Zumiez (ZUMZ)

We wouldn’t buy Zumiez. Not only are its sales cratering but also its low returns on capital suggest it struggles to generate profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Zumiez Will Underperform

With store associates called “Zumiez Stash Members”, Zumiez (NASDAQ:ZUMZ) is a specialty retailer of street and skate apparel, footwear, and accessories.

- Sales tumbled by 3.6% annually over the last three years, showing consumer trends are working against its favor

- Historical operating margin losses point to an inefficient cost structure

- ROIC of 3.7% reflects management’s challenges in identifying attractive investment opportunities, and its shrinking returns suggest its past profit sources are losing steam

Zumiez’s quality is insufficient. More profitable opportunities exist elsewhere.

Why There Are Better Opportunities Than Zumiez

At $22.68 per share, Zumiez trades at 25.5x forward P/E. This multiple is high given its weaker fundamentals.

It’s better to pay up for high-quality businesses with strong long-term earnings potential rather than to buy lower-quality companies with open questions and big downside risks.

3. Zumiez (ZUMZ) Research Report: Q3 CY2025 Update

Clothing and footwear retailer Zumiez (NASDAQ:ZUMZ) reported Q3 CY2025 results beating Wall Street’s revenue expectations, with sales up 7.5% year on year to $239.1 million. Guidance for next quarter’s revenue was optimistic at $293.5 million at the midpoint, 2.7% above analysts’ estimates. Its GAAP profit of $0.55 per share was significantly above analysts’ consensus estimates.

Zumiez (ZUMZ) Q3 CY2025 Highlights:

- Revenue: $239.1 million vs analyst estimates of $234.4 million (7.5% year-on-year growth, 2% beat)

- EPS (GAAP): $0.55 vs analyst estimates of $0.27 (significant beat)

- Adjusted EBITDA: $13.44 million vs analyst estimates of $11.45 million (5.6% margin, 17.4% beat)

- Revenue Guidance for Q4 CY2025 is $293.5 million at the midpoint, above analyst estimates of $285.9 million

- EPS (GAAP) guidance for Q4 CY2025 is $1.02 at the midpoint, beating analyst estimates by 4.8%

- Operating Margin: 4.9%, up from 1.1% in the same quarter last year

- Free Cash Flow was $3.09 million, up from -$22.31 million in the same quarter last year

