AAR (AIR)

AAR catches our eye. Its revenue is growing quickly while its profitability is rising, giving it multiple ways to win.― StockStory Analyst Team

1. News

2. Summary

Why AAR Is Interesting

The first third-party MRO approved by the FAA for Safety Management System Requirements, AAR (NYSE:AIR) is a provider of aircraft maintenance services

- Market share will likely rise over the next 12 months as its expected revenue growth of 15.5% is robust

- Earnings growth has massively outpaced its peers over the last five years as its EPS has compounded at 25.6% annually

- One pitfall is its lacking free cash flow limits its freedom to invest in growth initiatives, execute share buybacks, or pay dividends

AAR is close to becoming a high-quality business. If you like the stock, the price looks fair.

Why Is Now The Time To Buy AAR?

At $106.95 per share, AAR trades at 20x forward P/E. This multiple is lower than the broader industrials space, and we think it’s fair given the revenue growth.

If you think the market is not giving the company enough credit for its fundamentals, now could be a good time to invest.

3. AAR (AIR) Research Report: Q1 CY2026 Update

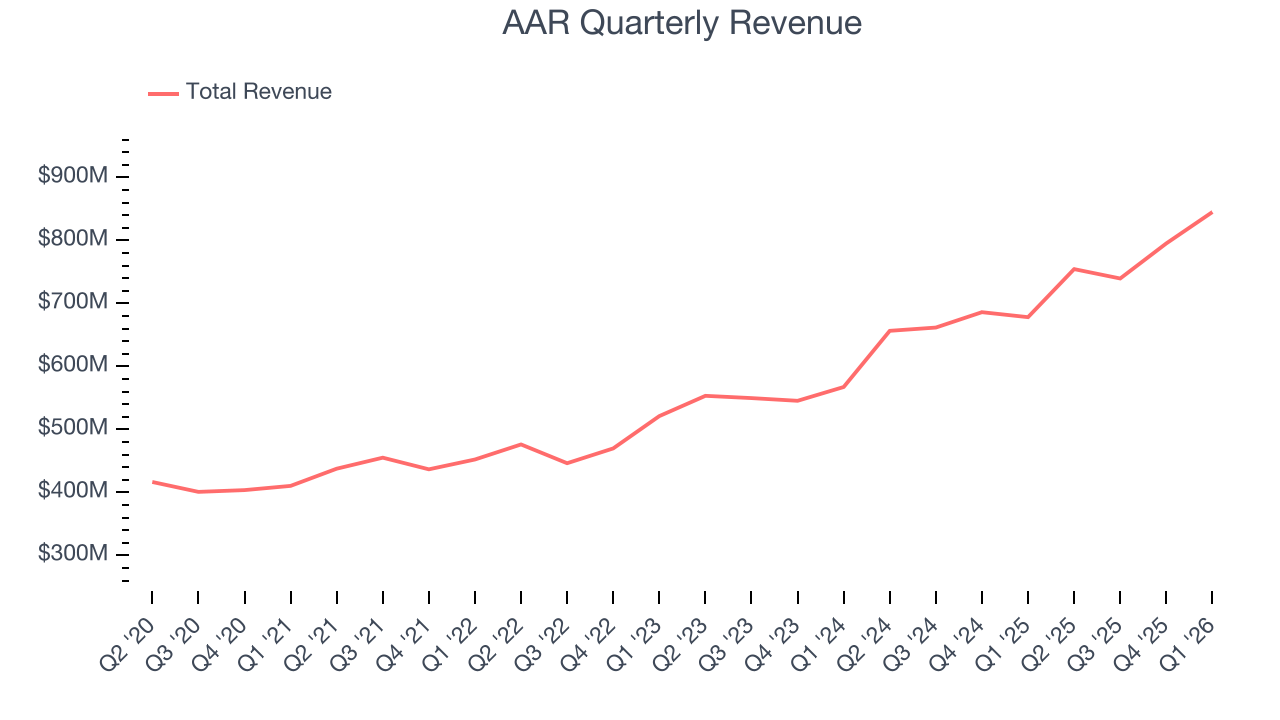

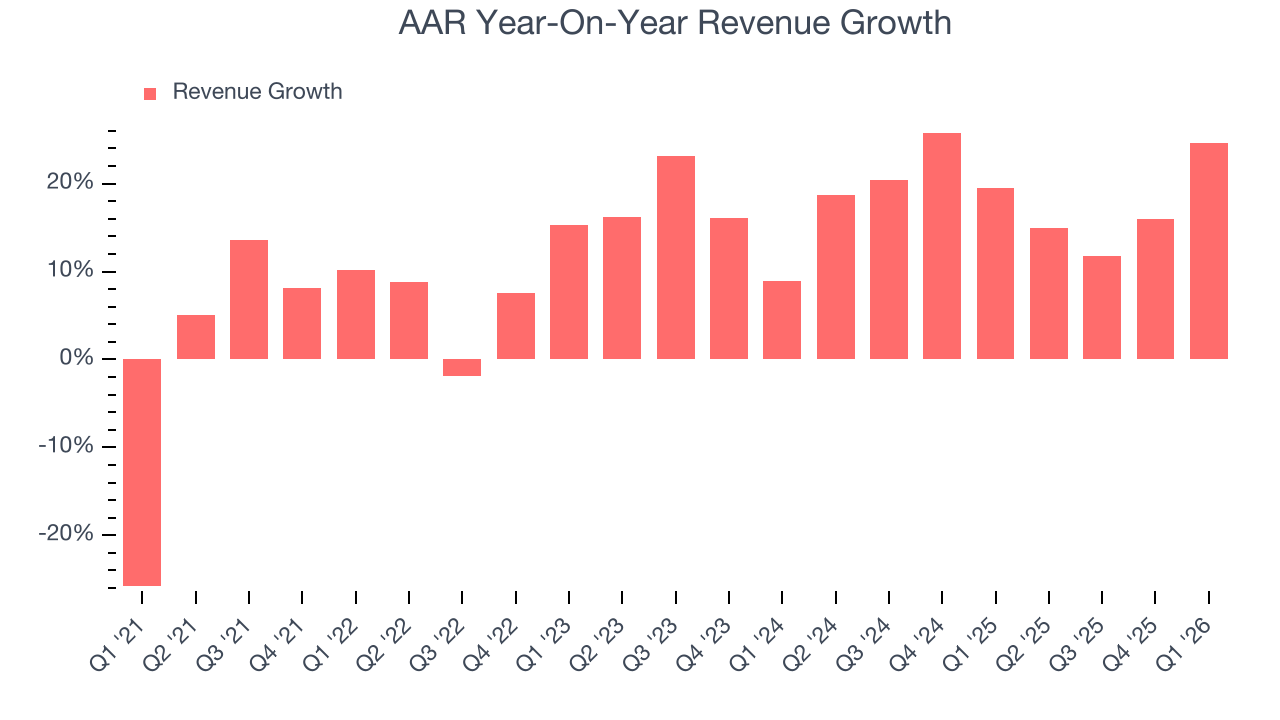

