AMN Healthcare Services (AMN)

AMN Healthcare Services is up against the odds. Its poor sales growth and falling returns on capital suggest its growth opportunities are shrinking.― StockStory Analyst Team

1. News

2. Summary

Why We Think AMN Healthcare Services Will Underperform

With a network of thousands of healthcare professionals ranging from nurses to physicians to executives, AMN Healthcare (NYSE:AMN) provides healthcare workforce solutions including temporary staffing, permanent placement, and technology platforms for hospitals and healthcare facilities across the United States.

- Products and services are facing significant end-market challenges during this cycle as sales have declined by 15.1% annually over the last two years

- Earnings per share have dipped by 16.9% annually over the past five years, which is concerning because stock prices follow EPS over the long term

- Poor expense management has led to an adjusted operating margin that is below the industry average

AMN Healthcare Services’s quality is not up to our standards. We’d search for superior opportunities elsewhere.

Why There Are Better Opportunities Than AMN Healthcare Services

AMN Healthcare Services is trading at $19.02 per share, or 9.5x forward P/E. This sure is a cheap multiple, but you get what you pay for.

Cheap stocks can look like a great deal at first glance, but they can be value traps. They often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. AMN Healthcare Services (AMN) Research Report: Q4 CY2025 Update

Healthcare staffing company AMN Healthcare Services (NYSE:AMN) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 1.8% year on year to $748.2 million. On top of that, next quarter’s revenue guidance ($1.23 billion at the midpoint) was surprisingly good and 95% above what analysts were expecting. Its non-GAAP profit of $0.22 per share was 17.9% below analysts’ consensus estimates.

AMN Healthcare Services (AMN) Q4 CY2025 Highlights:

- Revenue: $748.2 million vs analyst estimates of $723.9 million (1.8% year-on-year growth, 3.4% beat)

- Adjusted EPS: $0.22 vs analyst expectations of $0.27 (17.9% miss)

- Adjusted EBITDA: $54.48 million vs analyst estimates of $51.34 million (7.3% margin, 6.1% beat)

- Revenue Guidance for Q1 CY2026 is $1.23 billion at the midpoint, above analyst estimates of $631.9 million

- Operating Margin: 1.1%, up from -27.6% in the same quarter last year

- Sales Volumes fell 5.3% year on year (-22.4% in the same quarter last year)

- Market Capitalization: $656.1 million

Company Overview

With a network of thousands of healthcare professionals ranging from nurses to physicians to executives, AMN Healthcare (NYSE:AMN) provides healthcare workforce solutions including temporary staffing, permanent placement, and technology platforms for hospitals and healthcare facilities across the United States.

AMN Healthcare operates through three main segments: nurse and allied solutions, physician and leadership solutions, and technology and workforce solutions. The company serves as a crucial intermediary between healthcare professionals and the facilities that need them, helping to address staffing shortages and workforce challenges in the healthcare industry.

In its nurse and allied solutions segment, AMN offers travel nursing assignments (typically 13 weeks), international nurse recruitment, crisis staffing for emergencies, and local staffing services. Allied health professionals placed by AMN include physical therapists, respiratory therapists, medical technologists, and pharmacists.

The physician and leadership solutions segment provides locum tenens (temporary physician) staffing, permanent physician recruitment, and interim leadership for healthcare organizations needing executives or clinical leaders on a temporary basis. This allows facilities to maintain operations during leadership transitions or address unexpected vacancies.

Through its technology and workforce solutions segment, AMN offers managed services programs (MSPs) where it oversees a client's entire contingent staffing process. The company's vendor management systems (VMS) help healthcare organizations track and manage their staffing needs efficiently. AMN also provides language interpretation services through video and phone platforms, helping healthcare providers communicate with patients who speak different languages.

AMN generates revenue by charging healthcare facilities for its staffing and workforce solutions while paying the healthcare professionals it places. The company typically earns the difference between what clients pay for services and what AMN pays to the healthcare professionals, creating a margin on each placement. For technology solutions, AMN often uses a subscription or service-fee model.

