Skyworks Solutions (SWKS)

Skyworks Solutions is up against the odds. Its weak gross margin and failure to generate revenue growth show it lacks demand and decent unit economics.― StockStory Analyst Team

1. News

2. Summary

Why We Think Skyworks Solutions Will Underperform

Result of a merger of Alpha Industries and the wireless communications division of Conexant, Skyworks Solutions (NASDAQ: SWKS) is a designer and manufacturer of chips used in smartphones, autos, and industrial applications to amplify, filter, and process wireless signals.

- Sales are expected to decline once again over the next 12 months as it continues working through a challenging demand environment

- Falling earnings per share over the last five years has some investors worried as stock prices ultimately follow EPS over the long term

- Annual sales declines of 6.6% for the past two years show its products and services struggled to connect with the market during this cycle

Skyworks Solutions’s quality doesn’t meet our bar. We’re on the lookout for more interesting opportunities.

Why There Are Better Opportunities Than Skyworks Solutions

At $57.43 per share, Skyworks Solutions trades at 12.5x forward P/E. Yes, this valuation multiple is lower than that of other semiconductor peers, but we’ll remind you that you often get what you pay for.

We’d rather pay up for companies with elite fundamentals than get a bargain on weak ones. Cheap stocks can be value traps, and as their performance deteriorates, they will stay cheap or get even cheaper.

3. Skyworks Solutions (SWKS) Research Report: Q4 CY2025 Update

Wireless chips maker Skyworks Solutions (NASDAQ: SWKS) reported Q4 CY2025 results topping the market’s revenue expectations, but sales fell by 3.1% year on year to $1.04 billion. On top of that, next quarter’s revenue guidance ($900 billion at the midpoint) was surprisingly good and 103,166% above what analysts were expecting. Its non-GAAP profit of $1.54 per share was 10.1% above analysts’ consensus estimates.

Skyworks Solutions (SWKS) Q4 CY2025 Highlights:

- Revenue: $1.04 billion vs analyst estimates of $1.00 billion (3.1% year-on-year decline, 3.4% beat)

- Adjusted EPS: $1.54 vs analyst estimates of $1.40 (10.1% beat)

- Adjusted Operating Income: $252.1 million vs analyst estimates of $228 million (24.3% margin, 10.6% beat)

- Revenue Guidance for Q1 CY2026 is $900 billion at the midpoint, above analyst estimates of $871.5 million

- Adjusted EPS guidance for Q1 CY2026 is $1.04 at the midpoint, above analyst estimates of $0.96

- Operating Margin: 10%, down from 16.9% in the same quarter last year

- Free Cash Flow Margin: 32.7%, up from 31.7% in the same quarter last year

- Inventory Days Outstanding: 115, up from 105 in the previous quarter

- Market Capitalization: $8.45 billion

Company Overview

Result of a merger of Alpha Industries and the wireless communications division of Conexant, Skyworks Solutions (NASDAQ: SWKS) is a designer and manufacturer of chips used in smartphones, autos, and industrial applications to amplify, filter, and process wireless signals.

Skyworks is an analog chip maker whose chips are used in radio frequency (RF) functions, essentially the chips that decode wireless signals. The most obvious use case is in mobile phones, and this is its biggest business, supplying Apple with RF chips for its iPhones accounts for a significant part of Skyworks revenues.

But Skyworks chips are also used for any connected device that processes wireless signals – such as the array of sensors that make up the Internet of Things and growing uses in factories and autos.

In 2021, Skyworks acquired Silicon Lab’s infrastructure and automotive business, to increase its exposure to autos and industrials. As the world’s wireless networks evolve from 3G to 4G to 5G, a wider variety of wireless spectrum and frequency bands come into play, which translates into a rising amount of RF content in smartphones, cars, and any connected device, a long term secular tailwind RF producers stand to benefit from.

Skyworks’s peers and competitors include Broadcom (NASDAQ:AVGO), Cirrus Logic (NASDAQ:CRUS), MACOM Technology (NASDAQ:MTSI), Qorvo (NASDAQ:QRVO), Qualcomm (NASDAQ:QCOM), and Texas Instruments (NASDAQ:TXN).

4. Analog Semiconductors

Longer manufacturing duration allows analog chip makers to generate greater efficiencies, leading to structurally higher gross margins than their fabless digital peers. The downside of vertical integration is that cyclicality can be more pronounced for analog chipmakers, as capacity utilization upsides work in reverse during down periods.