Aviation and defense services provider AAR CORP (NYSE:AIR) announced better-than-expected revenue in Q1 CY2026, with sales up 24.6% year on year to $845.1 million. On top of that, next quarter’s revenue guidance ($905.4 million at the midpoint) was surprisingly good and 4.6% above what analysts were expecting. Its non-GAAP profit of $1.25 per share was 8.1% above analysts’ consensus estimates.

AAR (AIR) Q1 CY2026 Highlights:

- Revenue: $845.1 million vs analyst estimates of $811.4 million (24.6% year-on-year growth, 4.1% beat)

- Adjusted EPS: $1.25 vs analyst estimates of $1.16 (8.1% beat)

- Adjusted EBITDA: $102.1 million vs analyst estimates of $96.23 million (12.1% margin, 6.1% beat)

- Revenue Guidance for Q2 CY2026 is $905.4 million at the midpoint, above analyst estimates of $865.9 million

- Operating Margin: 7.8%, down from 10.5% in the same quarter last year

- Free Cash Flow was $66.2 million, up from -$27.2 million in the same quarter last year

- Market Capitalization: $4.04 billion

Company Overview

The first third-party MRO approved by the FAA for Safety Management System Requirements, AAR (NYSE:AIR) is a provider of aircraft maintenance services

Founded in 1951 and headquartered in Wood Dale, Illinois, AAR has established itself in the aviation aftermarket and defense sectors.The company operates through two primary business segments: Aviation Services and Expeditionary Services.