4. Specialized Medical & Nursing Services

The skilled nursing services industry provides specialized care for patients requiring medical or rehabilitative support after hospital stays or for chronic conditions. These companies benefit from stable demand driven by an aging population and recurring revenue from Medicare, Medicaid, and private insurance. However, the industry faces challenges such as thin margins due to high labor costs and stringent regulatory requirements. Looking ahead, the industry is supported by tailwinds from an aging population, which means higher chronic disease prevalence. Advances in medical technology, including using AI to better predict, diagnose, and treat illnesses, may reduce hospital readmissions and improve outcomes. However, headwinds such as labor shortages, wage inflation, and potential government reimbursement cuts pose challenges. Adapting to value-based care models may further squeeze margins by requiring investments in training, technology, and compliance.

AMN Healthcare's main competitors include Cross Country Healthcare (NASDAQ: CCRN), CHG Healthcare Services, Aya Healthcare, HealthTrust Workforce Solutions, and Ingenovis Health. In the language services segment, it competes with LanguageLine Solutions.

5. Economies of Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $2.73 billion in revenue over the past 12 months, AMN Healthcare Services has decent scale. This is important as it gives the company more leverage in a heavily regulated, competitive environment that is complex and resource-intensive.

6. Revenue Growth

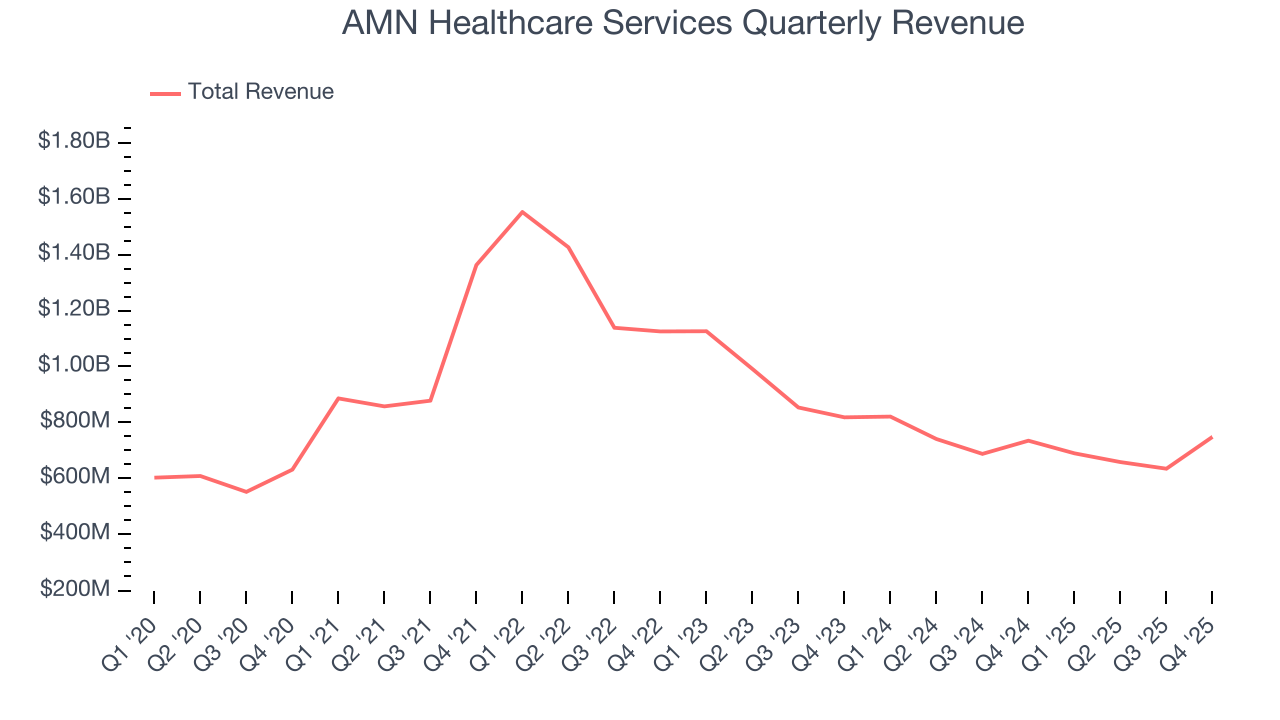

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, AMN Healthcare Services grew its sales at a tepid 2.7% compounded annual growth rate. This was below our standards and is a poor baseline for our analysis.