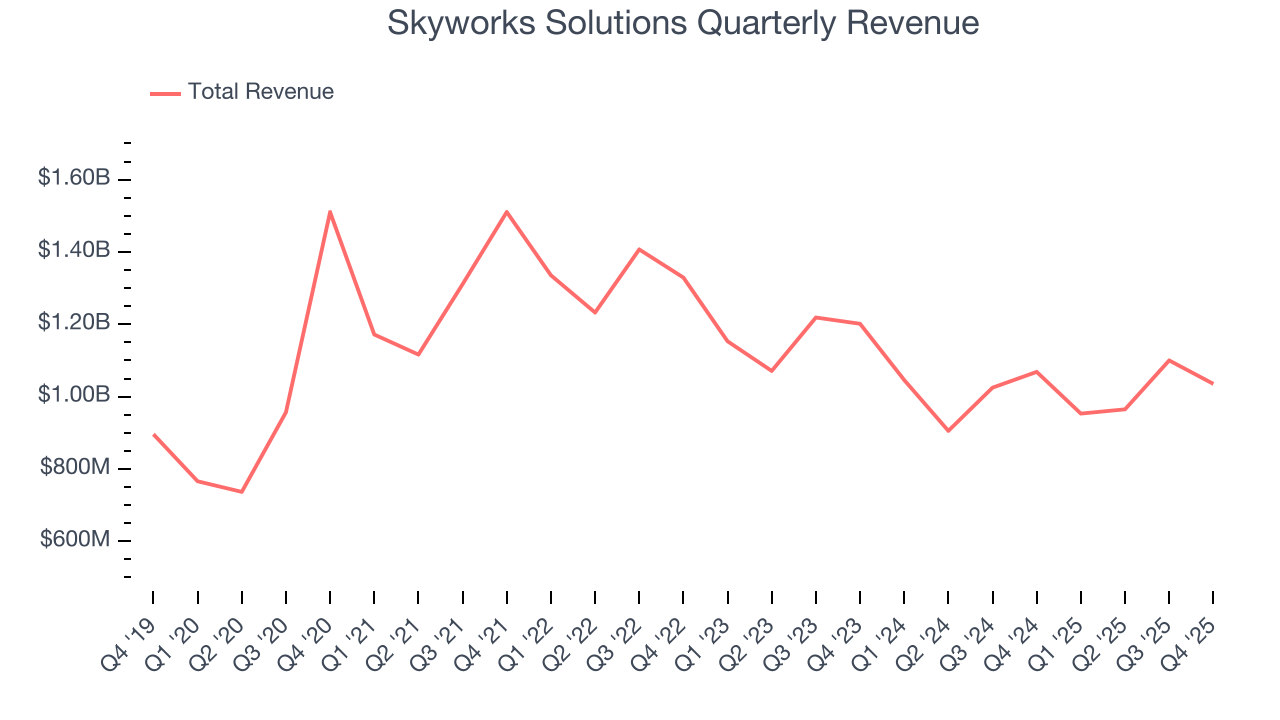

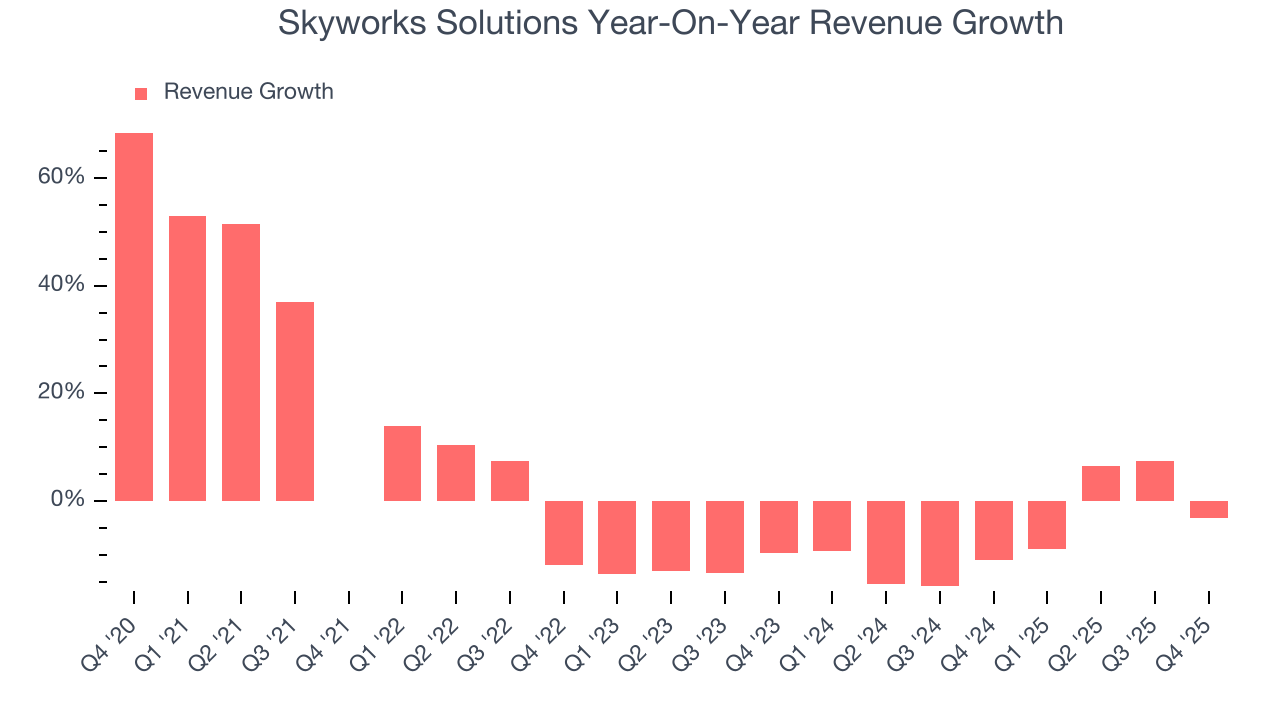

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, Skyworks Solutions struggled to consistently increase demand as its $4.05 billion of sales for the trailing 12 months was close to its revenue five years ago. This was below our standards and suggests it’s a low quality business. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

Long-term growth is the most important, but short-term results matter for semiconductors because the rapid pace of technological innovation (Moore's Law) could make yesterday's hit product obsolete today. Skyworks Solutions’s recent performance shows its demand remained suppressed as its revenue has declined by 6.6% annually over the last two years.

This quarter, Skyworks Solutions’s revenue fell by 3.1% year on year to $1.04 billion but beat Wall Street’s estimates by 3.4%. Company management is currently guiding for a 94,319% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to decline by 10.1% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will see some demand headwinds.

