EchoStar (SATS)

We’re wary of EchoStar. Not only has its sales growth been weak but also its negative returns on capital show it destroyed value.― StockStory Analyst Team

1. News

2. Summary

Why We Think EchoStar Will Underperform

Following its 2023 acquisition of DISH Network, EchoStar (NASDAQ:SATS) provides satellite communications, pay-TV services, wireless networks, and broadband solutions across consumer and enterprise markets.

- Forecasted revenue decline of 4.7% for the upcoming 12 months implies demand will fall even further

- Poor expense management has led to adjusted operating margin losses

- EBITDA losses may force it to accept punitive lending terms or high-cost debt

EchoStar doesn’t check our boxes. There are more appealing investments to be made.

Why There Are Better Opportunities Than EchoStar

EchoStar is trading at $107.60 per share, or 27.9x forward EV-to-EBITDA. This multiple is higher than that of business services peers; it’s also rich for the business quality. Not a great combination.

There are stocks out there featuring similar valuation multiples with better fundamentals. We prefer to invest in those.

3. EchoStar (SATS) Research Report: Q4 CY2025 Update

Satellite communications company EchoStar (NASDAQGS:SATS) reported Q4 CY2025 results beating Wall Street’s revenue expectations, but sales fell by 4.3% year on year to $3.8 billion. Its GAAP loss of $4.19 per share was significantly below analysts’ consensus estimates.

EchoStar (SATS) Q4 CY2025 Highlights:

- Revenue: $3.8 billion vs analyst estimates of $3.75 billion (4.3% year-on-year decline, 1.3% beat)

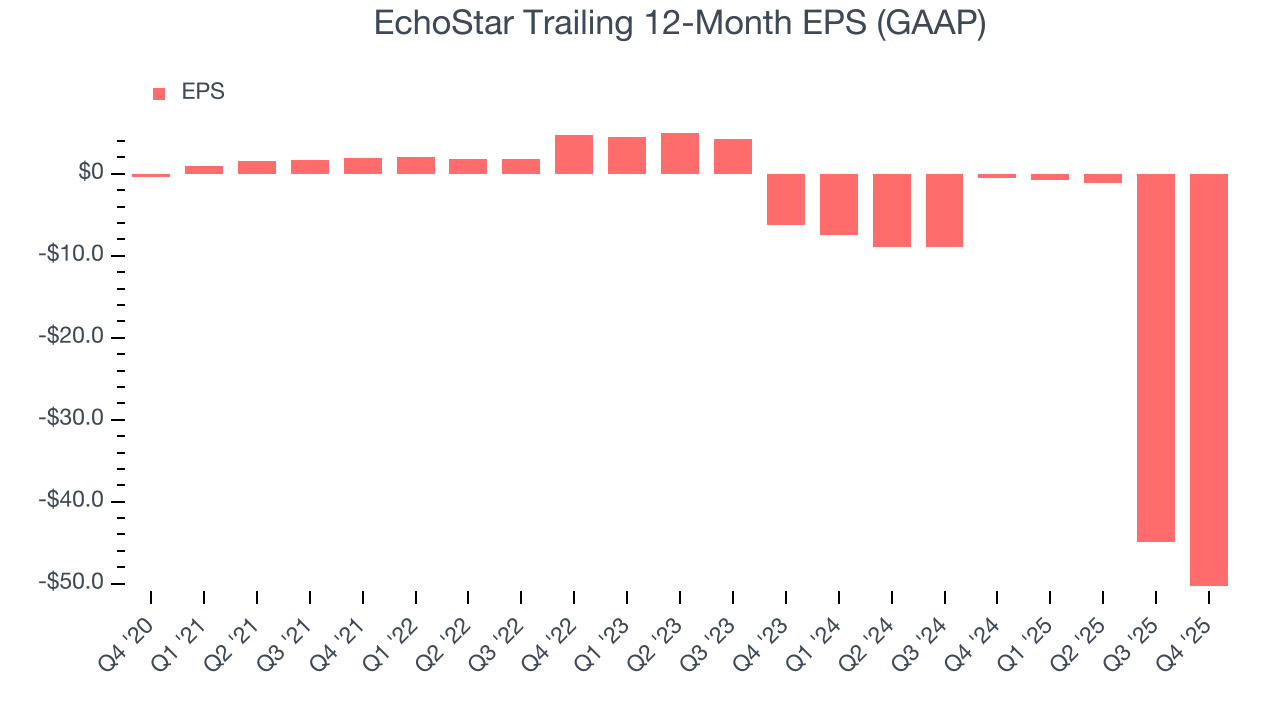

- EPS (GAAP): -$4.19 vs analyst estimates of -$0.75 (significant miss largely due to non-cash asset impairments and other expenses totaling approximately $17.63 billion)

