Stewart Information Services (STC)

Stewart Information Services doesn’t impress us. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why Stewart Information Services Is Not Exciting

Founded in 1893 during America's westward expansion when property records were often disputed, Stewart Information Services (NYSE:STC) provides title insurance and real estate services, helping homebuyers, sellers, and lenders verify property ownership and protect against title defects.

- Earnings per share fell by 4.8% annually over the last five years while its revenue grew, showing its incremental sales were much less profitable

- Net premiums earned expanded by 2% annually over the last five years, falling below our expectations for the insurance sector

- On the plus side, its demand for the next 12 months is expected to accelerate above its two-year trend as Wall Street forecasts robust revenue growth of 16.2%

Stewart Information Services fails to meet our quality criteria. There are better opportunities in the market.

Why There Are Better Opportunities Than Stewart Information Services

Stewart Information Services’s stock price of $64.48 implies a valuation ratio of 1.1x forward P/B. Yes, this valuation multiple is lower than that of other insurance peers, but we’ll remind you that you often get what you pay for.

We’d rather pay up for companies with elite fundamentals than get a bargain on weak ones. Cheap stocks can be value traps, and as their performance deteriorates, they will stay cheap or get even cheaper.

3. Stewart Information Services (STC) Research Report: Q4 CY2025 Update

Title insurance provider Stewart Information Services (NYSE:STC) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 18.8% year on year to $790.6 million. Its non-GAAP profit of $1.65 per share was 21.9% above analysts’ consensus estimates.

Stewart Information Services (STC) Q4 CY2025 Highlights:

- Revenue: $790.6 million vs analyst estimates of $774.9 million (18.8% year-on-year growth, 2% beat)

- Pre-tax Profit: $51.73 million (6.5% margin)

- Adjusted EPS: $1.65 vs analyst estimates of $1.35 (21.9% beat)

- Book Value per Share: $54.30 (7.5% year-on-year growth)

- Market Capitalization: $2.05 billion

Company Overview

Founded in 1893 during America's westward expansion when property records were often disputed, Stewart Information Services (NYSE:STC) provides title insurance and real estate services, helping homebuyers, sellers, and lenders verify property ownership and protect against title defects.

Stewart operates through a network of direct operations and approved agencies, serving as a critical intermediary in real estate transactions. The company's core business involves searching and examining property records to identify potential ownership issues before a sale closes. When a property changes hands, Stewart's professionals verify that sellers have clear ownership rights and that there are no undisclosed liens, judgments, or other claims that could affect the new owner's rights.

Title insurance differs fundamentally from other insurance types by protecting against past (not future) events. Once issued, an owner's policy remains effective for as long as they own the property, while lender policies protect mortgage providers' interests. If an undiscovered title defect emerges later—such as a forged deed, undisclosed heir, or recording error—Stewart defends the policyholder and covers financial losses up to policy limits.

Beyond title insurance, Stewart has expanded into complementary real estate services. Through subsidiaries like Stewart Valuation Intelligence, NotaryCam, and PropStream, the company offers appraisal management, online notarization, digital closings, and property data services. A mortgage lender might use Stewart's appraisal management services to determine property value, conduct the closing through Stewart's digital platform, and secure title insurance—all within the same company ecosystem.

Stewart generates revenue primarily through one-time premiums paid at closing, with fees typically proportional to the property's value or loan amount. The company serves diverse customers including attorneys, mortgage lenders, real estate agents, developers, and individual homebuyers across both residential and commercial real estate markets.

4. Property & Casualty Insurance

Property & Casualty (P&C) insurers protect individuals and businesses against financial loss from damage to property or from legal liability. This is a cyclical industry, and the sector benefits when there is 'hard market', characterized by strong premium rate increases that outpace loss and cost inflation, resulting in robust underwriting margins. The opposite is true in a 'soft market'. Interest rates also matter, as they determine the yields earned on fixed-income portfolios. On the other hand, P&C insurers face a major secular headwind from the increasing frequency and severity of catastrophe losses due to climate change. Furthermore, the liability side of the business is pressured by 'social inflation'—the trend of rising litigation costs and larger jury awards.

Stewart Information Services competes primarily with three larger title insurance providers: Fidelity National Financial (NYSE:FNF), which operates Fidelity National Title and Chicago Title; First American Financial (NYSE:FAF), which includes First American Title Insurance; and Old Republic International (NYSE:ORI), which operates Old Republic National Title Insurance.