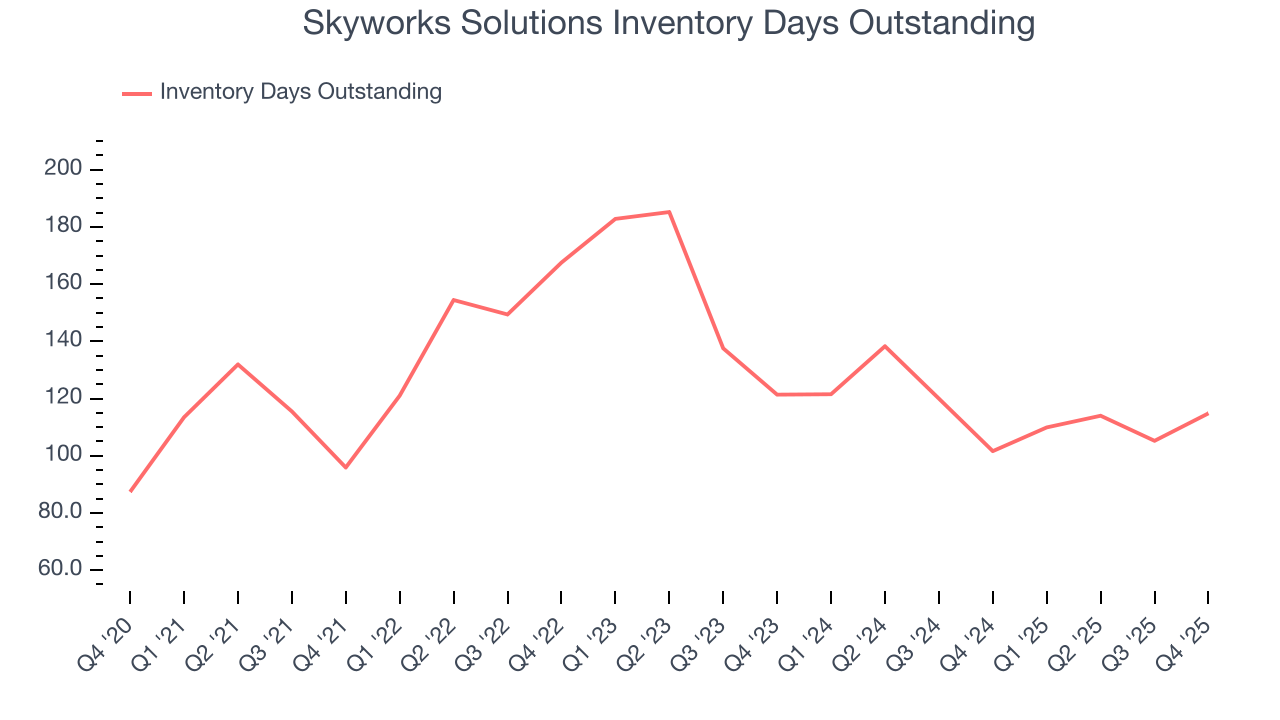

6. Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business’ capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Skyworks Solutions’s DIO came in at 115, which is 15 days below its five-year average. These numbers show that despite the recent increase, there’s no indication of an excessive inventory buildup.

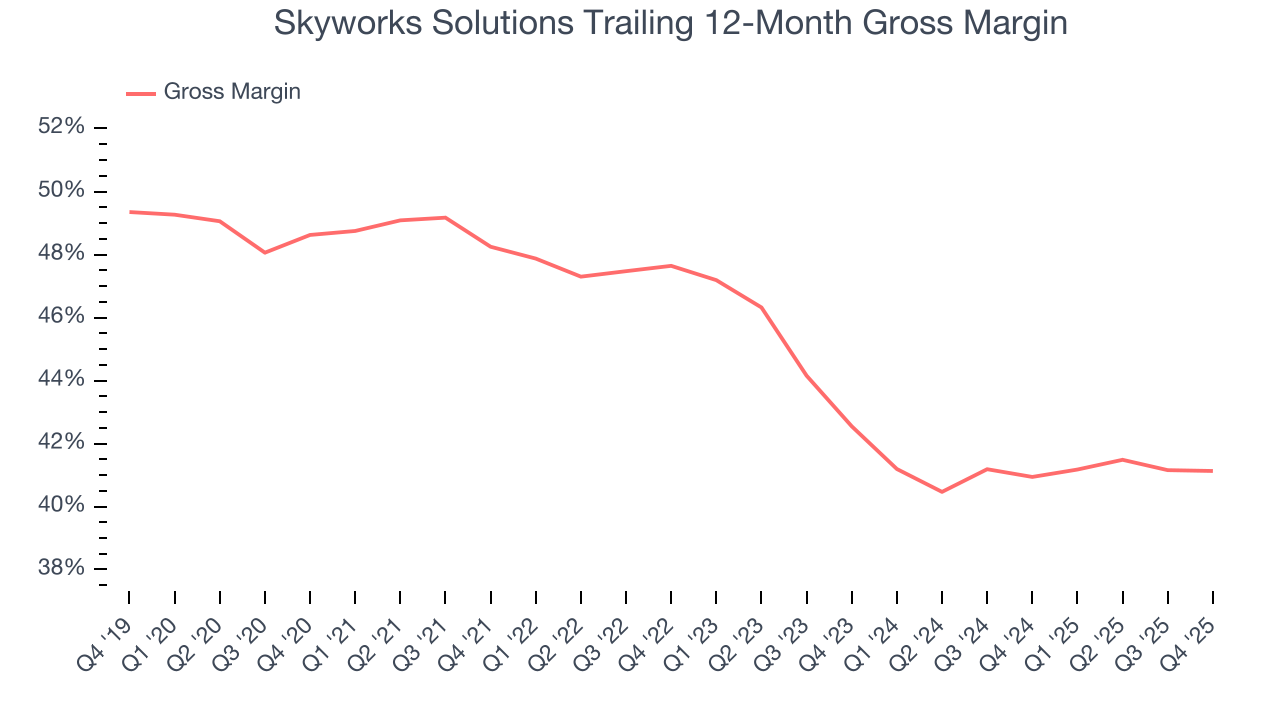

7. Gross Margin & Pricing Power

Gross profit margin is a key metric to track because it shows how much money a semiconductor company gets to keep after paying for its raw materials, manufacturing, and other input costs.

Skyworks Solutions’s gross margin is well below other semiconductor companies, indicating a lack of pricing power and a competitive market. As you can see below, it averaged a 41% gross margin over the last two years. That means Skyworks Solutions paid its suppliers a lot of money ($58.97 for every $100 in revenue) to run its business.

