United Therapeutics (UTHR)

We like United Therapeutics. Its high free cash flow margin and returns on capital show it can produce cash and invest it wisely.― StockStory Analyst Team

1. News

2. Summary

Why We Like United Therapeutics

Founded by a mother seeking treatment for her daughter's pulmonary arterial hypertension, United Therapeutics (NASDAQ:UTHR) develops and commercializes medications for chronic lung diseases and other life-threatening conditions, with a focus on pulmonary hypertension treatments.

- Healthy adjusted operating margin shows it’s a well-run company with efficient processes

- Powerful free cash flow generation enables it to reinvest its profits or return capital to investors consistently, and its improved cash conversion implies it’s becoming a less capital-intensive business

- Industry-leading 26.8% return on capital demonstrates management’s skill in finding high-return investments, and its rising returns show it’s making even more lucrative bets

We have an affinity for United Therapeutics. The valuation looks reasonable in light of its quality, so this might be a prudent time to buy some shares.

Why Is Now The Time To Buy United Therapeutics?

United Therapeutics is trading at $533.14 per share, or 19.2x forward P/E. Scanning the healthcare landscape, we think this multiple is reasonable - arguably even attractive - for the quality you get.

Where you buy a stock impacts returns. Our analysis shows that business quality is a much bigger determinant of market outperformance over the long term compared to entry price, but getting a good deal on a stock certainly isn’t a bad thing.

3. United Therapeutics (UTHR) Research Report: Q4 CY2025 Update

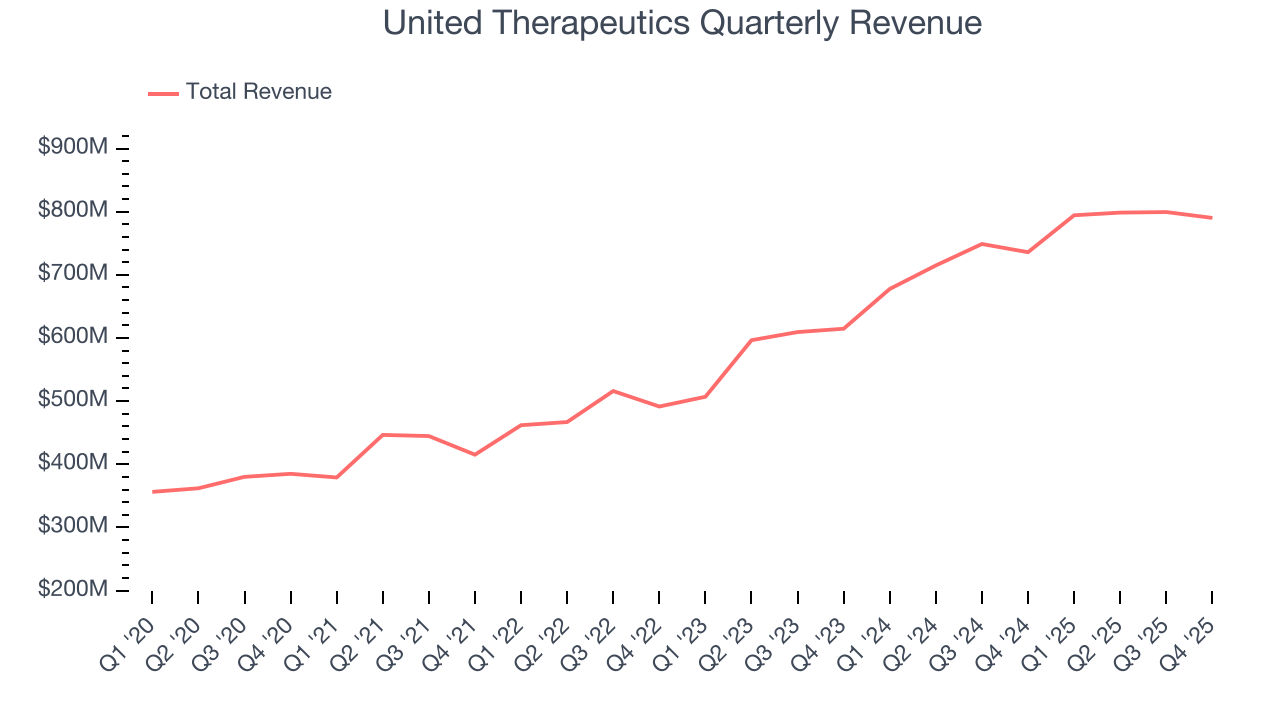

Biotechnology company United Therapeutics (NASDAQ:UTHR) missed Wall Street’s revenue expectations in Q4 CY2025, but sales rose 7.4% year on year to $790.2 million. Its GAAP profit of $7.70 per share was 14% above analysts’ consensus estimates.

