Bowhead Specialty (BOW)

Bowhead Specialty is an amazing business. Its revenue and EPS are projected to skyrocket next year, an optimistic sign for its share price.― StockStory Analyst Team

1. News

2. Summary

Why We Like Bowhead Specialty

Named after the Arctic bowhead whale known for navigating challenging waters, Bowhead Specialty Holdings (NYSE:BOW) is a specialty insurance company that provides customized coverage for complex and high-risk commercial sectors.

- Annual revenue growth of 47.1% over the past three years was outstanding, reflecting market share gains this cycle

- Earnings per share grew by 28.9% annually over the last three years, massively outpacing its peers

- Annual book value per share growth of 30.9% over the last two years was superb and indicates its capital strength increased during this cycle

We see a bright future for Bowhead Specialty. The valuation looks fair based on its quality, and we think now is a good time to buy the stock.

Why Is Now The Time To Buy Bowhead Specialty?

Bowhead Specialty is trading at $22.59 per share, or 1.5x forward P/B. Valuation is lower than most companies in the insurance space, and we believe Bowhead Specialty is attractively-priced for its quality.

Our analysis and backtests show high-quality businesses routinely outperform the market over a multi-year period, especially when priced like this.

3. Bowhead Specialty (BOW) Research Report: Q4 CY2025 Update

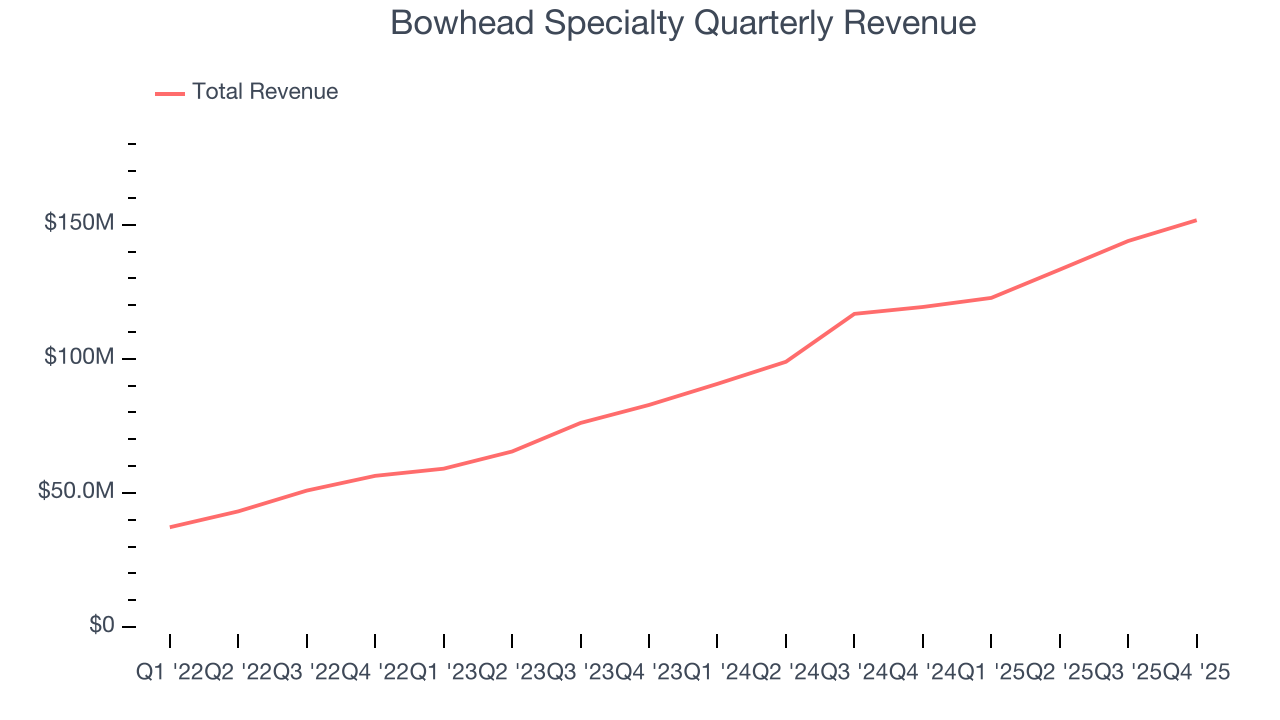

Specialty insurance company Bowhead Specialty Holdings (NYSE:BOW) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 27.1% year on year to $151.7 million. Its GAAP profit of $0.44 per share was 2.2% below analysts’ consensus estimates.

