Allegion (ALLE)

We aren’t fans of Allegion. Its weak sales growth and declining returns on capital show its demand and profits are shrinking.― StockStory Analyst Team

1. News

2. Summary

Why Allegion Is Not Exciting

Allegion plc (NYSE:ALLE) is a provider of security products and solutions that keep people and assets safe and secure in various environments.

- Organic sales performance over the past two years indicates the company may need to make strategic adjustments or rely on M&A to catalyze faster growth

- Demand will likely be soft over the next 12 months as Wall Street’s estimates imply tepid growth of 7.3%

- On the plus side, its successful business model is illustrated by its impressive operating margin, and its rise over the last five years was fueled by some leverage on its fixed costs

Allegion’s quality doesn’t meet our hurdle. We’re redirecting our focus to better businesses.

Why There Are Better Opportunities Than Allegion

Allegion’s stock price of $166.56 implies a valuation ratio of 19.3x forward P/E. This multiple is lower than most industrials companies, but for good reason.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Allegion (ALLE) Research Report: Q3 CY2025 Update

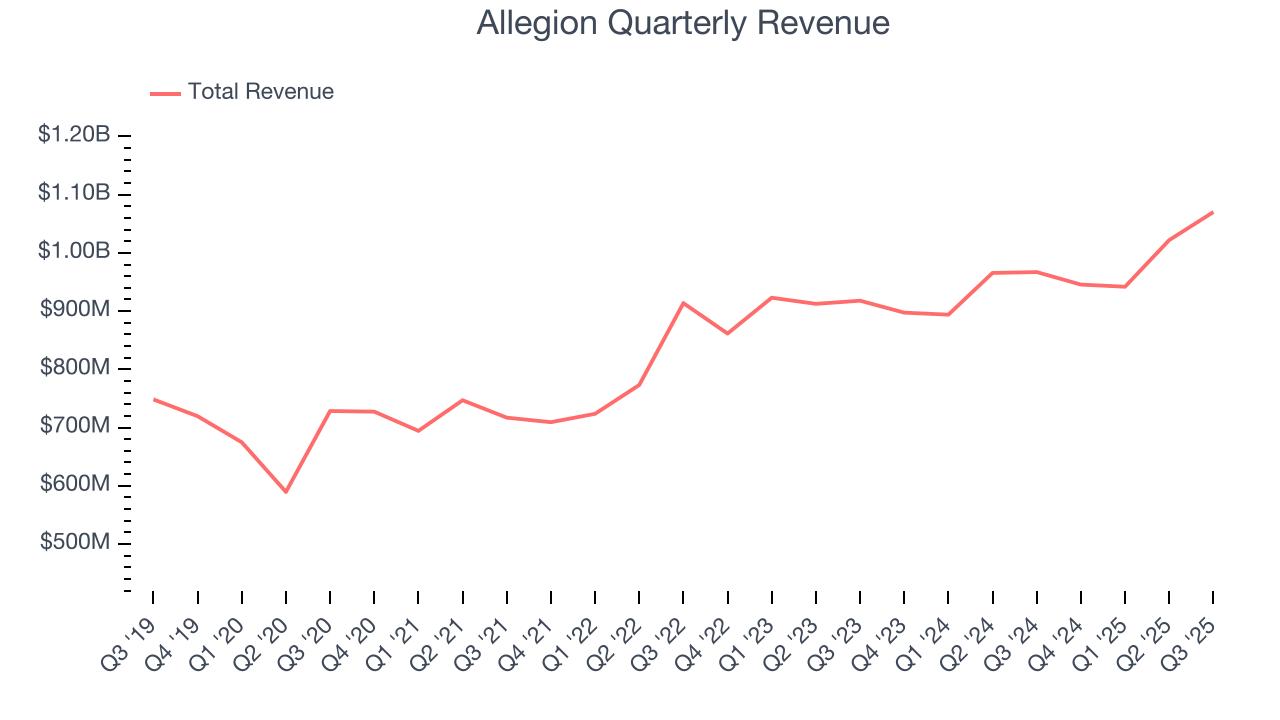

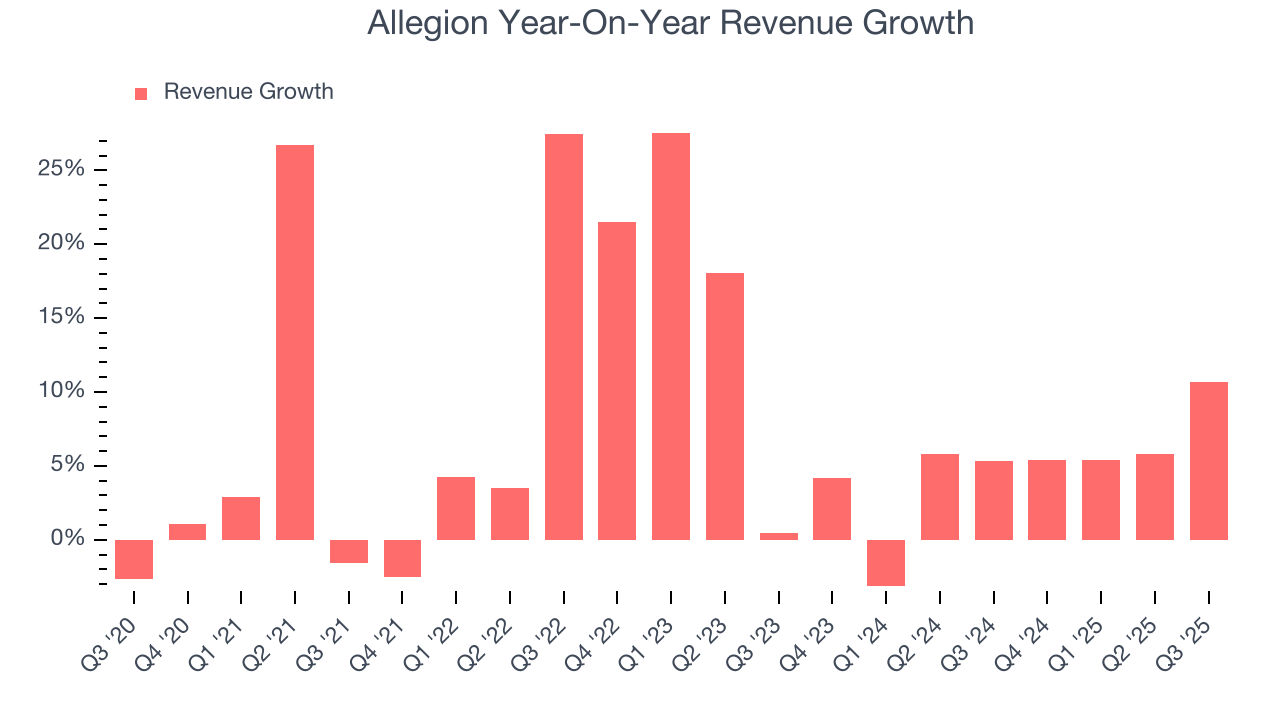

Security hardware provider Allegion (NYSE:ALLE) reported Q3 CY2025 results exceeding the market’s revenue expectations, with sales up 10.7% year on year to $1.07 billion. Its non-GAAP profit of $2.30 per share was 2.5% above analysts’ consensus estimates.

Allegion (ALLE) Q3 CY2025 Highlights:

- Revenue: $1.07 billion vs analyst estimates of $1.04 billion (10.7% year-on-year growth, 2.5% beat)

- Adjusted EPS: $2.30 vs analyst estimates of $2.24 (2.5% beat)

- Management slightly raised its full-year Adjusted EPS guidance to $8.15 at the midpoint

