Dentsply Sirona (XRAY)

Dentsply Sirona is up against the odds. Not only has its sales growth been weak but also its negative returns on capital show it destroyed value.― StockStory Analyst Team

1. News

2. Summary

Why We Think Dentsply Sirona Will Underperform

With roots dating back to 1877 when it introduced the first dental electric drill, Dentsply Sirona (NASDAQ:XRAY) manufactures and sells professional dental equipment, technologies, and consumable products used by dentists and specialists worldwide.

- Negative returns on capital show that some of its growth strategies have backfired, and its falling returns suggest its earlier profit pools are drying up

- Sales tumbled by 4% annually over the last two years, showing market trends are working against its favor during this cycle

- Earnings per share were flat over the last five years while its revenue grew, showing its incremental sales were less profitable

Dentsply Sirona doesn’t fulfill our quality requirements. There are superior opportunities elsewhere.

Why There Are Better Opportunities Than Dentsply Sirona

Dentsply Sirona’s stock price of $12.27 implies a valuation ratio of 8.2x forward P/E. This certainly seems like a cheap stock, but we think there are valid reasons why it trades this way.

Cheap stocks can look like a great deal at first glance, but they can be value traps. They often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Dentsply Sirona (XRAY) Research Report: Q3 CY2025 Update

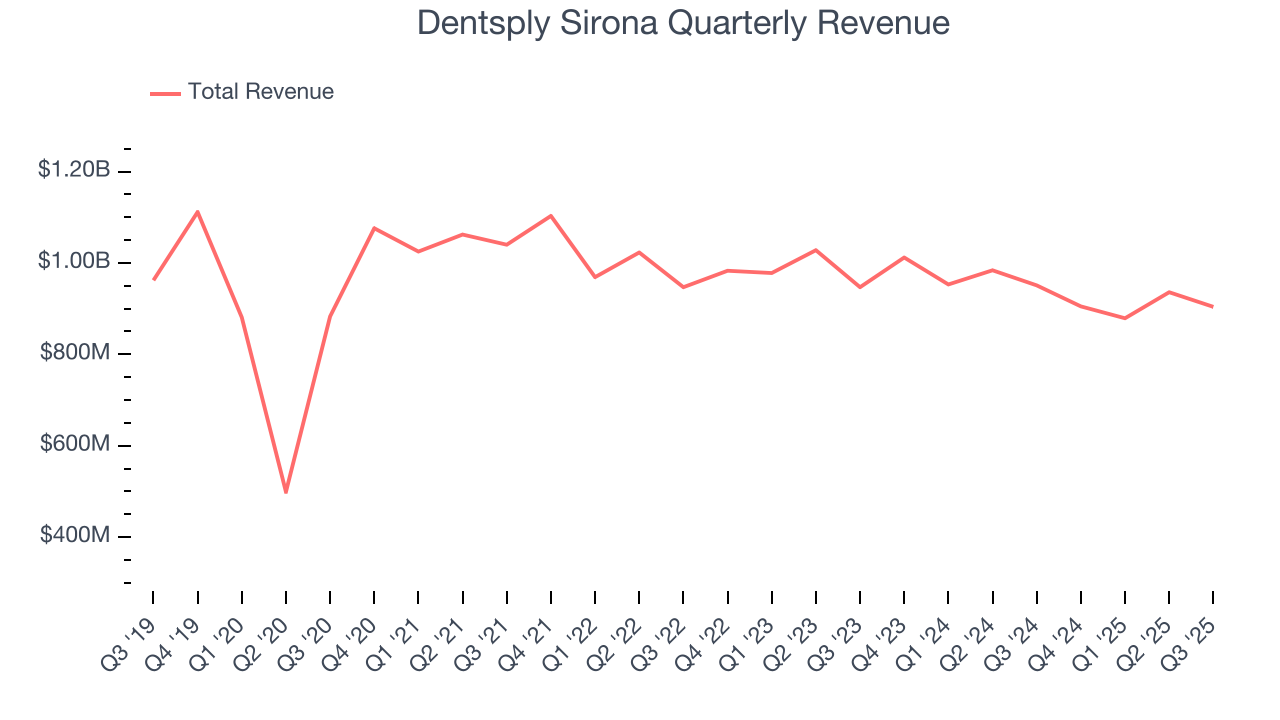

Dental products company Dentsply Sirona (NASDAQ:XRAY) beat Wall Street’s revenue expectations in Q3 CY2025, but sales fell by 4.9% year on year to $904 million. The company expects the full year’s revenue to be around $3.65 billion, close to analysts’ estimates. Its non-GAAP profit of $0.37 per share was 17.7% below analysts’ consensus estimates.