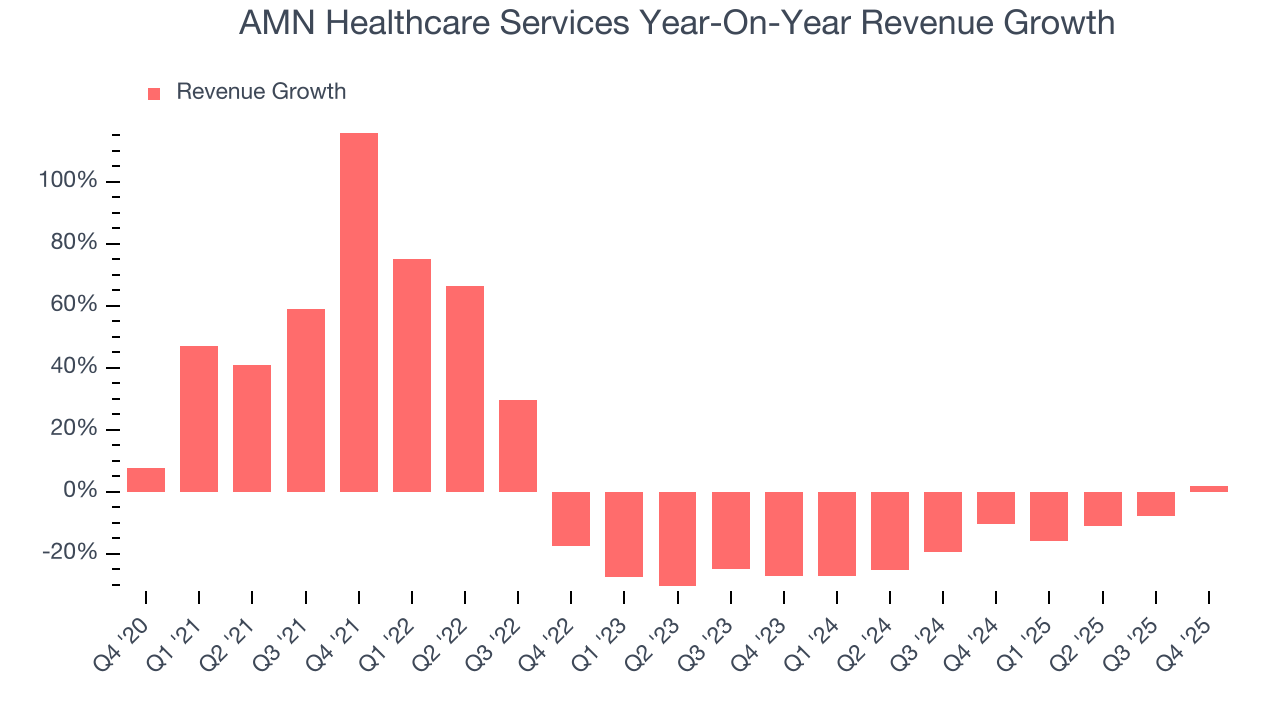

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. AMN Healthcare Services’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 15.1% annually.

