Ameriprise Financial (AMP)

Ameriprise Financial is a great business. Its top-tier ROE showcases its ability to seek out and invest in ventures that yield significant returns.― StockStory Analyst Team

1. News

2. Summary

Why We Like Ameriprise Financial

Founded in 1894 and spun off from American Express in 2005, Ameriprise Financial (NYSE:AMP) provides financial planning, wealth management, asset management, and insurance products to help individuals and institutions achieve their financial goals.

- Annual tangible book value per share growth of 35.5% over the past two years was outstanding, reflecting strong capital accumulation this cycle

- ROE punches in at 59.9%, illustrating management’s expertise in identifying profitable investments

- Performance over the past five years shows its incremental sales were extremely profitable, as its annual earnings per share growth of 22.5% outpaced its revenue gains

We’re fond of companies like Ameriprise Financial. The price looks reasonable when considering its quality, so this could be a good time to invest in some shares.

Why Is Now The Time To Buy Ameriprise Financial?

Ameriprise Financial’s stock price of $508.15 implies a valuation ratio of 12.1x forward P/E. The valuation multiple is below many companies in the financials sector. We therefore think the stock is a good deal for the fundamentals.

Entry price matters much less than business quality when investing for the long term, but hey, it certainly doesn’t hurt to get in at an attractive price.

3. Ameriprise Financial (AMP) Research Report: Q4 CY2025 Update

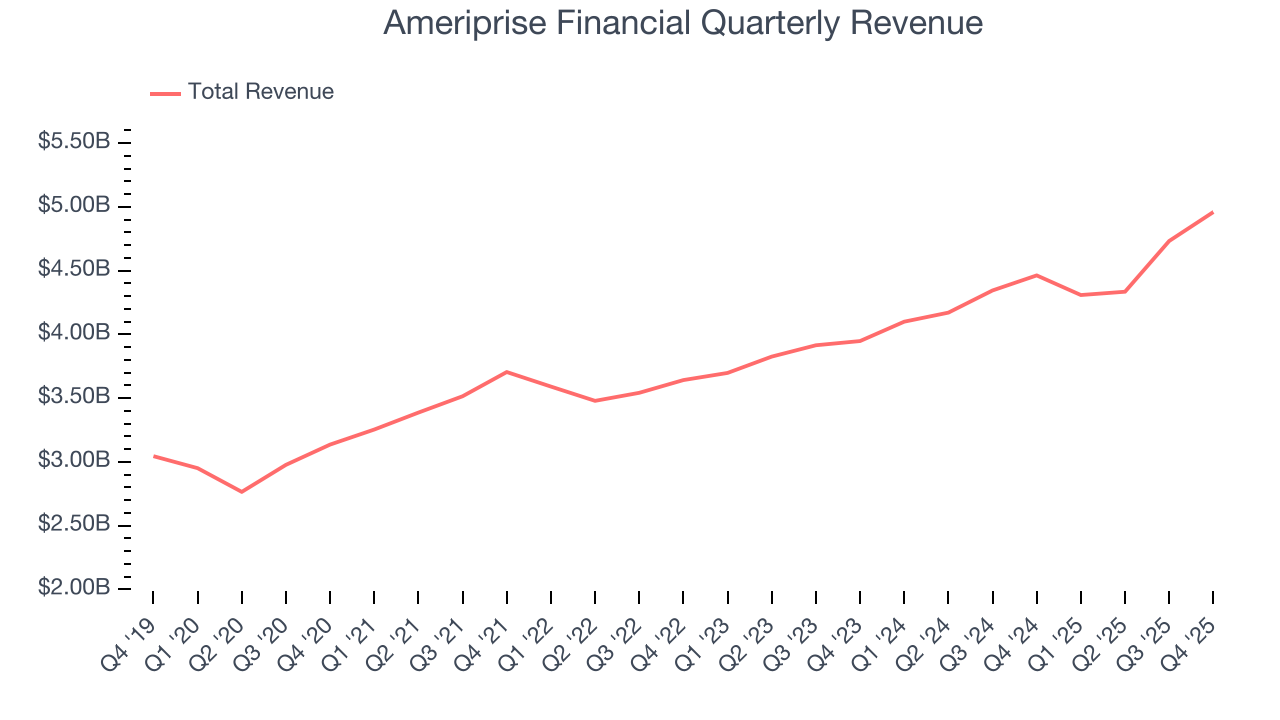

Financial services company Ameriprise Financial (NYSE:AMP) reported revenue ahead of Wall Streets expectations in Q4 CY2025, with sales up 11.1% year on year to $4.96 billion. Its non-GAAP profit of $10.83 per share was 5% above analysts’ consensus estimates.

