10x Genomics (TXG)

We wouldn’t buy 10x Genomics. Its negative returns on capital show it destroyed value by losing money on unprofitable business ventures.― StockStory Analyst Team

1. News

2. Summary

Why We Think 10x Genomics Will Underperform

Founded in 2012 by scientists seeking to overcome limitations in traditional biological research methods, 10x Genomics (NASDAQ:TXG) develops instruments, consumables, and software that enable researchers to analyze biological systems at single-cell resolution and spatial context.

- Push for growth has led to negative returns on capital, signaling value destruction

- Modest revenue base of $642.8 million gives it less fixed cost leverage and fewer distribution channels than larger companies

- Historical adjusted operating margin losses point to an inefficient cost structure

10x Genomics’s quality doesn’t meet our bar. There’s a wealth of better opportunities.

Why There Are Better Opportunities Than 10x Genomics

10x Genomics’s stock price of $18.56 implies a valuation ratio of 3.9x forward price-to-sales. The market typically values companies like 10x Genomics based on their anticipated profits for the next 12 months, but it expects the business to lose money. We also think the upside isn’t great compared to the potential downside here - there are more exciting stocks to buy.

It’s better to invest in high-quality businesses with strong long-term earnings potential rather than to buy lower-quality companies with open questions and big downside risks.

3. 10x Genomics (TXG) Research Report: Q4 CY2025 Update

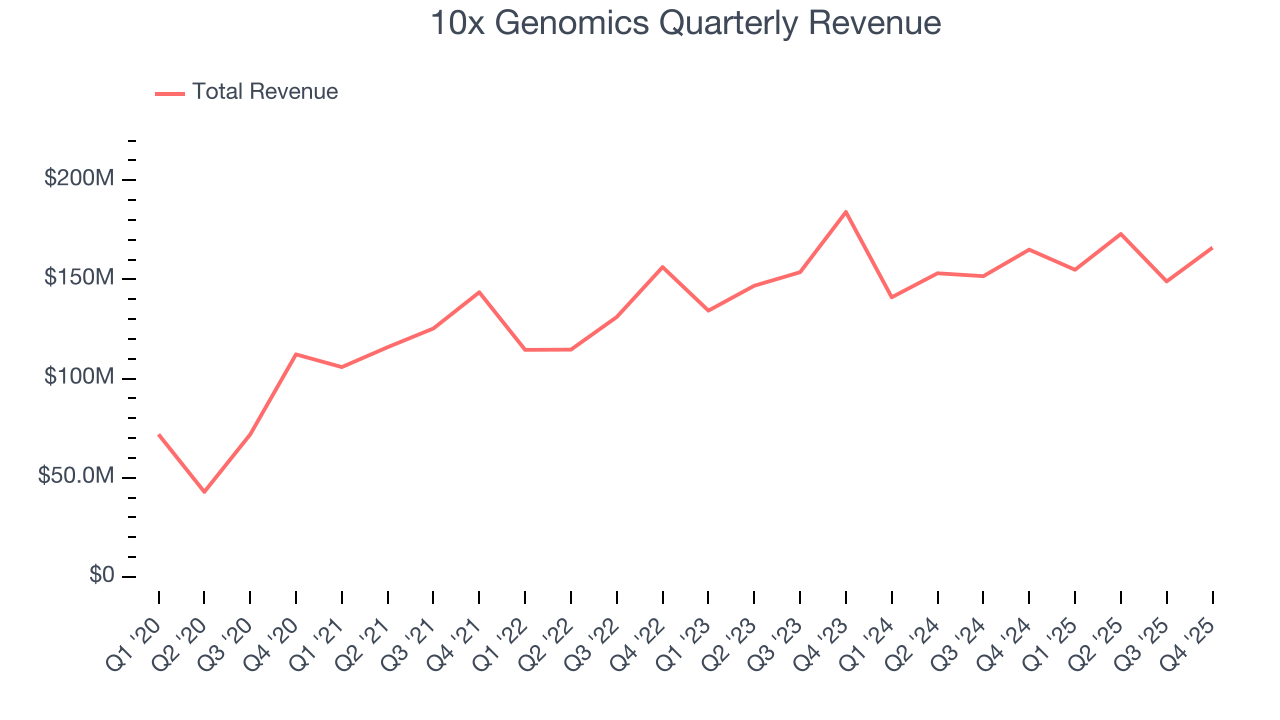

Biotech company 10x Genomics (NASDAQ:TXG) beat Wall Street’s revenue expectations in Q4 CY2025, but sales were flat year on year at $166 million. The company expects the full year’s revenue to be around $612.5 million, close to analysts’ estimates. Its GAAP loss of $0.13 per share was 37.5% above analysts’ consensus estimates.