The Aviation Services segment, which accounts for the majority of AAR's sales, provides aftermarket support and services for commercial aviation and government and defense markets. This segment's offerings include inventory management and distribution services, maintenance, repair, and overhaul (MRO) services, and engineering services. AAR's Aviation Services segment sells and leases a variety of new, overhauled, and repaired engine and airframe parts and components to commercial aviation and government/defense customers.

AAR's Expeditionary Services segment primarily focuses on products and services supporting the movement of equipment and personnel by the U.S. and foreign governments and non-governmental organizations. This segment designs, manufactures, and repairs transportation pallets, containers, and shelters used in military and humanitarian tactical deployment activities.

The company has numerous facilities across North America, Europe, and Asia. AAR's customer base includes domestic and foreign passenger airlines, cargo airlines, regional and commuter airlines, business and general aviation operators, original equipment manufacturers (OEMs), aircraft leasing companies, aftermarket aviation support companies, the U.S. Department of Defense and its contractors, the U.S. Department of State, and foreign military organizations or governments.

The company recently acquired Trax USA Corp., a leading provider of aircraft MRO and fleet management software, enhancing its portfolio with higher-margin aviation aftermarket software offerings. This acquisition aligns with AAR's strategy to provide opportunities for cross-selling products and services.

4. Aerospace

Aerospace companies often possess technical expertise and have made significant capital investments to produce complex products. It is an industry where innovation is important, and lately, emissions and automation are in focus, so companies that boast advances in these areas can take market share. On the other hand, demand for aerospace products can ebb and flow with economic cycles and geopolitical tensions, which can be particularly painful for companies with high fixed costs.

AAR’s competitors include General Dynamics (NSYE:GD) and Kratos Defense and Security (NASDAQ:KTOS)

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Luckily, AAR’s sales grew at an exceptional 14% compounded annual growth rate over the last five years. Its growth beat the average industrials company and shows its offerings resonate with customers, a helpful starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. AAR’s annualized revenue growth of 18.9% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

