Upwork (UPWK)

Upwork is intriguing. Its efficient marketing engine and robust unit economics tee it up for immense long-term profits.― StockStory Analyst Team

1. News

2. Summary

Why Upwork Is Interesting

Formed through the 2013 merger of Elance and oDesk, Upwork (NASDAQ:UPWK) is an online platform where businesses and independent professionals connect to get work done.

- Successful business model is illustrated by its impressive EBITDA margin, and its rise over the last few years was fueled by some leverage on its fixed costs

- Impressive free cash flow profitability enables the company to fund new investments or reward investors with share buybacks/dividends, and its improved cash conversion implies it’s becoming a less capital-intensive business

- A drawback is its value proposition isn’t resonating strongly as its active clients averaged 7% drops over the last two years

Upwork has some respectable qualities. If you believe in the company, the price looks fair.

3. Upwork (UPWK) Research Report: Q4 CY2025 Update

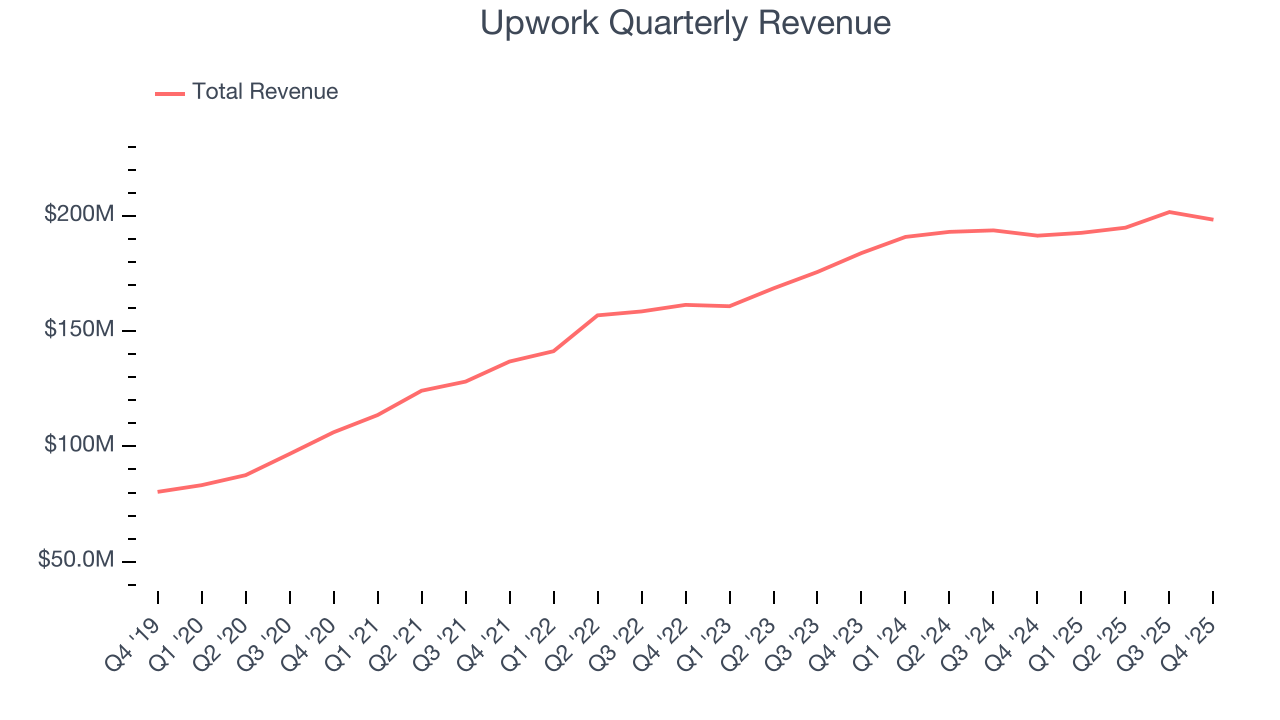

Online work marketplace Upwork (NASDAQ:UPWK) met Wall Street’s revenue expectations in Q4 CY2025, with sales up 3.6% year on year to $198.4 million. On the other hand, next quarter’s revenue guidance of $194.5 million was less impressive, coming in 3.1% below analysts’ estimates. Its non-GAAP profit of $0.36 per share was 15.5% above analysts’ consensus estimates.

Correction note:

The previous version of this report had a wrong label for Active Clients count. This has been updated in the current version.