Dentsply Sirona (XRAY) Q3 CY2025 Highlights:

- Revenue: $904 million vs analyst estimates of $899.5 million (4.9% year-on-year decline, 0.5% beat)

- Adjusted EPS: $0.37 vs analyst expectations of $0.45 (17.7% miss)

- Adjusted EBITDA: $167 million vs analyst estimates of $171.1 million (18.5% margin, 2.4% miss)

- The company reconfirmed its revenue guidance for the full year of $3.65 billion at the midpoint

- Management lowered its full-year Adjusted EPS guidance to $1.60 at the midpoint, a 15.8% decrease

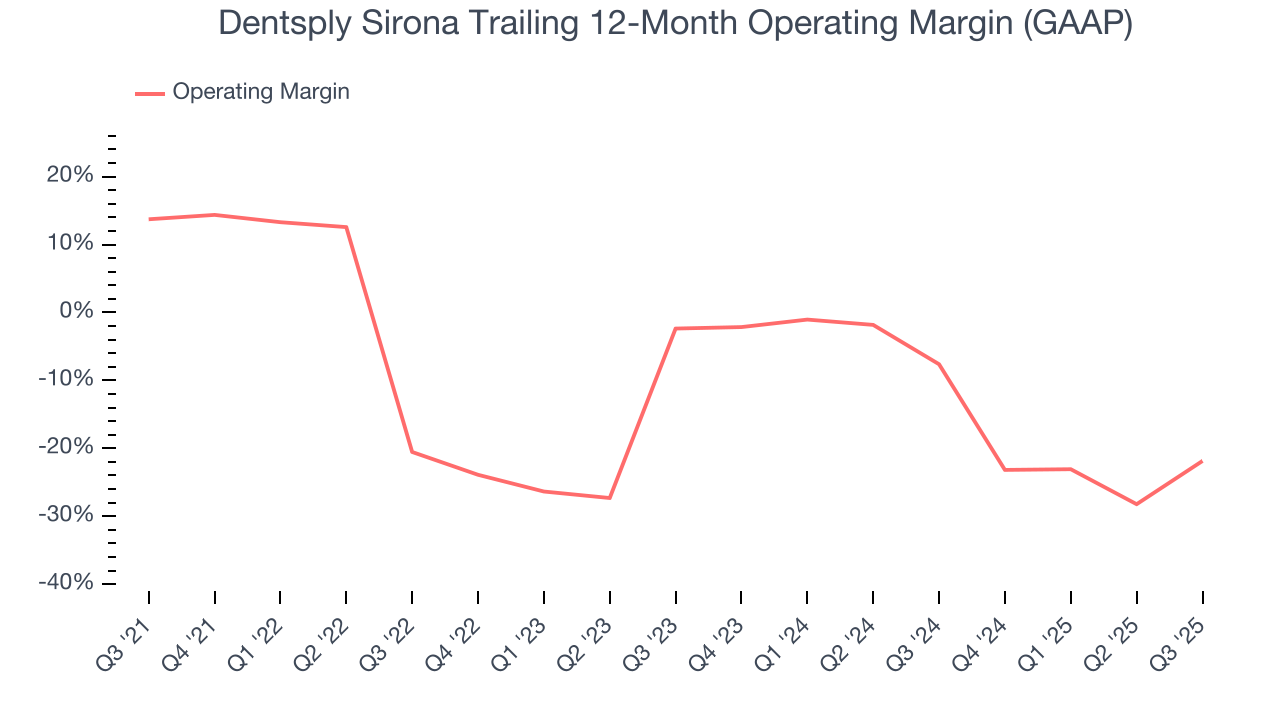

- Operating Margin: -24.1%, up from -48.6% in the same quarter last year

- Free Cash Flow Margin: 4.4%, down from 10.3% in the same quarter last year

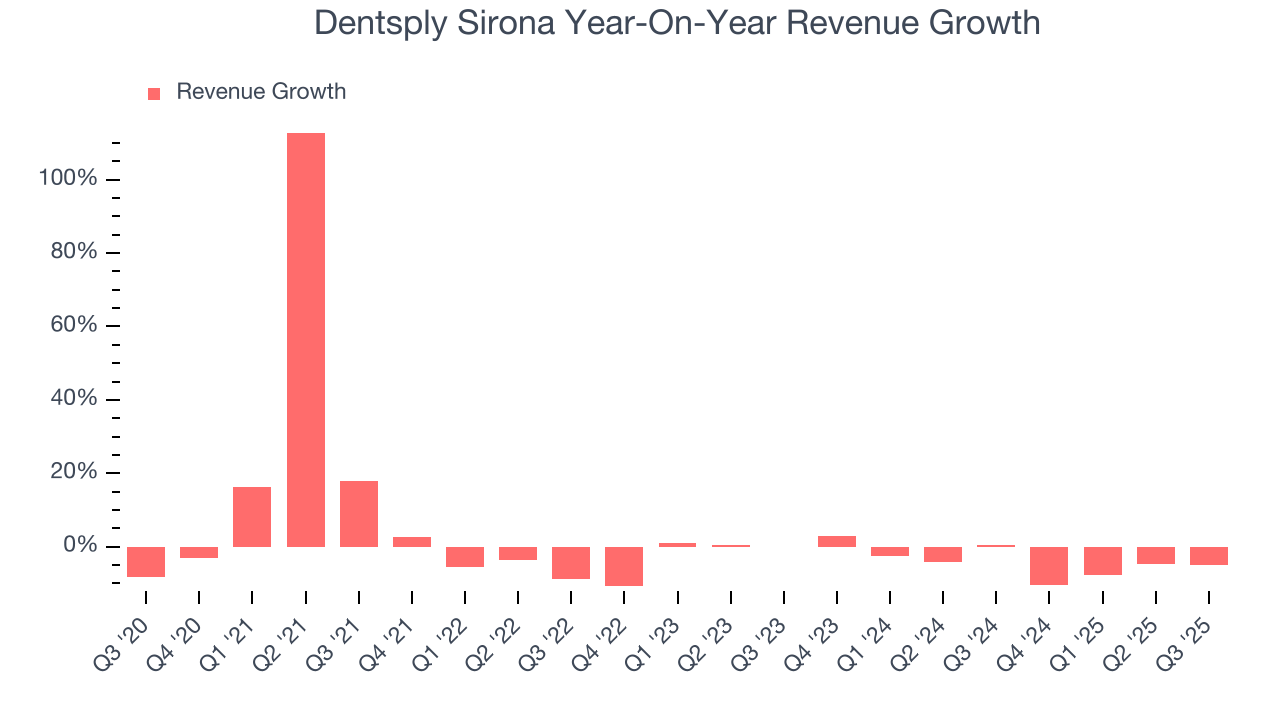

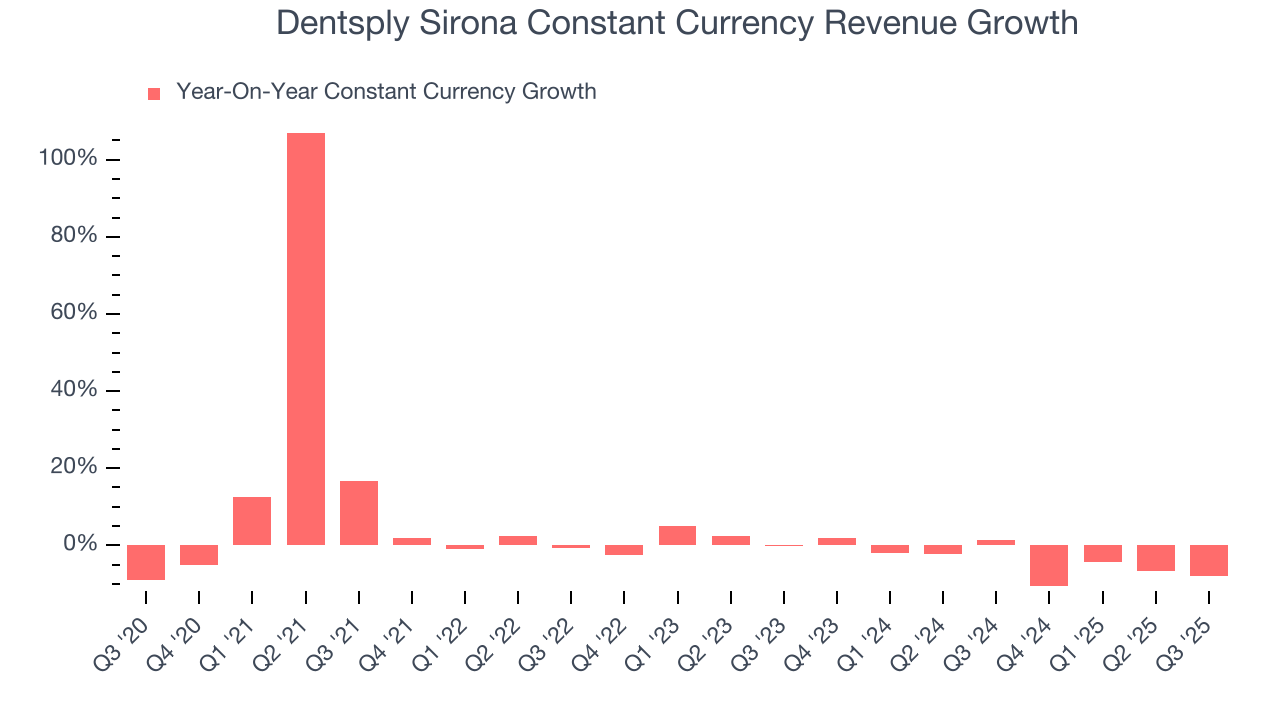

- Constant Currency Revenue fell 8% year on year (1.3% in the same quarter last year)

- Market Capitalization: $2.52 billion

Company Overview

With roots dating back to 1877 when it introduced the first dental electric drill, Dentsply Sirona (NASDAQ:XRAY) manufactures and sells professional dental equipment, technologies, and consumable products used by dentists and specialists worldwide.