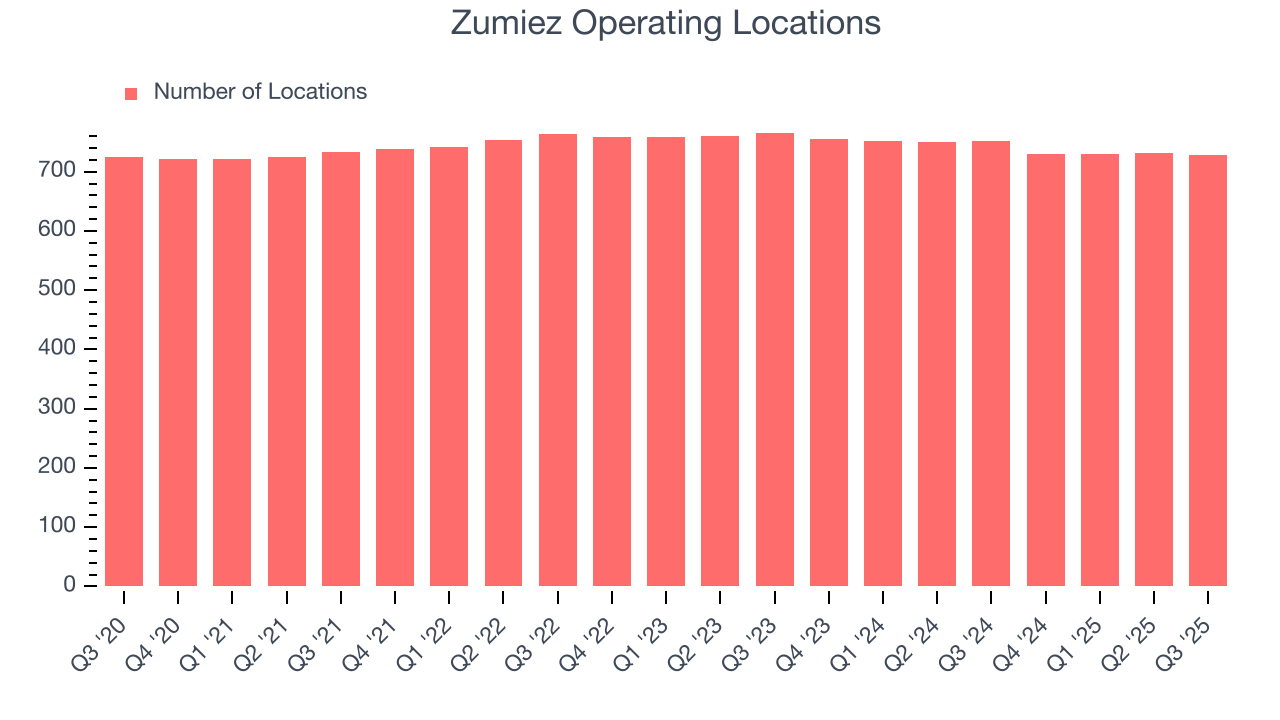

- Locations: 728 at quarter end, down from 752 in the same quarter last year

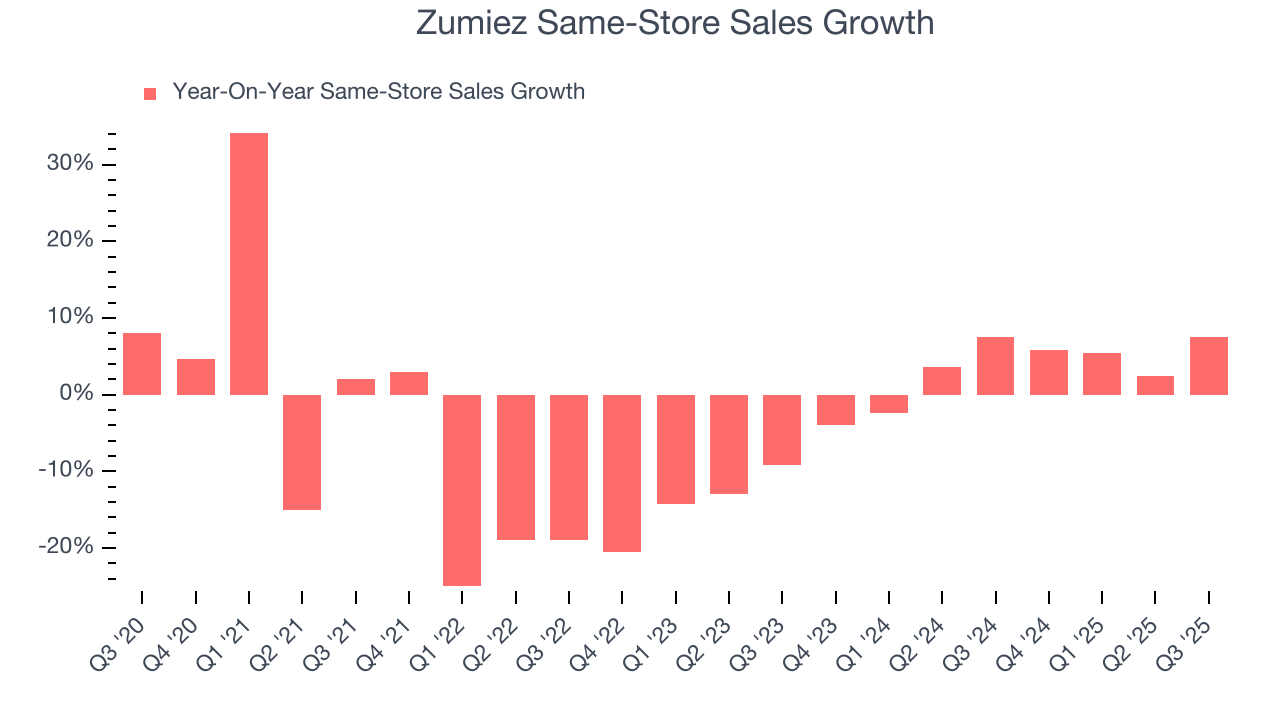

- Same-Store Sales rose 7.6% year on year, in line with the same quarter last year

- Market Capitalization: $476 million

Company Overview

With store associates called “Zumiez Stash Members”, Zumiez (NASDAQ:ZUMZ) is a specialty retailer of street and skate apparel, footwear, and accessories.