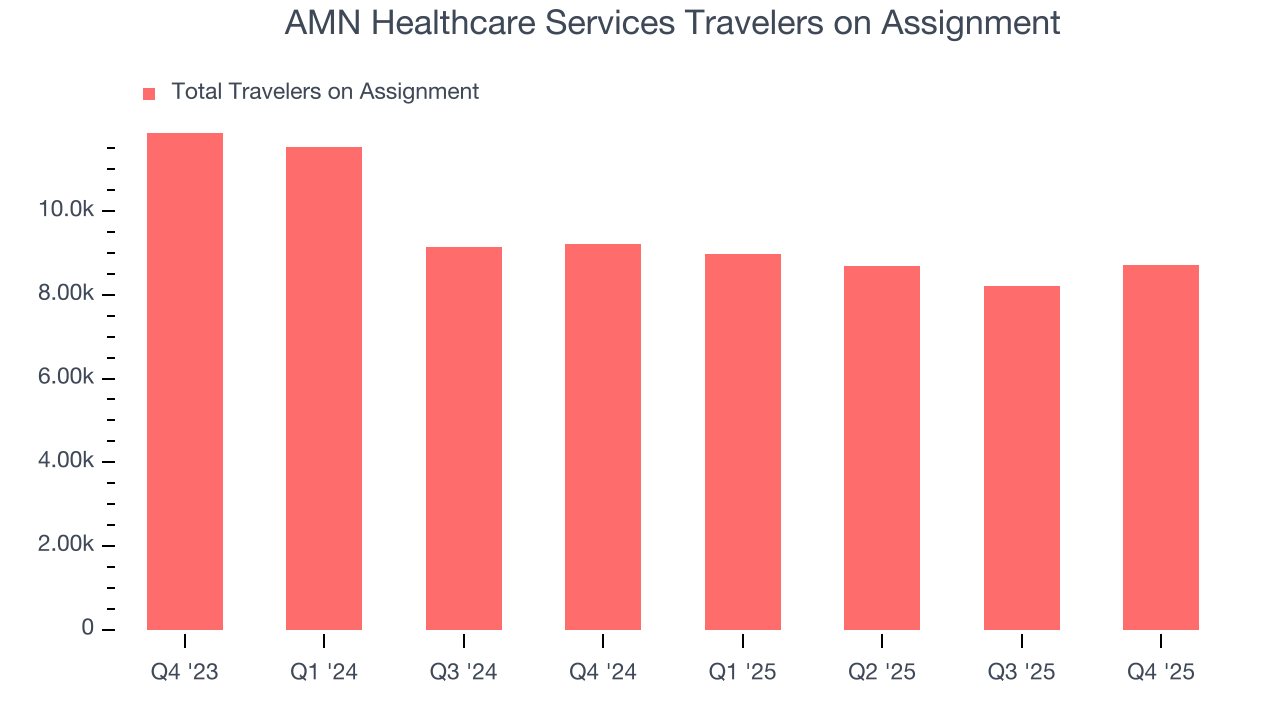

We can better understand the company’s revenue dynamics by analyzing its number of travelers on assignment, which reached 8,722 in the latest quarter. Over the last two years, AMN Healthcare Services’s travelers on assignment averaged 15% year-on-year declines. Because this number is in line with its revenue growth, we can see the company kept its prices fairly consistent.

This quarter, AMN Healthcare Services reported modest year-on-year revenue growth of 1.8% but beat Wall Street’s estimates by 3.4%. Company management is currently guiding for a 78.7% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to decline by 6.5% over the next 12 months. Although this projection is better than its two-year trend, it’s tough to feel optimistic about a company facing demand difficulties.

7. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

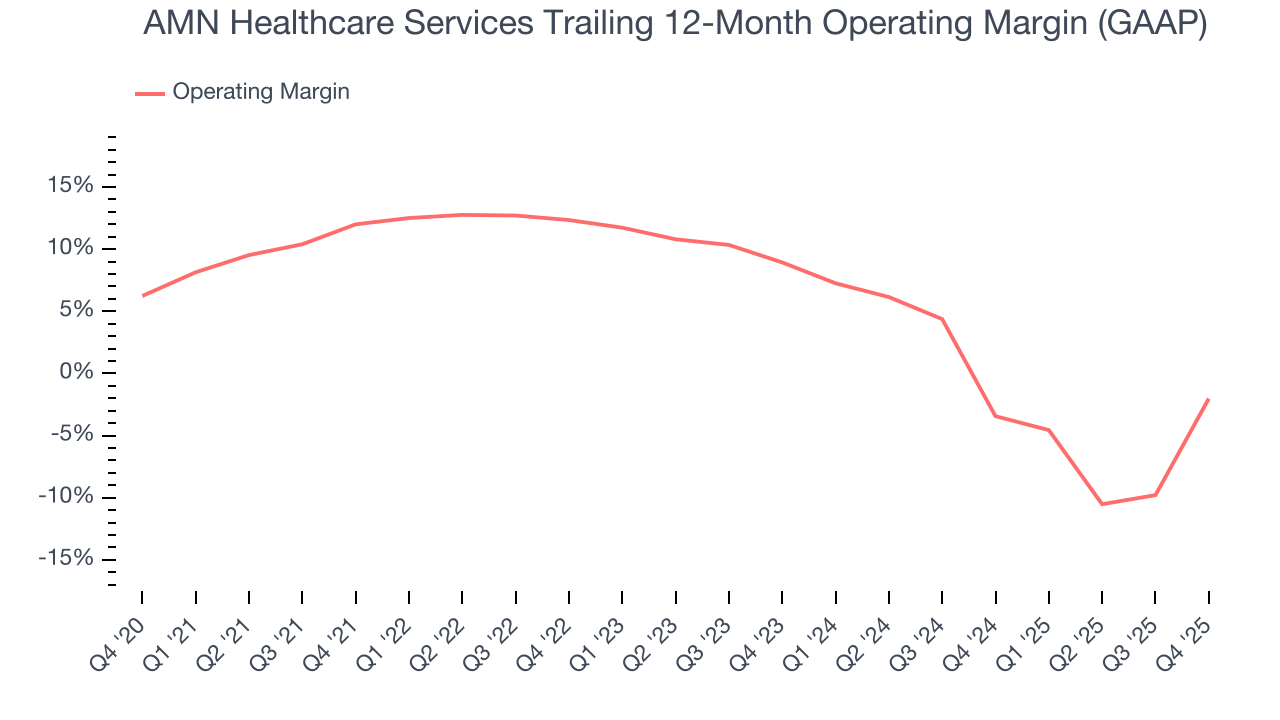

AMN Healthcare Services was profitable over the last five years but held back by its large cost base. Its average operating margin of 7% was weak for a healthcare business.

Analyzing the trend in its profitability, AMN Healthcare Services’s operating margin decreased by 14 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 11 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

In Q4, AMN Healthcare Services generated an operating margin profit margin of 1.1%, up 28.7 percentage points year on year. This increase was a welcome development and shows it was more efficient.

