Palomar Holdings (PLMR)

Not many stocks excite us like Palomar Holdings. Its strong sales growth and returns on capital show it’s capable of quick and profitable expansion.― StockStory Analyst Team

1. News

2. Summary

Why We Like Palomar Holdings

Founded in 2013 to fill gaps in catastrophe insurance markets, Palomar Holdings (NASDAQ:PLMR) is a specialty insurance provider that offers property and casualty insurance products in underserved markets, with a focus on earthquake coverage.

- Market share has increased this cycle as its 39.1% annual revenue growth over the last five years was exceptional

- Incremental sales significantly boosted profitability as its annual earnings per share growth of 84.4% over the last five years outstripped its revenue performance

- Annual book value per share growth of 20.1% over the last five years was superb and indicates its capital strength increased during this cycle

We’re optimistic about Palomar Holdings. The price seems fair based on its quality, and we believe now is a prudent time to buy.

Why Is Now The Time To Buy Palomar Holdings?

Palomar Holdings’s stock price of $120.63 implies a valuation ratio of 2.8x forward P/B. Yes, the stock’s seemingly high valuation multiple could mean short-term volatility. But given its business quality, we think the multiple is justified.

Our analysis and backtests show it’s often prudent to pay up for high-quality businesses because they routinely outperform the market over a multi-year period almost regardless of the entry price.

3. Palomar Holdings (PLMR) Research Report: Q4 CY2025 Update

Specialty insurance provider Palomar Holdings (NASDAQ:PLMR) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 62.7% year on year to $253.4 million. Its non-GAAP profit of $2.24 per share was 7.1% above analysts’ consensus estimates.

Palomar Holdings (PLMR) Q4 CY2025 Highlights:

- Net Premiums Earned: $233.5 million vs analyst estimates of $206.3 million (61.1% year-on-year growth, 13.2% beat)

- Revenue: $253.4 million vs analyst estimates of $223.7 million (62.7% year-on-year growth, 13.2% beat)

- Combined Ratio: 76.8% vs analyst estimates of 74.7% (206 basis point miss)

- Adjusted EPS: $2.24 vs analyst estimates of $2.09 (7.1% beat)

- Market Capitalization: $3.43 billion

Company Overview

Founded in 2013 to fill gaps in catastrophe insurance markets, Palomar Holdings (NASDAQ:PLMR) is a specialty insurance provider that offers property and casualty insurance products in underserved markets, with a focus on earthquake coverage.

Palomar operates through two insurance subsidiaries: Palomar Specialty Insurance Company, which offers admitted insurance products in 42 states, and Palomar Excess and Surplus Insurance Company, which provides excess and surplus (E&S) coverage nationwide. The company's product portfolio includes residential and commercial earthquake insurance, inland marine coverage, casualty insurance, Hawaii hurricane protection, residential flood insurance, and crop coverage.

What distinguishes Palomar is its data-driven approach to underwriting in catastrophe-prone and specialty markets. The company employs proprietary analytics and modeling techniques that allow for highly granular risk assessment—often down to the geocode or ZIP code level—enabling precise pricing in markets where many larger insurers are reluctant to participate. For residential policies, this technology enables automated underwriting that can process applications within minutes.

Palomar distributes its products through multiple channels, including retail agents, wholesale brokers, program administrators, and partnerships with other insurance companies. For example, a homeowner in California might purchase Palomar's earthquake coverage through their local insurance agent as a companion policy to their standard homeowners insurance. Similarly, a commercial property owner might obtain Palomar's coverage through a wholesale broker specializing in catastrophe insurance.

The company manages catastrophe exposure through a comprehensive reinsurance program that transfers portions of risk to reinsurers, reducing earnings volatility while maintaining protection against major events. This strategy allows Palomar to maintain financial stability while operating in catastrophe-exposed markets.

4. Property & Casualty Insurance

Property & Casualty (P&C) insurers protect individuals and businesses against financial loss from damage to property or from legal liability. This is a cyclical industry, and the sector benefits when there is 'hard market', characterized by strong premium rate increases that outpace loss and cost inflation, resulting in robust underwriting margins. The opposite is true in a 'soft market'. Interest rates also matter, as they determine the yields earned on fixed-income portfolios. On the other hand, P&C insurers face a major secular headwind from the increasing frequency and severity of catastrophe losses due to climate change. Furthermore, the liability side of the business is pressured by 'social inflation'—the trend of rising litigation costs and larger jury awards.