Ameriprise Financial (AMP) Q4 CY2025 Highlights:

- Revenue: $4.96 billion vs analyst estimates of $4.75 billion (11.1% year-on-year growth, 4.5% beat)

- Pre-tax Profit: $1.29 billion (26% margin)

- Adjusted EPS: $10.83 vs analyst estimates of $10.31 (5% beat)

- Market Capitalization: $46.42 billion

Company Overview

Founded in 1894 and spun off from American Express in 2005, Ameriprise Financial (NYSE:AMP) provides financial planning, wealth management, asset management, and insurance products to help individuals and institutions achieve their financial goals.

Ameriprise operates through three main business segments: Advice & Wealth Management, Asset Management, and Retirement & Protection Solutions. The company's network of more than 10,000 financial advisors serves as its primary channel for delivering personalized financial planning and wealth management services to clients, primarily targeting households with $500,000 to $5 million in investable assets.

The Advice & Wealth Management segment offers financial planning, brokerage services, banking products, and investment advisory accounts. Clients pay fees based on assets under management, financial planning fees, and transaction fees. For example, a client might work with an Ameriprise advisor to develop a comprehensive retirement plan, then implement that plan through a mix of investment accounts and insurance products.

The Asset Management segment operates globally under the Columbia Threadneedle Investments brand, managing $637 billion in assets across various investment vehicles including mutual funds, exchange-traded funds, and separately managed accounts. Columbia Threadneedle maintains investment offices in seven countries and distributes its products through both Ameriprise's advisor network and third-party channels.

The Retirement & Protection Solutions segment offers annuities and insurance products exclusively through the company's RiverSource brand. These include variable annuities, structured variable annuities, life insurance, and disability income insurance. For instance, a client approaching retirement might purchase a structured variable annuity that provides market-linked returns with downside protection.

Ameriprise generates revenue through advisory fees, asset management fees, banking spreads, insurance premiums, and product distribution. The company's integrated business model allows it to serve clients across their financial lifecycle, from accumulation to retirement income generation.

4. Custody Bank

Custody banks safeguard financial assets and provide services like settlement, accounting, and regulatory compliance for institutional investors. Growth opportunities stem from increasing global assets under custody, demand for data analytics, and blockchain technology adoption for settlement efficiency. Challenges include fee pressure from large clients, substantial technology investment requirements, and competition from both traditional players and fintech firms entering the space.

Ameriprise Financial competes with major wealth management firms like Morgan Stanley (NYSE:MS), Bank of America's Merrill Lynch (NYSE:BAC), and Raymond James Financial (NYSE:RJF). In asset management, its competitors include BlackRock (NYSE:BLK), T. Rowe Price (NASDAQ:TROW), and Invesco (NYSE:IVZ). For insurance and annuity products, it competes with Prudential Financial (NYSE:PRU) and Lincoln National (NYSE:LNC).