Customers can also find skateboards, snowboards, and related equipment such as wheels and bindings. The core Zumiez customer is typically a teen or young adult who skates, snowboards, or surfs and wants to reflect these interests in their clothing and footwear choices. Unsurprisingly, brands focused on these subcultures such as Vans, Thrasher, Volcom, and Element are featured in Zumiez stores.

Zumiez stores tend to be small–roughly 3,000 square feet on average–and located in suburban malls and shopping centers. There are various merchandise zones dedicated to apparel, footwear, and hard goods such as skate decks. Two unique aspects of Zumiez stores are video screens or televisions featuring endless loops of action sports as well as interactive areas where customers can handle and lightly try out equipment.

In addition to its physical store footprint, Zumiez also has an e-commerce platform, which was launched in 2005. It allows the company to reach customers that may not have a physical store near them, and it allows customers with access to a store to buy online and pick up physically.

4. Apparel Retailer

Apparel sales are not driven so much by personal needs but by seasons, trends, and innovation, and over the last few decades, the category has shifted meaningfully online. Retailers that once only had brick-and-mortar stores are responding with omnichannel presences. The online shopping experience continues to improve and retail foot traffic in places like shopping malls continues to stall, so the evolution of clothing sellers marches on.

Competitors that offer street or skate apparel and footwear include Tilly’s (NYSE:TLYS), Genesco’s (NYSE:GCO) Journeys banner, Foot Locker (NYSE:FL), and private company PacSun.