Upwork (UPWK) Q4 CY2025 Highlights:

- Revenue: $198.4 million vs analyst estimates of $197.6 million (3.6% year-on-year growth, in line)

- Adjusted EPS: $0.36 vs analyst estimates of $0.31 (15.5% beat)

- Adjusted EBITDA: $52.86 million vs analyst estimates of $51.63 million (26.6% margin, 2.4% beat)

- Revenue Guidance for Q1 CY2026 is $194.5 million at the midpoint, below analyst estimates of $200.7 million

- Adjusted EPS guidance for the upcoming financial year 2026 is $1.46 at the midpoint, in line with analyst estimates

- EBITDA guidance for the upcoming financial year 2026 is $245 million at the midpoint, in line with analyst expectations

- Operating Margin: 14.3%, up from 7.1% in the same quarter last year

- Free Cash Flow Margin: 28.9%, down from 34.4% in the previous quarter

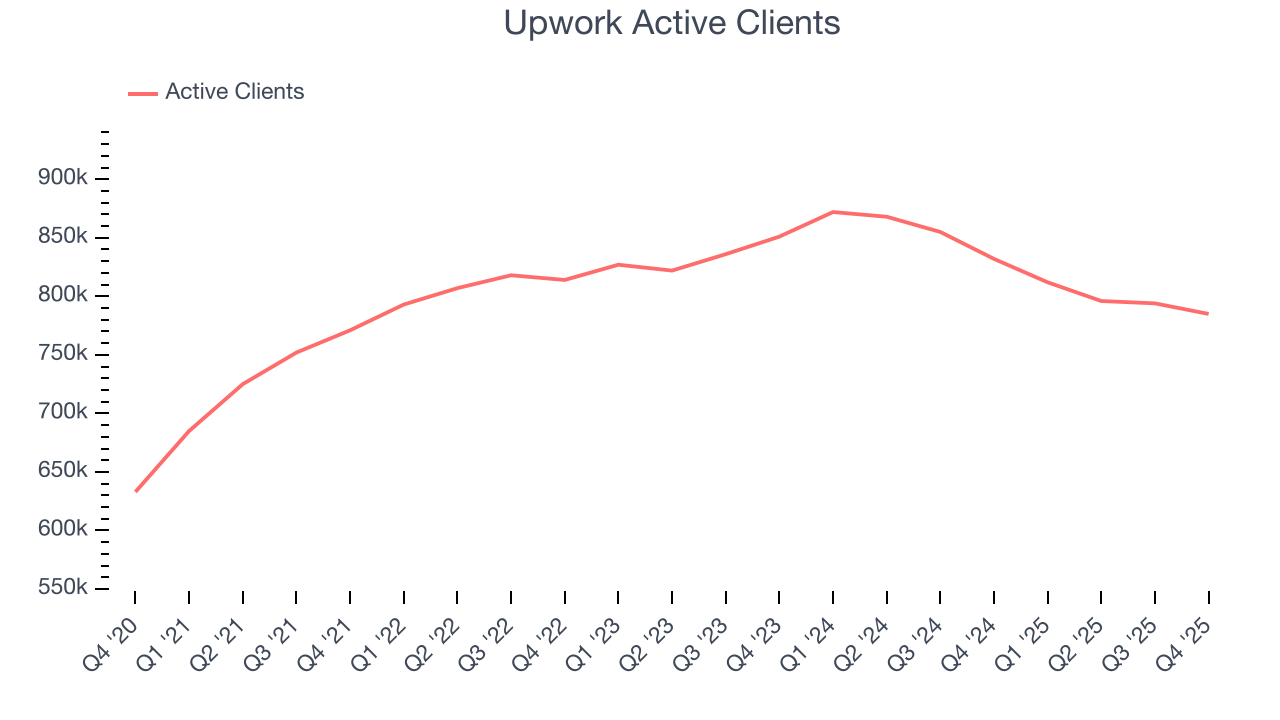

- Active Clients: 785,000, down 47,000 year on year

- Market Capitalization: $1.99 billion

Company Overview

Formed through the 2013 merger of Elance and oDesk, Upwork (NASDAQ:UPWK) is an online platform where businesses and independent professionals connect to get work done.

Upwork was born to address the growing need for a flexible workforce and remote collaboration. Its platform serves as a bridge between businesses needing specialized skills and freelancers offering those skills. Specific projects that Upwork facilitates include web development, graphic design, content writing, and marketing. Employers post jobs, freelancers submit proposals, and Upwork provides the tools for contract management, time tracking, and secure payments.

Upwork's revenue comes from service fees charged to freelancers and clients, premium membership subscriptions, and payment processing fees. Its business model is centered on creating value by enabling efficient, trustworthy remote work relationships. The platform appeals to startups, SMBs, and large enterprises, offering scalable solutions from one-off projects to long-term contracts.

Today, Upwork operates in over 180 countries and is one of the largest global freelancer marketplaces. Roughly half of its business is overseas, with a focus on India and the Philippines.