5. Revenue Growth

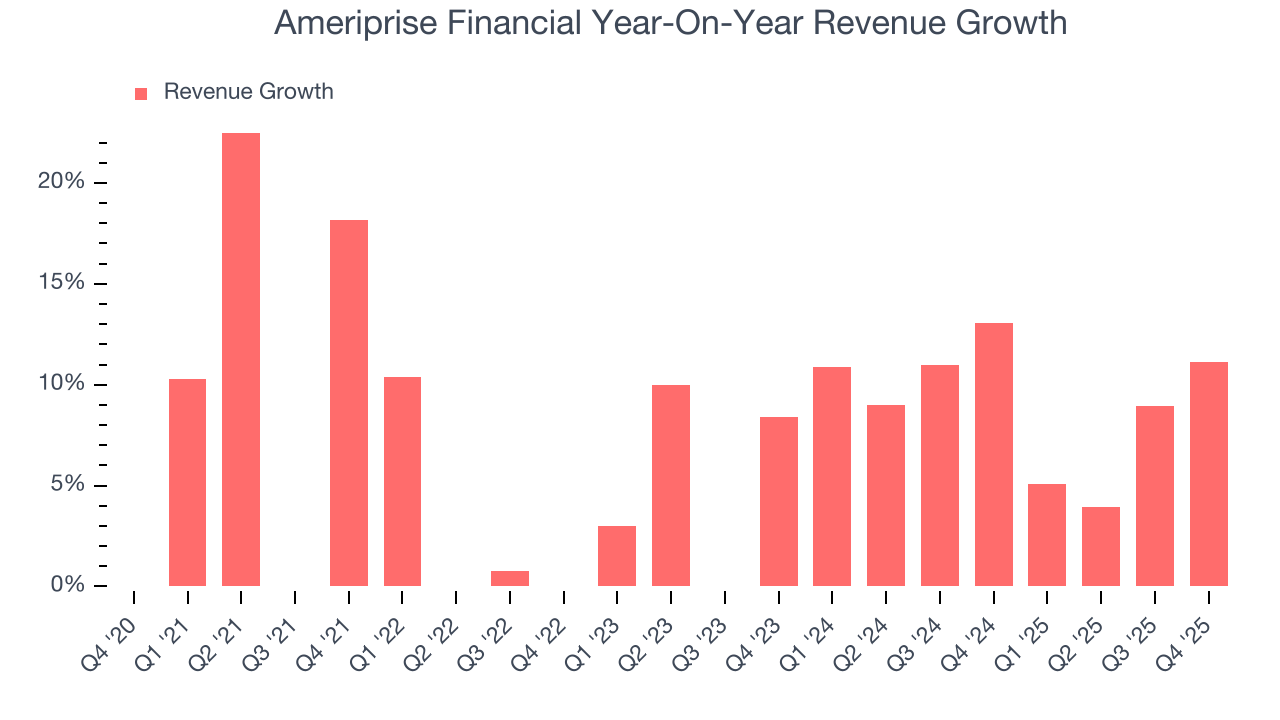

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, Ameriprise Financial’s 9.2% annualized revenue growth over the last five years was decent. Its growth was slightly above the average financials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Ameriprise Financial’s annualized revenue growth of 9.2% over the last two years aligns with its five-year trend, suggesting its demand was stable.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Ameriprise Financial reported year-on-year revenue growth of 11.1%, and its $4.96 billion of revenue exceeded Wall Street’s estimates by 4.5%.