Skyworks Solutions’s gross profit margin came in at 41.3% this quarter, in line with the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

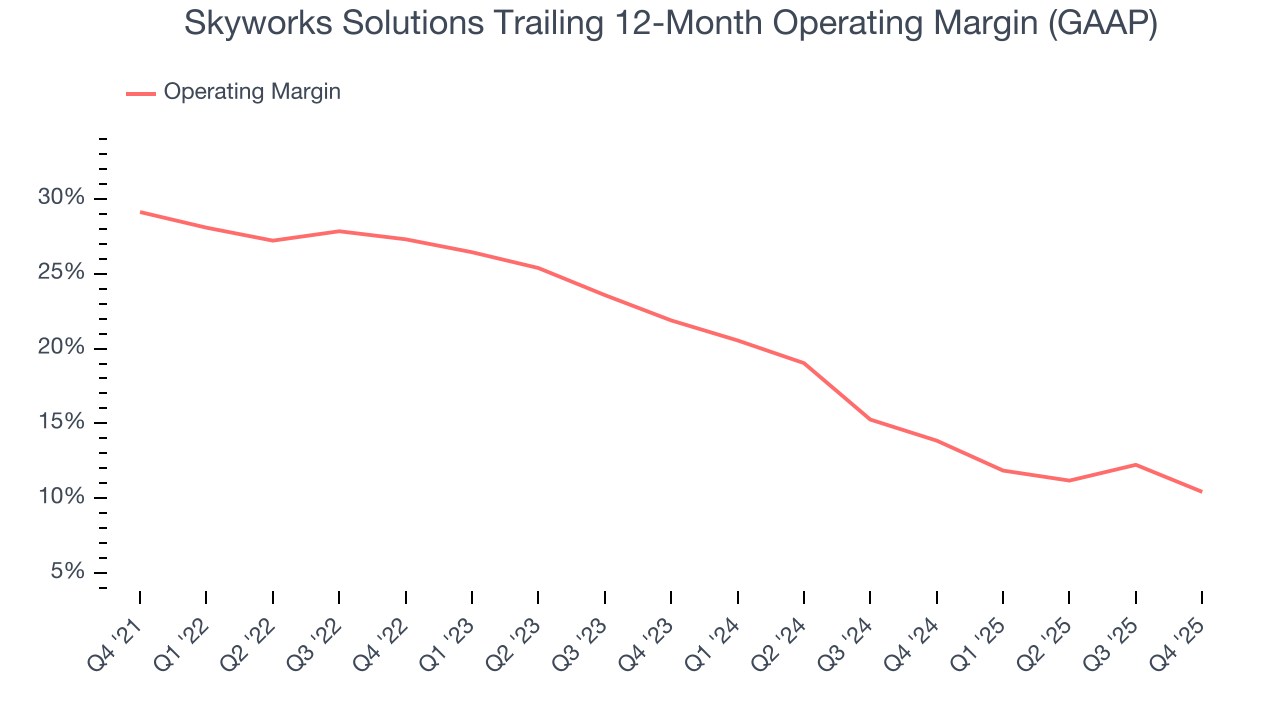

8. Operating Margin

Skyworks Solutions was profitable over the last two years but held back by its large cost base. Its average operating margin of 12.1% was weak for a semiconductor business. This result isn’t too surprising given its low gross margin as a starting point.

Analyzing the trend in its profitability, Skyworks Solutions’s operating margin decreased by 18.7 percentage points over the last five years. Skyworks Solutions’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q4, Skyworks Solutions generated an operating margin profit margin of 10%, down 6.9 percentage points year on year. Since Skyworks Solutions’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