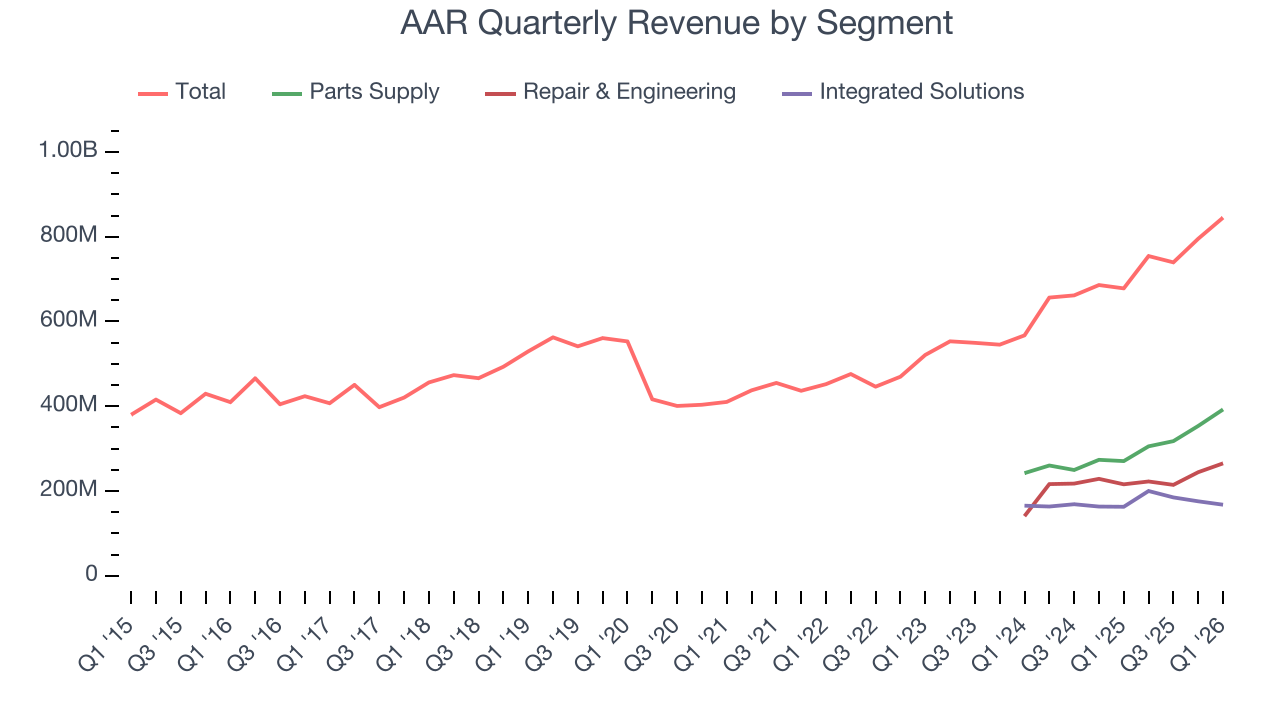

AAR also breaks out the revenue for its three most important segments: Parts Supply, Repair & Engineering, and Integrated Solutions, which are 46.4%, 31.4%, and 19.9% of revenue. Over the last two years, AAR’s revenues in all three segments increased. Its Parts Supply revenue (engine and airframe parts) averaged year-on-year growth of 26.1% while its Repair & Engineering (maintenance, repair, and overhaul services) and Integrated Solutions (fleet management) revenues averaged 16.9% and 8.2%.

This quarter, AAR reported robust year-on-year revenue growth of 24.6%, and its $845.1 million of revenue topped Wall Street estimates by 4.1%. Company management is currently guiding for a 20% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 11.3% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is admirable and implies the market is forecasting success for its products and services.