10x Genomics (TXG) Q4 CY2025 Highlights:

- Revenue: $166 million vs analyst estimates of $159.2 million (flat year on year, 4.3% beat)

- EPS (GAAP): -$0.13 vs analyst estimates of -$0.21 (37.5% beat)

- Operating Margin: -11.8%, up from -30.2% in the same quarter last year

- Market Capitalization: $2.42 billion

Company Overview

Founded in 2012 by scientists seeking to overcome limitations in traditional biological research methods, 10x Genomics (NASDAQ:TXG) develops instruments, consumables, and software that enable researchers to analyze biological systems at single-cell resolution and spatial context.

10x Genomics' technology platforms allow scientists to examine the complexity of biology with unprecedented detail and scale. The company's solutions are built on expertise across multiple disciplines including chemistry, biology, microfluidics, hardware engineering, and computational software.

The company offers three main technology platforms. The Chromium platform enables high-throughput analysis of individual biological components by partitioning samples into millions of microscopic reaction chambers, allowing researchers to analyze single cells in detail. The Visium platform provides spatial analysis, showing where biological components are located within tissue samples, creating visual maps of gene expression across tissues. The Xenium platform performs in situ analysis, detecting RNA directly within tissue sections without requiring conventional sequencing.

These platforms are used by researchers to make discoveries in oncology, immunology, neuroscience, and other fields. For example, cancer researchers might use 10x technology to identify rare cell types within tumors that could influence treatment response, while immunologists might map immune cell interactions to develop more effective therapies.

The company's business model involves selling instruments that run exclusively with its proprietary consumables and software. A typical customer workflow begins with sample preparation, followed by processing on one of 10x's instruments, then analysis using the company's software. For instance, a neuroscience researcher studying Alzheimer's disease might use the Visium platform to visualize gene expression changes across brain tissue sections, revealing which regions show early disease markers.

10x Genomics primarily serves academic institutions, government research labs, and biopharmaceutical companies worldwide. The company maintains a direct sales force in North America and parts of Europe, while working with distribution partners in Asia and other regions.

4. Genomics & Sequencing

Genomics and sequencing companies within the life sciences industry provide the technology for increasingly personalized medicine, drug discovery, and disease research. These firms leverage cutting-edge platforms for high-throughput sequencing and genomic analysis, enabling researchers and healthcare providers to better understand genetic underpinnings of diseases. While the industry enjoys high barriers to entry due to proprietary technology and intellectual property, the business model also faces significant R&D costs, reliance on continued innovation, and exposure to shifts in academic, biotech, and clinical research funding. Over the next few years, the subsector is well-positioned to benefit from tailwinds such as increasing adoption of precision medicine, expanded applications for sequencing technologies in areas like oncology and rare disease diagnostics, and growing use of genomic data in drug development. Advances in artificial intelligence could further enhance the speed and accuracy of genomic insights. However, potential headwinds include price sensitivity among research institutions and healthcare systems that are constantly trying to contain and lower costs. Additionally, regulations around data privacy and genomic testing are not yet set in stone, adding uncertainty to the industry.

10x Genomics competes with NanoString Technologies (NASDAQ:NSTG), Bio-Rad Laboratories (NYSE:BIO), Illumina (NASDAQ:ILMN), and Akoya Biosciences (NASDAQ:AKYA) in the spatial biology and single-cell analysis markets. The company also faces competition from emerging private companies like Parse Biosciences and Vizgen.