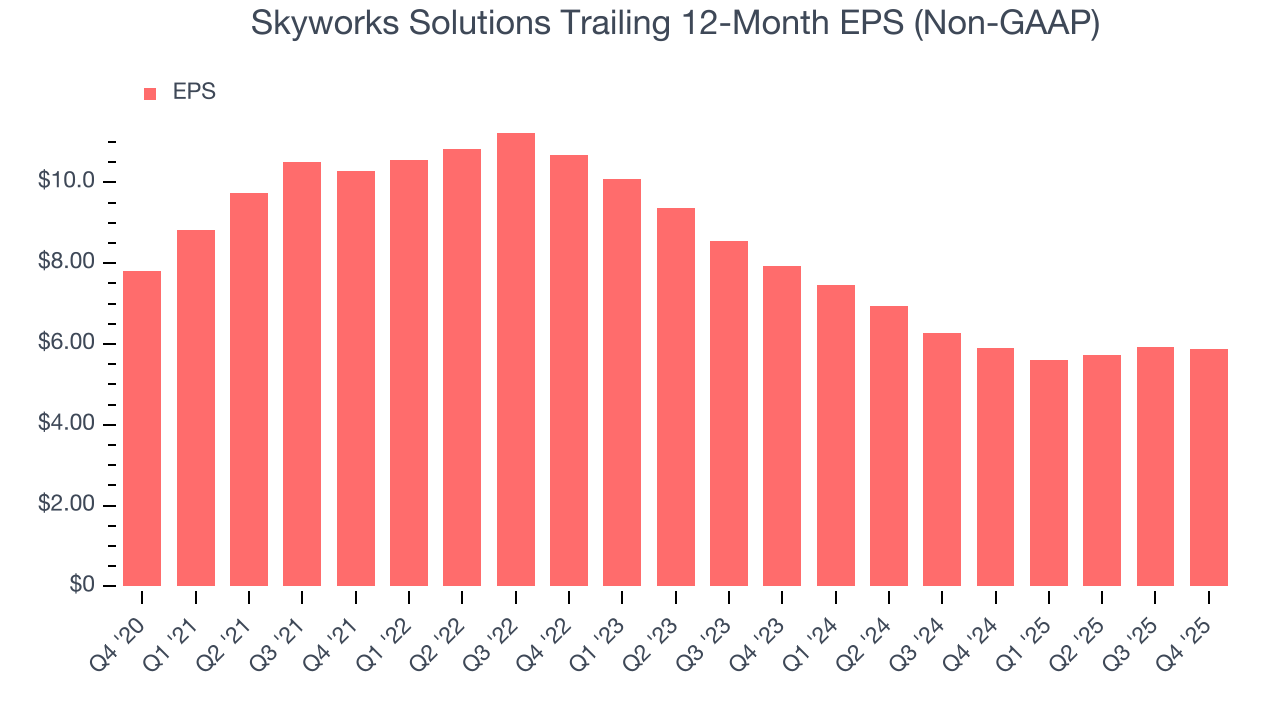

9. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Skyworks Solutions, its EPS declined by 5.5% annually over the last five years while its revenue was flat. This tells us the company struggled because its fixed cost base made it difficult to adjust to choppy demand.

We can take a deeper look into Skyworks Solutions’s earnings to better understand the drivers of its performance. As we mentioned earlier, Skyworks Solutions’s operating margin declined by 18.7 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, Skyworks Solutions reported adjusted EPS of $1.54, down from $1.60 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Skyworks Solutions’s full-year EPS of $5.87 to shrink by 25.8%.