5. Revenue Growth

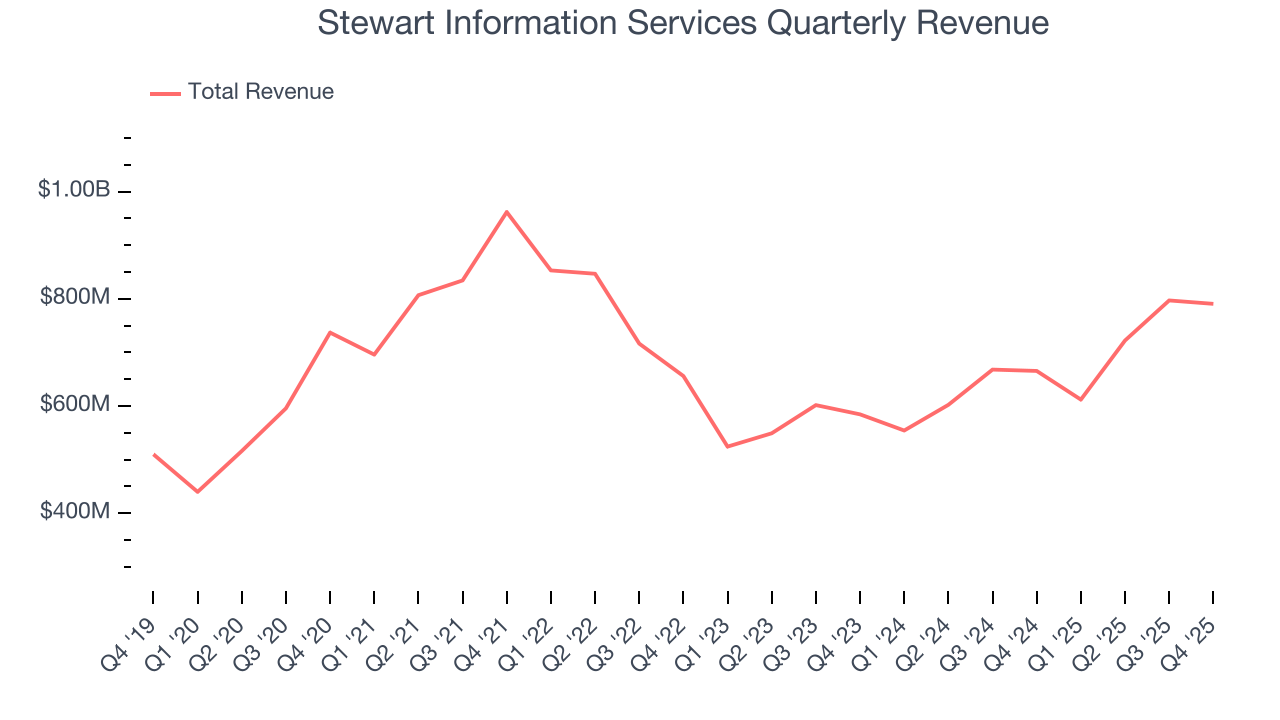

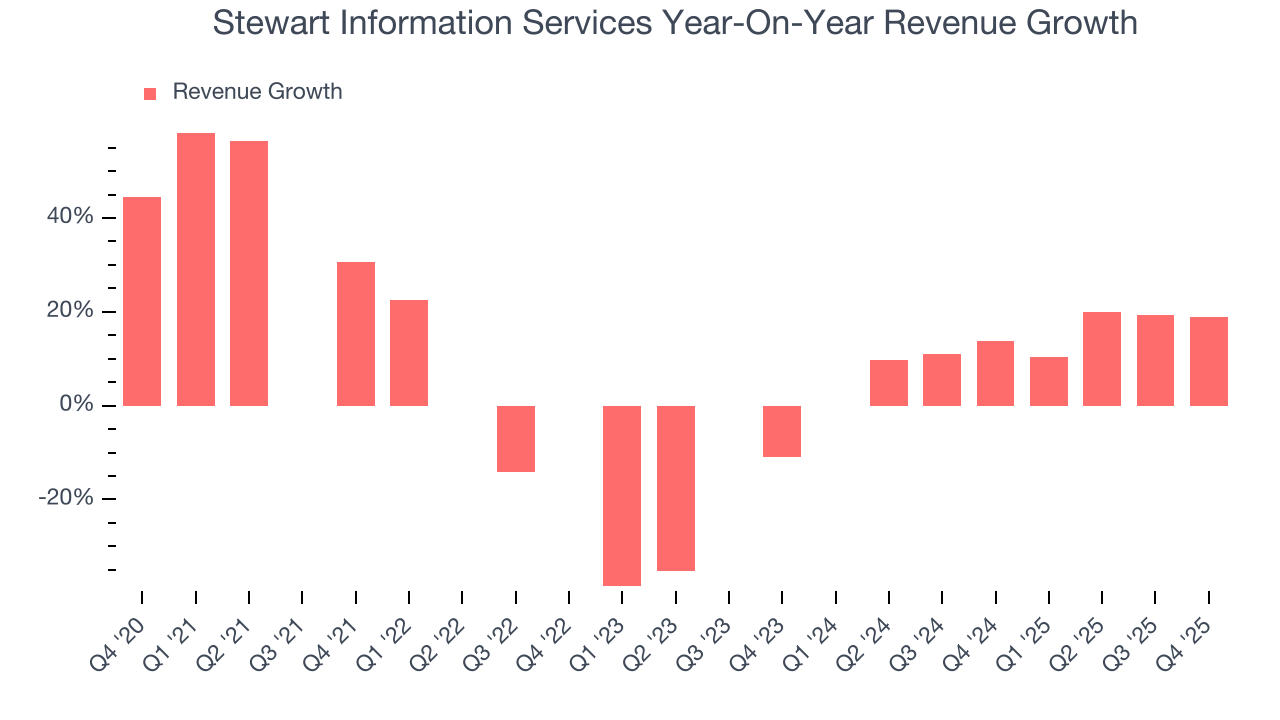

Insurance companies earn revenue from three primary sources: 1) The core insurance business itself, often called underwriting and represented in the income statement as premiums 2) Income from investing the “float” (premiums collected upfront not yet paid out as claims) in assets such as fixed-income assets and equities 3) Fees from various sources such as policy administration, annuities, or other value-added services. Unfortunately, Stewart Information Services’s 5% annualized revenue growth over the last five years was tepid. This was below our standard for the insurance sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Stewart Information Services’s annualized revenue growth of 13.7% over the last two years is above its five-year trend, suggesting its demand recently accelerated.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Stewart Information Services reported year-on-year revenue growth of 18.8%, and its $790.6 million of revenue exceeded Wall Street’s estimates by 2%.