5. Revenue Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With just $642.8 million in revenue over the past 12 months, 10x Genomics is a small company in an industry where scale matters. This makes it difficult to build trust with customers because healthcare is heavily regulated, complex, and resource-intensive.

6. Revenue Growth

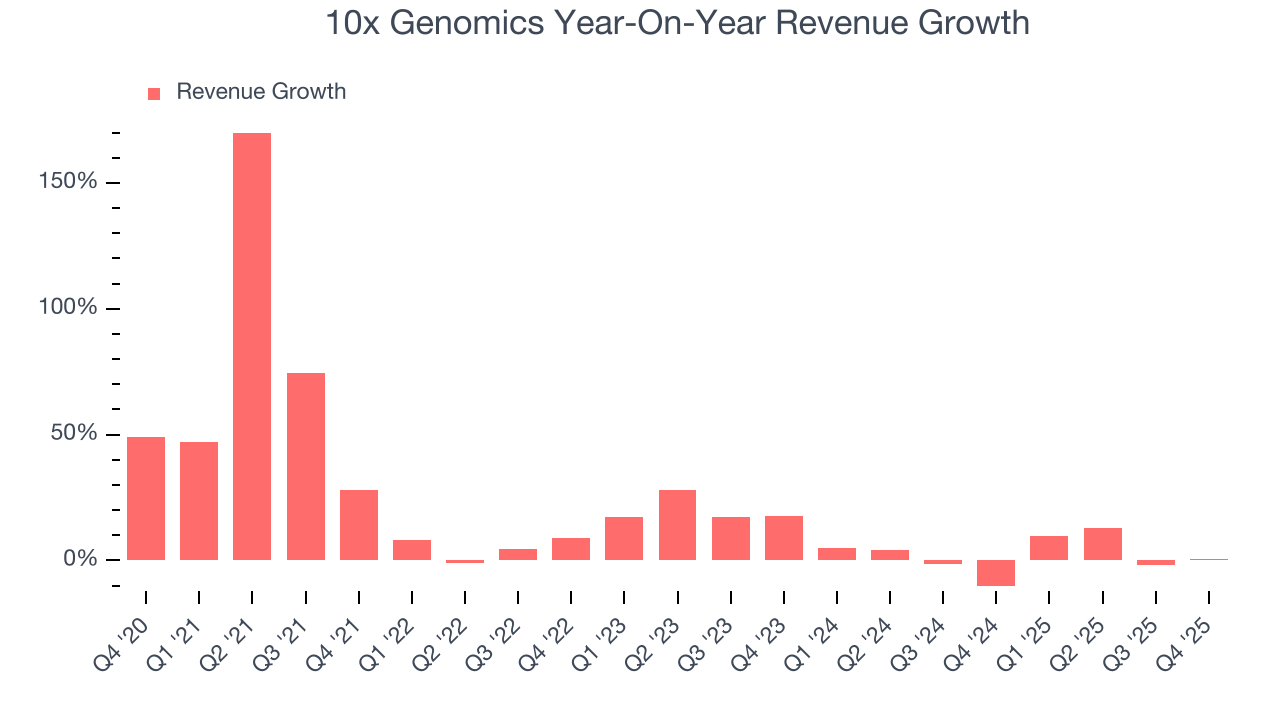

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years. Thankfully, 10x Genomics’s 16.6% annualized revenue growth over the last five years was impressive. Its growth beat the average healthcare company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. 10x Genomics’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 1.9% over the last two years was well below its five-year trend.

