Ameresco (AMRC)

Ameresco doesn’t excite us. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Ameresco Will Underperform

Having played a role in upgrading the energy solutions of Alcatraz Island, Ameresco (NYSE:AMRC) provides energy and renewable energy solutions for various sectors.

- Cash-burning history makes us doubt the long-term viability of its business model

- Earnings per share have contracted by 5.4% annually over the last five years, a headwind for returns as stock prices often echo long-term EPS performance

- Limited cash reserves may force the company to seek unfavorable financing terms that could dilute shareholders

Ameresco doesn’t satisfy our quality benchmarks. More profitable opportunities exist elsewhere.

Why There Are Better Opportunities Than Ameresco

Ameresco’s stock price of $26.76 implies a valuation ratio of 23.6x forward P/E. This valuation is fair for the quality you get, but we’re on the sidelines for now.

There are stocks out there featuring similar valuation multiples with better fundamentals. We prefer to invest in those.

3. Ameresco (AMRC) Research Report: Q4 CY2025 Update

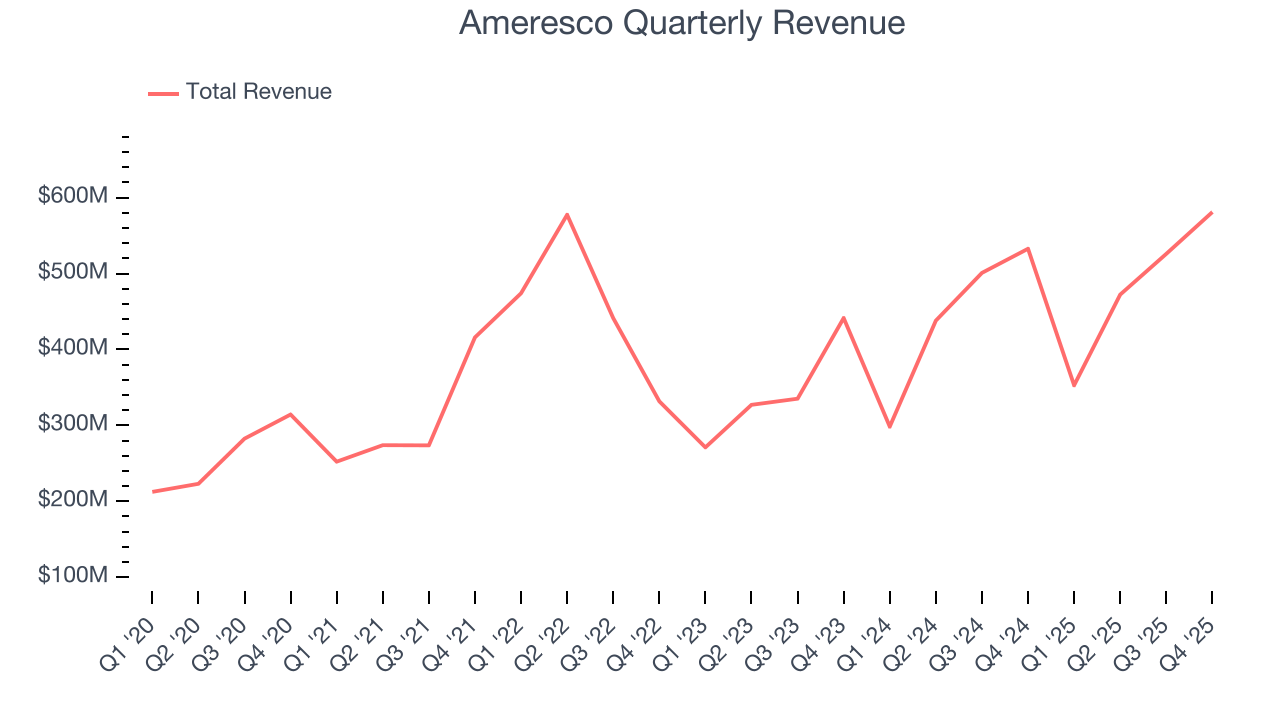

Energy and renewable energy projects company Ameresco (NYSE:AMRC) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 9.1% year on year to $581 million. The company’s full-year revenue guidance of $2.1 billion at the midpoint came in 0.5% above analysts’ estimates. Its non-GAAP profit of $0.39 per share was 9.2% above analysts’ consensus estimates.