- Adjusted EBITDA: $583.7 million vs analyst estimates of $355.3 million (15.4% margin, 64.3% beat due to a large "impairments and other" add-back in the Broadband and Satellite Services segment)

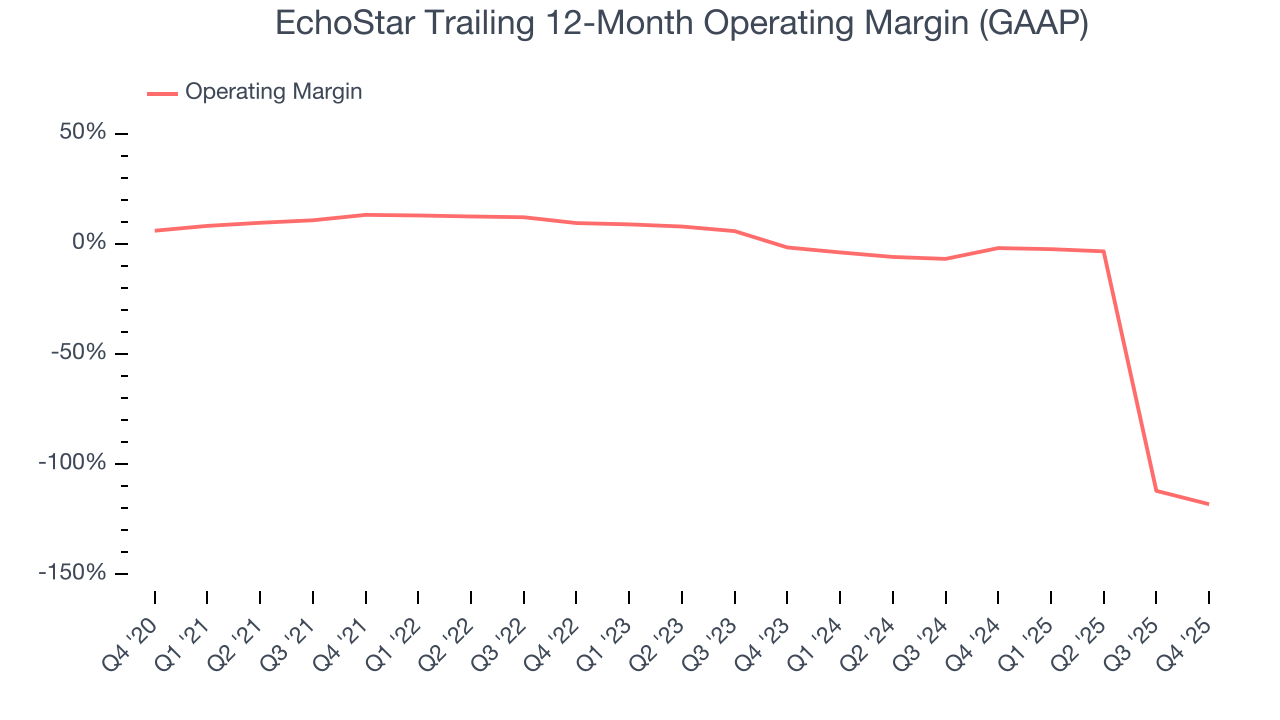

- Operating Margin: -20.5%, down from -1.6% in the same quarter last year

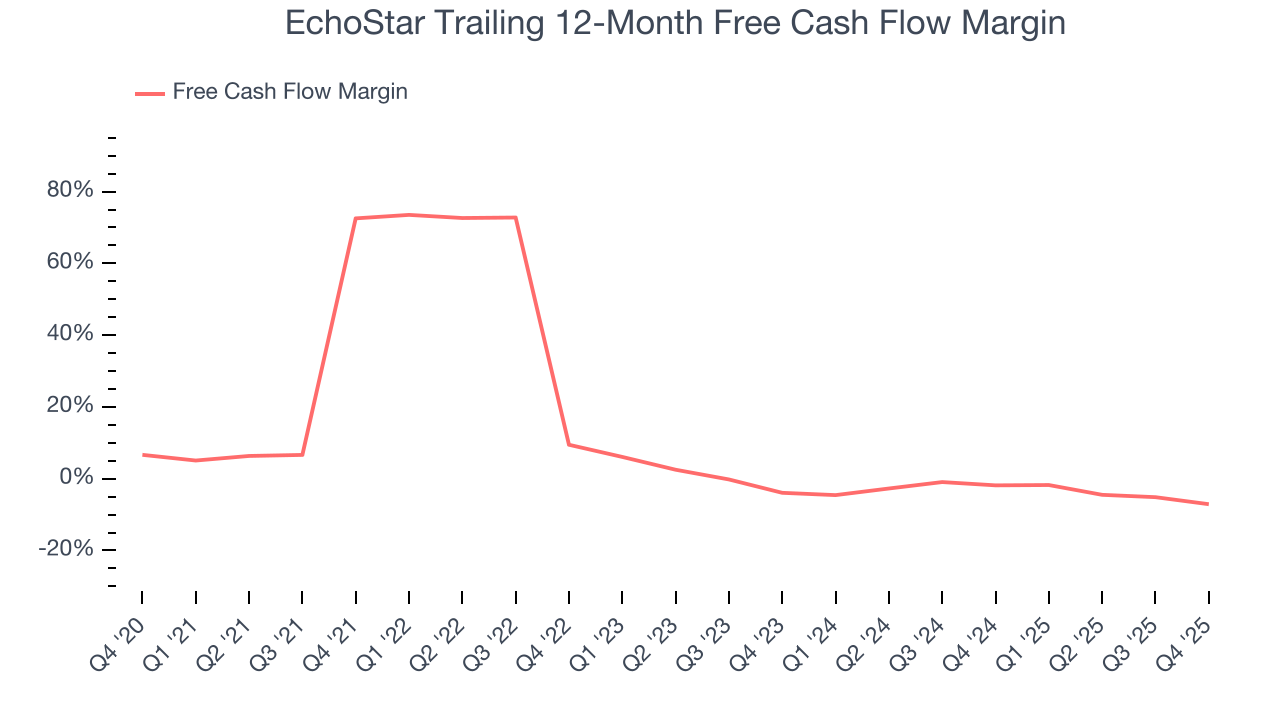

- Free Cash Flow was -$583.4 million compared to -$298.7 million in the same quarter last year

- Market Capitalization: $33.26 billion

Company Overview

Following its 2023 acquisition of DISH Network, EchoStar (NASDAQ:SATS) provides satellite communications, pay-TV services, wireless networks, and broadband solutions across consumer and enterprise markets.

EchoStar operates through four primary business segments that span both consumer and enterprise markets. The Pay-TV segment offers television services under the DISH and SLING brands, with DISH TV providing traditional satellite television and SLING TV delivering streaming content over the internet. These services reach millions of subscribers with various programming packages including national networks, local broadcasts, and specialty content.

The Retail Wireless segment provides prepaid and postpaid mobile services primarily under the Boost Mobile and Gen Mobile brands. Currently operating mostly as a mobile virtual network operator (MVNO) using T-Mobile and AT&T's networks, EchoStar is gradually transitioning to become a mobile network operator (MNO) as it builds out its own 5G infrastructure.

The 5G Network Deployment segment represents EchoStar's ambitious effort to build America's first cloud-native, Open Radio Access Network (O-RAN) based 5G network. The company has invested heavily in wireless spectrum licenses and has met significant FCC-mandated population coverage requirements, reaching over 73% of the U.S. population with its 5G service.

The Broadband and Satellite Services segment leverages EchoStar's satellite fleet to provide internet connectivity to consumers and businesses across the Americas. The company also offers enterprise solutions including network services, satellite ground systems, and telecommunications infrastructure to government agencies and corporate clients. Its recently launched EchoStar XXIV satellite has expanded broadband capacity across North and South America.