United Therapeutics (UTHR) Q4 CY2025 Highlights:

- Revenue: $790.2 million vs analyst estimates of $810.4 million (7.4% year-on-year growth, 2.5% miss)

- EPS (GAAP): $7.70 vs analyst estimates of $6.76 (14% beat)

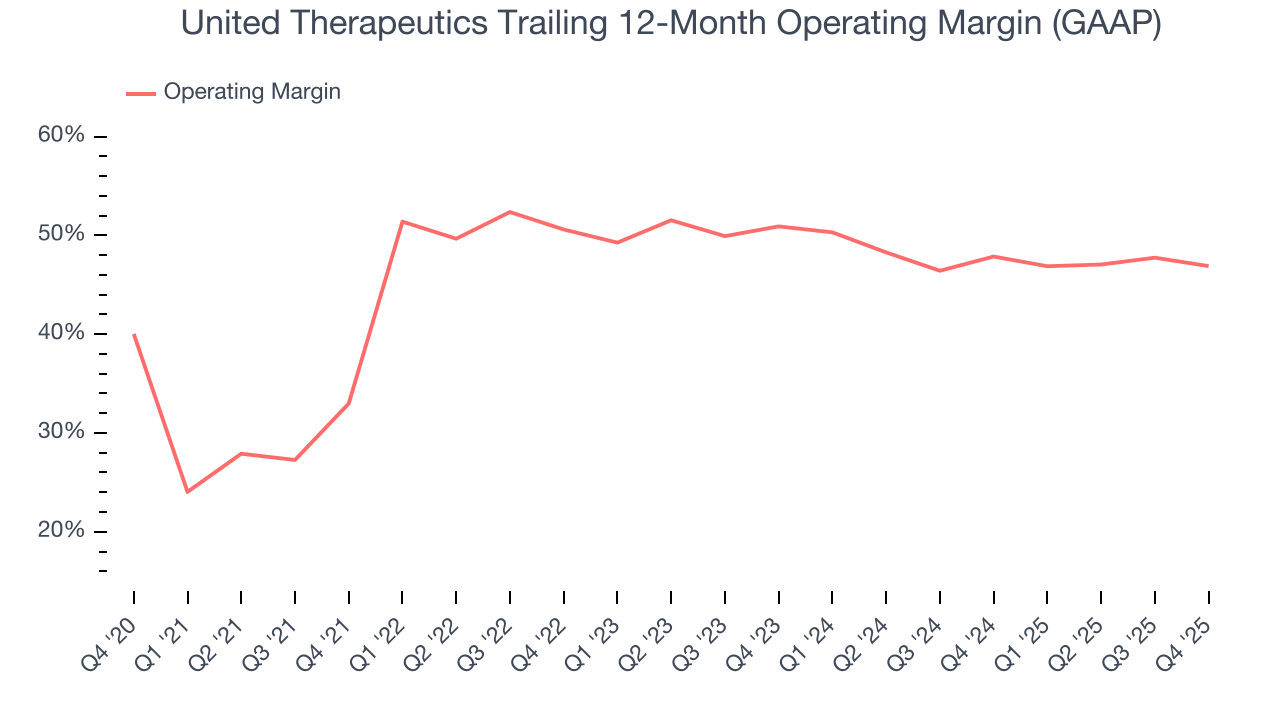

- Operating Margin: 45.1%, down from 48.6% in the same quarter last year

- Market Capitalization: $20.38 billion

Company Overview

Founded by a mother seeking treatment for her daughter's pulmonary arterial hypertension, United Therapeutics (NASDAQ:UTHR) develops and commercializes medications for chronic lung diseases and other life-threatening conditions, with a focus on pulmonary hypertension treatments.