Bowhead Specialty (BOW) Q4 CY2025 Highlights:

- Net Premiums Earned: $134.3 million vs analyst estimates of $129.2 million (25.7% year-on-year growth, 3.9% beat)

- Revenue: $151.7 million vs analyst estimates of $143.1 million (27.1% year-on-year growth, 6% beat)

- Combined Ratio: 96.9% vs analyst estimates of 95.9% (100 basis point miss)

- EPS (GAAP): $0.44 vs analyst expectations of $0.45 (2.2% miss)

- Book Value per Share: $13.70 (20.8% year-on-year growth)

- Market Capitalization: $812.7 million

Company Overview

Named after the Arctic bowhead whale known for navigating challenging waters, Bowhead Specialty Holdings (NYSE:BOW) is a specialty insurance company that provides customized coverage for complex and high-risk commercial sectors.

Bowhead Specialty operates in the specialty insurance market, focusing on segments that traditional insurers often avoid due to their complexity or elevated risk profiles. The company underwrites policies across several specialized areas including excess and surplus lines, professional liability, marine and energy, aviation, and specialty property coverage.

Unlike standard insurers that offer standardized policies for common risks, Bowhead tailors its coverage to address unique exposures faced by businesses in challenging industries. For example, a deep-water drilling company might secure a customized policy from Bowhead that covers specific operational risks that standard commercial policies would exclude.

The company employs specialized underwriters with deep industry knowledge who can accurately assess and price complex risks. This expertise allows Bowhead to serve clients ranging from construction firms operating in hurricane-prone regions to technology companies facing emerging cyber threats.

Bowhead generates revenue through premium payments from policyholders, with pricing reflecting the specialized nature of the risks covered. The company balances its risk exposure through strategic reinsurance arrangements, allowing it to take on larger or more volatile risks while maintaining financial stability.

The company distributes its products primarily through a network of independent brokers and agents who specialize in connecting clients with appropriate specialty coverage. These intermediaries value Bowhead's underwriting flexibility and willingness to consider risks that larger, more standardized insurers might decline.

4. Property & Casualty Insurance

Property & Casualty (P&C) insurers protect individuals and businesses against financial loss from damage to property or from legal liability. This is a cyclical industry, and the sector benefits when there is 'hard market', characterized by strong premium rate increases that outpace loss and cost inflation, resulting in robust underwriting margins. The opposite is true in a 'soft market'. Interest rates also matter, as they determine the yields earned on fixed-income portfolios. On the other hand, P&C insurers face a major secular headwind from the increasing frequency and severity of catastrophe losses due to climate change. Furthermore, the liability side of the business is pressured by 'social inflation'—the trend of rising litigation costs and larger jury awards.

Bowhead Specialty's competitors include other specialty insurance providers such as Markel Corporation (NYSE:MKL), RLI Corp (NYSE:RLI), W.R. Berkley Corporation (NYSE:WRB), and Arch Capital Group (NASDAQ:ACGL).