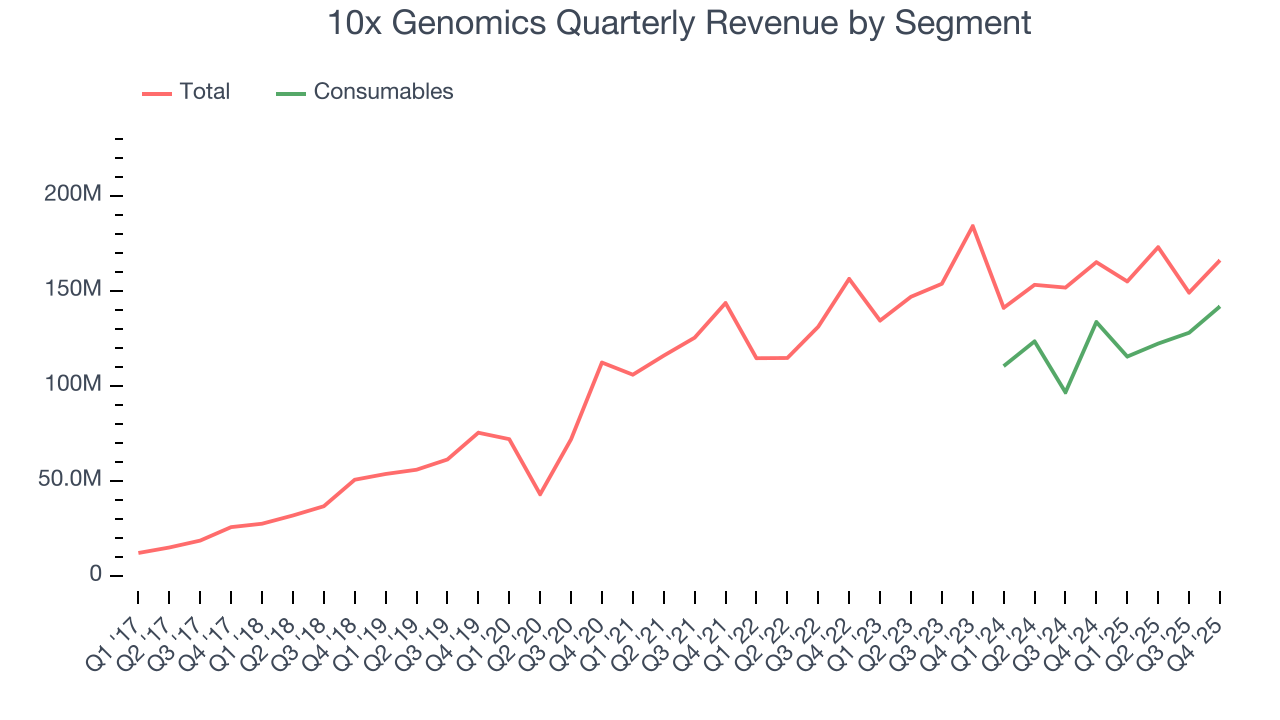

We can dig further into the company’s revenue dynamics by analyzing its most important segment, Consumables. Over the last two years, 10x Genomics’s Consumables revenue (recurring orders) averaged 10.6% year-on-year growth. This segment has outperformed its total sales during the same period, lifting the company’s performance.

This quarter, 10x Genomics’s $166 million of revenue was flat year on year but beat Wall Street’s estimates by 4.3%.

Looking ahead, sell-side analysts expect revenue to decline by 5% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and implies its products and services will see some demand headwinds.