Dentsply Sirona operates through four main business segments that together form a comprehensive dental solutions ecosystem. The Connected Technology Solutions segment provides the digital backbone of modern dentistry, offering imaging equipment, treatment centers, and CAD/CAM technologies that enable same-day dental restorations. Their cloud-based platform, DS Core, connects these technologies to streamline workflows for dental practices.

The Essential Dental Solutions segment focuses on consumable products and small equipment used in everyday dental procedures. This includes endodontic tools for root canal treatments, restorative materials for prosthetic work, and preventive products like curing lights and ultrasonic scalers.

Through its Orthodontic and Implant Solutions segment, the company offers dental implant systems, digital dentures, and clear aligner solutions. This includes both professional-directed aligners (SureSmile) and direct-to-consumer aligners (Byte), giving dentists and patients multiple treatment options.

The Wellspect Healthcare segment extends beyond dentistry, providing continence care solutions for urinary and bowel management, primarily through catheters and related products.

Dentsply Sirona maintains a global presence, distributing products in over 150 countries through a combination of third-party distributors and direct sales. Major dental supply distributors Henry Schein and Patterson Companies represent significant distribution channels for the company.

The company invests heavily in clinical education, operating 57 academies and education centers across 35 countries. These facilities provide training for dental professionals on new techniques and technologies, helping to drive adoption of the company's products while building relationships with practitioners.

Research and development remains a priority, with recent innovations including the DS Core cloud platform, 3D printing solutions, and enhanced implant systems. The company's products must comply with strict medical device regulations in all markets where they operate, including FDA requirements in the US and MDR standards in Europe.