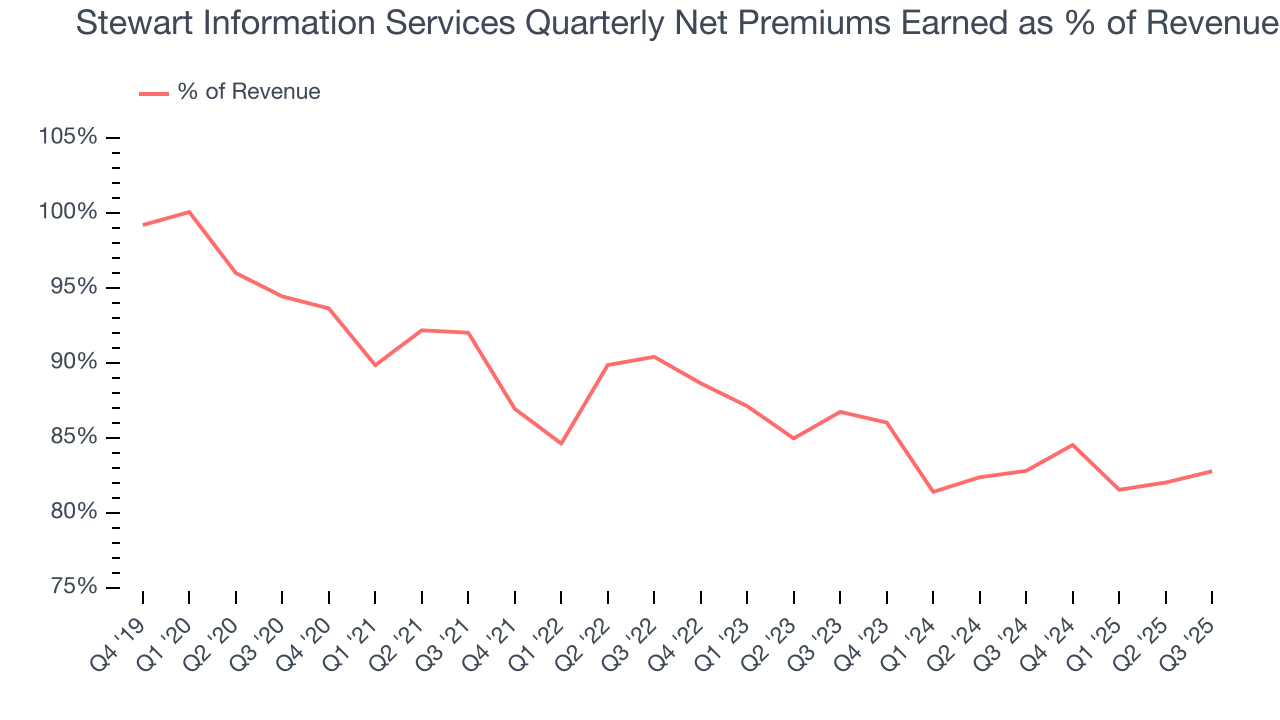

Net premiums earned made up 86.4% of the company’s total revenue during the last five years, meaning Stewart Information Services barely relies on non-insurance activities to drive its overall growth.

Net premiums earned commands greater market attention due to its reliability and consistency, whereas investment and fee income are often seen as more volatile revenue streams that fluctuate with market conditions.