Ameresco (AMRC) Q4 CY2025 Highlights:

- Revenue: $581 million vs analyst estimates of $553.4 million (9.1% year-on-year growth, 5% beat)

- Adjusted EPS: $0.39 vs analyst estimates of $0.36 (9.2% beat)

- Adjusted EBITDA: $70.01 million vs analyst estimates of $70.25 million (12% margin, in line)

- Adjusted EPS guidance for the upcoming financial year 2026 is $1.23 at the midpoint, beating analyst estimates by 2.1%

- EBITDA guidance for the upcoming financial year 2026 is $282.5 million at the midpoint, above analyst estimates of $279.8 million

- Operating Margin: 6.8%, down from 8.4% in the same quarter last year

- Free Cash Flow was $161.2 million, up from -$58.06 million in the same quarter last year

- Market Capitalization: $1.61 billion

Company Overview

Having played a role in upgrading the energy solutions of Alcatraz Island, Ameresco (NYSE:AMRC) provides energy and renewable energy solutions for various sectors.

The company's products and services reduce energy costs and greenhouse gas emissions for its clients, which include federal, state, and local governments, healthcare and educational institutions, and commercial and industrial entities. One notable example showing its expertise in renewable energy solutions for existing infrastructure was the design and installation of solar panels on Alcatraz Island.

In addition to installing solar panels, Ameresco offers wind power and geothermal systems. With its technology and expertise, it also gets hired to refurbish and upgrade existing power systems to make them more modern, renewable, and efficient. The company rounds out its products and services by providing insulation improvements, lighting retrofits, and heating, ventilation, and air conditioning systems. These solutions are all designed to reduce energy costs.

The design and installation of its products in large-scale infrastructure projects make up the vast majority of its revenue, which is earned through contracts. After completing a project, Ameresco will provide ongoing operations and maintenance services under multi-year contracts that act as a steady source of recurring revenue.

4. Energy Products and Services

Areas like the energy transition and emission reduction are thematic and front of mind today. This can be a double-edged sword for the energy products and services industry. Those who innovate and build new expertise can jolt demand while those who cling to legacy technologies or fall behind in the trending areas could see their market shares diminish. Bigger picture, energy products and services companies are still at the whim of construction and infrastructure project volumes, which tend to be cyclical and can be impacted heavily by economic factors such as interest rates.

Ameresco’s top competitors include Johnson Controls (NYSE:JCI), and private companies Schneider Electric and ENGIE Services.