- Operating Margin: 21.8%, in line with the same quarter last year

- Free Cash Flow Margin: 19.6%, down from 21.9% in the same quarter last year

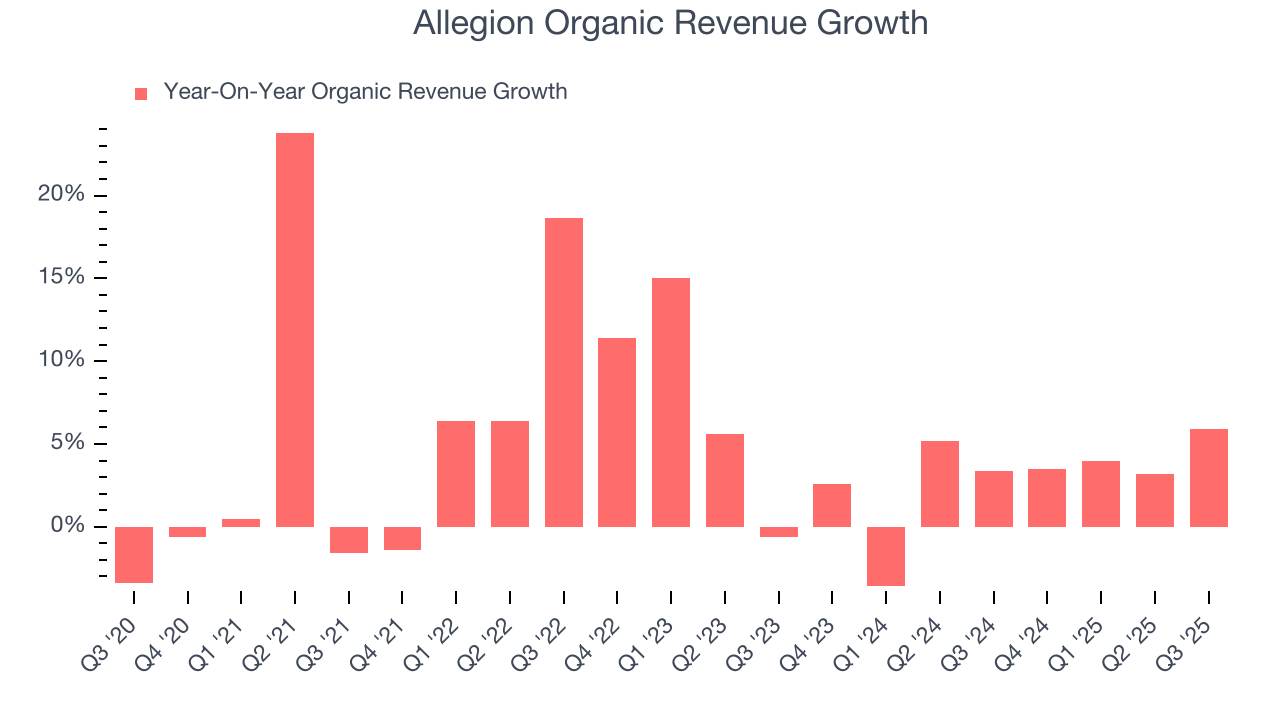

- Organic Revenue rose 5.9% year on year vs analyst estimates of 4.4% growth (154.2 basis point beat)

- Market Capitalization: $15.07 billion

Company Overview

Allegion plc (NYSE:ALLE) is a provider of security products and solutions that keep people and assets safe and secure in various environments.

Allegion offers an extensive portfolio of security and access control products across a range of market-leading brands, serving commercial, institutional, and residential markets. The company's product offerings include locks, locksets, portable locks, key systems, electronic security products, time and attendance systems, door controls, exit devices, doors and accessories, and various services and software solutions.

Allegion operates through two main segments: Allegion Americas and Allegion International. The Americas segment focuses on North and South America, while the International segment covers Europe, Asia, and Oceania.

The largest portion of revenue comes from locks, locksets, and key systems, followed by electronic security products and access control systems. Additionally, Allegion has been expanding its service and software offerings, which provide a growing stream of recurring revenue. The company primarily sells through distribution and retail channels, including specialty distributors, e-commerce platforms, and wholesalers. Allegion also sells directly to end-users through some of its businesses, such as Access Technologies and Interflex.

A recent acquisition for the company is that of Stanley Access Technologies in 2022 expanded Allegion's presence in the automatic entrance solutions market.

4. Electrical Systems

Like many equipment and component manufacturers, electrical systems companies are buoyed by secular trends such as connectivity and industrial automation. More specific pockets of strong demand include Internet of Things (IoT) connectivity and the 5G telecom upgrade cycle, which can benefit companies whose cables and conduits fit those needs. But like the broader industrials sector, these companies are also at the whim of economic cycles. Interest rates, for example, can greatly impact projects that drive demand for these products.

Competitors in the security solutions industry include ASSA ABLOY (OTC:ASAZY), Fortune Brands (NYSE:FBHS), and Stanley Black & Decker (NYSE:SWK)

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, Allegion’s 8% annualized revenue growth over the last five years was decent. Its growth was slightly above the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Allegion’s recent performance shows its demand has slowed as its annualized revenue growth of 4.9% over the last two years was below its five-year trend. We also note many other Electrical Systems businesses have faced declining sales because of cyclical headwinds. While Allegion grew slower than we’d like, it did do better than its peers.

We can dig further into the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Allegion’s organic revenue averaged 3% year-on-year growth. Because this number is lower than its two-year revenue growth, we can see that some mixture of acquisitions and foreign exchange rates boosted its headline results.

This quarter, Allegion reported year-on-year revenue growth of 10.7%, and its $1.07 billion of revenue exceeded Wall Street’s estimates by 2.5%.

Looking ahead, sell-side analysts expect revenue to grow 5.5% over the next 12 months, similar to its two-year rate. This projection is underwhelming and indicates its newer products and services will not lead to better top-line performance yet.