4. Gig Economy

The iPhone changed the world, ushering in the era of the “always-on” internet and “on-demand” services - anything someone could want is just a few taps away. Likewise, the gig economy sprang up in a similar fashion, with a proliferation of tech-enabled freelance labor marketplaces, which work hand and hand with many on demand services. Individuals can now work on demand too. What began with tech-enabled platforms that aggregated riders and drivers has expanded over the past decade to include food delivery, groceries, and now even a plumber or graphic designer are all just a few taps away.

Upwork's competitors include Fiverr (NYSE:FVRR), TaskUs (NASDAQ:TASK), Robert Half (NYSE:RHI), Meta's Facebook Marketplace (NASDAQ:META), and Microsoft’s LinkedIn (NASDAQ:MSFT).

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, Upwork’s 8.4% annualized revenue growth over the last three years was mediocre. This wasn’t a great result compared to the rest of the consumer internet sector, but there are still things to like about Upwork.

This quarter, Upwork grew its revenue by 3.6% year on year, and its $198.4 million of revenue was in line with Wall Street’s estimates. Company management is currently guiding for flat sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 7% over the next 12 months, similar to its three-year rate. This projection doesn't excite us and suggests its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

6. Active Clients

Customer Growth

As a gig economy marketplace, Upwork generates revenue growth by expanding the number of services on its platform (e.g. rides, deliveries, freelance jobs) and raising the commission fee from each service provided.

Upwork struggled with new customer acquisition over the last two years as its active clients have declined by 2.1% annually to 785,000 in the latest quarter. This performance isn't ideal because internet usage is secular, meaning there are typically unaddressed market opportunities. If Upwork wants to accelerate growth, it likely needs to enhance the appeal of its current offerings or innovate with new products.

In Q4, Upwork’s active clients once again decreased by 47,000, a 5.6% drop since last year. The quarterly print was lower than its two-year result, suggesting its new initiatives aren’t moving the needle for customers yet.

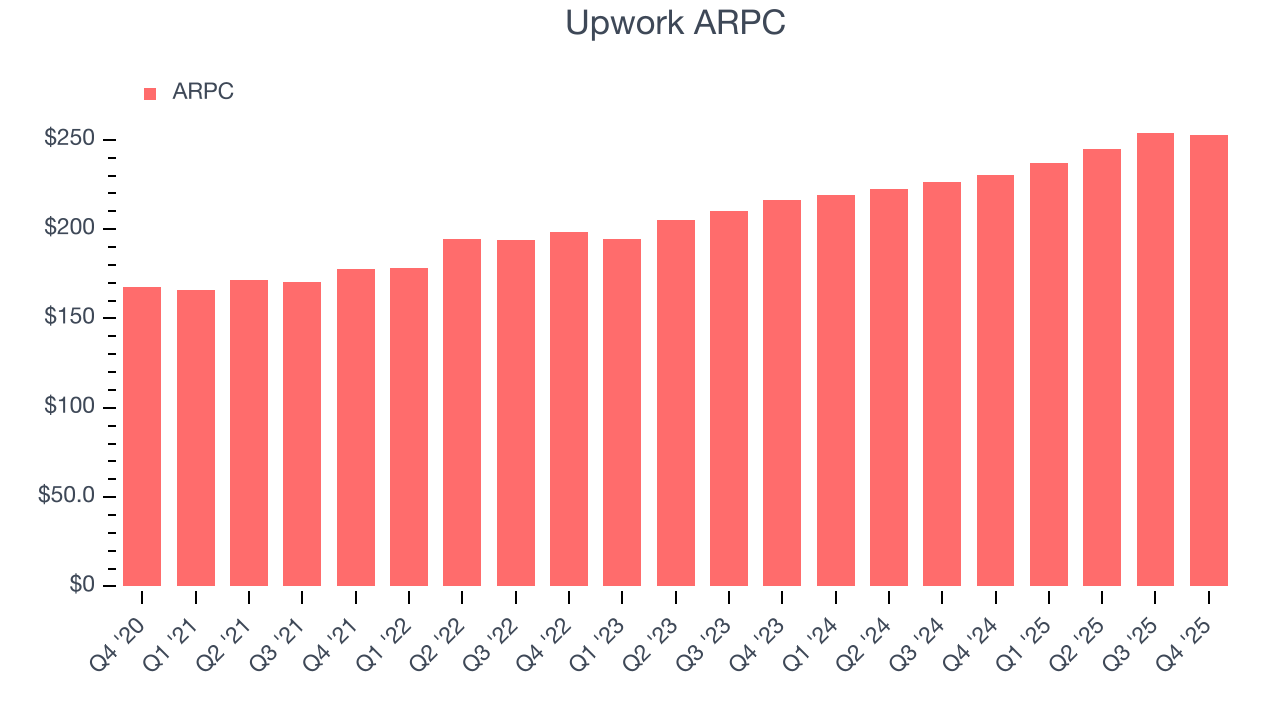

Revenue Per Customer

Average revenue per customer (ARPC) is a critical metric to track because it measures how much the company earns in transaction fees from each customer. This number also informs us about Upwork’s take rate, which represents its pricing leverage over the ecosystem, or "cut" from each transaction.