United Therapeutics' product portfolio centers around treprostinil, a compound delivered in multiple formulations to treat pulmonary arterial hypertension (PAH) and pulmonary hypertension associated with interstitial lung disease (PH-ILD). The company's flagship products include Tyvaso DPI (an inhalable powder), nebulized Tyvaso (an inhalation solution), Remodulin (an injectable form), and Orenitram (an oral tablet). These medications help patients with these serious conditions improve exercise capacity and delay disease progression.

Patients with PAH and PH-ILD experience high blood pressure in the arteries of their lungs, making it difficult for the heart to pump blood through the lungs. This leads to symptoms like shortness of breath, fatigue, and can eventually lead to heart failure. United Therapeutics' medications work by mimicking the effects of prostacyclin, a naturally occurring substance that dilates blood vessels and prevents platelets from clumping together.

Beyond pulmonary hypertension treatments, the company markets Unituxin, an antibody therapy for high-risk neuroblastoma, a rare pediatric cancer. This treatment works by helping the patient's immune system target and attack cancer cells.

United Therapeutics is also pioneering organ manufacturing technologies through several innovative approaches. Its xenotransplantation program aims to develop genetically modified pig organs for human transplantation. The company is working on bioartificial organs using 3D printing technology and decellularized organ scaffolds repopulated with human cells. Additionally, it operates the only commercially available centralized ex vivo lung perfusion service in the U.S., which helps increase the supply of transplantable lungs.

The company sells its products primarily through specialty pharmaceutical distributors in the United States and partners with various distributors internationally. United Therapeutics invests heavily in research and development, with clinical trials exploring new indications for existing products and developing novel therapies for unmet medical needs.

4. Therapeutics

Over the next few years, therapeutic companies, which develop a wide variety of treatments for diseases and disorders, face strong tailwinds from advancements in precision medicine (including the use of AI to improve hit rates) and growing demand for treatments targeting rare diseases. However, headwinds such as rising scrutiny over drug pricing, regulatory unknowns, and competition from larger, more resourced pharmaceutical companies could weigh on growth.

United Therapeutics' competitors in the pulmonary hypertension treatment space include Johnson & Johnson (NYSE:JNJ), which markets Uptravi and Opsumit, Merck (NYSE:MRK) with Adempas, and Pfizer (NYSE:PFE) with Revatio. In the organ manufacturing field, competitors include Revivicor (a subsidiary of United Therapeutics), eGenesis, and Recombinetics.

5. Economies of Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $3.18 billion in revenue over the past 12 months, United Therapeutics has decent scale. This is important as it gives the company more leverage in a heavily regulated, competitive environment that is complex and resource-intensive.