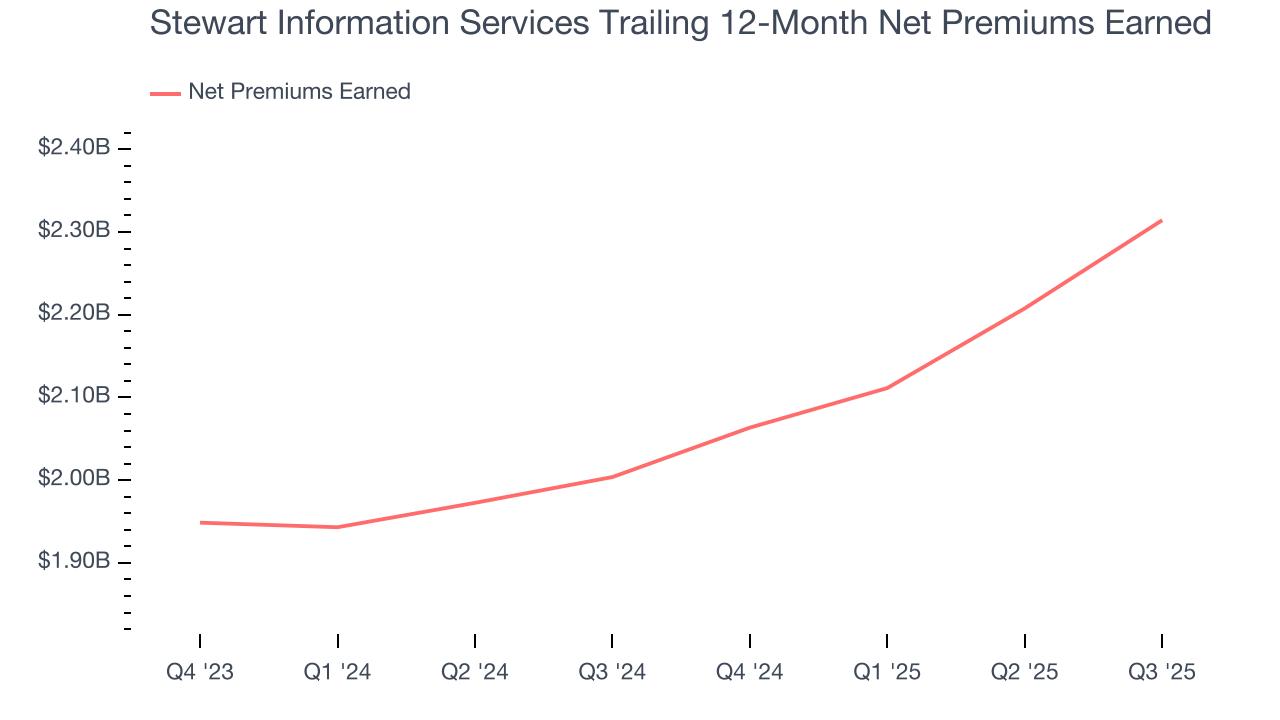

6. Net Premiums Earned

When insurers sell policies, they protect themselves from extremely large losses or an outsized accumulation of losses with reinsurance (insurance for insurance companies). Net premiums earned are therefore gross premiums less what’s ceded to reinsurers as a risk mitigation and transfer strategy.

Stewart Information Services’s net premiums earned has grown at a 3.2% annualized rate over the last five years, worse than the broader insurance industry and slower than its total revenue.

When analyzing Stewart Information Services’s net premiums earned over the last two years, we can see that growth accelerated to 10.1% annually. Since two-year net premiums earned grew slower than total revenue over this period, it’s implied