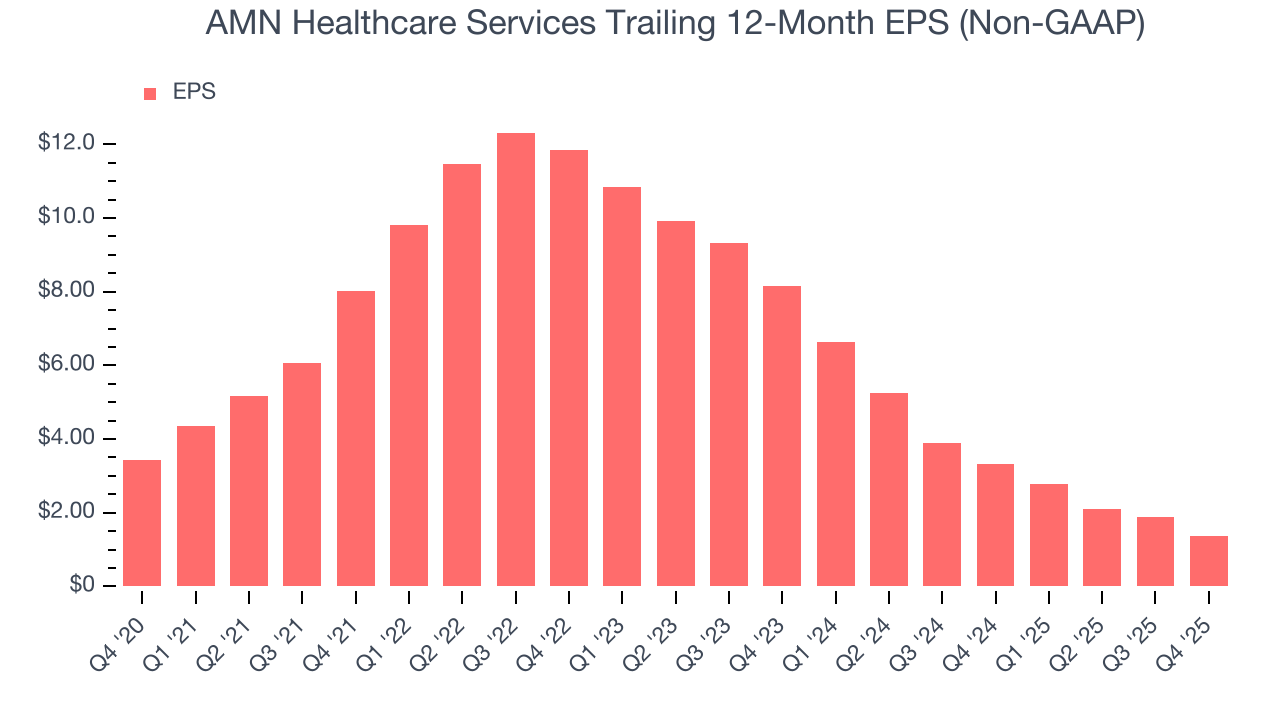

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for AMN Healthcare Services, its EPS declined by 16.9% annually over the last five years while its revenue grew by 2.7%. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

We can take a deeper look into AMN Healthcare Services’s earnings to better understand the drivers of its performance. As we mentioned earlier, AMN Healthcare Services’s operating margin expanded this quarter but declined by 14 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, AMN Healthcare Services reported adjusted EPS of $0.22, down from $0.75 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects AMN Healthcare Services’s full-year EPS of $1.36 to shrink by 50.5%.

9. Cash Is King

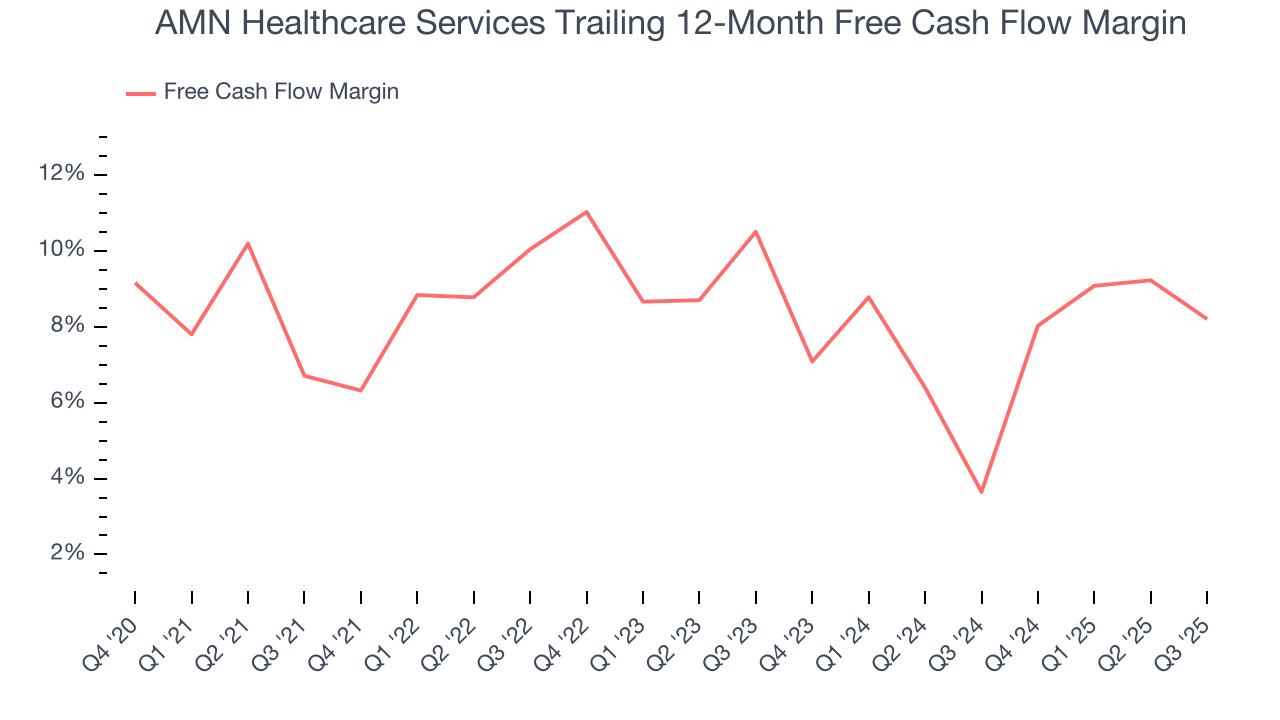

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

AMN Healthcare Services has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 8.4% over the last five years, slightly better than the broader healthcare sector.