4. Dental Equipment & Technology

The dental equipment and technology industry encompasses companies that manufacture orthodontic products, dental implants, imaging systems, and digital tools for dental professionals. These companies benefit from recurring revenue streams tied to consumables, ongoing maintenance, and growing demand for aesthetic and restorative dentistry. However, high R&D costs, significant capital investment requirements, and reliance on discretionary spending make them vulnerable to economic cycles. Over the next few years, tailwinds for the sector include innovation in digital workflows, such as 3D printing and AI-driven diagnostics, which enhance the efficiency and precision of dental care. However, headwinds include economic uncertainty, which could reduce patient spending on elective procedures, regulatory challenges, and potential pricing pressures from consolidated dental service organizations (DSOs).

Dentsply Sirona's competitors include Align Technology (NASDAQ:ALGN) in the clear aligner space, Envista Holdings (NYSE:NVST) for dental equipment and consumables, and Straumann Holding (SWX:STMN) in the dental implant market. The company also competes with 3M (NYSE:MMM) and Henry Schein's (NASDAQ:HSIC) private label products in various dental categories.

5. Economies of Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $3.62 billion in revenue over the past 12 months, Dentsply Sirona has decent scale. This is important as it gives the company more leverage in a heavily regulated, competitive environment that is complex and resource-intensive.

6. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, Dentsply Sirona’s sales grew at a tepid 1.4% compounded annual growth rate over the last five years. This fell short of our benchmarks and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Dentsply Sirona’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 4% annually.

We can dig further into the company’s sales dynamics by analyzing its constant currency revenue, which excludes currency movements that are outside their control and not indicative of demand. Over the last two years, its constant currency sales averaged 3.9% year-on-year declines. Because this number aligns with its normal revenue growth, we can see that Dentsply Sirona has properly hedged its foreign currency exposure.

This quarter, Dentsply Sirona’s revenue fell by 4.9% year on year to $904 million but beat Wall Street’s estimates by 0.5%.

Looking ahead, sell-side analysts expect revenue to grow 2.4% over the next 12 months. Although this projection indicates its newer products and services will fuel better top-line performance, it is still below the sector average.

7. Operating Margin

Dentsply Sirona’s high expenses have contributed to an average operating margin of negative 7.3% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Looking at the trend in its profitability, Dentsply Sirona’s operating margin decreased by 35.6 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 19.5 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

In Q3, Dentsply Sirona generated a negative 24.1% operating margin. The company's consistent lack of profits raise a flag.

