SEI Investments (SEIC)

We’d invest in SEI Investments. Its remarkable ROE underscores its knack for targeting and investing in highly profitable growth initiatives.― StockStory Analyst Team

1. News

2. Summary

Why We Like SEI Investments

Founded in 1968 as Simulated Environments Inc. to train bank loan officers using computer simulations, SEI Investments (NASDAQ:SEIC) provides technology platforms, investment management, and operational solutions for financial institutions, wealth managers, and investors.

- Additional sales over the last two years increased its profitability as the 26.5% annual growth in its earnings per share outpaced its revenue

- Stellar return on equity showcases management’s ability to surface highly profitable business ventures

- Products and services resonate with customers, evidenced by its respectable 9.4% annualized sales growth over the last two years

SEI Investments is a market leader. The price looks fair relative to its quality, so this might be an opportune time to invest in some shares.

Why Is Now The Time To Buy SEI Investments?

SEI Investments is trading at $81.33 per share, or 14.2x forward P/E. Scanning the financials landscape, we think this multiple is reasonable - arguably even attractive - for the quality you get.

Our analysis and backtests consistently tell us that buying high-quality companies and holding them for many years leads to market outperformance. Entry price matters less, but if you can get a good one, all the better.

3. SEI Investments (SEIC) Research Report: Q4 CY2025 Update

Financial technology provider SEI Investments (NASDAQ:SEIC) announced better-than-expected revenue in Q4 CY2025, with sales up 9.1% year on year to $607.9 million. Its GAAP profit of $1.38 per share was 2.1% above analysts’ consensus estimates.

SEI Investments (SEIC) Q4 CY2025 Highlights:

- Assets Under Management: $215.9 billion vs analyst estimates of $546.6 billion (13.7% year-on-year growth, 60.5% miss)

- Revenue: $607.9 million vs analyst estimates of $599.4 million (9.1% year-on-year growth, 1.4% beat)

- Pre-tax Profit: $217.1 million (35.7% margin)

- EPS (GAAP): $1.38 vs analyst estimates of $1.35 (2.1% beat)

- Market Capitalization: $10.43 billion

Company Overview

Founded in 1968 as Simulated Environments Inc. to train bank loan officers using computer simulations, SEI Investments (NASDAQ:SEIC) provides technology platforms, investment management, and operational solutions for financial institutions, wealth managers, and investors.

SEI's business is organized into five segments, each serving different client types with tailored solutions. The Private Banks segment offers wealth management platforms that help banks and trust companies manage assets for high-net-worth clients. The Investment Advisors segment provides investment management and back-office administrative services to independent financial advisors. The Institutional Investors segment delivers outsourced investment management solutions to pension plans, endowments, and foundations. The Investment Managers segment offers fund administration, accounting, and operational support to investment managers. Finally, the Investments in New Businesses segment focuses on developing innovative solutions for private wealth management.

At the core of SEI's offerings is its technology infrastructure, which includes the SEI Wealth Platform. This platform integrates various financial services functions—from client relationship management to portfolio management to reporting—into a unified system. For example, a wealth manager might use SEI's platform to onboard new clients, construct personalized investment portfolios, execute trades, and generate comprehensive performance reports, all within a single ecosystem.

SEI generates revenue through a combination of asset-based fees, transaction-based fees, and subscription fees. Asset-based fees are calculated as a percentage of assets under management or administration, transaction fees are charged for processing activities like trades, and subscription fees are collected for access to technology platforms. The company serves clients globally, with operations across North America, Europe, and Asia, allowing financial institutions of various sizes to benefit from enterprise-grade technology without building proprietary systems.

4. Custody Bank

Custody banks safeguard financial assets and provide services like settlement, accounting, and regulatory compliance for institutional investors. Growth opportunities stem from increasing global assets under custody, demand for data analytics, and blockchain technology adoption for settlement efficiency. Challenges include fee pressure from large clients, substantial technology investment requirements, and competition from both traditional players and fintech firms entering the space.

SEI Investments competes with financial technology and investment management firms including Broadridge Financial Solutions (NYSE:BR), SS&C Technologies (NASDAQ:SSNC), BlackRock (NYSE:BLK), and Fidelity National Information Services (NYSE:FIS).