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

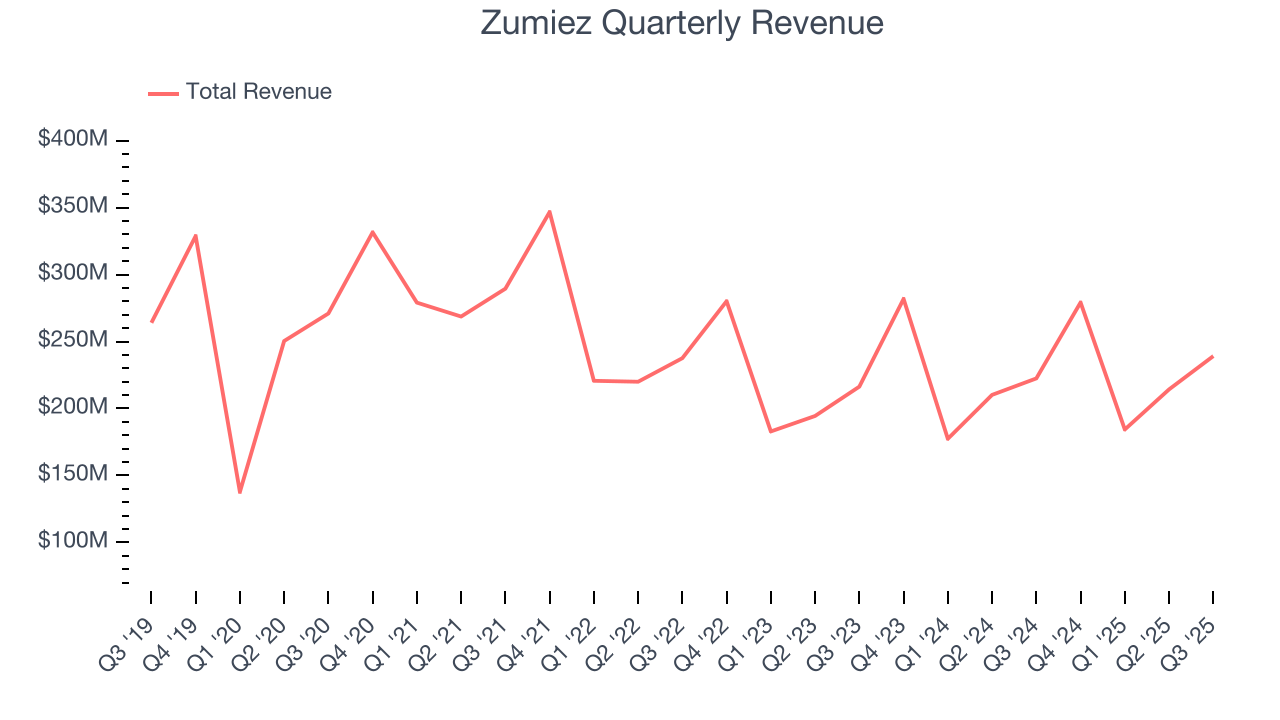

With $916.9 million in revenue over the past 12 months, Zumiez is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers.

As you can see below, Zumiez struggled to generate demand over the last three years (we compare to 2019 to normalize for COVID-19 impacts). Its sales dropped by 3.6% annually as it closed stores.

This quarter, Zumiez reported year-on-year revenue growth of 7.5%, and its $239.1 million of revenue exceeded Wall Street’s estimates by 2%. Company management is currently guiding for a 5.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 1.1% over the next 12 months. While this projection suggests its newer products will fuel better top-line performance, it is still below the sector average.

6. Store Performance

Number of Stores

A retailer’s store count influences how much it can sell and how quickly revenue can grow.

Zumiez listed 728 locations in the latest quarter and has generally closed its stores over the last two years, averaging 2.1% annual declines.

When a retailer shutters stores, it usually means that brick-and-mortar demand is less than supply, and it is responding by closing underperforming locations to improve profitability.

Same-Store Sales

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales provides a deeper understanding of this issue because it measures organic growth at brick-and-mortar shops for at least a year.

Zumiez’s demand has been spectacular for a retailer over the last two years. On average, the company has increased its same-store sales by an impressive 3.3% per year. Given its declining store base over the same period, this performance stems from a mixture of higher e-commerce sales and increased foot traffic at existing locations (closing stores can sometimes boost same-store sales).

In the latest quarter, Zumiez’s same-store sales rose 7.6% year on year. This growth was an acceleration from its historical levels, which is always an encouraging sign.