7. Operating Margin

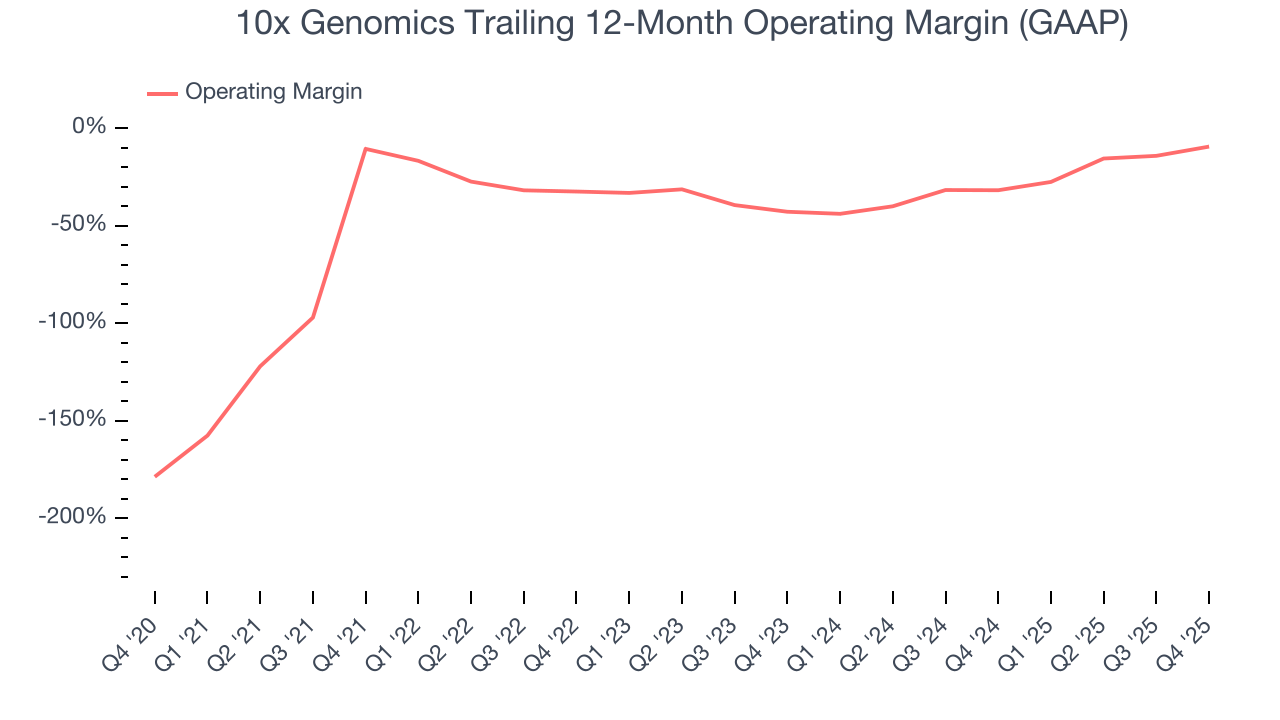

10x Genomics’s high expenses have contributed to an average operating margin of negative 25.7% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, 10x Genomics’s operating margin rose by 1.2 percentage points over the last five years, as its sales growth gave it operating leverage. This performance was mostly driven by its recent improvements as the company’s margin has increased by 33.4 percentage points on a two-year basis.

10x Genomics’s operating margin was negative 11.8% this quarter.