that other line items such as investment income grew at a faster rate. These additional streams do play a key role in the bottom line, but their impact can vary. While some firms have excelled in consistently investing their float, sudden shifts in the fixed income and equity markets can heavily sway short-term performance.

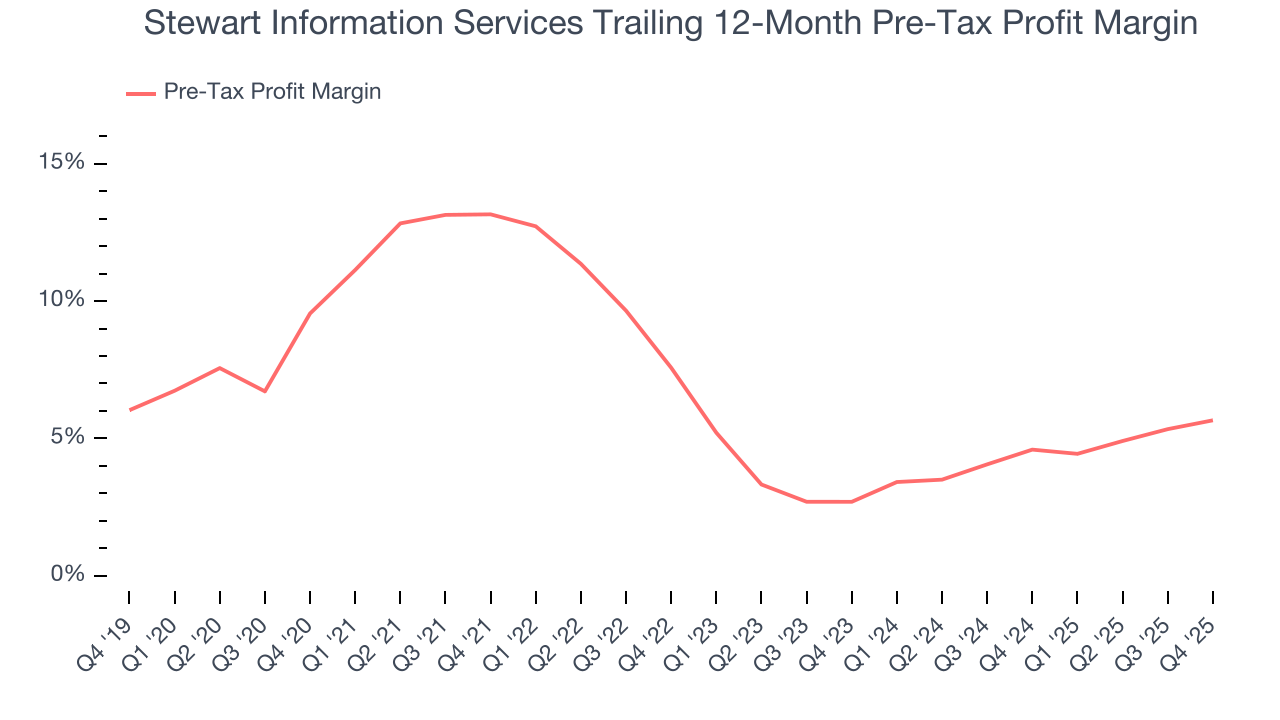

7. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For insurance companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

Insurance companies are balance sheet businesses, where assets and liabilities define the economics. Interest income and expense should therefore be factored into the definition of profit but taxes - which are largely out of a company’s control - should not. This is pre-tax profit by definition.