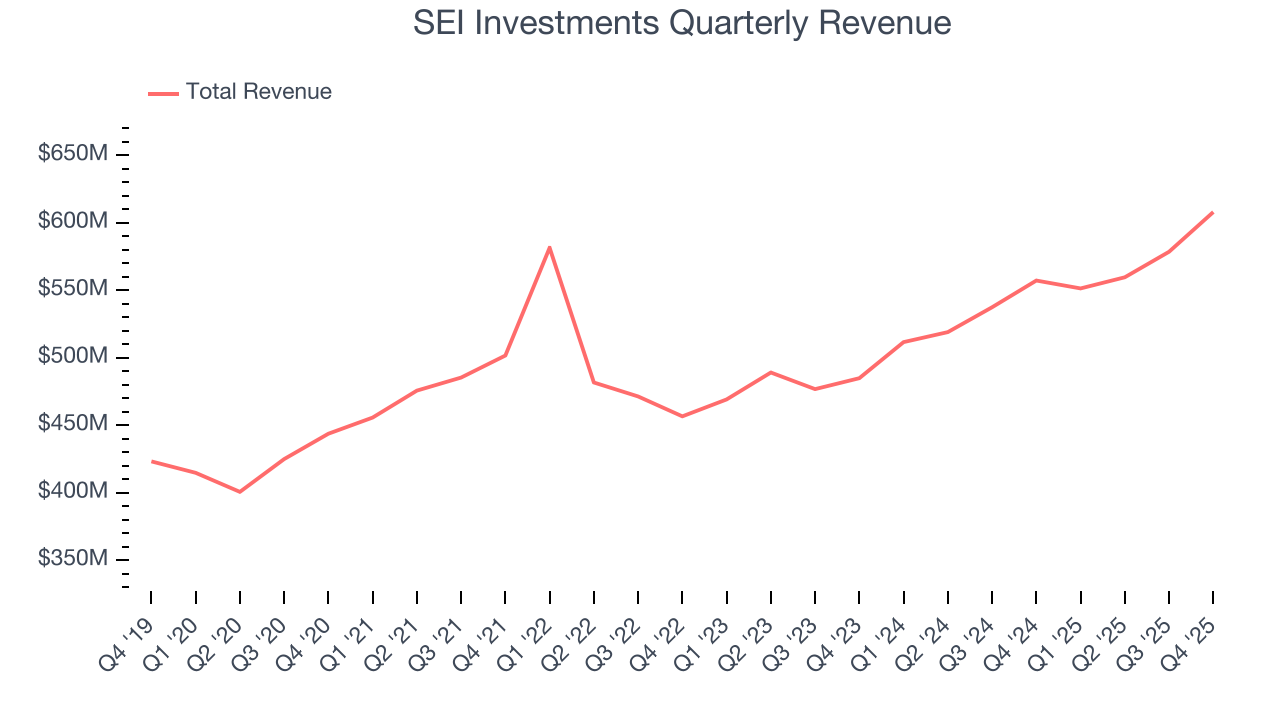

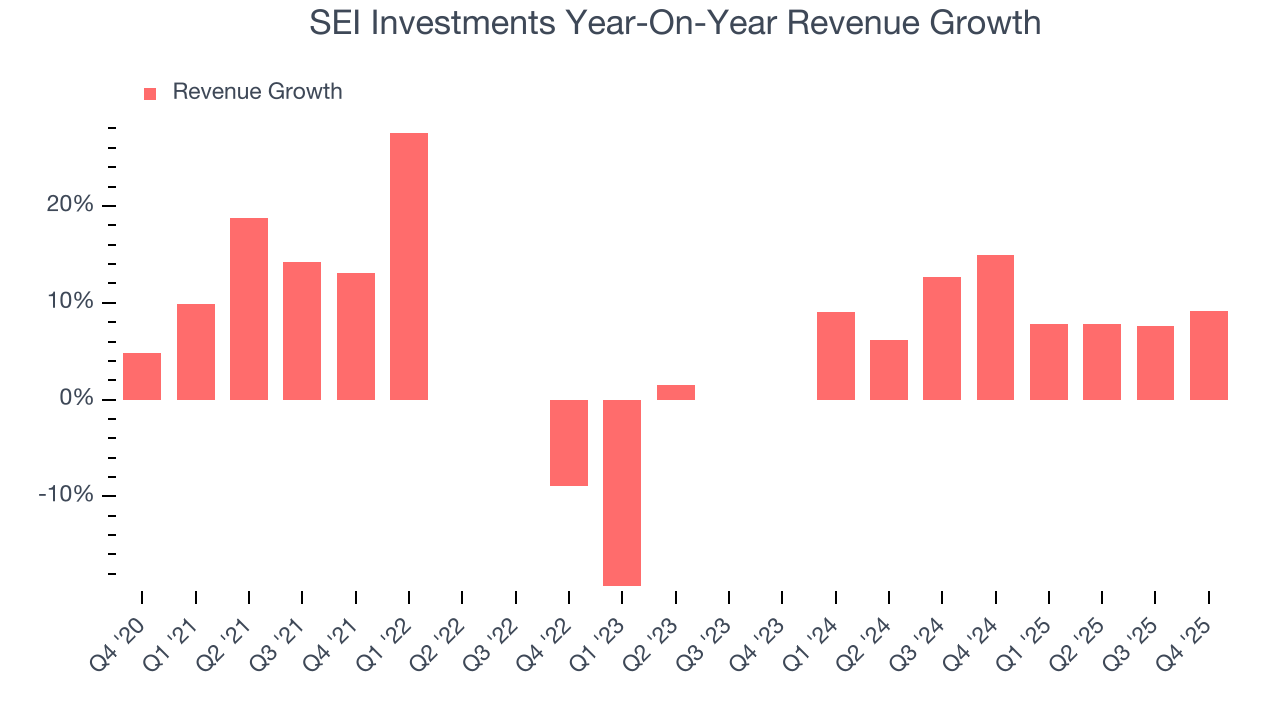

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Regrettably, SEI Investments’s revenue grew at a mediocre 6.4% compounded annual growth rate over the last five years. This wasn’t a great result compared to the rest of the financials sector, but there are still things to like about SEI Investments.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. SEI Investments’s annualized revenue growth of 9.4% over the last two years is above its five-year trend, suggesting some bright spots.