ePlus (PLUS)

We’re skeptical of ePlus. Its weak sales growth and declining returns on capital show its demand and profits are shrinking.― StockStory Analyst Team

1. News

2. Summary

Why We Think ePlus Will Underperform

Starting as a financing company in 1990 before evolving into a full-service technology provider, ePlus (NASDAQ:PLUS) provides comprehensive IT solutions, professional services, and financing options to help organizations optimize their technology infrastructure and supply chain processes.

- Projected sales growth of 2.3% for the next 12 months suggests sluggish demand

- Subpar operating margin constrains its ability to invest in process improvements or effectively respond to new competitive threats

- On the bright side, its incremental sales over the last five years have been more profitable as its earnings per share increased by 10.3% annually, topping its revenue gains

ePlus doesn’t measure up to our expectations. There are more promising prospects in the market.

Why There Are Better Opportunities Than ePlus

At $84.92 per share, ePlus trades at 18.5x forward P/E. This multiple is quite expensive for the quality you get.

Paying up for elite businesses with strong earnings potential is better than investing in lower-quality companies with shaky fundamentals. That’s how you avoid big downside over the long term.

3. ePlus (PLUS) Research Report: Q4 CY2025 Update

IT solutions provider ePlus (NASDAQ:PLUS) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 20.3% year on year to $614.8 million. Its non-GAAP profit of $1.45 per share was 43.6% above analysts’ consensus estimates.

ePlus (PLUS) Q4 CY2025 Highlights:

- Revenue: $614.8 million vs analyst estimates of $551.8 million (20.3% year-on-year growth, 11.4% beat)

- Adjusted EPS: $1.45 vs analyst estimates of $1.01 (43.6% beat)

- Adjusted EBITDA: $53.38 billion vs analyst estimates of $41.1 million (8,683% margin, significant beat)

- Operating Margin: 7.1%, up from 5.6% in the same quarter last year

- Market Capitalization: $2.22 billion

Company Overview

Starting as a financing company in 1990 before evolving into a full-service technology provider, ePlus (NASDAQ:PLUS) provides comprehensive IT solutions, professional services, and financing options to help organizations optimize their technology infrastructure and supply chain processes.

ePlus operates through two main business segments: technology and financing. The technology segment, which generates about 98% of revenue, offers hardware, software, and a suite of professional and managed services. The company partners with major technology manufacturers like Cisco, Amazon Web Services, Microsoft, Dell EMC, and NetApp to deliver solutions across cloud computing, cybersecurity, data center infrastructure, networking, and collaboration technologies.

The company's professional services team helps clients design and implement complex IT systems, while their managed services division provides ongoing support through offerings like cloud management, security monitoring, and IT help desk services. For example, a healthcare organization might engage ePlus to design a secure cloud infrastructure, implement the solution, and then provide 24/7 monitoring and management.

ePlus serves mid-market to large enterprises across diverse sectors, with telecommunications, technology, government/education, healthcare, and financial services being their primary markets. Verizon Communications represents a significant customer, accounting for approximately 19% of net sales.

The financing segment, though smaller at just 2% of revenue, contributes about 16% of operating income. This division helps customers acquire technology through various financing arrangements including leases, loans, and consumption-based models. Beyond simple financing, ePlus offers asset management services throughout the technology lifecycle, from procurement to end-of-life disposal.

With operations primarily in the United States and select international markets including the United Kingdom, European Union, India, and Singapore, ePlus employs hundreds of sales and technical professionals who hold certifications from leading technology manufacturers. This expertise allows the company to design and deliver integrated solutions that address complex business challenges rather than simply selling individual products.

4. IT Distribution & Solutions

IT Distribution & Solutions will be buoyed by the increasing complexity of IT ecosystems, rising cloud adoption, and demand for cybersecurity solutions. Enterprises are less likely than ever to embark on these complicated journeys solo, and companies in the sector boast expertise and scale in these areas. However, cloud migration also means less need for hardware, which could dent demand for large portions of the product portfolio and hurt margins. Additionally, planning for potentially supply chain disruptions is ongoing, as the COVID-19 pandemic showed how damaging a pause in global trade could be in areas like semiconductor procurement.

ePlus competes with large IT solution providers and value-added resellers such as CDW (NASDAQ:CDW), Insight Enterprises (NASDAQ:NSIT), and Connection (NASDAQ:CNXN), as well as with the professional services divisions of major technology manufacturers and consulting firms.