6. Gross Margin & Pricing Power

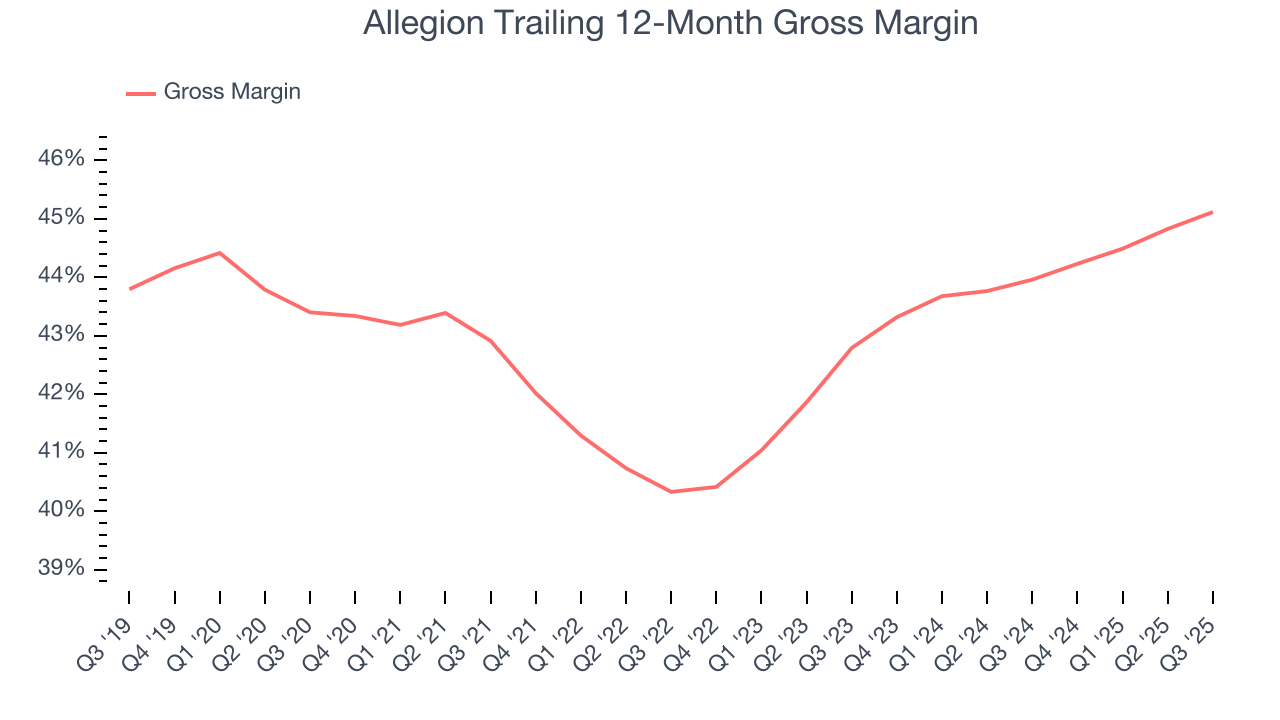

Allegion has best-in-class unit economics for an industrials company, enabling it to invest in areas such as research and development. Its margin also signals it sells differentiated products, not commodities. As you can see below, it averaged an elite 43.2% gross margin over the last five years. That means Allegion only paid its suppliers $56.85 for every $100 in revenue.

Allegion produced a 45.8% gross profit margin in Q3, marking a 1.1 percentage point increase from 44.7% in the same quarter last year. Allegion’s full-year margin has also been trending up over the past 12 months, increasing by 1.2 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold (such as manufacturing expenses).

