Latham (SWIM)

Latham is up against the odds. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Latham Will Underperform

Started as a family business, Latham (NASDAQ:SWIM) is a global designer and manufacturer of in-ground residential swimming pools and related products.

- Lackluster 6.2% annual revenue growth over the last five years indicates the company is losing ground to competitors

- Responsiveness to unforeseen market trends is restricted due to its substandard operating margin profitability

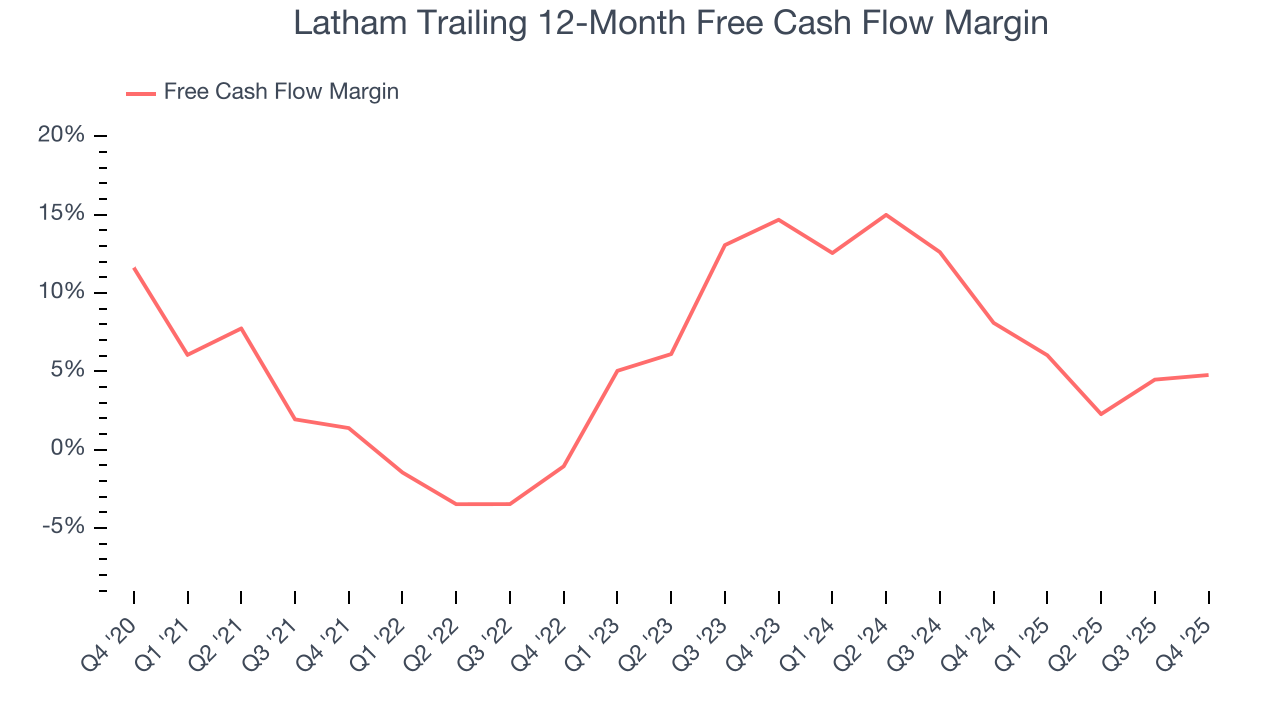

- Ability to fund investments or reward shareholders with increased buybacks or dividends is restricted by its weak free cash flow margin of 6.4% for the last two years

Latham’s quality is not up to our standards. More profitable opportunities exist elsewhere.

Why There Are Better Opportunities Than Latham

Latham is trading at $5.30 per share, or 29.4x forward P/E. Not only is Latham’s multiple richer than most consumer discretionary peers, but it’s also expensive for its revenue characteristics.

There are stocks out there similarly priced with better business quality. We prefer owning these.