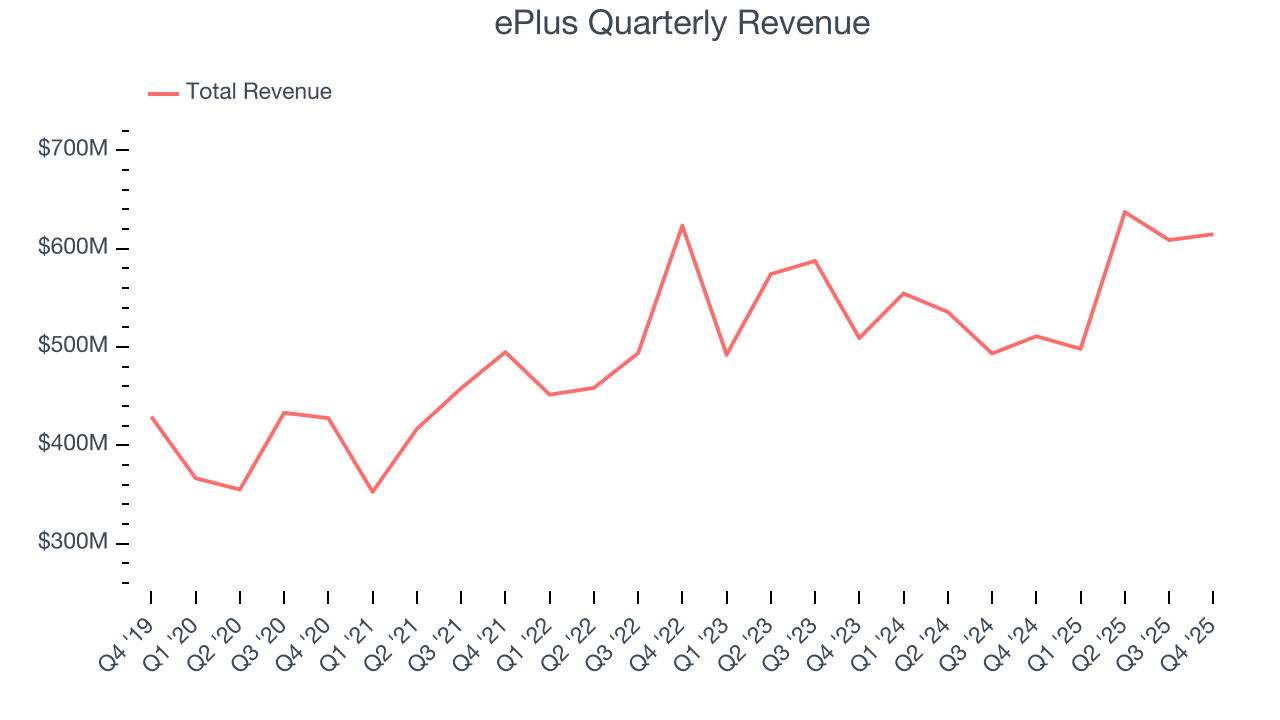

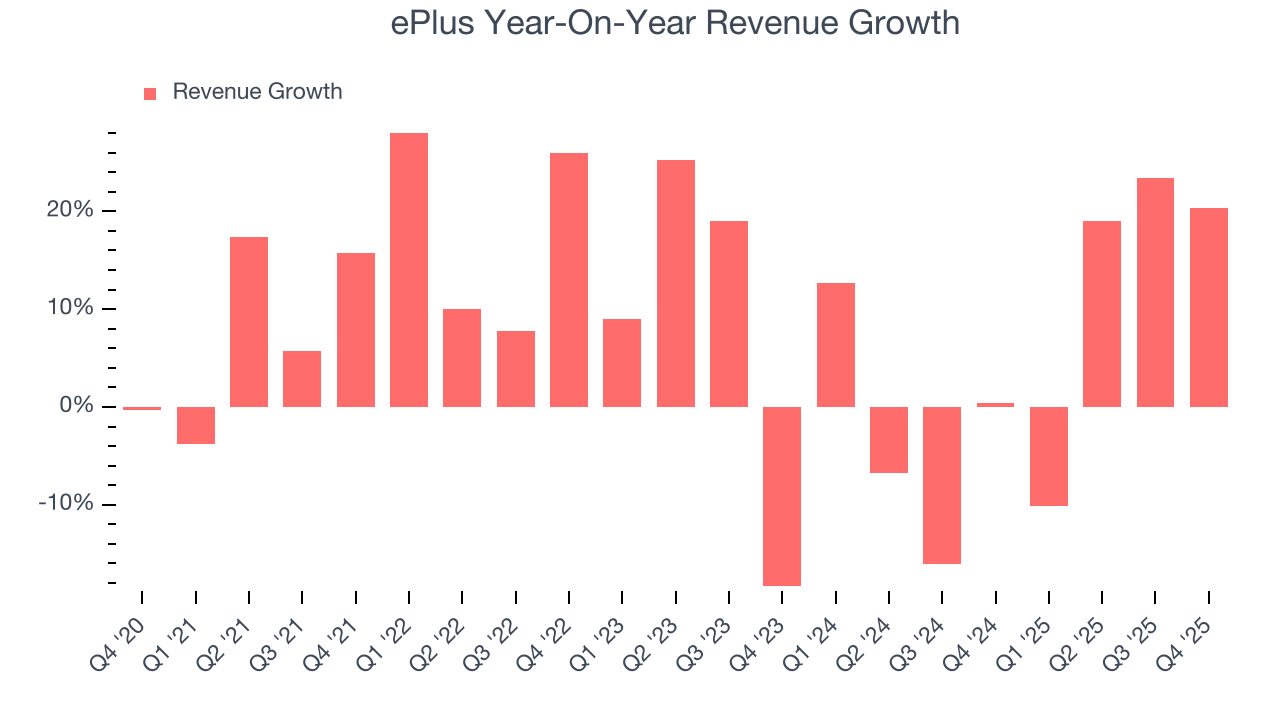

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years.

With $2.36 billion in revenue over the past 12 months, ePlus is a mid-sized business services company, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale. On the bright side, it can still flex high growth rates because it’s working from a smaller revenue base.

As you can see below, ePlus grew its sales at a solid 8.3% compounded annual growth rate over the last five years. This shows it had high demand, a useful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. ePlus’s recent performance shows its demand has slowed as its annualized revenue growth of 4.4% over the last two years was below its five-year trend.

This quarter, ePlus reported robust year-on-year revenue growth of 20.3%, and its $614.8 million of revenue topped Wall Street estimates by 11.4%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will see some demand headwinds.