Upwork’s ARPC growth has been excellent over the last two years, averaging 9.5%. Although its active clients shrank during this time, the company’s ability to successfully increase monetization demonstrates its platform’s value for existing customers.

This quarter, Upwork’s ARPC clocked in at $252.75. It grew by 9.8% year on year, faster than its active clients.

7. Gross Margin & Pricing Power

A company’s gross profit margin has a significant impact on its ability to exert pricing power, develop new products, and invest in marketing. These factors can determine the winner in a competitive market.

For gig economy businesses like Upwork, gross profit tells us how much money the company gets to keep after covering the base cost of its products and services, which typically include server hosting, customer support, and payment processing fees. Another cost of revenue could also be insurance to protect against liabilities arising from providing transportation, housing, or freelance work services.

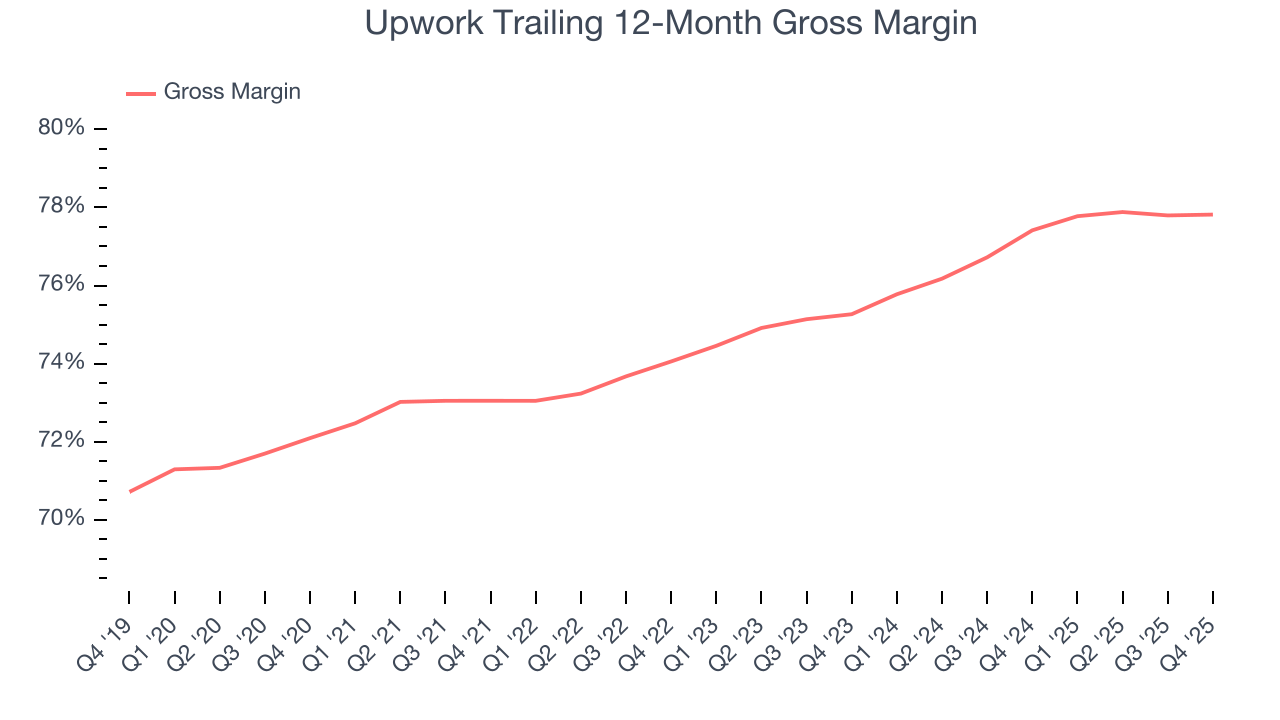

Upwork has robust unit economics, an output of its asset-lite business model and pricing power. Its margin is better than the broader consumer internet industry and enables the company to fund large investments in new products and marketing during periods of rapid growth to achieve higher profits in the future. As you can see below, it averaged an excellent 77.6% gross margin over the last two years. That means Upwork only paid its providers $22.38 for every $100 in revenue.

