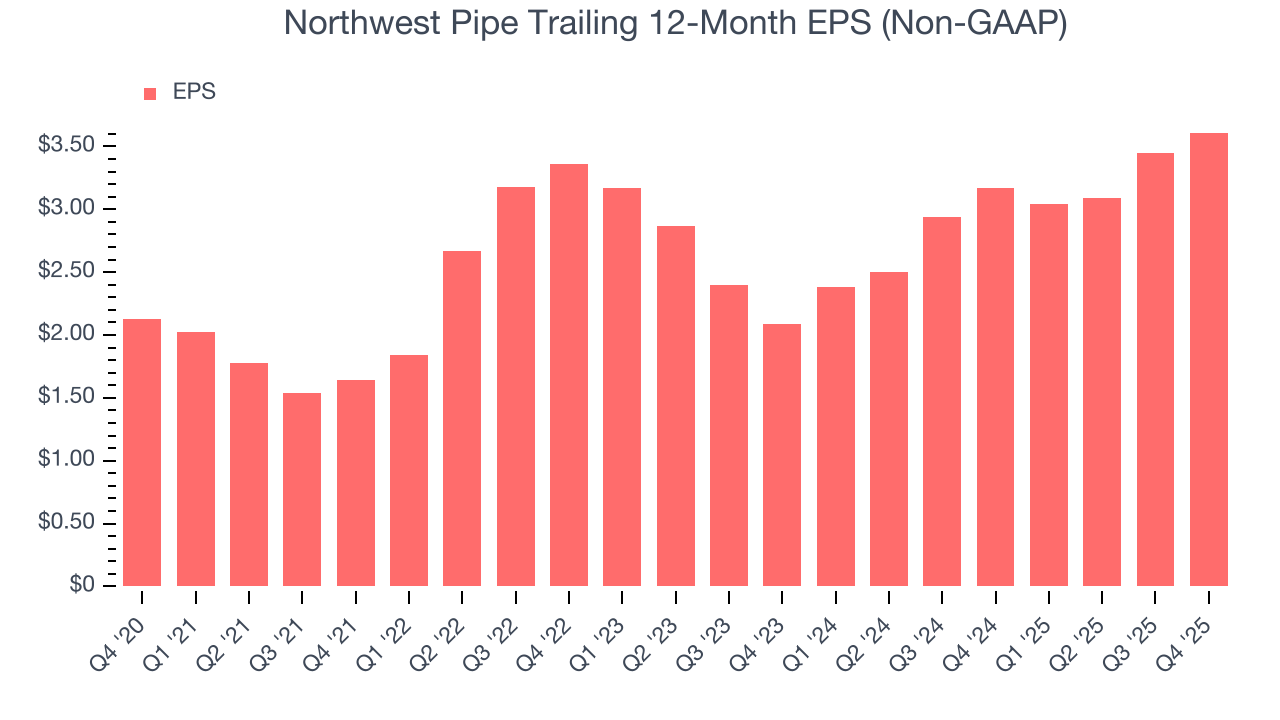

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Northwest Pipe’s solid 11.1% annual EPS growth over the last five years aligns with its revenue performance. This tells us its incremental sales were profitable.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Northwest Pipe’s two-year annual EPS growth of 31.4% was fantastic and topped its 8.8% two-year revenue growth.

