Stride (LRN)

We’re bullish on Stride. Its blend of high growth and robust profitability makes for an attractive return algorithm.― StockStory Analyst Team

1. News

2. Summary

Why We Like Stride

Formerly known as K12, Stride (NYSE:LRN) is an education technology company providing education solutions through digital platforms.

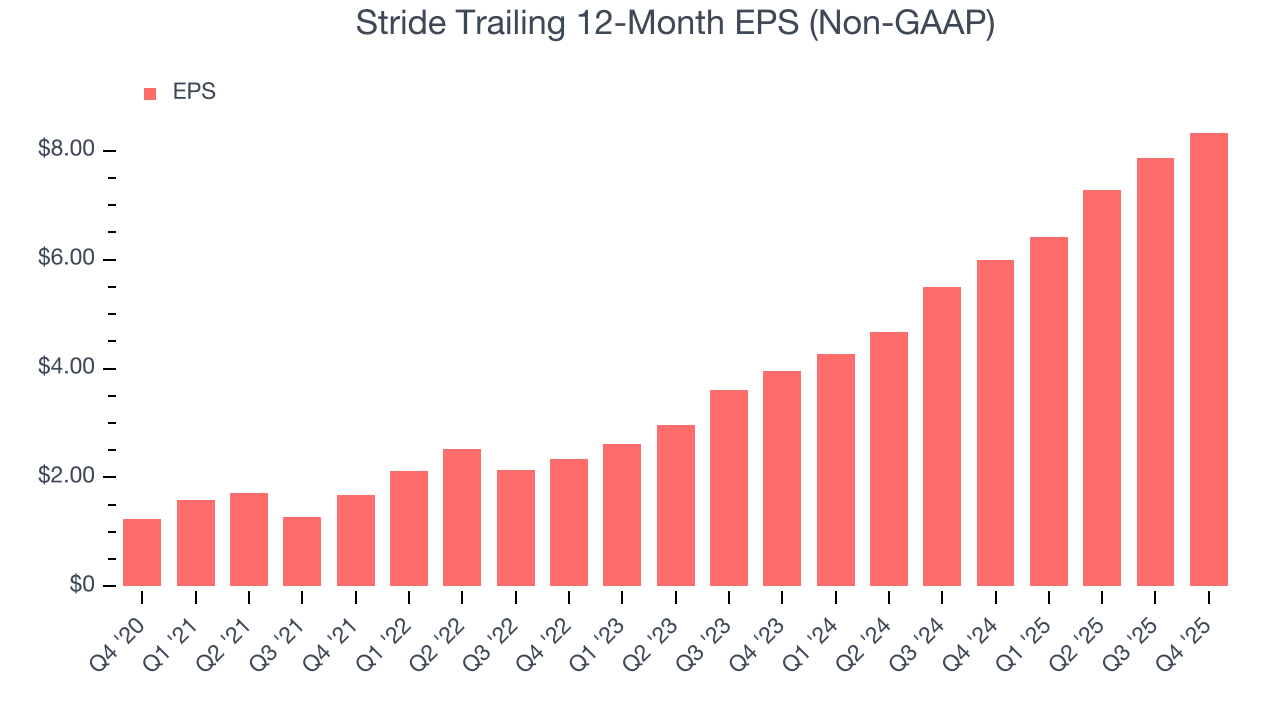

- Earnings per share grew by 46.4% annually over the last five years, massively outpacing its peers