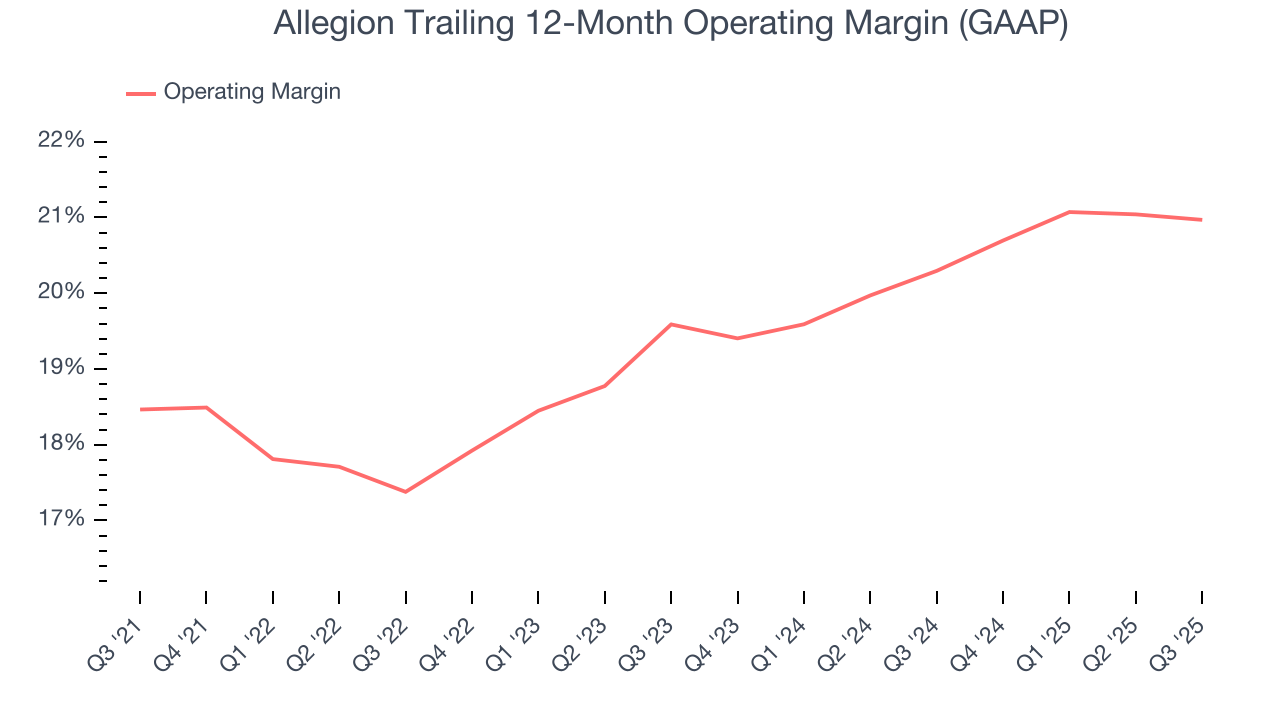

7. Operating Margin

Allegion has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 19.5%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Allegion’s operating margin rose by 2.5 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, Allegion generated an operating margin profit margin of 21.8%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

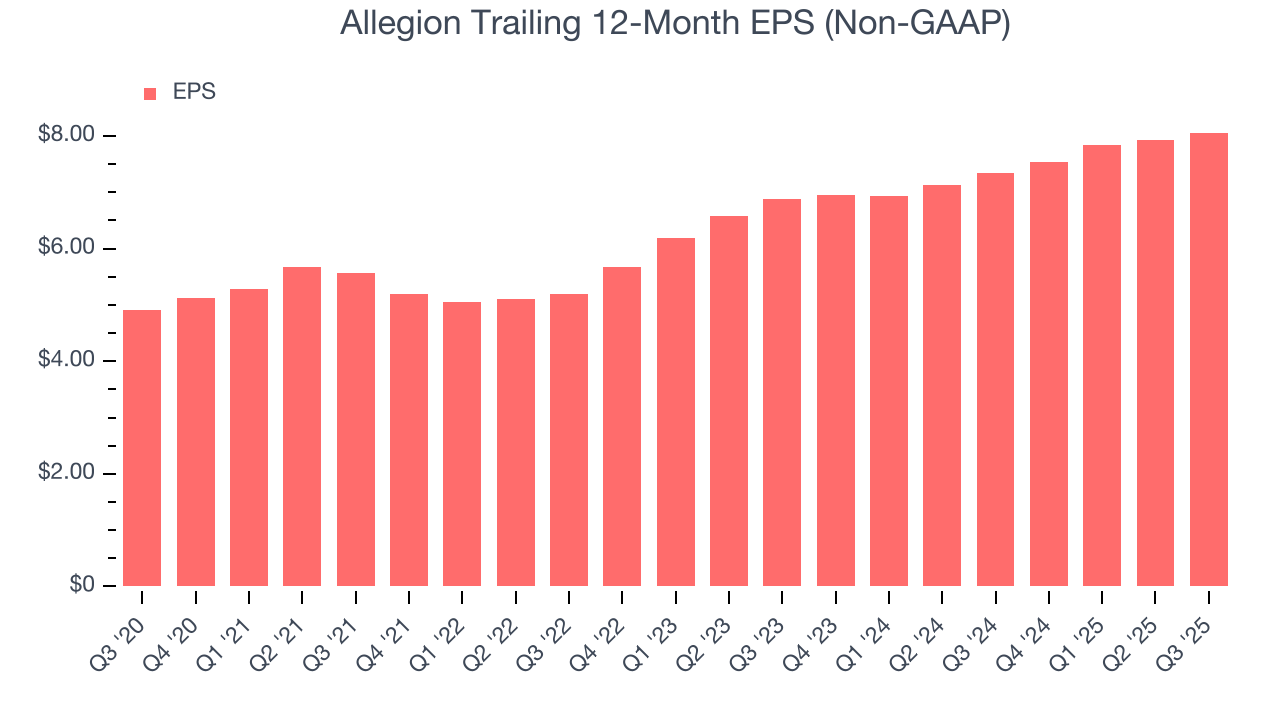

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Allegion’s EPS grew at a solid 10.4% compounded annual growth rate over the last five years, higher than its 8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