3. Latham (SWIM) Research Report: Q4 CY2025 Update

Residential swimming pool manufacturer Latham (NASDAQ:SWIM) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 14.5% year on year to $99.95 million. The company’s full-year revenue guidance of $595 million at the midpoint came in 4.2% above analysts’ estimates. Its GAAP loss of $0.06 per share was 45.2% above analysts’ consensus estimates.

Latham (SWIM) Q4 CY2025 Highlights:

- Revenue: $99.95 million vs analyst estimates of $95.74 million (14.5% year-on-year growth, 4.4% beat)

- EPS (GAAP): -$0.06 vs analyst estimates of -$0.11 (45.2% beat)

- Adjusted EBITDA: $10.49 million vs analyst estimates of $6.41 million (10.5% margin, 63.5% beat)

- EBITDA guidance for the upcoming financial year 2026 is $112.5 million at the midpoint, above analyst estimates of $107.7 million

- Operating Margin: -10.7%, up from -14.9% in the same quarter last year

- Free Cash Flow was $2.08 million, up from -$98,000 in the same quarter last year

- Market Capitalization: $769.9 million

Company Overview

Started as a family business, Latham (NASDAQ:SWIM) is a global designer and manufacturer of in-ground residential swimming pools and related products.

Latham was created to provide high-quality, long-lasting swimming pools and has since evolved into a globally recognized company in the residential swimming pool sector. Over time, the business expanded its reach and product line, adapting to changing consumer needs and the evolving landscape of outdoor home improvement.

Latham's primary offerings encompass a range of in-ground residential swimming pools, including fiberglass and vinyl-liner models, along with various pool-related products like covers, liners, and safety fencing. The company addresses the need for durable, aesthetically pleasing, customizable pool solutions for residential settings.

Latham generates revenue through both direct sales and an extensive dealer network spanning multiple countries. This business model allows the company to maintain a balance between broad market reach and the provision of personalized, localized service. The company's products primarily appeal to homeowners seeking to improve their properties and builders and contractors looking for reliable and high-quality pool solutions.

4. Consumer Discretionary - Leisure Products

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare.

Leisure products companies manufacture recreational goods such as bicycles, marine vessels, fitness equipment, camping gear, and musical instruments. Tailwinds include heightened outdoor-activity participation, health-and-wellness awareness, and periodic innovation cycles that drive trade-up purchases. Headwinds are pronounced: demand is highly discretionary and sensitive to economic cycles—consumers readily defer big-ticket leisure purchases during downturns. Post-pandemic normalization has created excess channel inventory after demand surged then retreated. Raw-material and shipping cost inflation squeezes margins, while competition from low-cost imports and a fragmented market make pricing power elusive for most players.

Competitors in the outdoor recreation and water leisure industry include Brunswick (NYSE:BC), MasterCraft Boat (NASDAQ:MCFT), and Malibu Boats (NASDAQ:MBUU).