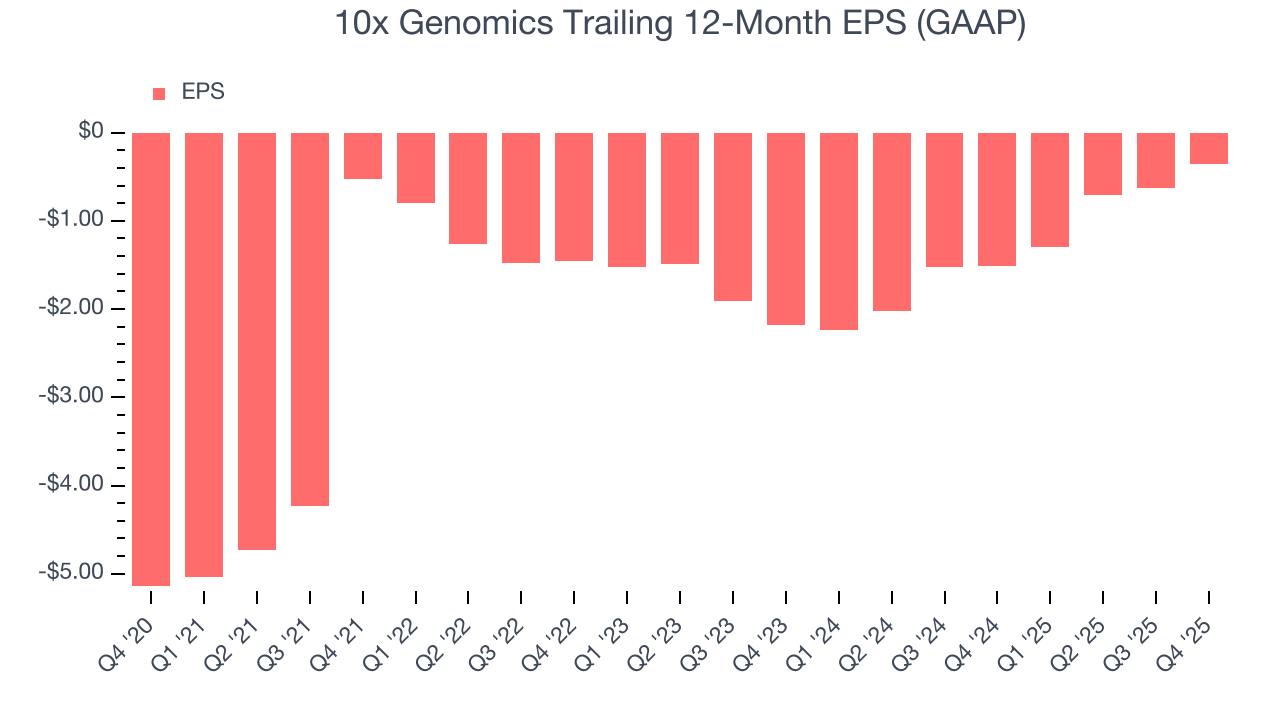

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Although 10x Genomics’s full-year earnings are still negative, it reduced its losses and improved its EPS by 41.5% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability.

In Q4, 10x Genomics reported EPS of negative $0.13, up from negative $0.40 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects 10x Genomics to perform poorly. Analysts forecast its full-year EPS of negative $0.35 will tumble to negative $0.94.

9. Cash Is King

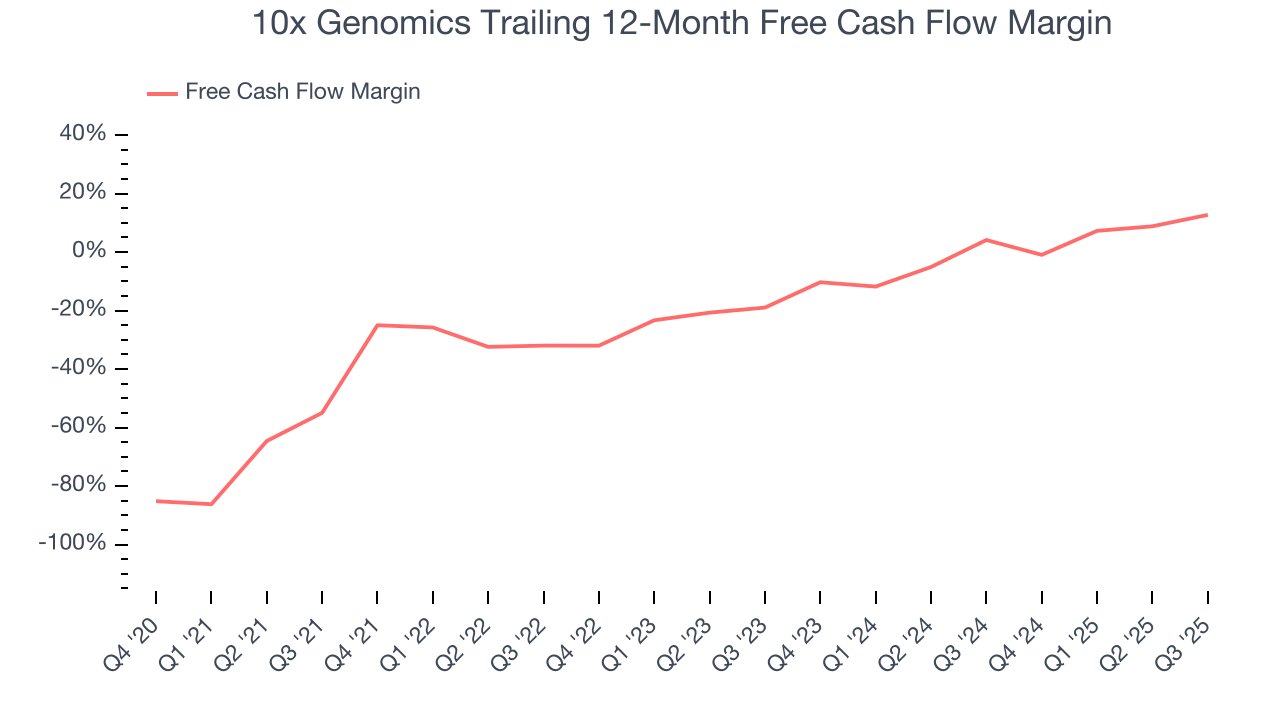

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

10x Genomics’s demanding reinvestments have consumed many resources over the last five years, contributing to an average free cash flow margin of negative 9.8%. This means it lit $9.82 of cash on fire for every $100 in revenue.

