Wix (WIX)

We’re wary of Wix. Its weak revenue growth and gross margin show it not only lacks demand but also decent unit economics.― StockStory Analyst Team

1. News

2. Summary

Why We Think Wix Will Underperform

Powering over 263 million registered users worldwide with its AI-driven tools, Wix (NASDAQ:WIX) provides a cloud-based platform that helps individuals and businesses create and manage professional websites without requiring coding skills.

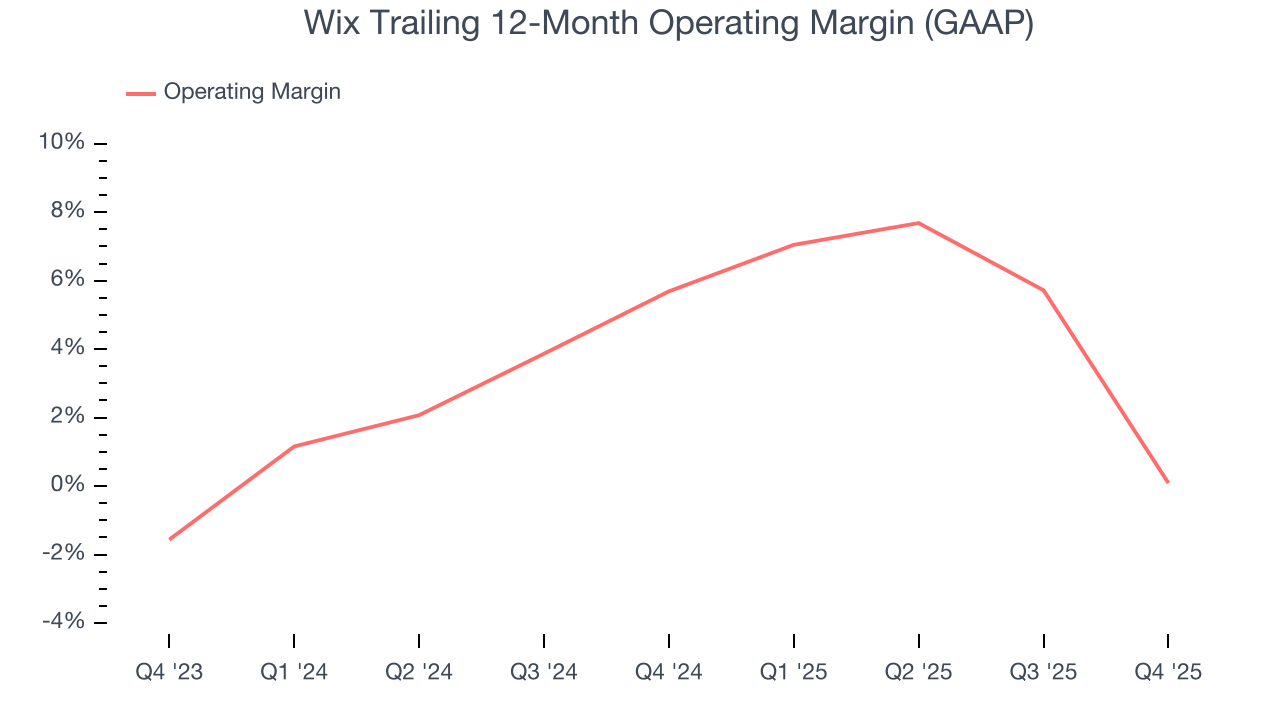

- Efficiency has decreased over the last year as its operating margin fell by 5.6 percentage points

- Gross margin of 68.1% is below its competitors, leaving less money to invest in areas like marketing and R&D

- On the bright side, its powerful free cash flow generation enables it to reinvest its profits or return capital to investors consistently

Wix’s quality isn’t up to par. We see more attractive opportunities in the market.

Why There Are Better Opportunities Than Wix

At $87.90 per share, Wix trades at 2.1x forward price-to-sales. This sure is a cheap multiple, but you get what you pay for.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Wix (WIX) Research Report: Q4 CY2025 Update