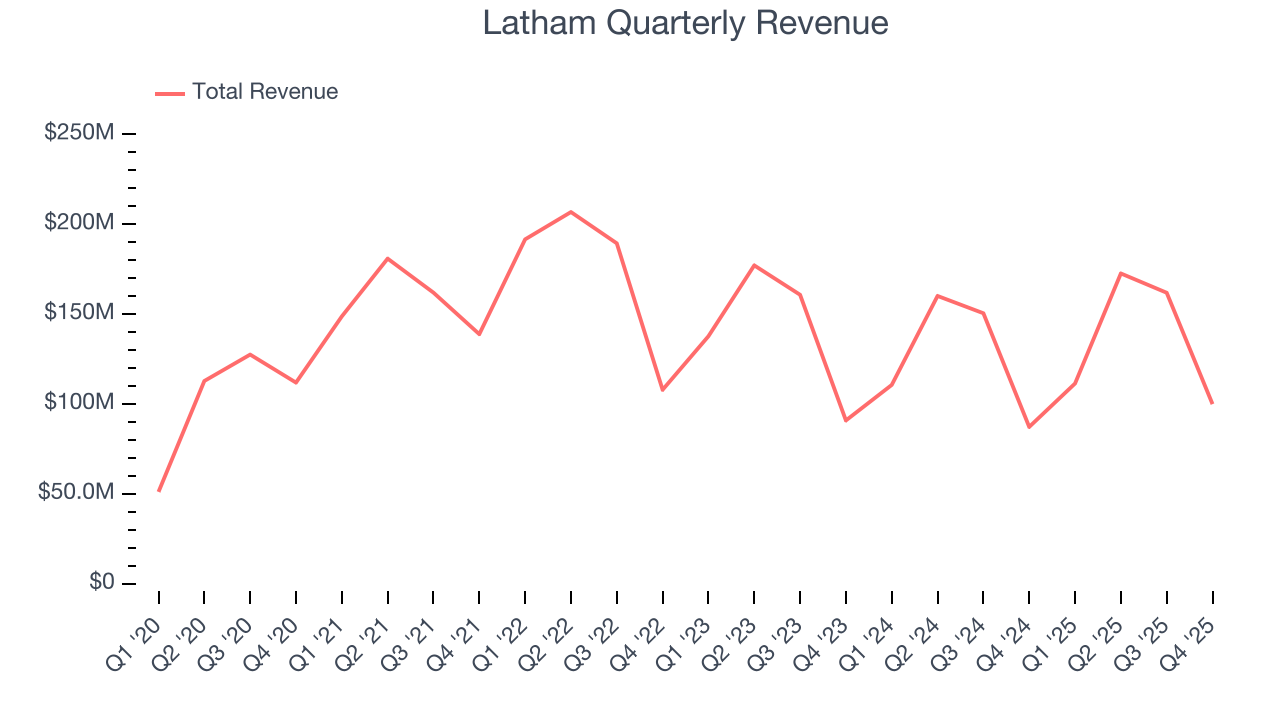

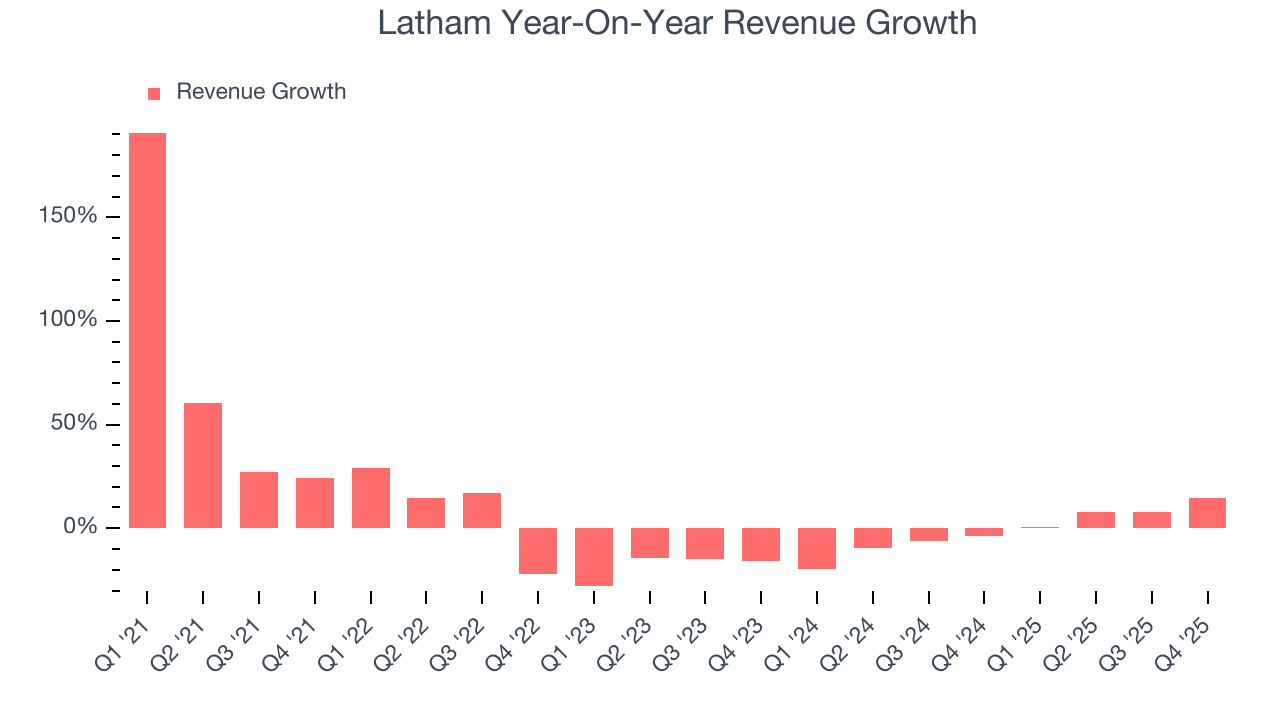

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Regrettably, Latham’s sales grew at a weak 6.2% compounded annual growth rate over the last five years. This was below our standard for the consumer discretionary sector and is a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Latham’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 1.8% annually.

This quarter, Latham reported year-on-year revenue growth of 14.5%, and its $99.95 million of revenue exceeded Wall Street’s estimates by 4.4%.