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, SEI Investments reported year-on-year revenue growth of 9.1%, and its $607.9 million of revenue exceeded Wall Street’s estimates by 1.4%.

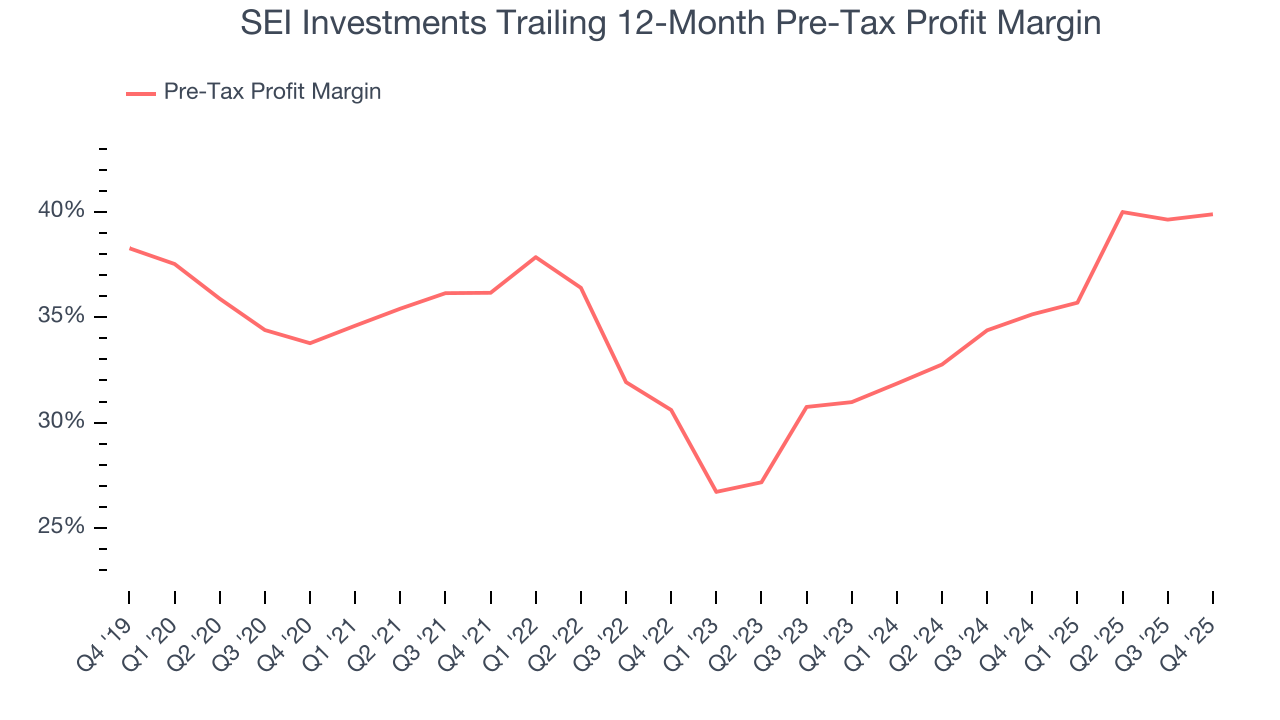

6. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For Custody Bank companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

The pre-tax profit margin includes interest because it's central to how financial institutions generate revenue and manage costs. Tax considerations are excluded since they represent government policy rather than operational performance, giving investors a clearer view of business fundamentals.