6. Revenue Growth

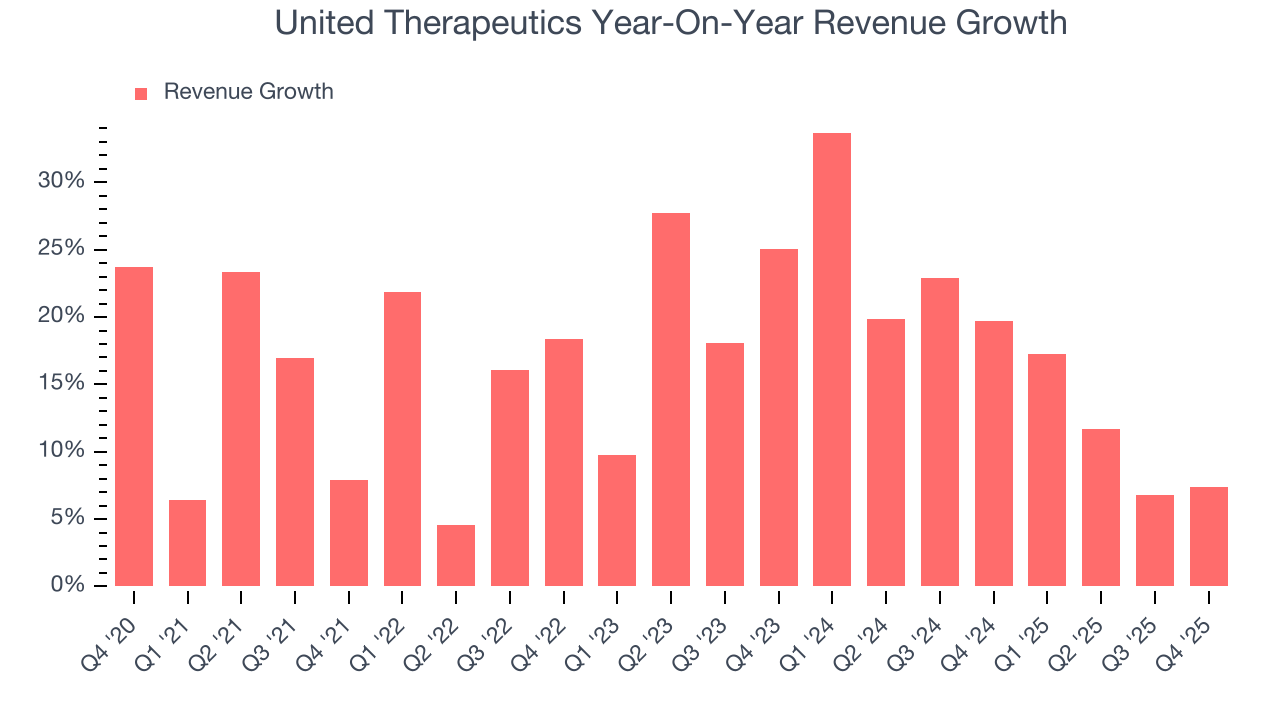

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, United Therapeutics grew its sales at a solid 16.5% compounded annual growth rate. Its growth surpassed the average healthcare company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. United Therapeutics’s annualized revenue growth of 16.9% over the last two years aligns with its five-year trend, suggesting its demand was predictably strong.

This quarter, United Therapeutics’s revenue grew by 7.4% year on year to $790.2 million, missing Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

7. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

United Therapeutics has been a well-oiled machine over the last five years. It demonstrated elite profitability for a healthcare business, boasting an average operating margin of 46.5%.

Looking at the trend in its profitability, United Therapeutics’s operating margin rose by 13.9 percentage points over the last five years, as its sales growth gave it operating leverage. Zooming into its more recent performance, however, we can see the company’s margin has decreased by 4 percentage points on a two-year basis. Given its business quality, we’re optimistic that United Therapeutics can correct course and return to expansion.

This quarter, United Therapeutics generated an operating margin profit margin of 45.1%, down 3.5 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