Looking ahead, sell-side analysts expect revenue to grow 4.8% over the next 12 months. While this projection implies its newer products and services will spur better top-line performance, it is still below the sector average.

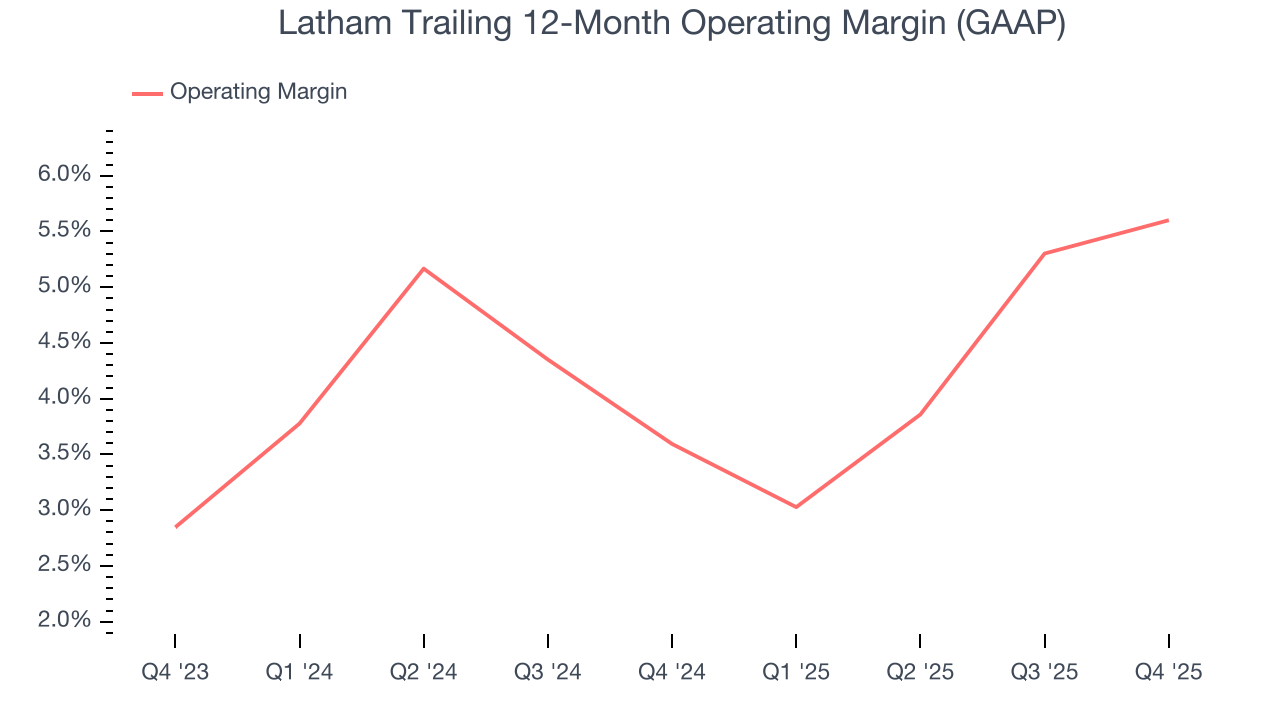

6. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Latham’s operating margin has been trending up over the last 12 months and averaged 4.6% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports inadequate profitability for a consumer discretionary business.