5. Revenue Growth

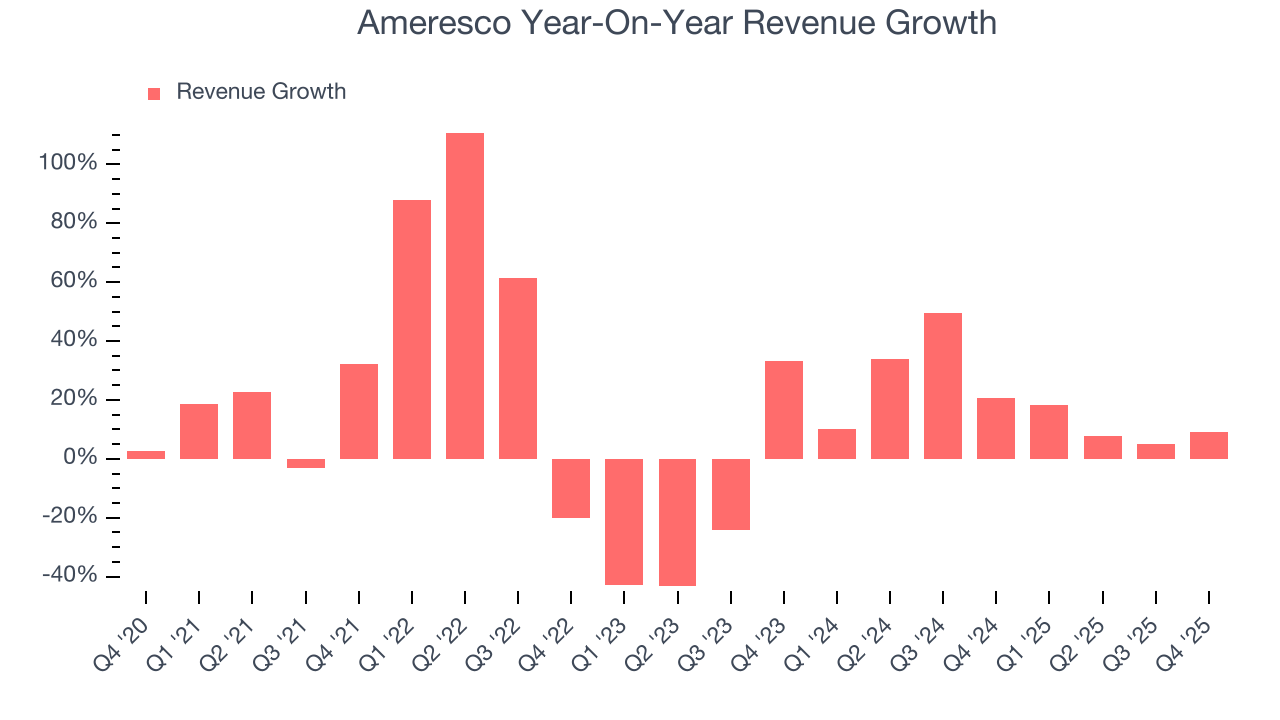

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Luckily, Ameresco’s sales grew at an excellent 13.4% compounded annual growth rate over the last five years. Its growth beat the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Ameresco’s annualized revenue growth of 18.6% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Ameresco reported year-on-year revenue growth of 9.1%, and its $581 million of revenue exceeded Wall Street’s estimates by 5%.

Looking ahead, sell-side analysts expect revenue to grow 7.5% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is above average for the sector and suggests the market is forecasting some success for its newer products and services.