EchoStar generates revenue through subscription fees for its consumer services, equipment sales, and enterprise service contracts. The company maintains distribution networks that include direct sales channels, third-party retailers, and online platforms. For its satellite and enterprise services, EchoStar designs and manufactures much of its equipment, sometimes outsourcing production to third-party manufacturers.

4. Traditional Media & Publishing

The sector faces structural headwinds from declining linear TV viewership, shifts in advertising spend toward digital platforms, and ongoing challenges in monetizing print and broadcast content. However, for companies that invest wisely, tailwinds can include AI, the power of which can result in more personalized content creation and more detailed audience analysis. These can create a flywheel of success where one feeds into the other. Still there are outstanding questions around AI-generated content oversight, and the regulatory framework around this could evolve in unseen ways over the next few years.

EchoStar's competitors vary by business segment. In Pay-TV, it competes with cable providers like Comcast and Charter, as well as streaming services such as Netflix and Disney+. In wireless, it faces major carriers including Verizon, AT&T, and T-Mobile. For satellite broadband, key competitors include ViaSat, SpaceX's Starlink, and OneWeb.

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $15 billion in revenue over the past 12 months, EchoStar is a behemoth in the business services sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices.

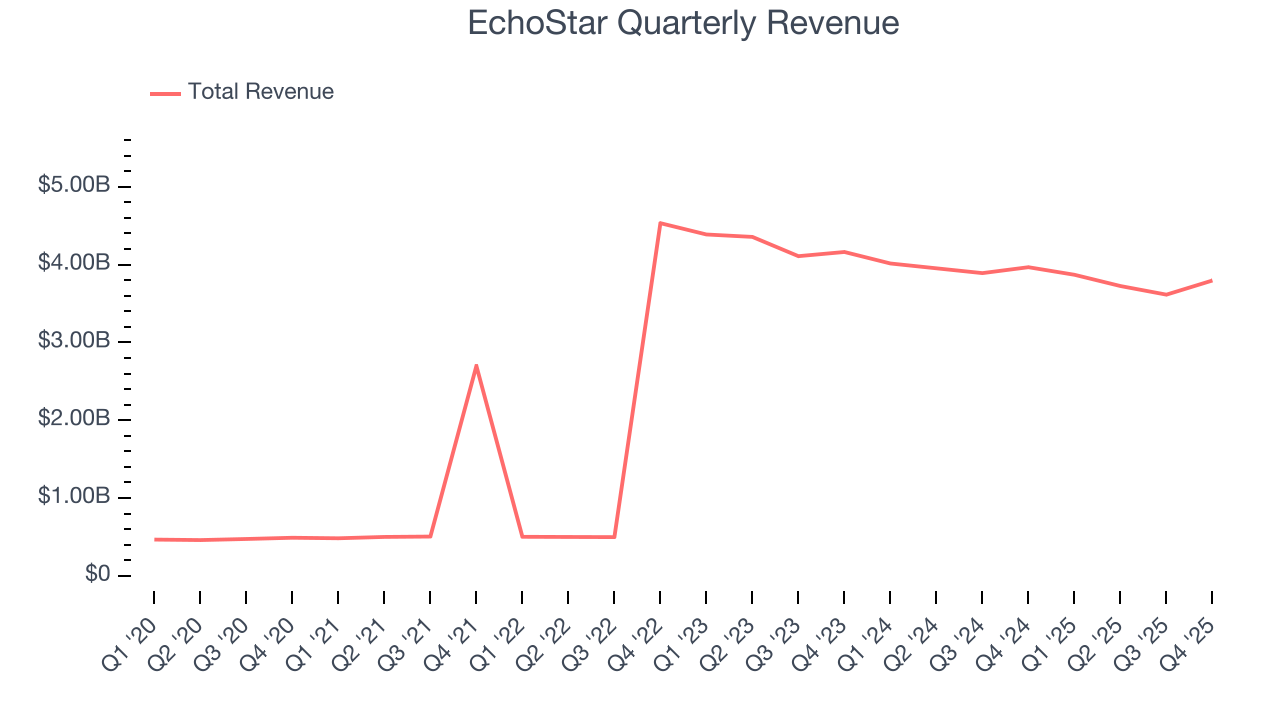

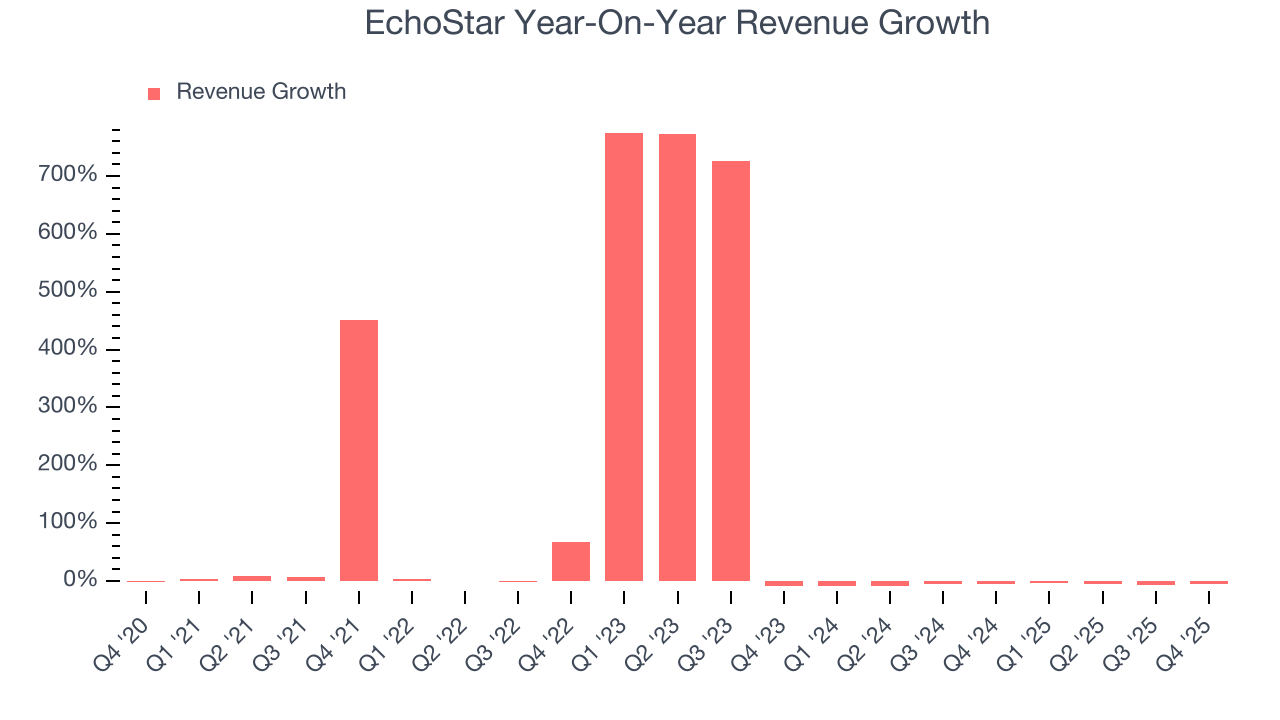

As you can see below, EchoStar’s sales grew at an incredible 51.4% compounded annual growth rate over the last five years. This shows it had high demand, a useful starting point for our analysis.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. EchoStar’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 6.1% over the last two years.