8. Earnings Per Share

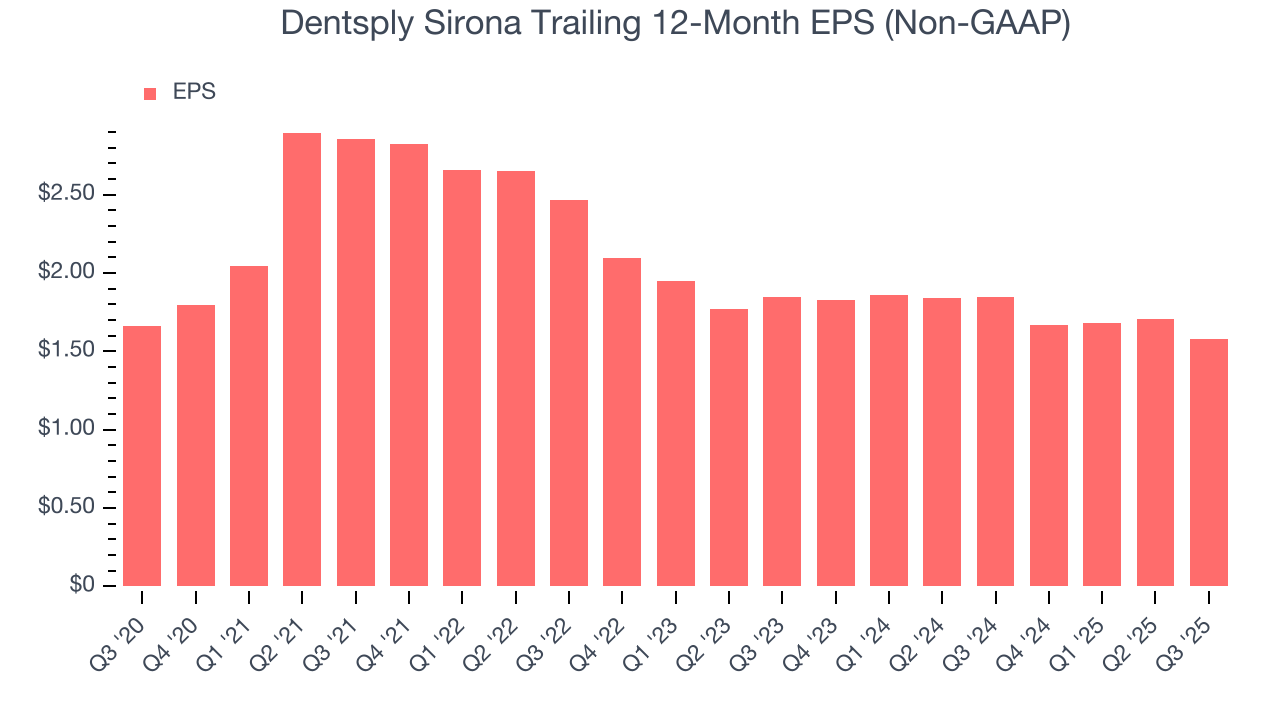

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Dentsply Sirona’s flat EPS over the last five years was below its 1.4% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

Diving into the nuances of Dentsply Sirona’s earnings can give us a better understanding of its performance. As we mentioned earlier, Dentsply Sirona’s operating margin expanded this quarter but declined by 35.6 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q3, Dentsply Sirona reported adjusted EPS of $0.37, down from $0.50 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Dentsply Sirona’s full-year EPS of $1.58 to grow 24.4%.

9. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

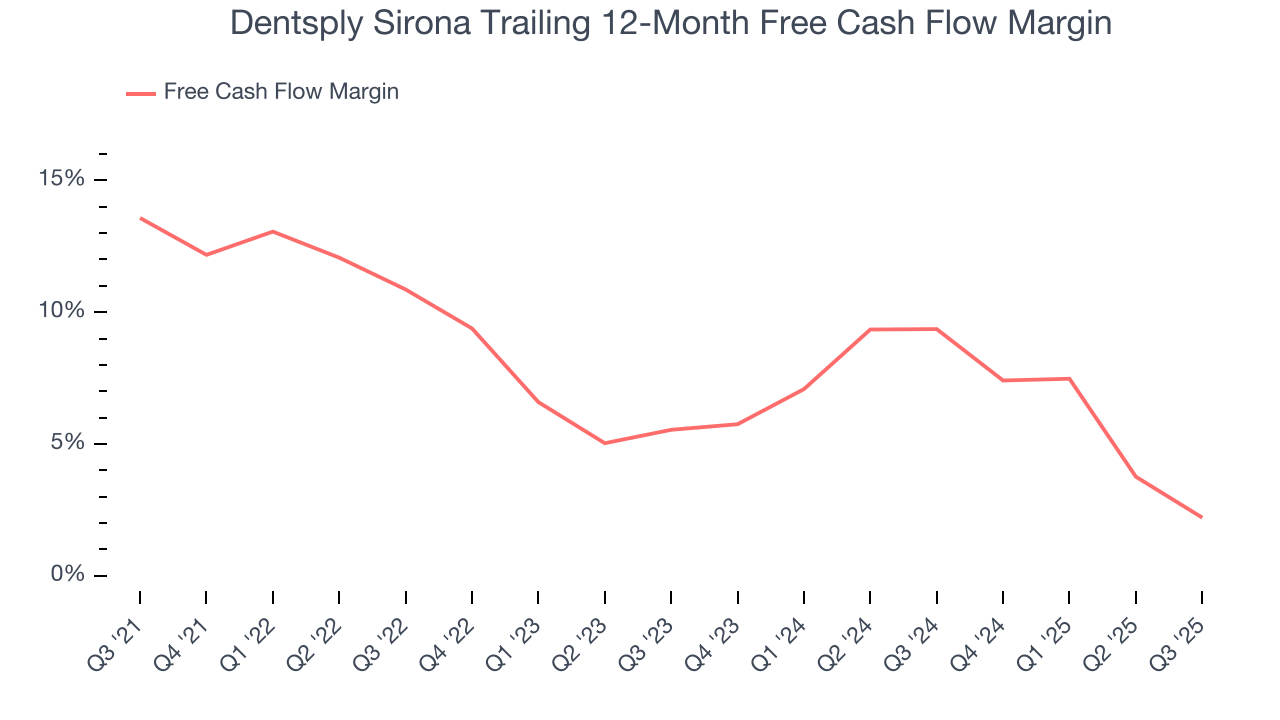

Dentsply Sirona has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 8.5% over the last five years, slightly better than the broader healthcare sector.