Over the last five years, Stewart Information Services’s pre-tax profit margin has risen by 3.9 percentage points, going from 13.2% to 5.7%. Luckily, it seems the company has recently taken steps to address its expense base as its pre-tax profit margin expanded by 3 percentage points on a two-year basis.

Stewart Information Services’s pre-tax profit margin came in at 6.5% this quarter. This result was 1.2 percentage points better than the same quarter last year.

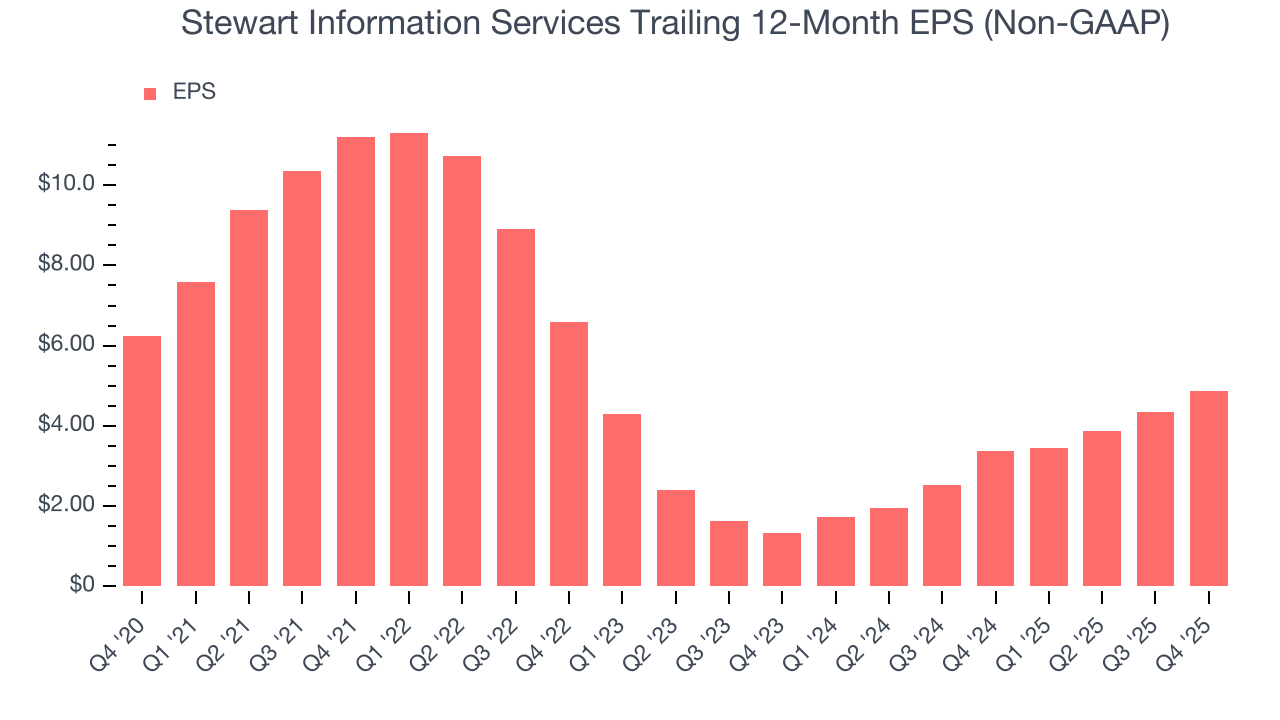

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Stewart Information Services, its EPS declined by 4.8% annually over the last five years while its revenue grew by 5%. However, its combined ratio actually improved during this time, telling us that non-fundamental factors such as interest expenses and taxes affected its ultimate earnings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Stewart Information Services, its two-year annual EPS growth of 92.2% was higher than its five-year trend. This acceleration made it one of the faster-growing insurance companies in recent history.

In Q4, Stewart Information Services reported adjusted EPS of $1.65, up from $1.12 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Stewart Information Services’s full-year EPS of $4.88 to grow 19.8%.