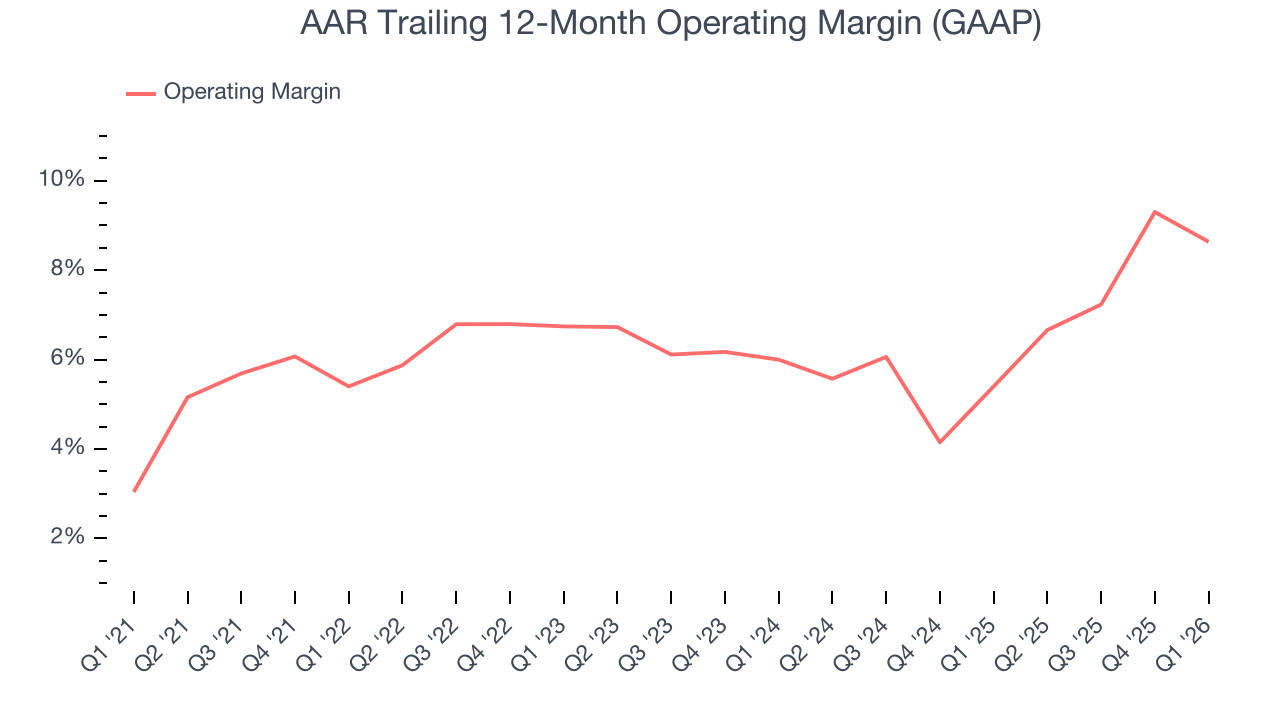

6. Operating Margin

AAR was profitable over the last five years but held back by its large cost base. Its average operating margin of 6.6% was weak for an industrials business.

On the plus side, AAR’s operating margin rose by 3.2 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q1, AAR generated an operating margin profit margin of 7.8%, down 2.7 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

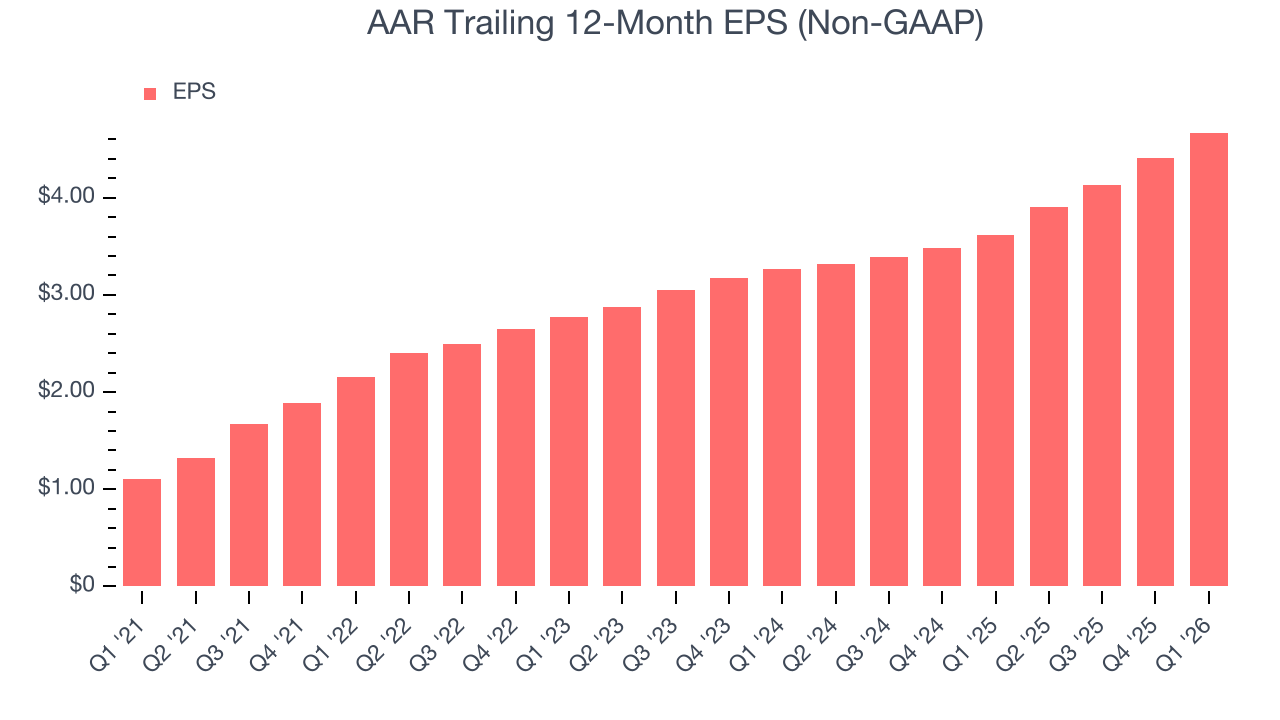

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

AAR’s EPS grew at 33.3% compounded annual growth rate over the last five years, higher than its 14% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