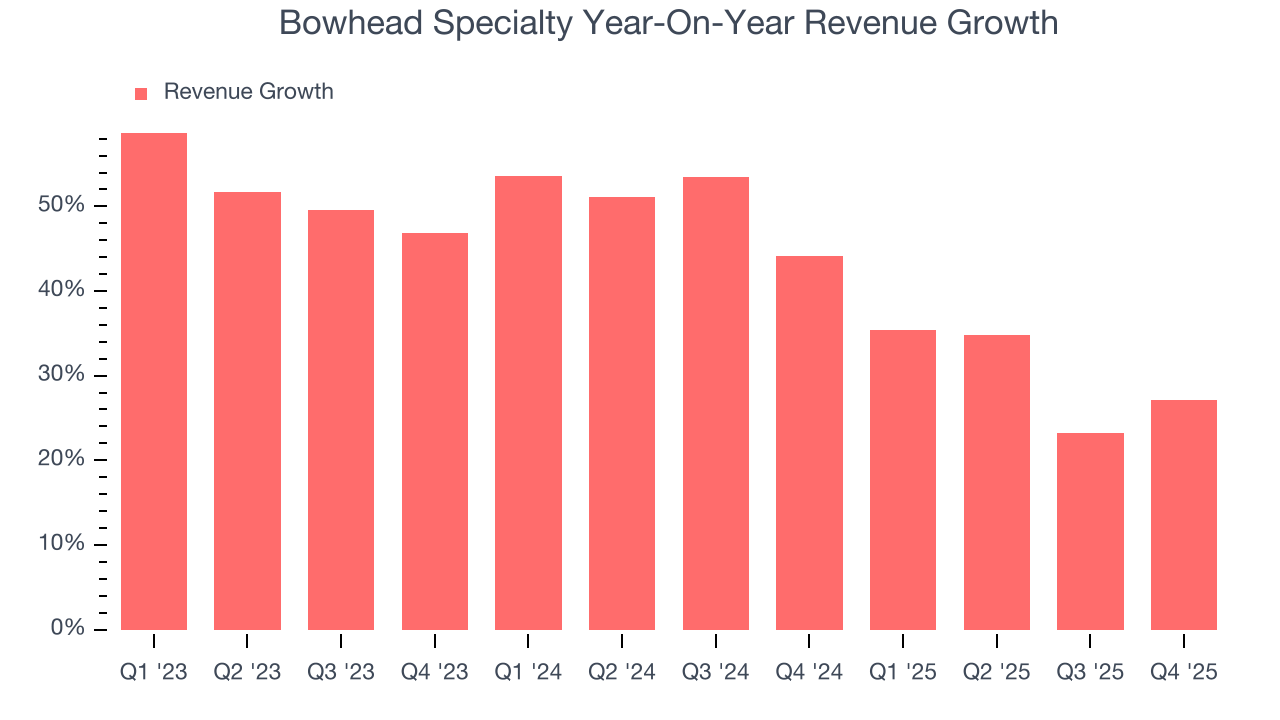

5. Revenue Growth

Insurance companies generate revenue three ways. The first is the core insurance business itself, represented in the income statement as premiums earned. The second source is investment income from investing the “float” (premiums collected but not yet paid out as claims) in assets such as fixed-income assets and equities. The third is fees from policy administration, annuities, and other value-added services. Luckily, Bowhead Specialty’s revenue grew at an incredible 47.1% compounded annual growth rate over the last three years. Its growth surpassed the average insurance company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within financials, a stretched historical view may miss recent interest rate changes, market returns, and industry trends. Bowhead Specialty’s annualized revenue growth of 39.5% over the last two years is below its three-year trend, but we still think the results suggest healthy demand.

This quarter, Bowhead Specialty reported robust year-on-year revenue growth of 27.1%, and its $151.7 million of revenue topped Wall Street estimates by 6%.