Taking a step back, an encouraging sign is that 10x Genomics’s margin expanded by 48.2 percentage points during that time. We have no doubt shareholders would like to continue seeing its cash conversion rise.

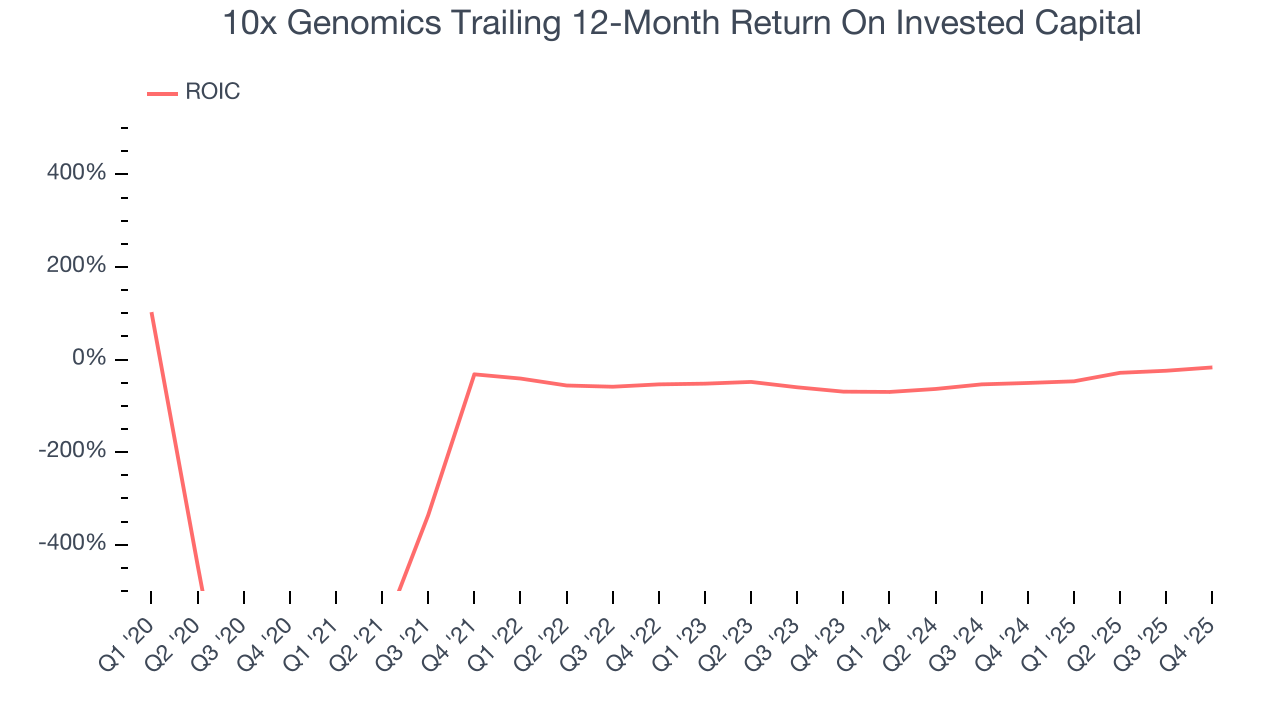

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

10x Genomics’s five-year average ROIC was negative 44.5%, meaning management lost money while trying to expand the business. Its returns were among the worst in the healthcare sector.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, 10x Genomics’s ROIC has increased. This is a good sign, but we recognize its lack of profitable growth during the COVID era was the primary reason for the change.