This quarter, Upwork’s gross profit margin was 78%, in line with the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

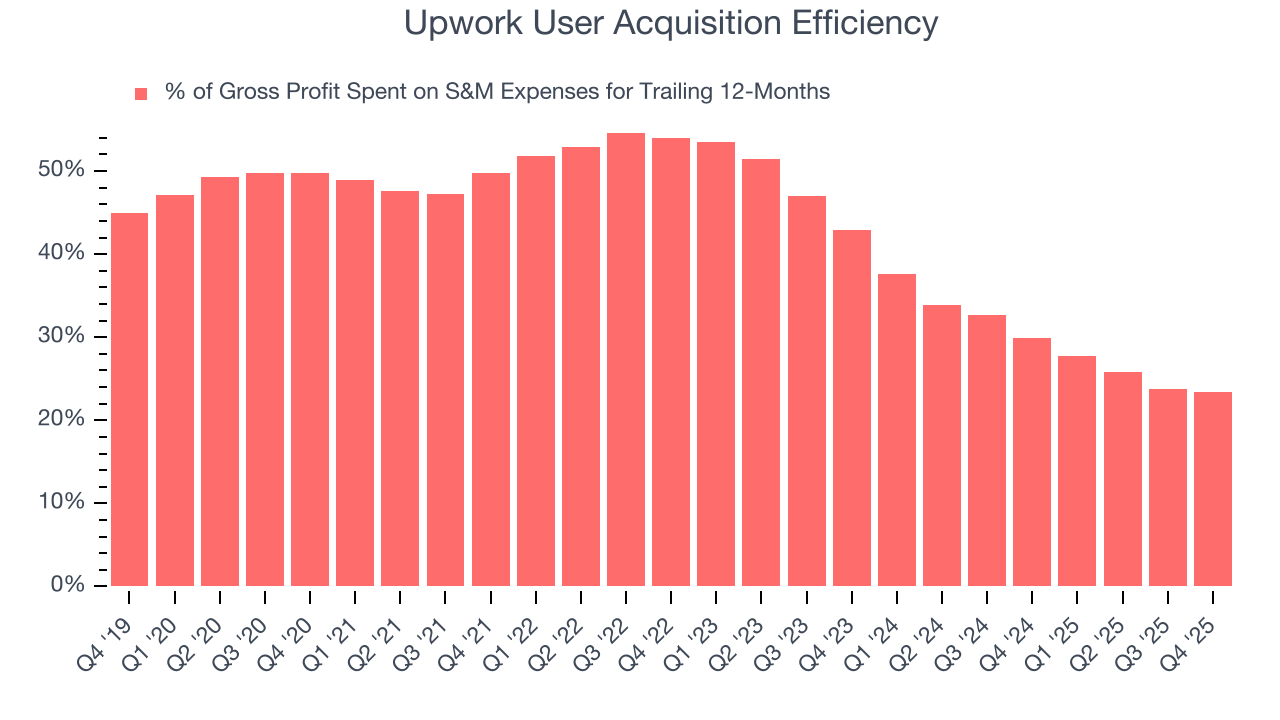

8. User Acquisition Efficiency

Unlike enterprise software that’s typically sold by dedicated sales teams, consumer internet businesses like Upwork grow from a combination of product virality, paid advertisement, and incentives.

Upwork is very efficient at acquiring new users, spending only 23.4% of its gross profit on sales and marketing expenses over the last year. This efficiency indicates that it has a highly differentiated product offering and strong brand reputation, giving Upwork the freedom to invest its resources into new growth initiatives while maintaining optionality.