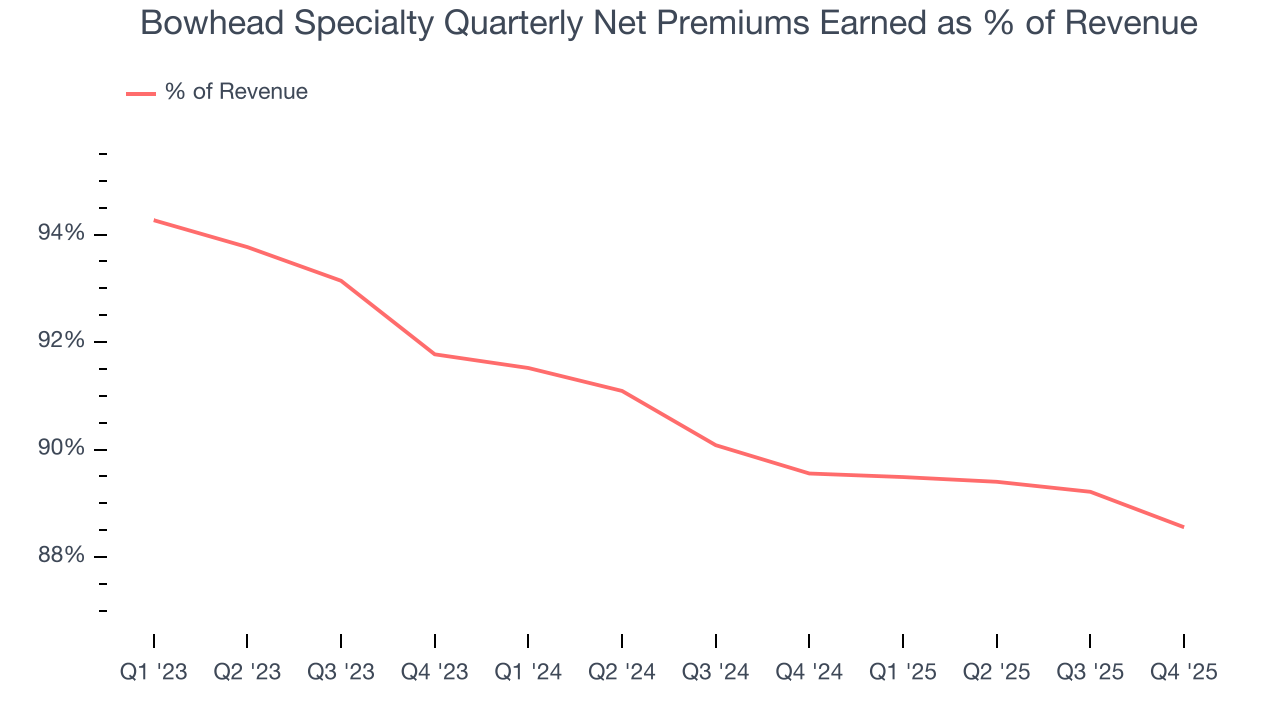

Net premiums earned made up 90.5% of the company’s total revenue during the last three years, meaning Bowhead Specialty lives and dies by its underwriting activities because non-insurance operations barely move the needle.

Net premiums earned commands greater market attention due to its reliability and consistency, whereas investment and fee income are often seen as more volatile revenue streams that fluctuate with market conditions.