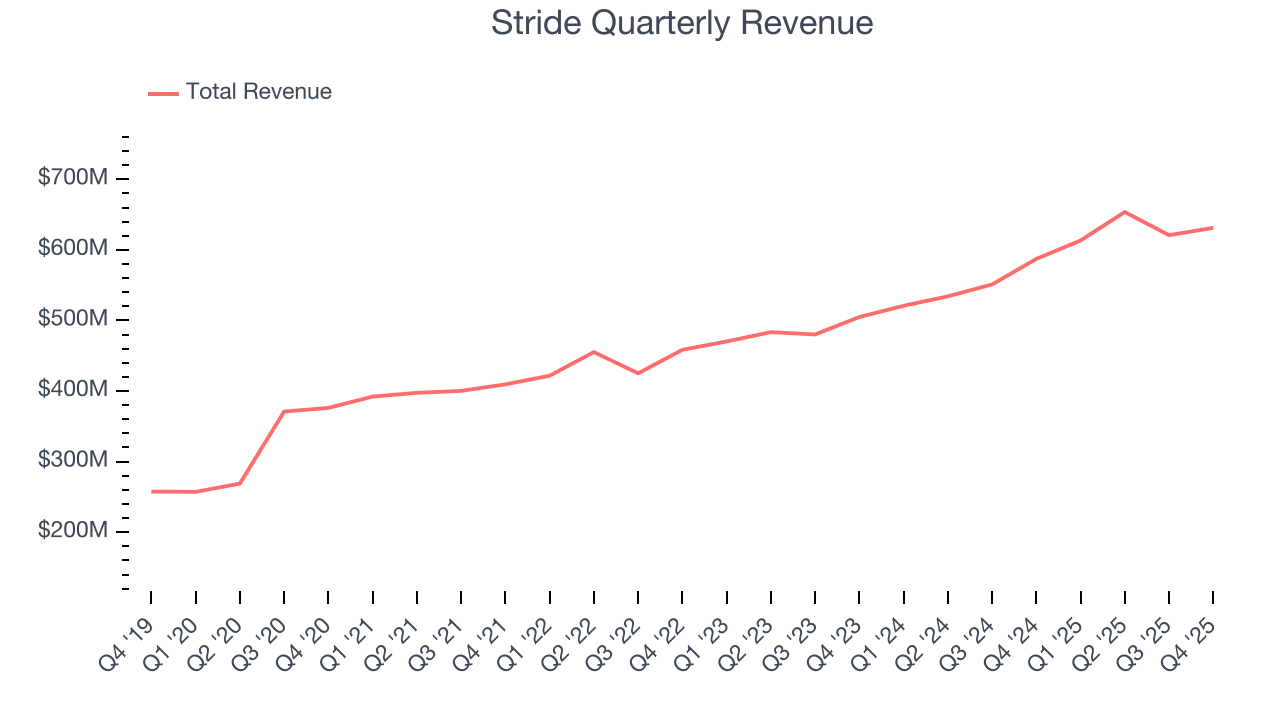

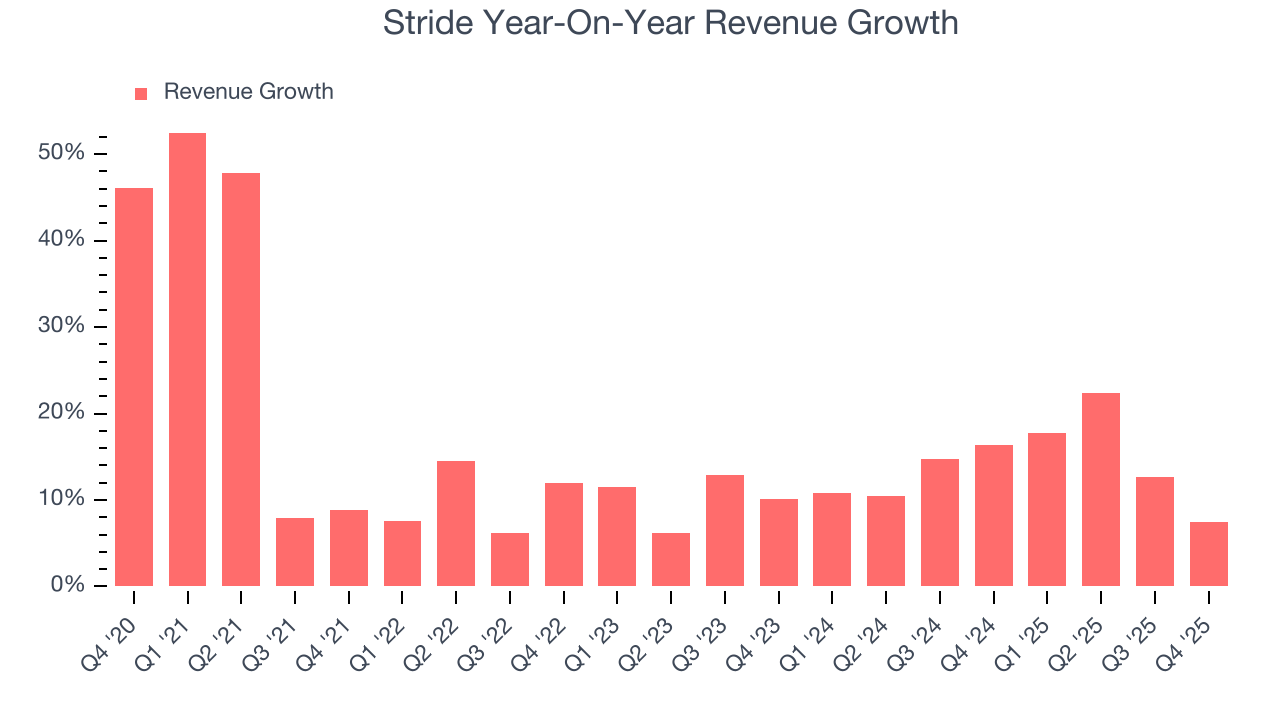

- Impressive 14.6% annual revenue growth over the last five years indicates it’s winning market share this cycle

- ROIC punches in at 17.4%, illustrating management’s expertise in identifying profitable investments, and its returns are growing as it capitalizes on even better market opportunities

We have an affinity for Stride. The price seems fair relative to its quality, and we think now is the time to buy.

Why Is Now The Time To Buy Stride?

At $83.61 per share, Stride trades at 9.9x forward P/E. The stock’s multiple sure seems like a bargain relative to its business quality and fundamentals.

Our eyes light up when companies with elite fundamentals go on sale because it enables investors to profit from earnings growth and a potential re-rating - the coveted “double play”.

3. Stride (LRN) Research Report: Q4 CY2025 Update

Online education Stride (NYSE:LRN) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 7.5% year on year to $631.3 million. Guidance for next quarter’s revenue was better than expected at $630 million at the midpoint, 1.9% above analysts’ estimates. Its non-GAAP profit of $2.50 per share was 7.8% above analysts’ consensus estimates.

Stride (LRN) Q4 CY2025 Highlights:

- Revenue: $631.3 million vs analyst estimates of $627.9 million (7.5% year-on-year growth, 0.5% beat)

- Adjusted EPS: $2.50 vs analyst estimates of $2.32 (7.8% beat)

- Adjusted EBITDA: $188.1 million vs analyst estimates of $166.9 million (29.8% margin, 12.7% beat)

- The company reconfirmed its revenue guidance for the full year of $2.52 billion at the midpoint

- Operating Margin: 23.3%, up from 21.3% in the same quarter last year

- Free Cash Flow Margin: 12%, down from 35.5% in the same quarter last year

- Market Capitalization: $3.10 billion

Company Overview

Formerly known as K12, Stride (NYSE:LRN) is an education technology company providing education solutions through digital platforms.

Stride specializes in high-quality, personalized K-12 education, offering online public and private schooling, curriculum development, and career learning programs. Recognizing the unique needs, talents, and interests of each student, Stride tailors its educational approach to move beyond the limitations of traditional, one-size-fits-all education.