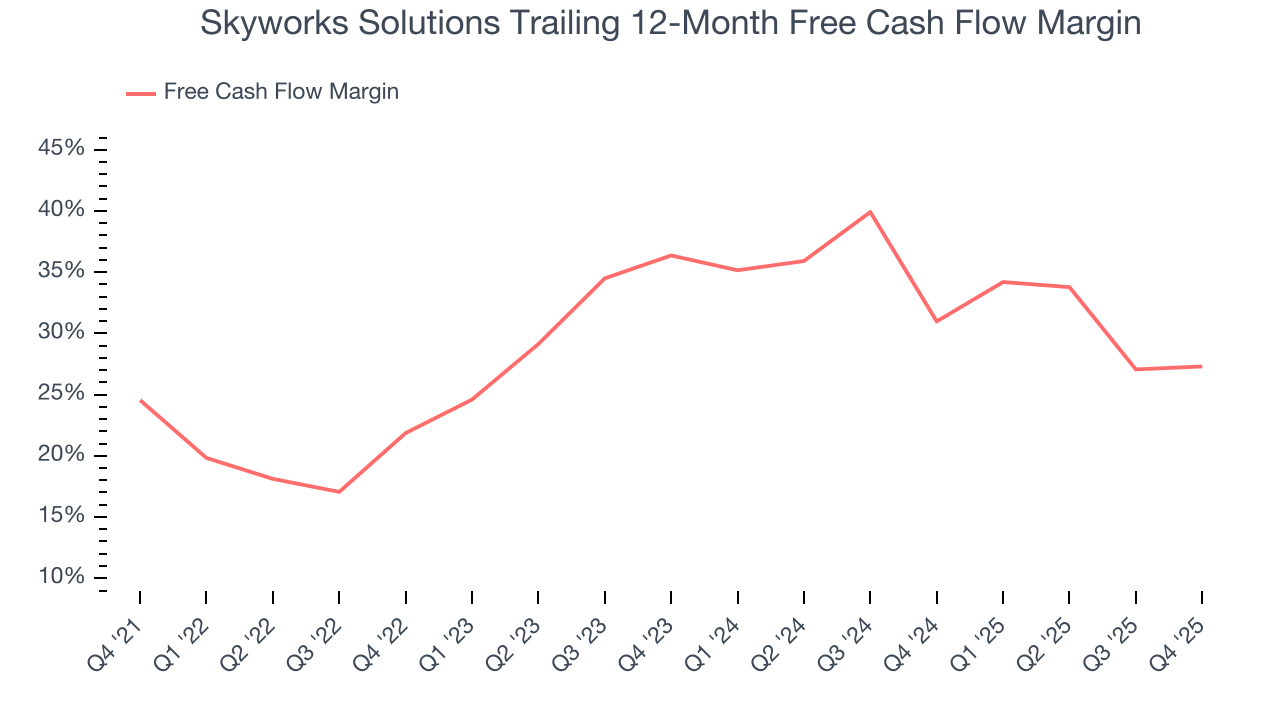

10. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Skyworks Solutions has shown terrific cash profitability, and if sustainable, puts it in an advantageous position to invest in new products, return capital to investors, and consolidate the market during industry downturns. The company’s free cash flow margin was among the best in the semiconductor sector, averaging 29.1% over the last two years.

Taking a step back, we can see that Skyworks Solutions’s margin expanded by 2.8 percentage points over the last five years. This shows the company is heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability fell.