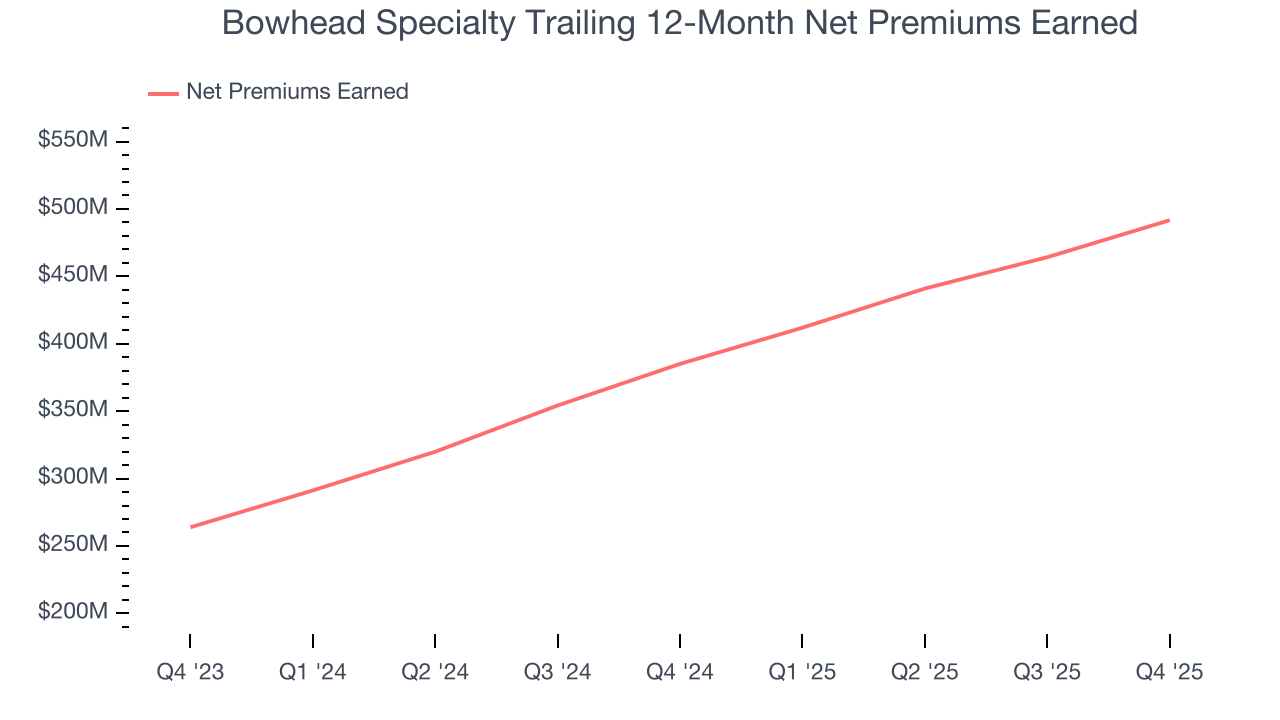

6. Net Premiums Earned

When insurers sell policies, they protect themselves from extremely large losses or an outsized accumulation of losses with reinsurance (insurance for insurance companies). Net premiums earned are therefore net of what’s ceded to reinsurers as a risk mitigation and transfer strategy.

Bowhead Specialty’s net premiums earned has grown at a 36.5% annualized rate over the last two years, much better than the broader insurance industry but slower than its total revenue.

This quarter, Bowhead Specialty’s net premiums earned was $134.3 million, up a hearty 25.7% year on year and topping Wall Street Consensus estimates by 3.9%.

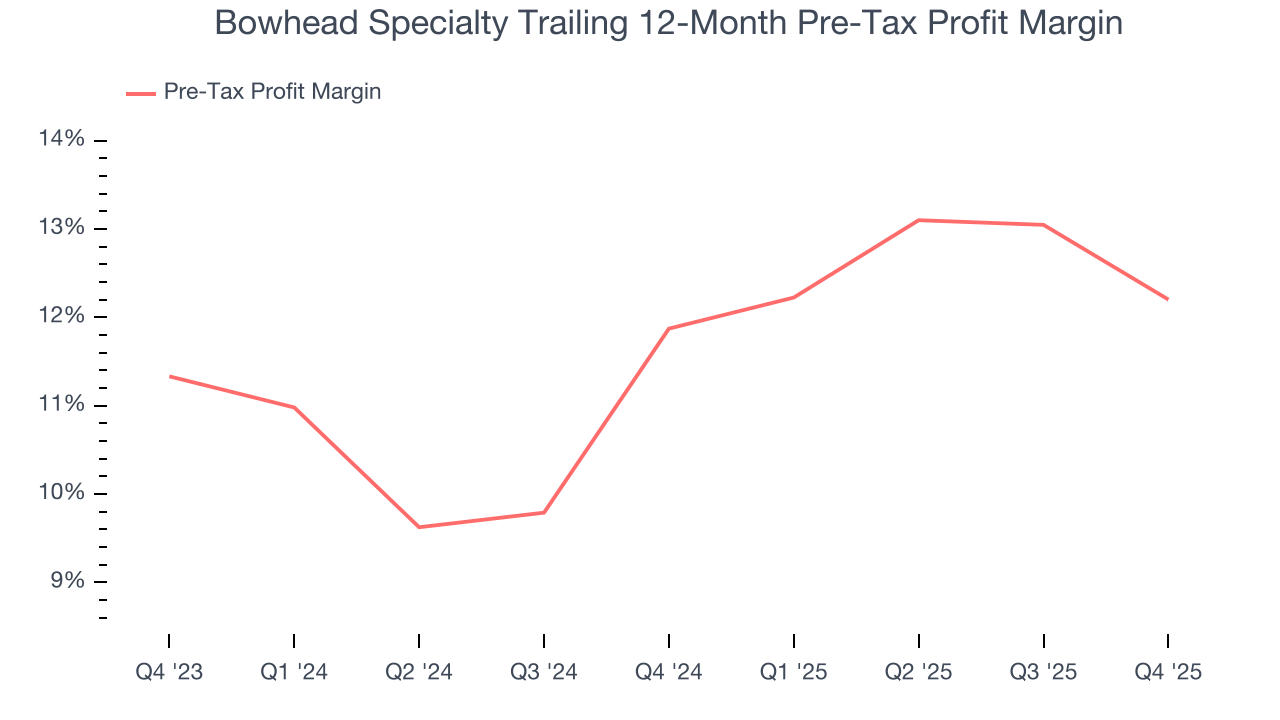

7. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For insurance companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

This is because insurers are balance sheet businesses, where assets and liabilities define the core economics. This means that interest income and expense should be factored into the definition of profit but taxes - which are largely out of a company’s control - should not.