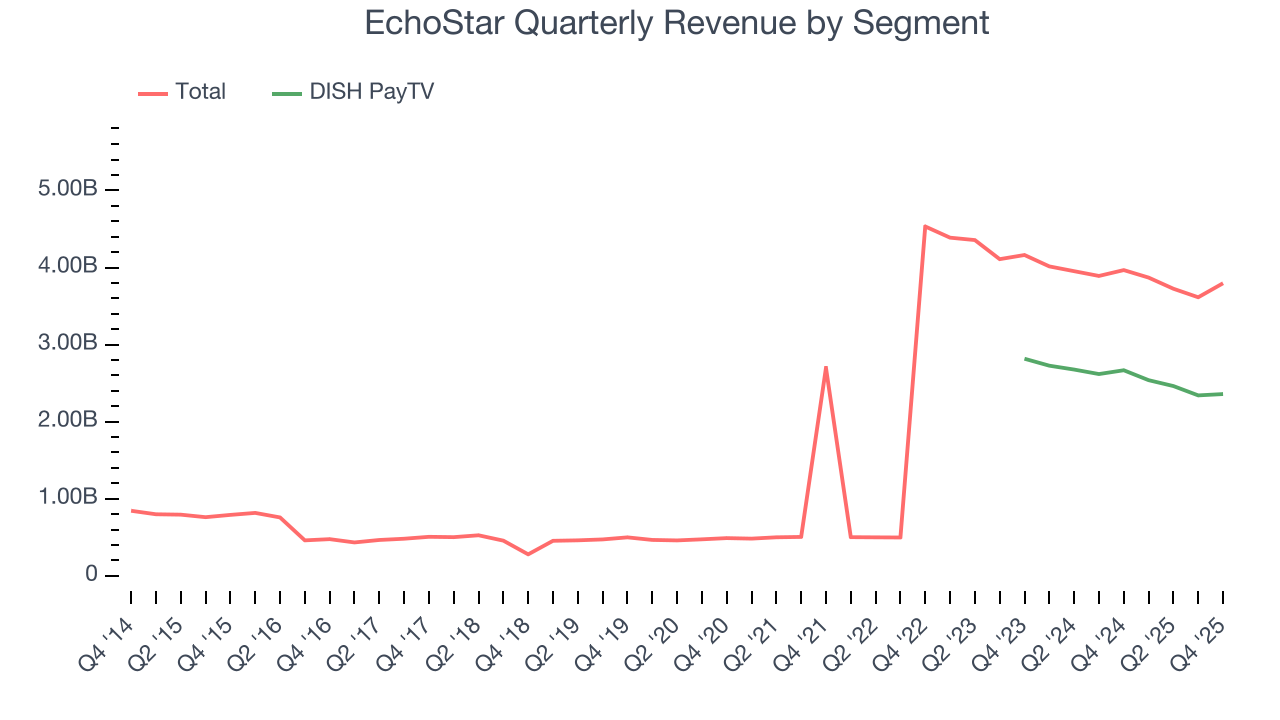

EchoStar also breaks out the revenue for its most important segment, DISH PayTV. Over the last two years, EchoStar’s DISH PayTV revenue averaged 8.5% year-on-year declines. This segment has lagged the company’s overall sales.

This quarter, EchoStar’s revenue fell by 4.3% year on year to $3.8 billion but beat Wall Street’s estimates by 1.3%.

Looking ahead, sell-side analysts expect revenue to decline by 4.2% over the next 12 months. While this projection is better than its two-year trend, it’s hard to get excited about a company that is struggling with demand.

6. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

EchoStar’s high expenses have contributed to an average operating margin of negative 29.6% over the last five years. Unprofitable business services companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Analyzing the trend in its profitability, EchoStar’s operating margin decreased significantly over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. EchoStar’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q4, EchoStar generated a negative 20.5% operating margin.

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

EchoStar’s earnings losses deepened over the last five years as its EPS dropped 162% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, EchoStar’s low margin of safety could leave its stock price susceptible to large downswings.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For EchoStar, its two-year annual EPS declines of 183% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, EchoStar reported EPS of negative $4.19, down from $1.19 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast EchoStar’s full-year EPS of negative $50.33 will flip to positive $7.20.

8. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

EchoStar has shown weak cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 2.7%, subpar for a business services business.

Taking a step back, we can see that EchoStar’s margin dropped by 79.6 percentage points during that time. Almost any movement in the wrong direction is undesirable because of its already low cash conversion. If the trend continues, it could signal it’s in the middle of a big investment cycle.

EchoStar burned through $583.4 million of cash in Q4, equivalent to a negative 15.4% margin. The company’s cash burn increased from $298.7 million of lost cash in the same quarter last year. These numbers deviate from its longer-term margin, indicating it is a seasonal business that must build up inventory during certain quarters.