Palomar's competitors include large national insurers such as American International Group (NYSE:AIG), Chubb Limited (NYSE:CB), and Zurich Insurance Group, as well as state-managed enterprises like the California Earthquake Authority. In certain specialty lines, Palomar also competes with Lloyd's of London syndicates and other excess and surplus carriers.

5. Revenue Growth

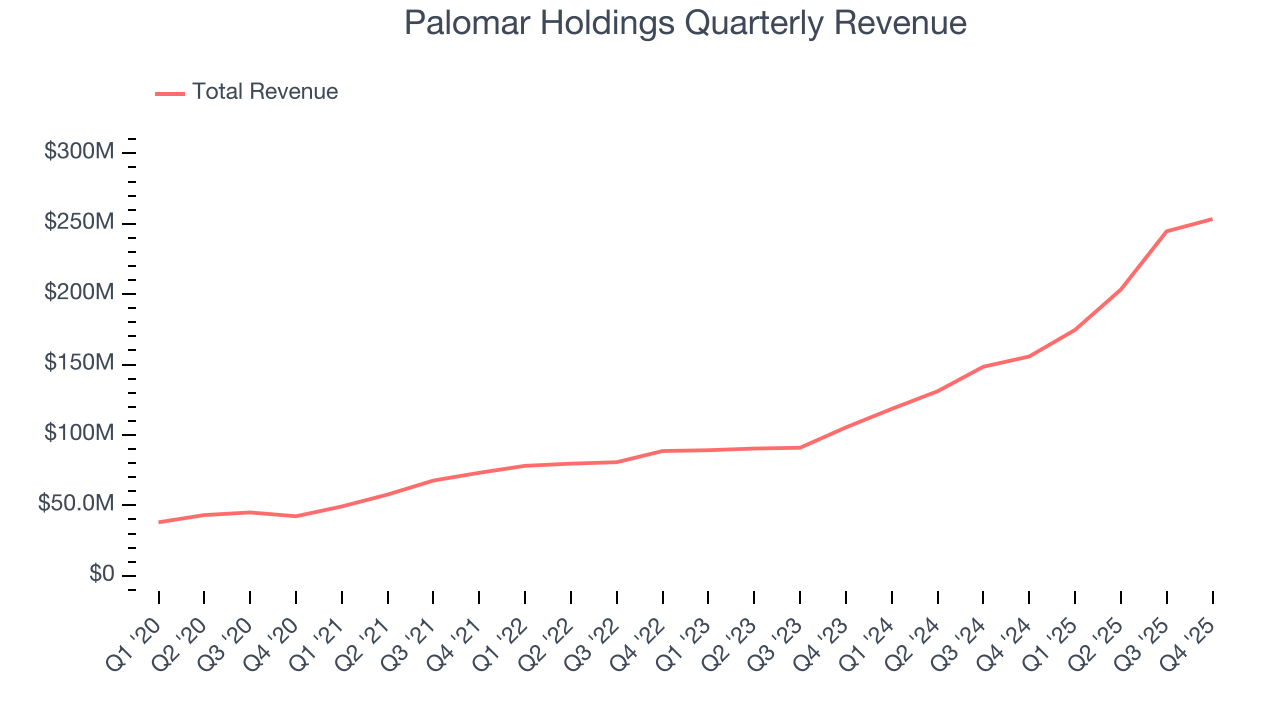

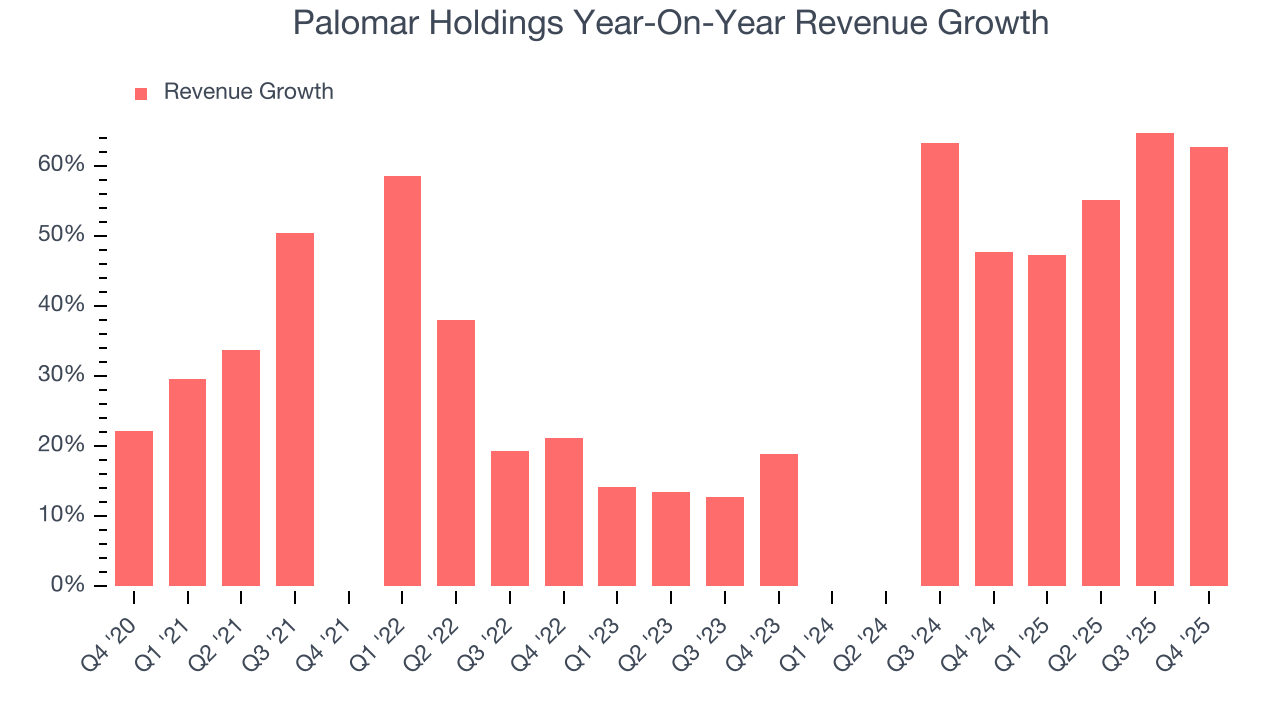

In general, insurance companies earn revenue from three primary sources. The first is the core insurance business itself, often called underwriting and represented in the income statement as premiums earned. The second source is investment income from investing the “float” (premiums collected upfront not yet paid out as claims) in assets such as fixed-income assets and equities. The third is fees from various sources such as policy administration, annuities, or other value-added services. Luckily, Palomar Holdings’s revenue grew at an incredible 39.1% compounded annual growth rate over the last five years. Its growth surpassed the average insurance company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Palomar Holdings’s annualized revenue growth of 52.6% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Palomar Holdings reported magnificent year-on-year revenue growth of 62.7%, and its $253.4 million of revenue beat Wall Street’s estimates by 13.2%.