The company collaborates with school districts and charter schools to operate virtual public schools, providing a comprehensive K-12 curriculum, state-certified teachers, and a blend of online and offline coursework. This flexible learning model caters to a variety of students, including advanced learners and those with medical challenges, and is complemented by Stride's private online school options.

A key feature of Stride's offerings is its career learning programs, designed to connect education with the workforce by equipping students with practical skills in fields like IT, business, health science, and manufacturing. These programs align with evolving industry demands, preparing students for future career opportunities.

Stride's expertise also extends to curriculum development, where it creates and supplies innovative, interactive online courses that adhere to high academic standards and accommodate different learning styles. These courses are utilized in Stride's educational institutions and are also available to traditional schools and other online education platforms.

4. Digital Media & Content Platforms

AI-driven content creation, personalized media experiences, and digital advertising are evolving, which could benefit companies investing in these themes. For example, companies with a portfolio of licensed visual content or platforms facilitating direct monetization models could see increased demand for years. On the other hand, headwinds include growing regulatory scrutiny on AI-generated content, with many publishers balking at anything that gets no human oversight. Additional areas to navigate include the phasing out of third-party cookies, which could make traditional ways of tracking the online behavior of consumers (a secret sauce in digital marketing) much less effective.

Stride’s primary competitors include Pearson PLC (NYSE:PSO), Chegg (NYSE:CHGG), Grand Canyon Education (NASDAQ:LOPE), 2U (NASDAQ:TWOU), and private companies Connections Academy and Edmentum.