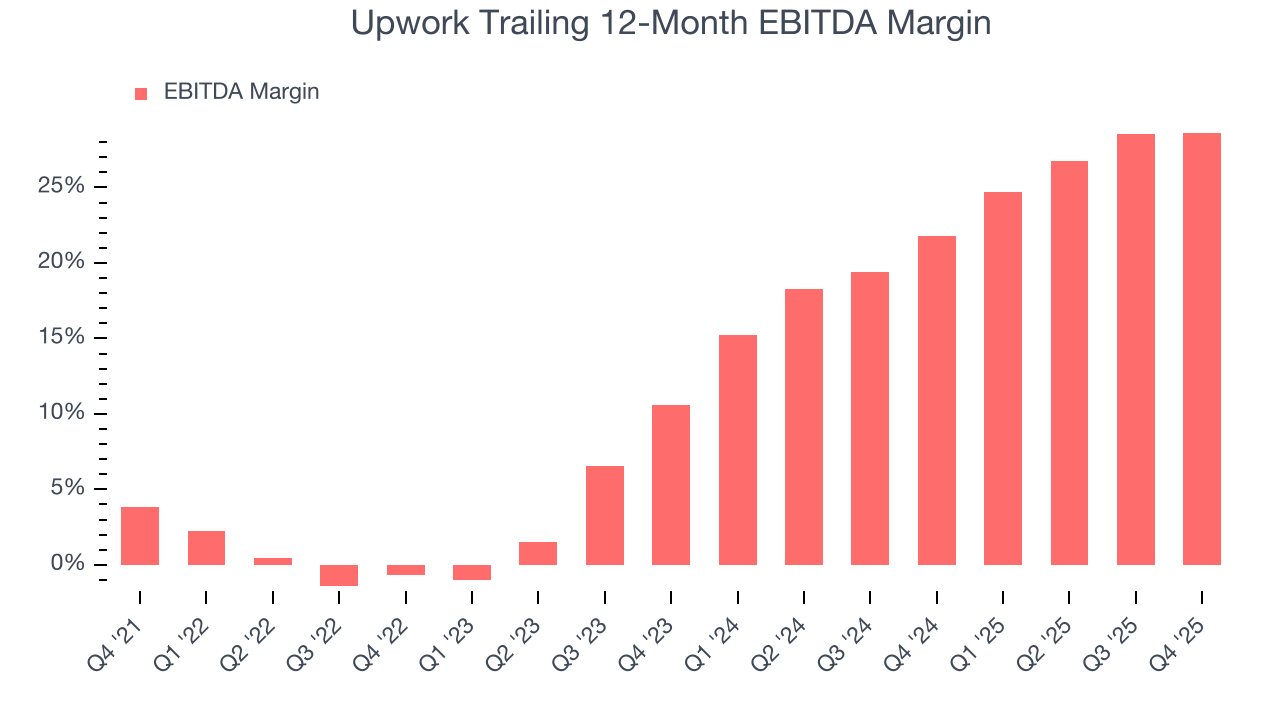

9. EBITDA

Operating income is often evaluated to assess a company’s underlying profitability. In a similar vein, EBITDA is used to analyze consumer internet companies because it excludes various one-time or non-cash expenses (depreciation), providing a clearer view of the business’s profit potential.

Upwork has been a well-oiled machine over the last two years. It demonstrated elite profitability for a consumer internet business, boasting an average EBITDA margin of 25.2%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Upwork’s EBITDA margin rose by 29.3 percentage points over the last few years, as its sales growth gave it operating leverage.

In Q4, Upwork generated an EBITDA margin profit margin of 26.6%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