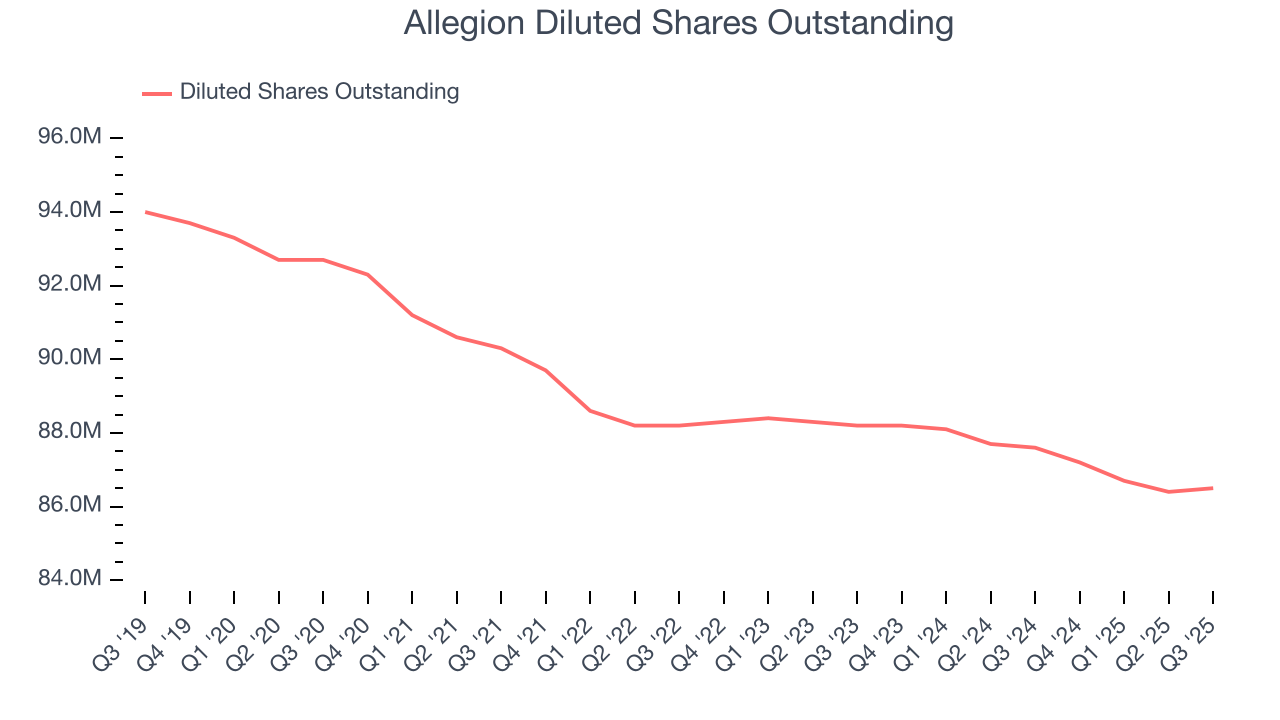

Diving into the nuances of Allegion’s earnings can give us a better understanding of its performance. As we mentioned earlier, Allegion’s operating margin was flat this quarter but expanded by 2.5 percentage points over the last five years. On top of that, its share count shrank by 6.7%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Allegion, its two-year annual EPS growth of 8.2% was lower than its five-year trend. We hope its growth can accelerate in the future.

In Q3, Allegion reported adjusted EPS of $2.30, up from $2.16 in the same quarter last year. This print beat analysts’ estimates by 2.5%. Over the next 12 months, Wall Street expects Allegion’s full-year EPS of $8.06 to grow 2.9%.