7. Gross Margin & Pricing Power

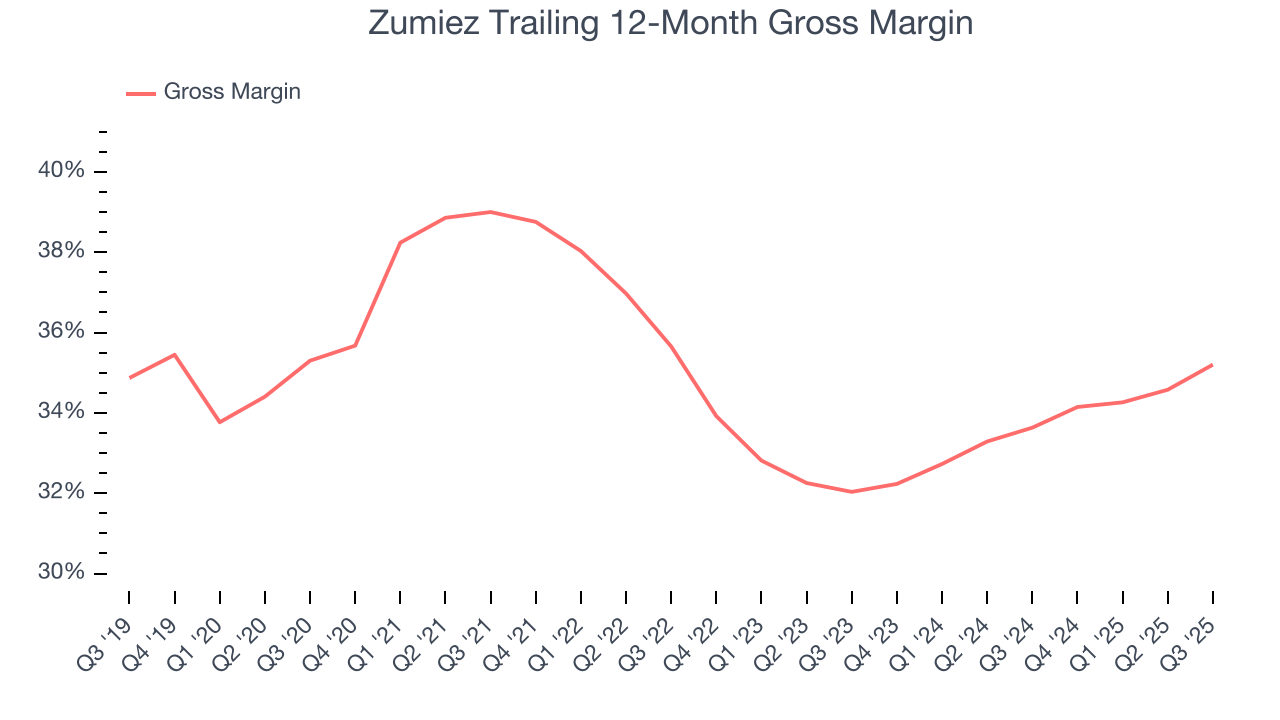

Gross profit margins are an important measure of a retailer’s pricing power, product differentiation, and negotiating leverage.

Zumiez has bad unit economics for a retailer, signaling it operates in a competitive market and lacks pricing power because its inventory is sold in many places. As you can see below, it averaged a 34.4% gross margin over the last two years. Said differently, Zumiez had to pay a chunky $65.57 to its suppliers for every $100 in revenue.

In Q3, Zumiez produced a 37.6% gross profit margin, marking a 2.4 percentage point increase from 35.2% in the same quarter last year. Zumiez’s full-year margin has also been trending up over the past 12 months, increasing by 1.6 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold.