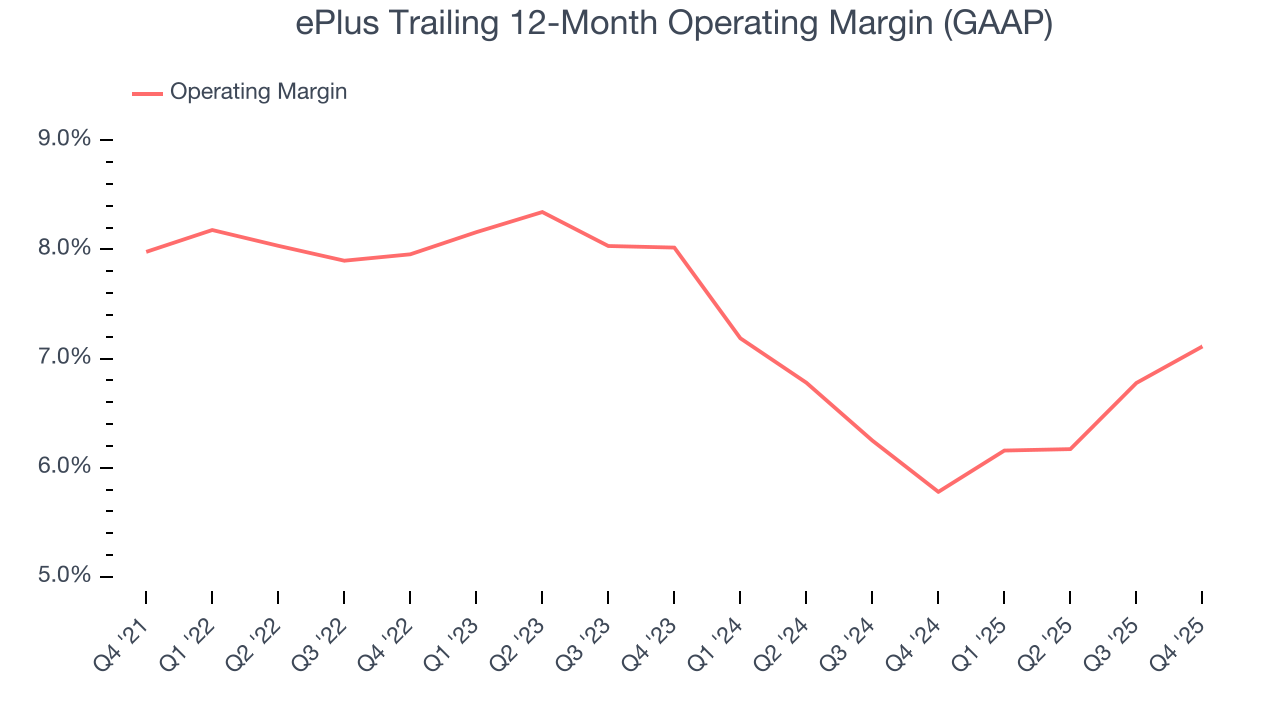

6. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

ePlus’s operating margin has been trending up over the last 12 months and averaged 7.3% over the last five years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports paltry profitability for a business services business.

Looking at the trend in its profitability, ePlus’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, ePlus generated an operating margin profit margin of 7.1%, up 1.5 percentage points year on year. This increase was a welcome development and shows it was more efficient.