Skyworks Solutions’s free cash flow clocked in at $339 million in Q4, equivalent to a 32.7% margin. This result was good as its margin was 1.1 percentage points higher than in the same quarter last year, building on its favorable historical trend.

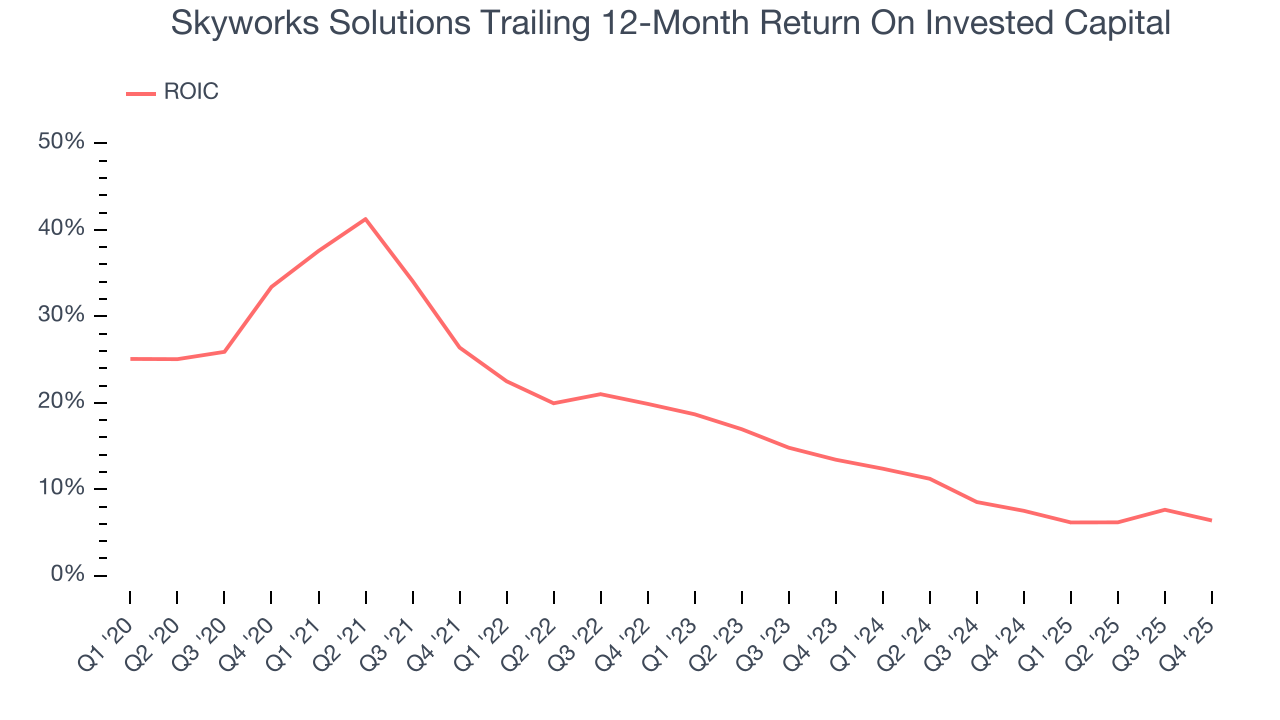

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Skyworks Solutions historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 14.7%, somewhat low compared to the best semiconductor companies that consistently pump out 35%+.