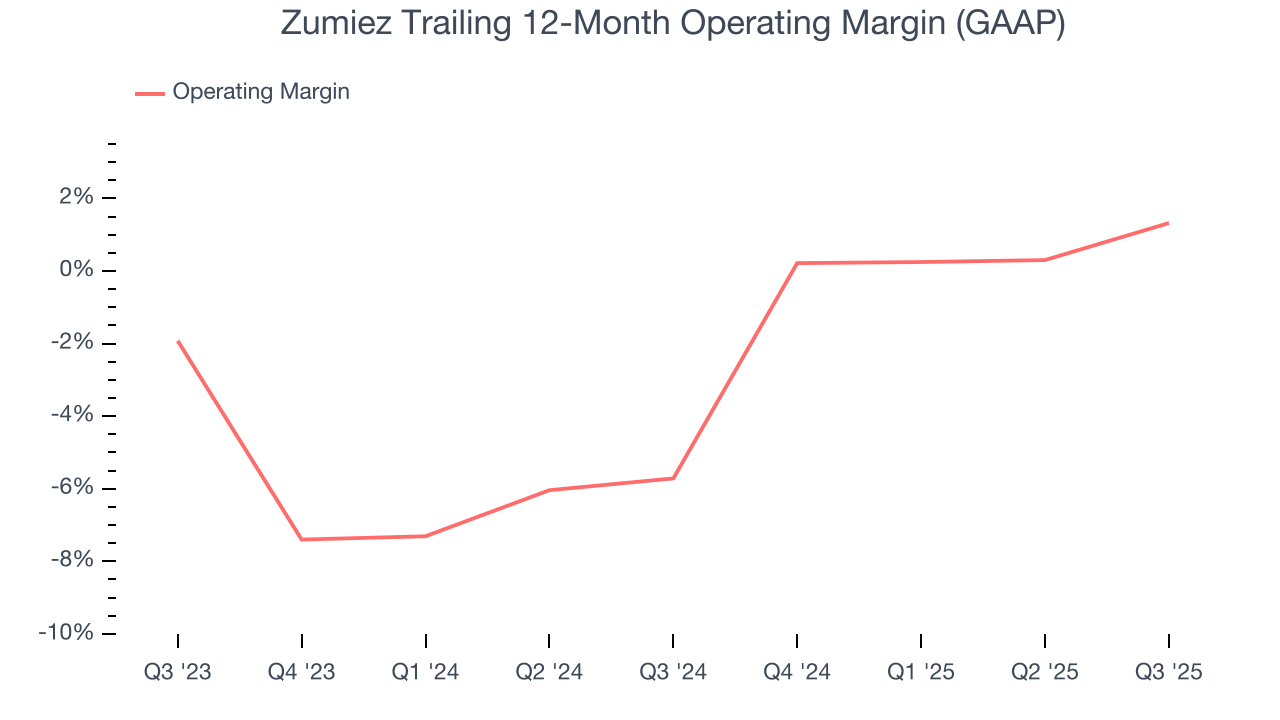

8. Operating Margin

Although Zumiez was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 2.1% over the last two years. Despite the consumer retail industry’s secular decline, unprofitable public companies are few and far between. It’s unfortunate that Zumiez was one of them.

On the plus side, Zumiez’s operating margin rose by 7 percentage points over the last year. Still, it will take much more for the company to show consistent profitability.

This quarter, Zumiez generated an operating margin profit margin of 4.9%, up 3.9 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, and administrative overhead.

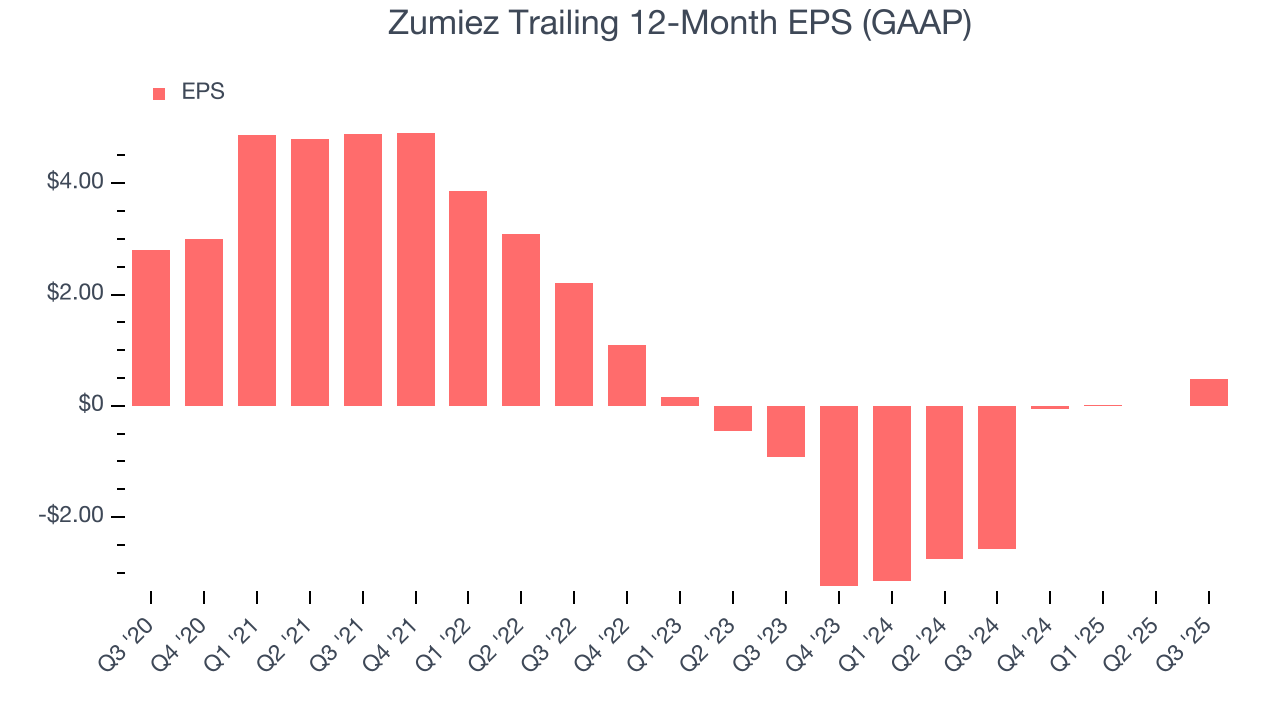

9. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Zumiez, its EPS declined by 39.7% annually over the last three years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

In Q3, Zumiez reported EPS of $0.55, up from $0.06 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Zumiez’s full-year EPS of $0.48 to grow 95.4%.