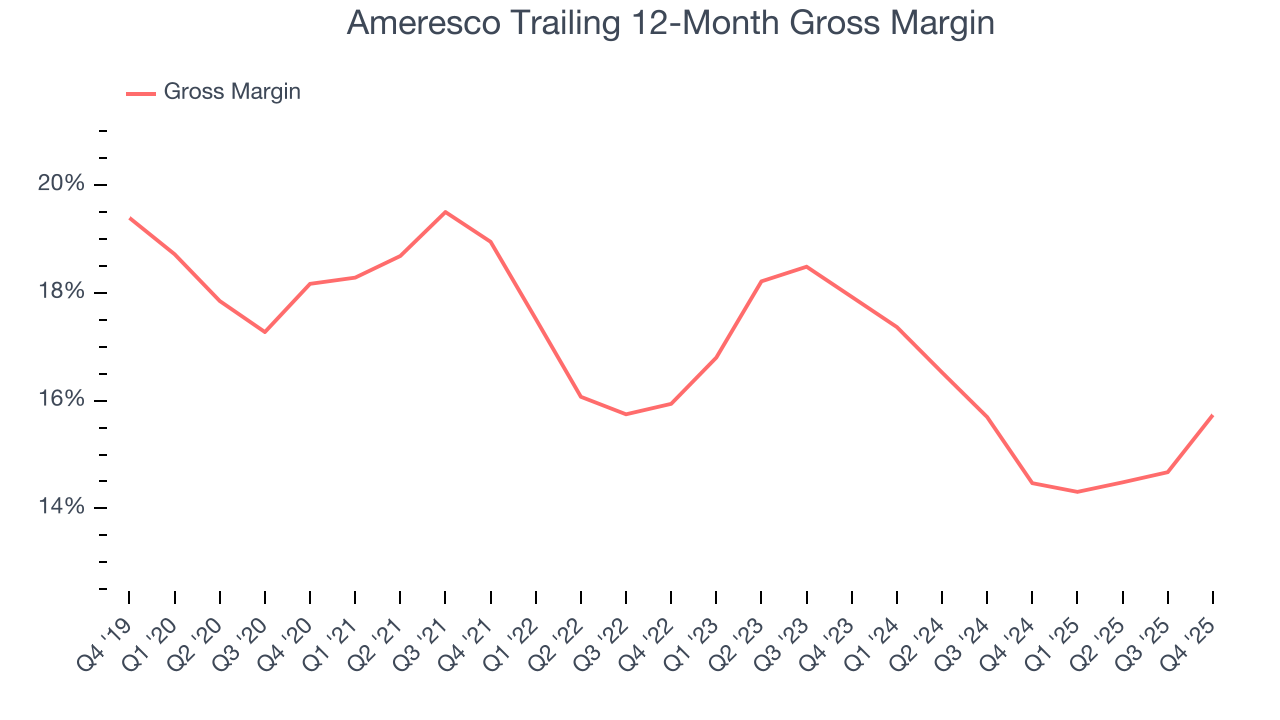

6. Gross Margin & Pricing Power

For industrials businesses, cost of sales is usually comprised of the direct labor, raw materials, and supplies needed to offer a product or service. These costs can be impacted by inflation and supply chain dynamics in the short term and a company’s purchasing power and scale over the long term.

Ameresco has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 16.4% gross margin over the last five years. That means Ameresco paid its suppliers a lot of money ($83.64 for every $100 in revenue) to run its business.

This quarter, Ameresco’s gross profit margin was 16.2%, up 3.7 percentage points year on year. Ameresco’s full-year margin has also been trending up over the past 12 months, increasing by 1.3 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold (such as manufacturing expenses).