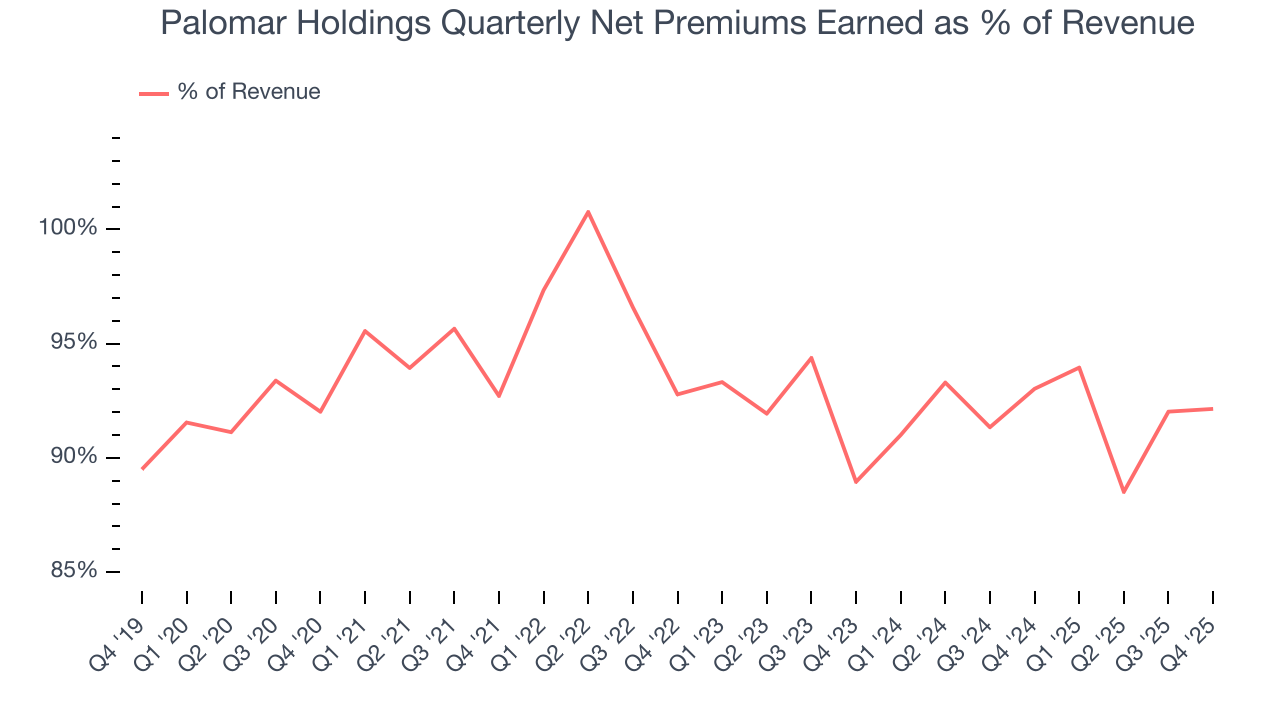

Net premiums earned made up 92.8% of the company’s total revenue during the last five years, meaning Palomar Holdings lives and dies by its underwriting activities because non-insurance operations barely move the needle.

Net premiums earned commands greater market attention due to its reliability and consistency, whereas investment and fee income are often seen as more volatile revenue streams that fluctuate with market conditions.

6. Net Premiums Earned

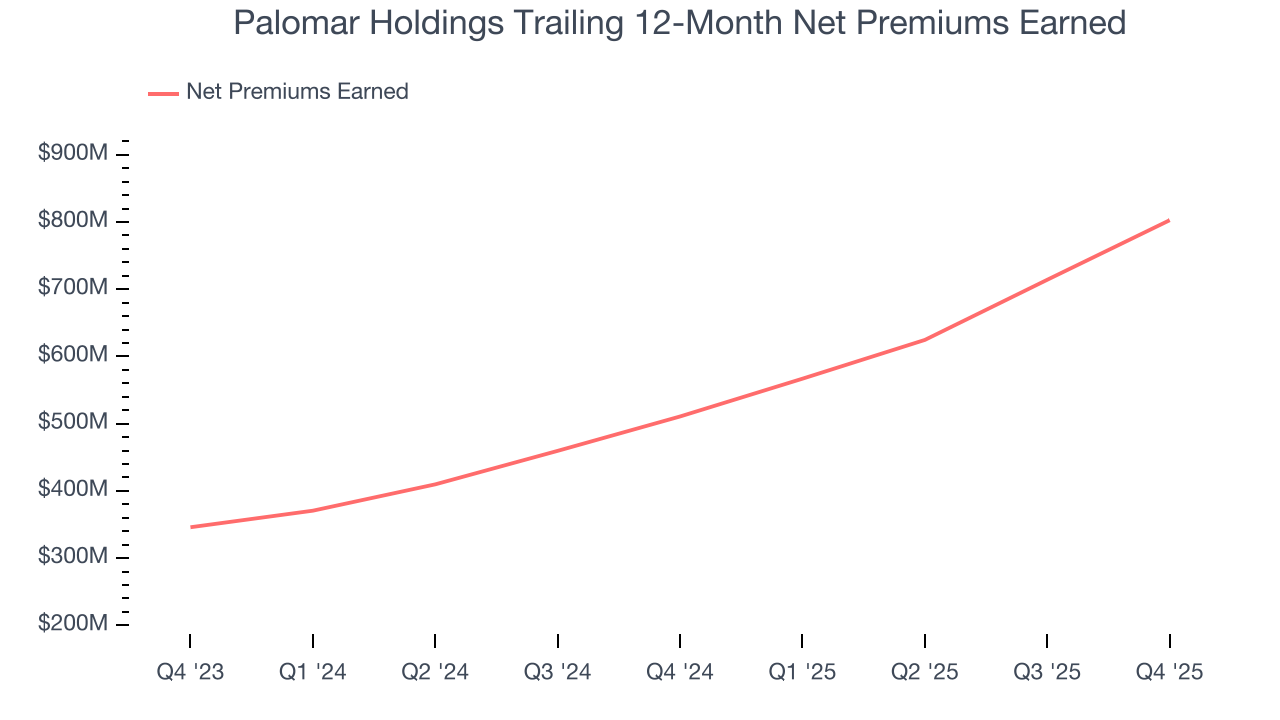

Insurers sell policies then use reinsurance (insurance for insurance companies) to protect themselves from large losses. Net premiums earned are therefore what's collected from selling policies less what’s paid to reinsurers as a risk mitigation tool.