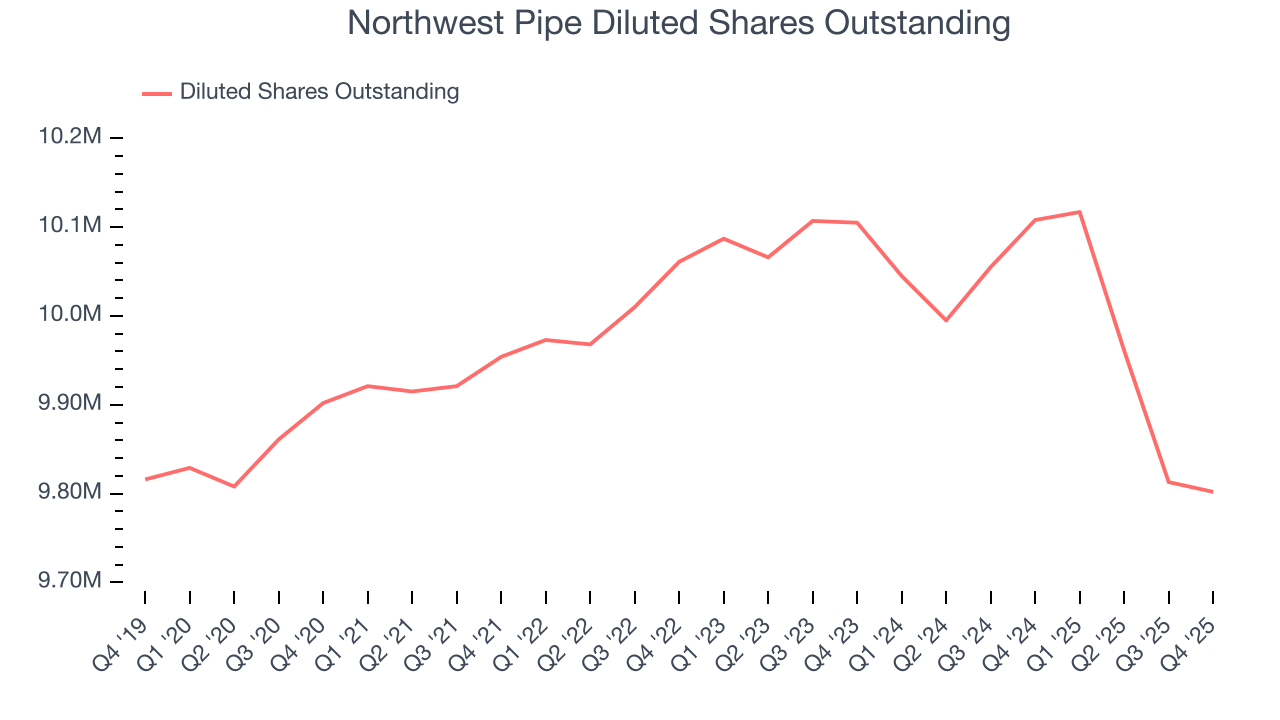

We can take a deeper look into Northwest Pipe’s earnings to better understand the drivers of its performance. Northwest Pipe’s operating margin has expanded over the last two yearswhile its share count has shrunk 3%. Improving profitability and share buybacks are positive signs for shareholders as they juice EPS growth relative to revenue growth.

In Q4, Northwest Pipe reported adjusted EPS of $0.93, up from $0.77 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Northwest Pipe’s full-year EPS of $3.61 to grow 15%.