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $2.52 billion in revenue over the past 12 months, Stride is a mid-sized business services company, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale. On the bright side, it can still flex high growth rates because it’s working from a smaller revenue base.

As you can see below, Stride’s 14.6% annualized revenue growth over the last five years was exceptional. This is a great starting point for our analysis because it shows Stride’s demand was higher than many business services companies.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. Stride’s annualized revenue growth of 14% over the last two years aligns with its five-year trend, suggesting its demand was predictably strong.

This quarter, Stride reported year-on-year revenue growth of 7.5%, and its $631.3 million of revenue exceeded Wall Street’s estimates by 0.5%. Company management is currently guiding for a 2.7% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 2% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and implies its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

6. Operating Margin

Stride has managed its cost base well over the last five years. It demonstrated solid profitability for a business services business, producing an average operating margin of 12.1%.

Analyzing the trend in its profitability, Stride’s operating margin rose by 9.1 percentage points over the last five years, as its sales growth gave it immense operating leverage.

In Q4, Stride generated an operating margin profit margin of 23.3%, up 2 percentage points year on year. This increase was a welcome development and shows it was more efficient.

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Stride’s EPS grew at an astounding 46.4% compounded annual growth rate over the last five years, higher than its 14.6% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

We can take a deeper look into Stride’s earnings quality to better understand the drivers of its performance. As we mentioned earlier, Stride’s operating margin expanded by 9.1 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Stride, its two-year annual EPS growth of 45% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q4, Stride reported adjusted EPS of $2.50, up from $2.03 in the same quarter last year. This print beat analysts’ estimates by 7.8%. Over the next 12 months, Wall Street expects Stride’s full-year EPS of $8.33 to grow 2.7%.