Palomar Holdings’s net premiums earned has grown at a 38.9% annualized rate over the last five years, much better than the broader insurance industry and in line with its total revenue.

When analyzing Palomar Holdings’s net premiums earned over the last two years, we can see that growth accelerated to 52.3% annually. This performance was similar to its total revenue.

This quarter, Palomar Holdings’s net premiums earned was $233.5 million, up a hearty 61.1% year on year and topping Wall Street Consensus estimates by 13.2%.

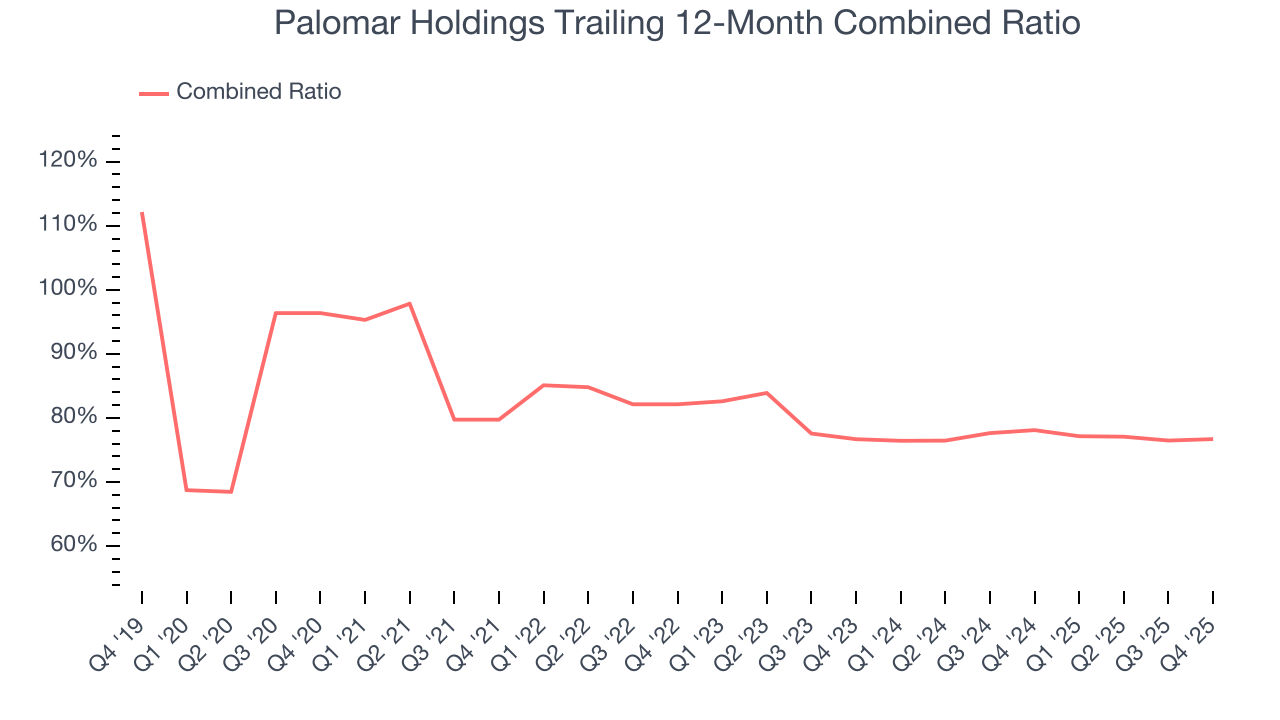

7. Combined Ratio

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For insurance companies, we look at the combined ratio rather than the operating expenses and margins that define sectors such as consumer, tech, and industrials.

The combined ratio is:

- The costs of underwriting (salaries, commissions, overhead) + what an insurer pays out in claims, all divided by net premiums earned

If a company boasts a combined ratio under 100%, it is underwriting profitably. If above 100%, it is losing money on its core operations of selling insurance policies.