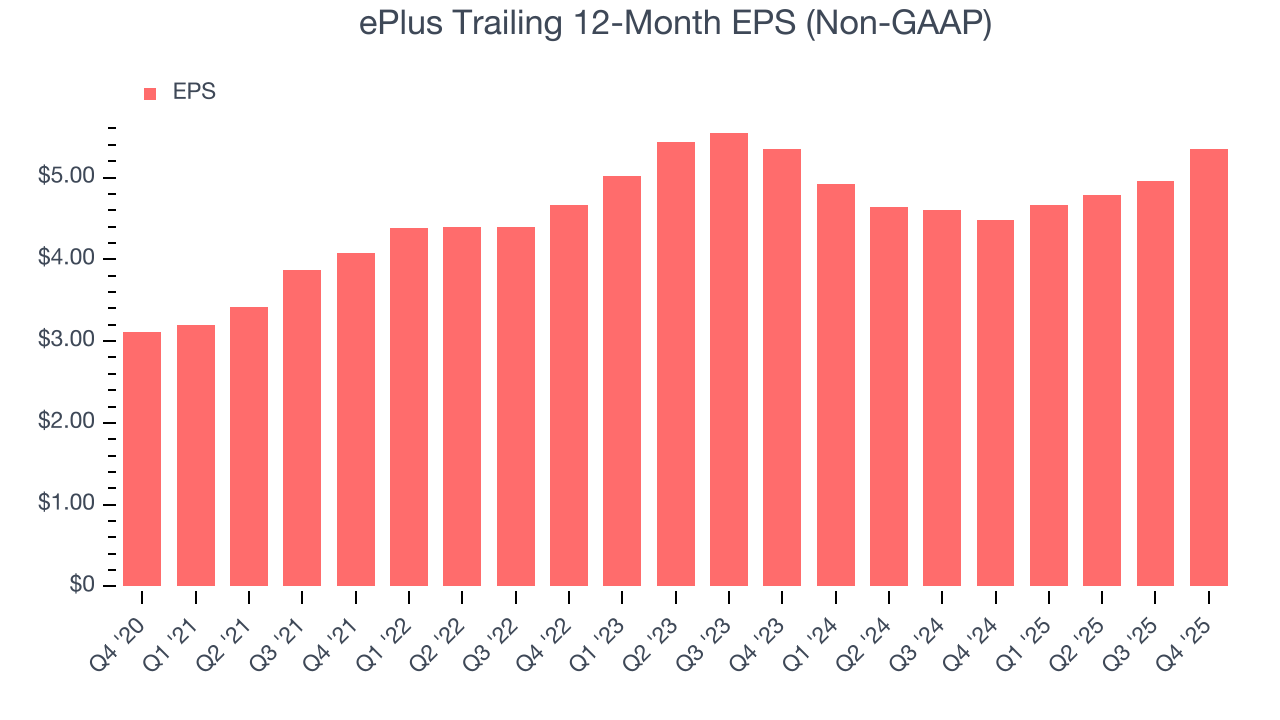

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

ePlus’s EPS grew at a remarkable 11.5% compounded annual growth rate over the last five years, higher than its 8.3% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t improve.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For ePlus, EPS didn’t budge over the last two years, a regression from its five-year trend. We hope it can revert to earnings growth in the coming years.

In Q4, ePlus reported adjusted EPS of $1.45, up from $1.06 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects ePlus’s full-year EPS of $5.35 to shrink by 5%.

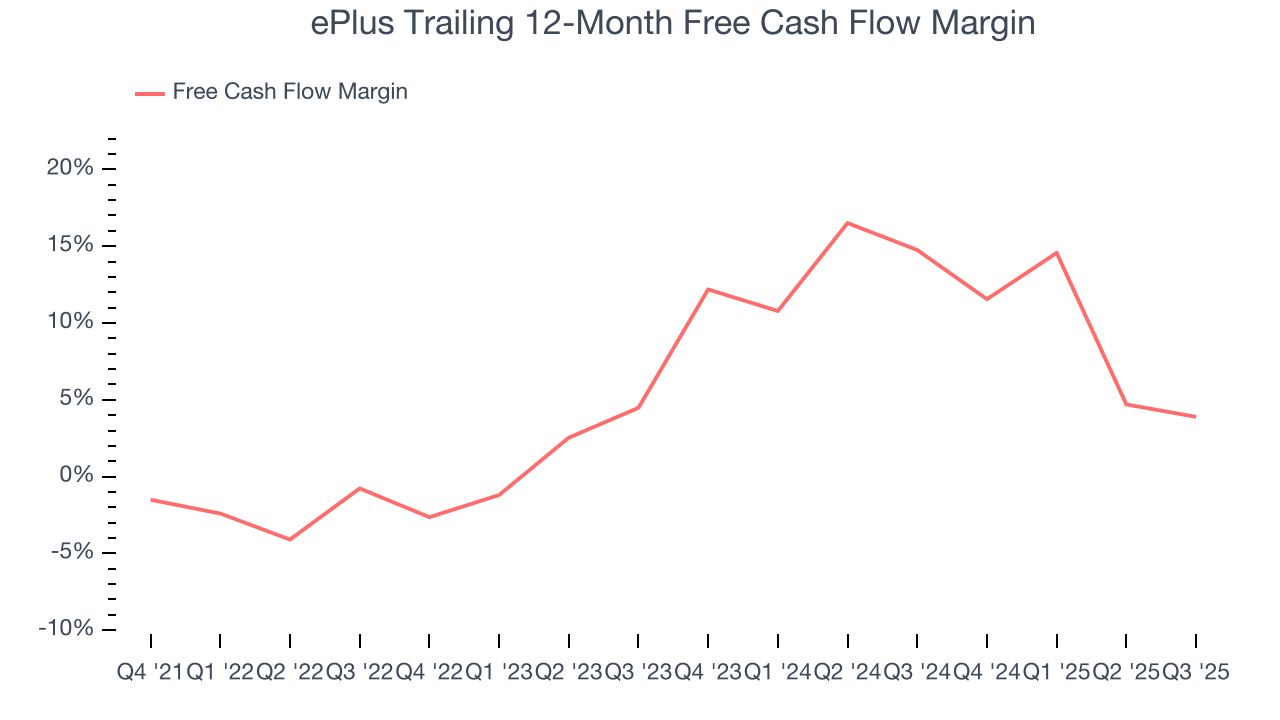

8. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

ePlus has shown mediocre cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 4.6%, subpar for a business services business.