We can take a deeper look into AAR’s earnings to better understand the drivers of its performance. As we mentioned earlier, AAR’s operating margin declined this quarter but expanded by 3.2 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For AAR, its two-year annual EPS growth of 19.5% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q1, AAR reported adjusted EPS of $1.25, up from $0.99 in the same quarter last year. This print beat analysts’ estimates by 8.1%. Over the next 12 months, Wall Street expects AAR’s full-year EPS of $4.67 to grow 12%.

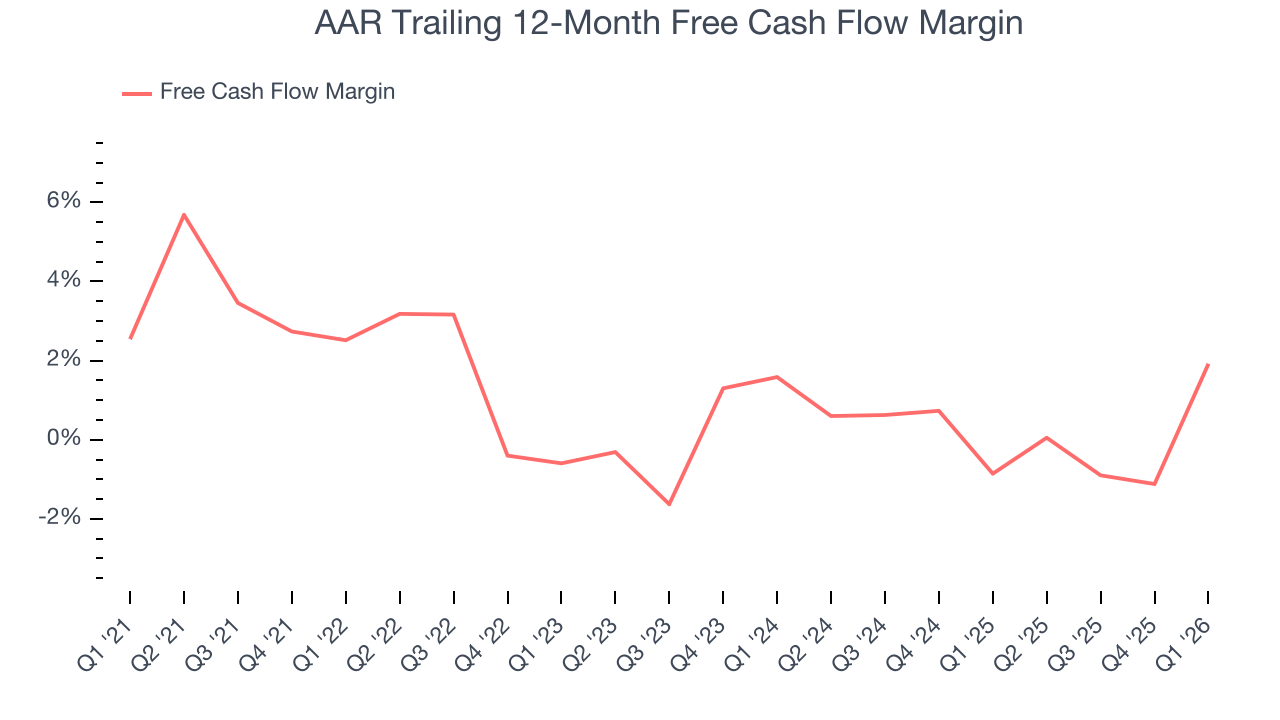

8. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

AAR broke even from a free cash flow perspective over the last five years, giving the company limited opportunities to return capital to shareholders.