9. Cash Is King

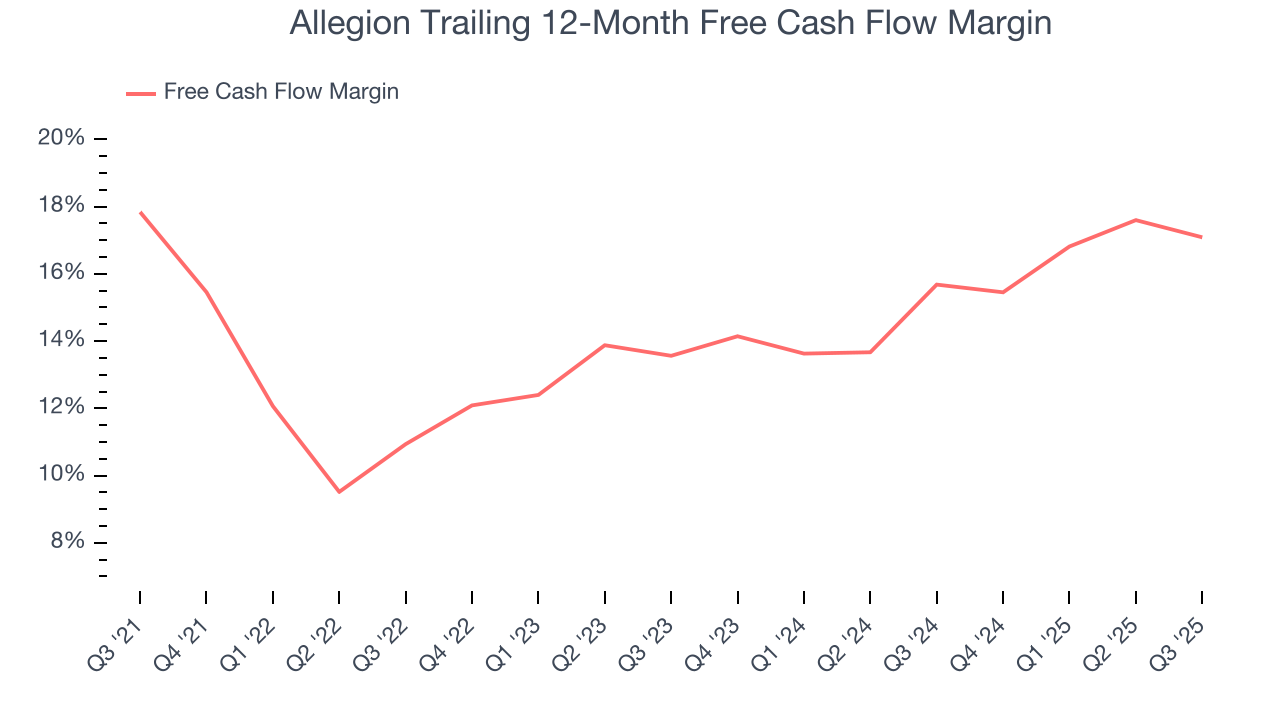

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Allegion has shown terrific cash profitability, putting it in an advantageous position to invest in new products, return capital to investors, and consolidate the market during industry downturns. The company’s free cash flow margin was among the best in the industrials sector, averaging 15.1% over the last five years.

Allegion’s free cash flow clocked in at $209.8 million in Q3, equivalent to a 19.6% margin. The company’s cash profitability regressed as it was 2.3 percentage points lower than in the same quarter last year, but it’s still above its five-year average. We wouldn’t put too much weight on this quarter’s decline because investment needs can be seasonal, causing short-term swings. Long-term trends trump temporary fluctuations.

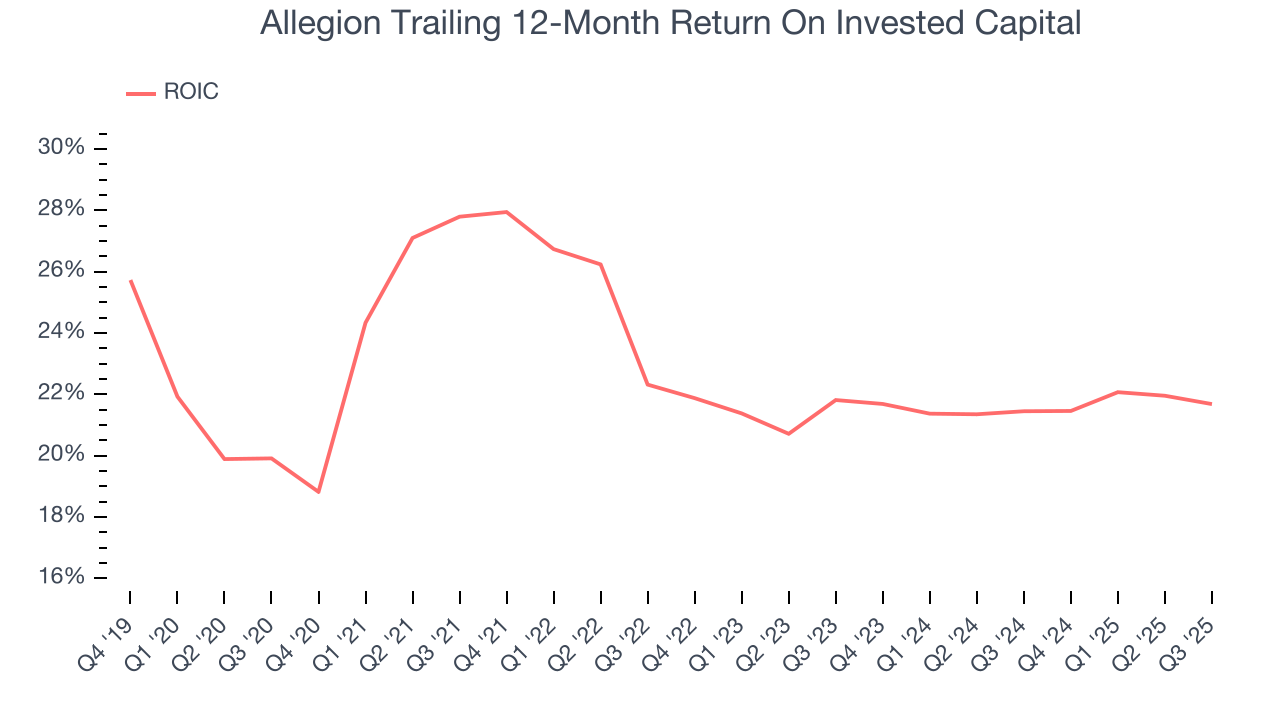

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Although Allegion hasn’t been the highest-quality company lately, it found a few growth initiatives in the past that worked out wonderfully. Its five-year average ROIC was 23%, splendid for an industrials business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Allegion’s ROIC averaged 3.5 percentage point decreases over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