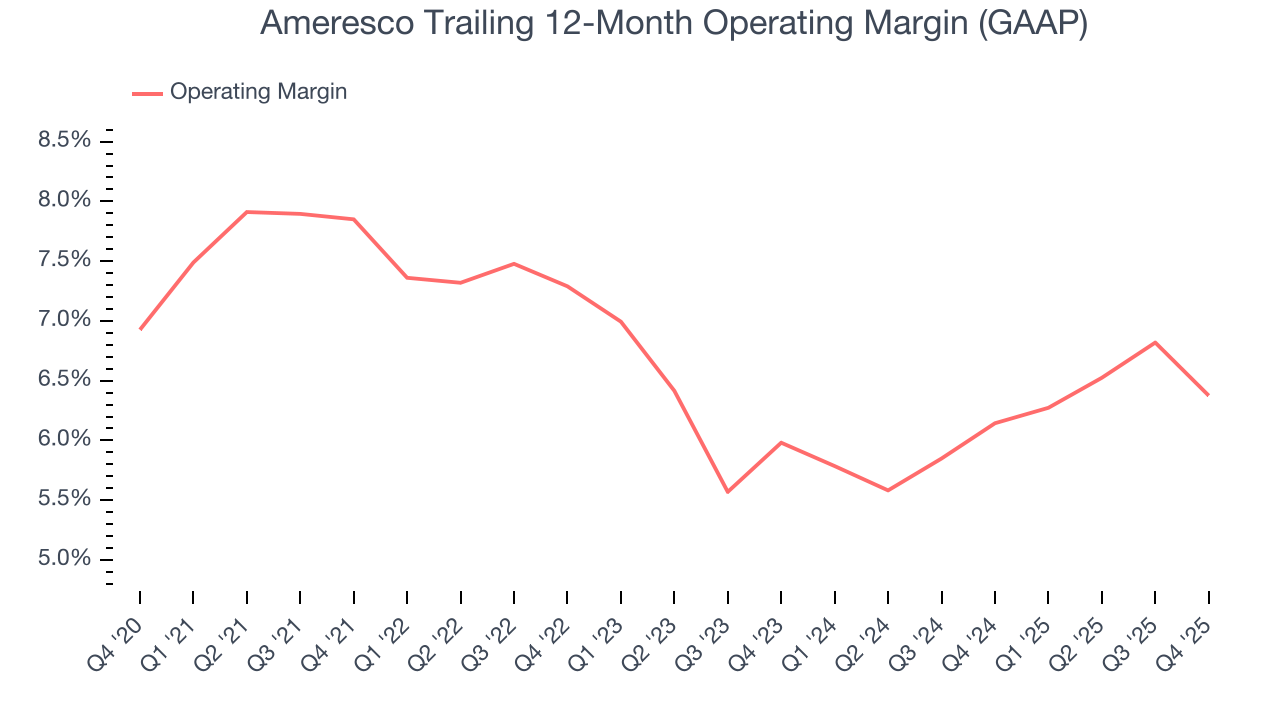

7. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Ameresco was profitable over the last five years but held back by its large cost base. Its average operating margin of 6.7% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

Looking at the trend in its profitability, Ameresco’s operating margin decreased by 1.5 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Ameresco’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, Ameresco generated an operating margin profit margin of 6.8%, down 1.6 percentage points year on year. Conversely, its revenue and gross margin actually rose, so we can assume it was less efficient because its operating expenses like marketing, R&D, and administrative overhead grew faster than its revenue.

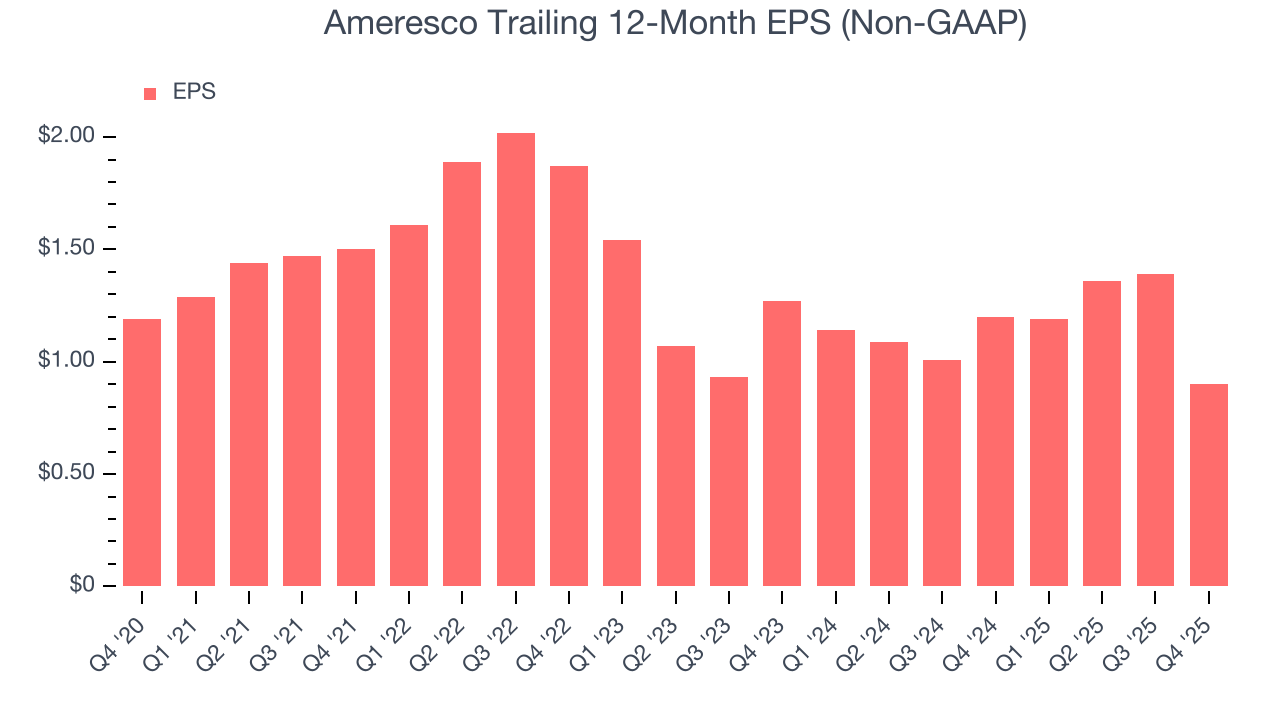

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Ameresco, its EPS declined by 5.4% annually over the last five years while its revenue grew by 13.4%. This tells us the company became less profitable on a per-share basis as it expanded.