AAR’s free cash flow clocked in at $66.2 million in Q1, equivalent to a 7.8% margin. Its cash flow turned positive after being negative in the same quarter last year. Its cash profitability was also above its five-year level, and we hope the company can build on this trend.

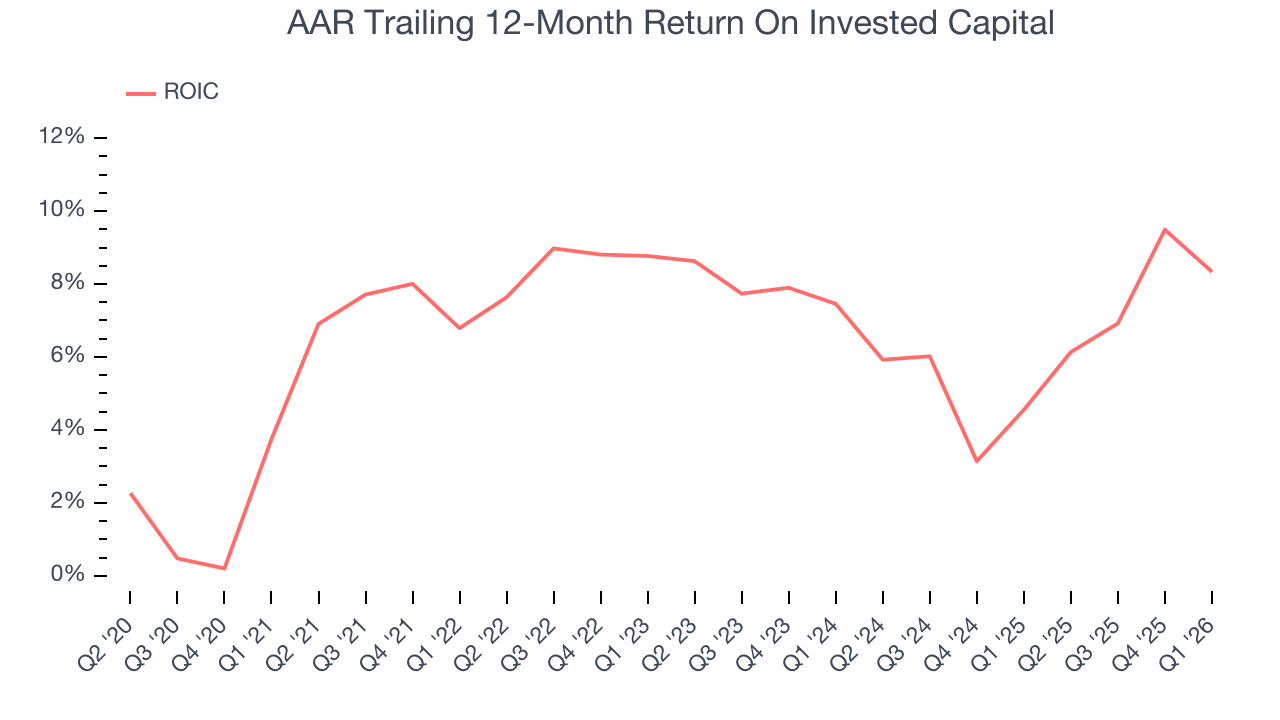

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Although AAR has shown solid fundamentals lately, it historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 7.2%, somewhat low compared to the best industrials companies that consistently pump out 20%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, AAR’s ROIC averaged 1.3 percentage point decreases each year. If its returns keep falling, it could suggest its profitable growth opportunities are drying up. We’ll keep a close eye.