Over the last two years, Bowhead Specialty’s pre-tax profit margin couldn’t build momentum, hanging around 12.2%.

Bowhead Specialty’s pre-tax profit margin came in at 11.7% this quarter. This result was 3.6 percentage points worse than the same quarter last year.

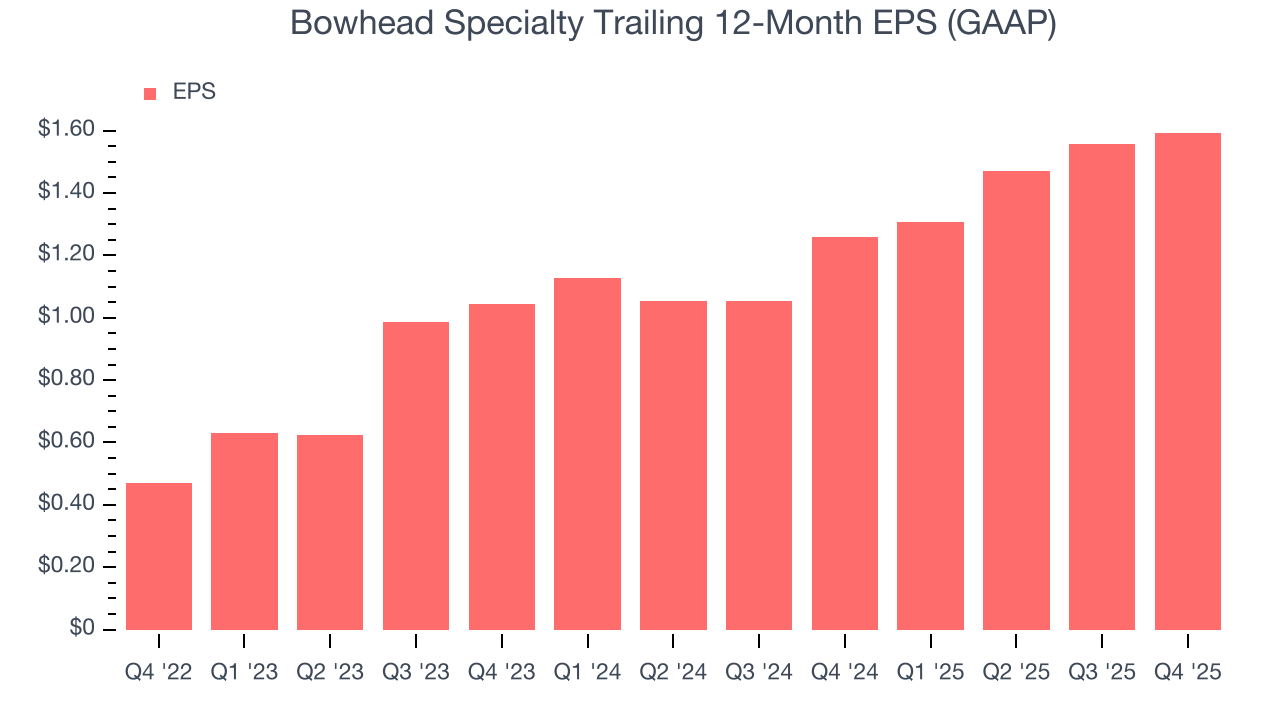

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Bowhead Specialty’s EPS grew at an astounding 28.9% compounded annual growth rate over the last three years. However, this performance was lower than its 47.1% annualized revenue growth, telling us the company became less profitable on a per-share basis as it expanded.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

In Q4, Bowhead Specialty reported EPS of $0.44, up from $0.41 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects Bowhead Specialty’s full-year EPS of $1.59 to grow 25.3%.