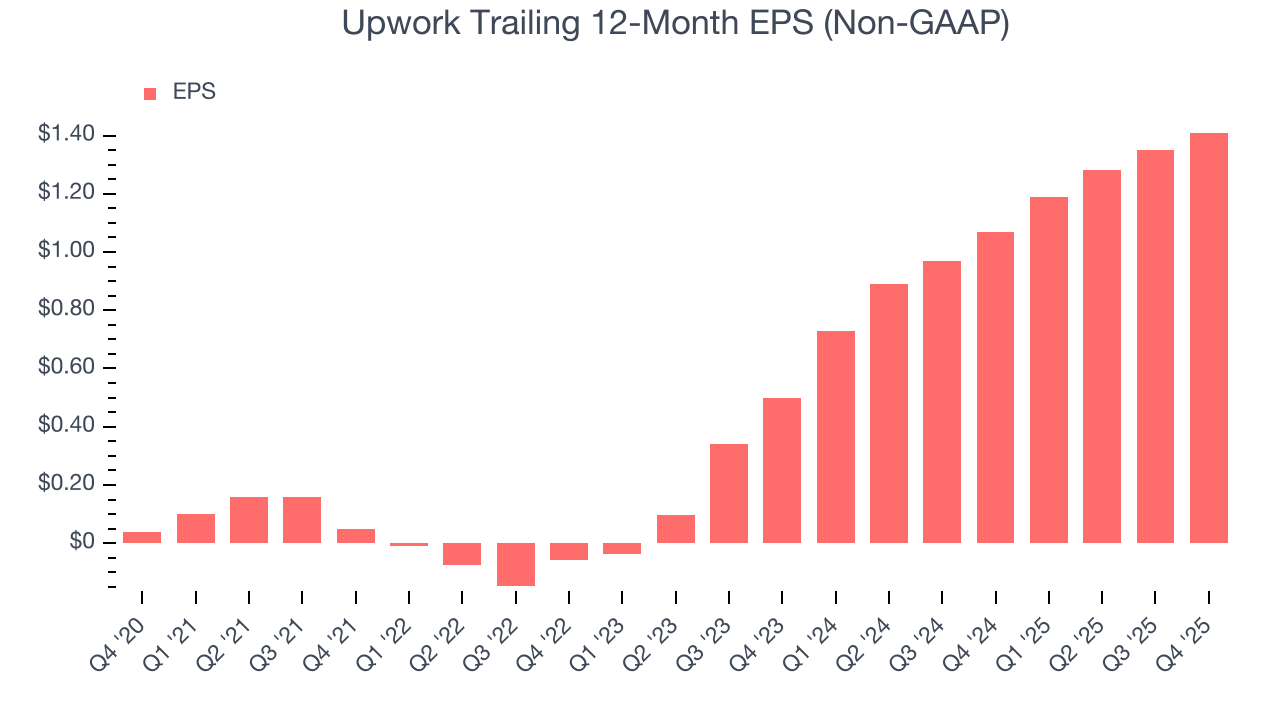

10. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Upwork’s full-year EPS flipped from negative to positive over the last three years. This is a good sign and shows it’s at an inflection point.

In Q4, Upwork reported adjusted EPS of $0.36, up from $0.30 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Upwork’s full-year EPS of $1.41 to grow 2.1%.

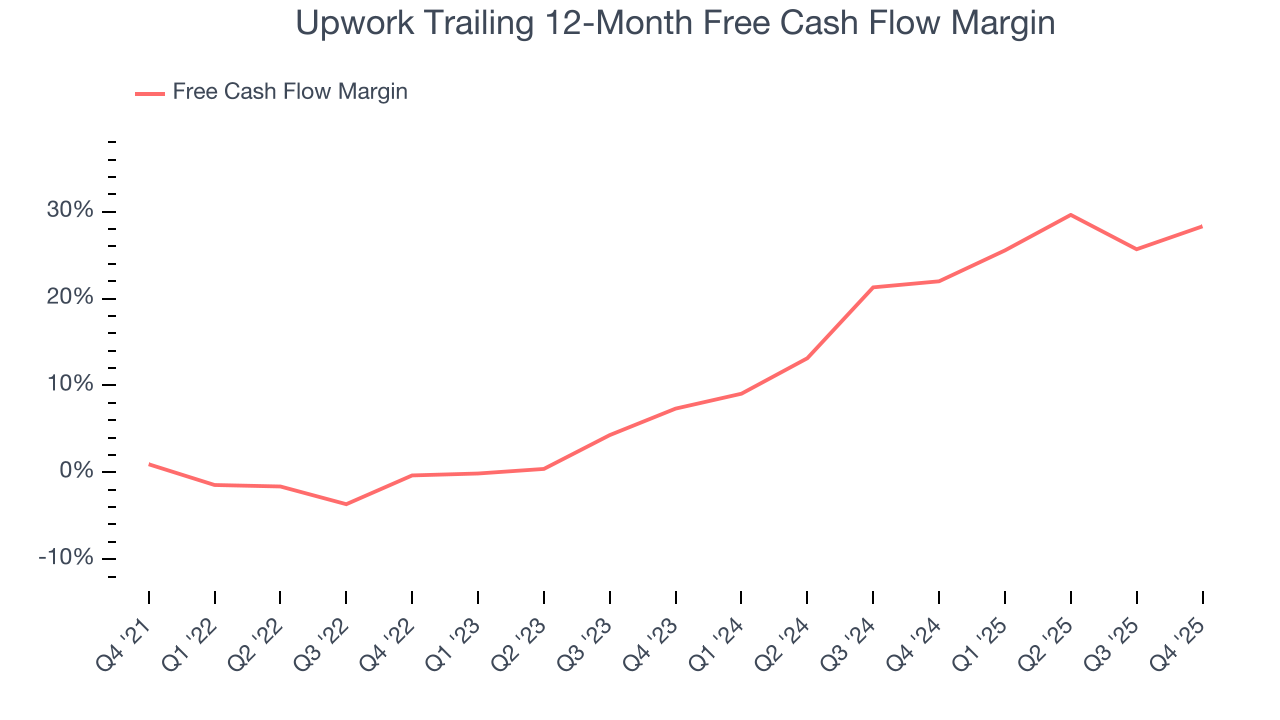

11. Cash Is King

Although EBITDA is undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Upwork has shown terrific cash profitability, driven by its lucrative business model and cost-effective customer acquisition strategy that enable it to stay ahead of the competition through investments in new products rather than sales and marketing. The company’s free cash flow margin was among the best in the consumer internet sector, averaging 25.2% over the last two years.

Taking a step back, we can see that Upwork’s margin expanded by 28.7 percentage points over the last few years. This is encouraging because it gives the company more optionality.