Taking a step back, we can see that Dentsply Sirona’s margin dropped by 11.4 percentage points during that time. Continued declines could signal it is in the middle of an investment cycle.

Dentsply Sirona’s free cash flow clocked in at $40 million in Q3, equivalent to a 4.4% margin. The company’s cash profitability regressed as it was 5.9 percentage points lower than in the same quarter last year, suggesting its historical struggles have dragged on.

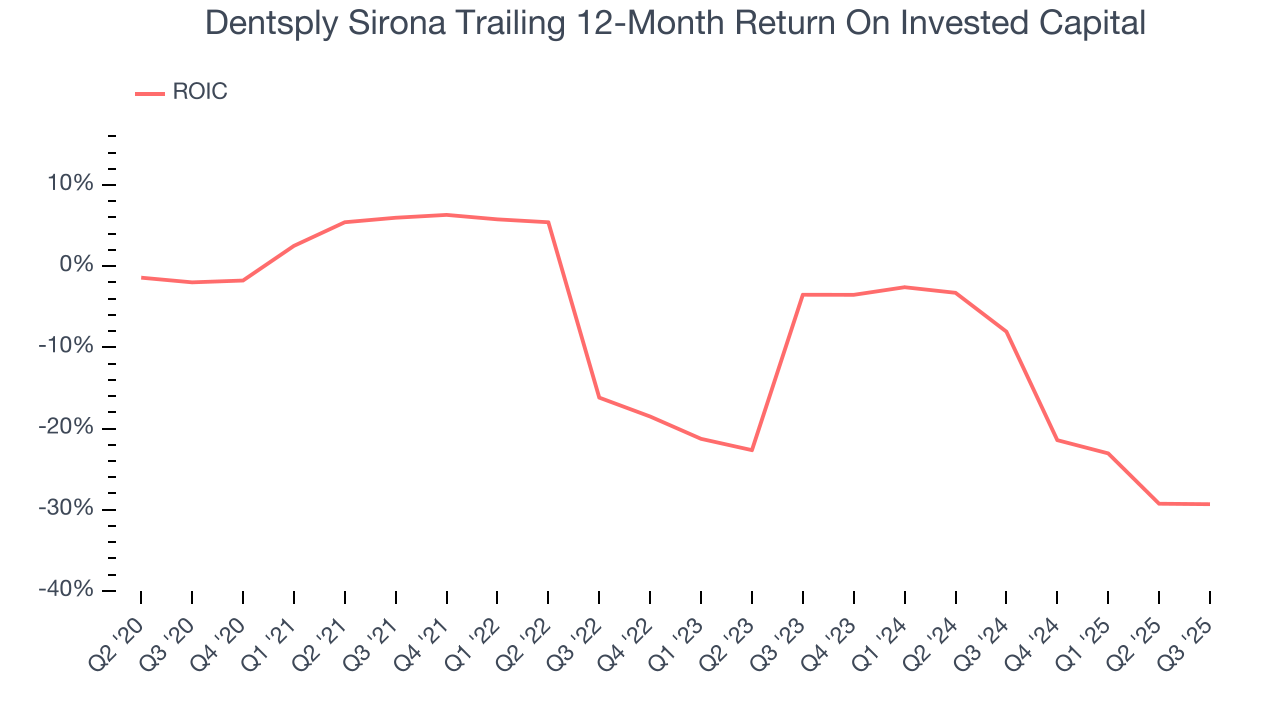

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Dentsply Sirona’s five-year average ROIC was negative 10.2%, meaning management lost money while trying to expand the business. Its returns were among the worst in the healthcare sector.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Dentsply Sirona’s ROIC has unfortunately decreased significantly. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