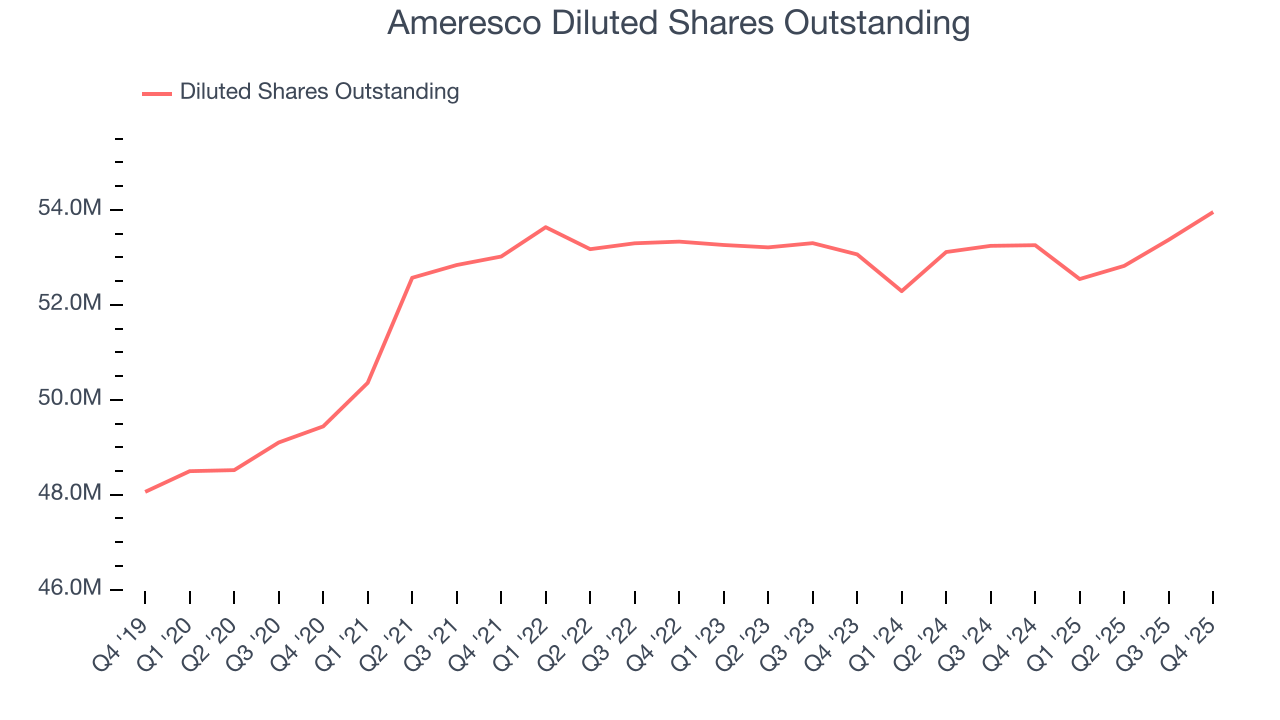

Diving into the nuances of Ameresco’s earnings can give us a better understanding of its performance. As we mentioned earlier, Ameresco’s operating margin declined by 1.5 percentage points over the last five years. Its share count also grew by 9.1%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Ameresco, its two-year annual EPS declines of 15.7% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, Ameresco reported adjusted EPS of $0.39, down from $0.88 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 9.2%. Over the next 12 months, Wall Street expects Ameresco’s full-year EPS of $0.90 to grow 22.2%.