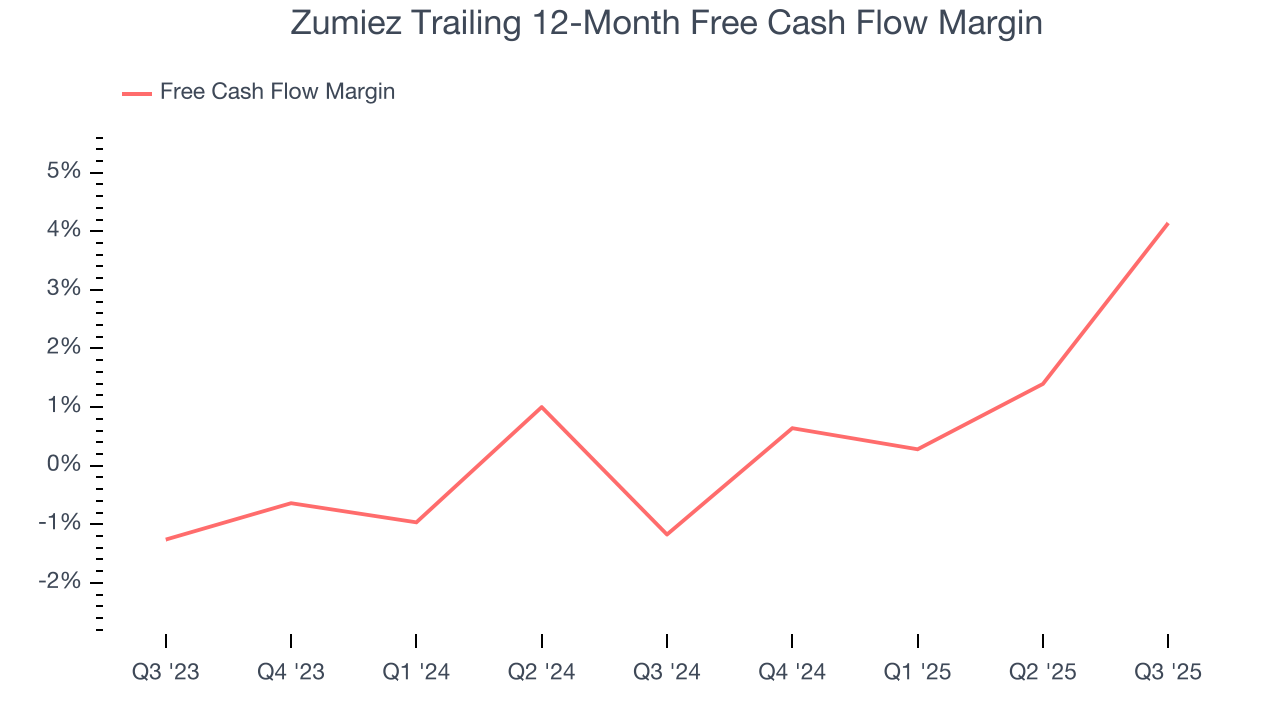

10. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Zumiez has shown mediocre cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 1.5%, subpar for a consumer retail business.

Taking a step back, an encouraging sign is that Zumiez’s margin expanded by 5.3 percentage points over the last year. We have no doubt shareholders would like to continue seeing its cash conversion rise as it gives the company more optionality.

Zumiez’s free cash flow clocked in at $3.09 million in Q3, equivalent to a 1.3% margin. Its cash flow turned positive after being negative in the same quarter last year, building on its favorable historical trend.