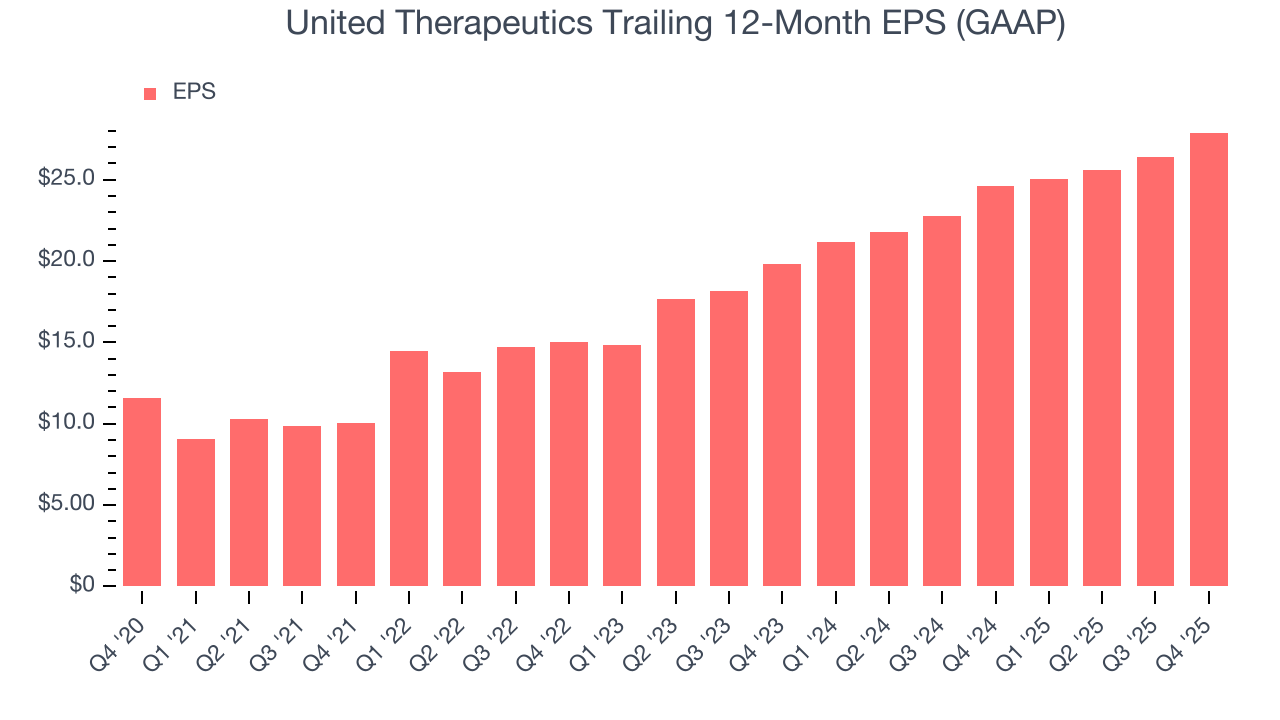

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

United Therapeutics’s EPS grew at an astounding 19.3% compounded annual growth rate over the last five years, higher than its 16.5% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Diving into United Therapeutics’s quality of earnings can give us a better understanding of its performance. As we mentioned earlier, United Therapeutics’s operating margin declined this quarter but expanded by 13.9 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, United Therapeutics reported EPS of $7.70, up from $6.19 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects United Therapeutics’s full-year EPS of $27.90 to grow 3.7%.