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

EchoStar historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 2.5%, lower than the typical cost of capital (how much it costs to raise money) for business services companies.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, EchoStar’s ROIC has unfortunately decreased. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

10. Balance Sheet Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

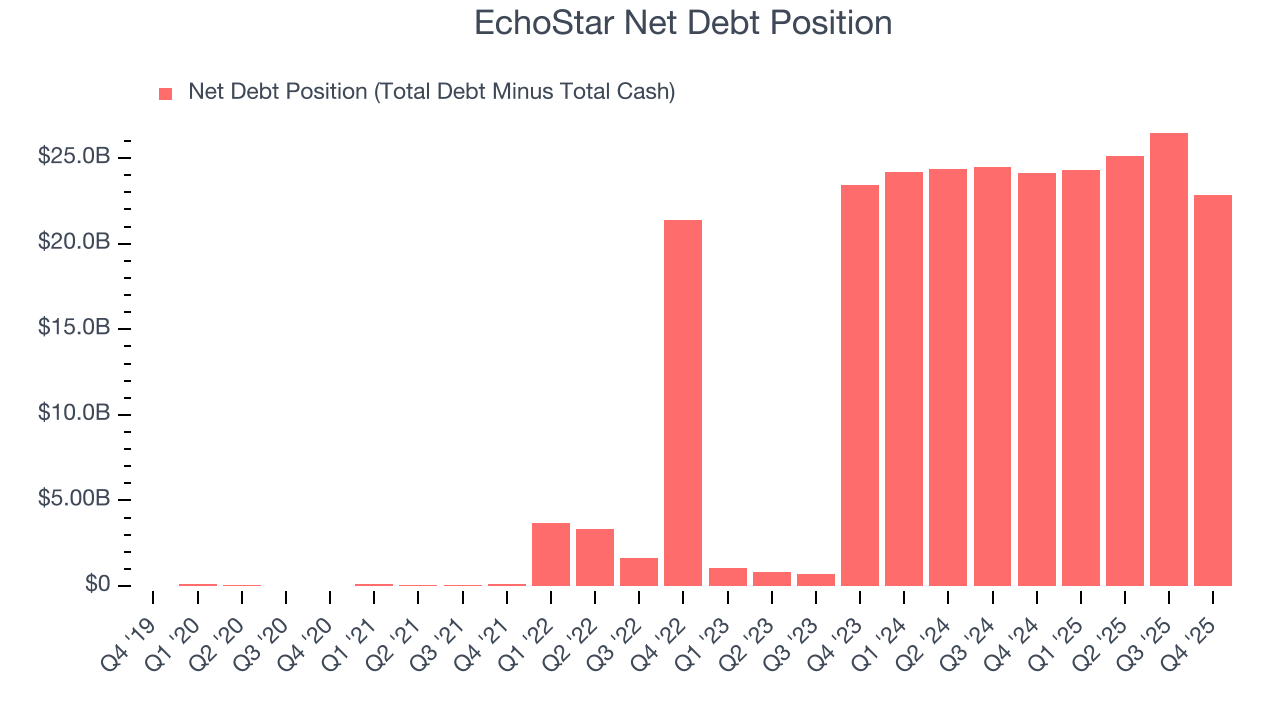

EchoStar posted negative $14.99 billion of EBITDA over the last 12 months, and its $25.98 billion of debt exceeds the $3.16 billion of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

We implore our readers to tread carefully because credit agencies could downgrade EchoStar if its unprofitable ways continue, making incremental borrowing more expensive and restricting growth prospects. The company could also be backed into a corner if the market turns unexpectedly. We hope EchoStar can improve its profitability and remain cautious until then.

11. Key Takeaways from EchoStar’s Q4 Results

It was good to see EchoStar narrowly top analysts’ revenue expectations this quarter. Other than that, results lacked comparability to Consensus due to non-recurring items. The stock traded down 1.2% to $112.84 immediately after reporting.

12. Is Now The Time To Buy EchoStar?

Updated: March 13, 2026 at 12:27 AM EDT

Before investing in or passing on EchoStar, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

EchoStar isn’t a terrible business, but it doesn’t pass our quality test. Although its revenue growth was exceptional over the last five years, it’s expected to deteriorate over the next 12 months and its diminishing returns show management's prior bets haven't worked out. And while the company’s scale makes it a trusted partner with negotiating leverage, the downside is its relatively low ROIC suggests management has struggled to find compelling investment opportunities.

EchoStar’s EV-to-EBITDA ratio based on the next 12 months is 27.9x. This valuation tells us a lot of optimism is priced in - we think there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $129.17 on the company (compared to the current share price of $107.60).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.