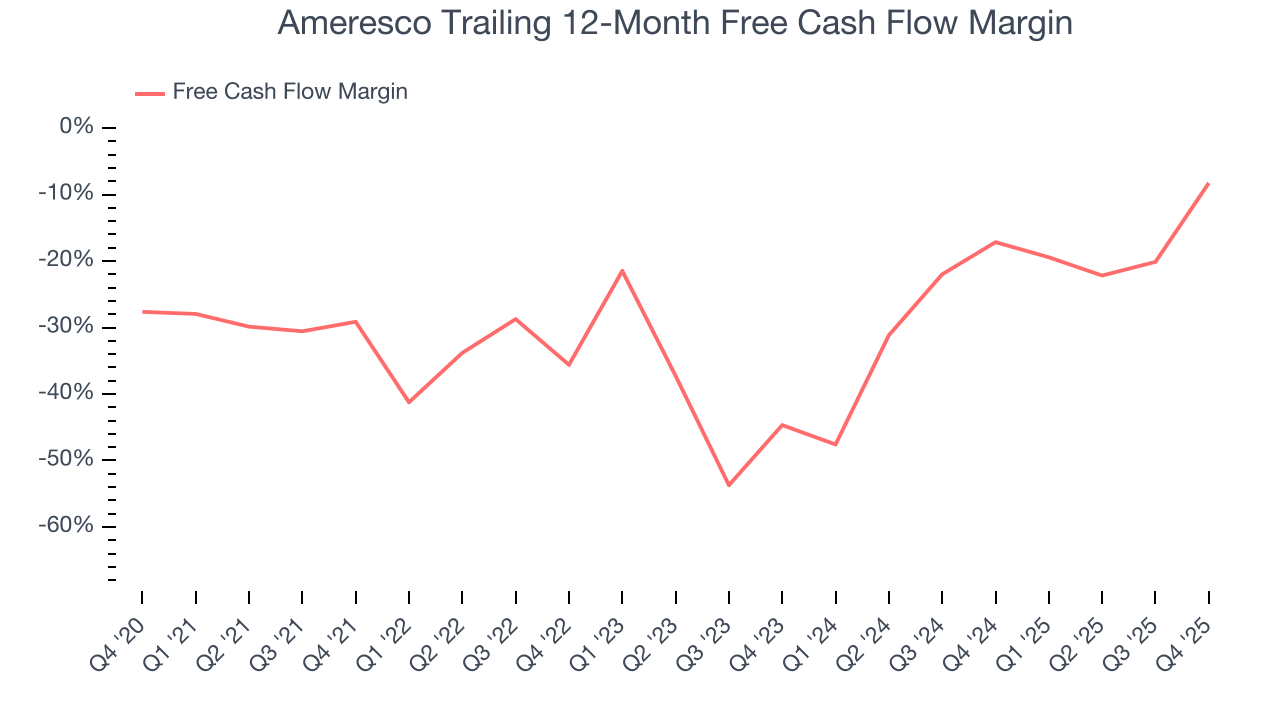

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

While Ameresco posted positive free cash flow this quarter, the broader story hasn’t been so clean. Ameresco’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 25.6%, meaning it lit $25.64 of cash on fire for every $100 in revenue.

Taking a step back, an encouraging sign is that Ameresco’s margin expanded by 20.9 percentage points during that time. In light of its glaring cash burn, however, this improvement is a bucket of hot water in a cold ocean.

Ameresco’s free cash flow clocked in at $161.2 million in Q4, equivalent to a 27.8% margin. Its cash flow turned positive after being negative in the same quarter last year, marking a potential inflection point.