Given the calculation, a lower expense ratio is better. Over the last five years, Palomar Holdings’s combined ratio has swelled by 19.7 percentage points, going from 79.7% to 76.7%. However, fixed cost leverage was muted more recently as the company’s combined ratio was flat on a two-year basis.

In Q4, Palomar Holdings’s combined ratio was 76.8%, falling short of analysts’ expectations by 206 basis points (100 basis points = 1 percentage point). This result was in line with the same quarter last year.

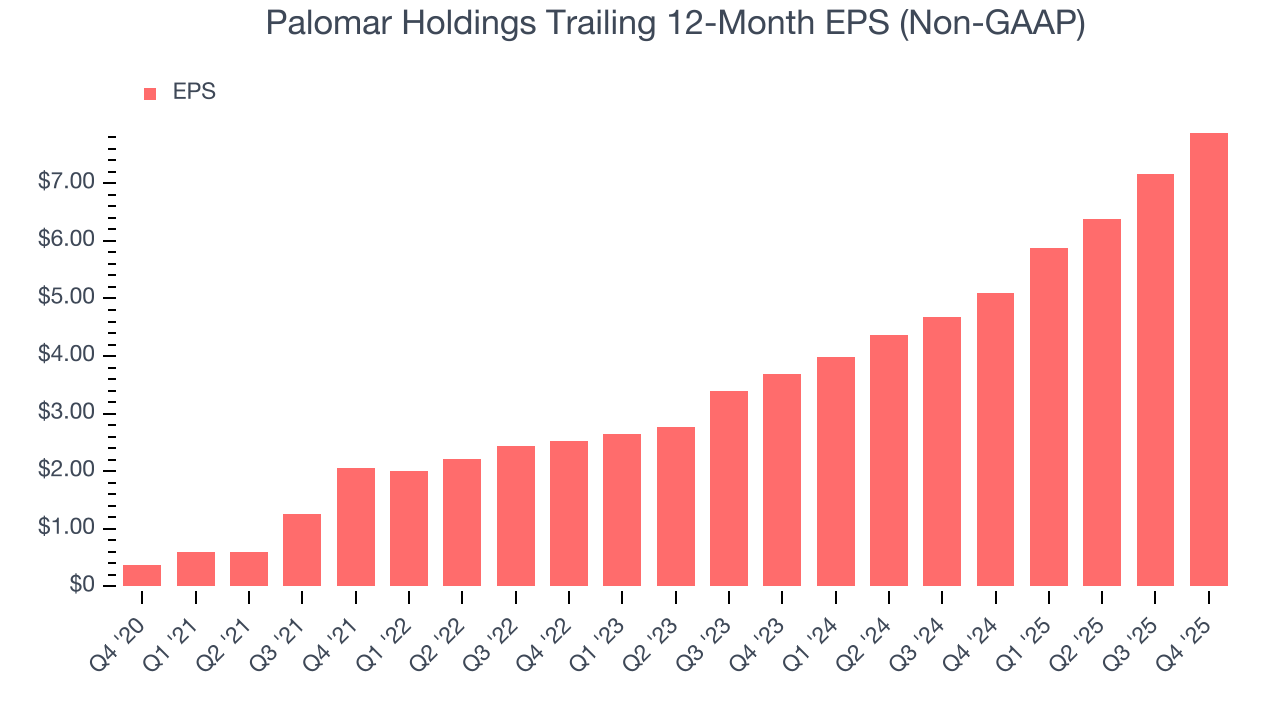

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Palomar Holdings’s EPS grew at an astounding 84.4% compounded annual growth rate over the last five years, higher than its 39.1% annualized revenue growth. However, we take this with a grain of salt because its combined ratio didn’t improve and it didn’t repurchase its shares, meaning the delta came from factors we consider non-core or less sustainable over the long term.

We can take a deeper look into Palomar Holdings’s earnings quality to better understand the drivers of its performance. As we mentioned earlier, Palomar Holdings’s combined ratio was flat this quarter but improved by 19.7 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Palomar Holdings, its two-year annual EPS growth of 46.1% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q4, Palomar Holdings reported adjusted EPS of $2.24, up from $1.52 in the same quarter last year. This print beat analysts’ estimates by 7.1%. Over the next 12 months, Wall Street expects Palomar Holdings’s full-year EPS of $7.88 to grow 9.9%.