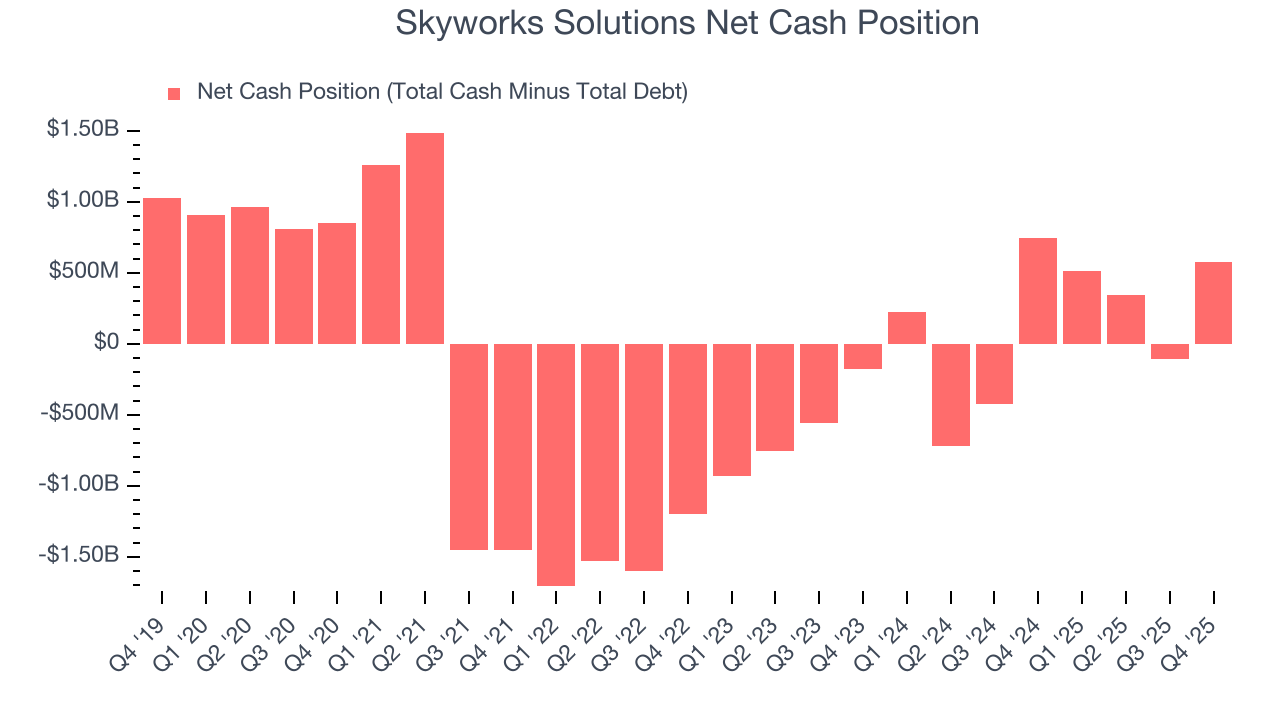

12. Balance Sheet Assessment

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

Skyworks Solutions is a profitable, well-capitalized company with $1.57 billion of cash and $996.2 million of debt on its balance sheet. This $572.4 million net cash position is 6.9% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

13. Key Takeaways from Skyworks Solutions’s Q4 Results

It was good to see Skyworks Solutions beat analysts’ EPS expectations this quarter. We were also excited its adjusted operating income outperformed Wall Street’s estimates by a wide margin. On the other hand, its inventory levels materially increased. Zooming out, we think this quarter featured some important positives. The stock traded up 1.8% to $57.04 immediately after reporting.

14. Is Now The Time To Buy Skyworks Solutions?

Updated: March 26, 2026 at 10:22 PM EDT

Before deciding whether to buy Skyworks Solutions or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

We cheer for all companies solving complex technology issues, but in the case of Skyworks Solutions, we’ll be cheering from the sidelines. To begin with, its revenue growth was weak over the last five years, and analysts expect its demand to deteriorate over the next 12 months. While its powerful free cash flow generation enables it to stay ahead of the competition through consistent reinvestment of profits, the downside is its projected EPS for the next year is lacking. On top of that, its declining operating margin shows the business has become less efficient.

Skyworks Solutions’s P/E ratio based on the next 12 months is 12.5x. At this valuation, there’s a lot of good news priced in - we think there are better opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $67.16 on the company (compared to the current share price of $57.43).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.