8. Cash Is King

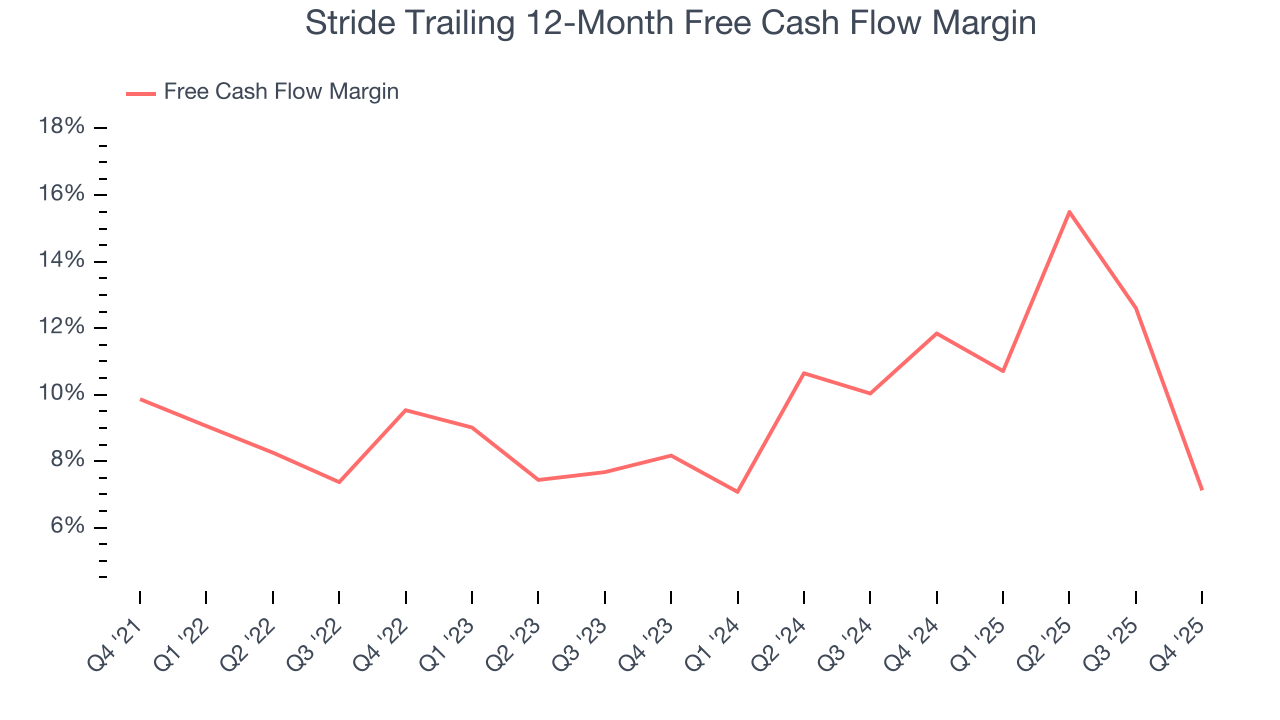

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Stride has shown robust cash profitability, giving it an edge over its competitors and the ability to reinvest or return capital to investors. The company’s free cash flow margin averaged 9.2% over the last five years, quite impressive for a business services business.

Taking a step back, we can see that Stride’s margin dropped by 2.7 percentage points during that time. If its declines continue, it could signal increasing investment needs and capital intensity.

Stride’s free cash flow clocked in at $75.92 million in Q4, equivalent to a 12% margin. The company’s cash profitability regressed as it was 23.5 percentage points lower than in the same quarter last year, but it’s still above its five-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, leading to short-term swings. Long-term trends carry greater meaning.

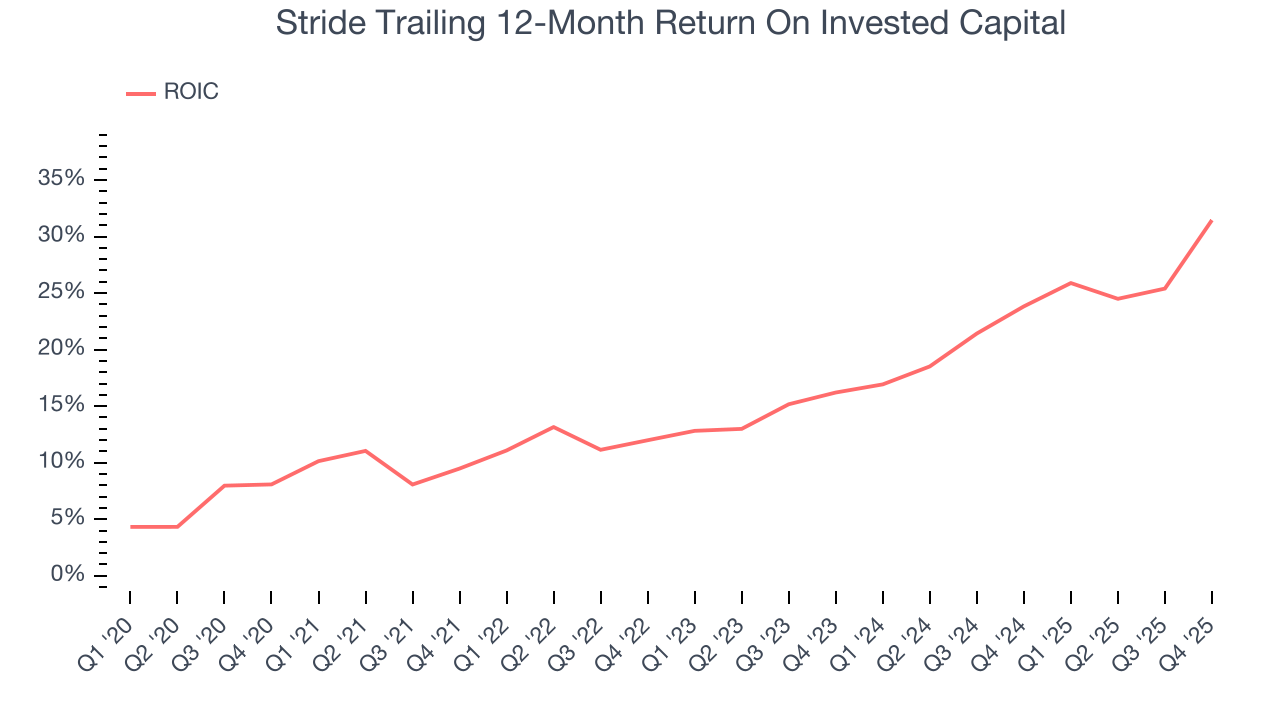

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Stride’s five-year average ROIC was 18.6%, beating other business services companies by a wide margin. This illustrates its management team’s ability to invest in attractive growth opportunities and produce tangible results for shareholders.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Stride’s ROIC has increased significantly. This is a great sign when paired with its already strong returns. It could suggest its competitive advantage or profitable growth opportunities are expanding.