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Ameresco historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 5.6%, somewhat low compared to the best industrials companies that consistently pump out 20%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Ameresco’s ROIC averaged 2.3 percentage point decreases each year. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

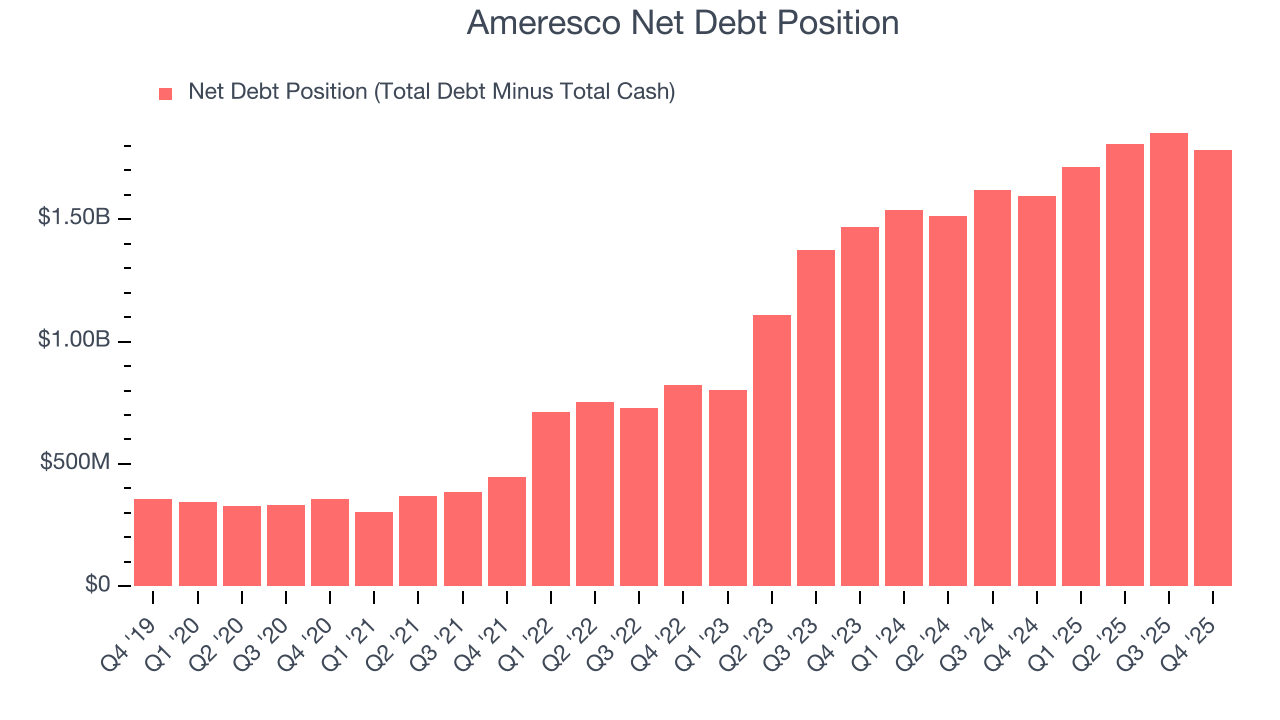

11. Balance Sheet Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Ameresco burned through $159.8 million of cash over the last year, and its $1.95 billion of debt exceeds the $164.3 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

Unless the Ameresco’s fundamentals change quickly, it might find itself in a position where it must raise capital from investors to continue operating. Whether that would be favorable is unclear because dilution is a headwind for shareholder returns.

We remain cautious of Ameresco until it generates consistent free cash flow or any of its announced financing plans materialize on its balance sheet.

12. Key Takeaways from Ameresco’s Q4 Results

We were impressed by how significantly Ameresco blew past analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 3.5% to $32.02 immediately following the results.

13. Is Now The Time To Buy Ameresco?

Updated: March 29, 2026 at 11:24 PM EDT

Before deciding whether to buy Ameresco or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

Ameresco isn’t a terrible business, but it isn’t one of our picks. Although its revenue growth was impressive over the last five years, it’s expected to deteriorate over the next 12 months and its declining EPS over the last five years makes it a less attractive asset to the public markets. And while the company’s rising cash profitability gives it more optionality, the downside is its cash burn raises the question of whether it can sustainably maintain growth.

Ameresco’s P/E ratio based on the next 12 months is 23.6x. This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're pretty confident there are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $42.60 on the company (compared to the current share price of $26.76).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.