9. Cash Is King

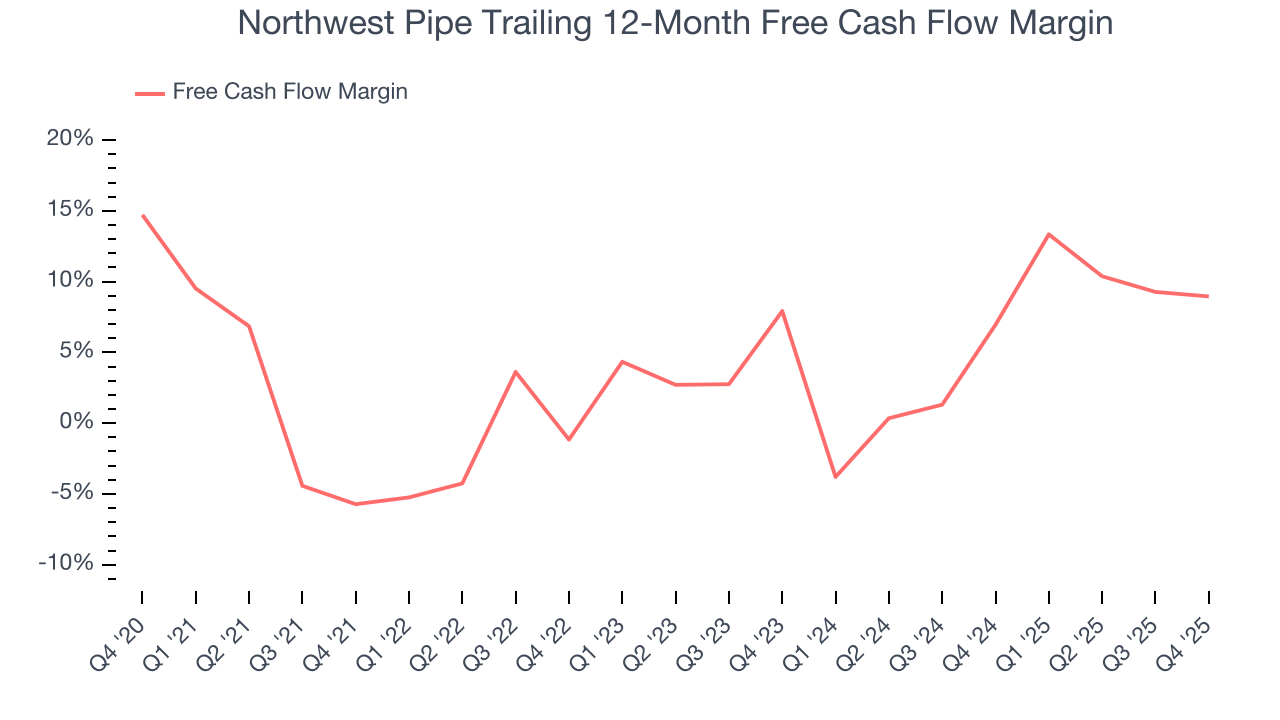

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Northwest Pipe has shown weak cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 4.1%, subpar for an industrials business.

Taking a step back, an encouraging sign is that Northwest Pipe’s margin expanded by 14.7 percentage points during that time. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

Northwest Pipe’s free cash flow clocked in at $30.82 million in Q4, equivalent to a 24.5% margin. The company’s cash profitability regressed as it was 2.2 percentage points lower than in the same quarter last year, but it’s still above its five-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, causing short-term swings. Long-term trends are more important.

10. Return on Invested Capital (ROIC)

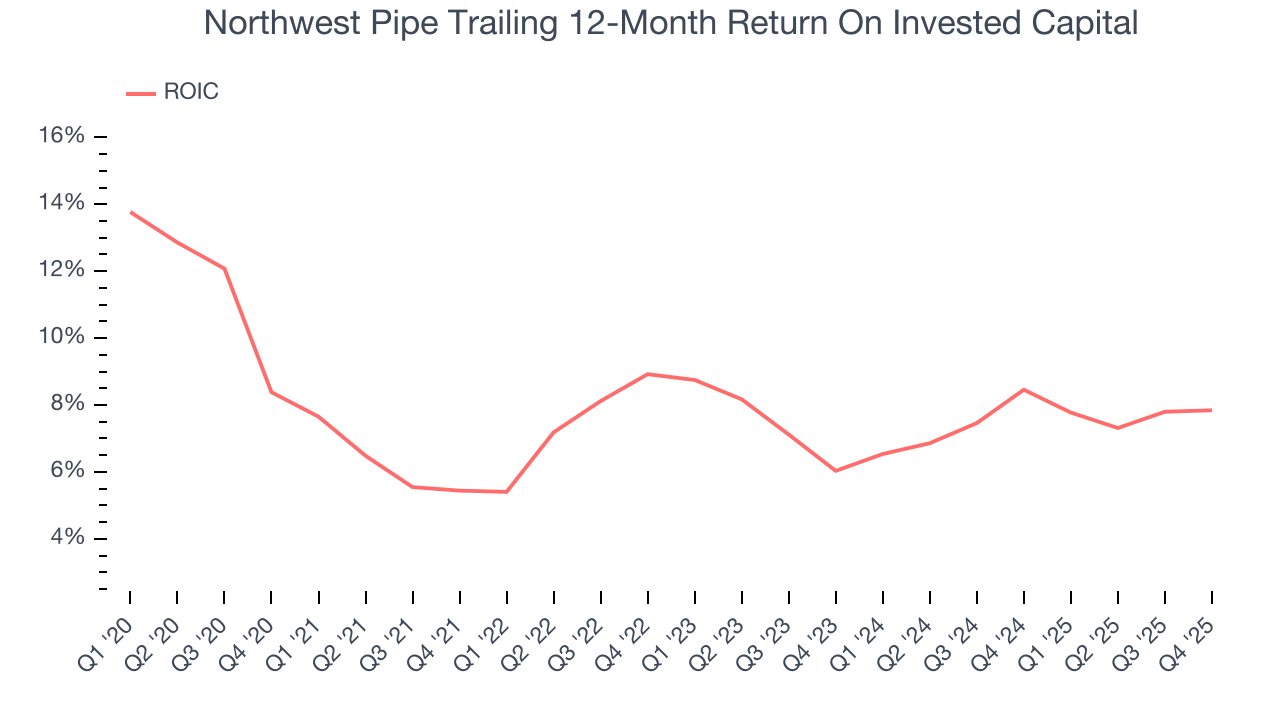

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Although Northwest Pipe has shown solid fundamentals lately, it historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 7.3%, somewhat low compared to the best industrials companies that consistently pump out 20%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Northwest Pipe’s ROIC has stayed the same over the last few years. We still think it’s a good business, but if the company wants to reach the next level, it must improve its returns.