6. Pre-Tax Profit Margin

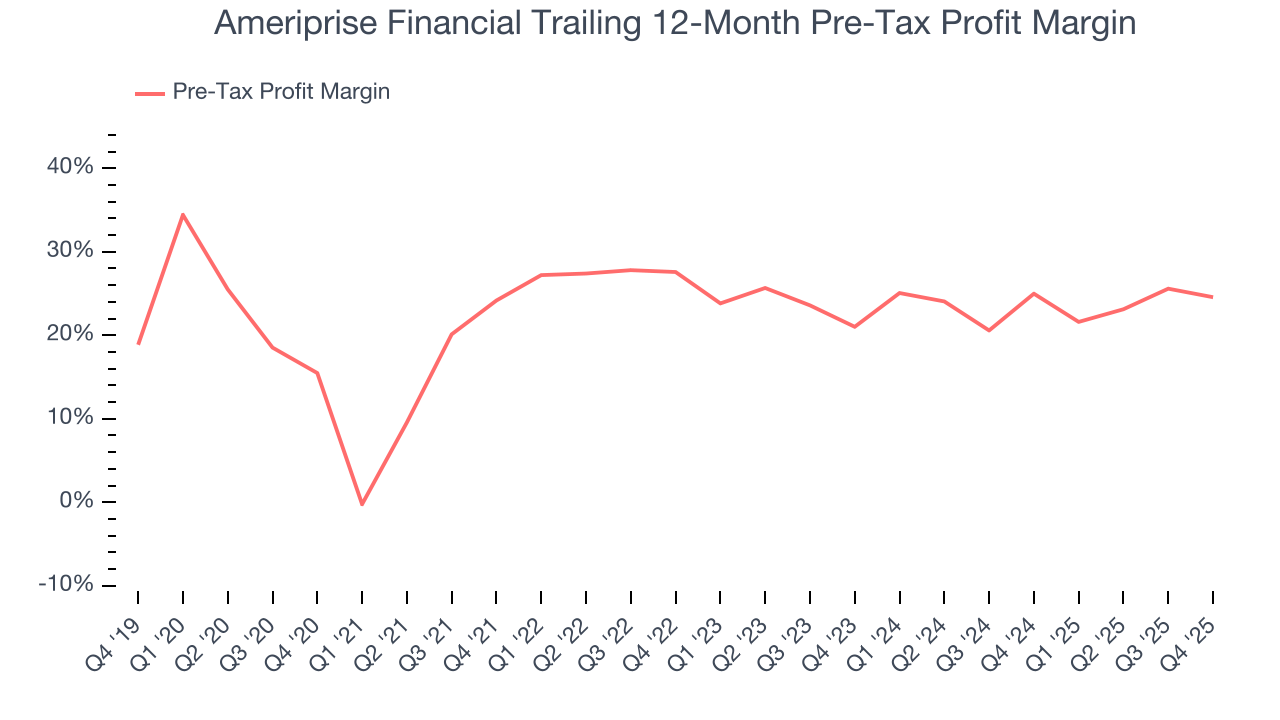

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For Custody Bank companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

Interest income and expenses play a big role in financial institutions' profitability, so they should be factored into the definition of profit. Taxes, however, should not as they are largely out of a company's control. This is pre-tax profit by definition.

Over the last five years, Ameriprise Financial’s pre-tax profit margin has fallen by 9.1 percentage points, going from 24.2% to 24.6%. It has also expanded by 3.5 percentage points on a two-year basis, showing its expenses have consistently grown at a slower rate than revenue. This typically signals prudent management.

In Q4, Ameriprise Financial’s pre-tax profit margin was 26%. This result was 4.2 percentage points worse than the same quarter last year.