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Zumiez historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 3.7%, lower than the typical cost of capital (how much it costs to raise money) for consumer retail companies.

12. Balance Sheet Assessment

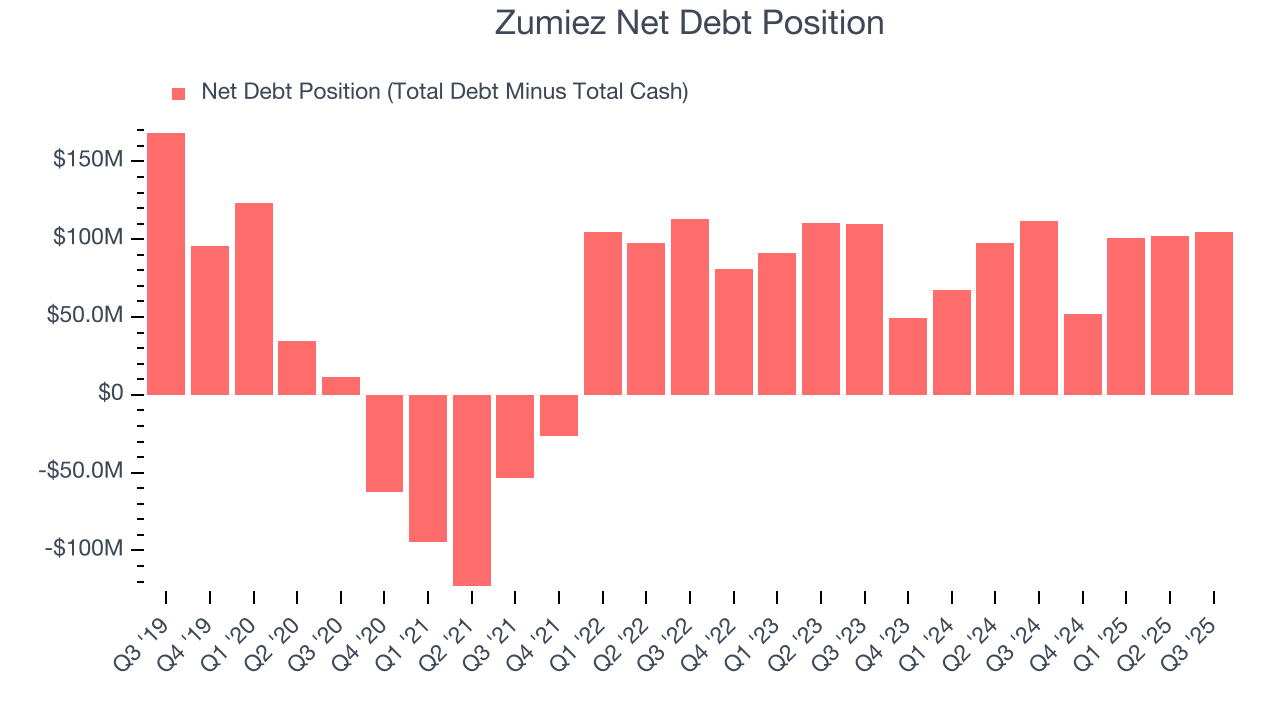

Zumiez reported $104.5 million of cash and $209.1 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $35.51 million of EBITDA over the last 12 months, we view Zumiez’s 2.9× net-debt-to-EBITDA ratio as safe. We also see its $4.63 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from Zumiez’s Q3 Results

It was good to see Zumiez beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a solid print. The stock traded up 4.3% to $28.46 immediately following the results.

14. Is Now The Time To Buy Zumiez?

Updated: March 7, 2026 at 9:54 PM EST

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Zumiez.

We see the value of companies helping consumers, but in the case of Zumiez, we’re out. First off, its revenue has declined over the last three years. While its projected EPS for the next year implies the company’s fundamentals will improve, the downside is its brand caters to a niche market. On top of that, its declining EPS over the last three years makes it a less attractive asset to the public markets.

Zumiez’s P/E ratio based on the next 12 months is 25.5x. This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $24 on the company (compared to the current share price of $22.68).