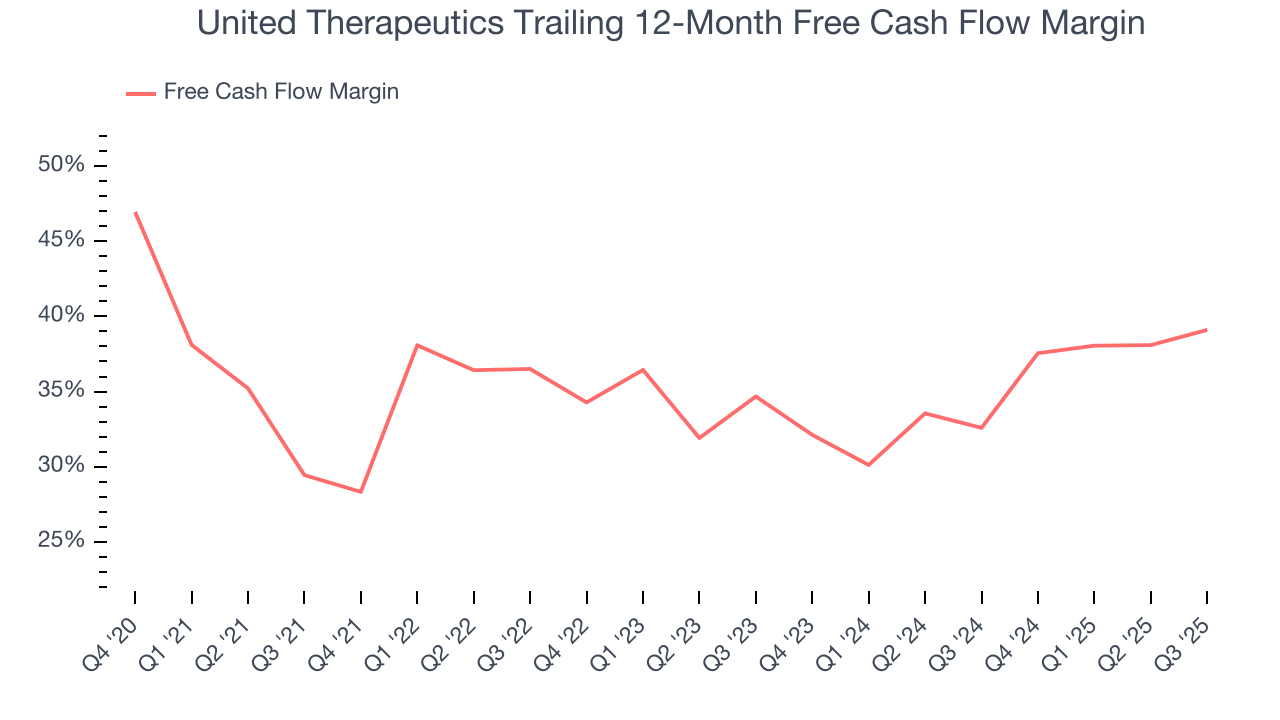

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

United Therapeutics has shown terrific cash profitability, enabling it to reinvest, return capital to investors, and stay ahead of the competition while maintaining an ample cushion. The company’s free cash flow margin was among the best in the healthcare sector, averaging an eye-popping 35.1% over the last five years.

Taking a step back, we can see that United Therapeutics’s margin expanded by 11.1 percentage points during that time. This is encouraging because it gives the company more optionality.

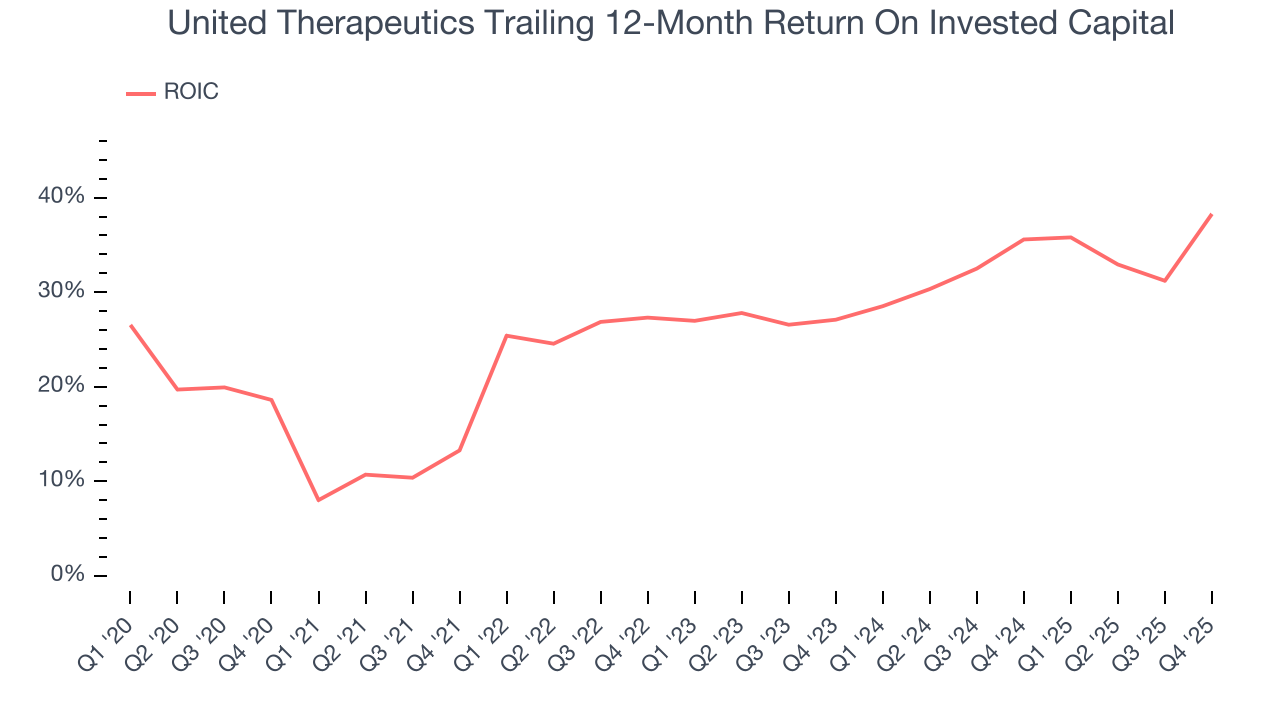

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

United Therapeutics’s five-year average ROIC was 28.3%, placing it among the best healthcare companies. This illustrates its management team’s ability to invest in highly profitable ventures and produce tangible results for shareholders.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, United Therapeutics’s ROIC has increased significantly. This is a great sign when paired with its already strong returns. It could suggest its competitive advantage or profitable growth opportunities are expanding.