This quarter, Latham generated an operating margin profit margin of negative 10.7%, up 4.2 percentage points year on year. This increase was a welcome development and shows it was more efficient.

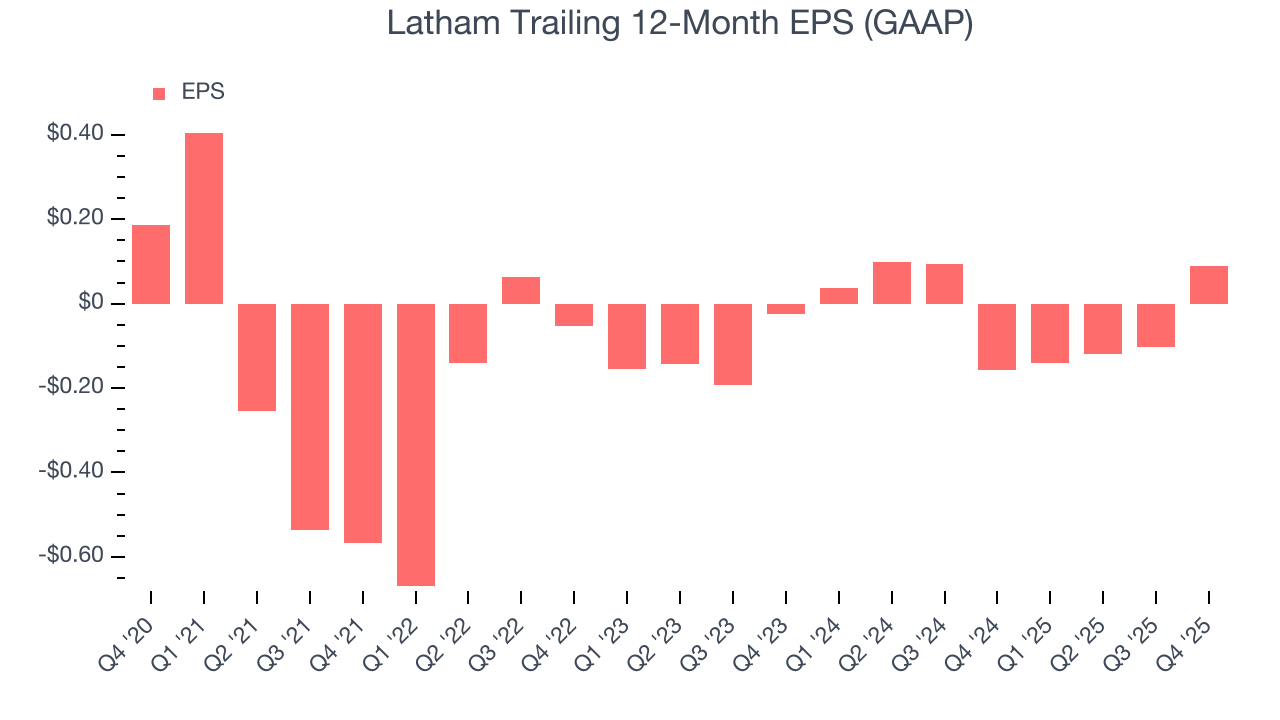

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Latham, its EPS declined by 13.6% annually over the last five years while its revenue grew by 6.2%. This tells us the company became less profitable on a per-share basis as it expanded.

In Q4, Latham reported EPS of negative $0.06, up from negative $0.25 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Latham’s full-year EPS of $0.09 to grow 26.5%.

8. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Latham has shown poor cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 6.4%, below what we’d expect for a consumer discretionary business.

Latham’s free cash flow clocked in at $2.08 million in Q4, equivalent to a 2.1% margin. This result was good as its margin was 2.2 percentage points higher than in the same quarter last year, but we wouldn’t put too much weight on the short term because investment needs can be seasonal, causing temporary swings. Long-term trends carry greater meaning.

Over the next year, analysts’ consensus estimates show they’re expecting Latham’s free cash flow margin of 4.8% for the last 12 months to remain the same.

9. Return on Invested Capital (ROIC)

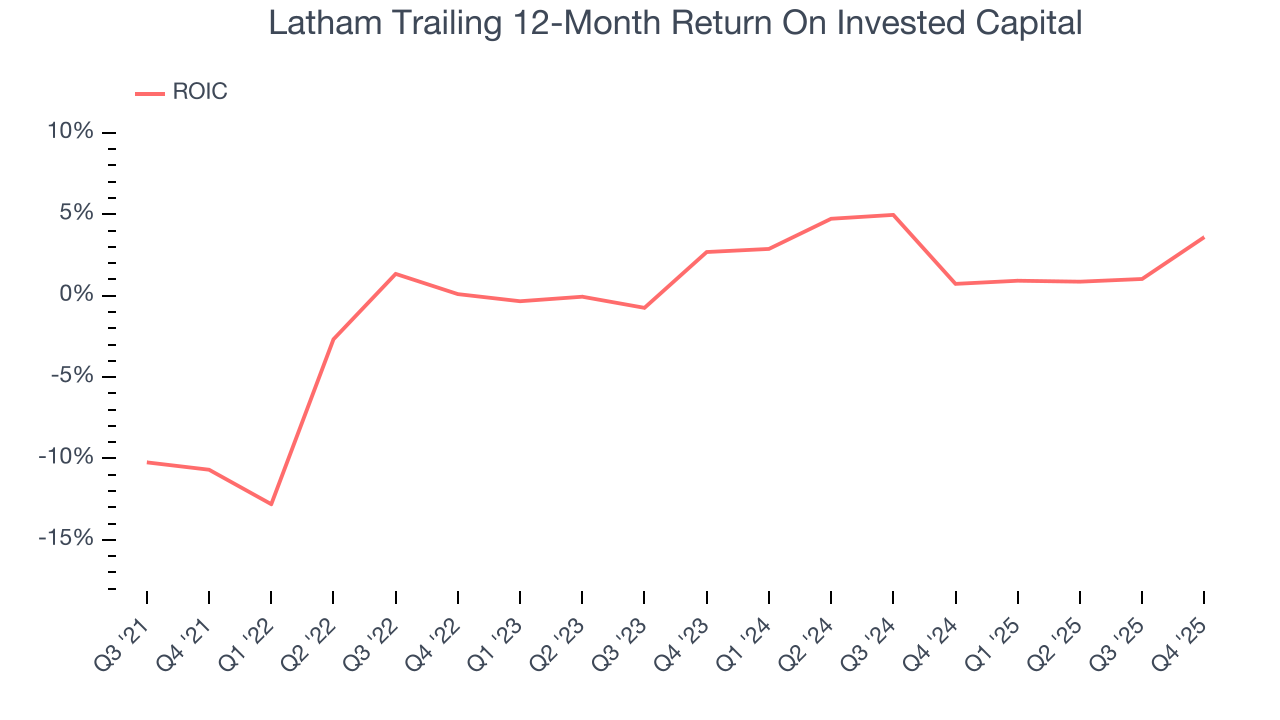

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Latham’s five-year average ROIC was negative 0.7%, meaning management lost money while trying to expand the business. Its returns were among the worst in the consumer discretionary sector.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Latham’s ROIC has increased. This is a good sign, but we recognize its lack of profitable growth during the COVID era was the primary reason for the change.