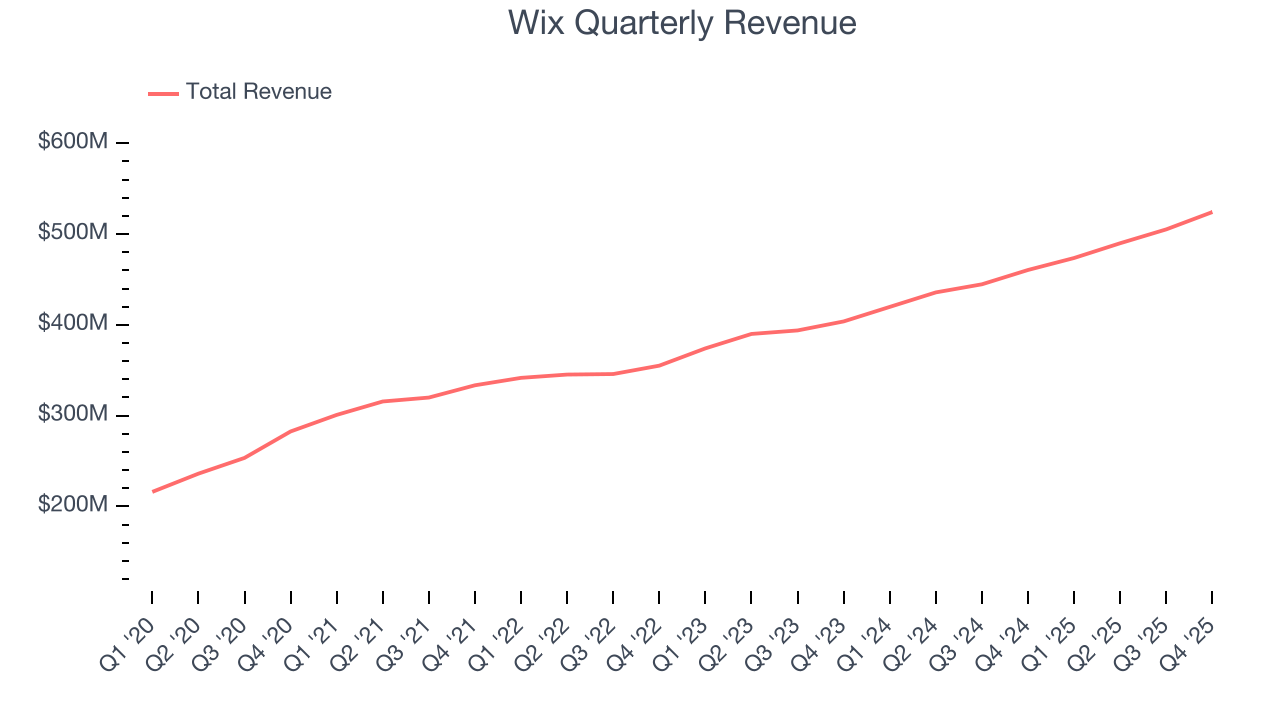

Website building platform Wix (NASDAQ:WIX) met Wall Street’s revenue expectations in Q4 CY2025, with sales up 13.9% year on year to $524.3 million. Its non-GAAP profit of $1.81 per share was 23% above analysts’ consensus estimates.

Wix (WIX) Q4 CY2025 Highlights:

- Revenue: $524.3 million vs analyst estimates of $526.9 million (13.9% year-on-year growth, in line)

- Adjusted EPS: $1.81 vs analyst estimates of $1.47 (23% beat)

- Adjusted Operating Income: $81.18 million vs analyst estimates of $76.52 million (15.5% margin, 6.1% beat)