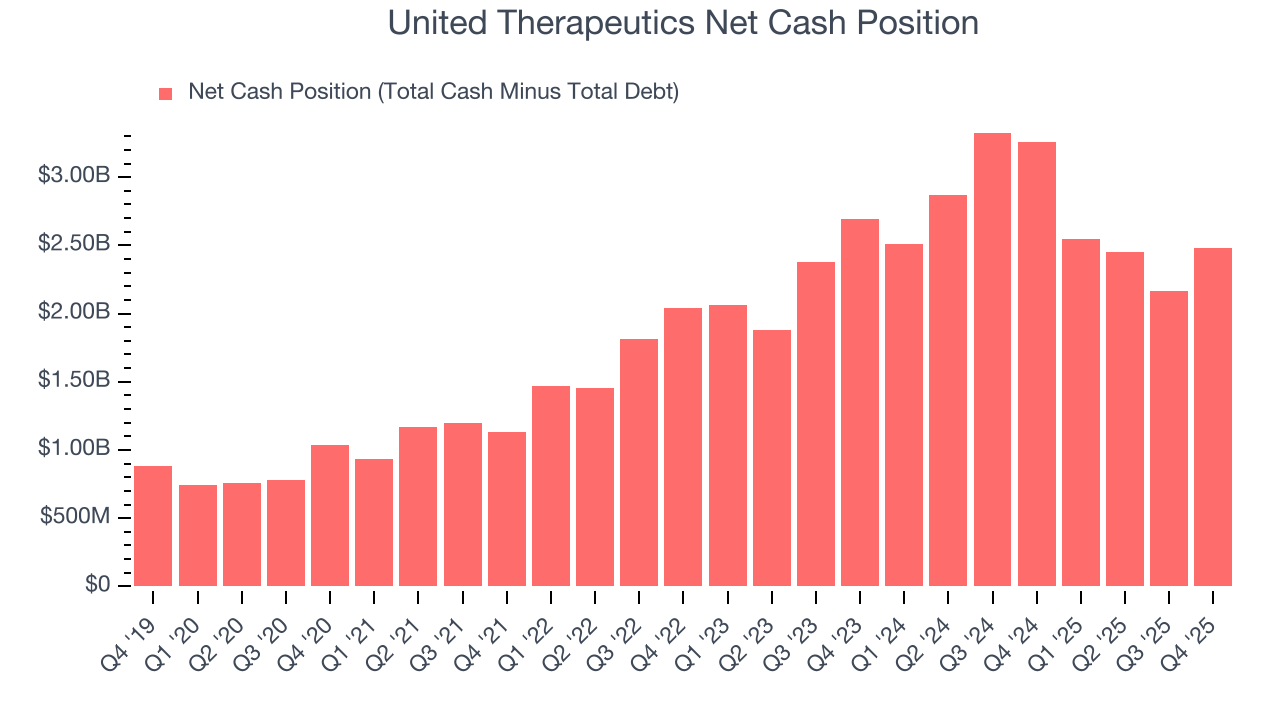

11. Balance Sheet Assessment

Companies with more cash than debt have lower bankruptcy risk.

United Therapeutics is a profitable, well-capitalized company with $3.08 billion of cash and $600 million of debt on its balance sheet. This $2.48 billion net cash position is 10.8% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from United Therapeutics’s Q4 Results

It was good to see United Therapeutics beat analysts’ EPS expectations this quarter. On the other hand, its revenue missed. Overall, this was a softer quarter. The stock traded down 3.9% to $454.81 immediately following the results.

13. Is Now The Time To Buy United Therapeutics?

Updated: March 14, 2026 at 11:46 PM EDT

Are you wondering whether to buy United Therapeutics or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

There are multiple reasons why we think United Therapeutics is an amazing business. For starters, its revenue growth was solid over the last five years. On top of that, its powerful free cash flow generation enables it to stay ahead of the competition through consistent reinvestment of profits, and its impressive operating margins show it has a highly efficient business model.

United Therapeutics’s P/E ratio based on the next 12 months is 19.2x. Looking across the spectrum of healthcare companies today, United Therapeutics’s fundamentals shine bright. We like the stock at this price.

Wall Street analysts have a consensus one-year price target of $592.25 on the company (compared to the current share price of $533.14), implying they see 11.1% upside in buying United Therapeutics in the short term.