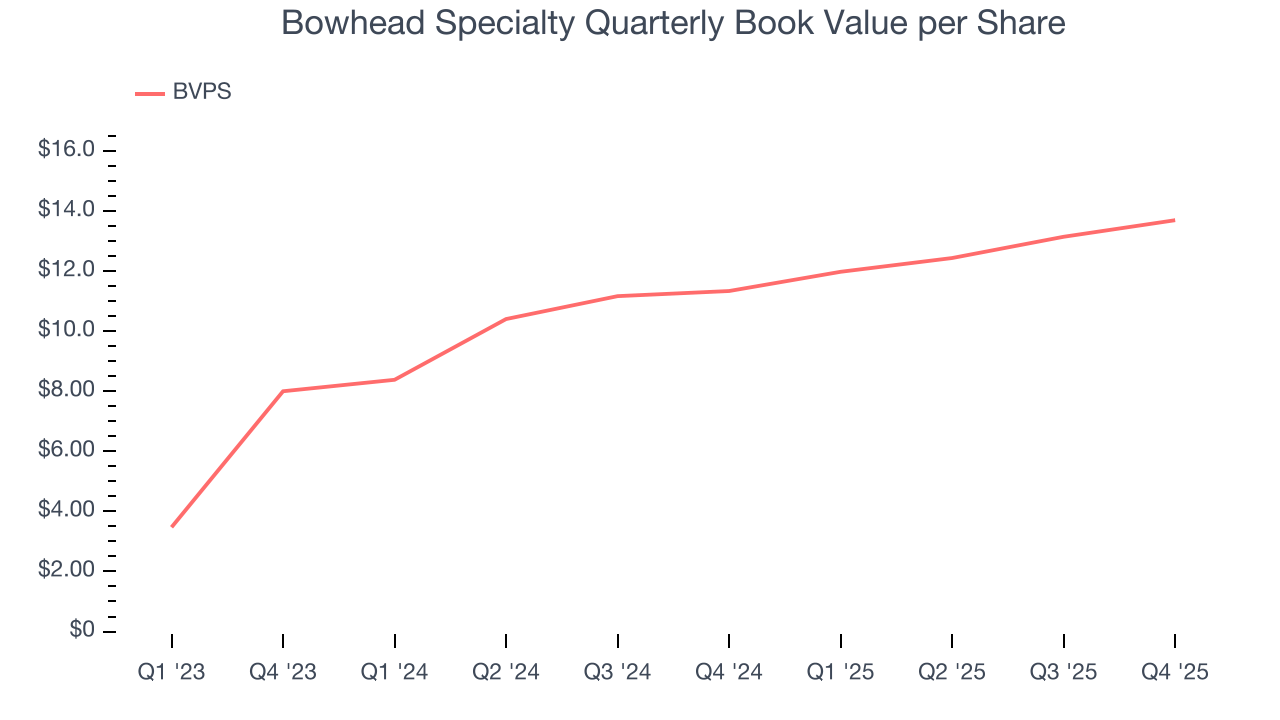

9. Book Value Per Share (BVPS)

Insurance companies are balance sheet businesses, collecting premiums upfront and paying out claims over time. The float–premiums collected but not yet paid out–are invested, creating an asset base supported by a liability structure. Book value per share (BVPS) captures this dynamic by measuring these assets (investment portfolio, cash, reinsurance recoverables) less liabilities (claim reserves, debt, future policy benefits). BVPS is essentially the residual value for shareholders.

We therefore consider BVPS very important to track for insurers and a metric that sheds light on business quality because it reflects long-term capital growth and is harder to manipulate than more commonly-used metrics like EPS.

Fortunately for investors, Bowhead Specialty’s BVPS grew at an incredible 30.8% annual clip over the last two years.

10. Balance Sheet Assessment

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

Bowhead Specialty has no debt, so leverage is not an issue here.

11. Key Takeaways from Bowhead Specialty’s Q4 Results

We were impressed by how significantly Bowhead Specialty blew past analysts’ net premiums earned expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. On the other hand, its EPS missed. Overall, this print had some key positives. The stock remained flat at $24.83 immediately after reporting.

12. Is Now The Time To Buy Bowhead Specialty?

Updated: March 15, 2026 at 12:20 AM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Bowhead Specialty, you should also grasp the company’s longer-term business quality and valuation.

There are multiple reasons why we think Bowhead Specialty is an elite insurance company. For starters, its revenue growth was exceptional over the last three years. On top of that, its net premiums earned growth was exceptional over the last two years, and its astounding EPS growth over the last three years shows its profits are trickling down to shareholders.

Bowhead Specialty’s P/B ratio based on the next 12 months is 1.5x. Looking at the insurance space today, Bowhead Specialty’s qualities as one of the best businesses really stand out, and we like it at this price.

Wall Street analysts have a consensus one-year price target of $31.29 on the company (compared to the current share price of $22.59), implying they see 38.5% upside in buying Bowhead Specialty in the short term.