11. Balance Sheet Assessment

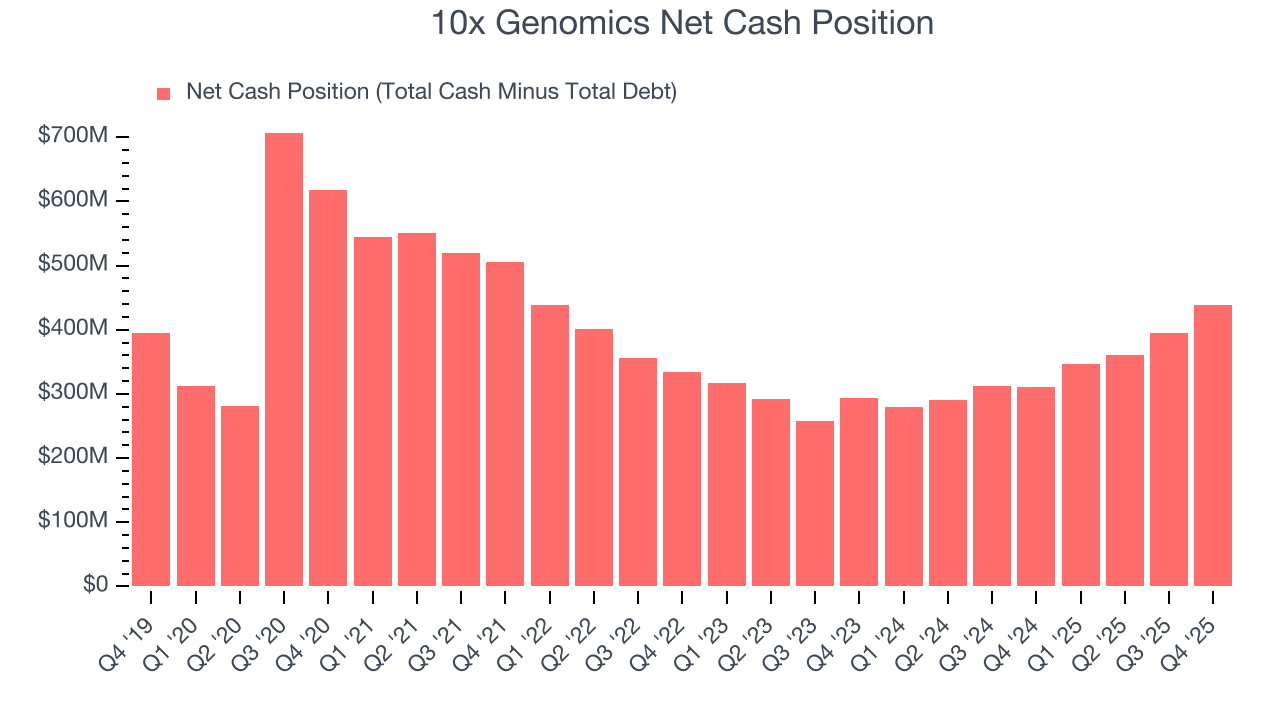

Companies with more cash than debt have lower bankruptcy risk.

10x Genomics is a well-capitalized company with $523.4 million of cash and $84.36 million of debt on its balance sheet. This $439 million net cash position is 19.1% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from 10x Genomics’s Q4 Results

It was good to see 10x Genomics beat analysts’ EPS expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock remained flat at $17.44 immediately following the results.

13. Is Now The Time To Buy 10x Genomics?

Updated: March 16, 2026 at 12:29 AM EDT

Are you wondering whether to buy 10x Genomics or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

We see the value of companies making people healthier, but in the case of 10x Genomics, we’re out. Although its revenue growth was impressive over the last five years, it’s expected to deteriorate over the next 12 months and its relatively low ROIC suggests management has struggled to find compelling investment opportunities. And while the company’s rising cash profitability gives it more optionality, the downside is its subscale operations give it fewer distribution channels than its larger rivals.

10x Genomics’s forward price-to-sales ratio is 3.9x. The market typically values companies like 10x Genomics based on their anticipated profits for the next 12 months, but it expects the business to lose money. We also think the upside isn’t great compared to the potential downside here - there are more exciting stocks to buy.

Wall Street analysts have a consensus one-year price target of $20.14 on the company (compared to the current share price of $18.56).