11. Balance Sheet Assessment

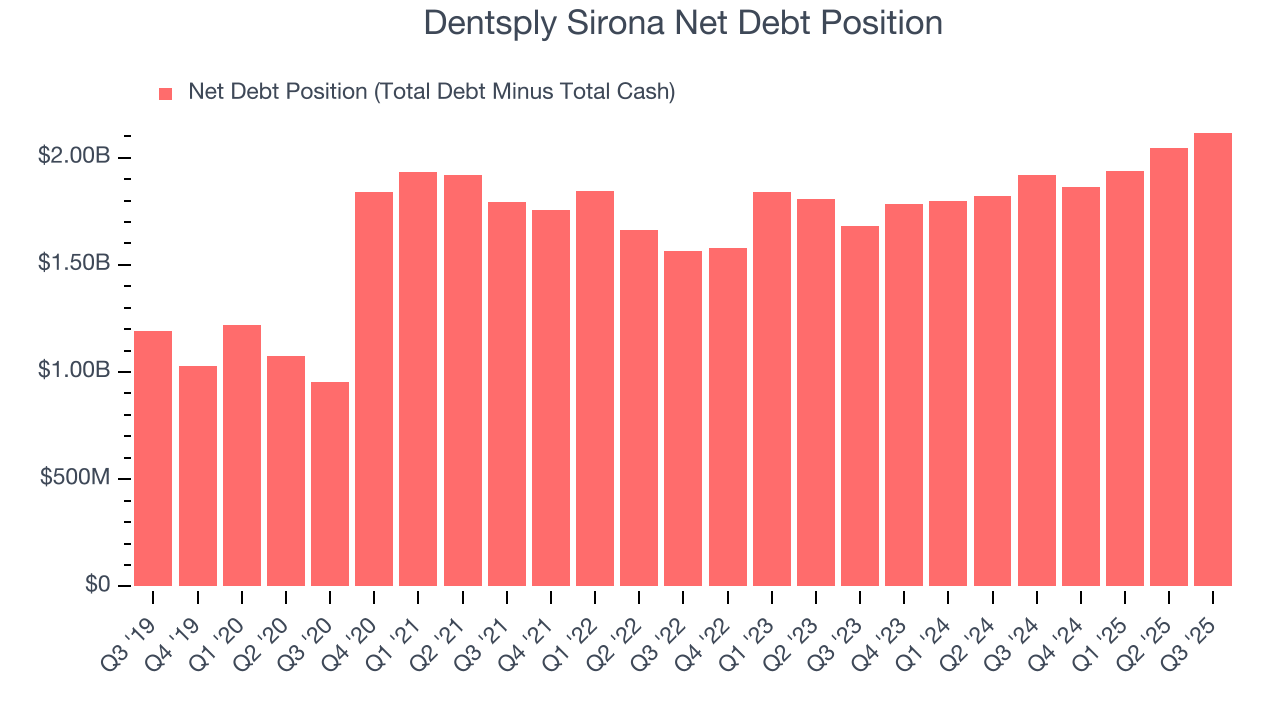

Dentsply Sirona reported $363 million of cash and $2.48 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $660 million of EBITDA over the last 12 months, we view Dentsply Sirona’s 3.2× net-debt-to-EBITDA ratio as safe. We also see its $36 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Dentsply Sirona’s Q3 Results

It was good to see Dentsply Sirona narrowly top analysts’ revenue expectations this quarter. On the other hand, its full-year EPS guidance missed and its EPS fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 10% to $11.37 immediately following the results.

13. Is Now The Time To Buy Dentsply Sirona?

Updated: January 29, 2026 at 10:44 PM EST

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Dentsply Sirona, you should also grasp the company’s longer-term business quality and valuation.

Dentsply Sirona doesn’t pass our quality test. To begin with, its revenue growth was uninspiring over the last five years, and analysts don’t see anything changing over the next 12 months. And while its sturdy operating margins show it has disciplined cost controls, the downside is its relatively low ROIC suggests management has struggled to find compelling investment opportunities. On top of that, its diminishing returns show management's prior bets haven't worked out.

Dentsply Sirona’s P/E ratio based on the next 12 months is 8.2x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $13.03 on the company (compared to the current share price of $12.27).