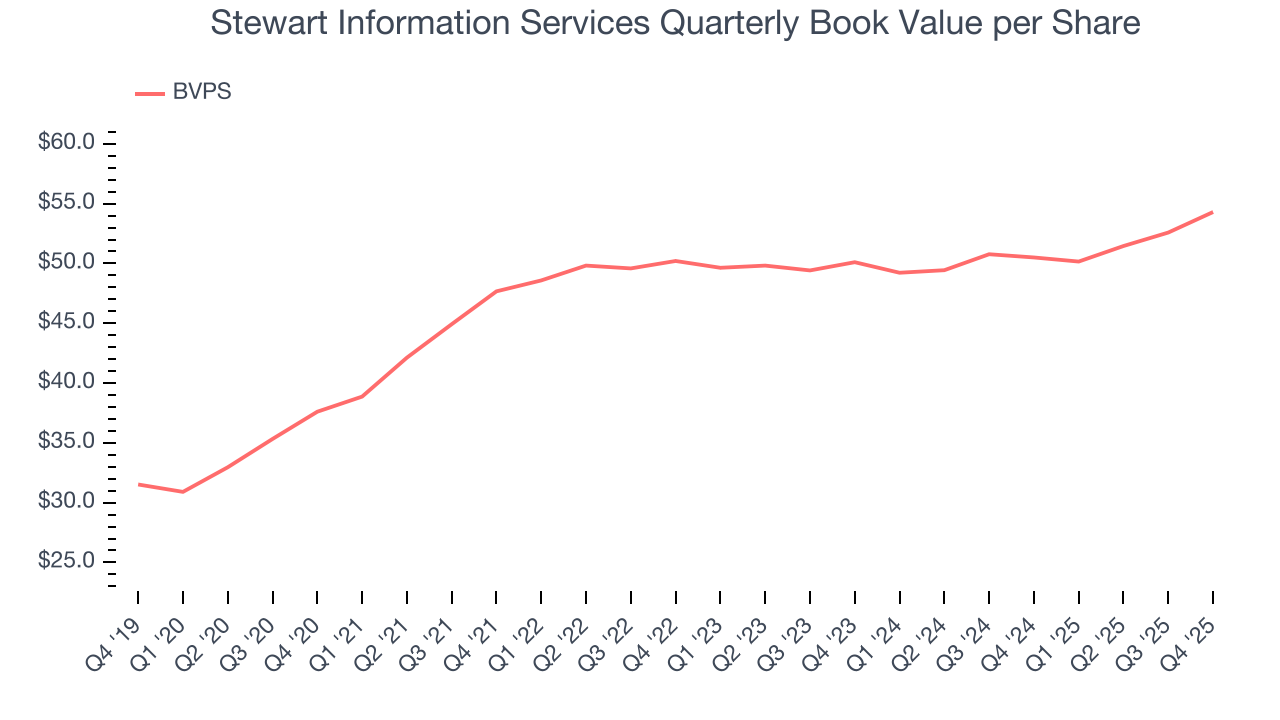

9. Book Value Per Share (BVPS)

Insurance companies are balance sheet businesses, collecting premiums upfront and paying out claims over time. The float–premiums collected but not yet paid out–are invested, creating an asset base supported by a liability structure. Book value per share (BVPS) captures this dynamic by measuring these assets (investment portfolio, cash, reinsurance recoverables) less liabilities (claim reserves, debt, future policy benefits). BVPS is essentially the residual value for shareholders.

We therefore consider BVPS very important to track for insurers and a metric that sheds light on business quality because it reflects long-term capital growth and is harder to manipulate than more commonly-used metrics like EPS.

Stewart Information Services’s BVPS grew at a decent 7.6% annual clip over the last five years. However, BVPS growth has recently decelerated to 4.1% annual growth over the last two years (from $50.11 to $54.30 per share).