10. Balance Sheet Assessment

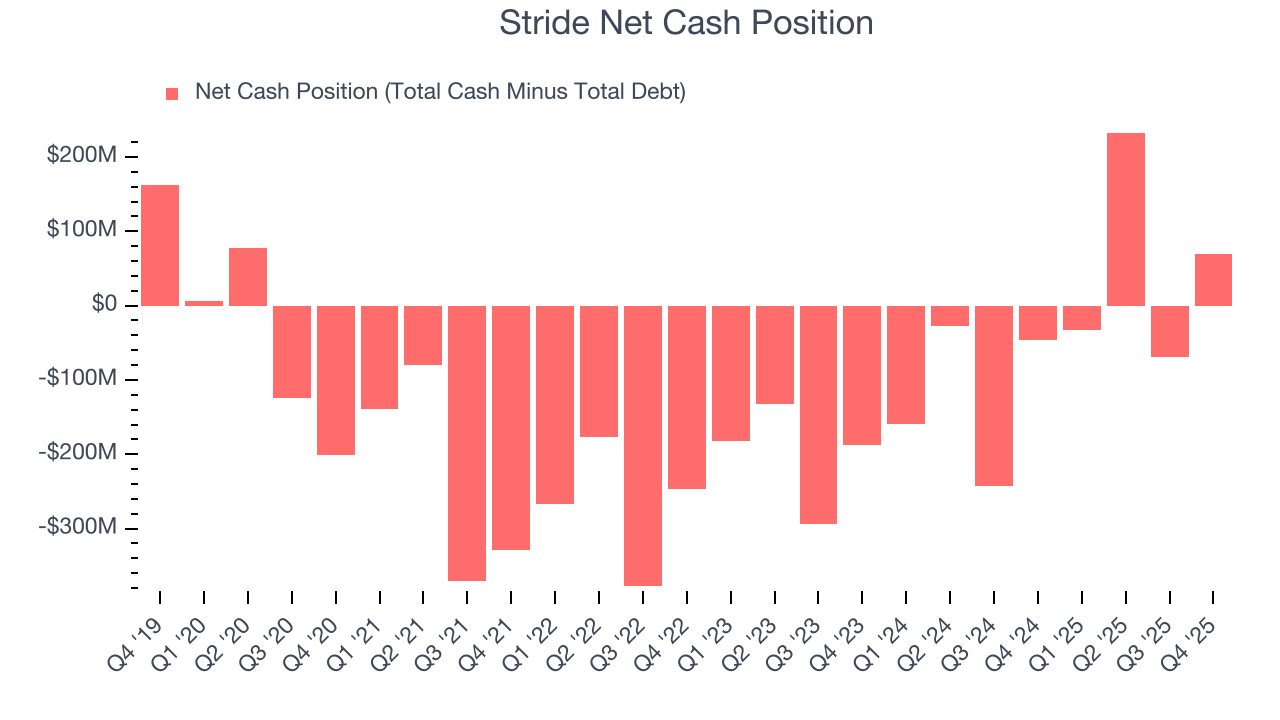

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

Stride is a profitable, well-capitalized company with $625.7 million of cash and $556.3 million of debt on its balance sheet. This $69.45 million net cash position is 2.2% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

11. Key Takeaways from Stride’s Q4 Results

It was great to see Stride’s revenue guidance for next quarter top analysts’ expectations. We were also glad its EPS outperformed Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 13.6% to $82.31 immediately after reporting.

12. Is Now The Time To Buy Stride?

Updated: March 16, 2026 at 11:13 PM EDT

Before deciding whether to buy Stride or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

Stride is truly a cream-of-the-crop business services company. For starters, its revenue growth was exceptional over the last five years. And while its projected EPS for the next year is lacking, its expanding adjusted operating margin shows the business has become more efficient. Additionally, Stride’s astounding EPS growth over the last five years shows its profits are trickling down to shareholders.

Stride’s P/E ratio based on the next 12 months is 9.9x. Looking at the business services space today, Stride’s qualities as one of the best businesses really stand out, and we’re pounding the table at this bargain price.

Wall Street analysts have a consensus one-year price target of $106.33 on the company (compared to the current share price of $83.61), implying they see 27.2% upside in buying Stride in the short term.