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

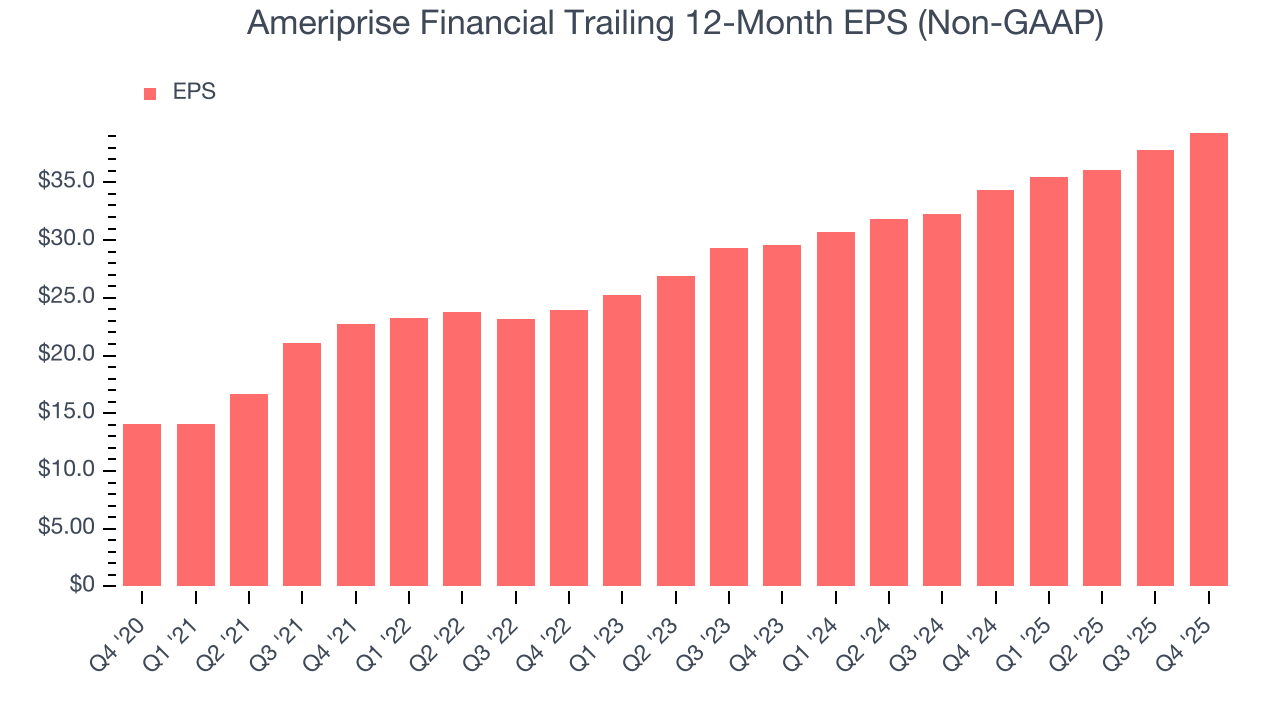

Ameriprise Financial’s EPS grew at a spectacular 22.8% compounded annual growth rate over the last five years, higher than its 9.2% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Ameriprise Financial, its two-year annual EPS growth of 15.3% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q4, Ameriprise Financial reported adjusted EPS of $10.83, up from $9.36 in the same quarter last year. This print beat analysts’ estimates by 5%. Over the next 12 months, Wall Street expects Ameriprise Financial’s full-year EPS of $39.31 to grow 6.3%.

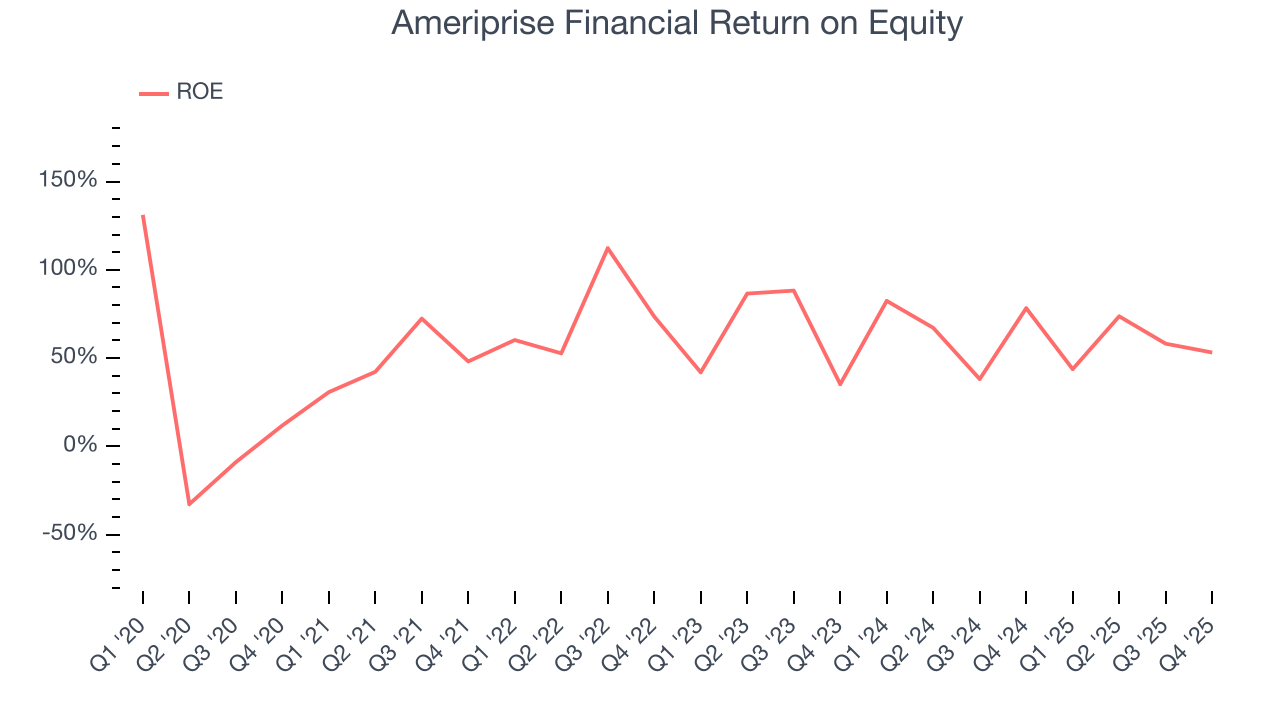

8. Return on Equity

Return on equity (ROE) reveals the profit generated per dollar of shareholder equity, which represents a key source of bank funding. Banks maintaining elevated ROE levels tend to accelerate wealth creation for shareholders via earnings retention, buybacks, and distributions.

Over the last five years, Ameriprise Financial has averaged an ROE of 62%, exceptional for a company operating in a sector where the average shakes out around 10% and those putting up 25%+ are greatly admired. This shows Ameriprise Financial has a strong competitive moat.