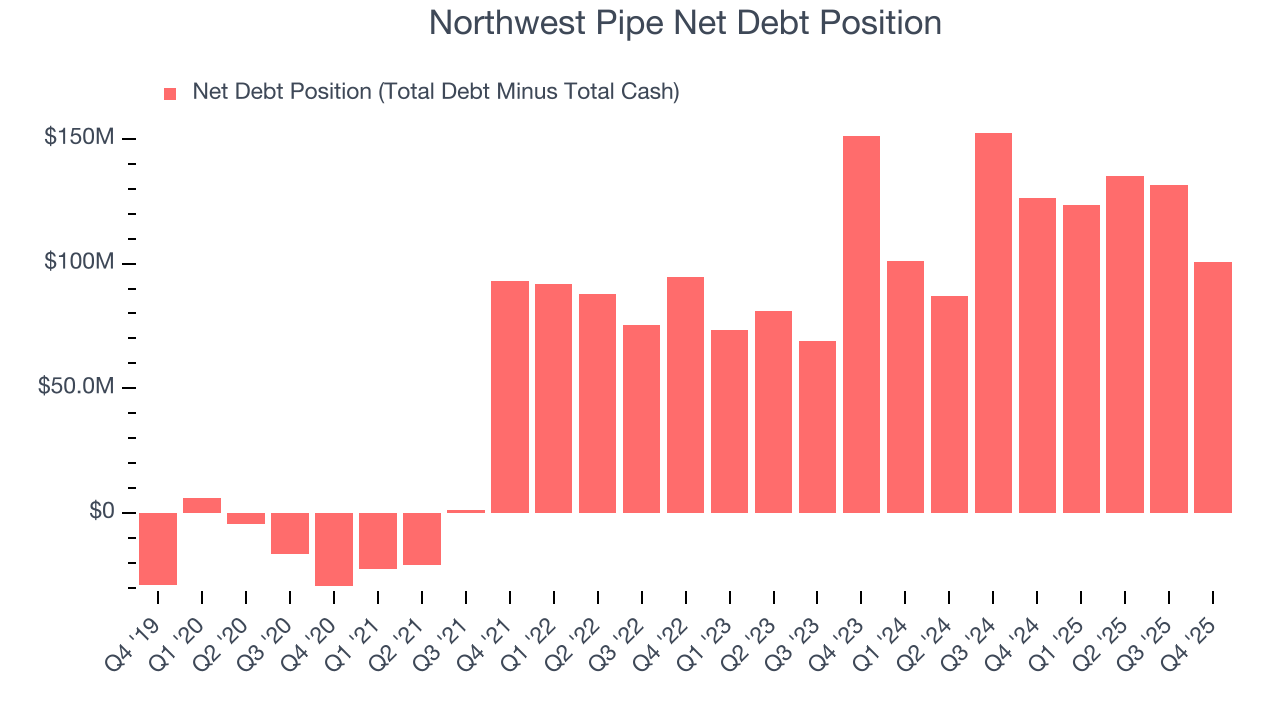

11. Balance Sheet Assessment

Northwest Pipe reported $2.27 million of cash and $102.8 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $71.84 million of EBITDA over the last 12 months, we view Northwest Pipe’s 1.4× net-debt-to-EBITDA ratio as safe. We also see its $2.61 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Northwest Pipe’s Q4 Results

It was good to see Northwest Pipe beat analysts’ EPS expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock traded up 1% to $74.84 immediately after reporting.

13. Is Now The Time To Buy Northwest Pipe?

Updated: March 16, 2026 at 11:32 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Northwest Pipe.

In our opinion, Northwest Pipe is a solid company. First off, its revenue growth was impressive over the last five years. And while its low gross margins indicate some combination of competitive pressures and high production costs, its rising cash profitability gives it more optionality. On top of that, its projected EPS for the next year implies the company’s fundamentals will improve.

Northwest Pipe’s P/E ratio based on the next 12 months is 17.2x. Looking at the industrials landscape right now, Northwest Pipe trades at a pretty interesting price. If you trust the business and its direction, this is an ideal time to buy.

Wall Street analysts have a consensus one-year price target of $86 on the company (compared to the current share price of $72.25), implying they see 19% upside in buying Northwest Pipe in the short term.