Over the last five years, SEI Investments’s pre-tax profit margin has fallen by 6.1 percentage points, going from 36.2% to 39.9%. It has also expanded by 8.9 percentage points on a two-year basis, showing its expenses have consistently grown at a slower rate than revenue. This typically signals prudent management.

SEI Investments’s pre-tax profit margin came in at 35.7% this quarter. This result was 1.4 percentage points better than the same quarter last year.

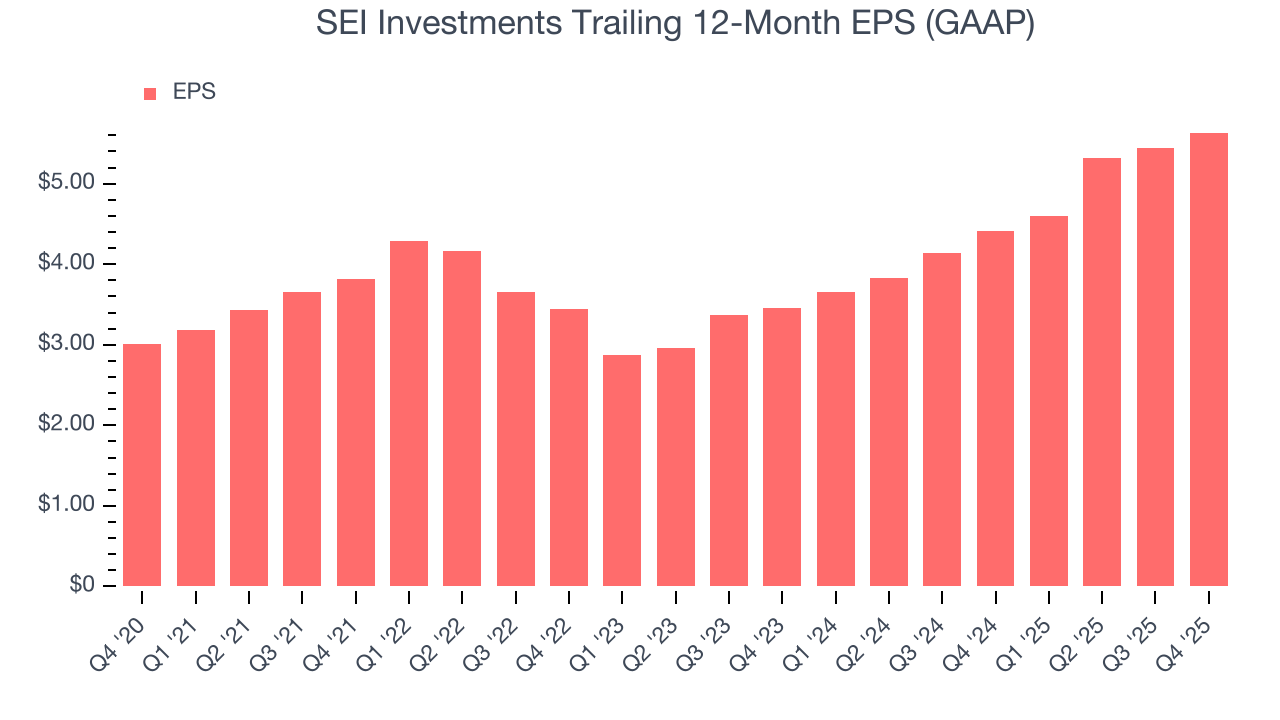

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

SEI Investments’s EPS grew at a solid 13.4% compounded annual growth rate over the last five years, higher than its 6.4% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For SEI Investments, its two-year annual EPS growth of 27.6% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q4, SEI Investments reported EPS of $1.38, up from $1.19 in the same quarter last year. This print beat analysts’ estimates by 2.1%. Over the next 12 months, Wall Street expects SEI Investments’s full-year EPS of $5.63 to stay about the same.

8. Return on Equity

Return on equity (ROE) reveals the profit generated per dollar of shareholder equity, which represents a key source of bank funding. Banks maintaining elevated ROE levels tend to accelerate wealth creation for shareholders via earnings retention, buybacks, and distributions.