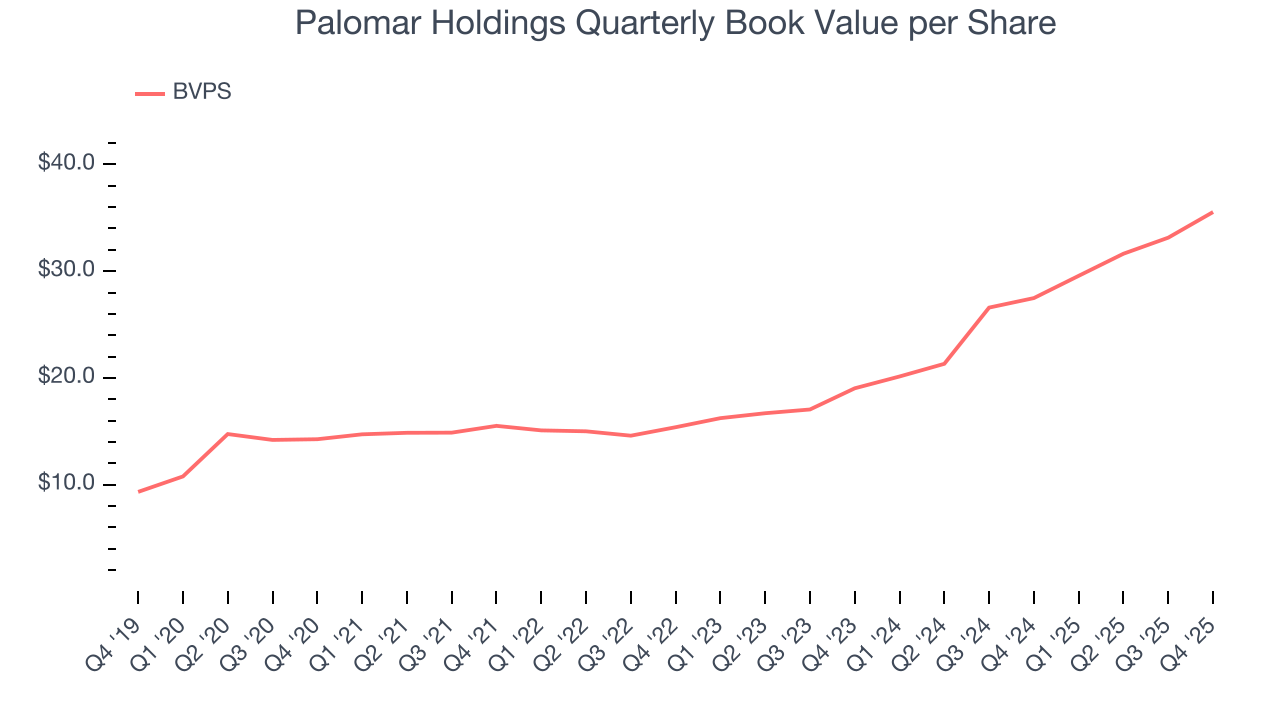

9. Book Value Per Share (BVPS)

Insurance companies are balance sheet businesses, collecting premiums upfront and paying out claims over time. The float – premiums collected but not yet paid out – are invested, creating an asset base supported by a liability structure. Book value captures this dynamic by measuring:

- Assets (investment portfolio, cash, reinsurance recoverables) - liabilities (claim reserves, debt, future policy benefits)

BVPS is essentially the residual value for shareholders.

We therefore consider BVPS very important to track for insurers and a metric that sheds light on business quality. While other (and more commonly known) per-share metrics like EPS can sometimes be lumpy due to reserve releases or one-time items and can be managed or skewed while still following accounting rules, BVPS reflects long-term capital growth and is harder to manipulate.

Palomar Holdings’s BVPS grew at an incredible 20.1% annual clip over the last five years. BVPS growth has also accelerated recently, growing by 36.7% annually over the last two years from $19.02 to $35.54 per share.

Over the next 12 months, Consensus estimates call for Palomar Holdings’s BVPS to grow by 23.1% to $35.47, elite growth rate.

10. Balance Sheet Assessment

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

Palomar Holdings has no debt, so leverage is not an issue here.