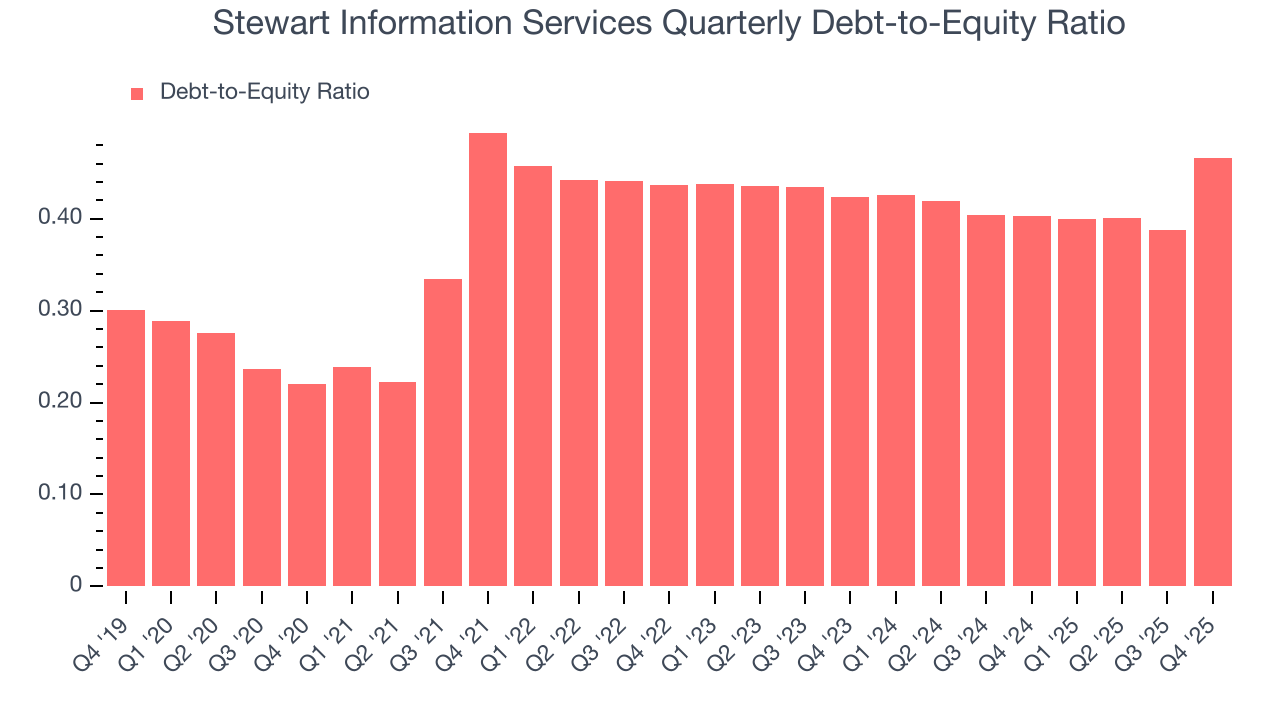

10. Balance Sheet Assessment

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

Stewart Information Services currently has $768.8 million of debt and $1.65 billion of shareholder's equity on its balance sheet, and over the past four quarters, has averaged a debt-to-equity ratio of 0.4×. We think this is safe and raises no red flags. In general, we’re comfortable with any ratio below 1.0× for an insurance business. Anything below 0.5× is a bonus.

11. Return on Equity

Return on Equity, or ROE, ties everything together and is a vital metric. It tells us how much profit the insurer generates for each dollar of shareholder equity entrusted to management. Over a long period, insurers with higher ROEs tend to compound shareholder wealth faster through retained earnings, buybacks, and dividends.

Over the last five years, Stewart Information Services has averaged an ROE of 12.5%, uninspiring for a company operating in a sector where the average shakes out around 12.5%.

12. Key Takeaways from Stewart Information Services’s Q4 Results

It was good to see Stewart Information Services beat analysts’ EPS expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. Zooming out, we think this was a solid print. The stock remained flat at $68.92 immediately following the results.

13. Is Now The Time To Buy Stewart Information Services?

Updated: March 14, 2026 at 12:38 AM EDT

Before investing in or passing on Stewart Information Services, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

Stewart Information Services has a few positive attributes, but it doesn’t top our wishlist. Although its revenue growth was uninspiring over the last five years, its growth over the next 12 months is expected to be higher. And while Stewart Information Services’s declining EPS over the last five years makes it a less attractive asset to the public markets, its projected EPS for the next year implies the company’s fundamentals will improve.

Stewart Information Services’s P/B ratio based on the next 12 months is 1.1x. While this valuation is fair, the upside isn’t great compared to the potential downside. We're pretty confident there are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $81.33 on the company (compared to the current share price of $64.48).