10. Balance Sheet Assessment

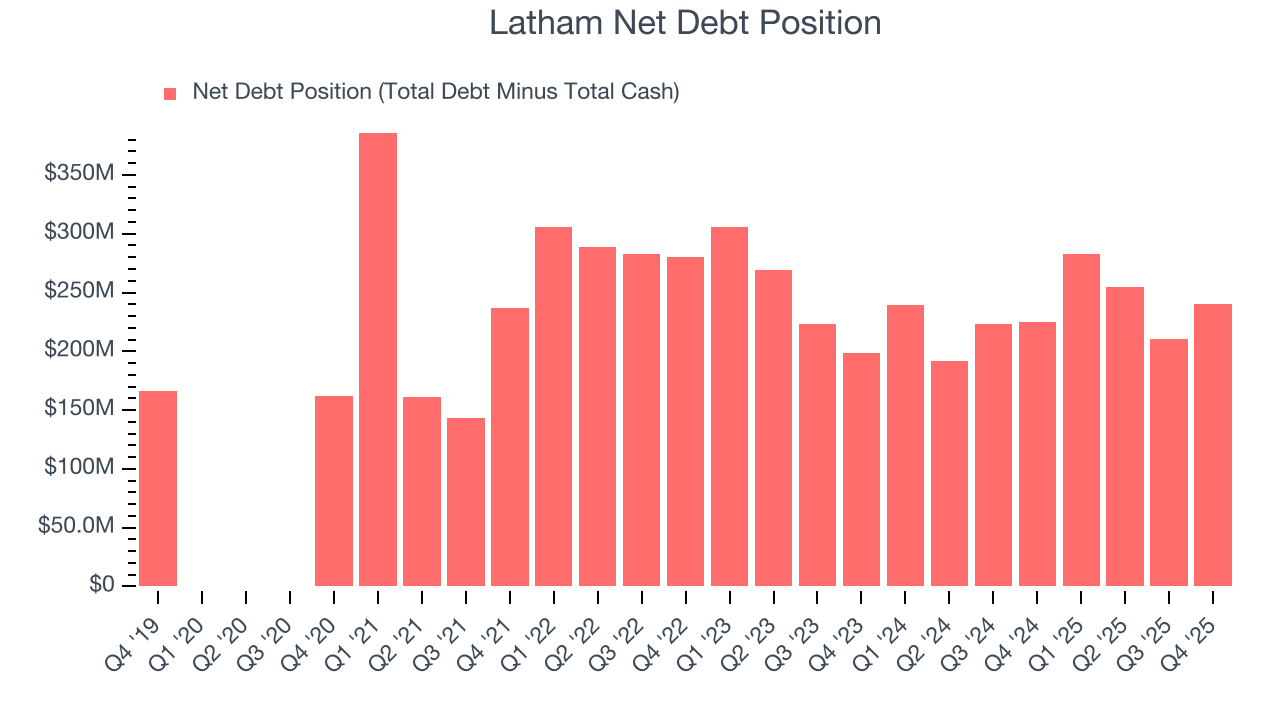

Latham reported $71.04 million of cash and $311.4 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $99.84 million of EBITDA over the last 12 months, we view Latham’s 2.4× net-debt-to-EBITDA ratio as safe. We also see its $13.37 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Latham’s Q4 Results

It was good to see Latham beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a solid print. The stock traded up 14.8% to $7.41 immediately following the results.

12. Is Now The Time To Buy Latham?

Updated: March 29, 2026 at 11:04 PM EDT

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

We see the value of companies helping consumers, but in the case of Latham, we’re out. While its projected EPS for the next year implies the company’s fundamentals will improve, the downside is its Forecasted free cash flow margin for next year suggests the company will fail to improve its cash conversion. On top of that, its relatively low ROIC suggests management has struggled to find compelling investment opportunities.

Latham’s P/E ratio based on the next 12 months is 29.4x. While this valuation is reasonable, we don’t see a big opportunity at the moment. There are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $8.82 on the company (compared to the current share price of $5.30).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.