- Operating Margin: -13.8%, down from 7.8% in the same quarter last year

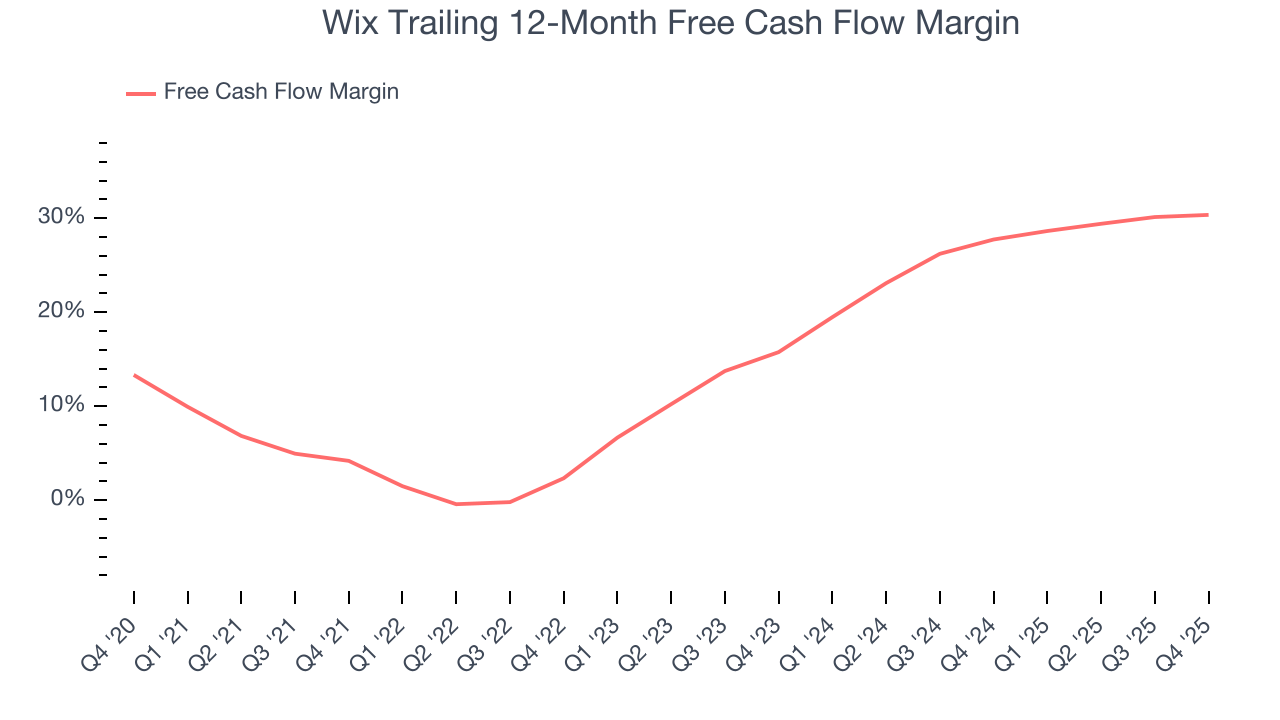

- Free Cash Flow Margin: 29.7%, down from 31.6% in the previous quarter

- Annual Recurring Revenue: $1.84 billion (36.7% year-on-year growth)

- Billings: $539.3 million at quarter end, up 16.1% year on year

- Market Capitalization: $4.07 billion

Company Overview

Powering over 263 million registered users worldwide with its AI-driven tools, Wix (NASDAQ:WIX) provides a cloud-based platform that helps individuals and businesses create and manage professional websites without requiring coding skills.

The Wix platform offers two main website creation products: Wix Editor for users with basic to average technical skills, and Wix Studio for professionals and agencies. Both leverage an extensive suite of AI-powered tools, including an AI Website Builder that generates complete websites through conversational prompts, AI text and image generators, and specialized design assistants.

Beyond website creation, Wix provides comprehensive business solutions tailored to specific industries. These include Wix Stores for e-commerce, Wix Bookings for appointment scheduling, Wix Restaurants for food establishments, and specialized applications for events, fitness, hotels, and creative professionals. The company also offers Velo by Wix, a development environment that enables users to extend website functionality without extensive coding knowledge.

Wix operates on a freemium business model. Its free tier provides access to website creation tools with Wix branding and domain restrictions, while premium subscriptions remove these limitations and unlock additional features. Revenue also comes from complementary services such as Payments by Wix (payment processing), domain registration, email marketing, and business app solutions.

The company's cloud infrastructure handles hosting, security, and scalability concerns, allowing users to focus on content and design rather than technical maintenance. This approach has made Wix particularly popular among small businesses, freelancers, and organizations seeking a professional online presence without significant technical investment or ongoing development costs.

4. E-commerce Software

While e-commerce has been around for over two decades and enjoyed meaningful growth, its overall penetration of retail still remains low. Only around $1 in every $5 spent on retail purchases comes from digital orders, leaving over 80% of the retail market still ripe for online disruption. It is these large swathes of the retail where e-commerce has not yet taken hold that drives the demand for various e-commerce software solutions.

Wix competes with other website building platforms like Squarespace (NYSE:SQSP), Shopify (NYSE:SHOP) for e-commerce, WordPress.com by Automattic (private), GoDaddy (NYSE:GDDY), and Webflow (private).

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Wix grew its sales at a 15.1% compounded annual growth rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the software sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. Wix’s recent performance shows its demand has slowed as its annualized revenue growth of 13% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, Wix’s year-on-year revenue growth was 13.9%, and its $524.3 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 13.8% over the next 12 months, similar to its two-year rate. This projection is underwhelming and suggests its newer products and services will not catalyze better top-line performance yet.

6. Annual Recurring Revenue

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Wix’s ARR punched in at $1.84 billion in Q4, and over the last four quarters, its growth was solid as it averaged 17.2% year-on-year increases. This alternate topline metric grew faster than total sales, which likely means that the recurring portions of the business are growing faster than less predictable, choppier ones such as implementation fees. That could be a good sign for future revenue growth.

7. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Wix is quite efficient at acquiring new customers, and its CAC payback period checked in at 32.6 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a strong brand reputation, giving it more resources pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

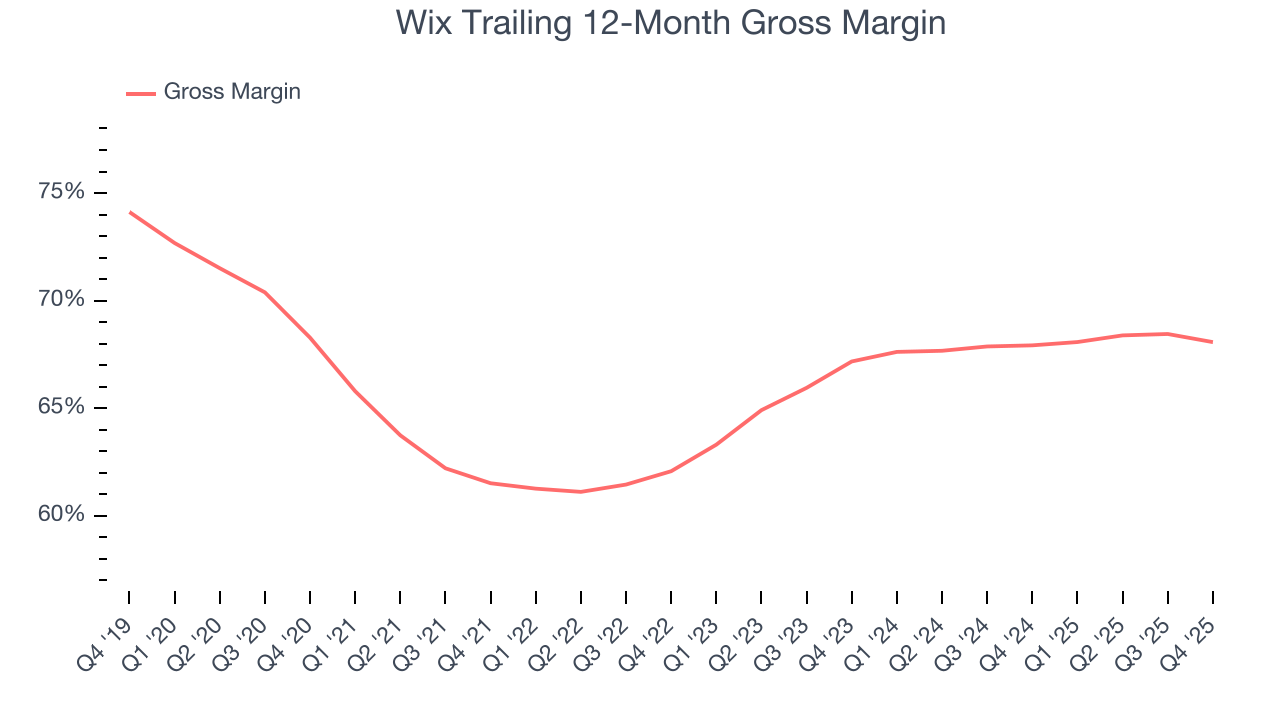

8. Gross Margin & Pricing Power

For software companies like Wix, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Wix’s gross margin is worse than the software industry average, giving it less room than its competitors to hire new talent that can expand its products and services. As you can see below, it averaged a 68.1% gross margin over the last year. Said differently, Wix had to pay a chunky $31.92 to its service providers for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Wix has seen gross margins improve by 0.9 percentage points over the last 2 year, which is slightly better than average for software.

Wix’s gross profit margin came in at 67.3% this quarter , marking a 1.5 percentage point decrease from 68.8% in the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

9. Operating Margin

While many software businesses point investors to their adjusted profits, which exclude stock-based compensation (SBC), we prefer GAAP operating margin because SBC is a legitimate expense used to attract and retain talent. This metric shows how much revenue remains after accounting for all core expenses – everything from the cost of goods sold to sales and R&D.

Wix was roughly breakeven when averaging the last year of quarterly operating profits, decent for a software business.

Analyzing the trend in its profitability, Wix’s operating margin decreased by 5.6 percentage points over the last two years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, Wix generated an operating margin profit margin of negative 13.8%, down 21.7 percentage points year on year. Since Wix’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

10. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Wix has shown robust cash profitability, driven by its cost-effective customer acquisition strategy that enables it to invest in new products and services rather than sales and marketing. The company’s free cash flow margin averaged an eye-popping 30.4% over the last year, quite impressive for a software business. Wix has shown robust cash profitability relative to peers over the last year, giving the company fewer opportunities to return capital to shareholders.