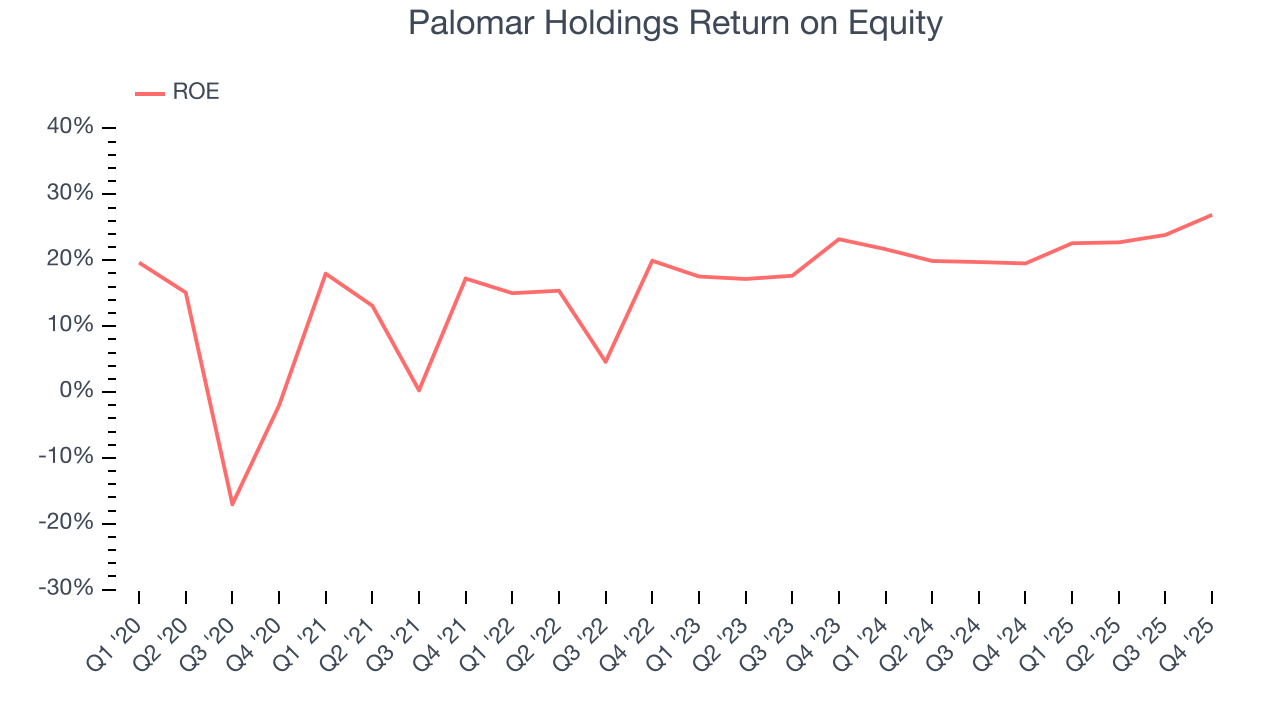

11. Return on Equity

Return on Equity, or ROE, ties everything together and is a vital metric. It tells us how much profit the insurer generates for each dollar of shareholder equity entrusted to management. Over a long period, insurers with higher ROEs tend to compound shareholder wealth faster through retained earnings, buybacks, and dividends.

Over the last five years, Palomar Holdings has averaged an ROE of 17.8%, excellent for a company operating in a sector where the average shakes out around 12.5% and those putting up 20%+ are greatly admired. This shows Palomar Holdings has a strong competitive moat.

12. Key Takeaways from Palomar Holdings’s Q4 Results

We were impressed by how significantly Palomar Holdings blew past analysts’ net premiums earned expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 2.1% to $134.56 immediately following the results.

13. Is Now The Time To Buy Palomar Holdings?

Updated: February 23, 2026 at 12:03 AM EST

Before investing in or passing on Palomar Holdings, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

There are multiple reasons why we think Palomar Holdings is an elite insurance company. First of all, the company’s revenue growth was exceptional over the last five years. On top of that, its net premiums earned growth was exceptional over the last five years, and its expanding pre-tax profit margin shows the business has become more efficient.

Palomar Holdings’s P/B ratio based on the next 12 months is 2.8x. This valuation may appear high at first glance, but the multiple is deserved because Palomar Holdings’s fundamentals clearly illustrate it’s an elite business. We think the stock is attractive here.

Wall Street analysts have a consensus one-year price target of $164.83 on the company (compared to the current share price of $120.63), implying they see 36.6% upside in buying Palomar Holdings in the short term.