Taking a step back, an encouraging sign is that ePlus’s margin expanded by 4.1 percentage points during that time. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability was flat.

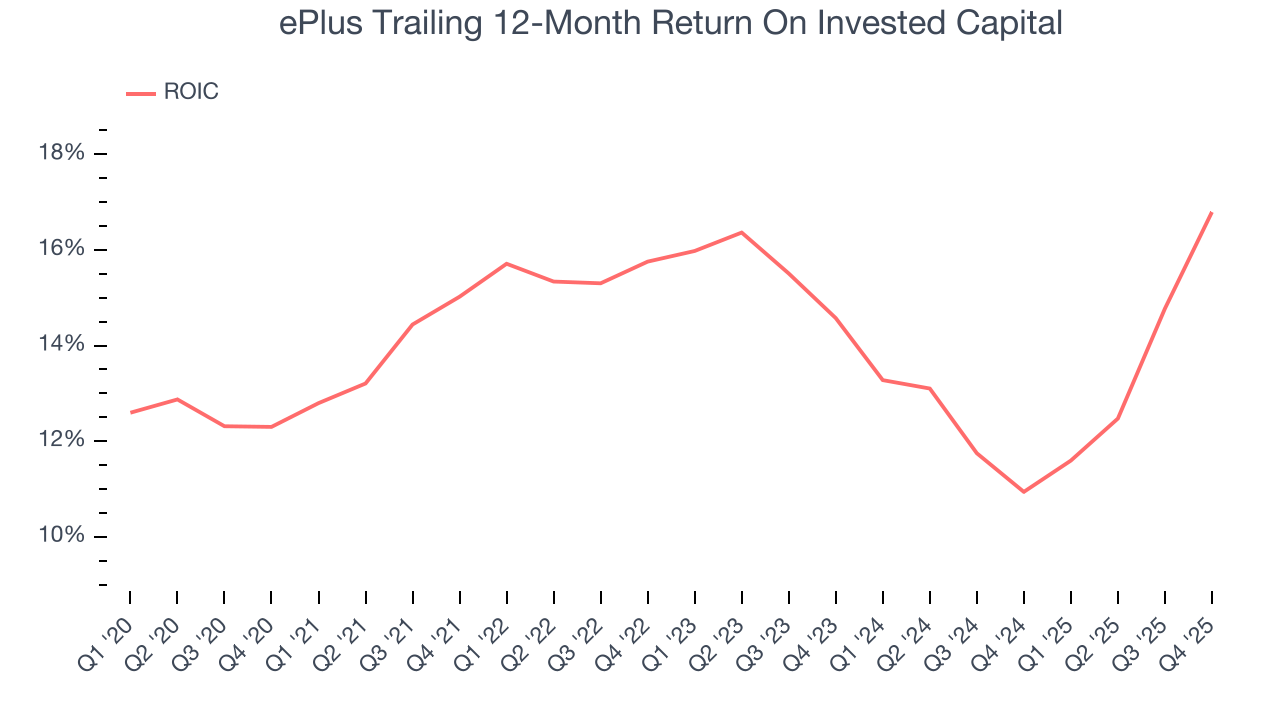

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Although ePlus hasn’t been the highest-quality company lately, it historically found a few growth initiatives that worked. Its five-year average ROIC was 14.6%, higher than most business services businesses.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. On average, ePlus’s ROIC decreased by 1.5 percentage points annually each year over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

10. Key Takeaways from ePlus’s Q4 Results

It was good to see ePlus beat analysts’ EPS expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this quarter featured some important positives. The stock traded up 3% to $88.67 immediately following the results.

11. Is Now The Time To Buy ePlus?

Updated: February 4, 2026 at 5:04 PM EST

When considering an investment in ePlus, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

ePlus isn’t a terrible business, but it doesn’t pass our quality test. Although its revenue growth was solid over the last five years, it’s expected to deteriorate over the next 12 months and its projected EPS for the next year is lacking. And while the company’s rising cash profitability gives it more optionality, the downside is its operating margins are low compared to other business services companies.

ePlus’s P/E ratio based on the next 12 months is 16.9x. This valuation multiple is fair, but we don’t have much faith in the company. We're fairly confident there are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $108 on the company (compared to the current share price of $88.67).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.