10. Balance Sheet Assessment

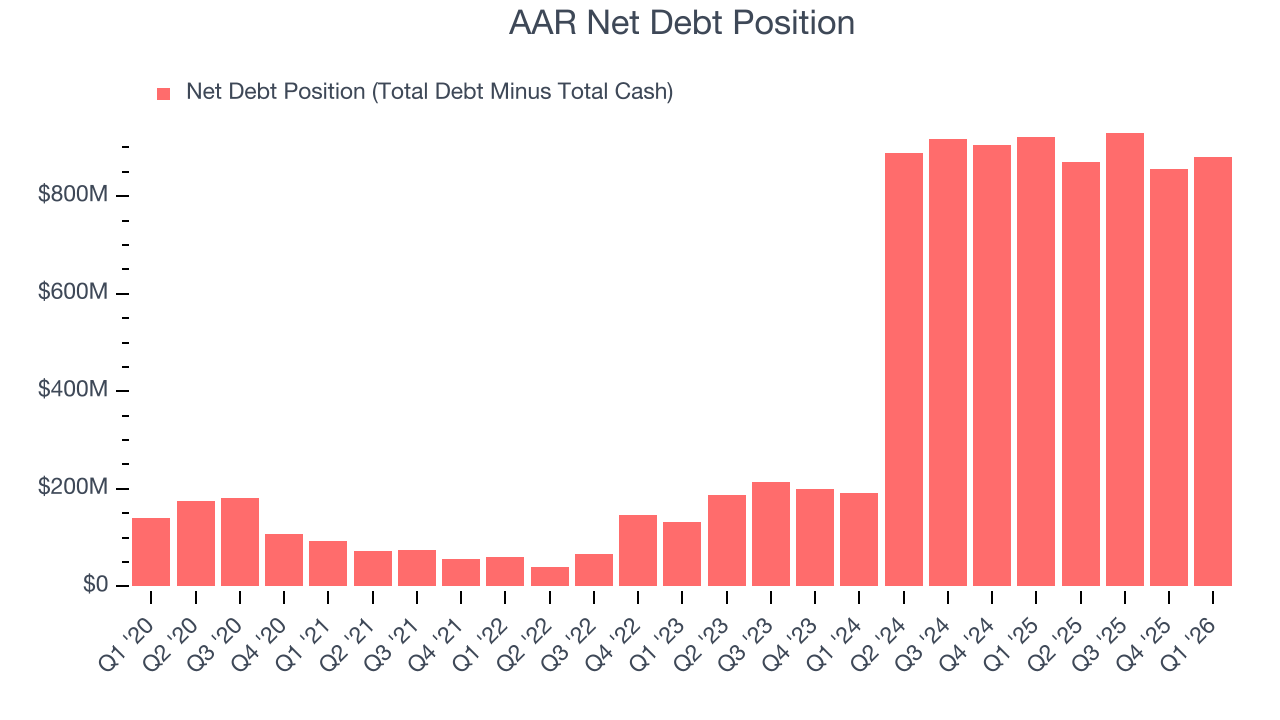

AAR reported $100.1 million of cash and $979.7 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $376.2 million of EBITDA over the last 12 months, we view AAR’s 2.3× net-debt-to-EBITDA ratio as safe. We also see its $72.6 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from AAR’s Q1 Results

We were impressed by how significantly AAR blew past analysts’ revenue expectations this quarter. We were also glad its EBITDA outperformed Wall Street’s estimates. Zooming out, we think this was a solid print. The stock remained flat at $108.86 immediately following the results.

12. Is Now The Time To Buy AAR?

Updated: March 24, 2026 at 10:07 PM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own AAR, you should also grasp the company’s longer-term business quality and valuation.

AAR is an amazing business ranking highly on our list. First of all, the company’s revenue growth was exceptional over the last five years. And while its low free cash flow margins give it little breathing room, its astounding EPS growth over the last five years shows its profits are trickling down to shareholders. Additionally, AAR’s expanding operating margin shows the business has become more efficient.

AAR’s P/E ratio based on the next 12 months is 19.8x. Analyzing the industrials landscape today, AAR’s positive attributes shine bright. We like the stock at this price.

Wall Street analysts have a consensus one-year price target of $119.80 on the company (compared to the current share price of $110.18), implying they see 8.7% upside in buying AAR in the short term.