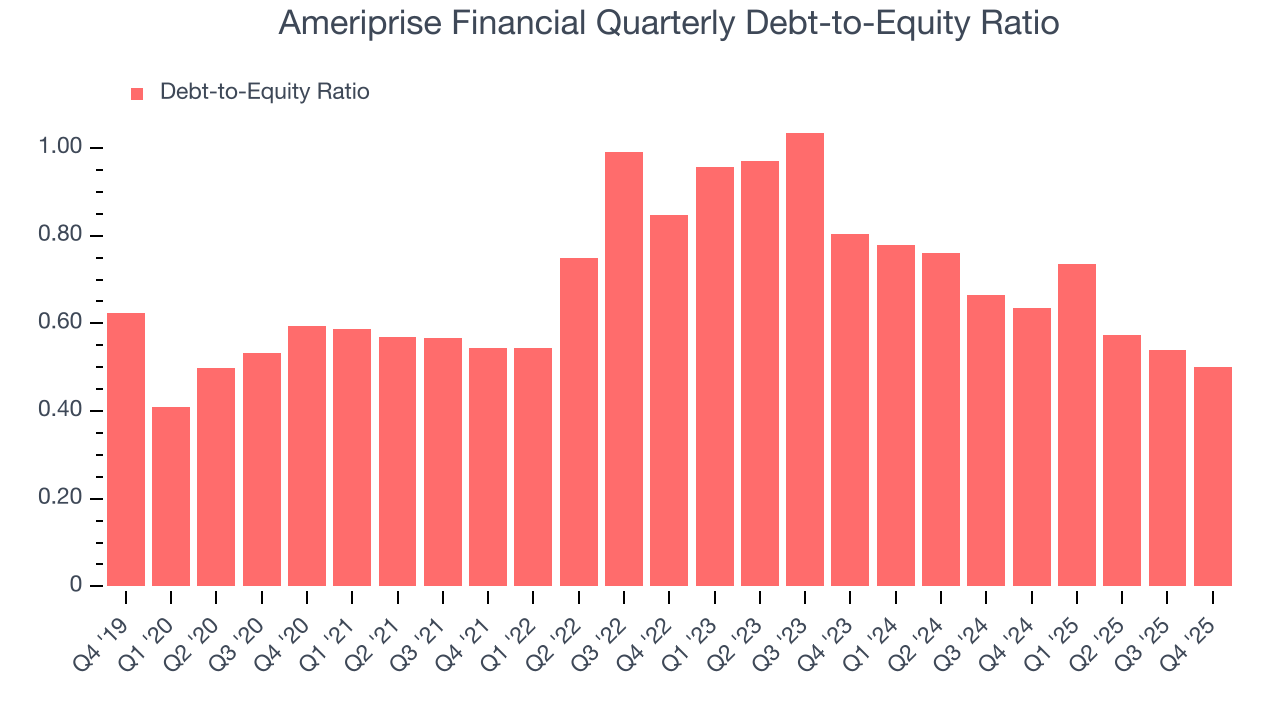

9. Balance Sheet Assessment

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

Ameriprise Financial currently has $3.28 billion of debt and $6.55 billion of shareholder's equity on its balance sheet, and over the past four quarters, has averaged a debt-to-equity ratio of 0.6×. We think this is safe and raises no red flags. In general, we’re comfortable with any ratio below 3.5× for a financials business.

10. Key Takeaways from Ameriprise Financial’s Q4 Results

We enjoyed seeing Ameriprise Financial beat analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 2.6% to $512.58 immediately after reporting.

11. Is Now The Time To Buy Ameriprise Financial?

Updated: January 29, 2026 at 7:11 AM EST

Are you wondering whether to buy Ameriprise Financial or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

There are multiple reasons why we think Ameriprise Financial is an elite financials company. First of all, the company’s revenue growth was decent over the last five years. On top of that, its stellar ROE suggests it has been a well-run company historically, and its expanding pre-tax profit margin shows the business has become more efficient.

Ameriprise Financial’s P/E ratio based on the next 12 months is 12x. Looking across the spectrum of financials businesses, Ameriprise Financial’s fundamentals clearly illustrate it’s a special business. We like the stock at this price.

Wall Street analysts have a consensus one-year price target of $545.30 on the company (compared to the current share price of $512.58), implying they see 6.4% upside in buying Ameriprise Financial in the short term.