Taking a step back, we can see that AMN Healthcare Services’s margin expanded by 1.2 percentage points during that time. This shows the company is heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability fell.

10. Return on Invested Capital (ROIC)

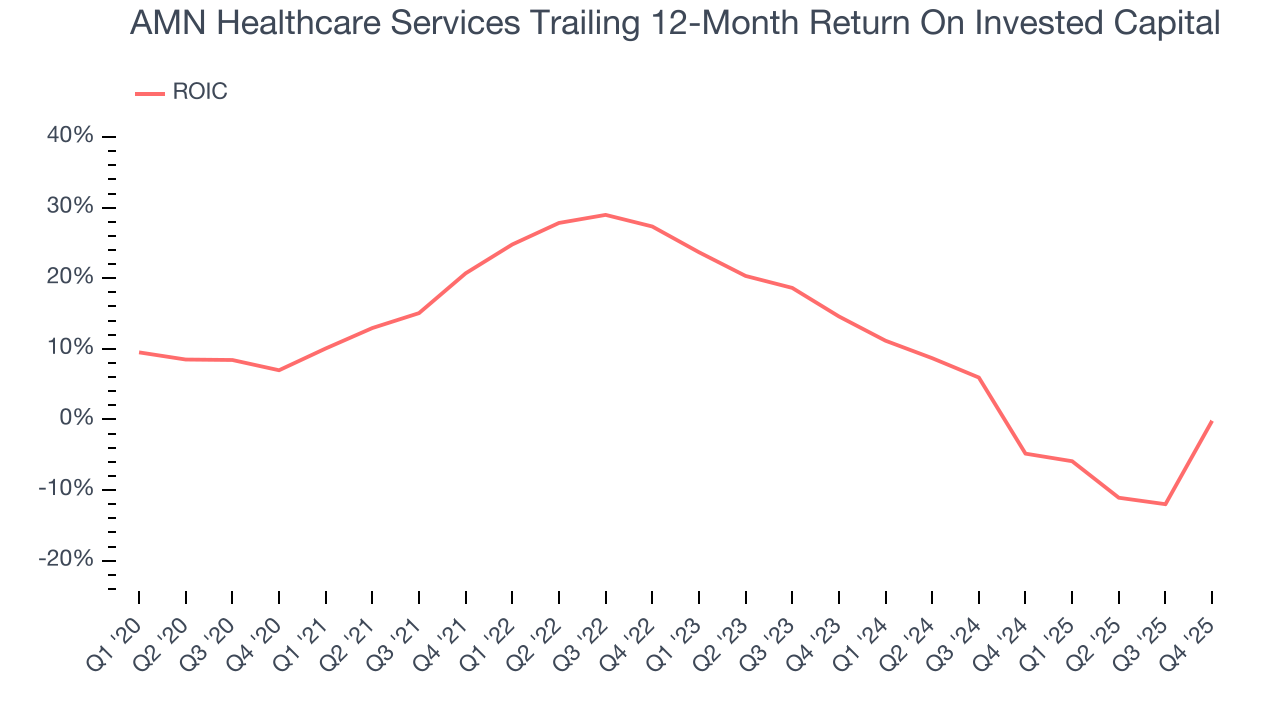

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although AMN Healthcare Services hasn’t been the highest-quality company lately because of its poor bottom-line (EPS) performance, it historically found a few growth initiatives that worked. Its five-year average ROIC was 11.5%, higher than most healthcare businesses.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, AMN Healthcare Services’s ROIC has unfortunately decreased significantly. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