11. Balance Sheet Assessment

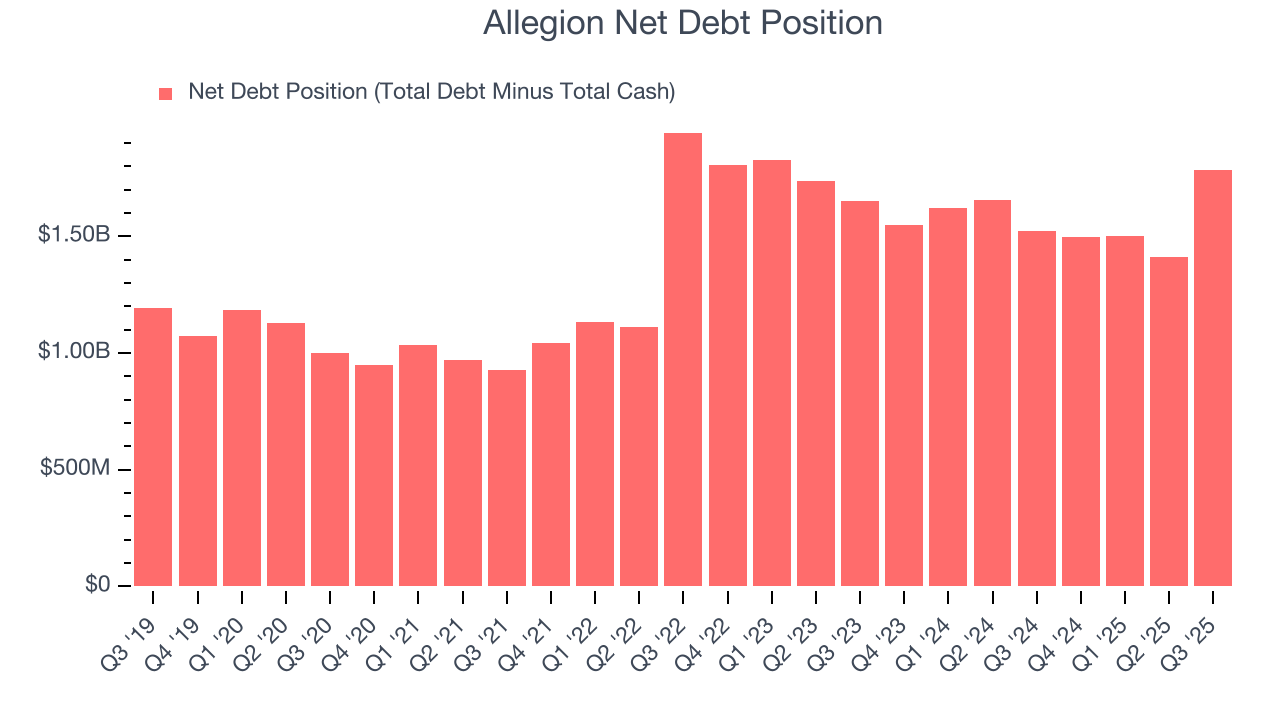

Allegion reported $302.7 million of cash and $2.09 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $983.8 million of EBITDA over the last 12 months, we view Allegion’s 1.8× net-debt-to-EBITDA ratio as safe. We also see its $36.5 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Allegion’s Q3 Results

We enjoyed seeing Allegion beat analysts’ revenue expectations this quarter. We were also glad its organic revenue outperformed Wall Street’s estimates. Overall, this print had some key positives. The stock traded up 1.4% to $178 immediately following the results.

13. Is Now The Time To Buy Allegion?

Updated: January 24, 2026 at 10:49 PM EST

When considering an investment in Allegion, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Allegion has some positive attributes, but it isn’t one of our picks. First off, its revenue growth was decent over the last five years, and analysts believe it can continue growing at these levels. And while Allegion’s diminishing returns show management's prior bets haven't worked out, its powerful free cash flow generation enables it to stay ahead of the competition through consistent reinvestment of profits.

Allegion’s P/E ratio based on the next 12 months is 19.3x. While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $181.55 on the company (compared to the current share price of $166.56).