Wix’s free cash flow clocked in at $155.6 million in Q4, equivalent to a 29.7% margin. This result was good as its margin was 1.1 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends trump fluctuations.

Over the next year, analysts predict Wix’s cash conversion will fall. Their consensus estimates imply its free cash flow margin of 30.4% for the last 12 months will decrease to 26.3%.

11. Balance Sheet Assessment

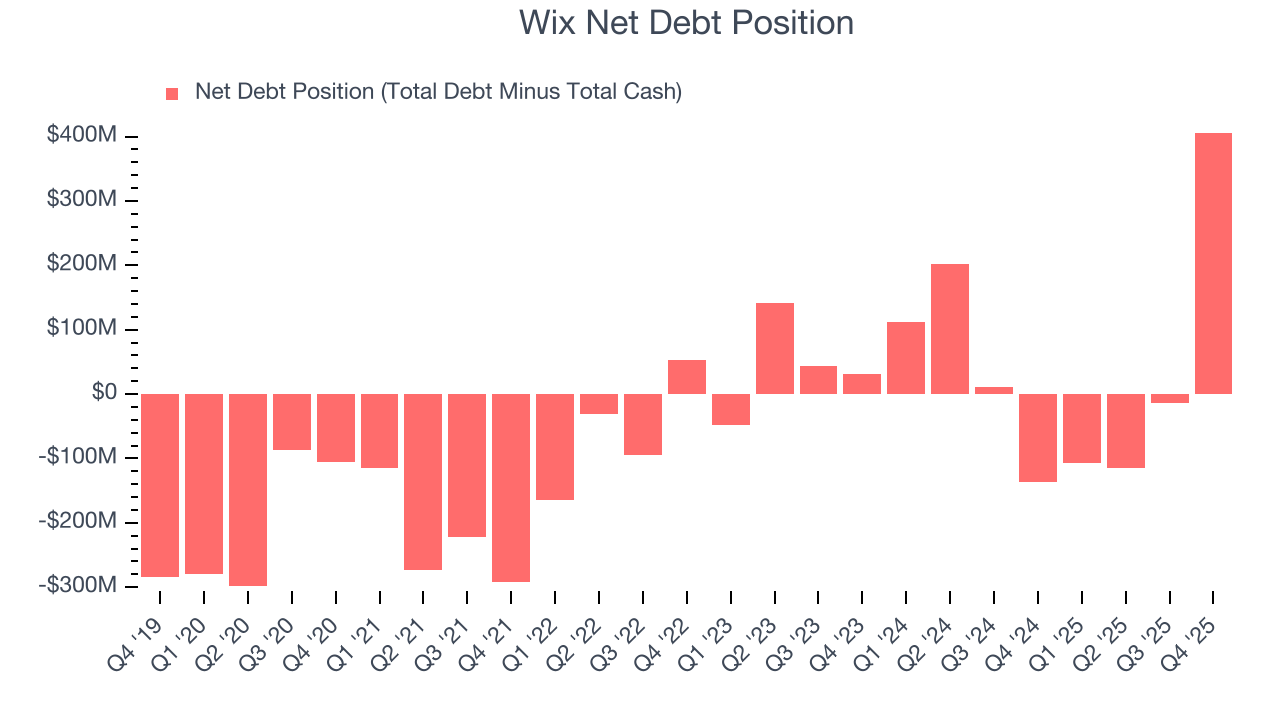

Wix reported $1.18 billion of cash and $1.59 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $405.6 million of EBITDA over the last 12 months, we view Wix’s 1.0× net-debt-to-EBITDA ratio as safe. We also see its $14.2 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Wix’s Q4 Results

It was good to see Wix narrowly top analysts’ billings expectations this quarter. Additionally, adjusted operating income beat quite convincingly. Overall, this was a solid quarter. The stock traded up 4.6% to $77.75 immediately following the results.

13. Is Now The Time To Buy Wix?

Updated: March 15, 2026 at 10:15 PM EDT

Before investing in or passing on Wix, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

Wix’s business quality ultimately falls short of our standards. For starters, its revenue growth was a little slower over the last five years, and analysts don’t see anything changing over the next 12 months. While its bountiful generation of free cash flow empowers it to invest in growth initiatives, the downside is its declining operating margin shows it’s becoming less efficient at building and selling its software. On top of that, its gross margin is below our standards.

Wix’s price-to-sales ratio based on the next 12 months is 2.1x. This valuation multiple is fair, but we don’t have much faith in the company. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $123.95 on the company (compared to the current share price of $87.90).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.