Upwork’s free cash flow clocked in at $57.27 million in Q4, equivalent to a 28.9% margin. This result was good as its margin was 10.7 percentage points higher than in the same quarter last year, building on its favorable historical trend.

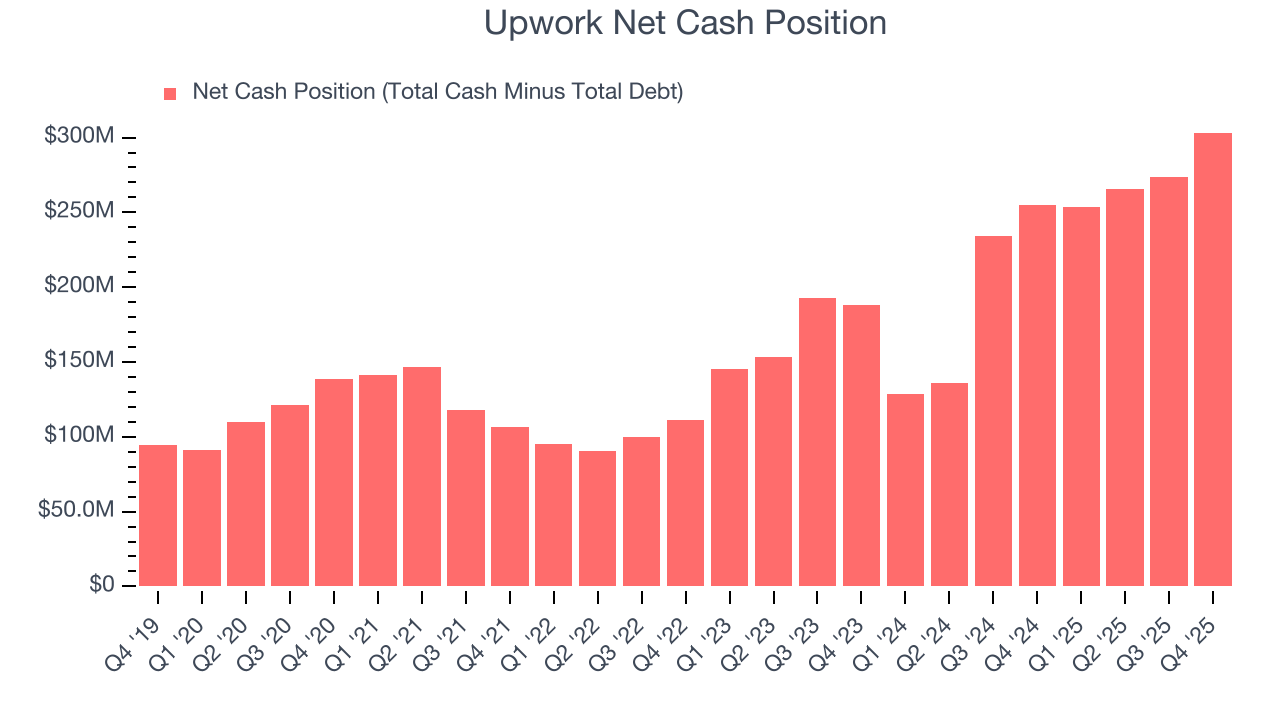

12. Balance Sheet Assessment

Businesses that maintain a cash surplus face reduced bankruptcy risk.

Upwork is a profitable, well-capitalized company with $672.8 million of cash and $369.5 million of debt on its balance sheet. This $303.3 million net cash position is 15.3% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

13. Key Takeaways from Upwork’s Q4 Results

It was encouraging to see Upwork beat analysts’ EBITDA expectations this quarter. We were also glad its full-year EBITDA guidance slightly exceeded Wall Street’s estimates. On the other hand, its number of customers declined and its revenue guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock remained flat at $15.22 immediately following the results.

14. Is Now The Time To Buy Upwork?

Updated: March 29, 2026 at 10:21 PM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Upwork, you should also grasp the company’s longer-term business quality and valuation.

In our opinion, Upwork is a solid company. Although its revenue growth was mediocre over the last three years and analysts expect growth to slow over the next 12 months, its powerful free cash flow generation enables it to stay ahead of the competition through consistent reinvestment of profits. And while its active customers have declined, its impressive EBITDA margins show it has a highly efficient business model.

Upwork’s EV/EBITDA ratio based on the next 12 months is 5.2x. Looking at the consumer internet landscape right now, Upwork trades at a pretty interesting price. If you trust the business and its direction, this is an ideal time to buy.

Wall Street analysts have a consensus one-year price target of $21.70 on the company (compared to the current share price of $11.00), implying they see 97.3% upside in buying Upwork in the short term.