Over the last five years, SEI Investments has averaged an ROE of 26.6%, exceptional for a company operating in a sector where the average shakes out around 10% and those putting up 25%+ are greatly admired. This shows SEI Investments has a strong competitive moat.

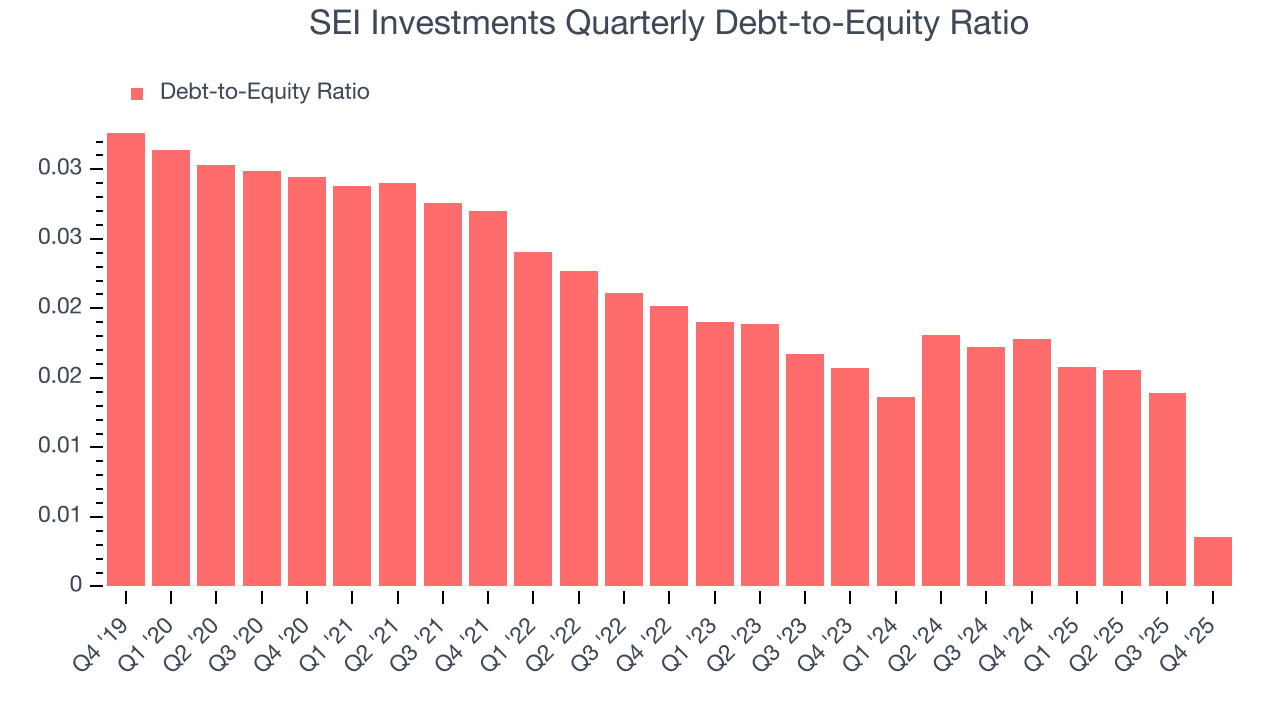

9. Balance Sheet Assessment

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

SEI Investments currently has $8.68 million of debt and $2.46 billion of shareholder's equity on its balance sheet, and over the past four quarters, has averaged a debt-to-equity ratio of 0×. We think this is safe and raises no red flags. In general, we’re comfortable with any ratio below 3.5× for a financials business.

10. Key Takeaways from SEI Investments’s Q4 Results

It was good to see SEI Investments narrowly top analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its AUM missed. Overall, this print had some key positives. The stock remained flat at $85.97 immediately following the results.

11. Is Now The Time To Buy SEI Investments?

Updated: February 21, 2026 at 12:14 AM EST

Before making an investment decision, investors should account for SEI Investments’s business fundamentals and valuation in addition to what happened in the latest quarter.

There are multiple reasons why we think SEI Investments is an amazing business. Although its revenue growth was mediocre over the last five years, its growth over the next 12 months is expected to be higher. Plus, its stellar ROE suggests it has been a well-run company historically, and its expanding pre-tax profit margin shows the business has become more efficient.

SEI Investments’s P/E ratio based on the next 12 months is 14.2x. Scanning the financials space today, SEI Investments’s fundamentals really stand out, and we like it at this price.

Wall Street analysts have a consensus one-year price target of $103.14 on the company (compared to the current share price of $81.33), implying they see 26.8% upside in buying SEI Investments in the short term.