11. Balance Sheet Assessment

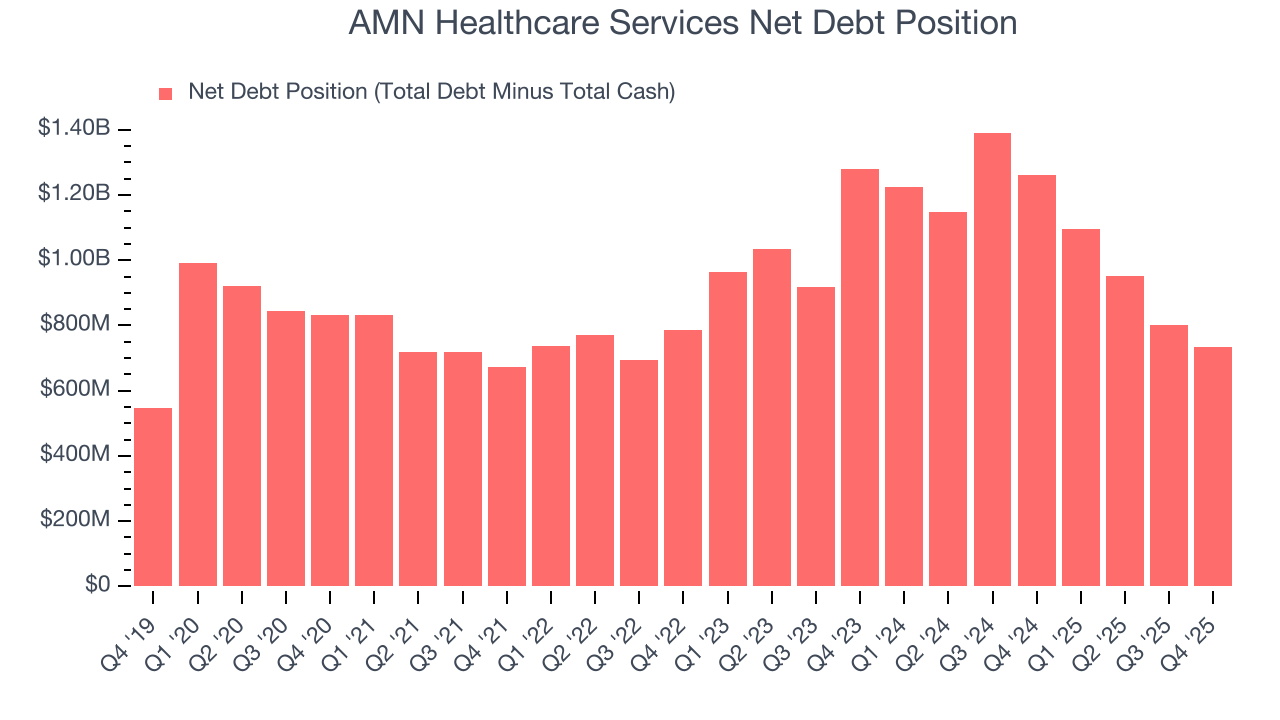

AMN Healthcare Services reported $33.97 million of cash and $767.1 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $234.5 million of EBITDA over the last 12 months, we view AMN Healthcare Services’s 3.1× net-debt-to-EBITDA ratio as safe. We also see its $21.03 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from AMN Healthcare Services’s Q4 Results

We were impressed by AMN Healthcare Services’s optimistic revenue guidance for next quarter, which blew past analysts’ expectations. We were also glad its revenue outperformed Wall Street’s estimates. On the other hand, its EPS missed. Overall, this print had some key positives. The stock traded up 10.8% to $19.13 immediately after reporting.

13. Is Now The Time To Buy AMN Healthcare Services?

Updated: March 14, 2026 at 12:07 AM EDT

When considering an investment in AMN Healthcare Services, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

We cheer for all companies helping people live better, but in the case of AMN Healthcare Services, we’ll be cheering from the sidelines. To kick things off, its revenue growth was uninspiring over the last five years. While its rising cash profitability gives it more optionality, the downside is its diminishing returns show management's prior bets haven't worked out. On top of that, its declining EPS over the last five years makes it a less attractive asset to the public markets.

AMN Healthcare Services’s P/E ratio based on the next 12 months is 9.5x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $22.21 on the company (compared to the current share price of $19.02).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.